Management Accounting Report: Analysis of Accounting Systems and Tools

VerifiedAdded on 2020/10/22

|15

|4140

|379

Report

AI Summary

This report provides an in-depth analysis of management accounting principles and their application within TECH (UK) LTD. It begins with an introduction to management accounting, highlighting its essential requirements and contrasting it with financial accounting. The report then delves into specific tools and techniques, including activity-based costing, relevant costing analysis, and various cost accounting systems (actual, normal, and standard costing). Furthermore, it examines inventory management systems, job costing, batch costing, contract costing, process costing, and service costing. The report also explores the presentation of financial information through budgeting reports, job cost reports, and inventory/manufacturing reports. Finally, it addresses the use of the Balanced Scorecard approach for responding to financial problems, offering a comprehensive overview of management accounting practices and their impact on organizational decision-making.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management accounting and its essential requirements........................................................3

P2 Presenting financial information............................................................................................7

M1 Benefits of management systems under the TECH (UK) LTD............................................8

D1. How management accounting system and management accounting reporting integrates

within the company process........................................................................................................9

TASK 2............................................................................................................................................9

P3 Calculation of net profit under marginal and absorption costing: -.......................................9

M2. Application of techniques:.................................................................................................12

D2. Data interpretation:.............................................................................................................12

TASK 3..........................................................................................................................................12

P4. Budget and its advantage and disadvantage........................................................................12

b).Different types of common costing systems which can be used for budgetary control:......13

c) Importance of budget as a method for planning and controlling purpose:...........................13

M3. Use of various planning tools for making budget:............................................................14

M4 How financial tools are used for evaluating the financial problems:.................................14

TASK 4..........................................................................................................................................14

P5 Balanced Scorecard Approach can be used to respond its financial problems: -................14

D3 How planning tools for accounting respond for solving financial problems:.....................15

CONCLUSION .............................................................................................................................15

REFERENCES..............................................................................................................................16

TASK 1............................................................................................................................................3

P1 Management accounting and its essential requirements........................................................3

P2 Presenting financial information............................................................................................7

M1 Benefits of management systems under the TECH (UK) LTD............................................8

D1. How management accounting system and management accounting reporting integrates

within the company process........................................................................................................9

TASK 2............................................................................................................................................9

P3 Calculation of net profit under marginal and absorption costing: -.......................................9

M2. Application of techniques:.................................................................................................12

D2. Data interpretation:.............................................................................................................12

TASK 3..........................................................................................................................................12

P4. Budget and its advantage and disadvantage........................................................................12

b).Different types of common costing systems which can be used for budgetary control:......13

c) Importance of budget as a method for planning and controlling purpose:...........................13

M3. Use of various planning tools for making budget:............................................................14

M4 How financial tools are used for evaluating the financial problems:.................................14

TASK 4..........................................................................................................................................14

P5 Balanced Scorecard Approach can be used to respond its financial problems: -................14

D3 How planning tools for accounting respond for solving financial problems:.....................15

CONCLUSION .............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

As per this record a technique for accounts for management, for providing important and

reliable report for accomplishment of purpose to the management. Management Accounting

includes functions such as planning, directing, controlling and helps management to perform

these functions in better and acceptable and in a systematic arrangement to organization in short

way (Arroyo, 2012). In this record, TECH (UK) LTD. manufactured a unique sound system and

it believes that, applying the principles of management accounting will lead to effective

communication and proper understanding in different department with regard to availability of

information for all the departments for making improvement in ability to make decisions. In this

record organization will prepare the accounting records related with management in such a way

that it will help them in making the decisions that are best for the purpose of the company. There

exists many type of techniques which can be used to check the overall achievement of

organization in achieving desired standards in a better and acceptable way.

TASK 1

P1 Management accounting and its essential requirements

Management Accounting is a way by which we interrelate, investigates, and

demonstrate the accounting data that is collected by considering the financial information and

costing information. It is used in controlling procedures of the organization and forming

conclusions for same and is also providing better concern regarding performance of organization

to Board, CEO” s and accounting executives of the organization.

The areas where management accounting can make difference are:

Measuring risk

Evaluating performance standard

Allocating resources properly

Assisting in readying financial statements of the organization

Forming policies and making decisions which are appropriate for the organization.

1. Differences between management accounting and financial accounting: -

Base Management accounting Financial accounting

Motive

It is used to give important information to

Financial accounting is an art of

classifying, summarizing and

As per this record a technique for accounts for management, for providing important and

reliable report for accomplishment of purpose to the management. Management Accounting

includes functions such as planning, directing, controlling and helps management to perform

these functions in better and acceptable and in a systematic arrangement to organization in short

way (Arroyo, 2012). In this record, TECH (UK) LTD. manufactured a unique sound system and

it believes that, applying the principles of management accounting will lead to effective

communication and proper understanding in different department with regard to availability of

information for all the departments for making improvement in ability to make decisions. In this

record organization will prepare the accounting records related with management in such a way

that it will help them in making the decisions that are best for the purpose of the company. There

exists many type of techniques which can be used to check the overall achievement of

organization in achieving desired standards in a better and acceptable way.

TASK 1

P1 Management accounting and its essential requirements

Management Accounting is a way by which we interrelate, investigates, and

demonstrate the accounting data that is collected by considering the financial information and

costing information. It is used in controlling procedures of the organization and forming

conclusions for same and is also providing better concern regarding performance of organization

to Board, CEO” s and accounting executives of the organization.

The areas where management accounting can make difference are:

Measuring risk

Evaluating performance standard

Allocating resources properly

Assisting in readying financial statements of the organization

Forming policies and making decisions which are appropriate for the organization.

1. Differences between management accounting and financial accounting: -

Base Management accounting Financial accounting

Motive

It is used to give important information to

Financial accounting is an art of

classifying, summarizing and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the management for performing its

function.

recording of events and

evaluating the results thereof in

an appropriate way.

Rules to be

followed

There is no requirement for following the

rules and requirements of accounting

principles as well as conventions in the

management accounting (Boyns and

Edwards, 2013).

In case of Financial accounting

there exists some rules and

regulations which are to be

followed if applicable to the

company and there is legal

binding to follow such

requirement.

Time period Management accounting records are

updated at regular time period in course of

the financial year

These records are always

developed at the end of

accounting period i.e when all

the transactions of organization

for the year are completed.

Usage Management accounting considers the

financial information as well as non-

financial information for evaluating the

performance standard of the company

Financial accounting considers

only the financial information

in preparing the final accounts

for the year.

Consideration In management accounting, each

subdivision of the organization is treated as

a distinct entity. Therefore, performance

reports and their analysis are prepared

separately for each division of the

organization wherever required.

Financial accounting are

constructed by considering all

the subdivisions of the

organization as one.

2. The important tools of management accounting information for assisting in making

decisions for the department managers are given below: -

Activity based costing: - (ABC) is a cost accounting method that analyze costs to

overhead actions and then apportions those costs to product. ABC costing identifies the relations

among costs, overhead processes and products which are manufactured by the organization

function.

recording of events and

evaluating the results thereof in

an appropriate way.

Rules to be

followed

There is no requirement for following the

rules and requirements of accounting

principles as well as conventions in the

management accounting (Boyns and

Edwards, 2013).

In case of Financial accounting

there exists some rules and

regulations which are to be

followed if applicable to the

company and there is legal

binding to follow such

requirement.

Time period Management accounting records are

updated at regular time period in course of

the financial year

These records are always

developed at the end of

accounting period i.e when all

the transactions of organization

for the year are completed.

Usage Management accounting considers the

financial information as well as non-

financial information for evaluating the

performance standard of the company

Financial accounting considers

only the financial information

in preparing the final accounts

for the year.

Consideration In management accounting, each

subdivision of the organization is treated as

a distinct entity. Therefore, performance

reports and their analysis are prepared

separately for each division of the

organization wherever required.

Financial accounting are

constructed by considering all

the subdivisions of the

organization as one.

2. The important tools of management accounting information for assisting in making

decisions for the department managers are given below: -

Activity based costing: - (ABC) is a cost accounting method that analyze costs to

overhead actions and then apportions those costs to product. ABC costing identifies the relations

among costs, overhead processes and products which are manufactured by the organization

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

through this relationship. It apportions indirect cost to product indirectly as compared to the

prevailing old methods of costing. It assists in reducing overhead cost to a much lower level

which is set as a standard by the organization and also this system will help the organization in

point out costing, production manufacturing line, analyzing profits, in the organization. ABC

betters the process of identifying costing in three ways. First, it increases the number of bases by

which we can bring overhead costs under one umbrella. It also brings out new standards for

apportioning indirect cost in such way that cost based on the activities that will produce cost

instead of on production measures, such as machine hours or direct labour cost.

Relevant costing analysis Buying decision: - when organization wants to purchase something

then this decision making process is used by organization regarding transaction before, during

and after the purchasing period (Herzig and et. al. 2012). It could be seen as special form of cost

saving analysis in the presence of many other options. It helps the management in selecting the

best supplier between outside source supplier and market and after analyzing the above

procedure the manager analyse which is much better alternative for the company.

3. Cost accounting system (actual, normal and standard costing):- This process is used by

the organization to estimate the price of the product for performing profitability analysis, stock

value and controlling cost for the same. An organization must have knowledge about its best

product and this can be only possible when it has sound knowledge regarding that product and

have applied correct measures to ascertain the cost of the product.

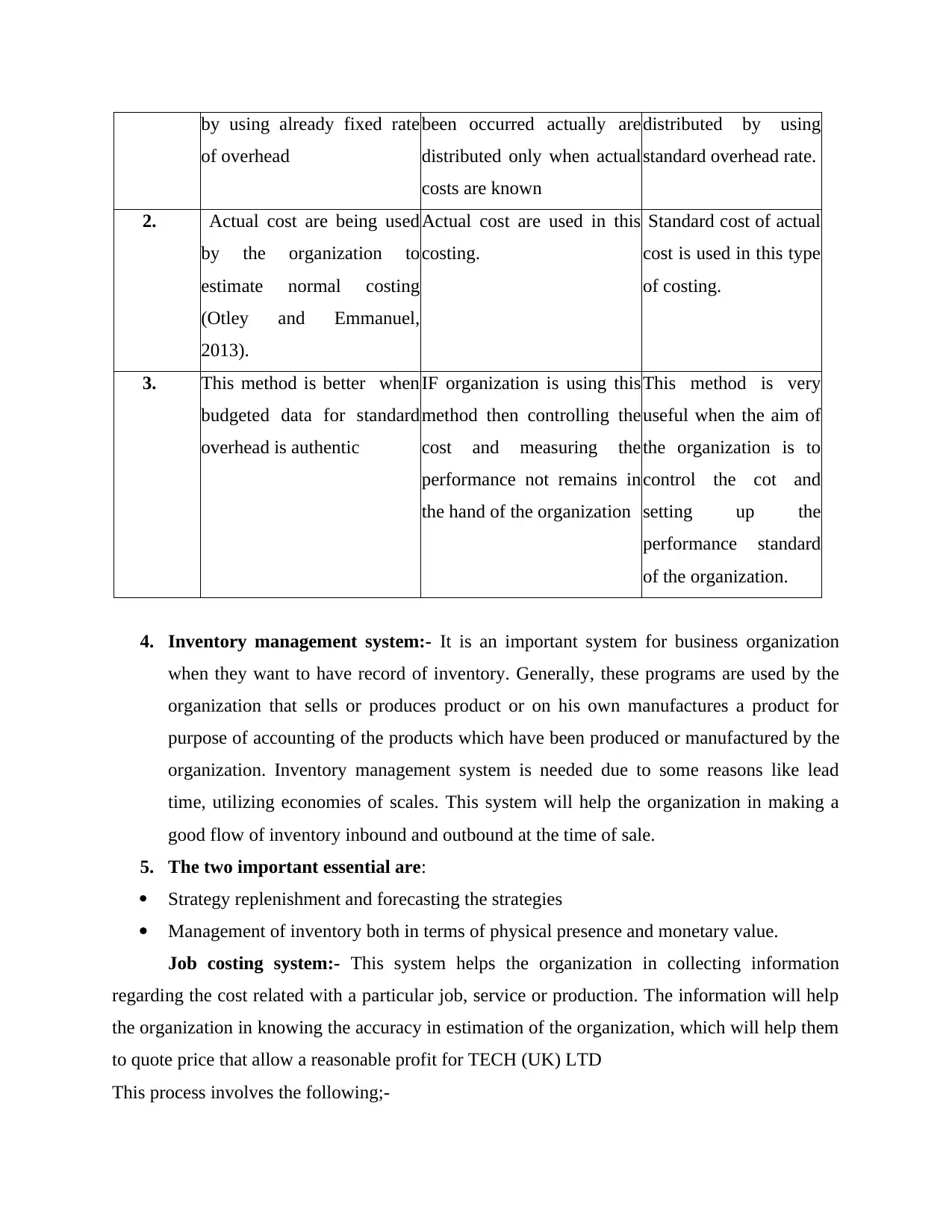

Difference between the NORMAL COSTING, ACTUAL COSTING AND STANDARD

COSTING:-

NO. NORMAL COSTING ACTUAL COSTING STANDARD

COSTING

1. Direct cost which are

apportioned to particular job

as soon it is occurred

Actual Direct costs are

assigned to job as it is

occurred

Standard direct costs

are apportioned to job

as occurred.

1. Overhead related with

manufacturing is distributed

Overhead related with

manufacturing which have

Overhead related with

manufacturing is

prevailing old methods of costing. It assists in reducing overhead cost to a much lower level

which is set as a standard by the organization and also this system will help the organization in

point out costing, production manufacturing line, analyzing profits, in the organization. ABC

betters the process of identifying costing in three ways. First, it increases the number of bases by

which we can bring overhead costs under one umbrella. It also brings out new standards for

apportioning indirect cost in such way that cost based on the activities that will produce cost

instead of on production measures, such as machine hours or direct labour cost.

Relevant costing analysis Buying decision: - when organization wants to purchase something

then this decision making process is used by organization regarding transaction before, during

and after the purchasing period (Herzig and et. al. 2012). It could be seen as special form of cost

saving analysis in the presence of many other options. It helps the management in selecting the

best supplier between outside source supplier and market and after analyzing the above

procedure the manager analyse which is much better alternative for the company.

3. Cost accounting system (actual, normal and standard costing):- This process is used by

the organization to estimate the price of the product for performing profitability analysis, stock

value and controlling cost for the same. An organization must have knowledge about its best

product and this can be only possible when it has sound knowledge regarding that product and

have applied correct measures to ascertain the cost of the product.

Difference between the NORMAL COSTING, ACTUAL COSTING AND STANDARD

COSTING:-

NO. NORMAL COSTING ACTUAL COSTING STANDARD

COSTING

1. Direct cost which are

apportioned to particular job

as soon it is occurred

Actual Direct costs are

assigned to job as it is

occurred

Standard direct costs

are apportioned to job

as occurred.

1. Overhead related with

manufacturing is distributed

Overhead related with

manufacturing which have

Overhead related with

manufacturing is

by using already fixed rate

of overhead

been occurred actually are

distributed only when actual

costs are known

distributed by using

standard overhead rate.

2. Actual cost are being used

by the organization to

estimate normal costing

(Otley and Emmanuel,

2013).

Actual cost are used in this

costing.

Standard cost of actual

cost is used in this type

of costing.

3. This method is better when

budgeted data for standard

overhead is authentic

IF organization is using this

method then controlling the

cost and measuring the

performance not remains in

the hand of the organization

This method is very

useful when the aim of

the organization is to

control the cot and

setting up the

performance standard

of the organization.

4. Inventory management system:- It is an important system for business organization

when they want to have record of inventory. Generally, these programs are used by the

organization that sells or produces product or on his own manufactures a product for

purpose of accounting of the products which have been produced or manufactured by the

organization. Inventory management system is needed due to some reasons like lead

time, utilizing economies of scales. This system will help the organization in making a

good flow of inventory inbound and outbound at the time of sale.

5. The two important essential are:

Strategy replenishment and forecasting the strategies

Management of inventory both in terms of physical presence and monetary value.

Job costing system:- This system helps the organization in collecting information

regarding the cost related with a particular job, service or production. The information will help

the organization in knowing the accuracy in estimation of the organization, which will help them

to quote price that allow a reasonable profit for TECH (UK) LTD

This process involves the following;-

of overhead

been occurred actually are

distributed only when actual

costs are known

distributed by using

standard overhead rate.

2. Actual cost are being used

by the organization to

estimate normal costing

(Otley and Emmanuel,

2013).

Actual cost are used in this

costing.

Standard cost of actual

cost is used in this type

of costing.

3. This method is better when

budgeted data for standard

overhead is authentic

IF organization is using this

method then controlling the

cost and measuring the

performance not remains in

the hand of the organization

This method is very

useful when the aim of

the organization is to

control the cot and

setting up the

performance standard

of the organization.

4. Inventory management system:- It is an important system for business organization

when they want to have record of inventory. Generally, these programs are used by the

organization that sells or produces product or on his own manufactures a product for

purpose of accounting of the products which have been produced or manufactured by the

organization. Inventory management system is needed due to some reasons like lead

time, utilizing economies of scales. This system will help the organization in making a

good flow of inventory inbound and outbound at the time of sale.

5. The two important essential are:

Strategy replenishment and forecasting the strategies

Management of inventory both in terms of physical presence and monetary value.

Job costing system:- This system helps the organization in collecting information

regarding the cost related with a particular job, service or production. The information will help

the organization in knowing the accuracy in estimation of the organization, which will help them

to quote price that allow a reasonable profit for TECH (UK) LTD

This process involves the following;-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Receiving any sort of inquiry

Determining the price of the job

Receiving the orders

Producing an order

Recording the cost

Completing a job Batch costing: This is a type of job costing and in this homogeneous goods are taken as

cost unit. This consists some specific number of products and that number varies from

another batch. Mainly batch cost is utilise to ascertain cost per unit and article per unit.

Procedure of batch costing is similar as per job costing and that’s why production order

number is allotted to every batch.

Contract costing: This is one of the most popular method of Job costing. Under this, a

separate number is allotted to each contract and records are maintained for each contract

separately. Mainly this is used by builders and construction firms. Main purpose of

prepare a contract account is to determine the cost of every contract separately and profit

of each contract.

Process costing: In this a method of assign manufacturing costs where cost of each unit

produced is assumed to be the same for every unit. This is mostly used when products are

mass produced and in the cases when cost linked to individual cannot be distinguish form

each other.

Service costing: This type of costing is used in service organisation like transport

organisation, power generation, colleges and hospitals. All cost incurred during a specific

time period is collected and examine and after that expresses in terms of a cost per unit of

service.

P2 Presenting financial information

Management accounting records are way through which we can get a good knowledge

about TECH (UK) LTD (Parker, 2012). This record can help us in reaching the opinion about the

working of the organization, helps organization in submitting additional reports that the company

must complete for tax purpose. The different management accounting reports helps the

management in preparing better reports related with management. The different type of records

which are prepared by the management and their advantage are given below:-

Determining the price of the job

Receiving the orders

Producing an order

Recording the cost

Completing a job Batch costing: This is a type of job costing and in this homogeneous goods are taken as

cost unit. This consists some specific number of products and that number varies from

another batch. Mainly batch cost is utilise to ascertain cost per unit and article per unit.

Procedure of batch costing is similar as per job costing and that’s why production order

number is allotted to every batch.

Contract costing: This is one of the most popular method of Job costing. Under this, a

separate number is allotted to each contract and records are maintained for each contract

separately. Mainly this is used by builders and construction firms. Main purpose of

prepare a contract account is to determine the cost of every contract separately and profit

of each contract.

Process costing: In this a method of assign manufacturing costs where cost of each unit

produced is assumed to be the same for every unit. This is mostly used when products are

mass produced and in the cases when cost linked to individual cannot be distinguish form

each other.

Service costing: This type of costing is used in service organisation like transport

organisation, power generation, colleges and hospitals. All cost incurred during a specific

time period is collected and examine and after that expresses in terms of a cost per unit of

service.

P2 Presenting financial information

Management accounting records are way through which we can get a good knowledge

about TECH (UK) LTD (Parker, 2012). This record can help us in reaching the opinion about the

working of the organization, helps organization in submitting additional reports that the company

must complete for tax purpose. The different management accounting reports helps the

management in preparing better reports related with management. The different type of records

which are prepared by the management and their advantage are given below:-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Budgeting reports:- these records are prepared by the company to make standard

regarding the manufacturing target which a company sincerely wants to achieve. For this

company obtains data from the previous period. Employees will be able to get more

incentive and bonus with the help of these records and will also able to achieve the target

of the company.

Job cost reports:- These records are obtained to collect information with respect to

each job, contract, product or work order. Each production subdivision is treated as

distinct entity in these records. These records are prepared to know the cost involved in

each project and the cost involved in material, labor, overhead of organization.

Inventory and manufacturing reports:- Organization use this record improve its

manufacturing standard in such a way that it will be better than previous. Information

about the cost per unit, labour and overhead are some of the highlights of these reports.

Performance report:- these records considers managerial accounting information and

are concerned with the performance of the organization. These records helps in

comparing budgeted cost and actual cost of the company. These reports may be prepared

by the organization half-yearly or quarterly as needed by the organization.

2. Recording system’s importance:-

It will help the management of the organization in knowing the performance standard of

the company and overall growth of the company in the year. It will record all the important

transaction which are essential for the survival of the organization and which provides the value

to the organization these report will also able the organization in having the records of debtor and

creditors of the organization. It will also enable the organization to have the records of inventory

which are currently available with the organization (Vasile and Man, 2012).

M1 Benefits of management systems under the TECH (UK) LTD.

These techniques will surely be going to help TECH (UK) LTD. It will help them to run

their business without any hiccups. These tools will help in achieving the goals set by the

organization in a better way. Management accounting gives more beneficial objective to

company when providing important information also increasing the ratios related with profits of

the company.

regarding the manufacturing target which a company sincerely wants to achieve. For this

company obtains data from the previous period. Employees will be able to get more

incentive and bonus with the help of these records and will also able to achieve the target

of the company.

Job cost reports:- These records are obtained to collect information with respect to

each job, contract, product or work order. Each production subdivision is treated as

distinct entity in these records. These records are prepared to know the cost involved in

each project and the cost involved in material, labor, overhead of organization.

Inventory and manufacturing reports:- Organization use this record improve its

manufacturing standard in such a way that it will be better than previous. Information

about the cost per unit, labour and overhead are some of the highlights of these reports.

Performance report:- these records considers managerial accounting information and

are concerned with the performance of the organization. These records helps in

comparing budgeted cost and actual cost of the company. These reports may be prepared

by the organization half-yearly or quarterly as needed by the organization.

2. Recording system’s importance:-

It will help the management of the organization in knowing the performance standard of

the company and overall growth of the company in the year. It will record all the important

transaction which are essential for the survival of the organization and which provides the value

to the organization these report will also able the organization in having the records of debtor and

creditors of the organization. It will also enable the organization to have the records of inventory

which are currently available with the organization (Vasile and Man, 2012).

M1 Benefits of management systems under the TECH (UK) LTD.

These techniques will surely be going to help TECH (UK) LTD. It will help them to run

their business without any hiccups. These tools will help in achieving the goals set by the

organization in a better way. Management accounting gives more beneficial objective to

company when providing important information also increasing the ratios related with profits of

the company.

D1. How management accounting system and management accounting reporting integrates

within the company process

Management accounting system helps to TECH (UK) LTD. There is a need to make sure

that reports are prepared in such a manner that it will help the business in achieving the business

goals by keeping in view the standards set by the organization to control the cost and achieving

the targets with stipulated time. This will help them in running their business with not so much

difficulty therefore both the system of management accounting reports and management

accounting system are need of the hour for the organization in attaining a smooth workable

balance (Cadez and Guilding, 2012).

TASK 2

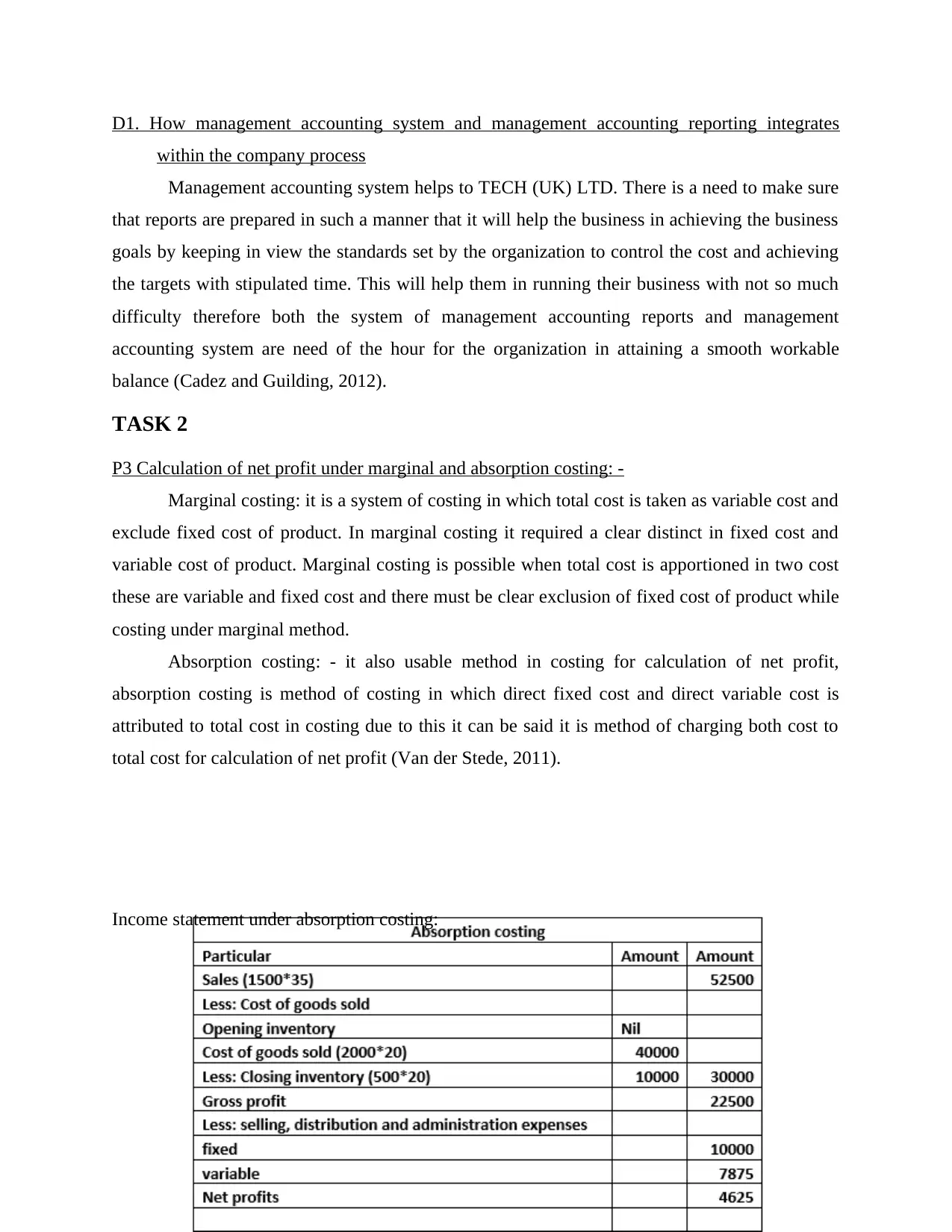

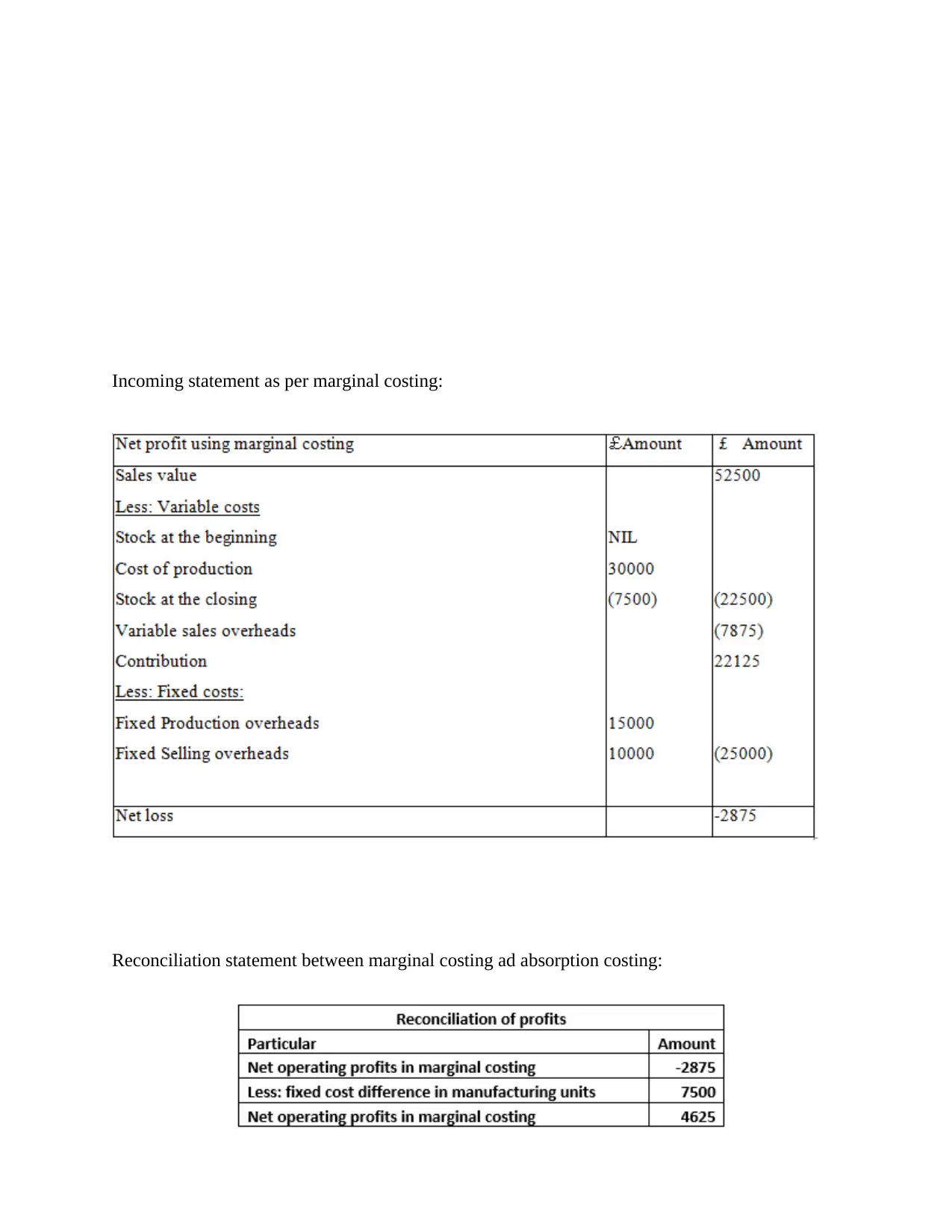

P3 Calculation of net profit under marginal and absorption costing: -

Marginal costing: it is a system of costing in which total cost is taken as variable cost and

exclude fixed cost of product. In marginal costing it required a clear distinct in fixed cost and

variable cost of product. Marginal costing is possible when total cost is apportioned in two cost

these are variable and fixed cost and there must be clear exclusion of fixed cost of product while

costing under marginal method.

Absorption costing: - it also usable method in costing for calculation of net profit,

absorption costing is method of costing in which direct fixed cost and direct variable cost is

attributed to total cost in costing due to this it can be said it is method of charging both cost to

total cost for calculation of net profit (Van der Stede, 2011).

Income statement under absorption costing:

within the company process

Management accounting system helps to TECH (UK) LTD. There is a need to make sure

that reports are prepared in such a manner that it will help the business in achieving the business

goals by keeping in view the standards set by the organization to control the cost and achieving

the targets with stipulated time. This will help them in running their business with not so much

difficulty therefore both the system of management accounting reports and management

accounting system are need of the hour for the organization in attaining a smooth workable

balance (Cadez and Guilding, 2012).

TASK 2

P3 Calculation of net profit under marginal and absorption costing: -

Marginal costing: it is a system of costing in which total cost is taken as variable cost and

exclude fixed cost of product. In marginal costing it required a clear distinct in fixed cost and

variable cost of product. Marginal costing is possible when total cost is apportioned in two cost

these are variable and fixed cost and there must be clear exclusion of fixed cost of product while

costing under marginal method.

Absorption costing: - it also usable method in costing for calculation of net profit,

absorption costing is method of costing in which direct fixed cost and direct variable cost is

attributed to total cost in costing due to this it can be said it is method of charging both cost to

total cost for calculation of net profit (Van der Stede, 2011).

Income statement under absorption costing:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Incoming statement as per marginal costing:

Reconciliation statement between marginal costing ad absorption costing:

Reconciliation statement between marginal costing ad absorption costing:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M2. Application of techniques:

In the situation of this case TECH (UK) LTD. Should use these technique to increase and

enhance its profit margin. It will be useful for the enterprises to operate their business in better

and effective way. These techniques is very important for the company for taking business

decision and planning for company’ goals and objecting to be directed.

D2. Data interpretation:

The calculation on net profit from both of the method that is marginal and absorption costing

identify many differences. According to the absorption costing method, the company earns (£)

4,625 net operating profits. On the other hand, the company loss (£)2,875 net operating loss by

using the marginal costing method. So, it is better for the company to use the absorption costing

method to earn the net operating profits (Fullerton, Kennedy and Widener, 2013).

TASK 3

P4. Budget and its advantage and disadvantage

Budget is very important and essential tool for company. Budget can be define as a

presentation of last year and old data and information based standard for current business.

Budget is tool of comparison of lat financial position and current financial position and help to

target the expenses and income for the company. It can be say that budget is very important part

for operating company’s business for accounting manager. A budget is made for applying the

forecasted plans and strategies to achieve business object with effective way. Due to budget the

company is able to reach the analysis of targets of business.

Operating budget: Operating budget is first step and starting budget, this budget is made for

the operational function like operating income, operating expenses and operating profit ratio of

company. It is a budget which provide essential for operating profit.

Advantage

By use of the operating budget company is able to know about operating total profit and

position of company.

In the situation of this case TECH (UK) LTD. Should use these technique to increase and

enhance its profit margin. It will be useful for the enterprises to operate their business in better

and effective way. These techniques is very important for the company for taking business

decision and planning for company’ goals and objecting to be directed.

D2. Data interpretation:

The calculation on net profit from both of the method that is marginal and absorption costing

identify many differences. According to the absorption costing method, the company earns (£)

4,625 net operating profits. On the other hand, the company loss (£)2,875 net operating loss by

using the marginal costing method. So, it is better for the company to use the absorption costing

method to earn the net operating profits (Fullerton, Kennedy and Widener, 2013).

TASK 3

P4. Budget and its advantage and disadvantage

Budget is very important and essential tool for company. Budget can be define as a

presentation of last year and old data and information based standard for current business.

Budget is tool of comparison of lat financial position and current financial position and help to

target the expenses and income for the company. It can be say that budget is very important part

for operating company’s business for accounting manager. A budget is made for applying the

forecasted plans and strategies to achieve business object with effective way. Due to budget the

company is able to reach the analysis of targets of business.

Operating budget: Operating budget is first step and starting budget, this budget is made for

the operational function like operating income, operating expenses and operating profit ratio of

company. It is a budget which provide essential for operating profit.

Advantage

By use of the operating budget company is able to know about operating total profit and

position of company.

The operating budget leads to run business without financial issues.

Disadvantage:

The operating budget is not helping in identify with actual relation with operating

position of company (Luft and Shields, 2010).

Standard made for the budget will not match with actual outcomes.

Cash budget: it is also very important budget which is use for cash flows of company. This

budget entails about the cash receipt and cash payment of company is required in attaining goals

and aim of company with the effective liquidity of company and availability of cash reserves in

company for initial payment of creditors and loans of business (Tucker and Lowe, 2014).

Advantage

It entails the company about the liquidity of company.

Cash budget is important in procurement of cash fund for initial payment of cash.

It is useful in managing proper cash requirement of company.

Disadvantage

Cash budget not useful to relate with non cash activity.

Cash budget not entail essential opportunity cost of cash outlay.

b).Different types of common costing systems which can be used for budgetary control:

Standard costing: standard costing is method of identify the adverse and favourable

position of company in this method actual cost of product got compared with standard

cost of product.

Normal costing: normal costing is a method whereby all the direct costs are chargeable

which are actually incurred for product.

Actual costing: it is method of costing where all actual data are prefer for purpose of

costing and require the actual cost of product for costing.

c) Importance of budget as a method for planning and controlling purpose:

The making of budget is very useful for the company, budget are pre-determined data

which is incurred on the basis of last financial data of company and lead to achieve the business

objective and goals for the management. Due to budget company will be able to know financial

position and fund requirement of company and what action should be taken by the company for

remove the bugs and hurdle of operating business (Morales and Lambert, 2013).

Disadvantage:

The operating budget is not helping in identify with actual relation with operating

position of company (Luft and Shields, 2010).

Standard made for the budget will not match with actual outcomes.

Cash budget: it is also very important budget which is use for cash flows of company. This

budget entails about the cash receipt and cash payment of company is required in attaining goals

and aim of company with the effective liquidity of company and availability of cash reserves in

company for initial payment of creditors and loans of business (Tucker and Lowe, 2014).

Advantage

It entails the company about the liquidity of company.

Cash budget is important in procurement of cash fund for initial payment of cash.

It is useful in managing proper cash requirement of company.

Disadvantage

Cash budget not useful to relate with non cash activity.

Cash budget not entail essential opportunity cost of cash outlay.

b).Different types of common costing systems which can be used for budgetary control:

Standard costing: standard costing is method of identify the adverse and favourable

position of company in this method actual cost of product got compared with standard

cost of product.

Normal costing: normal costing is a method whereby all the direct costs are chargeable

which are actually incurred for product.

Actual costing: it is method of costing where all actual data are prefer for purpose of

costing and require the actual cost of product for costing.

c) Importance of budget as a method for planning and controlling purpose:

The making of budget is very useful for the company, budget are pre-determined data

which is incurred on the basis of last financial data of company and lead to achieve the business

objective and goals for the management. Due to budget company will be able to know financial

position and fund requirement of company and what action should be taken by the company for

remove the bugs and hurdle of operating business (Morales and Lambert, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.