Management Accounting Report: Costing Methods and Financial Analysis

VerifiedAdded on 2020/06/04

|14

|4068

|34

Report

AI Summary

This report delves into the realm of management accounting, focusing on its core principles and practical applications within the context of Tech UK. It initiates with an introduction to management accounting, emphasizing its significance in financial data recording, summarization, evaluation, and control. The report proceeds to explore various reporting methods, including performance reports, accounts receivable reports, and inventory management reports, highlighting their importance in organizational financial analysis. It then analyzes the benefits of accounting systems, particularly cost accounting and inventory management systems, and critically evaluates the impact of reporting systems. The report further examines costing methods, specifically absorption and marginal costing, to calculate net profitability. Budgeting, planning tools, and their merits and demerits are assessed, followed by a critical evaluation of financial issues. The balance scorecard approach is also addressed. The report concludes with an analysis of financial problems and offers insights into potential solutions, providing a comprehensive overview of management accounting practices.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Meaning of management accounting and its essential requirements...............................1

P2: Various types of reporting method...................................................................................3

M1: Analyse benefits of using accounting system.................................................................4

D1: Critical analysis of reporting system...............................................................................4

TASK 2............................................................................................................................................5

P3: Costing method use to calculate net profitability for the company.................................5

M2: Analysis of using management accounting techniques..................................................8

D2: Critical evaluation of collected data in income statements.............................................8

TASK 3............................................................................................................................................8

P4: Merits and demerits of using budgets..............................................................................8

M3: Analysis of various planning tools................................................................................10

D3: Critical evaluation of financial issues............................................................................10

TASK 4..........................................................................................................................................10

P5: Balance scorecard approach...........................................................................................10

M4: Analysis of financial problems.....................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Meaning of management accounting and its essential requirements...............................1

P2: Various types of reporting method...................................................................................3

M1: Analyse benefits of using accounting system.................................................................4

D1: Critical analysis of reporting system...............................................................................4

TASK 2............................................................................................................................................5

P3: Costing method use to calculate net profitability for the company.................................5

M2: Analysis of using management accounting techniques..................................................8

D2: Critical evaluation of collected data in income statements.............................................8

TASK 3............................................................................................................................................8

P4: Merits and demerits of using budgets..............................................................................8

M3: Analysis of various planning tools................................................................................10

D3: Critical evaluation of financial issues............................................................................10

TASK 4..........................................................................................................................................10

P5: Balance scorecard approach...........................................................................................10

M4: Analysis of financial problems.....................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Account is a systematic study of financial transactions that are being use for the purpose of

evaluating overall impacts of an organisation. The information that is collected by the company

is needed to be record, summarise, evaluate and control its related implication before posting it

into their respective format. Management is held responsible for providing necessary information

and support to account officers to regulate their operations in more effective manner. The main

motive of an organisation is to attain future aims and objectives through using reliable data about

the company.

This particular project is all about explaining necessary information about accounting

system and reporting methods. While some costing methods are utilised for the purpose of

evaluating net profit for the company. Further, this report is analysing merits and demerits of

using planning tools that are essential of budget controlling are discussed under this report. In

accordance with this, all financial problems that are present in an organisation are analyse and

measures is being use to overcomes them are explain in this report (Zoni, Dossi and Morelli,

2012).

TASK 1

P1: Meaning of management accounting and its essential requirements

Nowadays, it has been seen that recording of financial data in utmost important aspects for

an organisation. This will assist in managers to make use of appropriate accounting data into

their respective format as per their date of occurrence. The main motive behind doing so is to

reduce extra costs and expenses that are being done during an accounting period of time. Every

data collected from different sources are having valuable consideration during preparation of

essential statements (Van der Stede, 2015). The primary aim of an organisation is to attain sort

and long term aims and objectives that are crucial for the company. All data collected would be

analyse and regulated in appropriate manner before presenting it in front of various outside

stakeholders and investors.

Comparison

Management accounting Financial accounting

This is responsible for making valuable rules

and regulations in order to prepare financial

While in this particular accounting, accountant

need to make use of policies and rules in

1

Account is a systematic study of financial transactions that are being use for the purpose of

evaluating overall impacts of an organisation. The information that is collected by the company

is needed to be record, summarise, evaluate and control its related implication before posting it

into their respective format. Management is held responsible for providing necessary information

and support to account officers to regulate their operations in more effective manner. The main

motive of an organisation is to attain future aims and objectives through using reliable data about

the company.

This particular project is all about explaining necessary information about accounting

system and reporting methods. While some costing methods are utilised for the purpose of

evaluating net profit for the company. Further, this report is analysing merits and demerits of

using planning tools that are essential of budget controlling are discussed under this report. In

accordance with this, all financial problems that are present in an organisation are analyse and

measures is being use to overcomes them are explain in this report (Zoni, Dossi and Morelli,

2012).

TASK 1

P1: Meaning of management accounting and its essential requirements

Nowadays, it has been seen that recording of financial data in utmost important aspects for

an organisation. This will assist in managers to make use of appropriate accounting data into

their respective format as per their date of occurrence. The main motive behind doing so is to

reduce extra costs and expenses that are being done during an accounting period of time. Every

data collected from different sources are having valuable consideration during preparation of

essential statements (Van der Stede, 2015). The primary aim of an organisation is to attain sort

and long term aims and objectives that are crucial for the company. All data collected would be

analyse and regulated in appropriate manner before presenting it in front of various outside

stakeholders and investors.

Comparison

Management accounting Financial accounting

This is responsible for making valuable rules

and regulations in order to prepare financial

While in this particular accounting, accountant

need to make use of policies and rules in

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

reports in appropriate manner. formulation of specific reports.

The data presented in front of management is

based on historical cost that is mainly use for

the purpose of planning in their future

operations.

These are associated with all activities those

are based on past data.

It is not use to evaluate financial and

operations performances of an Tech UK.

This is related with only financial data for the

cited company.

Importance of using types of management accounting systems:

It has been determine that accounting systems are more reliable and appropriate techniques

by which all information can be recorded into their respective format in more effective and

accurate manner. The manager can easily be able to take some crucial decision regarding their

future growth and stability by the help of management accounting systems (Tessier and Otley,

2012). The performance of the company can also be enhancing by using right kind of techniques

in their daily course of actions. It is used to measure all necessary tools and methods for an

organisation through comparing past performance with the current one.

Types of accounting system:

Cost accounting system: It happens to be primary accounting components of

management. They uses this as more reliable system in order to record, summarise and determine

best accurate alternative should be helpful for Tech UK in their regular operations. In this they

need to consider some crucial costs such as:

Standard costing: It is known as basic costing method which a company wants to

estimate to attain during the period of time. This particular cost would be atleast incur at

the time of production of products.

Actual costing: It is said to be one of the essential costing method which is actually

occurs in accordance to produce certain kind of products.

Normal costing: According to this particular costing, this much cost will be incur after

cutting down all costs or expenses.

Inventory management system: It is one of the most effective costing systems which can be

use by managers in order to control and regulate their position of inventory during an accounting

period of time. There are various techniques by which inventory can be managed such as:

2

The data presented in front of management is

based on historical cost that is mainly use for

the purpose of planning in their future

operations.

These are associated with all activities those

are based on past data.

It is not use to evaluate financial and

operations performances of an Tech UK.

This is related with only financial data for the

cited company.

Importance of using types of management accounting systems:

It has been determine that accounting systems are more reliable and appropriate techniques

by which all information can be recorded into their respective format in more effective and

accurate manner. The manager can easily be able to take some crucial decision regarding their

future growth and stability by the help of management accounting systems (Tessier and Otley,

2012). The performance of the company can also be enhancing by using right kind of techniques

in their daily course of actions. It is used to measure all necessary tools and methods for an

organisation through comparing past performance with the current one.

Types of accounting system:

Cost accounting system: It happens to be primary accounting components of

management. They uses this as more reliable system in order to record, summarise and determine

best accurate alternative should be helpful for Tech UK in their regular operations. In this they

need to consider some crucial costs such as:

Standard costing: It is known as basic costing method which a company wants to

estimate to attain during the period of time. This particular cost would be atleast incur at

the time of production of products.

Actual costing: It is said to be one of the essential costing method which is actually

occurs in accordance to produce certain kind of products.

Normal costing: According to this particular costing, this much cost will be incur after

cutting down all costs or expenses.

Inventory management system: It is one of the most effective costing systems which can be

use by managers in order to control and regulate their position of inventory during an accounting

period of time. There are various techniques by which inventory can be managed such as:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LIFO: It is a kind of cost flow assumption which should be used by UK companies in moving

the costs of goods from stock to the prices of products sold. In this the latest and more recent

product purchased are first costs expenditure can be recorded in this system.

FIFO: It is a kind of assets management and valuation techniques in which total assets produce

can be acquire to be sold initially (Lim, 2011).

AVCO: This method is more simple stock evaluation techniques to examine the value of ending

stock and costs of sales on regular basis of average units present for the purpose of sale.

Job costing system: According to this process of assigning the costs which is being incurred

to a particular job and individual and company is associated with. It consists of certain methods

such as:

Batch costing: It is a kind or particular order costing which is much similar to job costing.

With this each batch are number as identical units so that they look identical from one another

(Lavia López and Hiebl, 2014).

Process costing: This seems to be an effective costing methods uses as units of

production in companies those are associated with producing large amount of

homogeneous products.

P2: Various types of reporting method

In every business organisation, they are always aims to product more reliable results by the

help of using appropriate financial data during an accounting period of time. It is essential for an

organisation to make use of reporting methods for the purpose of preparing valuable reports for

the company. The main motive behind formulating this kind of report is to control cost and extra

wastages that are seen in measuring performance of an organisation. On the basis of this report,

investors would be able to make valuable decision regarding their capital investments in

upcoming projects. Some methods are discussed underneath:

Performance report: According to this particular reporting method company would be

able to make comparison of actual performance to with the standard one. This will assist Tech

UK company to determine their current position in terms of finance (Klychova and et. al., 2015).

Account receivable report: This particular method is useful to determine total list of

unpaid customer invoices those are remain outstanding during the period of time. By the help of

this, company can easily be able to analyse total time to collect recovery of payment from

debtors.

3

the costs of goods from stock to the prices of products sold. In this the latest and more recent

product purchased are first costs expenditure can be recorded in this system.

FIFO: It is a kind of assets management and valuation techniques in which total assets produce

can be acquire to be sold initially (Lim, 2011).

AVCO: This method is more simple stock evaluation techniques to examine the value of ending

stock and costs of sales on regular basis of average units present for the purpose of sale.

Job costing system: According to this process of assigning the costs which is being incurred

to a particular job and individual and company is associated with. It consists of certain methods

such as:

Batch costing: It is a kind or particular order costing which is much similar to job costing.

With this each batch are number as identical units so that they look identical from one another

(Lavia López and Hiebl, 2014).

Process costing: This seems to be an effective costing methods uses as units of

production in companies those are associated with producing large amount of

homogeneous products.

P2: Various types of reporting method

In every business organisation, they are always aims to product more reliable results by the

help of using appropriate financial data during an accounting period of time. It is essential for an

organisation to make use of reporting methods for the purpose of preparing valuable reports for

the company. The main motive behind formulating this kind of report is to control cost and extra

wastages that are seen in measuring performance of an organisation. On the basis of this report,

investors would be able to make valuable decision regarding their capital investments in

upcoming projects. Some methods are discussed underneath:

Performance report: According to this particular reporting method company would be

able to make comparison of actual performance to with the standard one. This will assist Tech

UK company to determine their current position in terms of finance (Klychova and et. al., 2015).

Account receivable report: This particular method is useful to determine total list of

unpaid customer invoices those are remain outstanding during the period of time. By the help of

this, company can easily be able to analyse total time to collect recovery of payment from

debtors.

3

Inventory management report: This reporting technique is uses to analyse overall

opening and closing stock position that is being kept by the company during the time. It is

considered as primary report on the basis of which current position as well level of inventory can

easily be determine by the company.

Job cost report: On the basis of this particular report, company is would be able to

analyse total cost and expense a company is being investing in production of one unit of products

from the available resources.

Importance of using reporting method:

It is an effective decision to be made by the managers to make use appropriate reporting

method that can assists an organisation to analyse their total financial position during the

financial year. All the above mentioned reports are having their own benefits and limitation.

Some of them are, performance report is used to compare to actual and past position of Tech UK.

While account receivable report will be essential to make identification of total time to get

outstanding balance from debtors. All of them are uses by the investors and other stakeholders to

collect more specific data from prepared reports (Klemstine and Maher, 2014).

M1: Analyse benefits of using accounting system

In accordance to analyse the performance of Tech UK, specific accounting systems are can

be leads to be used by the managers of that company. It is the capacity of an organisation to

present financial image more clearly to investors and their potential stakeholders. Cost

accounting systems can be more reliable and accurate system that can assist managers to analyse

total cost incur in production process. While inventory management system is use to evaluate

total inventory kept by the company with them.

D1: Critical analysis of reporting system

In respect to attaining more positive outcomes for the company, the managers need to

make use of proper reporting method during the evaluation process. This will help an

organisation to analyse their current position in front of investors. Some of method such as

performance report is use to evaluate actual stage with the standard one. While account

receivable report can make company an ideas about their total recovery period to collect their

outstanding balances.

4

opening and closing stock position that is being kept by the company during the time. It is

considered as primary report on the basis of which current position as well level of inventory can

easily be determine by the company.

Job cost report: On the basis of this particular report, company is would be able to

analyse total cost and expense a company is being investing in production of one unit of products

from the available resources.

Importance of using reporting method:

It is an effective decision to be made by the managers to make use appropriate reporting

method that can assists an organisation to analyse their total financial position during the

financial year. All the above mentioned reports are having their own benefits and limitation.

Some of them are, performance report is used to compare to actual and past position of Tech UK.

While account receivable report will be essential to make identification of total time to get

outstanding balance from debtors. All of them are uses by the investors and other stakeholders to

collect more specific data from prepared reports (Klemstine and Maher, 2014).

M1: Analyse benefits of using accounting system

In accordance to analyse the performance of Tech UK, specific accounting systems are can

be leads to be used by the managers of that company. It is the capacity of an organisation to

present financial image more clearly to investors and their potential stakeholders. Cost

accounting systems can be more reliable and accurate system that can assist managers to analyse

total cost incur in production process. While inventory management system is use to evaluate

total inventory kept by the company with them.

D1: Critical analysis of reporting system

In respect to attaining more positive outcomes for the company, the managers need to

make use of proper reporting method during the evaluation process. This will help an

organisation to analyse their current position in front of investors. Some of method such as

performance report is use to evaluate actual stage with the standard one. While account

receivable report can make company an ideas about their total recovery period to collect their

outstanding balances.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

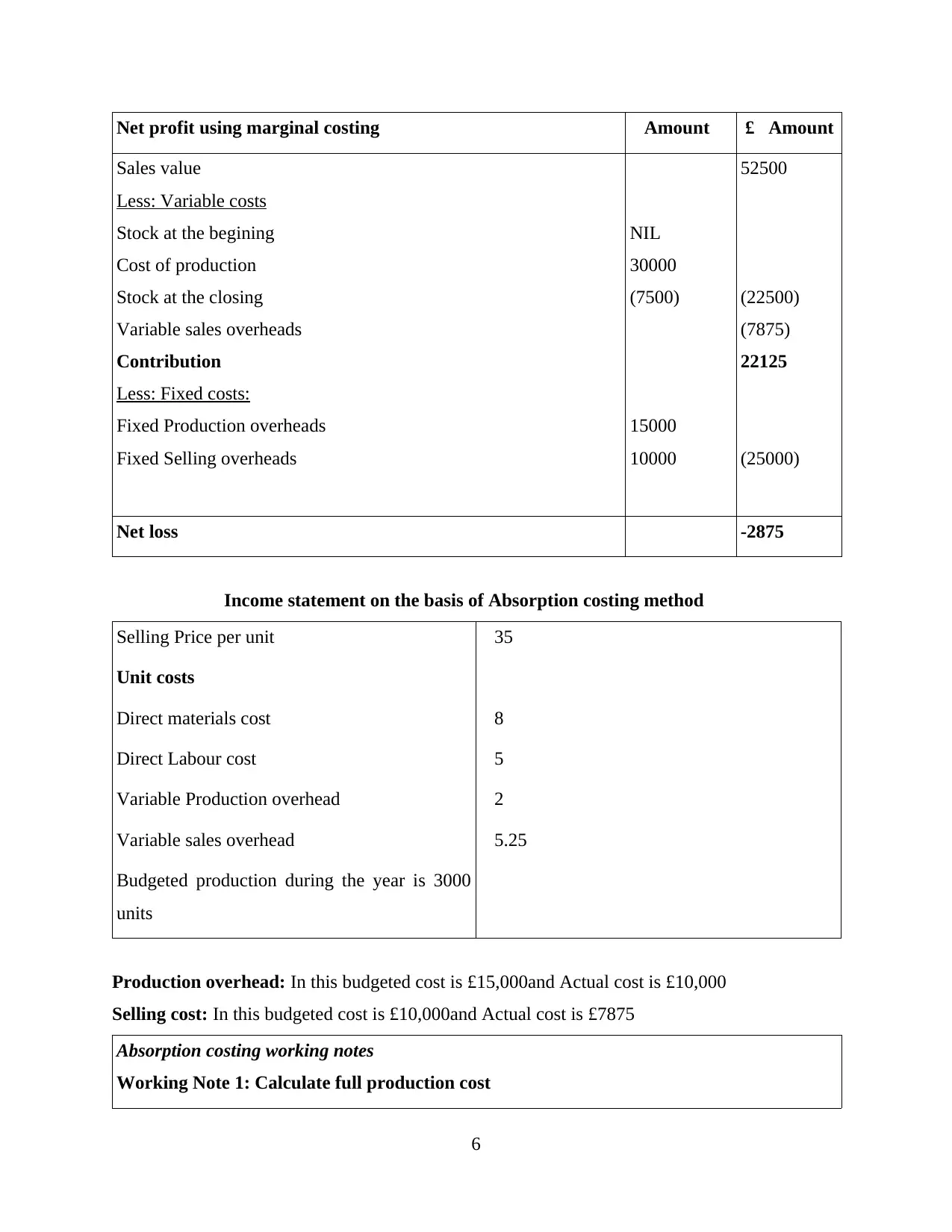

P3: Costing method use to calculate net profitability for the company

Cost is an important tool for an organisation; they can use this to produce products and

services for the purpose of increasing overall growth and sustainability in an accounting period

of time. These costs are direct or indirectly associated with the manufacturing process. There are

various types of costs that can be uses by the managers while making future decision for

increasing goodwill for the company. Some of them are discussed underneath:

Absorption costing: This type of costing techniques is more reliable for evaluating

performance of an organisation (Absorption costing, 2018). In this, all costs are applicable to the

production process. It consists of both variable and fixed costs at the same point of time. Because

of this it is known as full costing methods. It does not be taken as more reliable costing methods

for the purpose of making future decision.

Marginal costing: According to this particular costing a method which is used by an

organisation in the production of one additional products unit. It use to taken into account only

variable costs and fixed costs are not consider while calculating contribution per units. Because

of this, it is said to be period cost. It is more effective and reliable for making future decision

making (JOSHI and et. al., 2011).

Income statement as on September by using Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

5

P3: Costing method use to calculate net profitability for the company

Cost is an important tool for an organisation; they can use this to produce products and

services for the purpose of increasing overall growth and sustainability in an accounting period

of time. These costs are direct or indirectly associated with the manufacturing process. There are

various types of costs that can be uses by the managers while making future decision for

increasing goodwill for the company. Some of them are discussed underneath:

Absorption costing: This type of costing techniques is more reliable for evaluating

performance of an organisation (Absorption costing, 2018). In this, all costs are applicable to the

production process. It consists of both variable and fixed costs at the same point of time. Because

of this it is known as full costing methods. It does not be taken as more reliable costing methods

for the purpose of making future decision.

Marginal costing: According to this particular costing a method which is used by an

organisation in the production of one additional products unit. It use to taken into account only

variable costs and fixed costs are not consider while calculating contribution per units. Because

of this, it is said to be period cost. It is more effective and reliable for making future decision

making (JOSHI and et. al., 2011).

Income statement as on September by using Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net profit using marginal costing £Amount £ Amount

Sales value

Less: Variable costs

Stock at the begining

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

Net loss -2875

Income statement on the basis of Absorption costing method

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production during the year is 3000

units

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

6

Sales value

Less: Variable costs

Stock at the begining

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

Net loss -2875

Income statement on the basis of Absorption costing method

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production during the year is 3000

units

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

6

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit using absorption costings £Amount £Amount

Sales value

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

Net loss -375

7

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit using absorption costings £Amount £Amount

Sales value

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

Net loss -375

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M2: Analysis of using management accounting techniques

It is the company who make decision in respects to use of management accounting tools

and techniques that are beneficial in near future time. There are various accounting techniques

which are more reliable to control the performance of an organisation. Such as standard costing

is the appropriate techniques which can assist project managers to use the cost in effective

manner.

D2: Critical evaluation of collected data in income statements

On the basis of above calculation, it has been seen that there is negative gains attain. The

company have two important option such as marginal and absorption costing. Results are varied

from both the methods. The difference is seen because of fixed cost treatments during the

computation of net profit.

TASK 3

P4: Merits and demerits of using budgets

In every business enterprises, planning is considered to be utmost important aspects. This

can be required to make evaluation of upcoming aims and objectives in more effective manner.

Because of this, Tech UK wants to use various kinds of budgets in their daily business

operations. Some of them are discussed underneath:

Financial budgets: It is known as one of the primary budget that is being prepared by the

accountant in order to analyse current performance and position of the company in comparison to

last year. This is prepared after the end of financial year.

Advantage: This will provide crucial information about all costs and expenses that a

company is investing in regular course of business operations (Brewer, Sorensen and Stout,

2014).

Disadvantage: It does not be control additional expenses or costs those are unpredicted

to the company. It is too costly to prepared budgets always.

Operation budgets: This seems to be an effective budget which will be prepared by an

organization in order to determine total expense a company in investing for the production of one

unit. It can be prepared on regular, weekly, quarterly and yearly basis.

Advantage: These budgets will be able to control performance of operational department

through using minimum costs during the time.

8

It is the company who make decision in respects to use of management accounting tools

and techniques that are beneficial in near future time. There are various accounting techniques

which are more reliable to control the performance of an organisation. Such as standard costing

is the appropriate techniques which can assist project managers to use the cost in effective

manner.

D2: Critical evaluation of collected data in income statements

On the basis of above calculation, it has been seen that there is negative gains attain. The

company have two important option such as marginal and absorption costing. Results are varied

from both the methods. The difference is seen because of fixed cost treatments during the

computation of net profit.

TASK 3

P4: Merits and demerits of using budgets

In every business enterprises, planning is considered to be utmost important aspects. This

can be required to make evaluation of upcoming aims and objectives in more effective manner.

Because of this, Tech UK wants to use various kinds of budgets in their daily business

operations. Some of them are discussed underneath:

Financial budgets: It is known as one of the primary budget that is being prepared by the

accountant in order to analyse current performance and position of the company in comparison to

last year. This is prepared after the end of financial year.

Advantage: This will provide crucial information about all costs and expenses that a

company is investing in regular course of business operations (Brewer, Sorensen and Stout,

2014).

Disadvantage: It does not be control additional expenses or costs those are unpredicted

to the company. It is too costly to prepared budgets always.

Operation budgets: This seems to be an effective budget which will be prepared by an

organization in order to determine total expense a company in investing for the production of one

unit. It can be prepared on regular, weekly, quarterly and yearly basis.

Advantage: These budgets will be able to control performance of operational department

through using minimum costs during the time.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Disadvantage: The main limitation of this budget is that, it is too time consuming or

need to make more than one reports such as sales, raw material and production budgets.

Process of budget:

Estimation of budgets idea: It is necessary to make proper idea about requirement of

budget after that process of preparation can be started.

Check availability of capital: The next objective is to make examination of various

sources from which funds can be collected.

Develop budget package: It is vital for the managers to make proper package which is

affordable to the company (Bennett, Schaltegger and Zvezdov, 2013).

Obtain revenue forecast: It happens to be earning predication from total sales done during

an accounting period of time.

Collection of capital budget request: It is essential to make proper capital budget request

and transfer it to the upper level.

Udate budget model: In this particular process, proper analysis of budget data in the form

of final budget is needed to take into account.

Review of budget: It is last process in which collection of appropriate feedbacks from

employees to make order to prepare budgets for the company.

Pricing policy: There are various types of pricing policies needed to be taken into consideration.

Some of them are discussed underneath:

Price skimming: It consist of setting up of cost in the beginning stage of a new products

which is more high as compare to other companies product.

Cost based pricing: It is known as utmost important and simple tools through which a

product can be placed in more accurate manner. It consists of two major aspects such as

direct cost and marginal costing.

Importance of budget tools and objectives:

It is utmost important part for an organisation which is prepared for the purpose of

controlling all impacts those are going to be arises in coming future time. The main aims of using

all the above budgets are to control wastages and frauds that are occur in an organisation.

M3: Analysis of various planning tools

There are various tool and techniques which are helpful for an organisation to control their

budgets. Some of them are forecasting tools that is used to examine upcoming expenses and

9

need to make more than one reports such as sales, raw material and production budgets.

Process of budget:

Estimation of budgets idea: It is necessary to make proper idea about requirement of

budget after that process of preparation can be started.

Check availability of capital: The next objective is to make examination of various

sources from which funds can be collected.

Develop budget package: It is vital for the managers to make proper package which is

affordable to the company (Bennett, Schaltegger and Zvezdov, 2013).

Obtain revenue forecast: It happens to be earning predication from total sales done during

an accounting period of time.

Collection of capital budget request: It is essential to make proper capital budget request

and transfer it to the upper level.

Udate budget model: In this particular process, proper analysis of budget data in the form

of final budget is needed to take into account.

Review of budget: It is last process in which collection of appropriate feedbacks from

employees to make order to prepare budgets for the company.

Pricing policy: There are various types of pricing policies needed to be taken into consideration.

Some of them are discussed underneath:

Price skimming: It consist of setting up of cost in the beginning stage of a new products

which is more high as compare to other companies product.

Cost based pricing: It is known as utmost important and simple tools through which a

product can be placed in more accurate manner. It consists of two major aspects such as

direct cost and marginal costing.

Importance of budget tools and objectives:

It is utmost important part for an organisation which is prepared for the purpose of

controlling all impacts those are going to be arises in coming future time. The main aims of using

all the above budgets are to control wastages and frauds that are occur in an organisation.

M3: Analysis of various planning tools

There are various tool and techniques which are helpful for an organisation to control their

budgets. Some of them are forecasting tools that is used to examine upcoming expenses and

9

costs. While contiegency tools are used to analyse all the risks factors those are presented in an

organisation.

D3: Critical evaluation of financial issues

In every business, there are some types of financial problems are happen which can make

huge impacts on the growth and stability of the company. In order to reduce them, accountant

needs to make used of balance scorecard approaches to deal with them in more effective manner.

TASK 4

P5: Balance scorecard approach

According to the presented case study about TECH UK LTD which is currently established

in their financial statements for the accounting year that is showing total loss of 1.5 million. The

company wants to reduce all the impacts that are arise because of these particular problems. The

accountant has suggested making use of balance scorecard method to deal with all issues. It

consists of various perspectives. Such as:

Financial: It is an important prospective which is associated with organization financial position

and their effective utilisation of resource in evaluation of performance of the company.

Customers and other stakeholders: It is responsible for analysing organisation performance

from the customer’s point of views. The main motive is to create wealth and interest to

stakeholders (Amoako, 2013).

Internal process: According to this, the organisation operation is views from the quality and

efficiency associated to their products and services delivery by the company.

Organisational capacity: It is analyse through using proper evaluation of human capital,

infrastructure, technology, culture and other important aspects.

M4: Analysis of financial problems

In accordance to overcome all the issues those are presented in Tech UK Ltd, managers

would need to apply all vital financial tools those are effective enough to defeat in more quick

time. Some of them are Key performance indicators; financial governance and benchmarking are

correct option for the company.

10

organisation.

D3: Critical evaluation of financial issues

In every business, there are some types of financial problems are happen which can make

huge impacts on the growth and stability of the company. In order to reduce them, accountant

needs to make used of balance scorecard approaches to deal with them in more effective manner.

TASK 4

P5: Balance scorecard approach

According to the presented case study about TECH UK LTD which is currently established

in their financial statements for the accounting year that is showing total loss of 1.5 million. The

company wants to reduce all the impacts that are arise because of these particular problems. The

accountant has suggested making use of balance scorecard method to deal with all issues. It

consists of various perspectives. Such as:

Financial: It is an important prospective which is associated with organization financial position

and their effective utilisation of resource in evaluation of performance of the company.

Customers and other stakeholders: It is responsible for analysing organisation performance

from the customer’s point of views. The main motive is to create wealth and interest to

stakeholders (Amoako, 2013).

Internal process: According to this, the organisation operation is views from the quality and

efficiency associated to their products and services delivery by the company.

Organisational capacity: It is analyse through using proper evaluation of human capital,

infrastructure, technology, culture and other important aspects.

M4: Analysis of financial problems

In accordance to overcome all the issues those are presented in Tech UK Ltd, managers

would need to apply all vital financial tools those are effective enough to defeat in more quick

time. Some of them are Key performance indicators; financial governance and benchmarking are

correct option for the company.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.