Management Accounting Report: Budgetary Control and Cost Analysis

VerifiedAdded on 2020/06/03

|16

|4006

|37

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their application within a company, specifically focusing on X PLC. It delves into key concepts such as management accounting systems, types of reporting, and the benefits of implementing these systems to maximize profitability and enhance efficiency. The report includes a detailed analysis of marginal and absorption costing methods, demonstrated through income statements, and explores different planning tools for budgetary control, including capital and operating budgets. Furthermore, it examines the use of these tools in preparing and forecasting budgets, with a specific focus on sales budgets. The report concludes by evaluating how management accounting systems respond to financial problems and lead organizations to sustainable success, supported by case studies and financial data.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

P1 Management accounting and essential requirements of various type of management

accounting system..................................................................................................................1

P2 Types of management accounting reporting.....................................................................2

M1 Benefits of management accounting system and its application within the company.....3

CASE 1............................................................................................................................................3

P3 Calculate cost by using marginal costing method.............................................................3

M2 Income statement by using management accounting techniques....................................4

D2 Interpretation of financial reports.....................................................................................5

TASK...............................................................................................................................................6

P4 Explanation on different types of planning tools for budgetary control ..........................6

CASE 2............................................................................................................................................7

M3 Analyse the use of various planning tools and it application for prepare and forecast

budgets....................................................................................................................................7

P5 Management accounting system respond financial problems.........................................10

CASE 3..........................................................................................................................................10

M4 Analyse how management accounting can lead organisation to sustainable success....10

CASE 2&3.....................................................................................................................................11

D3 Critically evaluate how planning tools respond accounting problems...........................11

CONCLUSION ............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

P1 Management accounting and essential requirements of various type of management

accounting system..................................................................................................................1

P2 Types of management accounting reporting.....................................................................2

M1 Benefits of management accounting system and its application within the company.....3

CASE 1............................................................................................................................................3

P3 Calculate cost by using marginal costing method.............................................................3

M2 Income statement by using management accounting techniques....................................4

D2 Interpretation of financial reports.....................................................................................5

TASK...............................................................................................................................................6

P4 Explanation on different types of planning tools for budgetary control ..........................6

CASE 2............................................................................................................................................7

M3 Analyse the use of various planning tools and it application for prepare and forecast

budgets....................................................................................................................................7

P5 Management accounting system respond financial problems.........................................10

CASE 3..........................................................................................................................................10

M4 Analyse how management accounting can lead organisation to sustainable success....10

CASE 2&3.....................................................................................................................................11

D3 Critically evaluate how planning tools respond accounting problems...........................11

CONCLUSION ............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management Accounting is an application that assist the manager in formulation of

company's strategy, provide an accurate financial and statistical data to take short-term decisions.

It is the process that produced management reports on weekly or monthly basis to internal

stakeholders. The present report will be discussed on management costing techniques to prepare

financial reports (Tucker and Schaltegger,2016). The assignment covering all the aspects of

management accounting system and apply within the organisation. There will be also study on

the various types of planning tool that is adopted by company for budgetary control.

TASK

P1 Management accounting and essential requirements of various type of management

accounting system

Management accounting is a branch of accounting that identifying, measuring, analysing

and interpreting the financial and statistical data for the aim of achieving organisation's goals.

The information is used by manager of a firm to establish the dynamic solution to enhance the

business performance. The management accounting system is a collection of financial

information acquired from business operations. It involves fluctuation in cost of raw material,

shift in inventory and sales data that will be turned into management report. It is necessary to

integrate an accounting system within the company as it will assist the manager to take the

effective decisions. The Company has adopted different types of management accounting system

that will be described as follows:-

Throughput accounting system:- It is an approach of management accounting that

supports the managers by provide them essential information for the improvement in

entity profitability. It is mainly focused on cash and not consider cost of products or

services at the time of its selling (Dulleck and et. al., 2016). It has applied by Company to

determine the theory of constraints that helps them to maximize profits by reducing cost.

Cost accounting system:- It is a framework used by organisation for the purpose of

profitability analysis, control cost and inventory valuation through determine cost of

products. It indicated which products gives profitability or not and it has ascertained

accurate product cost. It helps the management accountant to provided a detailed

information of cost that able to operate business function effectively.

Difference between management accounting and financial accounting

1

Management Accounting is an application that assist the manager in formulation of

company's strategy, provide an accurate financial and statistical data to take short-term decisions.

It is the process that produced management reports on weekly or monthly basis to internal

stakeholders. The present report will be discussed on management costing techniques to prepare

financial reports (Tucker and Schaltegger,2016). The assignment covering all the aspects of

management accounting system and apply within the organisation. There will be also study on

the various types of planning tool that is adopted by company for budgetary control.

TASK

P1 Management accounting and essential requirements of various type of management

accounting system

Management accounting is a branch of accounting that identifying, measuring, analysing

and interpreting the financial and statistical data for the aim of achieving organisation's goals.

The information is used by manager of a firm to establish the dynamic solution to enhance the

business performance. The management accounting system is a collection of financial

information acquired from business operations. It involves fluctuation in cost of raw material,

shift in inventory and sales data that will be turned into management report. It is necessary to

integrate an accounting system within the company as it will assist the manager to take the

effective decisions. The Company has adopted different types of management accounting system

that will be described as follows:-

Throughput accounting system:- It is an approach of management accounting that

supports the managers by provide them essential information for the improvement in

entity profitability. It is mainly focused on cash and not consider cost of products or

services at the time of its selling (Dulleck and et. al., 2016). It has applied by Company to

determine the theory of constraints that helps them to maximize profits by reducing cost.

Cost accounting system:- It is a framework used by organisation for the purpose of

profitability analysis, control cost and inventory valuation through determine cost of

products. It indicated which products gives profitability or not and it has ascertained

accurate product cost. It helps the management accountant to provided a detailed

information of cost that able to operate business function effectively.

Difference between management accounting and financial accounting

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Basis Management accounting Financial accounting

Objectives To helps the manager of

company in decision making

process through give data on

several matters.

To give financial data to the

external stakeholder.

Time Frame It prepared management

reports in monthly or weekly

basis.

It prepared financial reports in

the accounting period once in a

year.

Information Financial and non-financial Financial information

Parties involved Internal stakeholders Internal and external

stakeholders

P2 Types of management accounting reporting

The company has adopted various types of management accounting reporting that will be

described as follows:-

Inventory management system: It is that type of management system helps the

organisation to maintain its stock on routine basis (Doolin, 2016). It keeps record all the

business transaction and track order, deliveries and sales.

Cost accounting system: The system mainly involves process and order costing that

helps the company in accumulates cost for each job or process. It is adopted by them to

record activities related to manufacturing of products that assist management to take

effective decisions.

Job-costing system:It is a that process which accumulated the data related to cost with

the particular service job. It is useful for the management accountant to ascertaining

company's accuracy that allow them to quote price of a product at reasonable

profitability. The system tracking cost of particular job and manage information that

operate the business effectively.

Price-optimising system: It is that system used by company to predicting the behaviour

of potential customers at various different pricing of products or services (Chenhall and

Moers, 2015). It assists them to ascertain pricing structure such as promotional pricing,

2

Objectives To helps the manager of

company in decision making

process through give data on

several matters.

To give financial data to the

external stakeholder.

Time Frame It prepared management

reports in monthly or weekly

basis.

It prepared financial reports in

the accounting period once in a

year.

Information Financial and non-financial Financial information

Parties involved Internal stakeholders Internal and external

stakeholders

P2 Types of management accounting reporting

The company has adopted various types of management accounting reporting that will be

described as follows:-

Inventory management system: It is that type of management system helps the

organisation to maintain its stock on routine basis (Doolin, 2016). It keeps record all the

business transaction and track order, deliveries and sales.

Cost accounting system: The system mainly involves process and order costing that

helps the company in accumulates cost for each job or process. It is adopted by them to

record activities related to manufacturing of products that assist management to take

effective decisions.

Job-costing system:It is a that process which accumulated the data related to cost with

the particular service job. It is useful for the management accountant to ascertaining

company's accuracy that allow them to quote price of a product at reasonable

profitability. The system tracking cost of particular job and manage information that

operate the business effectively.

Price-optimising system: It is that system used by company to predicting the behaviour

of potential customers at various different pricing of products or services (Chenhall and

Moers, 2015). It assists them to ascertain pricing structure such as promotional pricing,

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

discount pricing and initial pricing. The system is adopted to evaluate the price of

products for various customer segments by together the data about cost as well as

inventory levels.

M1 Benefits of management accounting system and its application within the company

The management accounting system is used by company for some purpose as it provide

various benefits by applying within the organisation. It will be further described as follows:-

Benefits

Maximizing profitability: The system involves budgetary control and capital budgeting

techniques which is used by Company for the purpose of minimizing expenditures

(Houtsma and van Veen, 2015). Thereafter, it also assists firm to minimize their price

through which they will get super profits.

Enhance efficiency: The company adopt management accounting system to take the

promotional decision by finding out deviation through comparison of employee

performance. For this, they motivate the individuals by offer them a reward for its

performance that will increase firm's efficiency.

Application

Keep record: It is applied by company for the purpose of recording business transaction

and ascertaining outcomes of financial changes. It is used to prepared the internal reports

and projecting financial impacts from the future transactions (Choi, 2016).

Decision making: The firm used the management accounting system for take effective

decision related to marketing, pricing and capital investment. The reason for applicability

of this system in a company assist them in evaluating product profitability and formulate

strategies.

CASE 1

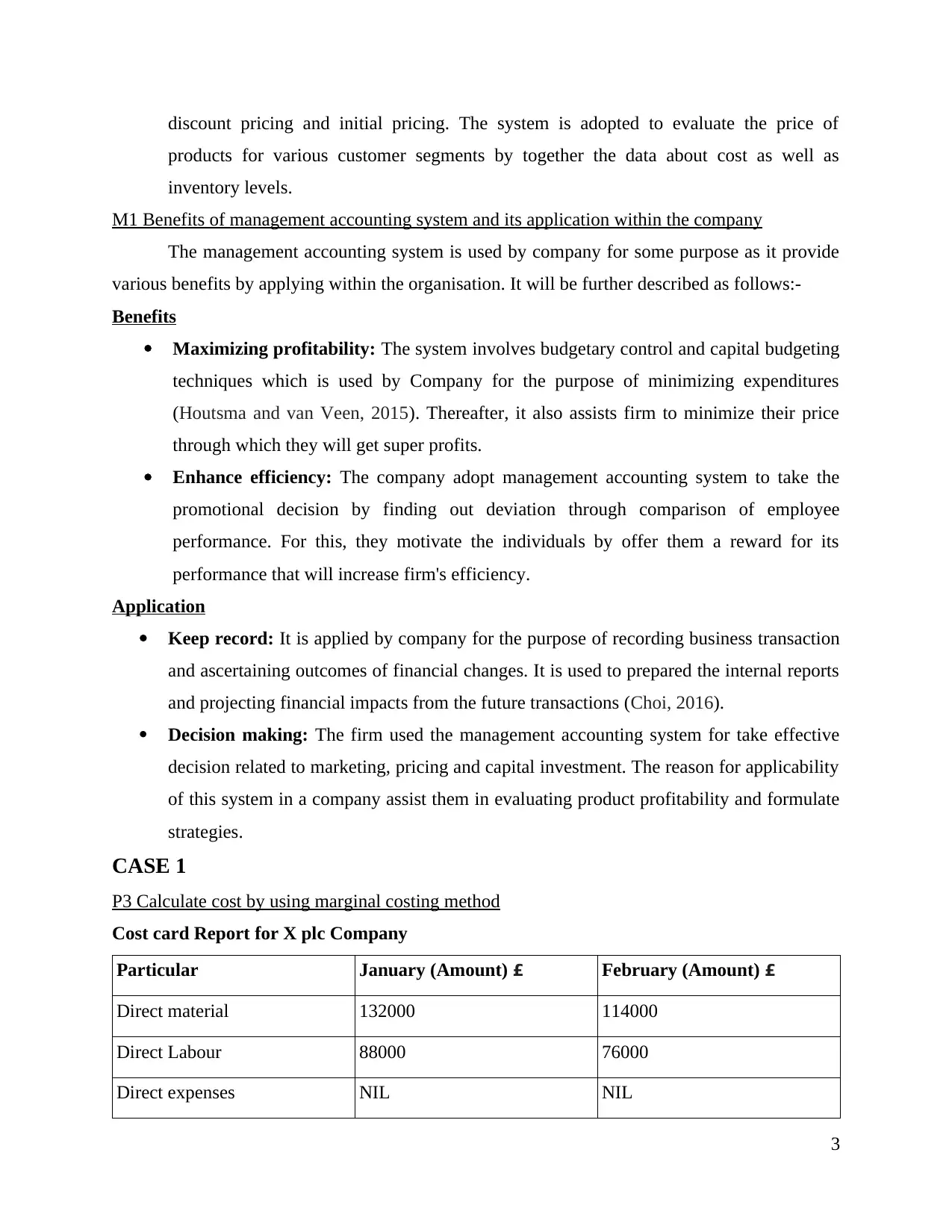

P3 Calculate cost by using marginal costing method

Cost card Report for X plc Company

Particular January (Amount) £ February (Amount) £

Direct material 132000 114000

Direct Labour 88000 76000

Direct expenses NIL NIL

3

products for various customer segments by together the data about cost as well as

inventory levels.

M1 Benefits of management accounting system and its application within the company

The management accounting system is used by company for some purpose as it provide

various benefits by applying within the organisation. It will be further described as follows:-

Benefits

Maximizing profitability: The system involves budgetary control and capital budgeting

techniques which is used by Company for the purpose of minimizing expenditures

(Houtsma and van Veen, 2015). Thereafter, it also assists firm to minimize their price

through which they will get super profits.

Enhance efficiency: The company adopt management accounting system to take the

promotional decision by finding out deviation through comparison of employee

performance. For this, they motivate the individuals by offer them a reward for its

performance that will increase firm's efficiency.

Application

Keep record: It is applied by company for the purpose of recording business transaction

and ascertaining outcomes of financial changes. It is used to prepared the internal reports

and projecting financial impacts from the future transactions (Choi, 2016).

Decision making: The firm used the management accounting system for take effective

decision related to marketing, pricing and capital investment. The reason for applicability

of this system in a company assist them in evaluating product profitability and formulate

strategies.

CASE 1

P3 Calculate cost by using marginal costing method

Cost card Report for X plc Company

Particular January (Amount) £ February (Amount) £

Direct material 132000 114000

Direct Labour 88000 76000

Direct expenses NIL NIL

3

Prime cost 220000 190000

Variable production overhead 55000 47500

Marginal production cost 275000 237500

Fixed production overheads 20000 20000

Total production cost 295000 257500

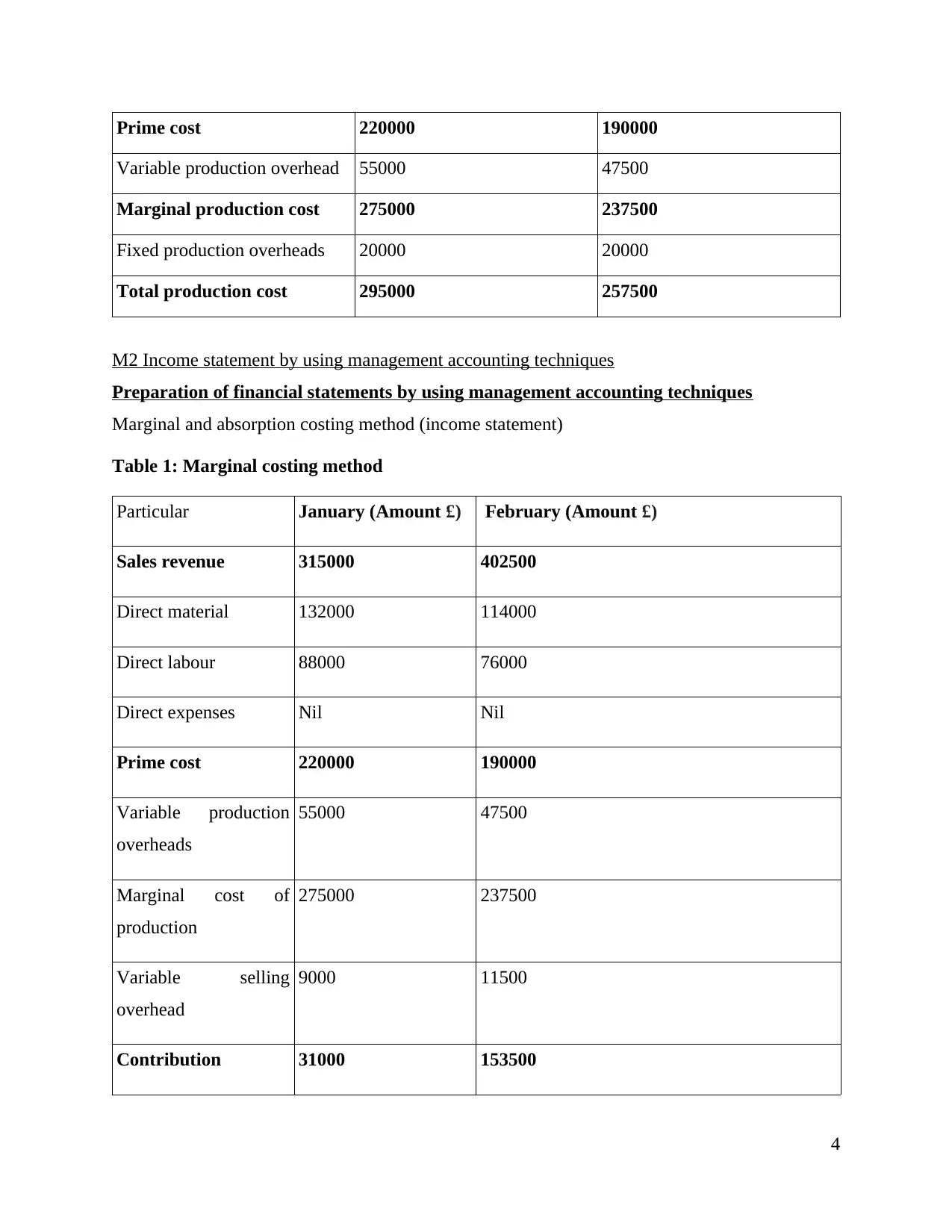

M2 Income statement by using management accounting techniques

Preparation of financial statements by using management accounting techniques

Marginal and absorption costing method (income statement)

Table 1: Marginal costing method

Particular January (Amount £) February (Amount £)

Sales revenue 315000 402500

Direct material 132000 114000

Direct labour 88000 76000

Direct expenses Nil Nil

Prime cost 220000 190000

Variable production

overheads

55000 47500

Marginal cost of

production

275000 237500

Variable selling

overhead

9000 11500

Contribution 31000 153500

4

Variable production overhead 55000 47500

Marginal production cost 275000 237500

Fixed production overheads 20000 20000

Total production cost 295000 257500

M2 Income statement by using management accounting techniques

Preparation of financial statements by using management accounting techniques

Marginal and absorption costing method (income statement)

Table 1: Marginal costing method

Particular January (Amount £) February (Amount £)

Sales revenue 315000 402500

Direct material 132000 114000

Direct labour 88000 76000

Direct expenses Nil Nil

Prime cost 220000 190000

Variable production

overheads

55000 47500

Marginal cost of

production

275000 237500

Variable selling

overhead

9000 11500

Contribution 31000 153500

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less: Fixed production

overheads

20000 20000

Fixed selling overhead 2000 2000

Total profit 9000 131500

Particular January (Amount£) February (Amount£)

Sales 315000 402500

Less:

Direct material

132000 114000

Direct labour 88000 76000

Variable production overhead 55000 47500

Fixed production overhead 20000 76000

Total production cost 295000 313500

Add: Opening stock - 2000

Less: Closing stock (2000) (2000)

COGS 293000 313500

Gross profit 22000 313500

Less:

Variable selling cost

9000 11500

Fixed selling cost 2000 2000

Net profit 11000 300000

5

overheads

20000 20000

Fixed selling overhead 2000 2000

Total profit 9000 131500

Particular January (Amount£) February (Amount£)

Sales 315000 402500

Less:

Direct material

132000 114000

Direct labour 88000 76000

Variable production overhead 55000 47500

Fixed production overhead 20000 76000

Total production cost 295000 313500

Add: Opening stock - 2000

Less: Closing stock (2000) (2000)

COGS 293000 313500

Gross profit 22000 313500

Less:

Variable selling cost

9000 11500

Fixed selling cost 2000 2000

Net profit 11000 300000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D2 Interpretation of financial reports

Marginal costing techniques:- It is that type of management accounting method in

which there is an increase in opportunity cost by producing an additional unit. Therefore, at the

time of determining net profit company charged only variable expenses and fixed cost is already.

From the above income statement has been prepared by marginal costing methods in

which the sales revenues of Xplc for a month January and February is 315000 and 402500

respectively. Therefore, only variable production overhead consider in calculating net profit for

month January and February that is 9000 and 131500 respectively.

Absorption costing techniques:- The method is used to prepare income statement of a

company at the time of calculation net profit. They consider all type of cost incurred in a

business operation for a particular time periods are fixed and variable expenses.

From the above income statement has been prepared by marginal costing methods in

which the sales revenues of Xplc for a month January and February is 315000 and 402500

respectively. Therefore, only variable production overhead consider in calculating net profit for

month January and February that is 11000 and 300000 respectively.

TASK

P4 Explanation on different types of planning tools for budgetary control

Budgeting is a procedure to estimate the expenses and revenues for a particular future

time period on periodic basis. Thereafter, the management accountant of a company adopt

budgetary control technique to set the financial goals with the budgets. It also makes possible

adjustment by comparison among actual and expected results. There are various type of budget

that will be discussed below:- Capital budget:- It is that process adopt by company to take investment decisions by

determining the potential expenses for a particular project. It shows the company to their

possible returns for initial investment in a project to meet the benchmark target (Rowley

and et. al., 2016). It can be possible through investment appraisal technique that involves

Internal rate of return, payback period, Net present value and discounted cash flow etc. It

helps firm to decide that proposal will provide better for its investment funds among

several options.

Advantages

6

Marginal costing techniques:- It is that type of management accounting method in

which there is an increase in opportunity cost by producing an additional unit. Therefore, at the

time of determining net profit company charged only variable expenses and fixed cost is already.

From the above income statement has been prepared by marginal costing methods in

which the sales revenues of Xplc for a month January and February is 315000 and 402500

respectively. Therefore, only variable production overhead consider in calculating net profit for

month January and February that is 9000 and 131500 respectively.

Absorption costing techniques:- The method is used to prepare income statement of a

company at the time of calculation net profit. They consider all type of cost incurred in a

business operation for a particular time periods are fixed and variable expenses.

From the above income statement has been prepared by marginal costing methods in

which the sales revenues of Xplc for a month January and February is 315000 and 402500

respectively. Therefore, only variable production overhead consider in calculating net profit for

month January and February that is 11000 and 300000 respectively.

TASK

P4 Explanation on different types of planning tools for budgetary control

Budgeting is a procedure to estimate the expenses and revenues for a particular future

time period on periodic basis. Thereafter, the management accountant of a company adopt

budgetary control technique to set the financial goals with the budgets. It also makes possible

adjustment by comparison among actual and expected results. There are various type of budget

that will be discussed below:- Capital budget:- It is that process adopt by company to take investment decisions by

determining the potential expenses for a particular project. It shows the company to their

possible returns for initial investment in a project to meet the benchmark target (Rowley

and et. al., 2016). It can be possible through investment appraisal technique that involves

Internal rate of return, payback period, Net present value and discounted cash flow etc. It

helps firm to decide that proposal will provide better for its investment funds among

several options.

Advantages

6

It helps the company to evaluating a new opportunity through estimate future cash

inflows. It assists the firm in controlling capital expenses.

Disadvantages

It is not used by all types of organisation as it needed a huge resource.

It involves high degree of risk Operating budget: It is that type of budget which helps firm to estimate detailed

projection by estimating expenses and revenues. It will be forecasting that is based upon

the sales figure at least on year. It involves budget for manufacturing expenses such as

material, labour and overhead, administration and selling expenses, sales etc. Therefore,

in this budget that includes Direct material budget, production and sales budget etc.

Advantages

The benefit of this budget is that it helps the firm in maintaining current expenses by

determining future cost.

It provides accurate financial information. It helps in saving, planning and investing for unanticipated condition.

Disadvantages

It will generate a lot of behavioural issues (Wu, Hug and Kar, 2015).

It creates difficulty in estimating expenses and revenues in a corporation realistically.

CASE 2

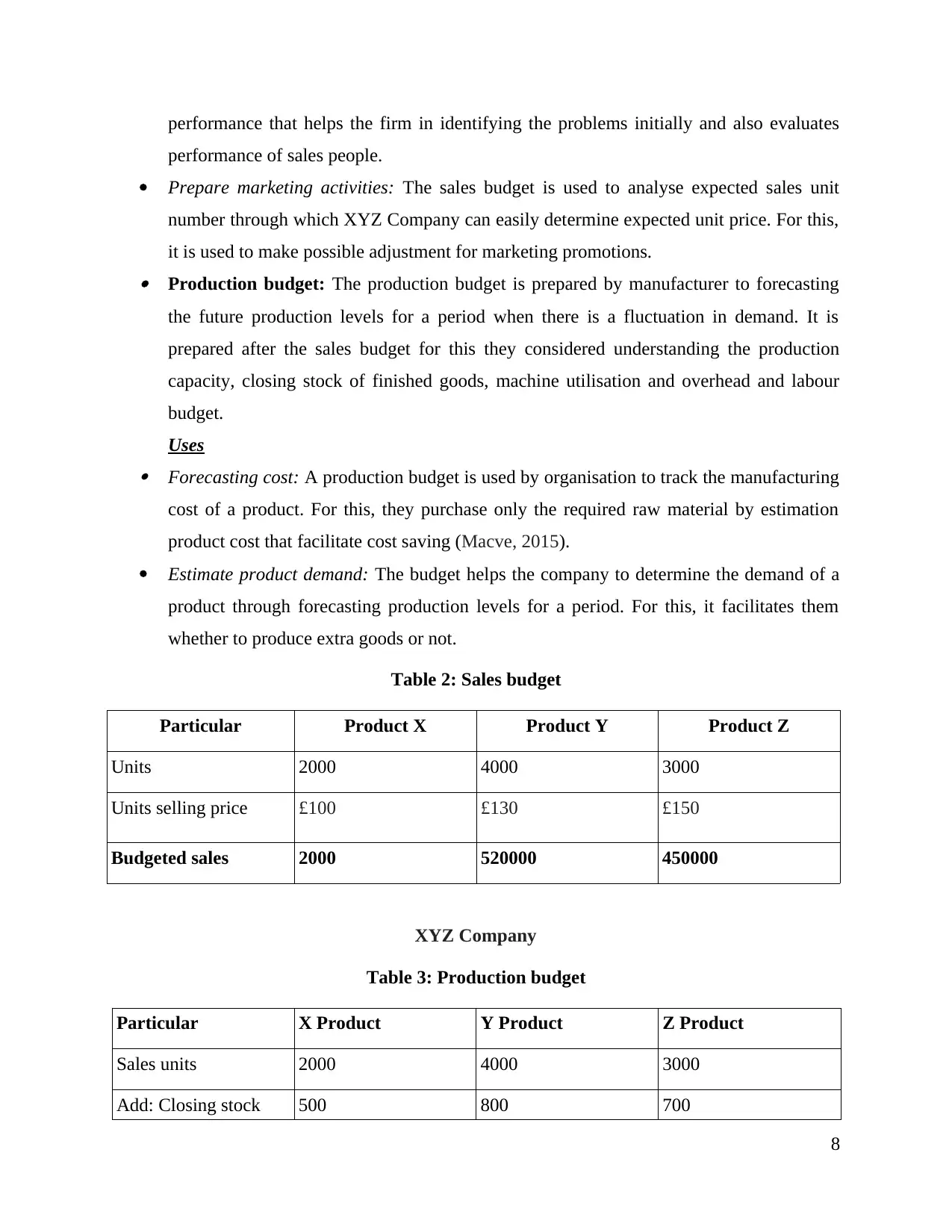

M3 Analyse the use of various planning tools and it application for prepare and forecast budgets

There are various types of planning tools adapt to prepare and forecast budgets that will

be discussed below:- Sales budget: It is that type of planning tool which is used to forecasting the future sales

from the past as well as current sales figures of a XYZ company for a particular time

period. It can be prepared on the basis of availability of raw materials, order in hand, past

sales trend, competition and return on capital employed etc.

Uses Performance: The sales budget is used by company to set their sales goals for the sales

department (Maas, Schaltegger and Crutzen, 2016). It also gives a benchmark for

7

inflows. It assists the firm in controlling capital expenses.

Disadvantages

It is not used by all types of organisation as it needed a huge resource.

It involves high degree of risk Operating budget: It is that type of budget which helps firm to estimate detailed

projection by estimating expenses and revenues. It will be forecasting that is based upon

the sales figure at least on year. It involves budget for manufacturing expenses such as

material, labour and overhead, administration and selling expenses, sales etc. Therefore,

in this budget that includes Direct material budget, production and sales budget etc.

Advantages

The benefit of this budget is that it helps the firm in maintaining current expenses by

determining future cost.

It provides accurate financial information. It helps in saving, planning and investing for unanticipated condition.

Disadvantages

It will generate a lot of behavioural issues (Wu, Hug and Kar, 2015).

It creates difficulty in estimating expenses and revenues in a corporation realistically.

CASE 2

M3 Analyse the use of various planning tools and it application for prepare and forecast budgets

There are various types of planning tools adapt to prepare and forecast budgets that will

be discussed below:- Sales budget: It is that type of planning tool which is used to forecasting the future sales

from the past as well as current sales figures of a XYZ company for a particular time

period. It can be prepared on the basis of availability of raw materials, order in hand, past

sales trend, competition and return on capital employed etc.

Uses Performance: The sales budget is used by company to set their sales goals for the sales

department (Maas, Schaltegger and Crutzen, 2016). It also gives a benchmark for

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

performance that helps the firm in identifying the problems initially and also evaluates

performance of sales people.

Prepare marketing activities: The sales budget is used to analyse expected sales unit

number through which XYZ Company can easily determine expected unit price. For this,

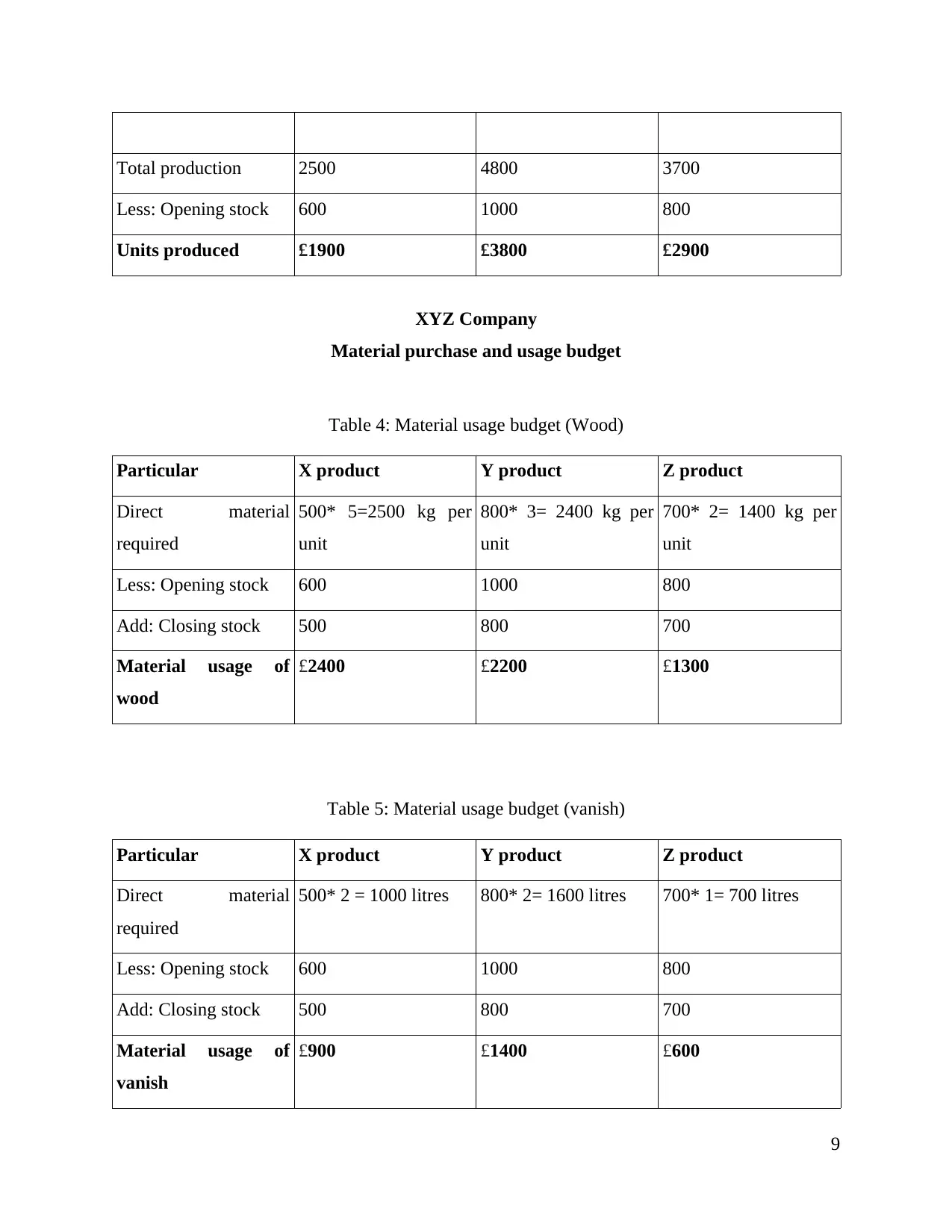

it is used to make possible adjustment for marketing promotions. Production budget: The production budget is prepared by manufacturer to forecasting

the future production levels for a period when there is a fluctuation in demand. It is

prepared after the sales budget for this they considered understanding the production

capacity, closing stock of finished goods, machine utilisation and overhead and labour

budget.

Uses Forecasting cost: A production budget is used by organisation to track the manufacturing

cost of a product. For this, they purchase only the required raw material by estimation

product cost that facilitate cost saving (Macve, 2015).

Estimate product demand: The budget helps the company to determine the demand of a

product through forecasting production levels for a period. For this, it facilitates them

whether to produce extra goods or not.

Table 2: Sales budget

Particular Product X Product Y Product Z

Units 2000 4000 3000

Units selling price £100 £130 £150

Budgeted sales 2000 520000 450000

XYZ Company

Table 3: Production budget

Particular X Product Y Product Z Product

Sales units 2000 4000 3000

Add: Closing stock 500 800 700

8

performance of sales people.

Prepare marketing activities: The sales budget is used to analyse expected sales unit

number through which XYZ Company can easily determine expected unit price. For this,

it is used to make possible adjustment for marketing promotions. Production budget: The production budget is prepared by manufacturer to forecasting

the future production levels for a period when there is a fluctuation in demand. It is

prepared after the sales budget for this they considered understanding the production

capacity, closing stock of finished goods, machine utilisation and overhead and labour

budget.

Uses Forecasting cost: A production budget is used by organisation to track the manufacturing

cost of a product. For this, they purchase only the required raw material by estimation

product cost that facilitate cost saving (Macve, 2015).

Estimate product demand: The budget helps the company to determine the demand of a

product through forecasting production levels for a period. For this, it facilitates them

whether to produce extra goods or not.

Table 2: Sales budget

Particular Product X Product Y Product Z

Units 2000 4000 3000

Units selling price £100 £130 £150

Budgeted sales 2000 520000 450000

XYZ Company

Table 3: Production budget

Particular X Product Y Product Z Product

Sales units 2000 4000 3000

Add: Closing stock 500 800 700

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total production 2500 4800 3700

Less: Opening stock 600 1000 800

Units produced £1900 £3800 £2900

XYZ Company

Material purchase and usage budget

Table 4: Material usage budget (Wood)

Particular X product Y product Z product

Direct material

required

500* 5=2500 kg per

unit

800* 3= 2400 kg per

unit

700* 2= 1400 kg per

unit

Less: Opening stock 600 1000 800

Add: Closing stock 500 800 700

Material usage of

wood

£2400 £2200 £1300

Table 5: Material usage budget (vanish)

Particular X product Y product Z product

Direct material

required

500* 2 = 1000 litres 800* 2= 1600 litres 700* 1= 700 litres

Less: Opening stock 600 1000 800

Add: Closing stock 500 800 700

Material usage of

vanish

£900 £1400 £600

9

Less: Opening stock 600 1000 800

Units produced £1900 £3800 £2900

XYZ Company

Material purchase and usage budget

Table 4: Material usage budget (Wood)

Particular X product Y product Z product

Direct material

required

500* 5=2500 kg per

unit

800* 3= 2400 kg per

unit

700* 2= 1400 kg per

unit

Less: Opening stock 600 1000 800

Add: Closing stock 500 800 700

Material usage of

wood

£2400 £2200 £1300

Table 5: Material usage budget (vanish)

Particular X product Y product Z product

Direct material

required

500* 2 = 1000 litres 800* 2= 1600 litres 700* 1= 700 litres

Less: Opening stock 600 1000 800

Add: Closing stock 500 800 700

Material usage of

vanish

£900 £1400 £600

9

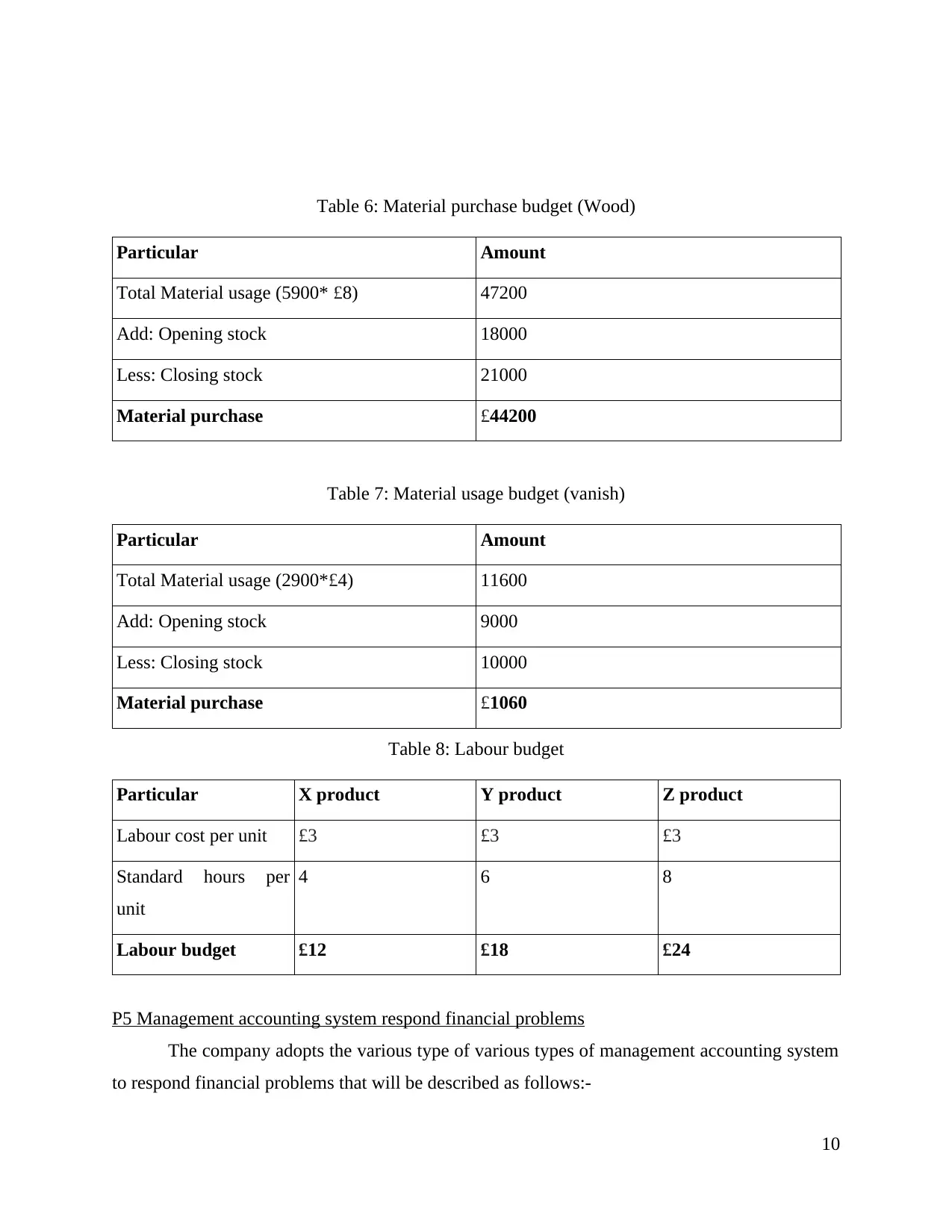

Table 6: Material purchase budget (Wood)

Particular Amount

Total Material usage (5900* £8) 47200

Add: Opening stock 18000

Less: Closing stock 21000

Material purchase £44200

Table 7: Material usage budget (vanish)

Particular Amount

Total Material usage (2900*£4) 11600

Add: Opening stock 9000

Less: Closing stock 10000

Material purchase £1060

Table 8: Labour budget

Particular X product Y product Z product

Labour cost per unit £3 £3 £3

Standard hours per

unit

4 6 8

Labour budget £12 £18 £24

P5 Management accounting system respond financial problems

The company adopts the various type of various types of management accounting system

to respond financial problems that will be described as follows:-

10

Particular Amount

Total Material usage (5900* £8) 47200

Add: Opening stock 18000

Less: Closing stock 21000

Material purchase £44200

Table 7: Material usage budget (vanish)

Particular Amount

Total Material usage (2900*£4) 11600

Add: Opening stock 9000

Less: Closing stock 10000

Material purchase £1060

Table 8: Labour budget

Particular X product Y product Z product

Labour cost per unit £3 £3 £3

Standard hours per

unit

4 6 8

Labour budget £12 £18 £24

P5 Management accounting system respond financial problems

The company adopts the various type of various types of management accounting system

to respond financial problems that will be described as follows:-

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.