Management Accounting Report: Systems, Methods and Planning Tools

VerifiedAdded on 2020/12/09

|19

|4723

|454

Report

AI Summary

This report analyzes various aspects of management accounting, focusing on its application within the context of R.L. Maynard, a property construction and development SME. It delves into different management accounting systems, including cost accounting, inventory management, job-costing, and price-optimizing systems, outlining their definitions, requirements, and benefits. The report also examines the types of management accounting reports, such as accounts receivable, budgeting, inventory, performance, and job cost reports, emphasizing their significance to management. Furthermore, it explores the integration between management accounting systems and reporting, along with an in-depth discussion of absorption and marginal costing methods. The report concludes by evaluating planning tools for budgetary control, their advantages and disadvantages, and their role in resolving financial problems, providing a comprehensive overview of management accounting principles and practices.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A) Definition of management accounting and requirements of different types of management

accounting systems.................................................................................................................1

Types of management accounting reports and the importance of such reports to management.

................................................................................................................................................2

C) Evaluate the benefits of different management accounting systems.................................3

D) How the management accounting systems and management accounting reporting are

integrated................................................................................................................................4

TASK 2............................................................................................................................................6

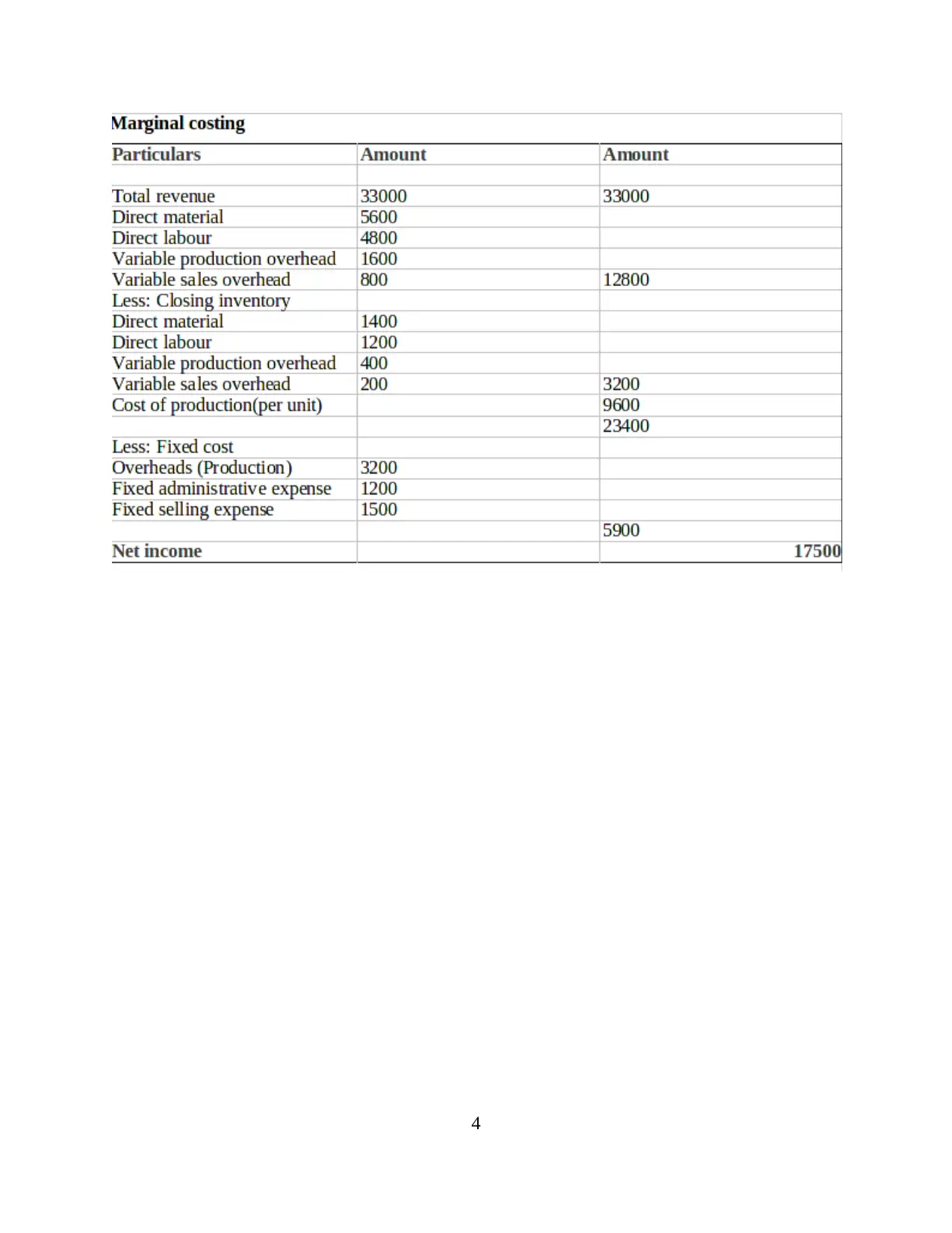

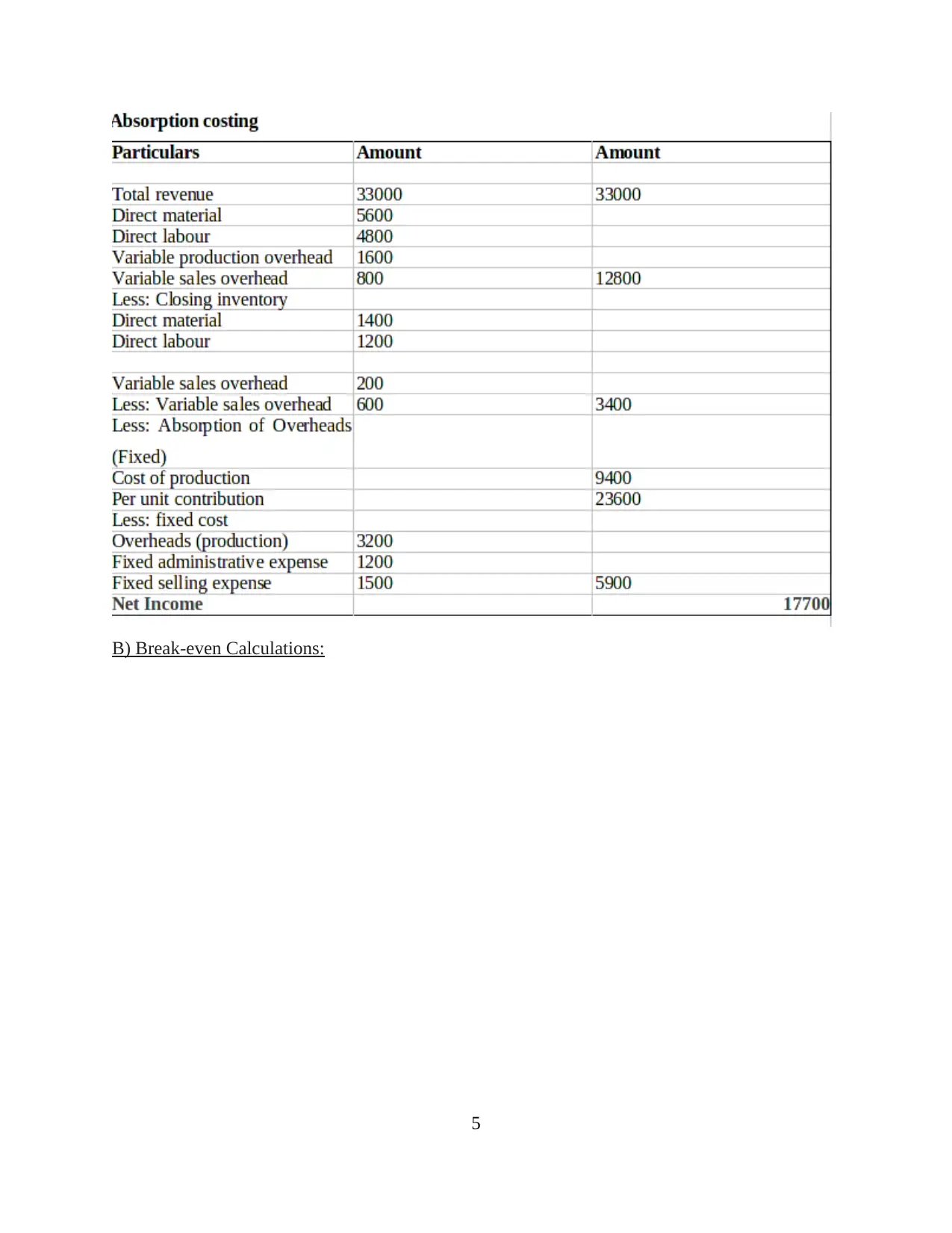

A) Absorption costing and marginal costing methods. .........................................................6

................................................................................................................................................7

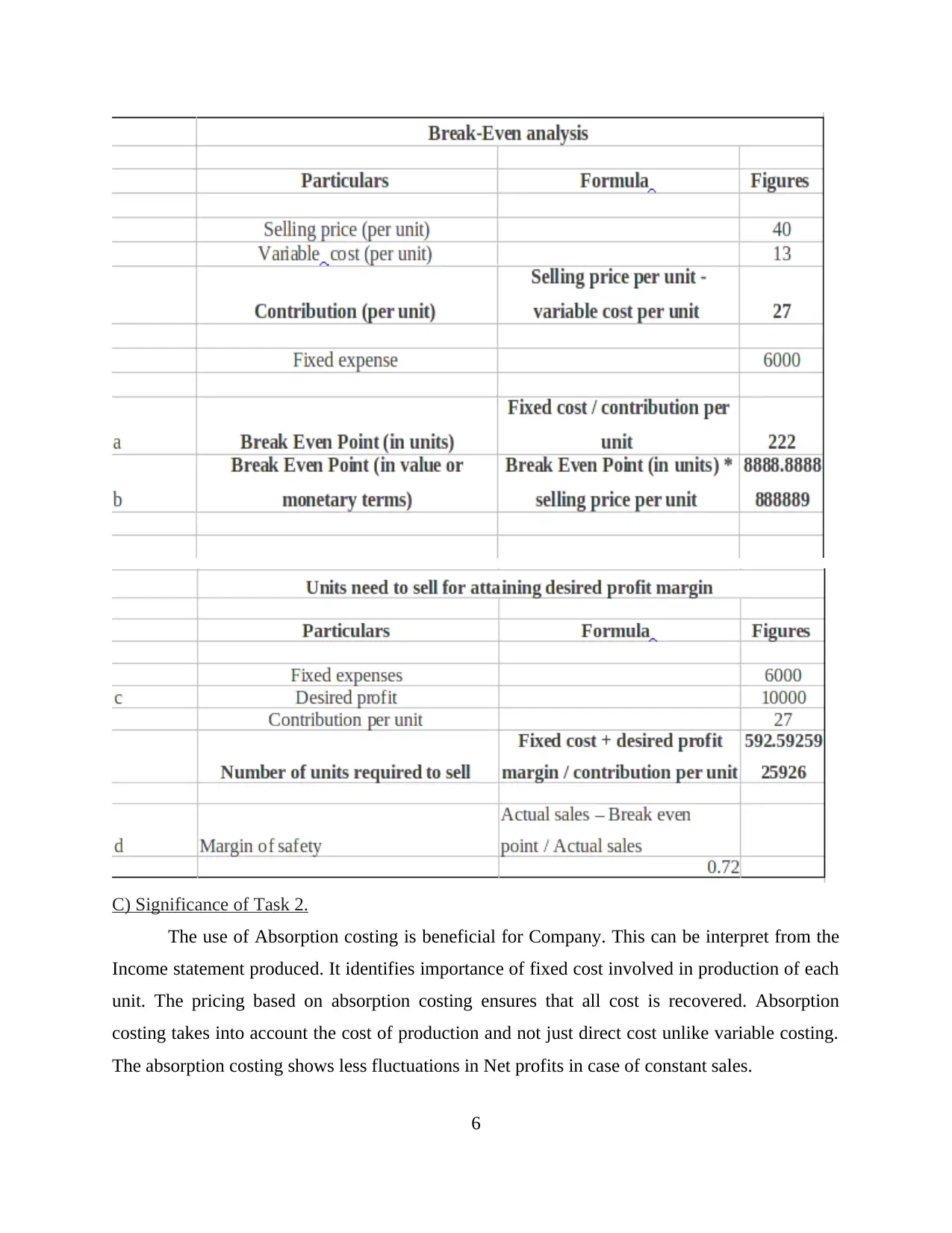

B) Break-even Calculations:...................................................................................................7

................................................................................................................................................8

C) Significance of Task 2.......................................................................................................8

D) Produce financial report....................................................................................................8

TASK 3............................................................................................................................................8

A) Advantages and disadvantages of different types of planning tools for budgetary control..8

B)Planning tools for preparing, forecasting and analysing budgets. ...................................10

B)Role of management accounting systems in reducing financial problems. ....................10

E) How Planning tools help in resolving financial problems.............................................12

CONCLUSION..............................................................................................................................12

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A) Definition of management accounting and requirements of different types of management

accounting systems.................................................................................................................1

Types of management accounting reports and the importance of such reports to management.

................................................................................................................................................2

C) Evaluate the benefits of different management accounting systems.................................3

D) How the management accounting systems and management accounting reporting are

integrated................................................................................................................................4

TASK 2............................................................................................................................................6

A) Absorption costing and marginal costing methods. .........................................................6

................................................................................................................................................7

B) Break-even Calculations:...................................................................................................7

................................................................................................................................................8

C) Significance of Task 2.......................................................................................................8

D) Produce financial report....................................................................................................8

TASK 3............................................................................................................................................8

A) Advantages and disadvantages of different types of planning tools for budgetary control..8

B)Planning tools for preparing, forecasting and analysing budgets. ...................................10

B)Role of management accounting systems in reducing financial problems. ....................10

E) How Planning tools help in resolving financial problems.............................................12

CONCLUSION..............................................................................................................................12

REFERENCES................................................................................................................................1

INTRODUCTION

Management Accounting refers to process of preparing of reports and accounts that

provides timely financial information to managers and helps them in taking day-to-day decisions.

This report discusses about different types of Management Accounting Systems. It discuss how

management reports are integrated with management systems. Further, The advantages and

disadvantages of using different types of Planning Tools for budgetary control and the

application of different tools for planning, preparing and analysing budget. R.L. Maynard is a

Small and Medium-Sized Enterprise established in 1973. It is engaged in property construction

and development business for past 45 years.

TASK 1.

A) Management Accounting and requirements of different types of management accounting

systems

Management accounting refers to presentation of accounting information that provides

accurate and timely financial and statistical information, which is required by managers to make

short-term decisions. It differs from financial accounting, which produces annual reports external

parties or stakeholders. Whereas Management Accounting generates monthly or weekly reports

that is used by organisation for their internal users like; department heads, CEO. The report

presented by management accounting includes details of Cash held by company, Sales revenue

or income generated by firm, current status of firm such as Account Payable and Receivable etc.

Importances of different types of Management Accounting Systems are as follows:

Cost Accounting Systems: It refers to framework used by companies to estimate cost

associated with their products in order to perform profitability analysis, inventory

valuation and cost control. It is crucial aspect as estimating accurate cost of raw materials

which go through production stages and slowly turned down into finished products. Cost

Accounting system helps R.L. Maynard to know which products are profitable in

construction purpose. It helps company in preparing financial report by estimating

closing value of materials, inventory, work-in-progress and finished goods (Ax and

Greve, 2017).

Inventory Management Systems: It refers to combination of technology, procedures

and process, which look over maintenance of stock or inventory held by company. This

helps R.L. Maynard to enhance their transparency. Company can achieve better reporting

1

Management Accounting refers to process of preparing of reports and accounts that

provides timely financial information to managers and helps them in taking day-to-day decisions.

This report discusses about different types of Management Accounting Systems. It discuss how

management reports are integrated with management systems. Further, The advantages and

disadvantages of using different types of Planning Tools for budgetary control and the

application of different tools for planning, preparing and analysing budget. R.L. Maynard is a

Small and Medium-Sized Enterprise established in 1973. It is engaged in property construction

and development business for past 45 years.

TASK 1.

A) Management Accounting and requirements of different types of management accounting

systems

Management accounting refers to presentation of accounting information that provides

accurate and timely financial and statistical information, which is required by managers to make

short-term decisions. It differs from financial accounting, which produces annual reports external

parties or stakeholders. Whereas Management Accounting generates monthly or weekly reports

that is used by organisation for their internal users like; department heads, CEO. The report

presented by management accounting includes details of Cash held by company, Sales revenue

or income generated by firm, current status of firm such as Account Payable and Receivable etc.

Importances of different types of Management Accounting Systems are as follows:

Cost Accounting Systems: It refers to framework used by companies to estimate cost

associated with their products in order to perform profitability analysis, inventory

valuation and cost control. It is crucial aspect as estimating accurate cost of raw materials

which go through production stages and slowly turned down into finished products. Cost

Accounting system helps R.L. Maynard to know which products are profitable in

construction purpose. It helps company in preparing financial report by estimating

closing value of materials, inventory, work-in-progress and finished goods (Ax and

Greve, 2017).

Inventory Management Systems: It refers to combination of technology, procedures

and process, which look over maintenance of stock or inventory held by company. This

helps R.L. Maynard to enhance their transparency. Company can achieve better reporting

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and forecasting capabilities, which reduces the storage cost of inventory held by R.L.

Maynard.

Job-costing systems: In this system, manufacturing cost is assigned to each individual

product or different batches of products. It is a useful tool for R.L. Maynard as it is

engaged in property construction business as each building developed by firm is unique

and it helps the company as job cost report direct materials and labour which utilised and

manufacturing overhead assigned to each job (Bromwich and Scapens, 2016).

Price-optimising systems: It is a mathematical analysis used by company to predict

how consumers will react to different prices for product/services of company when

offered through different channels. This help company to predict the revenue and margin

outcome for their products.

Types of management accounting reports and the importance of such reports to management

The management accounting reports help managers in preparing appropriate management

reports, which help company to forecast current situation for making cr The use of Absorption

costing is beneficial for Company. This can be interpret from the Income statement produced. It

identifies importance of fixed cost involved in production of each unit. The pricing based on

absorption costing ensures that all cost is recovered. Absorption costing takes into account the

cost of production and not just direct cost unlike variable costing. The absorption costing shows

less fluctuations in Net profits in case of constant sales.

Marginal costing helps determining and controlling cost of production. It prevents

arbitrary allocation of fixed cost which helps management to concentrate on achieving and

maintaining a uniform cost. As fixed overheads are not charged to cost of production each units

produced have standard cost assign to it. itical business decision.

These reports are as follows:

Accounts Receivable or Ageing Report: These reports are used to facilitate in

managing account for those companies who are engaged in extending the credits to their

consumers. It helps to review and monitor the status of the receivables, open credits,

finance charges and credit refunds (Chiwamit, Modell and Scapens, 2017)

Budgeting Report: It has been formulated to set out the plan for evaluating company

performance by making evaluation of departmental performance and control costs. These

are financial goals based on estimates and future projections. These budget reports are

2

Maynard.

Job-costing systems: In this system, manufacturing cost is assigned to each individual

product or different batches of products. It is a useful tool for R.L. Maynard as it is

engaged in property construction business as each building developed by firm is unique

and it helps the company as job cost report direct materials and labour which utilised and

manufacturing overhead assigned to each job (Bromwich and Scapens, 2016).

Price-optimising systems: It is a mathematical analysis used by company to predict

how consumers will react to different prices for product/services of company when

offered through different channels. This help company to predict the revenue and margin

outcome for their products.

Types of management accounting reports and the importance of such reports to management

The management accounting reports help managers in preparing appropriate management

reports, which help company to forecast current situation for making cr The use of Absorption

costing is beneficial for Company. This can be interpret from the Income statement produced. It

identifies importance of fixed cost involved in production of each unit. The pricing based on

absorption costing ensures that all cost is recovered. Absorption costing takes into account the

cost of production and not just direct cost unlike variable costing. The absorption costing shows

less fluctuations in Net profits in case of constant sales.

Marginal costing helps determining and controlling cost of production. It prevents

arbitrary allocation of fixed cost which helps management to concentrate on achieving and

maintaining a uniform cost. As fixed overheads are not charged to cost of production each units

produced have standard cost assign to it. itical business decision.

These reports are as follows:

Accounts Receivable or Ageing Report: These reports are used to facilitate in

managing account for those companies who are engaged in extending the credits to their

consumers. It helps to review and monitor the status of the receivables, open credits,

finance charges and credit refunds (Chiwamit, Modell and Scapens, 2017)

Budgeting Report: It has been formulated to set out the plan for evaluating company

performance by making evaluation of departmental performance and control costs. These

are financial goals based on estimates and future projections. These budget reports are

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

used to provide incentives to employees and motivate them to achieve goals and

objectives of R.L. Maynard.

Inventory Report: It includes summary of items belonging to a company. Inventory

Report provides a comprehensive account of stock or supply of various items. These

reports contain per unit overhead costs, wastage concerned with inventory and labour

cost, which provides manager of R.L. Maynard to see opportunities of improvement that

can be utilised by their employees.

Performance Report: It refers to detailed statement that measures results of different

activities in terms of its success for a given time period. They are generally prepared

annually but if a company want it can make performance report monthly or weekly as per

their requirement.

Job Cost Report: The report listed job costs that is incurred on each project. It is

concerned with identifying expenses, cost and profitability related to particular job. Job

cost report evaluates cost even when a project is in progress so that unprofitable or

wastage areas can be eliminated and project can be made more workable (Fullerton and

et. al., 2014).

C) Benefits of different management accounting systems

Advantages of different management accounting system are as follows:

Cost accounting systems

Cost accounting system helps R.L. Maynard to eliminate losses and inefficiencies by

fixing standard for tasks. Company can take necessary steps in order to eliminate those

activities, which generates little or no benefits to company.

It provides information upon which estimates and tenders are based. Thus, it is an

essential tool for R.L. Maynard as company is engaged in Construction business and

information provided by cost accounting can be very useful for them.

Cost accounting system helps in generating more profits to organisation as unprofitable

activities are eliminated (Hall, 2016).

Costs of labour are easy to control and monitor through this accounting system as R.L.

Maynard can utilise cost accounting system to estimate efficiency and productivity.

3

objectives of R.L. Maynard.

Inventory Report: It includes summary of items belonging to a company. Inventory

Report provides a comprehensive account of stock or supply of various items. These

reports contain per unit overhead costs, wastage concerned with inventory and labour

cost, which provides manager of R.L. Maynard to see opportunities of improvement that

can be utilised by their employees.

Performance Report: It refers to detailed statement that measures results of different

activities in terms of its success for a given time period. They are generally prepared

annually but if a company want it can make performance report monthly or weekly as per

their requirement.

Job Cost Report: The report listed job costs that is incurred on each project. It is

concerned with identifying expenses, cost and profitability related to particular job. Job

cost report evaluates cost even when a project is in progress so that unprofitable or

wastage areas can be eliminated and project can be made more workable (Fullerton and

et. al., 2014).

C) Benefits of different management accounting systems

Advantages of different management accounting system are as follows:

Cost accounting systems

Cost accounting system helps R.L. Maynard to eliminate losses and inefficiencies by

fixing standard for tasks. Company can take necessary steps in order to eliminate those

activities, which generates little or no benefits to company.

It provides information upon which estimates and tenders are based. Thus, it is an

essential tool for R.L. Maynard as company is engaged in Construction business and

information provided by cost accounting can be very useful for them.

Cost accounting system helps in generating more profits to organisation as unprofitable

activities are eliminated (Hall, 2016).

Costs of labour are easy to control and monitor through this accounting system as R.L.

Maynard can utilise cost accounting system to estimate efficiency and productivity.

3

Inventory management systems

The effective inventory system helps in raising operating performance, which leads to

more productivity.

It protects R.L. Maynard against variations in raw material and delivery time.

Inventory management system helps to minimise losses that occur due to obsolescence,

deterioration, damage, etc as R.L. Maynard is engaged in property construction as it

needs to keep their building materials safe from getting damaged.

Job-costing systems

Revenue generated from each job is known separately in this system.

It helps managers of R.L. Maynard to estimate cost of job on basis of past records and

actual cost of previous job can be compared with those records.

Ineffective work can be identified with specific job and responsibilities for it can be fixed

over individuals.

Price-optimising systems

This system helps company to realise reaction of customer for different price beforehand

and thus, it can evaluate price that their clients are ready to pay for their work.

It helps company drive customers to their services and increases their margin growth.

D) Management accounting systems and management accounting reporting are integrated

Management Accounting system are interlinked to management reports. These systems

help managers with required information to prepare reports.

R.L. Maynard uses these management accounting systems that are as follows:

Cost accounting systems: It is a management accounting system that aims to capture a

company’s cost of production by assessing the cost of their products for purpose of

inventory evaluation, cost control and profitability analysis. They provide required

information to manager on whether to make or buy a product in open market. R.L.

Maynard is an active company that deals in property construction thus it is important for

managers of company to decide whether construction materials can be manufactured

within an organisation itself or it needs to buy the raw materials. Managers can used the

information to make Purchase Report for different materials (Saeidi, and et. al., 2018).

Further, information generated by cost accounting system helps managers to

formulate cost reports. However, at times information generated by these reports are

1

The effective inventory system helps in raising operating performance, which leads to

more productivity.

It protects R.L. Maynard against variations in raw material and delivery time.

Inventory management system helps to minimise losses that occur due to obsolescence,

deterioration, damage, etc as R.L. Maynard is engaged in property construction as it

needs to keep their building materials safe from getting damaged.

Job-costing systems

Revenue generated from each job is known separately in this system.

It helps managers of R.L. Maynard to estimate cost of job on basis of past records and

actual cost of previous job can be compared with those records.

Ineffective work can be identified with specific job and responsibilities for it can be fixed

over individuals.

Price-optimising systems

This system helps company to realise reaction of customer for different price beforehand

and thus, it can evaluate price that their clients are ready to pay for their work.

It helps company drive customers to their services and increases their margin growth.

D) Management accounting systems and management accounting reporting are integrated

Management Accounting system are interlinked to management reports. These systems

help managers with required information to prepare reports.

R.L. Maynard uses these management accounting systems that are as follows:

Cost accounting systems: It is a management accounting system that aims to capture a

company’s cost of production by assessing the cost of their products for purpose of

inventory evaluation, cost control and profitability analysis. They provide required

information to manager on whether to make or buy a product in open market. R.L.

Maynard is an active company that deals in property construction thus it is important for

managers of company to decide whether construction materials can be manufactured

within an organisation itself or it needs to buy the raw materials. Managers can used the

information to make Purchase Report for different materials (Saeidi, and et. al., 2018).

Further, information generated by cost accounting system helps managers to

formulate cost reports. However, at times information generated by these reports are

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

insufficient as past performances are recorded in cost reports. And this is utilised by

managers to take decisions for future activities. Moreover, cost is ascertained on basis

of utilization of capacity. If capacity is partly generated then cost may not be true.

Inventory management systems: It refers to using combination of technology and

process of moving parts and products of company from their warehouses to different

locations of company. Data provided by Inventory Management System helps Managers

of R.L. Maynard to formulate Inventory Report showing the needs of different raw

materials and other equipments required for construction project. Moreover, the

information provided by this system helps to formulate adequate report showing how

much stock of particular material is left in the warehouse of company. This helps to

minimise capital investments on inventory. It provides scientific basis for planning of

inventory needs and help in maintaining reasonable safety stock at time of crisis.

However, managers cannot entirely depend upon the inventory management

system as it only reduces business risk and not eliminate it. The process of inventory

management is quite complex and time consuming. Company needs to install Inventory

management software, which may result in additional cost. Job-costing systems: This is a system used to assign manufacturing or job cost to each

product while keeping track on expense monitoring. Data received through job costing

system helps Manager to create Job Cost Report. This report includes cost related to each

job that helps Manager of R.L. Maynard to calculate profit margin for each job. Job

Costing System helps to calculate indirect cost such as manufacturing overhead. This

help manager to transfer a complex calculation process into simple operations which

further help them in faster preparation of Management Report.

The demerit of job costing is that accurate report is not obtained due to large

number of jobs are executed at time in job costing. Managers are not able to formulate

adequate report. Further, comparison of job costs become meaningless for company at

time of Inflation in economy (What are the advantages of Job Costing?, 2018).

Price-optimising systems: It helps to create that price which consumers are willing to

pay for products/services of a company. This helps company to formulate Sales Report

for assessing the sale target and budget. The system helps to set different prices for

2

managers to take decisions for future activities. Moreover, cost is ascertained on basis

of utilization of capacity. If capacity is partly generated then cost may not be true.

Inventory management systems: It refers to using combination of technology and

process of moving parts and products of company from their warehouses to different

locations of company. Data provided by Inventory Management System helps Managers

of R.L. Maynard to formulate Inventory Report showing the needs of different raw

materials and other equipments required for construction project. Moreover, the

information provided by this system helps to formulate adequate report showing how

much stock of particular material is left in the warehouse of company. This helps to

minimise capital investments on inventory. It provides scientific basis for planning of

inventory needs and help in maintaining reasonable safety stock at time of crisis.

However, managers cannot entirely depend upon the inventory management

system as it only reduces business risk and not eliminate it. The process of inventory

management is quite complex and time consuming. Company needs to install Inventory

management software, which may result in additional cost. Job-costing systems: This is a system used to assign manufacturing or job cost to each

product while keeping track on expense monitoring. Data received through job costing

system helps Manager to create Job Cost Report. This report includes cost related to each

job that helps Manager of R.L. Maynard to calculate profit margin for each job. Job

Costing System helps to calculate indirect cost such as manufacturing overhead. This

help manager to transfer a complex calculation process into simple operations which

further help them in faster preparation of Management Report.

The demerit of job costing is that accurate report is not obtained due to large

number of jobs are executed at time in job costing. Managers are not able to formulate

adequate report. Further, comparison of job costs become meaningless for company at

time of Inflation in economy (What are the advantages of Job Costing?, 2018).

Price-optimising systems: It helps to create that price which consumers are willing to

pay for products/services of a company. This helps company to formulate Sales Report

for assessing the sale target and budget. The system helps to set different prices for

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

multiple products used by companies while constructing a building. More over, this help

to evaluate competitors’ strategies and pricing which is used by them.

Drawbacks of Price Optimisation System that demands may not fluctuate at

different price levels. It is a complicated process and time consuming which affects in

preperation of Management Report.

TASK 2.

A) Absorption costing and marginal costing methods.

Absorption costing is a cost accounting method for valuing inventory. In this method,

inventory is valued by assigning all fixed and variable manufacturing costs to product. The

finished unit in inventory will include direct materials, labour and both variable and fixed

manufacturing overhead. Due to this reason Absorption costing is all termed as full costing

method. It is required by Accounting Standards to create an inventory valuation. The key cost

assigned to products in absorption costing are Direct Materials, Labour, Fixed manufacturing

overhead and variable manufacturing Overhead (Wagenhofer, 2016).

Marginal Costing is the accounting principles in which variable cost is charged on units

of cost and fixed costs of particular period is written off in full against the aggregate

contribution. In simple words, Marginal Costing refers to additional cost involved in producing

an extra unit of output.

3

to evaluate competitors’ strategies and pricing which is used by them.

Drawbacks of Price Optimisation System that demands may not fluctuate at

different price levels. It is a complicated process and time consuming which affects in

preperation of Management Report.

TASK 2.

A) Absorption costing and marginal costing methods.

Absorption costing is a cost accounting method for valuing inventory. In this method,

inventory is valued by assigning all fixed and variable manufacturing costs to product. The

finished unit in inventory will include direct materials, labour and both variable and fixed

manufacturing overhead. Due to this reason Absorption costing is all termed as full costing

method. It is required by Accounting Standards to create an inventory valuation. The key cost

assigned to products in absorption costing are Direct Materials, Labour, Fixed manufacturing

overhead and variable manufacturing Overhead (Wagenhofer, 2016).

Marginal Costing is the accounting principles in which variable cost is charged on units

of cost and fixed costs of particular period is written off in full against the aggregate

contribution. In simple words, Marginal Costing refers to additional cost involved in producing

an extra unit of output.

3

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

B) Break-even Calculations:

5

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

C) Significance of Task 2.

The use of Absorption costing is beneficial for Company. This can be interpret from the

Income statement produced. It identifies importance of fixed cost involved in production of each

unit. The pricing based on absorption costing ensures that all cost is recovered. Absorption

costing takes into account the cost of production and not just direct cost unlike variable costing.

The absorption costing shows less fluctuations in Net profits in case of constant sales.

6

The use of Absorption costing is beneficial for Company. This can be interpret from the

Income statement produced. It identifies importance of fixed cost involved in production of each

unit. The pricing based on absorption costing ensures that all cost is recovered. Absorption

costing takes into account the cost of production and not just direct cost unlike variable costing.

The absorption costing shows less fluctuations in Net profits in case of constant sales.

6

Marginal costing helps determining and controlling cost of production. It prevents

arbitrary allocation of fixed cost which helps management to concentrate on achieving and

maintaining a uniform cost. As fixed overheads are not charged to cost of production each units

produced have standard cost assign to it.

D) Produce financial report.

It provides specific details of producing and selling a single product. In the above case, it

has applied two methods i.e. Absorption and Marginal Costing. By considering Absorption

costing production variable is not considered so the cost of production represented by 9400 per

unit. Where as, in marginal costing along with all the variables it given outcome of 3200 which

gives production cost as 9600. By evaluating Income statement, Absorption cost has given more

profit margins i.e. by 200 pounds. This means this costing method should be applied in the

Company.

In above case, break Even point analysis, new product has been introduced in the market

whose selling price per unit is 40 and variable is 13. This shows contribution of 27 per unit and

altering adjustment of fixed cost is also used. The extracting number of products, which are sold

The use of Absorption costing is beneficial for Company. This can be interpret from the

Income statement produced. It identifies importance of fixed cost involved in production of each

unit. The pricing based on absorption costing ensures that all cost is recovered. Absorption

costing takes into account the cost of production and not just direct cost unlike variable costing.

The absorption costing shows less fluctuations in Net profits in case of constant sales.

Marginal costing helps determining and controlling cost of production. It prevents

arbitrary allocation of fixed cost which helps management to concentrate on achieving and

maintaining a uniform cost. As fixed overheads are not charged to cost of production each units

produced have standard cost assign to it. As break even, is 222 whose sales revenue is 8888.89.

In same series desired profits are about 10000 there is a requirement for selling 592.60 products.

TASK 3

A) Advantages and disadvantages of different types of planning tools for budgetary control

Activity based budgeting

It refers to planning system under which costs are related with activities and budgeted

expenditure is then compiled depending upon the expected activity level. This perspective is very

7

arbitrary allocation of fixed cost which helps management to concentrate on achieving and

maintaining a uniform cost. As fixed overheads are not charged to cost of production each units

produced have standard cost assign to it.

D) Produce financial report.

It provides specific details of producing and selling a single product. In the above case, it

has applied two methods i.e. Absorption and Marginal Costing. By considering Absorption

costing production variable is not considered so the cost of production represented by 9400 per

unit. Where as, in marginal costing along with all the variables it given outcome of 3200 which

gives production cost as 9600. By evaluating Income statement, Absorption cost has given more

profit margins i.e. by 200 pounds. This means this costing method should be applied in the

Company.

In above case, break Even point analysis, new product has been introduced in the market

whose selling price per unit is 40 and variable is 13. This shows contribution of 27 per unit and

altering adjustment of fixed cost is also used. The extracting number of products, which are sold

The use of Absorption costing is beneficial for Company. This can be interpret from the

Income statement produced. It identifies importance of fixed cost involved in production of each

unit. The pricing based on absorption costing ensures that all cost is recovered. Absorption

costing takes into account the cost of production and not just direct cost unlike variable costing.

The absorption costing shows less fluctuations in Net profits in case of constant sales.

Marginal costing helps determining and controlling cost of production. It prevents

arbitrary allocation of fixed cost which helps management to concentrate on achieving and

maintaining a uniform cost. As fixed overheads are not charged to cost of production each units

produced have standard cost assign to it. As break even, is 222 whose sales revenue is 8888.89.

In same series desired profits are about 10000 there is a requirement for selling 592.60 products.

TASK 3

A) Advantages and disadvantages of different types of planning tools for budgetary control

Activity based budgeting

It refers to planning system under which costs are related with activities and budgeted

expenditure is then compiled depending upon the expected activity level. This perspective is very

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.