Management Accounting Report: Cost Card, Budgets, and Variance

VerifiedAdded on 2020/06/04

|10

|2590

|54

Report

AI Summary

This report delves into various aspects of management accounting, beginning with the preparation of a cost card to determine per-unit costs, including direct materials, direct labor, and overheads. It then calculates the selling price using a cost-plus pricing method. The report proceeds to create and analyze various budgets, such as production, sales, direct material, direct labor, variable overhead, and fixed overhead budgets, demonstrating their role in controlling expenses and resource allocation. A significant portion is dedicated to variance analysis, explaining its importance in identifying deviations between budgeted and actual figures, and how it aids in financial control and decision-making. The report also highlights the advantages of management accounting, emphasizing its role in improved business functions, quality service, and efficient objective attainment.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

1. Preparation of cost card......................................................................................................1

2. Calculation of selling price.................................................................................................2

3. Preparation of various budgets...........................................................................................2

4. Variance analysis and its importance.................................................................................4

5. Advantages of management accounting.............................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

1. Preparation of cost card......................................................................................................1

2. Calculation of selling price.................................................................................................2

3. Preparation of various budgets...........................................................................................2

4. Variance analysis and its importance.................................................................................4

5. Advantages of management accounting.............................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

In the business, there are various aspects which are to be taken into consideration and it is

required that management accounting shall be used to deal with them (Banerjee, 2010). In this

report, several elements of it are discussed. Cost card is made and also, budget is prepared.

Further, procedure that is involved in variance analysis and how it helps in controlling of finance

are explained here as well.

TASK

1. Preparation of cost card

In the production of any product there are various costs which are incurred and they all

will be considered in making of cost card. By the help of this total cost in respect of any

particular product will be determined. The main purpose for which it is prepared is to determine

the cost involved in any item and also this can be used for the variance analysis.

Cost card per unit:

Particular Amount

Direct material £3

Direct labour £5

Variable overheads £2.5

Fixed overheads £5

Total cost per unit £15.5

It can be seen that in the total cost there are various elements which are involved and they

are as follows:

Direct material: It is the amount that is spend on raw material which is used in the

product and in given case it is determined to be £3.

Direct Labour: For making of any item workers will be required and in return of that

payment is to be made to them which is known as labour cost which is determined to be

£5.

Variable overheads: In addition to direct expenses there are some indirect expenses also

which are incurred (Giovannoni, Maraghini and Riccaboni, 2011). The amount which

1

In the business, there are various aspects which are to be taken into consideration and it is

required that management accounting shall be used to deal with them (Banerjee, 2010). In this

report, several elements of it are discussed. Cost card is made and also, budget is prepared.

Further, procedure that is involved in variance analysis and how it helps in controlling of finance

are explained here as well.

TASK

1. Preparation of cost card

In the production of any product there are various costs which are incurred and they all

will be considered in making of cost card. By the help of this total cost in respect of any

particular product will be determined. The main purpose for which it is prepared is to determine

the cost involved in any item and also this can be used for the variance analysis.

Cost card per unit:

Particular Amount

Direct material £3

Direct labour £5

Variable overheads £2.5

Fixed overheads £5

Total cost per unit £15.5

It can be seen that in the total cost there are various elements which are involved and they

are as follows:

Direct material: It is the amount that is spend on raw material which is used in the

product and in given case it is determined to be £3.

Direct Labour: For making of any item workers will be required and in return of that

payment is to be made to them which is known as labour cost which is determined to be

£5.

Variable overheads: In addition to direct expenses there are some indirect expenses also

which are incurred (Giovannoni, Maraghini and Riccaboni, 2011). The amount which

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

will be deviating with the change in total units is known as variable part and it affects

profit earned by company.

Fixed overheads: The expenses which remains same at all levels of production and by

them no impact is to be borne by business in terms of profit. The amount will be constant

and that is £5 per unit.

2. Calculation of selling price

Selling price is the amount at which product will be provided to customers. There are

many methods that can be used for the calculation of same. The main technique that can be used

for this is cost plus pricing in which a certain portion of cost is added as margin and the amount

that is derived after this is known as selling price. It is required that appropriate price shall be set

as it is directly related with the demand. If price is more then there will be decline in demand as

less number of people are willing to pay such price for product.

Selling price = Total cost + profit

Particulars Amount

Total cost per unit 15.5

Profit (20% of cost) 3.1

Selling price per unit 18.6

3. Preparation of various budgets

Budgets are the plans which are made on the basis of the standard data. They are required

to be followed by company so that it can control the overall expenses and by this resources that

are present can be used in best possible manner (Lukka and Modell, 2010). There are various

budgets which are prepared on the basis of all elements that are involved.

Production Budget:

Particulars January February March April May June Total

Units produced 2000 2100 2200 3000 3300 4000 16600

Production cost

per unit 15.5 15.5 15.5 15.5 15.5 15.5 15.5

Total cost of

production 31000 32550 34100 46500 51150 62000 257300

2

profit earned by company.

Fixed overheads: The expenses which remains same at all levels of production and by

them no impact is to be borne by business in terms of profit. The amount will be constant

and that is £5 per unit.

2. Calculation of selling price

Selling price is the amount at which product will be provided to customers. There are

many methods that can be used for the calculation of same. The main technique that can be used

for this is cost plus pricing in which a certain portion of cost is added as margin and the amount

that is derived after this is known as selling price. It is required that appropriate price shall be set

as it is directly related with the demand. If price is more then there will be decline in demand as

less number of people are willing to pay such price for product.

Selling price = Total cost + profit

Particulars Amount

Total cost per unit 15.5

Profit (20% of cost) 3.1

Selling price per unit 18.6

3. Preparation of various budgets

Budgets are the plans which are made on the basis of the standard data. They are required

to be followed by company so that it can control the overall expenses and by this resources that

are present can be used in best possible manner (Lukka and Modell, 2010). There are various

budgets which are prepared on the basis of all elements that are involved.

Production Budget:

Particulars January February March April May June Total

Units produced 2000 2100 2200 3000 3300 4000 16600

Production cost

per unit 15.5 15.5 15.5 15.5 15.5 15.5 15.5

Total cost of

production 31000 32550 34100 46500 51150 62000 257300

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

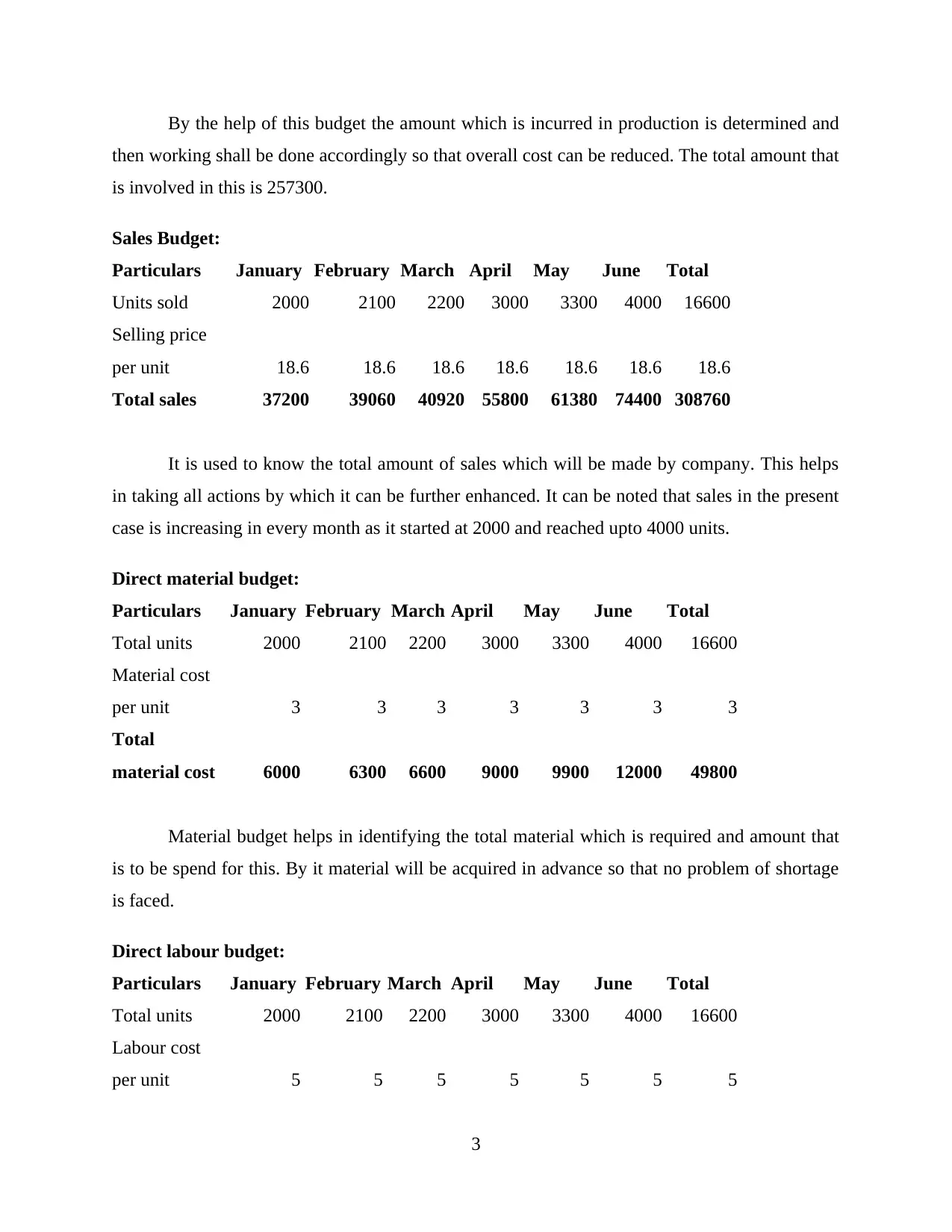

By the help of this budget the amount which is incurred in production is determined and

then working shall be done accordingly so that overall cost can be reduced. The total amount that

is involved in this is 257300.

Sales Budget:

Particulars January February March April May June Total

Units sold 2000 2100 2200 3000 3300 4000 16600

Selling price

per unit 18.6 18.6 18.6 18.6 18.6 18.6 18.6

Total sales 37200 39060 40920 55800 61380 74400 308760

It is used to know the total amount of sales which will be made by company. This helps

in taking all actions by which it can be further enhanced. It can be noted that sales in the present

case is increasing in every month as it started at 2000 and reached upto 4000 units.

Direct material budget:

Particulars January February March April May June Total

Total units 2000 2100 2200 3000 3300 4000 16600

Material cost

per unit 3 3 3 3 3 3 3

Total

material cost 6000 6300 6600 9000 9900 12000 49800

Material budget helps in identifying the total material which is required and amount that

is to be spend for this. By it material will be acquired in advance so that no problem of shortage

is faced.

Direct labour budget:

Particulars January February March April May June Total

Total units 2000 2100 2200 3000 3300 4000 16600

Labour cost

per unit 5 5 5 5 5 5 5

3

then working shall be done accordingly so that overall cost can be reduced. The total amount that

is involved in this is 257300.

Sales Budget:

Particulars January February March April May June Total

Units sold 2000 2100 2200 3000 3300 4000 16600

Selling price

per unit 18.6 18.6 18.6 18.6 18.6 18.6 18.6

Total sales 37200 39060 40920 55800 61380 74400 308760

It is used to know the total amount of sales which will be made by company. This helps

in taking all actions by which it can be further enhanced. It can be noted that sales in the present

case is increasing in every month as it started at 2000 and reached upto 4000 units.

Direct material budget:

Particulars January February March April May June Total

Total units 2000 2100 2200 3000 3300 4000 16600

Material cost

per unit 3 3 3 3 3 3 3

Total

material cost 6000 6300 6600 9000 9900 12000 49800

Material budget helps in identifying the total material which is required and amount that

is to be spend for this. By it material will be acquired in advance so that no problem of shortage

is faced.

Direct labour budget:

Particulars January February March April May June Total

Total units 2000 2100 2200 3000 3300 4000 16600

Labour cost

per unit 5 5 5 5 5 5 5

3

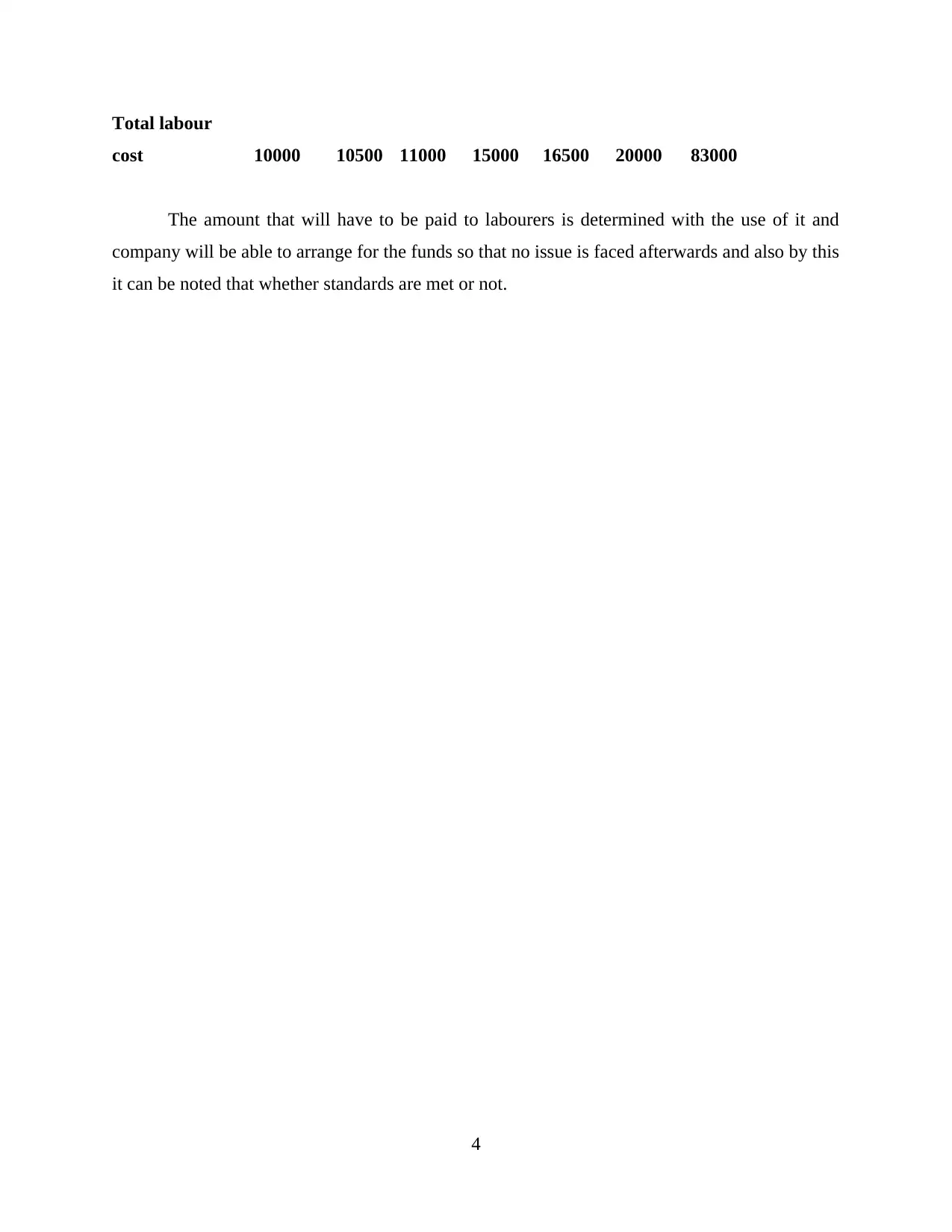

Total labour

cost 10000 10500 11000 15000 16500 20000 83000

The amount that will have to be paid to labourers is determined with the use of it and

company will be able to arrange for the funds so that no issue is faced afterwards and also by this

it can be noted that whether standards are met or not.

4

cost 10000 10500 11000 15000 16500 20000 83000

The amount that will have to be paid to labourers is determined with the use of it and

company will be able to arrange for the funds so that no issue is faced afterwards and also by this

it can be noted that whether standards are met or not.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

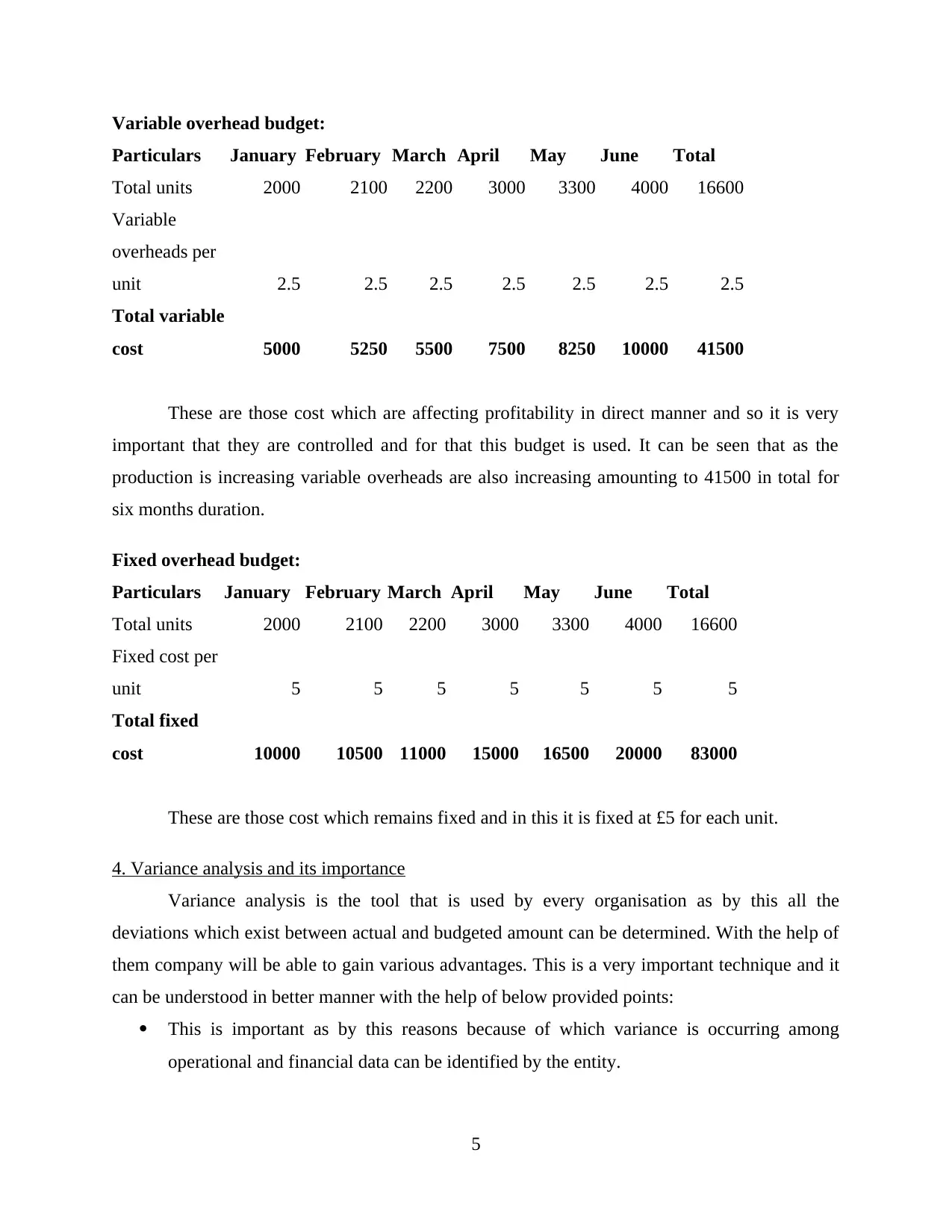

Variable overhead budget:

Particulars January February March April May June Total

Total units 2000 2100 2200 3000 3300 4000 16600

Variable

overheads per

unit 2.5 2.5 2.5 2.5 2.5 2.5 2.5

Total variable

cost 5000 5250 5500 7500 8250 10000 41500

These are those cost which are affecting profitability in direct manner and so it is very

important that they are controlled and for that this budget is used. It can be seen that as the

production is increasing variable overheads are also increasing amounting to 41500 in total for

six months duration.

Fixed overhead budget:

Particulars January February March April May June Total

Total units 2000 2100 2200 3000 3300 4000 16600

Fixed cost per

unit 5 5 5 5 5 5 5

Total fixed

cost 10000 10500 11000 15000 16500 20000 83000

These are those cost which remains fixed and in this it is fixed at £5 for each unit.

4. Variance analysis and its importance

Variance analysis is the tool that is used by every organisation as by this all the

deviations which exist between actual and budgeted amount can be determined. With the help of

them company will be able to gain various advantages. This is a very important technique and it

can be understood in better manner with the help of below provided points:

This is important as by this reasons because of which variance is occurring among

operational and financial data can be identified by the entity.

5

Particulars January February March April May June Total

Total units 2000 2100 2200 3000 3300 4000 16600

Variable

overheads per

unit 2.5 2.5 2.5 2.5 2.5 2.5 2.5

Total variable

cost 5000 5250 5500 7500 8250 10000 41500

These are those cost which are affecting profitability in direct manner and so it is very

important that they are controlled and for that this budget is used. It can be seen that as the

production is increasing variable overheads are also increasing amounting to 41500 in total for

six months duration.

Fixed overhead budget:

Particulars January February March April May June Total

Total units 2000 2100 2200 3000 3300 4000 16600

Fixed cost per

unit 5 5 5 5 5 5 5

Total fixed

cost 10000 10500 11000 15000 16500 20000 83000

These are those cost which remains fixed and in this it is fixed at £5 for each unit.

4. Variance analysis and its importance

Variance analysis is the tool that is used by every organisation as by this all the

deviations which exist between actual and budgeted amount can be determined. With the help of

them company will be able to gain various advantages. This is a very important technique and it

can be understood in better manner with the help of below provided points:

This is important as by this reasons because of which variance is occurring among

operational and financial data can be identified by the entity.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There are various projects which are undertaken by any business and by the help of this it

is possible for the business to determine the relativity and productivity of them (Nandan,

2010). Then the finding can be considered in the process further of decision making for

project selection. If it is not found to be reliable then shall not be undertaken and by this

entity is prevented from any kind of losses.

In respect of any project there are various planning which are done and in them budget is

also made and by using this difference of them with actuals can be found. So by this

deviation can be managed by managers in coming period as now they will incorporate the

reasons for deviation in new budget.

In respect of any project it is very much required that all the financial data shall be

accessed. For this reason manager of project will be undertaking analysis at all stages

involved in proposal.

By the use of this goals and objectives of business can be managed and redefined in

appropriate manner. This is because all the quantitative information which is related to

inventory, sales and expenses can be analysed by managers and then that will be used for

attainment of targets.

This is also important as budgets will become more efficient by using this. This can be

said as all the deviations will be identified and then such measures will be taken that

helps in reduction of them and also try that it does not arise in future. So for this all the

aspects which are reason for same will be considered in making of future budgets which

are more detailed.

Assigning of responsibilities will be facilitated by variance analysis and all the

departments that are present in company are kept under proper control mechanism. The

focus is given on that section regarding which more difference is identified (Management

Accounting, 2017). So it leads to improvement of function in that section and occurrence

of such activity again is avoided.

The position and picture of business is reflected in better manner by this and this helps in

making of such budget which will be accurate and therefore less difference will be

arising.

6

is possible for the business to determine the relativity and productivity of them (Nandan,

2010). Then the finding can be considered in the process further of decision making for

project selection. If it is not found to be reliable then shall not be undertaken and by this

entity is prevented from any kind of losses.

In respect of any project there are various planning which are done and in them budget is

also made and by using this difference of them with actuals can be found. So by this

deviation can be managed by managers in coming period as now they will incorporate the

reasons for deviation in new budget.

In respect of any project it is very much required that all the financial data shall be

accessed. For this reason manager of project will be undertaking analysis at all stages

involved in proposal.

By the use of this goals and objectives of business can be managed and redefined in

appropriate manner. This is because all the quantitative information which is related to

inventory, sales and expenses can be analysed by managers and then that will be used for

attainment of targets.

This is also important as budgets will become more efficient by using this. This can be

said as all the deviations will be identified and then such measures will be taken that

helps in reduction of them and also try that it does not arise in future. So for this all the

aspects which are reason for same will be considered in making of future budgets which

are more detailed.

Assigning of responsibilities will be facilitated by variance analysis and all the

departments that are present in company are kept under proper control mechanism. The

focus is given on that section regarding which more difference is identified (Management

Accounting, 2017). So it leads to improvement of function in that section and occurrence

of such activity again is avoided.

The position and picture of business is reflected in better manner by this and this helps in

making of such budget which will be accurate and therefore less difference will be

arising.

6

In the process of variance analysis it is possible that relationship that exist among various

variables in business can be identified. And all of them will be involved in planning as

negative and positive both correlations are important in it.

By the help of this predictions can be made by the use of data from earlier years and then

strategies and theories can be made by that. All this will help in improvement overall

business performance.

5. Advantages of management accounting

Management accounting is very helpful for any business and there are various benefits of

it which are as follows:

By the help of it all the functions will be performed in better manner by business as

proper plan will be formulated and executed (Soin and Collier, 2013). Some of the tasks

that are done under it includes making of budget and allocation of all data in most

appropriate manner.

Controlling of any fault that is taking place can be done as in this all the activities that are

performed will be measured and then on basis of findings measures will be specified that

are to be taken.

With the help of using of this form of accounting it is possible for the company to make

sure that services of better quality are being provided to customers.

Under this system all the responsibilities and authorities that are available with the

executives can be explained and defined in most appropriate manner. This helps in proper

organisation of work as every person will be aware about the task that is to be performed

by them.

All the objectives that have been set in company can be achieved in more effective

manner as this process helps in establishing coordination among various operations

which are performed. All the departments which includes finance, production, sales and

many others will be managed in proper manner.

All the defects, wastage and other defaults can be eliminated by the use of management

accounting and this will lead to improvement in overall efficiency of business.

Employees of organisation will be motivated by this and their morale is also boosted. All

the reports are made in which required information is provided and then it is submitted to

7

variables in business can be identified. And all of them will be involved in planning as

negative and positive both correlations are important in it.

By the help of this predictions can be made by the use of data from earlier years and then

strategies and theories can be made by that. All this will help in improvement overall

business performance.

5. Advantages of management accounting

Management accounting is very helpful for any business and there are various benefits of

it which are as follows:

By the help of it all the functions will be performed in better manner by business as

proper plan will be formulated and executed (Soin and Collier, 2013). Some of the tasks

that are done under it includes making of budget and allocation of all data in most

appropriate manner.

Controlling of any fault that is taking place can be done as in this all the activities that are

performed will be measured and then on basis of findings measures will be specified that

are to be taken.

With the help of using of this form of accounting it is possible for the company to make

sure that services of better quality are being provided to customers.

Under this system all the responsibilities and authorities that are available with the

executives can be explained and defined in most appropriate manner. This helps in proper

organisation of work as every person will be aware about the task that is to be performed

by them.

All the objectives that have been set in company can be achieved in more effective

manner as this process helps in establishing coordination among various operations

which are performed. All the departments which includes finance, production, sales and

many others will be managed in proper manner.

All the defects, wastage and other defaults can be eliminated by the use of management

accounting and this will lead to improvement in overall efficiency of business.

Employees of organisation will be motivated by this and their morale is also boosted. All

the reports are made in which required information is provided and then it is submitted to

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

higher authorities. This will help management in taking decisions regarding promotion

and demotion of all employees.

In the organisation there will be two way communication which is established by use of

it. All the aspects will be discussed in proper manner as there will be appropriate

interaction that is taking place among all employees and management (Zimmerman and

Yahya-Zadeh, 2011). So by this no default can arise due to lack of proper

communication.

So, all of them are some of the benefits which will be received by organisation by

undertaking management accounting.

CONCLUSION

From the above report, it can be said that management accounting is a useful tool that can

be used by every entity. In this report, aspects related to cost has been described and for that,

budgets are to be made. They help in proper management and evaluation. The advantages which

are attained by it have been understood here as well.

8

and demotion of all employees.

In the organisation there will be two way communication which is established by use of

it. All the aspects will be discussed in proper manner as there will be appropriate

interaction that is taking place among all employees and management (Zimmerman and

Yahya-Zadeh, 2011). So by this no default can arise due to lack of proper

communication.

So, all of them are some of the benefits which will be received by organisation by

undertaking management accounting.

CONCLUSION

From the above report, it can be said that management accounting is a useful tool that can

be used by every entity. In this report, aspects related to cost has been described and for that,

budgets are to be made. They help in proper management and evaluation. The advantages which

are attained by it have been understood here as well.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.