Management Accounting Report: Decision Making and Performance Analysis

VerifiedAdded on 2020/06/04

|14

|4207

|41

Report

AI Summary

This report provides a detailed analysis of management accounting principles and their practical applications within organizations. It explores the importance of management accounting in the decision-making process, focusing on how it improves overall performance by providing crucial financial and operational insights. The report delves into different management accounting systems, including job costing and inventory management, and examines the benefits derived from various reports such as budgeting, accounts receivable, and inventory reports. It further investigates the application of cost accounting techniques, specifically marginal and absorption costing, in the formulation of income statements. The second section of the report focuses on planning tools used for budgetary control, evaluating their advantages and disadvantages, and demonstrating their use in solving financial problems to achieve sustainable success. Additionally, the report assesses the effectiveness of management accounting systems in addressing financial issues and contributing to an organization's long-term success. The analysis includes case studies of companies like Rollin-son and Nero Ltd to illustrate the real-world application of these concepts.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

1. Importance of management accounting in decision making process for improving

performance.................................................................................................................................1

2. Different kind of management accounting systems ...............................................................2

3.Application of different kind of reports and benefits of management accounting systems ....3

4. Application of cost accounting techniques for formulation of income statements.................5

SECTION 2......................................................................................................................................8

PART A...........................................................................................................................................8

1. Advantages and disadvantages of planning tools used for budgetary control .......................8

2. Application of planning tools to solve financial problems and to attain sustainable success

...................................................................................................................................................10

PART B..........................................................................................................................................10

1. Effectiveness of management accounting systems to deal with financial problems ............10

2. Contribution of management accounting to lead organisation to attain sustainable success11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

1. Importance of management accounting in decision making process for improving

performance.................................................................................................................................1

2. Different kind of management accounting systems ...............................................................2

3.Application of different kind of reports and benefits of management accounting systems ....3

4. Application of cost accounting techniques for formulation of income statements.................5

SECTION 2......................................................................................................................................8

PART A...........................................................................................................................................8

1. Advantages and disadvantages of planning tools used for budgetary control .......................8

2. Application of planning tools to solve financial problems and to attain sustainable success

...................................................................................................................................................10

PART B..........................................................................................................................................10

1. Effectiveness of management accounting systems to deal with financial problems ............10

2. Contribution of management accounting to lead organisation to attain sustainable success11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting is important principle which combines accounting and costing

concepts with business operations and techniques which adds real value to the organisation.

Accounting officer of the organisation has the duty to implement accounting provisions which

help in functioning of different activities like planning, controlling, monitoring, risk assessment

etc. It helps in development of all areas and performance of every department. Through

collection of such different statistical and non statistical information different kind of reports are

formulated which helps to drive sustainable success (DRURY, 2013).

Section 1 includes the description about different kind of management accounting

systems and reports which are used by accounting officer of Rollin son and its importance

regarding improvement of the decision-making power. Also, application of marginal and

absorption costing for development of income statements. Section 2 of the report present about

different planning tools used by Nero Ltd. For budgetary control. Also, about use of management

accounting systems to respond financial issues.

SECTION 1

1. Importance of management accounting in decision making process for improving performance

Accounting officer of Rollin-son uses the provisions of management accounting to

improve their internal decisions and formulation of important policies which improves overall

performance of organisation. With the help of these systems large number of reports are prepared

which helps in determination of the roles for each and every employees. It contributes regarding

providence of direction to employees while performing their functions. Large number of benefits

are gathered by the management of Rollin-son through application of management accounting

provisions which are defined below:

Formulation of plan: Success of organisation is depends upon successful forecasting

and planning about future operations. It helps the production department of organisation

to produce the goods according to the needs of their customers. It helps in analysis of

present and future trend of business.

Determination of objectives: Provisions of management accounting helps in collection

of information about the functioning of different departments. On the basis of such

Management accounting is important principle which combines accounting and costing

concepts with business operations and techniques which adds real value to the organisation.

Accounting officer of the organisation has the duty to implement accounting provisions which

help in functioning of different activities like planning, controlling, monitoring, risk assessment

etc. It helps in development of all areas and performance of every department. Through

collection of such different statistical and non statistical information different kind of reports are

formulated which helps to drive sustainable success (DRURY, 2013).

Section 1 includes the description about different kind of management accounting

systems and reports which are used by accounting officer of Rollin son and its importance

regarding improvement of the decision-making power. Also, application of marginal and

absorption costing for development of income statements. Section 2 of the report present about

different planning tools used by Nero Ltd. For budgetary control. Also, about use of management

accounting systems to respond financial issues.

SECTION 1

1. Importance of management accounting in decision making process for improving performance

Accounting officer of Rollin-son uses the provisions of management accounting to

improve their internal decisions and formulation of important policies which improves overall

performance of organisation. With the help of these systems large number of reports are prepared

which helps in determination of the roles for each and every employees. It contributes regarding

providence of direction to employees while performing their functions. Large number of benefits

are gathered by the management of Rollin-son through application of management accounting

provisions which are defined below:

Formulation of plan: Success of organisation is depends upon successful forecasting

and planning about future operations. It helps the production department of organisation

to produce the goods according to the needs of their customers. It helps in analysis of

present and future trend of business.

Determination of objectives: Provisions of management accounting helps in collection

of information about the functioning of different departments. On the basis of such

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

information manager of organisation formulates the goals and provides the route which

helps in achievement of same.

Better services to customers: Application of cost control devices helps in reduction of

the cost and expenditures of their products. It helps in development of the felling of cost

conscious among employees. This system provides more emphasis on the maintenance of

quality of their products and provides to their customers at affordable prices.

Measurement of performance: The tools which are used by the accounting officer for

measurement of performance are budgetary control and standard costing. The method of

standard costing helps in determination of standards first and its comparison with actual.

Such comparison provides the information about deviations. It seems that performance of

organisation is good if actual cost not exceeds standard cost. On the other hand, method

of budgetary control helps in identification and measurement of efficiency of employees.

Helps in attainment of maximum profits: Management accounting provisions helps in

controlling unnecessary expenses. It provides the opportunity regarding removal of

inefficiencies. New techniques are identified which helps in achievement of the

predetermined goals and objectives. This results in attainment of maximum profits out of

the capital which is invested in business (Zang, 2011).

Forecasting cash flows: It is important for every organisation to improve their

understanding about the revenue which is going to ascertained in future period of time. It

can be analysed with the help of preparation of different kind of budgets and trend charts.

It helps in effective allocation of money and resources which provides opportunity to

attain maximum returns for their investments.

2. Different kind of management accounting systems

Management Accounting: It is the process which includes different functions like

collecting, analysing, reporting of information about the operations and finances of business.

These information is generally used by the the internal parties of organisation like manager for

proper operation of day to day functions and improvement of short term decision-making. It

includes the use of different kind of tools like budgeting, variance analysis, BEP etc. which

contributes in accomplishment of the common goals of organisation. It assist the manger of

Rollin-son regarding achievement of better planning and control through preparation of various

strategies and budgets.

helps in achievement of same.

Better services to customers: Application of cost control devices helps in reduction of

the cost and expenditures of their products. It helps in development of the felling of cost

conscious among employees. This system provides more emphasis on the maintenance of

quality of their products and provides to their customers at affordable prices.

Measurement of performance: The tools which are used by the accounting officer for

measurement of performance are budgetary control and standard costing. The method of

standard costing helps in determination of standards first and its comparison with actual.

Such comparison provides the information about deviations. It seems that performance of

organisation is good if actual cost not exceeds standard cost. On the other hand, method

of budgetary control helps in identification and measurement of efficiency of employees.

Helps in attainment of maximum profits: Management accounting provisions helps in

controlling unnecessary expenses. It provides the opportunity regarding removal of

inefficiencies. New techniques are identified which helps in achievement of the

predetermined goals and objectives. This results in attainment of maximum profits out of

the capital which is invested in business (Zang, 2011).

Forecasting cash flows: It is important for every organisation to improve their

understanding about the revenue which is going to ascertained in future period of time. It

can be analysed with the help of preparation of different kind of budgets and trend charts.

It helps in effective allocation of money and resources which provides opportunity to

attain maximum returns for their investments.

2. Different kind of management accounting systems

Management Accounting: It is the process which includes different functions like

collecting, analysing, reporting of information about the operations and finances of business.

These information is generally used by the the internal parties of organisation like manager for

proper operation of day to day functions and improvement of short term decision-making. It

includes the use of different kind of tools like budgeting, variance analysis, BEP etc. which

contributes in accomplishment of the common goals of organisation. It assist the manger of

Rollin-son regarding achievement of better planning and control through preparation of various

strategies and budgets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Different management accounting systems

Provisions of management accounting includes different kind of systems which helps in

controlling the different aspects of organisation. It is the duty of accounting officer of Rollin-son

is to integrate the functions of these systems with organisational processes. There is huge

requirement of implementation of such systems in organisation for completion of the tasks and

activities within stipulated period of time. It improves the overall efficiency of each and every

department of organisation. These accounting systems are defined below:

Job costing system: This system helps in tracking of the cost which is incurred on labour

used on performance of any particular job. It is used as profitability reporting enabling

from performance of job. It is used by the organisations which are manufacturing

different kind of products. It provides the opportunity regarding identification of most

profitable project on which need to provide more efforts for achieving maximum profits.

Price optimising system: It helps in analysis of the behaviour of customer. There is

direct relation of price regarding influencing the behaviour of customers. This system

helps in determination of the response of customers due to change in prices of different

products. It provides the opportunity to management of organisation is to adopt best price

strategies and policies which helps in attainment of objectives and maximisation of

operating profits (Qian, Burritt and Monroe, 2011).

Inventory management system: It is the process of supervision and monitoring the

existing stock and assets of organisation. Through implementation of this system

management of Rollin-son ensures effective and efficient flow of inventory within

organisation. This system helps in tracking of goods through entire supply chain. This

will include about adoption of inventory management software's which has different

features like bar coding, reporting, inventory alerts, inventory forecasting etc. In

manufacturing organisation like Rollin-son, process of inventory management includes

about materials tracking, level of stock of parts and finished products, automatic recoding

and integration with ERP software.

3.Application of different kind of reports and benefits of management accounting systems

It is a document which contains the information about diversified activities. Accounting

officer of Rollin-son prepares different kind of reports like performance, budgeting, accounts

receivable, inventory management etc. These reports makes the comparison work of actual

Provisions of management accounting includes different kind of systems which helps in

controlling the different aspects of organisation. It is the duty of accounting officer of Rollin-son

is to integrate the functions of these systems with organisational processes. There is huge

requirement of implementation of such systems in organisation for completion of the tasks and

activities within stipulated period of time. It improves the overall efficiency of each and every

department of organisation. These accounting systems are defined below:

Job costing system: This system helps in tracking of the cost which is incurred on labour

used on performance of any particular job. It is used as profitability reporting enabling

from performance of job. It is used by the organisations which are manufacturing

different kind of products. It provides the opportunity regarding identification of most

profitable project on which need to provide more efforts for achieving maximum profits.

Price optimising system: It helps in analysis of the behaviour of customer. There is

direct relation of price regarding influencing the behaviour of customers. This system

helps in determination of the response of customers due to change in prices of different

products. It provides the opportunity to management of organisation is to adopt best price

strategies and policies which helps in attainment of objectives and maximisation of

operating profits (Qian, Burritt and Monroe, 2011).

Inventory management system: It is the process of supervision and monitoring the

existing stock and assets of organisation. Through implementation of this system

management of Rollin-son ensures effective and efficient flow of inventory within

organisation. This system helps in tracking of goods through entire supply chain. This

will include about adoption of inventory management software's which has different

features like bar coding, reporting, inventory alerts, inventory forecasting etc. In

manufacturing organisation like Rollin-son, process of inventory management includes

about materials tracking, level of stock of parts and finished products, automatic recoding

and integration with ERP software.

3.Application of different kind of reports and benefits of management accounting systems

It is a document which contains the information about diversified activities. Accounting

officer of Rollin-son prepares different kind of reports like performance, budgeting, accounts

receivable, inventory management etc. These reports makes the comparison work of actual

performance with budgeted more easy. On the basis of such comparison, new methods are

adopted which helps to improve the level of work and contributes in achievement of such

standards. Different kind of reports are mentioned below:

Budgeting reports: This reports are prepared on the basis actual expenditure which is

incurred by organisation in earlier period of time. The main aim behind formulation of

this report is to provide help in evaluation of each and every department's performance. It

helps in controlling unnecessary expenses. Incentives programmes are designed by

management on the basis of their actual performances. It motivates the employees to earn

large through performing well in organisation.

Accounts receivable report: This report presents the list of unpaid customers. It is

considered as primary tool which helps in collection of the due amount within given

period. By using this system unpaid invoices are segregated on the basis of time period. It

helps in determination of the issues which are associated with collection process of

organisation. It helps in tightening of credit policies which contributes in reduction of

old bad debts and maintenance of effective working capital requirements (Lukka and

Vinnari, 2014).

Inventory and manufacturing reports: This report is prepared by manufacturing

organisation like Rollin-son for development of their manufacturing and inventory

process more effective and efficient. It improves the production capacity of the

organisation and brings quality in their products which satisfies the different demand of

customers. Effective and timely allocation of resources helps in optimum utilisation of

resources and reduction of wastes during manufacturing process.

Benefits of different kind of management accounting systems

There are many accounting systems are adopted by the management of Rollin-son which

are discussed above. All such systems have their own different benefits in organisation. Benefits

of all individual accounting systems are mentioned below:

Job costing system

It helps in identification of the profitability of the each job

It helps in detailed evaluation of the cost of material, labour and overheads

It helps in saving time and money through identification of defective work and processes

Price optimisation system

adopted which helps to improve the level of work and contributes in achievement of such

standards. Different kind of reports are mentioned below:

Budgeting reports: This reports are prepared on the basis actual expenditure which is

incurred by organisation in earlier period of time. The main aim behind formulation of

this report is to provide help in evaluation of each and every department's performance. It

helps in controlling unnecessary expenses. Incentives programmes are designed by

management on the basis of their actual performances. It motivates the employees to earn

large through performing well in organisation.

Accounts receivable report: This report presents the list of unpaid customers. It is

considered as primary tool which helps in collection of the due amount within given

period. By using this system unpaid invoices are segregated on the basis of time period. It

helps in determination of the issues which are associated with collection process of

organisation. It helps in tightening of credit policies which contributes in reduction of

old bad debts and maintenance of effective working capital requirements (Lukka and

Vinnari, 2014).

Inventory and manufacturing reports: This report is prepared by manufacturing

organisation like Rollin-son for development of their manufacturing and inventory

process more effective and efficient. It improves the production capacity of the

organisation and brings quality in their products which satisfies the different demand of

customers. Effective and timely allocation of resources helps in optimum utilisation of

resources and reduction of wastes during manufacturing process.

Benefits of different kind of management accounting systems

There are many accounting systems are adopted by the management of Rollin-son which

are discussed above. All such systems have their own different benefits in organisation. Benefits

of all individual accounting systems are mentioned below:

Job costing system

It helps in identification of the profitability of the each job

It helps in detailed evaluation of the cost of material, labour and overheads

It helps in saving time and money through identification of defective work and processes

Price optimisation system

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This system helps in determination and influencing the attitude of customers

It provides opportunity regarding segmentation of customers

It helps to earn large number of profits through selection of affordable pricing strategies

Inventory management system

It helps in ordering of the inventories at that time when they are needed

It provides the opportunity to management regarding saving of their time and cost

through attainment of effectiveness in inventory control system

Integration of reports with organisational functions

Budgeting reports: Integration of these reports helps in designing path which includes

the information regarding objectives and targets. It helps in providence of roles and

responsibilities to employees.

Accounts receivable report: Integration of this report helps in collection of due amount

by implementation of new credit policies. It brings flexibility and accuracy in their

policies which helps in maintaining liquidity in organisation.

Inventory and manufacturing reports: This report helps in management of level of

stock in organisation. It improves the productivity and quality of their existing products

and provides opportunity to satisfy the different demand of their customers (Bodie,

2013).

4. Application of cost accounting techniques for formulation of income statements

Cost: It is the amount which is paid or charged for achieving something special by

management of organisation. It provides the opportunity to the manager of Rollin-son is to

produce quality products which satisfies the different requirements and preferences of customers.

It is the monetary value of expenditures like raw materials, equipment, supplies, labour, products

etc.

Cost is bifurcated into different types in organisation. For ex., fixed and variable,

opportunity and outlay, historical and replacement cost etc. Variable and direct cost are

considered as most relevant which helps in maximisation of their profitability. Direct cost

includes important aspect which are related to the final mark-up stages of product or service.

Difference between Marginal and Absorption costing

It provides opportunity regarding segmentation of customers

It helps to earn large number of profits through selection of affordable pricing strategies

Inventory management system

It helps in ordering of the inventories at that time when they are needed

It provides the opportunity to management regarding saving of their time and cost

through attainment of effectiveness in inventory control system

Integration of reports with organisational functions

Budgeting reports: Integration of these reports helps in designing path which includes

the information regarding objectives and targets. It helps in providence of roles and

responsibilities to employees.

Accounts receivable report: Integration of this report helps in collection of due amount

by implementation of new credit policies. It brings flexibility and accuracy in their

policies which helps in maintaining liquidity in organisation.

Inventory and manufacturing reports: This report helps in management of level of

stock in organisation. It improves the productivity and quality of their existing products

and provides opportunity to satisfy the different demand of their customers (Bodie,

2013).

4. Application of cost accounting techniques for formulation of income statements

Cost: It is the amount which is paid or charged for achieving something special by

management of organisation. It provides the opportunity to the manager of Rollin-son is to

produce quality products which satisfies the different requirements and preferences of customers.

It is the monetary value of expenditures like raw materials, equipment, supplies, labour, products

etc.

Cost is bifurcated into different types in organisation. For ex., fixed and variable,

opportunity and outlay, historical and replacement cost etc. Variable and direct cost are

considered as most relevant which helps in maximisation of their profitability. Direct cost

includes important aspect which are related to the final mark-up stages of product or service.

Difference between Marginal and Absorption costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

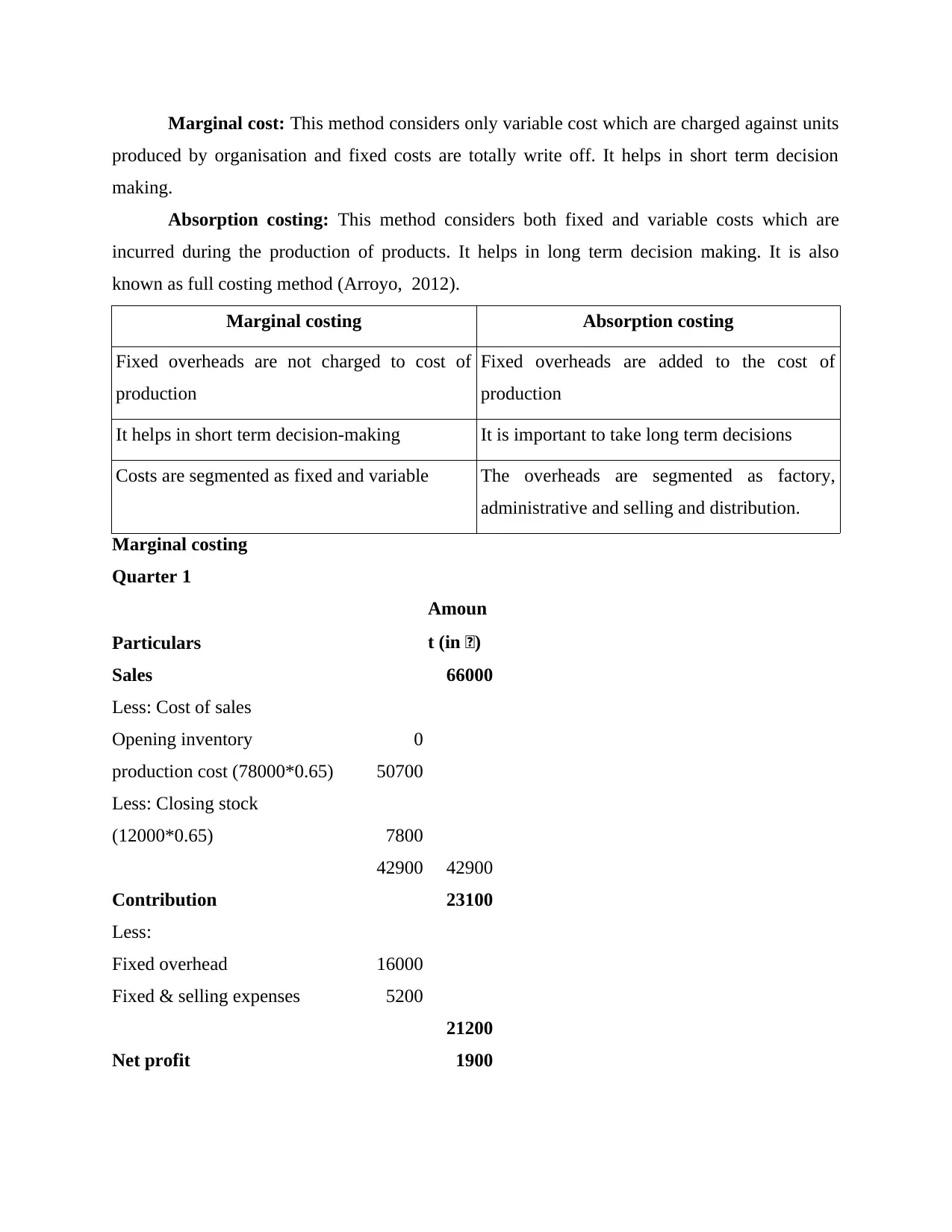

Marginal cost: This method considers only variable cost which are charged against units

produced by organisation and fixed costs are totally write off. It helps in short term decision

making.

Absorption costing: This method considers both fixed and variable costs which are

incurred during the production of products. It helps in long term decision making. It is also

known as full costing method (Arroyo, 2012).

Marginal costing Absorption costing

Fixed overheads are not charged to cost of

production

Fixed overheads are added to the cost of

production

It helps in short term decision-making It is important to take long term decisions

Costs are segmented as fixed and variable The overheads are segmented as factory,

administrative and selling and distribution.

Marginal costing

Quarter 1

Particulars

Amoun

t (in £)

Sales 66000

Less: Cost of sales

Opening inventory 0

production cost (78000*0.65) 50700

Less: Closing stock

(12000*0.65) 7800

42900 42900

Contribution 23100

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 1900

produced by organisation and fixed costs are totally write off. It helps in short term decision

making.

Absorption costing: This method considers both fixed and variable costs which are

incurred during the production of products. It helps in long term decision making. It is also

known as full costing method (Arroyo, 2012).

Marginal costing Absorption costing

Fixed overheads are not charged to cost of

production

Fixed overheads are added to the cost of

production

It helps in short term decision-making It is important to take long term decisions

Costs are segmented as fixed and variable The overheads are segmented as factory,

administrative and selling and distribution.

Marginal costing

Quarter 1

Particulars

Amoun

t (in £)

Sales 66000

Less: Cost of sales

Opening inventory 0

production cost (78000*0.65) 50700

Less: Closing stock

(12000*0.65) 7800

42900 42900

Contribution 23100

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 1900

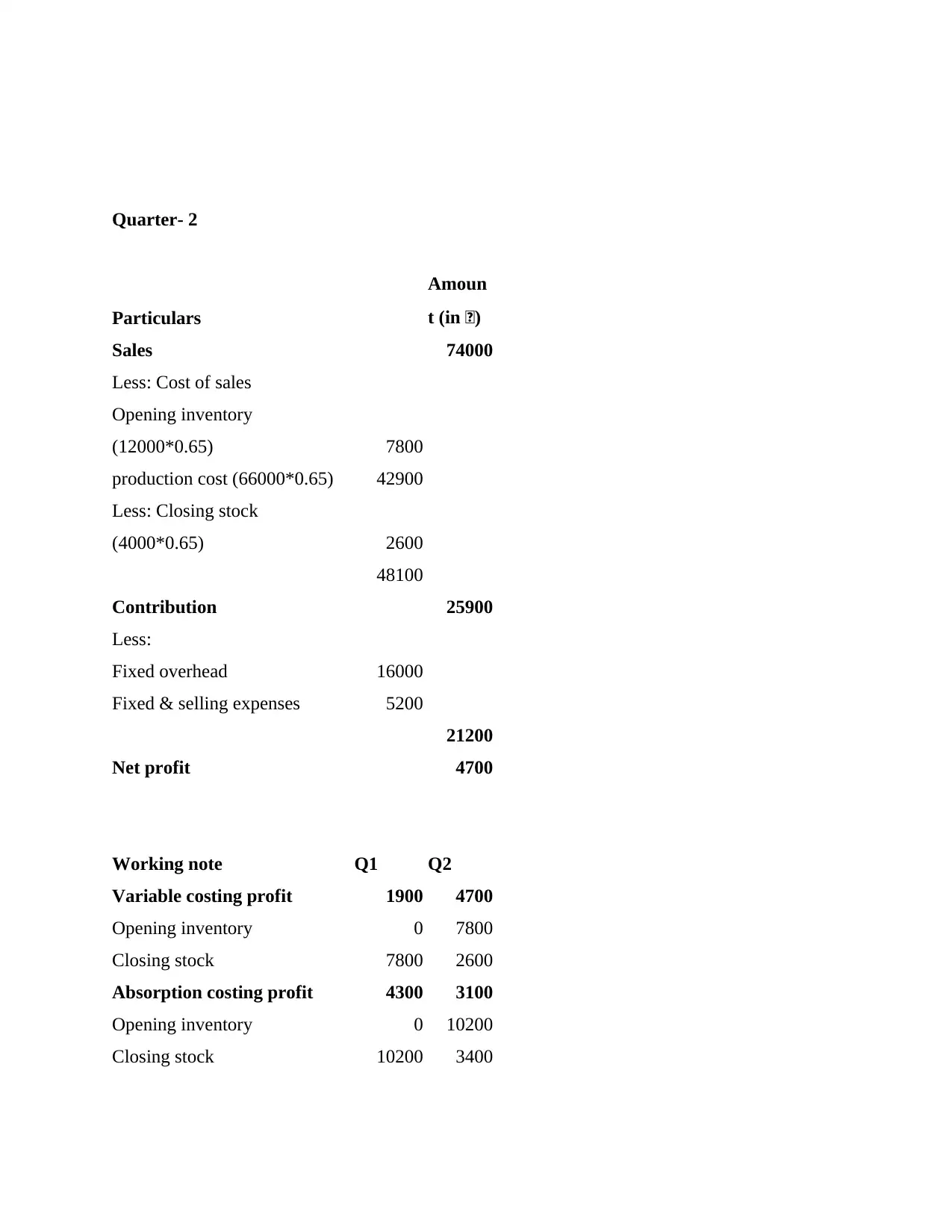

Quarter- 2

Particulars

Amoun

t (in £)

Sales 74000

Less: Cost of sales

Opening inventory

(12000*0.65) 7800

production cost (66000*0.65) 42900

Less: Closing stock

(4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 4700

Working note Q1 Q2

Variable costing profit 1900 4700

Opening inventory 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

Particulars

Amoun

t (in £)

Sales 74000

Less: Cost of sales

Opening inventory

(12000*0.65) 7800

production cost (66000*0.65) 42900

Less: Closing stock

(4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 4700

Working note Q1 Q2

Variable costing profit 1900 4700

Opening inventory 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

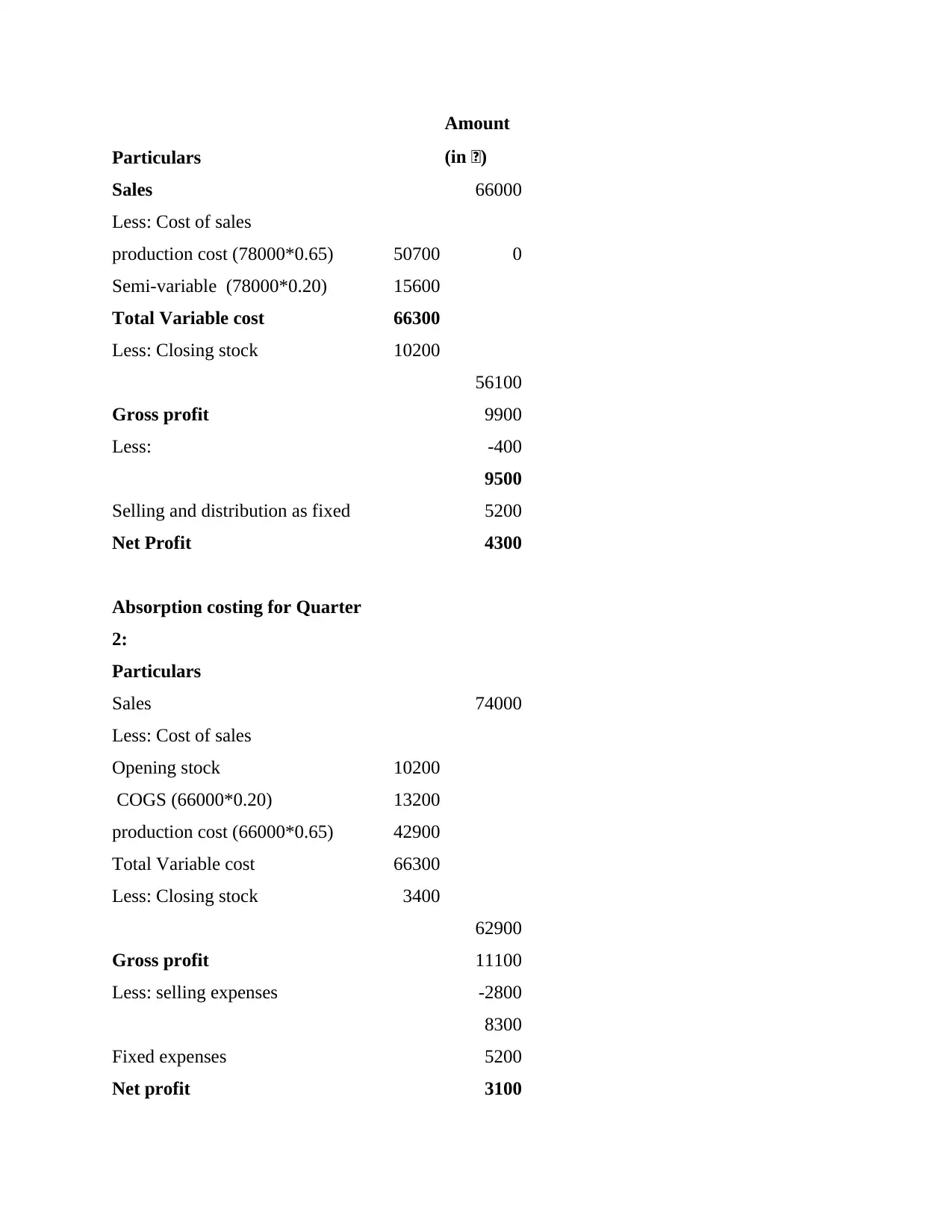

Absorption costing for Quarter

1:

1:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars

Amount

(in £)

Sales 66000

Less: Cost of sales

production cost (78000*0.65) 50700 0

Semi-variable (78000*0.20) 15600

Total Variable cost 66300

Less: Closing stock 10200

56100

Gross profit 9900

Less: -400

9500

Selling and distribution as fixed 5200

Net Profit 4300

Absorption costing for Quarter

2:

Particulars

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*0.20) 13200

production cost (66000*0.65) 42900

Total Variable cost 66300

Less: Closing stock 3400

62900

Gross profit 11100

Less: selling expenses -2800

8300

Fixed expenses 5200

Net profit 3100

Amount

(in £)

Sales 66000

Less: Cost of sales

production cost (78000*0.65) 50700 0

Semi-variable (78000*0.20) 15600

Total Variable cost 66300

Less: Closing stock 10200

56100

Gross profit 9900

Less: -400

9500

Selling and distribution as fixed 5200

Net Profit 4300

Absorption costing for Quarter

2:

Particulars

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*0.20) 13200

production cost (66000*0.65) 42900

Total Variable cost 66300

Less: Closing stock 3400

62900

Gross profit 11100

Less: selling expenses -2800

8300

Fixed expenses 5200

Net profit 3100

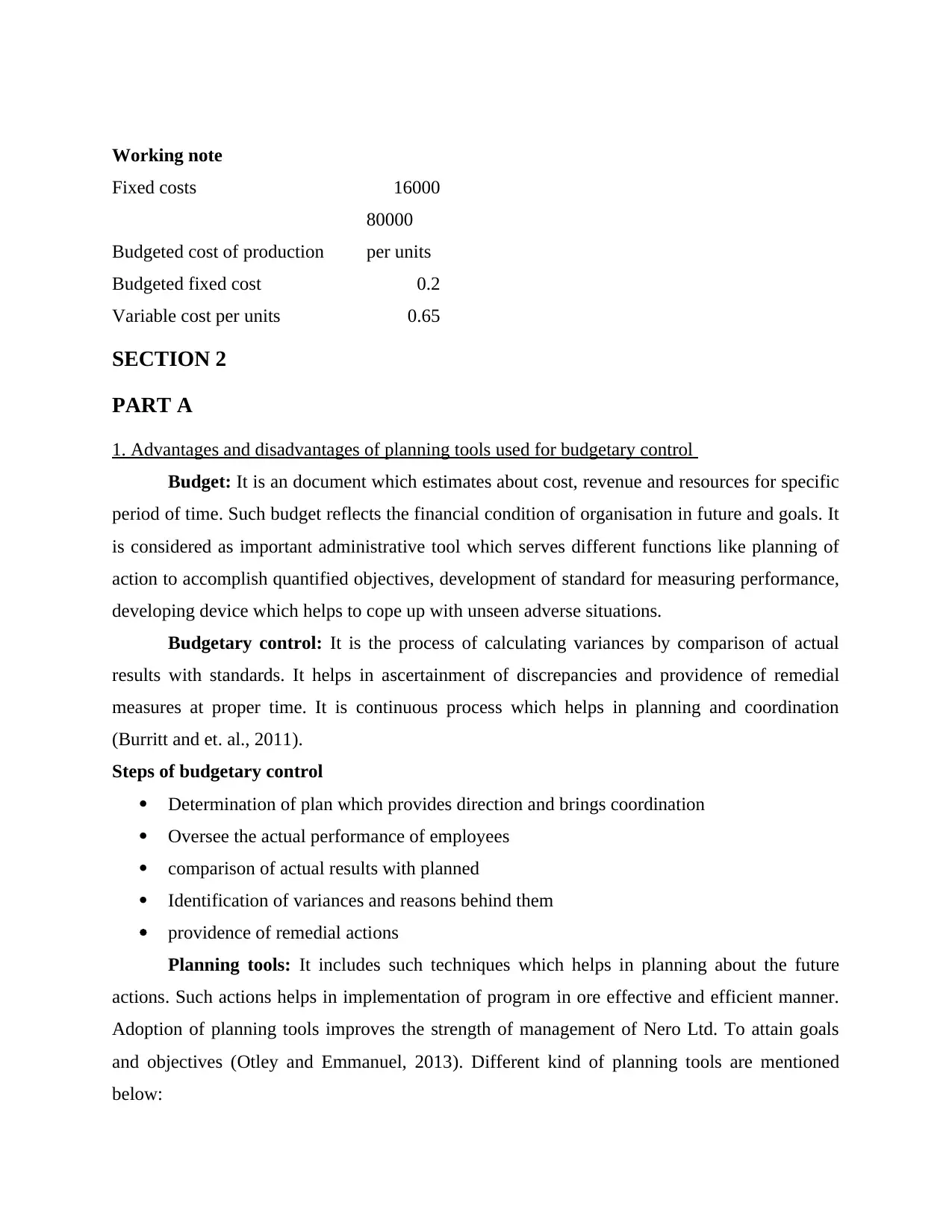

Working note

Fixed costs 16000

Budgeted cost of production

80000

per units

Budgeted fixed cost 0.2

Variable cost per units 0.65

SECTION 2

PART A

1. Advantages and disadvantages of planning tools used for budgetary control

Budget: It is an document which estimates about cost, revenue and resources for specific

period of time. Such budget reflects the financial condition of organisation in future and goals. It

is considered as important administrative tool which serves different functions like planning of

action to accomplish quantified objectives, development of standard for measuring performance,

developing device which helps to cope up with unseen adverse situations.

Budgetary control: It is the process of calculating variances by comparison of actual

results with standards. It helps in ascertainment of discrepancies and providence of remedial

measures at proper time. It is continuous process which helps in planning and coordination

(Burritt and et. al., 2011).

Steps of budgetary control

Determination of plan which provides direction and brings coordination

Oversee the actual performance of employees

comparison of actual results with planned

Identification of variances and reasons behind them

providence of remedial actions

Planning tools: It includes such techniques which helps in planning about the future

actions. Such actions helps in implementation of program in ore effective and efficient manner.

Adoption of planning tools improves the strength of management of Nero Ltd. To attain goals

and objectives (Otley and Emmanuel, 2013). Different kind of planning tools are mentioned

below:

Fixed costs 16000

Budgeted cost of production

80000

per units

Budgeted fixed cost 0.2

Variable cost per units 0.65

SECTION 2

PART A

1. Advantages and disadvantages of planning tools used for budgetary control

Budget: It is an document which estimates about cost, revenue and resources for specific

period of time. Such budget reflects the financial condition of organisation in future and goals. It

is considered as important administrative tool which serves different functions like planning of

action to accomplish quantified objectives, development of standard for measuring performance,

developing device which helps to cope up with unseen adverse situations.

Budgetary control: It is the process of calculating variances by comparison of actual

results with standards. It helps in ascertainment of discrepancies and providence of remedial

measures at proper time. It is continuous process which helps in planning and coordination

(Burritt and et. al., 2011).

Steps of budgetary control

Determination of plan which provides direction and brings coordination

Oversee the actual performance of employees

comparison of actual results with planned

Identification of variances and reasons behind them

providence of remedial actions

Planning tools: It includes such techniques which helps in planning about the future

actions. Such actions helps in implementation of program in ore effective and efficient manner.

Adoption of planning tools improves the strength of management of Nero Ltd. To attain goals

and objectives (Otley and Emmanuel, 2013). Different kind of planning tools are mentioned

below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.