Unit 5: Management Accounting Report for Capco Financial Services

VerifiedAdded on 2020/10/22

|20

|5074

|273

Report

AI Summary

This report, prepared by a junior accountant at Capco, offers a comprehensive overview of management accounting. It begins with an introduction to management accounting and its various types, including inventory management, cost accounting, and job costing systems, along with their specific requirements. The report then delves into different methods of management accounting reporting, such as cost reports, budgetary reports, inventory reports, and performance reports, while critically evaluating the adoption of these systems. Furthermore, it demonstrates the preparation of income statements using both marginal and absorption costing techniques, accompanied by interpretations and variance analysis. Finally, the report explores the use of planning tools within a budgetary control system and compares the adoption of various management accounting systems in response to financial challenges, offering valuable insights for financial decision-making at Capco.

Unit 5 – Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

SCENARIO 1...................................................................................................................................1

Explaining management accounting and various types of management accounting system along

with their requirements....................................................................................................................1

Explaining different methods of management accounting reporting...............................................3

Showing preparation of income statement using marginal and absorption costing techniques.....5

Explaining different types of planning tools of budgetary control system.................................8

Comparing the adoption of various management accounting systems as to respond to various

financial problems..........................................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

SCENARIO 1...................................................................................................................................1

Explaining management accounting and various types of management accounting system along

with their requirements....................................................................................................................1

Explaining different methods of management accounting reporting...............................................3

Showing preparation of income statement using marginal and absorption costing techniques.....5

Explaining different types of planning tools of budgetary control system.................................8

Comparing the adoption of various management accounting systems as to respond to various

financial problems..........................................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting can be defined as the branch of management that concerns with

the analysis of cost related activities of the business organisation (Otley, 2016). In this branch,

the professional knowledge and skills are used for preparation of a statement showing all the

accounting informations for helping the managers in their decision making activities. Capco is a

medium sized company in UK. The company was founded in 1998 for providing financial

consultancy services to its customers. The present study shows a report of junior accountant of

Capco which includes a brief introduction about the management accounting system along with

its various types management accounting and their requirements in the company. The study also

provides information about various methods of management accounting reporting and various

budgetary control planning tools. It also shows a comparison about the responding of various

management accounting systems for the purpose of responding various financial problems.

Further, the study also shows various calculations for the purpose of showing the use of various

management accounting techniques.

SCENARIO 1

Explaining management accounting and various types of management accounting system along

with their requirements

Management accounting

“ Management accounting can be defined as a process of applying professional

knowledge and skills for the purpose of preparing various accounting statements. These

statements are being prepared for the purpose of providing accounting informations to the

managers (Maas, Schaltegger and Crutzen, 2016). It is a process through which each accounting

information is being provided in such an efficient way so that it could help managers in

developing strategies for enhancing the financial performance of the business.”

management accounting system

Management accounting system is a set system that provides a set procedure through

which various financial statements and other financial reports are prepared in such a way so that

they can determine the financial performance of the business for the purpose of using it in their

decision making and strategic development procedure.

Types of management accounting system:

1

Management accounting can be defined as the branch of management that concerns with

the analysis of cost related activities of the business organisation (Otley, 2016). In this branch,

the professional knowledge and skills are used for preparation of a statement showing all the

accounting informations for helping the managers in their decision making activities. Capco is a

medium sized company in UK. The company was founded in 1998 for providing financial

consultancy services to its customers. The present study shows a report of junior accountant of

Capco which includes a brief introduction about the management accounting system along with

its various types management accounting and their requirements in the company. The study also

provides information about various methods of management accounting reporting and various

budgetary control planning tools. It also shows a comparison about the responding of various

management accounting systems for the purpose of responding various financial problems.

Further, the study also shows various calculations for the purpose of showing the use of various

management accounting techniques.

SCENARIO 1

Explaining management accounting and various types of management accounting system along

with their requirements

Management accounting

“ Management accounting can be defined as a process of applying professional

knowledge and skills for the purpose of preparing various accounting statements. These

statements are being prepared for the purpose of providing accounting informations to the

managers (Maas, Schaltegger and Crutzen, 2016). It is a process through which each accounting

information is being provided in such an efficient way so that it could help managers in

developing strategies for enhancing the financial performance of the business.”

management accounting system

Management accounting system is a set system that provides a set procedure through

which various financial statements and other financial reports are prepared in such a way so that

they can determine the financial performance of the business for the purpose of using it in their

decision making and strategic development procedure.

Types of management accounting system:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

There are numerous types of management accounting systems which helps the managers

in determining various financial activities. The major types of management accounting systems

are as under:

Inventory management system:

It is the type of management accounting system that concerns with the measurement of

inventories of the company. The inventory management system helps the business in measuring

and monitoring the flow of inventories in the business (Cooper, Ezzamel and Qu, 2017). This

system is useful in all those businesses that keeps the stock in their business for the purpose of

using them in further processing or for further selling them in the market like, manufacturing

concerns, construction companies, retail industries, etc..

Requirements

This system is required for monitoring each movement of the inventory within or outside

the business.

The system helps in tracking the flow of inventory.

For the purpose of determining the minimum requirement of inventory, the managers

need to involve this system within the organisation.

It helps the managers in elimination of under or over maintenance of inventories in the

firm.

Cost accounting system:

In the cost accounting system, the management performs their managerial functions by

predicting the future cost of the company as per its efficiency and also analysing business' actual

performance and identify its actual performance through comparing actual cost related activities

with the estimated activities. For this purpose, the cost accounting system provides numerous

methods like budgetary control system, standard costing techniques, etc.

Requirements

It is required by the company for having effective control over various costs of the

company.

2

in determining various financial activities. The major types of management accounting systems

are as under:

Inventory management system:

It is the type of management accounting system that concerns with the measurement of

inventories of the company. The inventory management system helps the business in measuring

and monitoring the flow of inventories in the business (Cooper, Ezzamel and Qu, 2017). This

system is useful in all those businesses that keeps the stock in their business for the purpose of

using them in further processing or for further selling them in the market like, manufacturing

concerns, construction companies, retail industries, etc..

Requirements

This system is required for monitoring each movement of the inventory within or outside

the business.

The system helps in tracking the flow of inventory.

For the purpose of determining the minimum requirement of inventory, the managers

need to involve this system within the organisation.

It helps the managers in elimination of under or over maintenance of inventories in the

firm.

Cost accounting system:

In the cost accounting system, the management performs their managerial functions by

predicting the future cost of the company as per its efficiency and also analysing business' actual

performance and identify its actual performance through comparing actual cost related activities

with the estimated activities. For this purpose, the cost accounting system provides numerous

methods like budgetary control system, standard costing techniques, etc.

Requirements

It is required by the company for having effective control over various costs of the

company.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It enhances the ability of managers in detecting various problems along with the reason

behind the problem through providing various cost related data.

The cost accounting system is required for determining change in the efficiency of

business through budgetary control ans standard techniques of this system.

Further, for the purpose of determining the change in capacity of business, cost

accounting system is needed to be adopted by business.

Job costing system

Job costing system is the management accounting system through which the each

managers can determine the cost incurred by business in production of each job (Hall, 2016).

Generally this system is Required by those business organisations that manufactures goods or

provides services to their customers on the customised bases.

Requirement

This system is required by business as to determine the appropriate price of a specific job

by providing actual cost incurred by business in manufacturing a specific job.

With the help of this system, managers can easily determine the amount of inventory

used by the business in producing specific job.

Further, for the purpose of determining and ensuring effectiveness in the budgetary

control system of the company, adoption of job costing system is required by the

managers.

In this regard, it can be evaluated that there are numerous types of management

accounting systems. Each system helps managers in enhancing the effectiveness in performance

of their managerial functions in different ways.

Explaining different methods of management accounting reporting

Management accounting reporting

Management accounting reporting can be defined as a process of preparing reports by

including all the relevant informations of financial activities of the business. In the process of

management accounting reporting, the managerial accountant uses various their professional

3

behind the problem through providing various cost related data.

The cost accounting system is required for determining change in the efficiency of

business through budgetary control ans standard techniques of this system.

Further, for the purpose of determining the change in capacity of business, cost

accounting system is needed to be adopted by business.

Job costing system

Job costing system is the management accounting system through which the each

managers can determine the cost incurred by business in production of each job (Hall, 2016).

Generally this system is Required by those business organisations that manufactures goods or

provides services to their customers on the customised bases.

Requirement

This system is required by business as to determine the appropriate price of a specific job

by providing actual cost incurred by business in manufacturing a specific job.

With the help of this system, managers can easily determine the amount of inventory

used by the business in producing specific job.

Further, for the purpose of determining and ensuring effectiveness in the budgetary

control system of the company, adoption of job costing system is required by the

managers.

In this regard, it can be evaluated that there are numerous types of management

accounting systems. Each system helps managers in enhancing the effectiveness in performance

of their managerial functions in different ways.

Explaining different methods of management accounting reporting

Management accounting reporting

Management accounting reporting can be defined as a process of preparing reports by

including all the relevant informations of financial activities of the business. In the process of

management accounting reporting, the managerial accountant uses various their professional

3

skills for preparing reports in such a way, so that they can be easily understand by the managers

and help them in their decision making process.

Management accounting reports includes budget reports, cost reports, performance

reports, inventory reports, etc. these are prepared by the managers for the purpose of helping the

managers in their various functions like planning, monitoring, organising, decision making, etc.

Further, there are various methods for preparing managerial accounting reporting as

under:

Cost reports: cost reports helps the managers in determining various areas where the

company has spent its funds and other resources. These reports include information

regarding various costs incurred by the business like fixed costs, various costs, labours,

various overheads, etc. managerial accountant prepares a final report that includes a

summary of all the costs incurred by the company (Methods of Management Accounting

Report, 2018). With the help of it, managers analyses the performance of business in cost

related activities and develops effective strategies for enhancing cost control within the

organisation.

Budgetary reports: Budgetary reports includes information regarding all the estimated

activities and performance of the business. These reports are helps the managers in

identifying the need of funds and other resources in the business within a specific time.

These reports are needed by the business in order to maintaining smoothness in various

activities of the business.

Inventory reports: Inventory report are also a method of managerial accounting

reporting through which the accountant of Capco can provide information relating to the

flow of inventory within the whole organisation. With the help of these reports, the

managers can determine the need of inventories in the business and develop more

effective plans for making the business more effective in using the inventories.

Performance reports: The performance reports are being prepared after analysing the

overall performance of the business and comparing it with the pre estimated performance

of it. These reports helps in determining the enhancement or reduction in performance of

4

and help them in their decision making process.

Management accounting reports includes budget reports, cost reports, performance

reports, inventory reports, etc. these are prepared by the managers for the purpose of helping the

managers in their various functions like planning, monitoring, organising, decision making, etc.

Further, there are various methods for preparing managerial accounting reporting as

under:

Cost reports: cost reports helps the managers in determining various areas where the

company has spent its funds and other resources. These reports include information

regarding various costs incurred by the business like fixed costs, various costs, labours,

various overheads, etc. managerial accountant prepares a final report that includes a

summary of all the costs incurred by the company (Methods of Management Accounting

Report, 2018). With the help of it, managers analyses the performance of business in cost

related activities and develops effective strategies for enhancing cost control within the

organisation.

Budgetary reports: Budgetary reports includes information regarding all the estimated

activities and performance of the business. These reports are helps the managers in

identifying the need of funds and other resources in the business within a specific time.

These reports are needed by the business in order to maintaining smoothness in various

activities of the business.

Inventory reports: Inventory report are also a method of managerial accounting

reporting through which the accountant of Capco can provide information relating to the

flow of inventory within the whole organisation. With the help of these reports, the

managers can determine the need of inventories in the business and develop more

effective plans for making the business more effective in using the inventories.

Performance reports: The performance reports are being prepared after analysing the

overall performance of the business and comparing it with the pre estimated performance

of it. These reports helps in determining the enhancement or reduction in performance of

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the business. These reports are required by the managers in order to enhance the overall

performance of the business organisation.

In this regard, it can be analysed that there are numerous methods of preparing

managerial accounting reporting. Preparation of these reports can help the managers of Capco in

developing more appropriate strategies for the business.

Critical evaluation of management accounting system and management accounting

reporting

Both management accounting system and management accounting reporting are needed

to be included in the business organisation, as both helps the managers in having effective

control over various business activities and enhancing the efficiency of company in performing

various business operations.

On the other hand, adoption of various management accounting systems and management

accounting tool may result in enhancing the functions of the managers and cost of overall

business organisation as well.

In this order, Capco should adopt management accounting system and management

accounting reporting after analysing each method and system carefully. Further, they should be

adopted in such a way so that they could result in providing a sustainable success to the business

organisation.

Showing preparation of income statement using marginal and absorption costing techniques

Management accounting techniques:

In management accounting system, managerial accountant creates various management

accounting reports like, income statement, budgetary reports, variance reports, etc. these reports

can be prepared by them through using some management accounting techniques like marginal

costing technique, absorption costing techniques, etc. although, these techniques may provide

different techniques to the business, therefore, the company should adopt the technique after

analysing all the techniques carefully.

Marginal costing technique

5

performance of the business organisation.

In this regard, it can be analysed that there are numerous methods of preparing

managerial accounting reporting. Preparation of these reports can help the managers of Capco in

developing more appropriate strategies for the business.

Critical evaluation of management accounting system and management accounting

reporting

Both management accounting system and management accounting reporting are needed

to be included in the business organisation, as both helps the managers in having effective

control over various business activities and enhancing the efficiency of company in performing

various business operations.

On the other hand, adoption of various management accounting systems and management

accounting tool may result in enhancing the functions of the managers and cost of overall

business organisation as well.

In this order, Capco should adopt management accounting system and management

accounting reporting after analysing each method and system carefully. Further, they should be

adopted in such a way so that they could result in providing a sustainable success to the business

organisation.

Showing preparation of income statement using marginal and absorption costing techniques

Management accounting techniques:

In management accounting system, managerial accountant creates various management

accounting reports like, income statement, budgetary reports, variance reports, etc. these reports

can be prepared by them through using some management accounting techniques like marginal

costing technique, absorption costing techniques, etc. although, these techniques may provide

different techniques to the business, therefore, the company should adopt the technique after

analysing all the techniques carefully.

Marginal costing technique

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

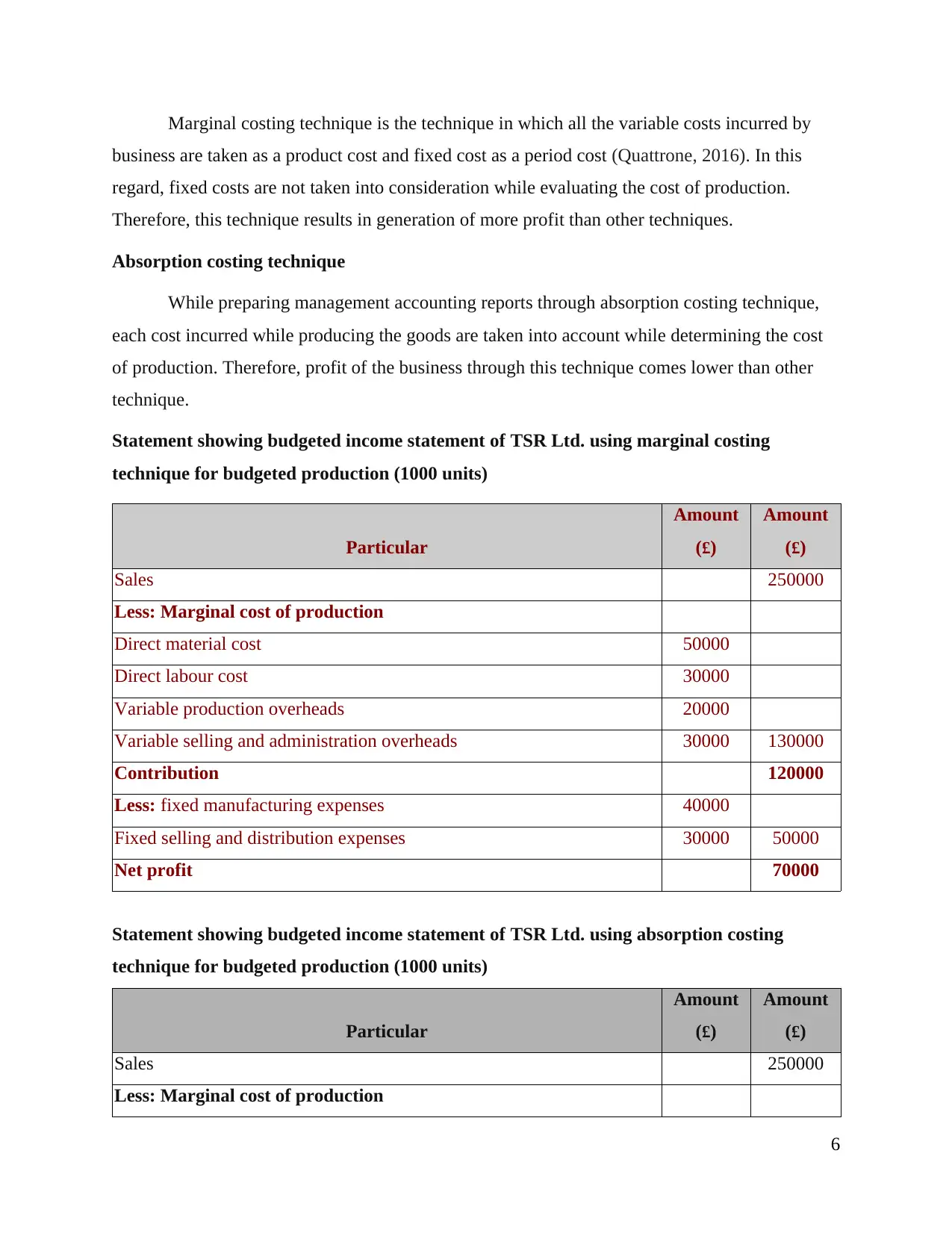

Marginal costing technique is the technique in which all the variable costs incurred by

business are taken as a product cost and fixed cost as a period cost (Quattrone, 2016). In this

regard, fixed costs are not taken into consideration while evaluating the cost of production.

Therefore, this technique results in generation of more profit than other techniques.

Absorption costing technique

While preparing management accounting reports through absorption costing technique,

each cost incurred while producing the goods are taken into account while determining the cost

of production. Therefore, profit of the business through this technique comes lower than other

technique.

Statement showing budgeted income statement of TSR Ltd. using marginal costing

technique for budgeted production (1000 units)

Particular

Amount

(£)

Amount

(£)

Sales 250000

Less: Marginal cost of production

Direct material cost 50000

Direct labour cost 30000

Variable production overheads 20000

Variable selling and administration overheads 30000 130000

Contribution 120000

Less: fixed manufacturing expenses 40000

Fixed selling and distribution expenses 30000 50000

Net profit 70000

Statement showing budgeted income statement of TSR Ltd. using absorption costing

technique for budgeted production (1000 units)

Particular

Amount

(£)

Amount

(£)

Sales 250000

Less: Marginal cost of production

6

business are taken as a product cost and fixed cost as a period cost (Quattrone, 2016). In this

regard, fixed costs are not taken into consideration while evaluating the cost of production.

Therefore, this technique results in generation of more profit than other techniques.

Absorption costing technique

While preparing management accounting reports through absorption costing technique,

each cost incurred while producing the goods are taken into account while determining the cost

of production. Therefore, profit of the business through this technique comes lower than other

technique.

Statement showing budgeted income statement of TSR Ltd. using marginal costing

technique for budgeted production (1000 units)

Particular

Amount

(£)

Amount

(£)

Sales 250000

Less: Marginal cost of production

Direct material cost 50000

Direct labour cost 30000

Variable production overheads 20000

Variable selling and administration overheads 30000 130000

Contribution 120000

Less: fixed manufacturing expenses 40000

Fixed selling and distribution expenses 30000 50000

Net profit 70000

Statement showing budgeted income statement of TSR Ltd. using absorption costing

technique for budgeted production (1000 units)

Particular

Amount

(£)

Amount

(£)

Sales 250000

Less: Marginal cost of production

6

Direct material cost 50000

Direct labour cost 30000

Variable production overhead 20000

Fixed production overhead 40000 140000

Gross profit 110000

Less: Selling and administrative costs

Variable cost 30000

Fixed cost 30000 60000

Net profit 50000

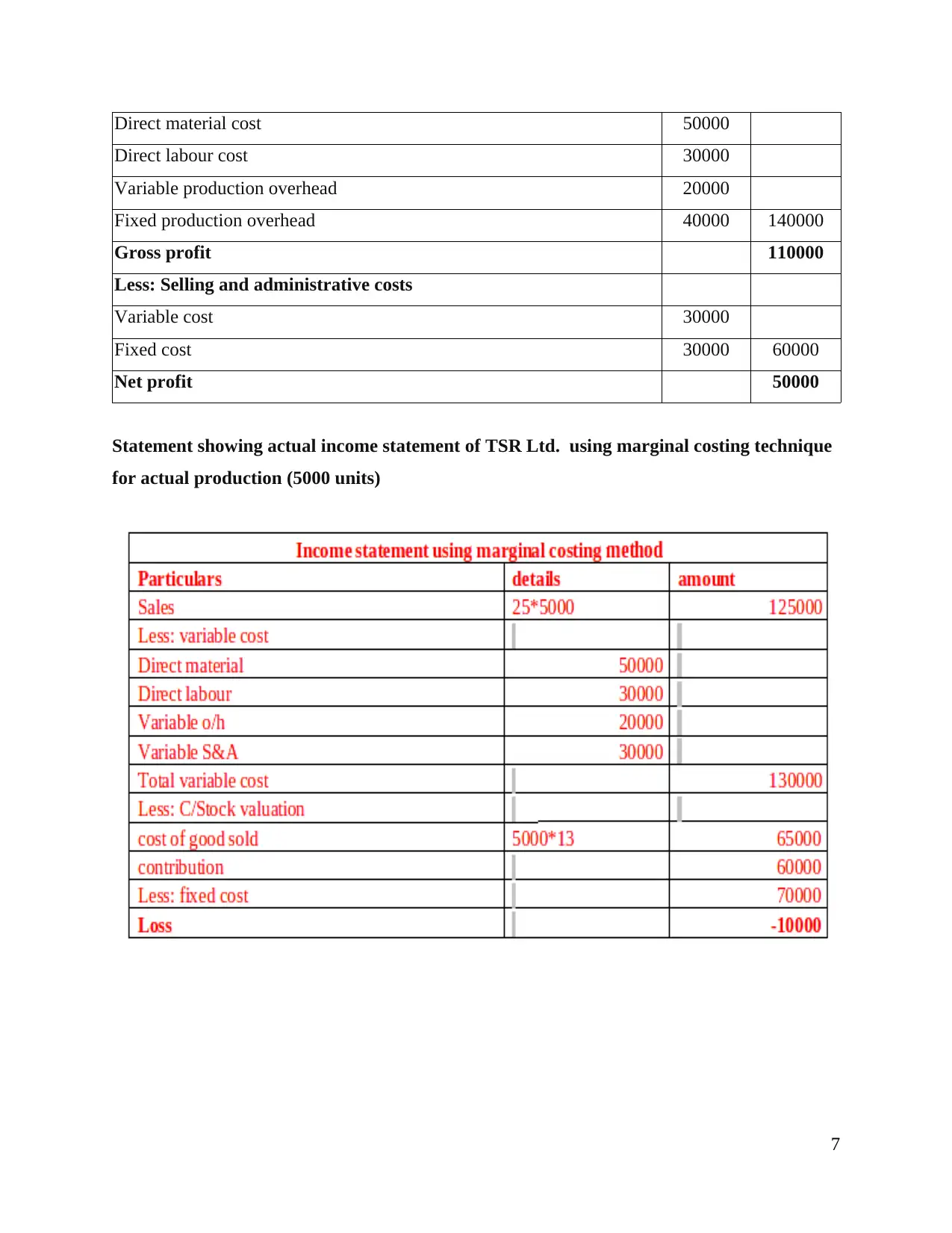

Statement showing actual income statement of TSR Ltd. using marginal costing technique

for actual production (5000 units)

7

Direct labour cost 30000

Variable production overhead 20000

Fixed production overhead 40000 140000

Gross profit 110000

Less: Selling and administrative costs

Variable cost 30000

Fixed cost 30000 60000

Net profit 50000

Statement showing actual income statement of TSR Ltd. using marginal costing technique

for actual production (5000 units)

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

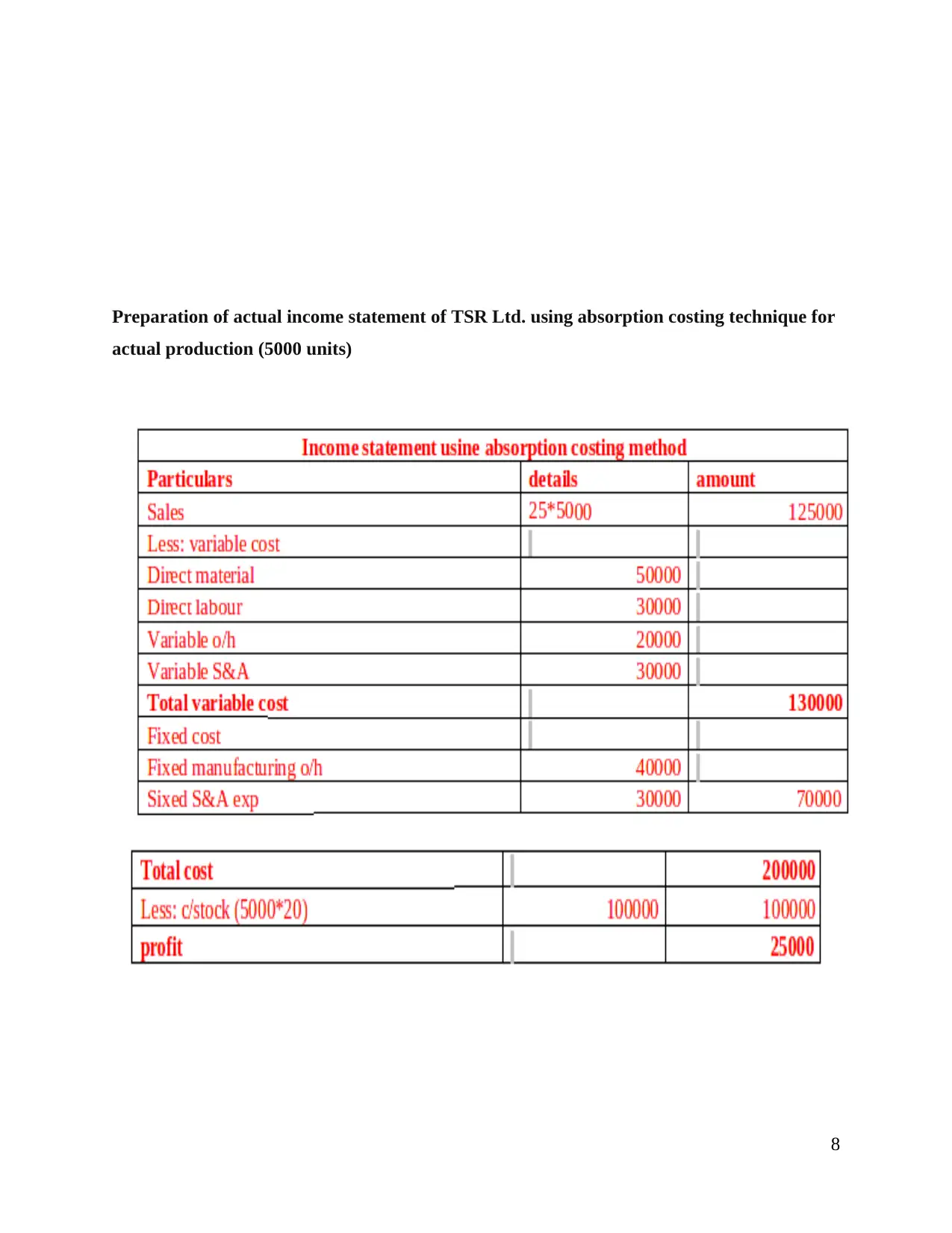

Preparation of actual income statement of TSR Ltd. using absorption costing technique for

actual production (5000 units)

8

actual production (5000 units)

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation

From the analysis of above income statements, it can be interpret that the TSR Ltd. Has

prepared a budget plan for producing 10000 units during a specific period. The company

produced 5000 units in the particular period.

Further, it can be interpret that the income statements form the marginal costing

technique for both actual and budgeted production are providing higher amount of profit than the

absorption costing. The key reason behind this difference is the difference in the methods of

evaluating cost of production of the business.

Variance:

Variance refers to the difference between the estimated position and actual position of the

company. For the purpose of determining variance in the business, the managers can use

standard costing system through which they can easily evaluate the difference between budgeted

data and estimated data of the business and detect the amount of variance easily.

Calculation of variance for TSR Ltd.

Particular

Actual

amount (£)

Budgeted

amount (£) Variance Percentage of variance

Material cost

variance 22000 20900 1100 (Adverse) 5.26 % (Adverse)

Material mix

variance 2200 2000 200 (Adverse) 10 % (Adverse)

Direct labour cost

variance 17680 15000 2680 (Adverse) 17.87 % (Adverse)

Direct labour hours 3400 3000 400 (Adverse) 13.33 % (Adverse)

9

From the analysis of above income statements, it can be interpret that the TSR Ltd. Has

prepared a budget plan for producing 10000 units during a specific period. The company

produced 5000 units in the particular period.

Further, it can be interpret that the income statements form the marginal costing

technique for both actual and budgeted production are providing higher amount of profit than the

absorption costing. The key reason behind this difference is the difference in the methods of

evaluating cost of production of the business.

Variance:

Variance refers to the difference between the estimated position and actual position of the

company. For the purpose of determining variance in the business, the managers can use

standard costing system through which they can easily evaluate the difference between budgeted

data and estimated data of the business and detect the amount of variance easily.

Calculation of variance for TSR Ltd.

Particular

Actual

amount (£)

Budgeted

amount (£) Variance Percentage of variance

Material cost

variance 22000 20900 1100 (Adverse) 5.26 % (Adverse)

Material mix

variance 2200 2000 200 (Adverse) 10 % (Adverse)

Direct labour cost

variance 17680 15000 2680 (Adverse) 17.87 % (Adverse)

Direct labour hours 3400 3000 400 (Adverse) 13.33 % (Adverse)

9

variance

Interpretation

From the interpretation of above variance statement, it can be evaluated that difference

has been occurred in the estimated cost and actual cost incurred by the TSR Ltd. These

difference can be arisen due to change in the cost of raw material, change in the labour cost or

change in the efficiency of working of the overall business as well.

Explaining different types of planning tools of budgetary control system

Budgetary control system

Budgetary control system can be defined as a process of management in which the

managers predicts various activities of the business by determining the efficiency of the business

based on its past performances (Li, 2016). This system helps the managers in developing

sufficiency of the resources within the business and ensuring the smooth working in each

department of the business organisation.

Budgetary control planning tools

For the purpose of preparing more effective and appropriate budget, the managers of

Capco can use various tools like cash budget, operating budget, etc. these tools of budgetary

control helps the managers in correctly predicting all the activities of the business for the purpose

of having effective control over all the activities of the business.

These planning tools can be easily understand as under: Cash budget: Cash budgets are prepared by the managers by estimating usage of cash

within various activities of the business (Cash Budget, 2019). The cash budget provides

information about various areas and sources through which cash would be spent and

raised within the business. Cash budgets helps the managers in planning for the utilisation

of cash and making sufficient cash available in the business as well.

Advantages

▪ It can help the mangers of Capco in reducing the chances of fraud within the

business.

▪ It may help in developing the business as more resourceful by predicting the

requirement of cash.

Disadvantages

10

Interpretation

From the interpretation of above variance statement, it can be evaluated that difference

has been occurred in the estimated cost and actual cost incurred by the TSR Ltd. These

difference can be arisen due to change in the cost of raw material, change in the labour cost or

change in the efficiency of working of the overall business as well.

Explaining different types of planning tools of budgetary control system

Budgetary control system

Budgetary control system can be defined as a process of management in which the

managers predicts various activities of the business by determining the efficiency of the business

based on its past performances (Li, 2016). This system helps the managers in developing

sufficiency of the resources within the business and ensuring the smooth working in each

department of the business organisation.

Budgetary control planning tools

For the purpose of preparing more effective and appropriate budget, the managers of

Capco can use various tools like cash budget, operating budget, etc. these tools of budgetary

control helps the managers in correctly predicting all the activities of the business for the purpose

of having effective control over all the activities of the business.

These planning tools can be easily understand as under: Cash budget: Cash budgets are prepared by the managers by estimating usage of cash

within various activities of the business (Cash Budget, 2019). The cash budget provides

information about various areas and sources through which cash would be spent and

raised within the business. Cash budgets helps the managers in planning for the utilisation

of cash and making sufficient cash available in the business as well.

Advantages

▪ It can help the mangers of Capco in reducing the chances of fraud within the

business.

▪ It may help in developing the business as more resourceful by predicting the

requirement of cash.

Disadvantages

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.