Analysis of Management Accounting System and Its Application

VerifiedAdded on 2021/02/21

|16

|4535

|27

Report

AI Summary

This report provides a comprehensive overview of management accounting systems and their applications within the context of ABC Ltd., a manufacturing company. It explores the requirements of different management accounting systems, including cost accounting, inventory management, and job costing. The report details various management accounting reports, such as budget reports, account receivable aging reports, and performance reports, highlighting their benefits in decision-making and organizational control. It further analyzes the integration of management accounting systems and reports, emphasizing their role in providing crucial information for internal users. The report also delves into different costing methods, comparing marginal and absorption costing, and analyzes various planning tools used in budgetary control, forecasting, and budget preparation. Finally, the report discusses the adaptation of management accounting systems to address financial problems and strategies that can lead to organizational success, including the use of tools like the balance scorecard and benchmarking.

MANAGEMENT

ACCOUNTING SYSTEM AND ITS

APPLICATION

ACCOUNTING SYSTEM AND ITS

APPLICATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1 ...........................................................................................................................................1

1. Management accounting system and requirements of different types of management

accounting system........................................................................................................................1

2. Different management accounting reports...............................................................................2

3. Benefits of management accounting system and their application with context of

organisation..................................................................................................................................3

4. Integration of managements accounting system and management accounting reports...........3

TASK 2............................................................................................................................................3

TASK 3............................................................................................................................................3

1. Advantages and disadvantages of different planning tools uses in the budgetary control......3

2. Analysing use of panning tools and their application for for casting and preparation of the

budgets.........................................................................................................................................5

TASK 4............................................................................................................................................6

1. Adaption of management accounting system in order to respond to the financial problems.. 6

And also Analysing the way through which organisation can leas to success by responding to

the financial problems..................................................................................................................6

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

TASK 1 ...........................................................................................................................................1

1. Management accounting system and requirements of different types of management

accounting system........................................................................................................................1

2. Different management accounting reports...............................................................................2

3. Benefits of management accounting system and their application with context of

organisation..................................................................................................................................3

4. Integration of managements accounting system and management accounting reports...........3

TASK 2............................................................................................................................................3

TASK 3............................................................................................................................................3

1. Advantages and disadvantages of different planning tools uses in the budgetary control......3

2. Analysing use of panning tools and their application for for casting and preparation of the

budgets.........................................................................................................................................5

TASK 4............................................................................................................................................6

1. Adaption of management accounting system in order to respond to the financial problems.. 6

And also Analysing the way through which organisation can leas to success by responding to

the financial problems..................................................................................................................6

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Management accounting system is the process of analysing the cost of business

operations, in order to prepare the financial reports and records which aid manges in decision

making which leads to the achievement of organisational goals and objectives.

the present study is based on the ABC Ltd. Company which exist in manufacturing industry

deals in production of goods and services. This is the medium sized enterprise.

The report will explain about the requirement of management accounting system and

management accounting reports which helps the internal uses in generation of essential

information which aids in decision making. The report will also explain about different

techniques of costing which generate and provide reasons for difference in the net profit of the

company.

Furthermore, the report will explain about different planing tools which can be used by

the company to forecast the budget. In addition to this some of the tools including balance score

card, benchmarking will also be explained for understanding of the tools which helps in solving

the financial problems .

TASK 1

1. Management accounting system and requirements of different types of management

accounting system

Management accounting system is the internal system of the organisation which helps

them in measuring and evaluating their processes (Kaplan and Atkinson,, 2015). This is

considered to be the process of preparing of the management reports and also the accounts which

can further help its users in making effective and efficient decision by using the financial

information generated by reports (Management Accounting – Meaning, Advantages &

Functions. 2018). These reports helps in generating in formation related to finial and statistical

data which helps mangers in making long term and short term decisions.

Management accounting is also called as managerial accounting and the cost accounting.

This is considered to be the process of analysing the cot of business operations, in order to

prepare the financial reports and records which aid manges in decision making which leads to the

achievement of organisational goals and objectives(Renz, 2016).

1

Management accounting system is the process of analysing the cost of business

operations, in order to prepare the financial reports and records which aid manges in decision

making which leads to the achievement of organisational goals and objectives.

the present study is based on the ABC Ltd. Company which exist in manufacturing industry

deals in production of goods and services. This is the medium sized enterprise.

The report will explain about the requirement of management accounting system and

management accounting reports which helps the internal uses in generation of essential

information which aids in decision making. The report will also explain about different

techniques of costing which generate and provide reasons for difference in the net profit of the

company.

Furthermore, the report will explain about different planing tools which can be used by

the company to forecast the budget. In addition to this some of the tools including balance score

card, benchmarking will also be explained for understanding of the tools which helps in solving

the financial problems .

TASK 1

1. Management accounting system and requirements of different types of management

accounting system

Management accounting system is the internal system of the organisation which helps

them in measuring and evaluating their processes (Kaplan and Atkinson,, 2015). This is

considered to be the process of preparing of the management reports and also the accounts which

can further help its users in making effective and efficient decision by using the financial

information generated by reports (Management Accounting – Meaning, Advantages &

Functions. 2018). These reports helps in generating in formation related to finial and statistical

data which helps mangers in making long term and short term decisions.

Management accounting is also called as managerial accounting and the cost accounting.

This is considered to be the process of analysing the cot of business operations, in order to

prepare the financial reports and records which aid manges in decision making which leads to the

achievement of organisational goals and objectives(Renz, 2016).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting plays essential role for the mangers of ABC Ltd. for

implementing their functions of planning, organising,controlling and the decision making . Their

aim is to provide the support decision making by mangers by collecting , processing and

communicating the important information to the Internal users as these will aid them in their

decision making efficiently .

There are different types of management accounting system which helps the business

and managers in generating different information based on the requirements and needs of the

management(Maas, Schaltegger and Crutzen, 2017) .

Some types of management accounting system are as follows:

Cost accounting system

This is also called the costing system or product costing which is the framework used by

the firms in order to estimate the cost of the products for analysing their profitability, cost control

and also for the inventory valuation. ABC Ltd. Use cost accounting system so that it helps them

in ascertaining the cost of every activity in which they need to incur expenses in order to

accomplish their activies and generating income.

Inventory management system

Inventory term is generally used to represent the stock, material, goods .Inventory

management system leads to the combination of the use of desktop software, barcode printers,

barcode scanners and also the mobile devices in order to streamline the management of the

inventory(Quattrone, 2016). This system also helpful for ABC Ltd. in tracking of the goods that

is receiving and shipping of the goods. This helps in controlling the inventory and also to

ascertain the current levels of the inventory which resulting in automatically reduction in under

stock and overstock situations. There are different method of this system which includes LIFO

and FIOFO method.

LIFO is the management system which focuses on selling of the inventory which produced in the

last and the fresh stock is being sold by the company in order to attract more customers.

FIFO is the inventory management system which focuses on selling of the product which

produces initially that is which ABC Ltd .have produced first are required to be sell first in order

to remove the older stock.

Job costing system

2

implementing their functions of planning, organising,controlling and the decision making . Their

aim is to provide the support decision making by mangers by collecting , processing and

communicating the important information to the Internal users as these will aid them in their

decision making efficiently .

There are different types of management accounting system which helps the business

and managers in generating different information based on the requirements and needs of the

management(Maas, Schaltegger and Crutzen, 2017) .

Some types of management accounting system are as follows:

Cost accounting system

This is also called the costing system or product costing which is the framework used by

the firms in order to estimate the cost of the products for analysing their profitability, cost control

and also for the inventory valuation. ABC Ltd. Use cost accounting system so that it helps them

in ascertaining the cost of every activity in which they need to incur expenses in order to

accomplish their activies and generating income.

Inventory management system

Inventory term is generally used to represent the stock, material, goods .Inventory

management system leads to the combination of the use of desktop software, barcode printers,

barcode scanners and also the mobile devices in order to streamline the management of the

inventory(Quattrone, 2016). This system also helpful for ABC Ltd. in tracking of the goods that

is receiving and shipping of the goods. This helps in controlling the inventory and also to

ascertain the current levels of the inventory which resulting in automatically reduction in under

stock and overstock situations. There are different method of this system which includes LIFO

and FIOFO method.

LIFO is the management system which focuses on selling of the inventory which produced in the

last and the fresh stock is being sold by the company in order to attract more customers.

FIFO is the inventory management system which focuses on selling of the product which

produces initially that is which ABC Ltd .have produced first are required to be sell first in order

to remove the older stock.

Job costing system

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This is the system which involve the process of the accumulating the information

regarding the cost associated with each product or each job( Hopper and Bui, 2016). This will

help ABC Ltd. In ascertaining the products which are profitable and need to expand and also

which are not profitable so that accordingly decisions can be made regarding the expansion of

the products .

2. Different management accounting reports

Management accounting reports focuses on receiving the data through using the financial

accounting . These reports generally helps in planning, controlling and decision making

regarding the organisation (Chenhall and Moers, 2015). There are different types of reports

which helps in providing different information related to their field. Some of the reports are as

follows;

Budget reports

These reports are the reports which helps the business in measuring the actual

performance with the planned performance ion order to take corrective measures to eliminate the

deviations if occurred. Budget reports helps and guide the business activities to move in the

direction of achieving the organisational goal(Ax and Greve, 2017). These reports also helps in

controlling of the activities and costs of the ABC Ltd. which leads in improving profitability and

increasing profits of the company.

Account receivable ageing reports

These are the reports which are made by the ABC Ltd. In case where they relies on

extending credit these reports helps in ascertaining the defaulters by breaking down the

remaining balance of the clients into specific time periods (van Helden and Uddin, 2016) . This

also helps in finding the issues in the company's collection process. These reports helps the

company in tightening the credit policies if they showing more defaulters.

Performance reports

ABC Ltd. Prepare these reports from reviewing the performance of the company .

Performance reports for each department is also made so that efficient management of activities

can be done and helps the company in directing the activities of employees towards achievement

of organisational goal . Performance reports helps in ascertaining, reviewing and controlling the

performances of organisation as whole(Shields, 2015). these reports helps the mangers in

3

regarding the cost associated with each product or each job( Hopper and Bui, 2016). This will

help ABC Ltd. In ascertaining the products which are profitable and need to expand and also

which are not profitable so that accordingly decisions can be made regarding the expansion of

the products .

2. Different management accounting reports

Management accounting reports focuses on receiving the data through using the financial

accounting . These reports generally helps in planning, controlling and decision making

regarding the organisation (Chenhall and Moers, 2015). There are different types of reports

which helps in providing different information related to their field. Some of the reports are as

follows;

Budget reports

These reports are the reports which helps the business in measuring the actual

performance with the planned performance ion order to take corrective measures to eliminate the

deviations if occurred. Budget reports helps and guide the business activities to move in the

direction of achieving the organisational goal(Ax and Greve, 2017). These reports also helps in

controlling of the activities and costs of the ABC Ltd. which leads in improving profitability and

increasing profits of the company.

Account receivable ageing reports

These are the reports which are made by the ABC Ltd. In case where they relies on

extending credit these reports helps in ascertaining the defaulters by breaking down the

remaining balance of the clients into specific time periods (van Helden and Uddin, 2016) . This

also helps in finding the issues in the company's collection process. These reports helps the

company in tightening the credit policies if they showing more defaulters.

Performance reports

ABC Ltd. Prepare these reports from reviewing the performance of the company .

Performance reports for each department is also made so that efficient management of activities

can be done and helps the company in directing the activities of employees towards achievement

of organisational goal . Performance reports helps in ascertaining, reviewing and controlling the

performances of organisation as whole(Shields, 2015). these reports helps the mangers in

3

making strategic decisions and also to award the employees for their commitment in the

organisation.

3. Benefits of management accounting system and their application with context of organisation

Management accounting system helps the ABC Ltd. In different ways for fulfilling

different objectives. This systems helps the mangers in accumulating the cost of each job which

helps them in ascertaining the difference of job which is profitable or which is not in order to

decide whether to continue with the job or not (Honggowati and et.al., 2017). This system also

helps in ascertaining the cost of products, controlling cost, tracking of inventory,minimising

costs, improving profitability and also in optimum utilisation of all the resources.

Management accounting system, leads ABC Ltd. in obtaining the essential information

which can used by the internal users which aids them in decision making which lead in

achievement of organisational goals effectively and efficiently.

4. Integration of managements accounting system and management accounting reports

Management accounting system of ABC Ltd. helps in generation of the useful

information which is then presented in form of reports that is management accounting reports in

summarised form which clearly show the results of activities of organisation(Christ and Burritt,

2017). This enables the mangers in planing, decision making and controlling their further

activities, these reports are communicated to the internal users for aiding decision making and

also for achievement of the organisational goals effectively and efficiently.

TASK 2

Income statement by applying marginal and absorption cost

There are different kinds of costing methods which are discussed below:

Marginal costing :

It is a technique of costing in which only variable cost is charged to unit cost of

production. It does not consider fixed costs for the period and is entirely written off against the

contribution.

Absorption costing :

It is costing technique in which both variable and fixed costs are charged to the unit cost

of production. This means that it takes direct and indirect expenses into account for calculating

the unit price of a product.

4

organisation.

3. Benefits of management accounting system and their application with context of organisation

Management accounting system helps the ABC Ltd. In different ways for fulfilling

different objectives. This systems helps the mangers in accumulating the cost of each job which

helps them in ascertaining the difference of job which is profitable or which is not in order to

decide whether to continue with the job or not (Honggowati and et.al., 2017). This system also

helps in ascertaining the cost of products, controlling cost, tracking of inventory,minimising

costs, improving profitability and also in optimum utilisation of all the resources.

Management accounting system, leads ABC Ltd. in obtaining the essential information

which can used by the internal users which aids them in decision making which lead in

achievement of organisational goals effectively and efficiently.

4. Integration of managements accounting system and management accounting reports

Management accounting system of ABC Ltd. helps in generation of the useful

information which is then presented in form of reports that is management accounting reports in

summarised form which clearly show the results of activities of organisation(Christ and Burritt,

2017). This enables the mangers in planing, decision making and controlling their further

activities, these reports are communicated to the internal users for aiding decision making and

also for achievement of the organisational goals effectively and efficiently.

TASK 2

Income statement by applying marginal and absorption cost

There are different kinds of costing methods which are discussed below:

Marginal costing :

It is a technique of costing in which only variable cost is charged to unit cost of

production. It does not consider fixed costs for the period and is entirely written off against the

contribution.

Absorption costing :

It is costing technique in which both variable and fixed costs are charged to the unit cost

of production. This means that it takes direct and indirect expenses into account for calculating

the unit price of a product.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

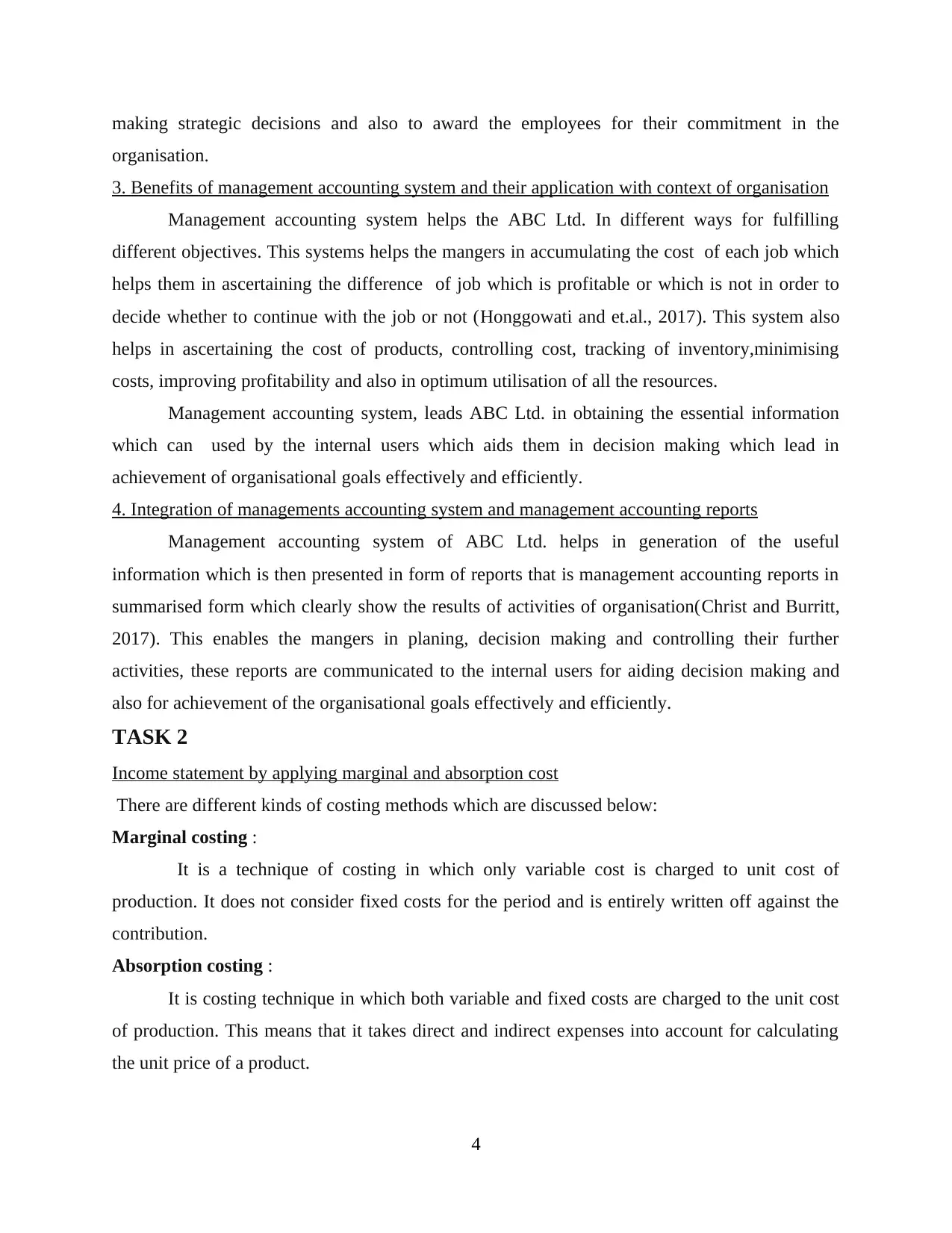

Cost of production (Marginal method)

Direct material 10

Direct labour 20

Variable production overhead 5

Per unit production cost 35

Total production cost :

Marginal costing :

Total units produced = 19000

Unit per cost = 35

Total cost of production = 665000

Cost of production (Absorption method)

Direct material 10

Direct labour 20

Variable production overhead 5

Production overhead 100000/19000

Per unit production cost 40.26

Total production cost:

Total units produced = 19000

Unit per cost = 40.26

Total cost of production = 764940

Total cost of sales for June month.

Absorption method

Opening stock 0

Add: purchases 18000 40.26 724680

Less: closing stock 2000 40.26 80520

Cost of Goods sold 805200

Marginal Method

Opening stock 0

Add: purchases 19000 35 665000

Less: closing stock 2000 35 70000

Cost of Goods sold 735000

Income statement for the month of June

5

Direct material 10

Direct labour 20

Variable production overhead 5

Per unit production cost 35

Total production cost :

Marginal costing :

Total units produced = 19000

Unit per cost = 35

Total cost of production = 665000

Cost of production (Absorption method)

Direct material 10

Direct labour 20

Variable production overhead 5

Production overhead 100000/19000

Per unit production cost 40.26

Total production cost:

Total units produced = 19000

Unit per cost = 40.26

Total cost of production = 764940

Total cost of sales for June month.

Absorption method

Opening stock 0

Add: purchases 18000 40.26 724680

Less: closing stock 2000 40.26 80520

Cost of Goods sold 805200

Marginal Method

Opening stock 0

Add: purchases 19000 35 665000

Less: closing stock 2000 35 70000

Cost of Goods sold 735000

Income statement for the month of June

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

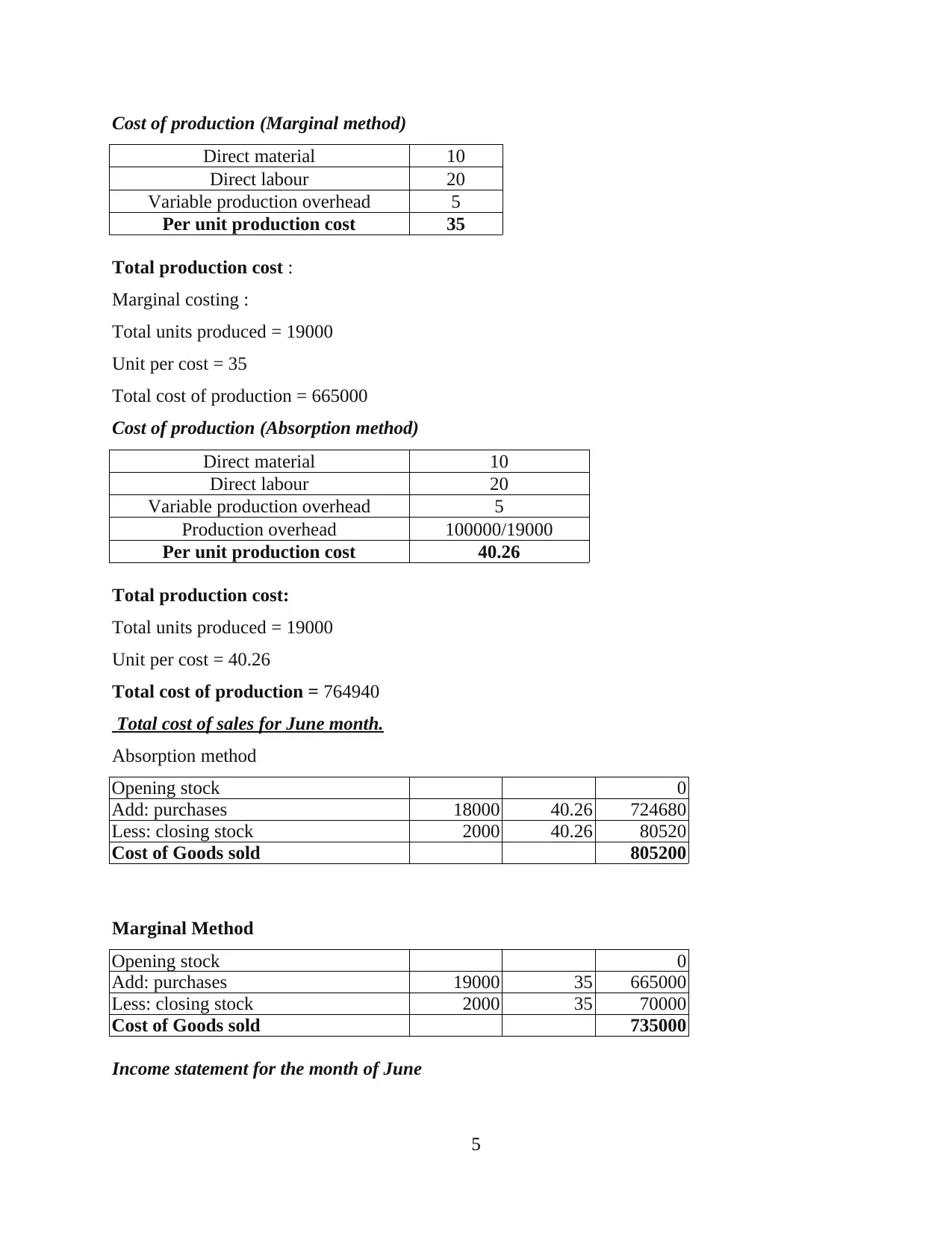

(Absorption costing)

Particulars

Sales 16000 50 800000

Less: COGS

Opening stock

Add: production 18000 35 630000

Less: closing stock 2000 35 70000 560000

GP/ NP 240000

(Marginal costing )

Particulars

Sales 16000 50 0 800000

Less: COGS

Opening stock

Add: purchases 18000 35 630000

Less: closing stock 2000 35 70000 560000

Contribution 240000

Less: fixed 100000

Net profit 140000

Difference Profit and loss statement for June

(For absorption cost)

Particulars

Sales 16000 50 800000

Less: COGS

Opening stock

6

Particulars

Sales 16000 50 800000

Less: COGS

Opening stock

Add: production 18000 35 630000

Less: closing stock 2000 35 70000 560000

GP/ NP 240000

(Marginal costing )

Particulars

Sales 16000 50 0 800000

Less: COGS

Opening stock

Add: purchases 18000 35 630000

Less: closing stock 2000 35 70000 560000

Contribution 240000

Less: fixed 100000

Net profit 140000

Difference Profit and loss statement for June

(For absorption cost)

Particulars

Sales 16000 50 800000

Less: COGS

Opening stock

6

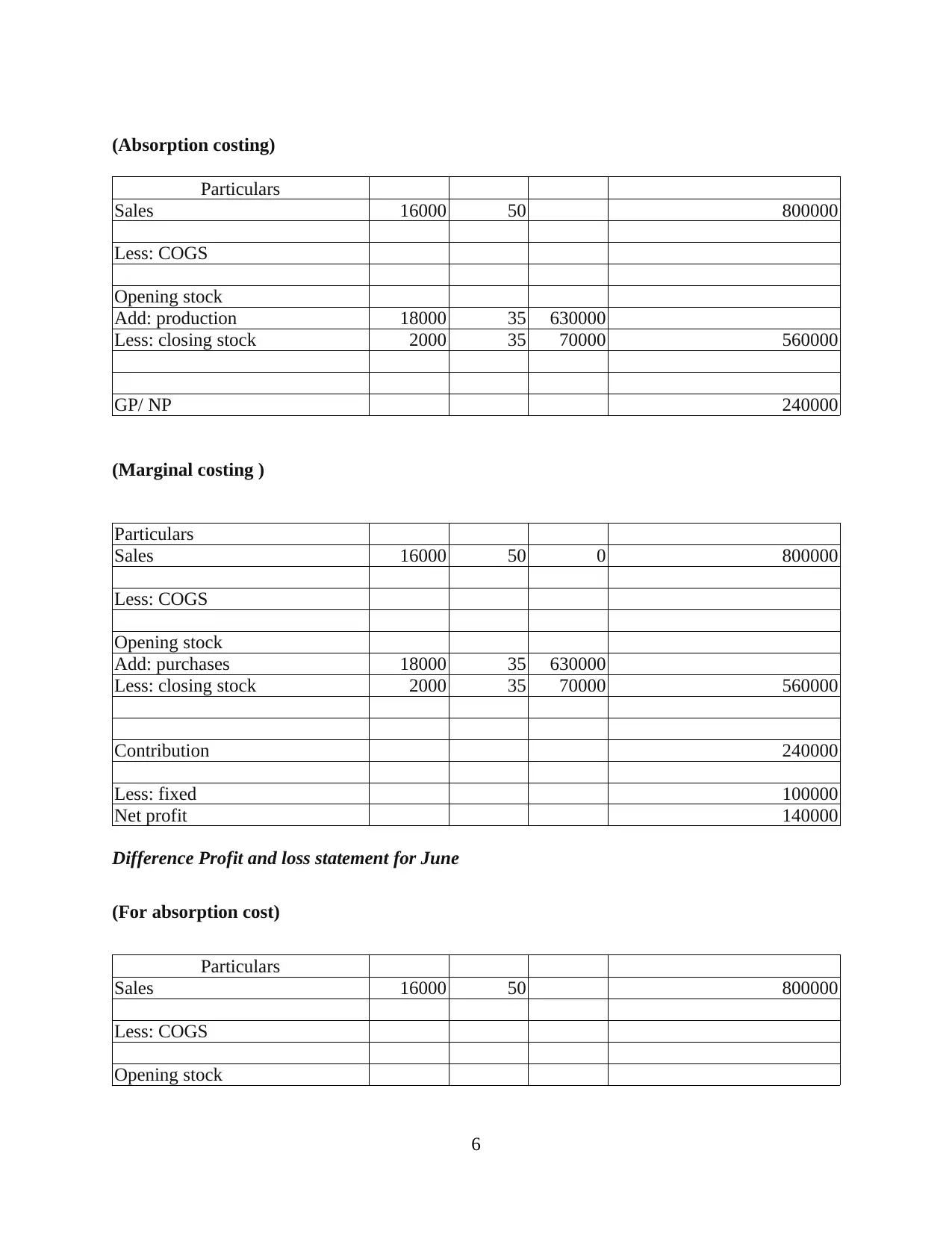

Add: production 19000 35 665000

Less: closing stock 3000 35 105000 560000

GP/ NP 240000

(marginal cost)

Particulars

Sales 16000 50 800000

Less: COGS

Opening stock

Add: production 19000 35 665000

Less: closing stock 3000 35 105000 560000

GP/ NP 240000

Advising company to employ other technique :

Job costing could be applied by the organisation in which costs for each job would be

collected and allotted on a project separately. This technique is preferable because job costing

facilitates managers the benefit of being able to keep record of teams and individuals

performance in the form of efficiency, cost-control and productivity.

TASK 3

1. Advantages and disadvantages of different planning tools uses in the budgetary control

There are many different types of planning tools available which can be used by ABC

Ltd. For effective and efficient planning of their business activities in order to direct all the

activities in direction of achievement of organisational goals. Some of the planning tools are

explained as follows;

Zero base budgeting

this is the method of budgeting which includes the preparation of the budget from the

zero base or the fresh evaluation of each of the item included in budget. There is no or zero base

7

Less: closing stock 3000 35 105000 560000

GP/ NP 240000

(marginal cost)

Particulars

Sales 16000 50 800000

Less: COGS

Opening stock

Add: production 19000 35 665000

Less: closing stock 3000 35 105000 560000

GP/ NP 240000

Advising company to employ other technique :

Job costing could be applied by the organisation in which costs for each job would be

collected and allotted on a project separately. This technique is preferable because job costing

facilitates managers the benefit of being able to keep record of teams and individuals

performance in the form of efficiency, cost-control and productivity.

TASK 3

1. Advantages and disadvantages of different planning tools uses in the budgetary control

There are many different types of planning tools available which can be used by ABC

Ltd. For effective and efficient planning of their business activities in order to direct all the

activities in direction of achievement of organisational goals. Some of the planning tools are

explained as follows;

Zero base budgeting

this is the method of budgeting which includes the preparation of the budget from the

zero base or the fresh evaluation of each of the item included in budget. There is no or zero base

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

while preparation of the zero base budgets (Coad, Jack and Kholeif, 2015). This approach

basically drive the manges in finding the cost effective techniques to the improve the activities.

Advantages

It helps the managers in justifying all the operating expenses.

It leads to keep legacy expenses in check

It helps in efficient allocation of the resources It drive the managers in finding the cost er effective techniques and ways in order to

improve the activities(Englund and Gerdin, 2018).

Disadvantages

It can leads to rewards short term thinking

Time consuming method as mangers needs to start with zero base

It requires manpower for justifying all the expenses It is necessary to have special knowledge regarding preparation of zero base budget(Van

der Stede, 2017)

Operating budget

Operating budget is the budget which includes all the cost associated on operation of the

business. It helps the mangers in describing the activities which are highly capable of generating

the income which includes production, sales, inventory finished goods(Kaplan and Atkinson,,

2015). This operating budget helps the management in preparation of the income statements and

ascertaining the operating profit.

Advantages

It helps the management in managing the current expenses of the company.

Operating budget lead to forecast and estimate the future expenses

it helps in building of the financial reserves(Renz, 2016) It provides benefits to the company by increasing accountability.

Disadvantages

It is time consuming process as it required to accumulate the cost of all the activities of

production

It requires special knowledge to prepare the operational budget

it leads to inflexible in decision making(Maas, Schaltegger and Crutzen, 2017)

8

basically drive the manges in finding the cost effective techniques to the improve the activities.

Advantages

It helps the managers in justifying all the operating expenses.

It leads to keep legacy expenses in check

It helps in efficient allocation of the resources It drive the managers in finding the cost er effective techniques and ways in order to

improve the activities(Englund and Gerdin, 2018).

Disadvantages

It can leads to rewards short term thinking

Time consuming method as mangers needs to start with zero base

It requires manpower for justifying all the expenses It is necessary to have special knowledge regarding preparation of zero base budget(Van

der Stede, 2017)

Operating budget

Operating budget is the budget which includes all the cost associated on operation of the

business. It helps the mangers in describing the activities which are highly capable of generating

the income which includes production, sales, inventory finished goods(Kaplan and Atkinson,,

2015). This operating budget helps the management in preparation of the income statements and

ascertaining the operating profit.

Advantages

It helps the management in managing the current expenses of the company.

Operating budget lead to forecast and estimate the future expenses

it helps in building of the financial reserves(Renz, 2016) It provides benefits to the company by increasing accountability.

Disadvantages

It is time consuming process as it required to accumulate the cost of all the activities of

production

It requires special knowledge to prepare the operational budget

it leads to inflexible in decision making(Maas, Schaltegger and Crutzen, 2017)

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Requirement of Experience manager in order to introduce the budgetary slack

Incremental budget

It is the budget which is prepared on the basis of the previous year's budget or the actual

performance for basis with the incremental amounts which are added for the new budget period.

This basically includes allocation of resources on basis of the allocation of the previous year.

Advantages

It is simple to understand and prepare as this is based on recent financial results of the

company and hence recent budget can easily be verified.

It ensures the funding stability as programmes requires the funding form many years to

achieve the objective and incremental budget is considered to be the structure which

ensures that fund ned to keep flowing towards the program(Quattrone, 2016). this also ensure that all department operate in consistent and the stable manner for the

longer term.

Disadvantages

This budget is considered to be incremental in nature that it only assumes and consider

the minor changes from previous period .

It fosters the overspending ( Hopper and Bui, 2016)

It perpetuates the allocation of resources as according to the previous year itself.

2. Analysing use of panning tools and their application for for casting and preparation of the

budgets

Incremental budget, operational budget, cash budget, sales budget, fixed and flexible

budget, Zero based budget, activity cost budgeting are some of the planning tools which are used

by the ABC Ltd. In order to preparation of the budget based on previous year or no base

depending on the tool which they are using.

These budgets helps them in accumulating the cost and income of the activities in their

organisation and will leads the company to make comparison between the actual performance

and the protected performance(Chenhall and Moers, 2015). This comparison is done in order to

take the corrective actions to eliminate the deviation if occurred between both the performances.

9

Incremental budget

It is the budget which is prepared on the basis of the previous year's budget or the actual

performance for basis with the incremental amounts which are added for the new budget period.

This basically includes allocation of resources on basis of the allocation of the previous year.

Advantages

It is simple to understand and prepare as this is based on recent financial results of the

company and hence recent budget can easily be verified.

It ensures the funding stability as programmes requires the funding form many years to

achieve the objective and incremental budget is considered to be the structure which

ensures that fund ned to keep flowing towards the program(Quattrone, 2016). this also ensure that all department operate in consistent and the stable manner for the

longer term.

Disadvantages

This budget is considered to be incremental in nature that it only assumes and consider

the minor changes from previous period .

It fosters the overspending ( Hopper and Bui, 2016)

It perpetuates the allocation of resources as according to the previous year itself.

2. Analysing use of panning tools and their application for for casting and preparation of the

budgets

Incremental budget, operational budget, cash budget, sales budget, fixed and flexible

budget, Zero based budget, activity cost budgeting are some of the planning tools which are used

by the ABC Ltd. In order to preparation of the budget based on previous year or no base

depending on the tool which they are using.

These budgets helps them in accumulating the cost and income of the activities in their

organisation and will leads the company to make comparison between the actual performance

and the protected performance(Chenhall and Moers, 2015). This comparison is done in order to

take the corrective actions to eliminate the deviation if occurred between both the performances.

9

This helps the organisation in achievement of organisational goals and objectives

effectively and efficiently and also to direct all the activities of the organisation towards the path

of achieving organisational goals efficiently.

Planning tools are applied in ABC Ltd. For forecasting and preparing the budgets in order

to designing the activities which they need to work and accordingly other activities could

directed. This will helps the in coma[prison between the actual and planned performance so that

deviations can be eliminated by taking corrective measures.

TASK 4

1. Adaption of management accounting system in order to respond to the financial problems.

And also Analysing the way through which organisation can leas to success by responding to the

financial problems

There are different ways through which financial problem can b solved by adapting

different tools of management accounting system as they help the ABC Ltd. In solving their

financial problems and also guide them the direction in which they are required to perform and

work for the achievement of the organisational goals effectively and efficiently.

Balance score card

Balance score card is the model used for the performance measurement or considered to

be the performance metric which is used in the strategic management in order to identify and

focusing on improving the different internal functions of the company(Ax and Greve, 2017).

This is generally used to measure the performance and to provide feedback to the organisation so

that changes can be made of the performance s not going into the right direction.

It is basically the set of the performance targets and also the result which is related to

the four dimensions that is financial, internal process, customers and the innovation(van Helden

and Uddin, 2016). It also helps in recognising that organisation is responsible for the

stakeholders group including employees, customers, suppliers, shareholder, communities, etc.

For Example

ABC Ltd. Uses balance score cards so that they can reduce their financial problems or

any financial loss. As it uses four different elements while measuring of the performances which

includes financials, customers , internal; process and the innovation so that they can make

alterations in goods and services according to the needs and wants of the customers which helps

10

effectively and efficiently and also to direct all the activities of the organisation towards the path

of achieving organisational goals efficiently.

Planning tools are applied in ABC Ltd. For forecasting and preparing the budgets in order

to designing the activities which they need to work and accordingly other activities could

directed. This will helps the in coma[prison between the actual and planned performance so that

deviations can be eliminated by taking corrective measures.

TASK 4

1. Adaption of management accounting system in order to respond to the financial problems.

And also Analysing the way through which organisation can leas to success by responding to the

financial problems

There are different ways through which financial problem can b solved by adapting

different tools of management accounting system as they help the ABC Ltd. In solving their

financial problems and also guide them the direction in which they are required to perform and

work for the achievement of the organisational goals effectively and efficiently.

Balance score card

Balance score card is the model used for the performance measurement or considered to

be the performance metric which is used in the strategic management in order to identify and

focusing on improving the different internal functions of the company(Ax and Greve, 2017).

This is generally used to measure the performance and to provide feedback to the organisation so

that changes can be made of the performance s not going into the right direction.

It is basically the set of the performance targets and also the result which is related to

the four dimensions that is financial, internal process, customers and the innovation(van Helden

and Uddin, 2016). It also helps in recognising that organisation is responsible for the

stakeholders group including employees, customers, suppliers, shareholder, communities, etc.

For Example

ABC Ltd. Uses balance score cards so that they can reduce their financial problems or

any financial loss. As it uses four different elements while measuring of the performances which

includes financials, customers , internal; process and the innovation so that they can make

alterations in goods and services according to the needs and wants of the customers which helps

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.