ACC 202: Management Accounting Analysis of Airline Decisions

VerifiedAdded on 2020/05/28

|8

|1517

|97

Homework Assignment

AI Summary

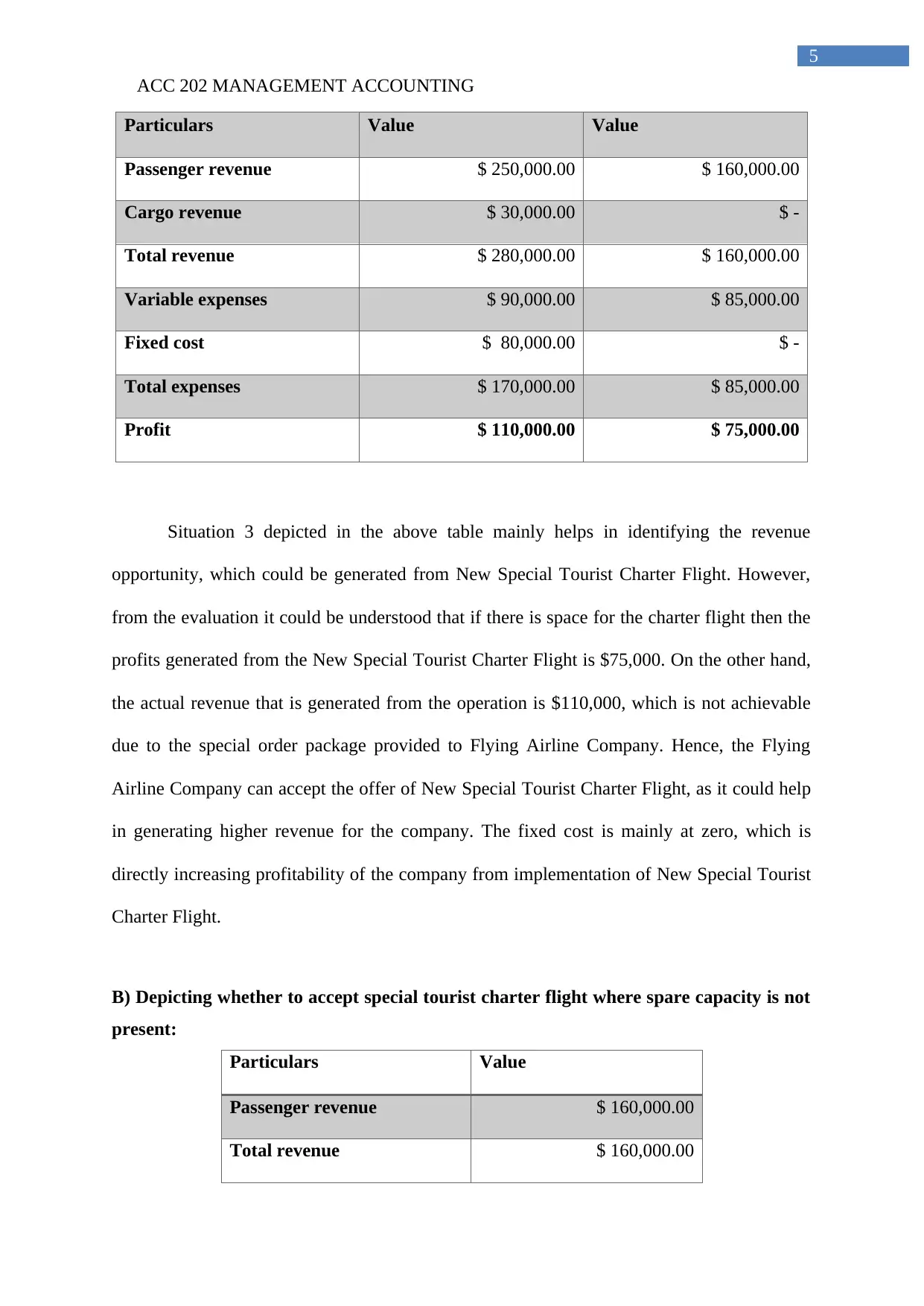

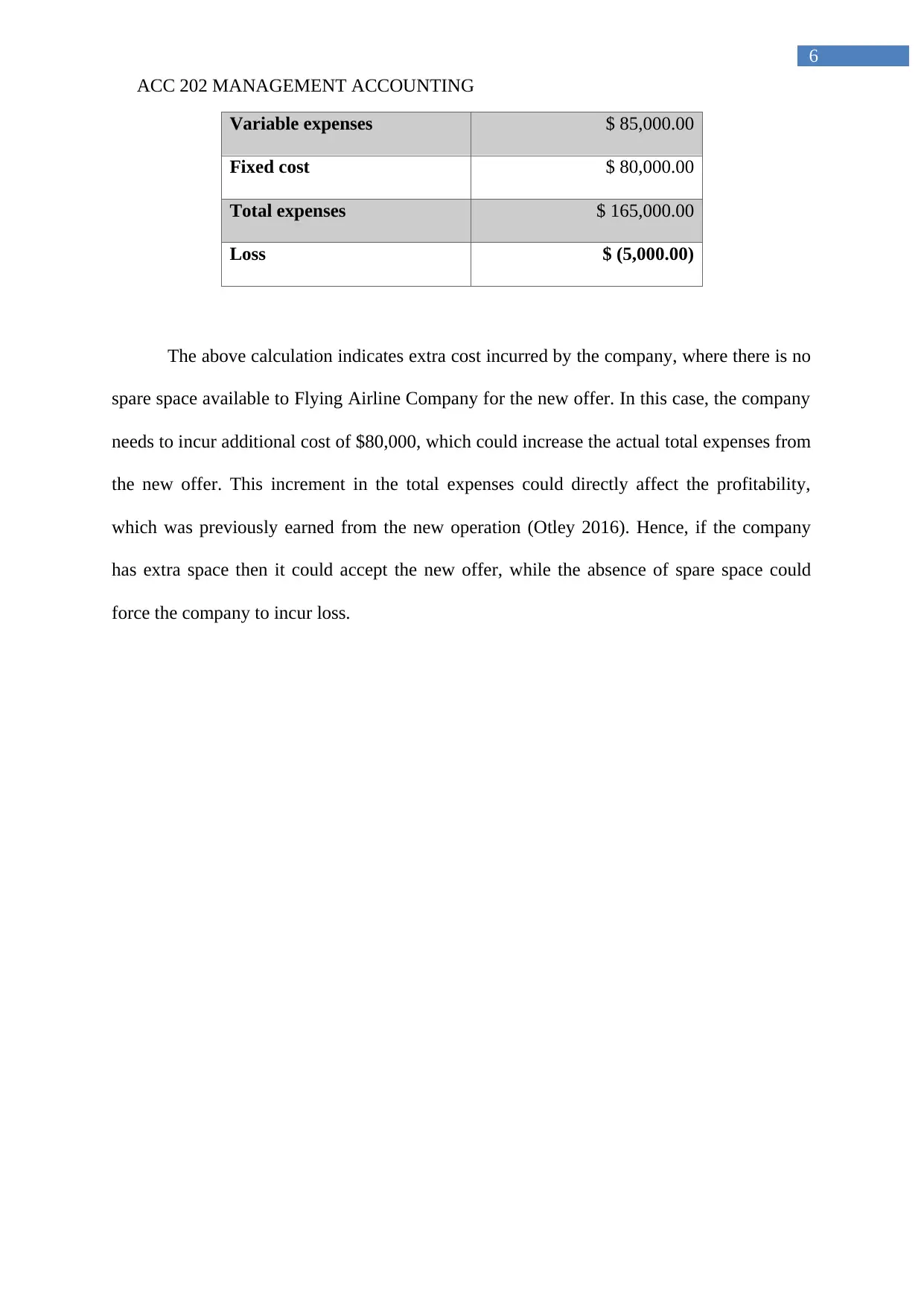

This assignment solution for ACC 202 Management Accounting analyzes financial scenarios faced by an airline company. The solution evaluates the decision of replacing a loader truck by comparing differential costs, concluding that the new loader is more beneficial. It also assesses the financial viability of different flight routes, comparing non-stop and with-stop routes using differential cost analysis, and considers other factors like social and economic influences. Finally, the solution determines whether to accept special tourist charter flights, considering situations with and without spare capacity, using relevant calculations to assess profitability. The assignment emphasizes cost analysis, revenue generation, and the impact of various decisions on the company's financial performance.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.