Management Accounting Report: Performance, Budgeting, and Variance

VerifiedAdded on 2020/01/07

|16

|4942

|164

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on cost classification, gross profit calculations, and expenditure types for Columbus Ltd and Steel Ltd. It delves into cost of production reports, performance indicators for improvement, and the purpose and methods of the budgeting process. The report also includes comparative budgets and a detailed variance analysis of Yuri's budget, along with the preparation of an operating statement and a memorandum report. The study covers various tasks such as cost analysis, improvement strategies, and the nature of the budgeting process, offering valuable insights into financial management and decision-making within organizations. The report concludes with a summary of the findings and recommendations for improvement.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Classifying cost into fixed, variable and semi variable.........................................................1

1.2, 1.3 Calculation of gross profit for each company.................................................................2

1.4 Type of expenditure...............................................................................................................3

TASK 2............................................................................................................................................4

2.1 Cost of production report.......................................................................................................4

2.2, 2.3 Performance indicators to identify potential improvements...........................................6

TASK 3............................................................................................................................................7

3.1 Purpose and nature of the budgeting process........................................................................7

3.2 Methods of budgeting............................................................................................................8

3.3 Creating comparative budgets...............................................................................................9

PART B (3.4).............................................................................................................................10

TASK 4 VARIANCE ANALYSIS...............................................................................................11

Part A) 4.1 Variance analysis of Yuri’s budget.........................................................................11

Part B 4.2 Preparation of Operating statement..........................................................................13

4.3 Memorandum report............................................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Classifying cost into fixed, variable and semi variable.........................................................1

1.2, 1.3 Calculation of gross profit for each company.................................................................2

1.4 Type of expenditure...............................................................................................................3

TASK 2............................................................................................................................................4

2.1 Cost of production report.......................................................................................................4

2.2, 2.3 Performance indicators to identify potential improvements...........................................6

TASK 3............................................................................................................................................7

3.1 Purpose and nature of the budgeting process........................................................................7

3.2 Methods of budgeting............................................................................................................8

3.3 Creating comparative budgets...............................................................................................9

PART B (3.4).............................................................................................................................10

TASK 4 VARIANCE ANALYSIS...............................................................................................11

Part A) 4.1 Variance analysis of Yuri’s budget.........................................................................11

Part B 4.2 Preparation of Operating statement..........................................................................13

4.3 Memorandum report............................................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting is regarded as the use of provisions of accounting data with the

aim to provide appropriate information the company. This type of accounting supports in

determining overall position of business in the market and corrective actions can be taken if

company is underperforming. It is the application of different principles of financial management

along with accounting with the motive to protect, create and increase the overall value for money

linked with stakeholders who plays significant role in the organization. Apart from this,

management accounting supports in reducing the financial risk along with uncertainty through

application of different tools (Galloway and Deakins, 2012). For conducting the present study

various organizations have been chosen such as Columbus Ltd, Howorth products etc. The entire

study is based on the concept of management accounting where cost reports have been

undertaken along with performance indicators in order to judge overall performance of business

in the market. Apart from this various tasks have been covered in the study which includes

calculation of different type of costs, improvement to reduce cost and enhance quality, nature of

budgeting process etc.

TASK 1

1.1 Classifying cost into fixed, variable and semi variable

Cost is regarded as the monetary measure of expenditure for material, supplier,

equipments etc. For production of any type of commodity business has to incur different type of

costs and it supports in determining price of the product. In regard with any specific firm,

different type of costs are associated which takes into consideration purchase of materials, staff

members employed, execution of operation etc (Graff, 2003). Further, operating cost is regarded

as the revenue expenditure of accountant which is crucial for firm with the motive to accomplish

desired goals along with objectives. Different types of costs are present which are linked with the

operations of Columbus Ltd and they are as follows:

On the basis of behavior

Fixed cost: It is the type of cost which does not changes with the alteration in level of output and

remains constant. Considering the present scenario, manufacturing cost of the firm is considered

as fixed cost.

1

Management accounting is regarded as the use of provisions of accounting data with the

aim to provide appropriate information the company. This type of accounting supports in

determining overall position of business in the market and corrective actions can be taken if

company is underperforming. It is the application of different principles of financial management

along with accounting with the motive to protect, create and increase the overall value for money

linked with stakeholders who plays significant role in the organization. Apart from this,

management accounting supports in reducing the financial risk along with uncertainty through

application of different tools (Galloway and Deakins, 2012). For conducting the present study

various organizations have been chosen such as Columbus Ltd, Howorth products etc. The entire

study is based on the concept of management accounting where cost reports have been

undertaken along with performance indicators in order to judge overall performance of business

in the market. Apart from this various tasks have been covered in the study which includes

calculation of different type of costs, improvement to reduce cost and enhance quality, nature of

budgeting process etc.

TASK 1

1.1 Classifying cost into fixed, variable and semi variable

Cost is regarded as the monetary measure of expenditure for material, supplier,

equipments etc. For production of any type of commodity business has to incur different type of

costs and it supports in determining price of the product. In regard with any specific firm,

different type of costs are associated which takes into consideration purchase of materials, staff

members employed, execution of operation etc (Graff, 2003). Further, operating cost is regarded

as the revenue expenditure of accountant which is crucial for firm with the motive to accomplish

desired goals along with objectives. Different types of costs are present which are linked with the

operations of Columbus Ltd and they are as follows:

On the basis of behavior

Fixed cost: It is the type of cost which does not changes with the alteration in level of output and

remains constant. Considering the present scenario, manufacturing cost of the firm is considered

as fixed cost.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variable cost: It takes into consideration direct along with indirect cost which changes with the

alteration in level of output. Direct material cost of Columbus is the variable cost as it changes

with production (James, Leavel and Mainam, 2002).

Semi variable cost: This type of cost considers attributes of both fixed and variable cost where it

is fixed at certain level of production and after crossing certain limit it becomes variable.

On the basis of pricing and costing

Indirect cost: This type of cost takes into consideration material and labor that are not directly

employed in producing any specific commodity. This cost is firstly charged to the cost centre and

segregated on the basis of products and services.

Direct cost: This type of cost undertakes material, labor and overhead which are incurred for

production of specific commodity (Method of costing. 2014). Direct cost is associated with

manufacturing process and for calculation of same managers consider job cards which supports

in knowing remuneration. Moreover, direct material is the cost which is incurred for purchase of

materials being used in the production. Apart from this, overheads are the cost incurred by

company for conducting manufacturing process example equipment maintenance etc.

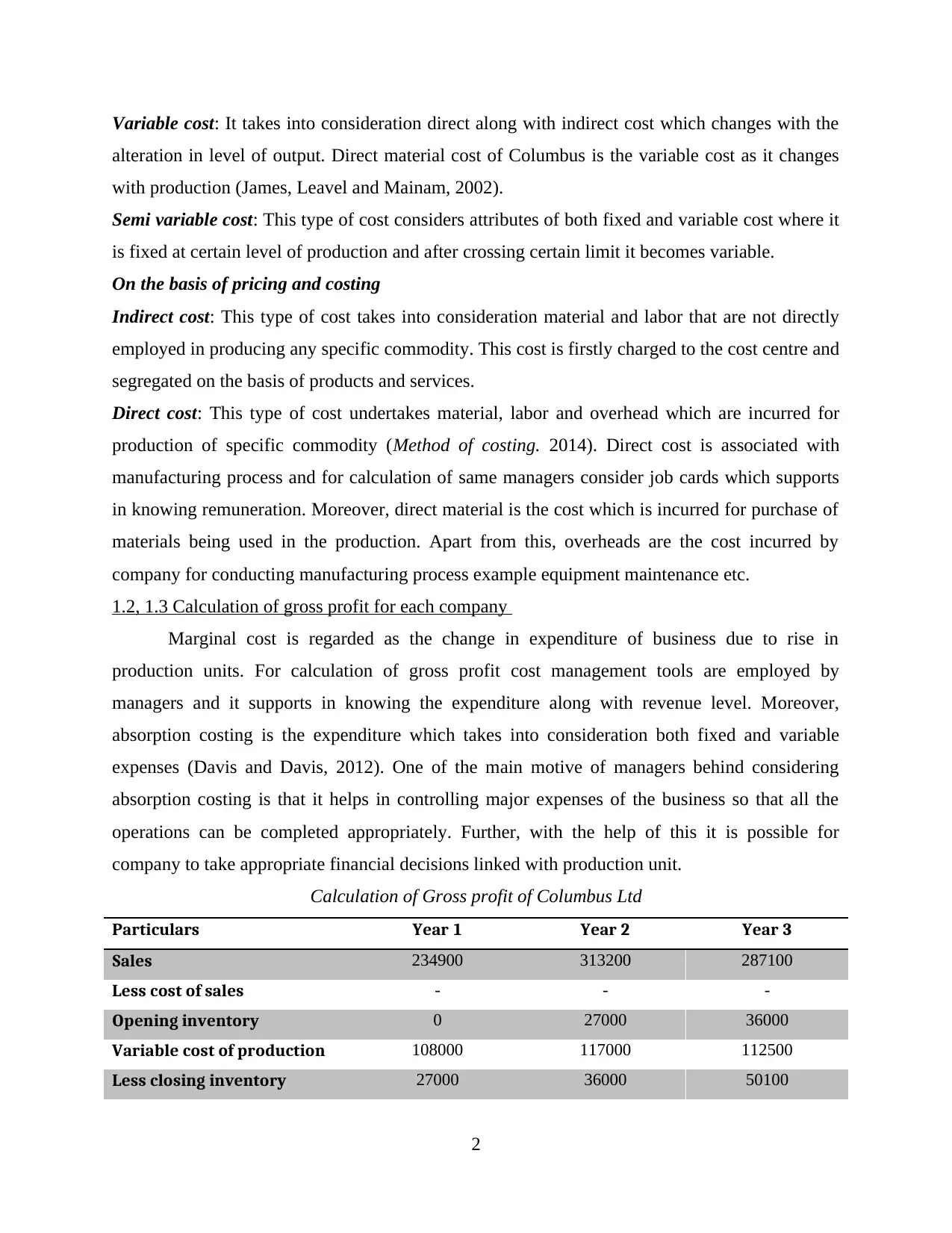

1.2, 1.3 Calculation of gross profit for each company

Marginal cost is regarded as the change in expenditure of business due to rise in

production units. For calculation of gross profit cost management tools are employed by

managers and it supports in knowing the expenditure along with revenue level. Moreover,

absorption costing is the expenditure which takes into consideration both fixed and variable

expenses (Davis and Davis, 2012). One of the main motive of managers behind considering

absorption costing is that it helps in controlling major expenses of the business so that all the

operations can be completed appropriately. Further, with the help of this it is possible for

company to take appropriate financial decisions linked with production unit.

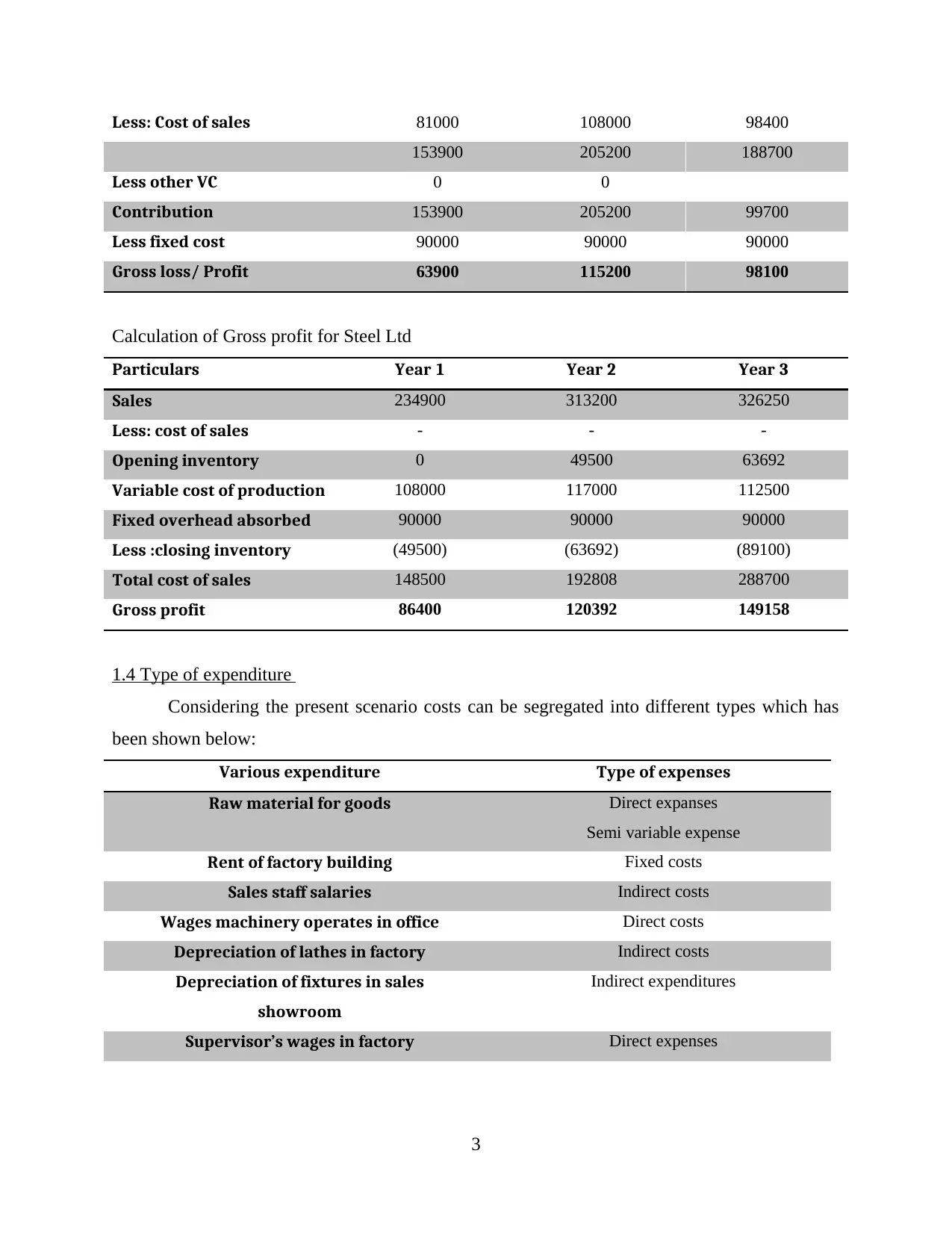

Calculation of Gross profit of Columbus Ltd

Particulars Year 1 Year 2 Year 3

Sales 234900 313200 287100

Less cost of sales - - -

Opening inventory 0 27000 36000

Variable cost of production 108000 117000 112500

Less closing inventory 27000 36000 50100

2

alteration in level of output. Direct material cost of Columbus is the variable cost as it changes

with production (James, Leavel and Mainam, 2002).

Semi variable cost: This type of cost considers attributes of both fixed and variable cost where it

is fixed at certain level of production and after crossing certain limit it becomes variable.

On the basis of pricing and costing

Indirect cost: This type of cost takes into consideration material and labor that are not directly

employed in producing any specific commodity. This cost is firstly charged to the cost centre and

segregated on the basis of products and services.

Direct cost: This type of cost undertakes material, labor and overhead which are incurred for

production of specific commodity (Method of costing. 2014). Direct cost is associated with

manufacturing process and for calculation of same managers consider job cards which supports

in knowing remuneration. Moreover, direct material is the cost which is incurred for purchase of

materials being used in the production. Apart from this, overheads are the cost incurred by

company for conducting manufacturing process example equipment maintenance etc.

1.2, 1.3 Calculation of gross profit for each company

Marginal cost is regarded as the change in expenditure of business due to rise in

production units. For calculation of gross profit cost management tools are employed by

managers and it supports in knowing the expenditure along with revenue level. Moreover,

absorption costing is the expenditure which takes into consideration both fixed and variable

expenses (Davis and Davis, 2012). One of the main motive of managers behind considering

absorption costing is that it helps in controlling major expenses of the business so that all the

operations can be completed appropriately. Further, with the help of this it is possible for

company to take appropriate financial decisions linked with production unit.

Calculation of Gross profit of Columbus Ltd

Particulars Year 1 Year 2 Year 3

Sales 234900 313200 287100

Less cost of sales - - -

Opening inventory 0 27000 36000

Variable cost of production 108000 117000 112500

Less closing inventory 27000 36000 50100

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Less: Cost of sales 81000 108000 98400

153900 205200 188700

Less other VC 0 0

Contribution 153900 205200 99700

Less fixed cost 90000 90000 90000

Gross loss/ Profit 63900 115200 98100

Calculation of Gross profit for Steel Ltd

Particulars Year 1 Year 2 Year 3

Sales 234900 313200 326250

Less: cost of sales - - -

Opening inventory 0 49500 63692

Variable cost of production 108000 117000 112500

Fixed overhead absorbed 90000 90000 90000

Less :closing inventory (49500) (63692) (89100)

Total cost of sales 148500 192808 288700

Gross profit 86400 120392 149158

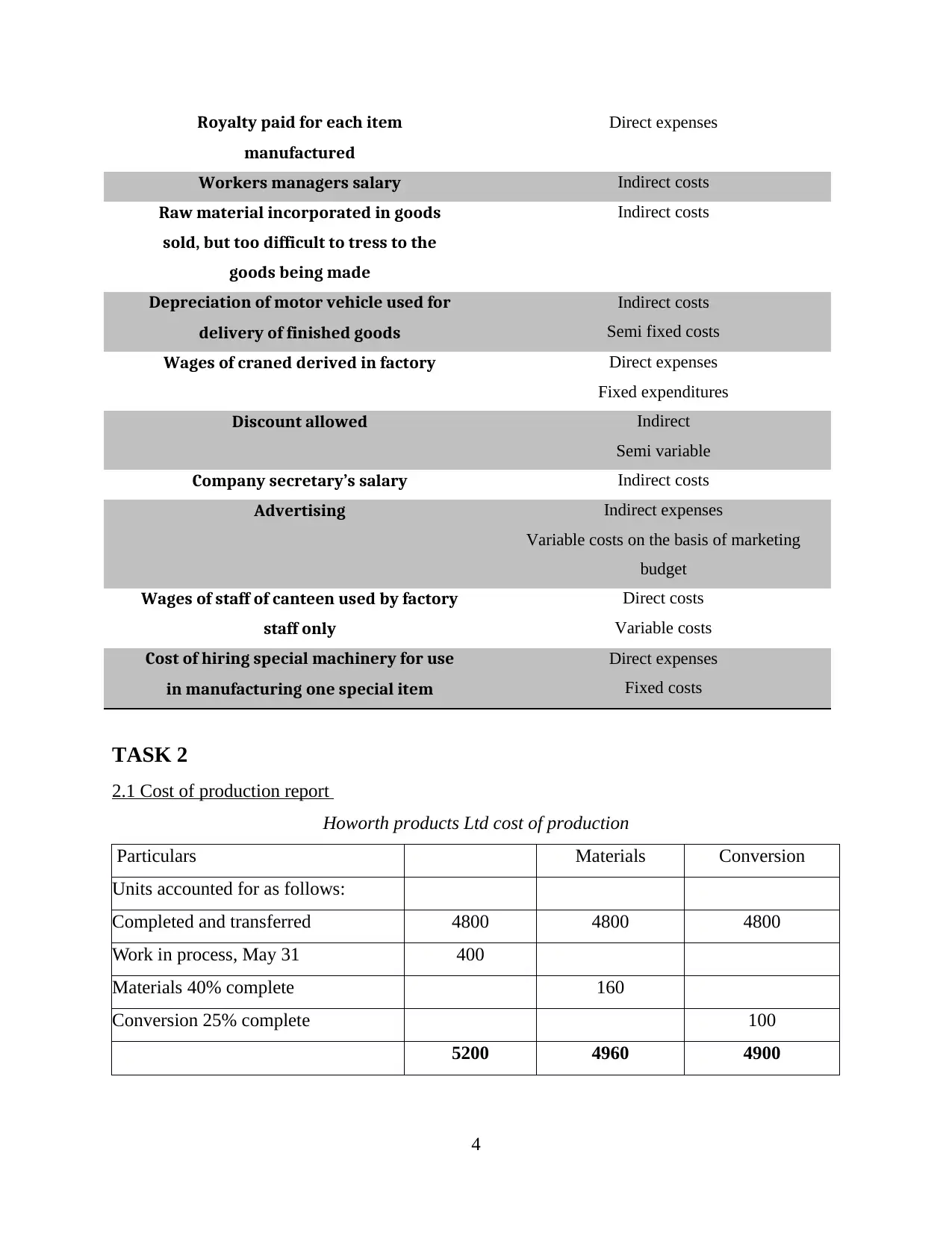

1.4 Type of expenditure

Considering the present scenario costs can be segregated into different types which has

been shown below:

Various expenditure Type of expenses

Raw material for goods Direct expanses

Semi variable expense

Rent of factory building Fixed costs

Sales staff salaries Indirect costs

Wages machinery operates in office Direct costs

Depreciation of lathes in factory Indirect costs

Depreciation of fixtures in sales

showroom

Indirect expenditures

Supervisor’s wages in factory Direct expenses

3

153900 205200 188700

Less other VC 0 0

Contribution 153900 205200 99700

Less fixed cost 90000 90000 90000

Gross loss/ Profit 63900 115200 98100

Calculation of Gross profit for Steel Ltd

Particulars Year 1 Year 2 Year 3

Sales 234900 313200 326250

Less: cost of sales - - -

Opening inventory 0 49500 63692

Variable cost of production 108000 117000 112500

Fixed overhead absorbed 90000 90000 90000

Less :closing inventory (49500) (63692) (89100)

Total cost of sales 148500 192808 288700

Gross profit 86400 120392 149158

1.4 Type of expenditure

Considering the present scenario costs can be segregated into different types which has

been shown below:

Various expenditure Type of expenses

Raw material for goods Direct expanses

Semi variable expense

Rent of factory building Fixed costs

Sales staff salaries Indirect costs

Wages machinery operates in office Direct costs

Depreciation of lathes in factory Indirect costs

Depreciation of fixtures in sales

showroom

Indirect expenditures

Supervisor’s wages in factory Direct expenses

3

Royalty paid for each item

manufactured

Direct expenses

Workers managers salary Indirect costs

Raw material incorporated in goods

sold, but too difficult to tress to the

goods being made

Indirect costs

Depreciation of motor vehicle used for

delivery of finished goods

Indirect costs

Semi fixed costs

Wages of craned derived in factory Direct expenses

Fixed expenditures

Discount allowed Indirect

Semi variable

Company secretary’s salary Indirect costs

Advertising Indirect expenses

Variable costs on the basis of marketing

budget

Wages of staff of canteen used by factory

staff only

Direct costs

Variable costs

Cost of hiring special machinery for use

in manufacturing one special item

Direct expenses

Fixed costs

TASK 2

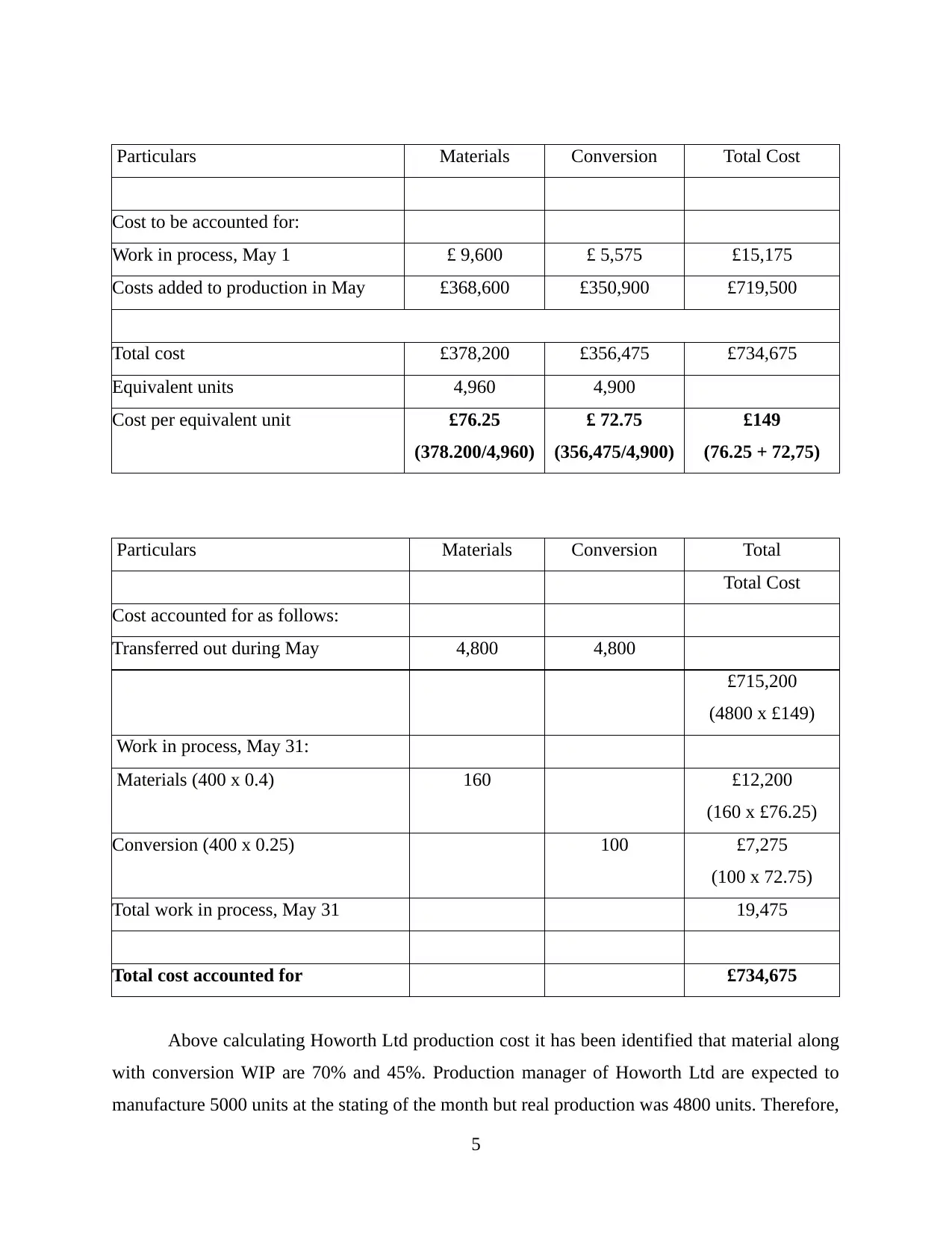

2.1 Cost of production report

Howorth products Ltd cost of production

Particulars Materials Conversion

Units accounted for as follows:

Completed and transferred 4800 4800 4800

Work in process, May 31 400

Materials 40% complete 160

Conversion 25% complete 100

5200 4960 4900

4

manufactured

Direct expenses

Workers managers salary Indirect costs

Raw material incorporated in goods

sold, but too difficult to tress to the

goods being made

Indirect costs

Depreciation of motor vehicle used for

delivery of finished goods

Indirect costs

Semi fixed costs

Wages of craned derived in factory Direct expenses

Fixed expenditures

Discount allowed Indirect

Semi variable

Company secretary’s salary Indirect costs

Advertising Indirect expenses

Variable costs on the basis of marketing

budget

Wages of staff of canteen used by factory

staff only

Direct costs

Variable costs

Cost of hiring special machinery for use

in manufacturing one special item

Direct expenses

Fixed costs

TASK 2

2.1 Cost of production report

Howorth products Ltd cost of production

Particulars Materials Conversion

Units accounted for as follows:

Completed and transferred 4800 4800 4800

Work in process, May 31 400

Materials 40% complete 160

Conversion 25% complete 100

5200 4960 4900

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars Materials Conversion Total Cost

Cost to be accounted for:

Work in process, May 1 £ 9,600 £ 5,575 £15,175

Costs added to production in May £368,600 £350,900 £719,500

Total cost £378,200 £356,475 £734,675

Equivalent units 4,960 4,900

Cost per equivalent unit £76.25

(378.200/4,960)

£ 72.75

(356,475/4,900)

£149

(76.25 + 72,75)

Particulars Materials Conversion Total

Total Cost

Cost accounted for as follows:

Transferred out during May 4,800 4,800

£715,200

(4800 x £149)

Work in process, May 31:

Materials (400 x 0.4) 160 £12,200

(160 x £76.25)

Conversion (400 x 0.25) 100 £7,275

(100 x 72.75)

Total work in process, May 31 19,475

Total cost accounted for £734,675

Above calculating Howorth Ltd production cost it has been identified that material along

with conversion WIP are 70% and 45%. Production manager of Howorth Ltd are expected to

manufacture 5000 units at the stating of the month but real production was 4800 units. Therefore,

5

Cost to be accounted for:

Work in process, May 1 £ 9,600 £ 5,575 £15,175

Costs added to production in May £368,600 £350,900 £719,500

Total cost £378,200 £356,475 £734,675

Equivalent units 4,960 4,900

Cost per equivalent unit £76.25

(378.200/4,960)

£ 72.75

(356,475/4,900)

£149

(76.25 + 72,75)

Particulars Materials Conversion Total

Total Cost

Cost accounted for as follows:

Transferred out during May 4,800 4,800

£715,200

(4800 x £149)

Work in process, May 31:

Materials (400 x 0.4) 160 £12,200

(160 x £76.25)

Conversion (400 x 0.25) 100 £7,275

(100 x 72.75)

Total work in process, May 31 19,475

Total cost accounted for £734,675

Above calculating Howorth Ltd production cost it has been identified that material along

with conversion WIP are 70% and 45%. Production manager of Howorth Ltd are expected to

manufacture 5000 units at the stating of the month but real production was 4800 units. Therefore,

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

200 units which were not produced will be undertaken in the month of May and it has lead

business to incur overall cost of £734675.

2.2, 2.3 Performance indicators to identify potential improvements

For enhancing overall performance in the market it is required for every business to

identify performance indicators. Further, it is well known fact that range of indicators considered

by company assist in judging the present performance and measures can be easily taken if

organization is underperforming. Apart from this, it allows business to work in favor of its

development and it supports in accomplishment of desired goals (Cohen and Kaimenaki, 2011).

In company like Howorth products Ltd main function of performance indicator is to identify

whether the manufacturing unit of organization is efficient or not. This supports in knowing

whether business is indulged into healthy production practices or not. Below shown are the

performance indicators for the manufacturing unit which are:

Reject ratio: It is regarded as one of the most crucial performance indicator which supports in

knowing the amount of waste in the process of production. Further, it is required for

management to know how much material is wasted as it increases overall cost of production.

Output: This performance indicator is also considered as most effective for business as

management sets target with the motive to produce certain level of output. So, monitoring overall

performance of staff members along with operations provides base in determining the variance

between actual and budgeted output (Kastantin, 2005).

Quality: This indictor allows business to ensure that right quality products are delivered to target

market. By knowing the quality level of the products it is possible for company whether it is

operating efficiently in the market or not.

Production time: It helps in knowing the overall time required in producing products. Further,

main motive of this performance indicator is to know whether the manufacturing process of

business is carried out efficiently or not.

Visual management: This technique is also regarded to be beneficial for business as through this

organization can easily define KPI for three aspects which takes into consideration quality,

efficiency and output. This method can be implemented by management at factory level with the

motive to know performance of staff members and corrective actions can be taken if employees

are underperforming.

6

business to incur overall cost of £734675.

2.2, 2.3 Performance indicators to identify potential improvements

For enhancing overall performance in the market it is required for every business to

identify performance indicators. Further, it is well known fact that range of indicators considered

by company assist in judging the present performance and measures can be easily taken if

organization is underperforming. Apart from this, it allows business to work in favor of its

development and it supports in accomplishment of desired goals (Cohen and Kaimenaki, 2011).

In company like Howorth products Ltd main function of performance indicator is to identify

whether the manufacturing unit of organization is efficient or not. This supports in knowing

whether business is indulged into healthy production practices or not. Below shown are the

performance indicators for the manufacturing unit which are:

Reject ratio: It is regarded as one of the most crucial performance indicator which supports in

knowing the amount of waste in the process of production. Further, it is required for

management to know how much material is wasted as it increases overall cost of production.

Output: This performance indicator is also considered as most effective for business as

management sets target with the motive to produce certain level of output. So, monitoring overall

performance of staff members along with operations provides base in determining the variance

between actual and budgeted output (Kastantin, 2005).

Quality: This indictor allows business to ensure that right quality products are delivered to target

market. By knowing the quality level of the products it is possible for company whether it is

operating efficiently in the market or not.

Production time: It helps in knowing the overall time required in producing products. Further,

main motive of this performance indicator is to know whether the manufacturing process of

business is carried out efficiently or not.

Visual management: This technique is also regarded to be beneficial for business as through this

organization can easily define KPI for three aspects which takes into consideration quality,

efficiency and output. This method can be implemented by management at factory level with the

motive to know performance of staff members and corrective actions can be taken if employees

are underperforming.

6

Rate: It is also another type of performance indicator which supports in knowing the overall rate

at which manufacturing is carried out so as to deliver high quality products as per expectations of

customers. In case, if speed of production is high then it enhances quality and vice versa when

rate is slow. Due to this basic reason, it is required for business to decide the overall rate at

which production can be carried out (Lindholm and Suomala, 2007).

Recommendation

Considering the present case it can be said that Howorth products Ltd can undertake

quality as one of the key performance indicator through which market performance of business

can be known easily. Further, it will allow business to satisfy overall requirement of its target

market in efficient manner and will have positive impact on the brand image also. Apart from

this, other indicator such as production time is also effective through which business can easily

indulge itself into efficient production activities and is fruitful in every possible manner.

TASK 3

3.1 Purpose and nature of the budgeting process

Budgeting is regarded as the process of forecasting where main stress is on

accomplishing the desired activities on time and in appropriate manner. It is considered as an

effective tool for planning where proper decisions can be taken by management regarding

allocation of financial resources and using them in different activities. Main purpose of preparing

budgets is as follows:

Determining performance of company: One of the main purpose behind preparing

budget is to preparing actual performance with expected one (Maelah and et. al., 2012).

Sharing information: By preparing budget it is possible for top level management of

enterprise to share important information linked with financial performance of the firm

and in case if business is not performing up to the mark then corrective actions can be

taken regarding same.

Control on major expenditure: One of the main purpose of budgeting is to control major

costs associated with the business. Further, it is possible to allocate all the major

resources in appropriate manner and can assist in maintaining proper cash balance.

On the other hand, budgetary control system is quite effective which relies on series of

stages. Below shown are the major stages of the system through which financial performance of

company can be managed easily.

7

at which manufacturing is carried out so as to deliver high quality products as per expectations of

customers. In case, if speed of production is high then it enhances quality and vice versa when

rate is slow. Due to this basic reason, it is required for business to decide the overall rate at

which production can be carried out (Lindholm and Suomala, 2007).

Recommendation

Considering the present case it can be said that Howorth products Ltd can undertake

quality as one of the key performance indicator through which market performance of business

can be known easily. Further, it will allow business to satisfy overall requirement of its target

market in efficient manner and will have positive impact on the brand image also. Apart from

this, other indicator such as production time is also effective through which business can easily

indulge itself into efficient production activities and is fruitful in every possible manner.

TASK 3

3.1 Purpose and nature of the budgeting process

Budgeting is regarded as the process of forecasting where main stress is on

accomplishing the desired activities on time and in appropriate manner. It is considered as an

effective tool for planning where proper decisions can be taken by management regarding

allocation of financial resources and using them in different activities. Main purpose of preparing

budgets is as follows:

Determining performance of company: One of the main purpose behind preparing

budget is to preparing actual performance with expected one (Maelah and et. al., 2012).

Sharing information: By preparing budget it is possible for top level management of

enterprise to share important information linked with financial performance of the firm

and in case if business is not performing up to the mark then corrective actions can be

taken regarding same.

Control on major expenditure: One of the main purpose of budgeting is to control major

costs associated with the business. Further, it is possible to allocate all the major

resources in appropriate manner and can assist in maintaining proper cash balance.

On the other hand, budgetary control system is quite effective which relies on series of

stages. Below shown are the major stages of the system through which financial performance of

company can be managed easily.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Development of new budget: It is the first important stage where new budget is being

prepared for every specific department (Ezeoha, 2011).

Defining performance measurement: When budget is developed then it is necessary for

business to define quantifying measurement of performance of budget by considering

efficiency of the overall business in the market.

Measuring actual performance: By undertaking this technique of budgetary control it is

possible for business to determine its actual performance and same can be evaluated for

performing better in the competitive market.

Determining variances: For identifying variance it is necessarily required to compare

actual performance with the expected one.

Taking corrective actions: After determining variance it is necessary to take corrective

actions so that it can be overcome and this can bring favorable results for business.

3.2 Methods of budgeting

Different methods of budgeting are present which provides base to management in

controlling overall operations. Further, through budgeting coordination along with planning

becomes easy for firm. In short budgets prepared by firm provide guideline to company on the

basis of which resources can be allocated by business in appropriate manner. Different types of

budgets are present which organization considers and they are as follows:

Zero base budgeting: In this type of budgeting technique each department of the business is

required to identify the key resources required for accomplishment of desired aim along with

objectives (Mohsin, 2013). Further, undertaking this method allows business to evaluate each

task and resources can be allocated in effective manner. One of the main advantages of

undertaking this method is that it assists in allocation of resources and provides a base to

organization in decreasing the overall cost associated with the business. Apart from this, zero

base budgeting as a techniques consumes large time as meetings along with reports are required

to be undertaken and it sometime leads to conflict in between departments.

Incremental budgeting: In this type of budgeting technique finance manager of enterprise

undertakes figure of last year and considers the changes taking place in different factors such as

price, inflation etc. Main advantage of employing this technique is that it is easy to understand.

On the other hand its main disadvantage is that no provision for alteration is present within the

budget in case when external along with internal factors affects operations of company. Apart

8

prepared for every specific department (Ezeoha, 2011).

Defining performance measurement: When budget is developed then it is necessary for

business to define quantifying measurement of performance of budget by considering

efficiency of the overall business in the market.

Measuring actual performance: By undertaking this technique of budgetary control it is

possible for business to determine its actual performance and same can be evaluated for

performing better in the competitive market.

Determining variances: For identifying variance it is necessarily required to compare

actual performance with the expected one.

Taking corrective actions: After determining variance it is necessary to take corrective

actions so that it can be overcome and this can bring favorable results for business.

3.2 Methods of budgeting

Different methods of budgeting are present which provides base to management in

controlling overall operations. Further, through budgeting coordination along with planning

becomes easy for firm. In short budgets prepared by firm provide guideline to company on the

basis of which resources can be allocated by business in appropriate manner. Different types of

budgets are present which organization considers and they are as follows:

Zero base budgeting: In this type of budgeting technique each department of the business is

required to identify the key resources required for accomplishment of desired aim along with

objectives (Mohsin, 2013). Further, undertaking this method allows business to evaluate each

task and resources can be allocated in effective manner. One of the main advantages of

undertaking this method is that it assists in allocation of resources and provides a base to

organization in decreasing the overall cost associated with the business. Apart from this, zero

base budgeting as a techniques consumes large time as meetings along with reports are required

to be undertaken and it sometime leads to conflict in between departments.

Incremental budgeting: In this type of budgeting technique finance manager of enterprise

undertakes figure of last year and considers the changes taking place in different factors such as

price, inflation etc. Main advantage of employing this technique is that it is easy to understand.

On the other hand its main disadvantage is that no provision for alteration is present within the

budget in case when external along with internal factors affects operations of company. Apart

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

from this, with the help of incremental budgeting it is difficult for organization to conduct new

activity in appropriate manner (Bragg, 2013).

Top down budgeting: As the name represents in this technique budget is prepared from top to

down. Further, main focus is on determining the cost of higher level and resources are divided to

the down level tasks for execution in effective manner. Through this budgeting technique it is

possible to save time as managers working in different division have right to take decisions but it

may be possible that managers at senior level may lose control over tasks in different

departments.

Bottom to top budgeting: This technique of budgeting provides base to budget holder in

contributing to the entire process of budgeting. Further, one of the main motive behind

undertaking this tool is that it helps in identifying and evaluating all the tasks required in

accomplishing all the operations in effective manner.

After analyzing different methods of budgeting it has been identified that one of the most

effective technique of budgeting for company like max ltd is top down budgeting with the help

of which it is possible to accomplish the goal of optimum utilization of resources.

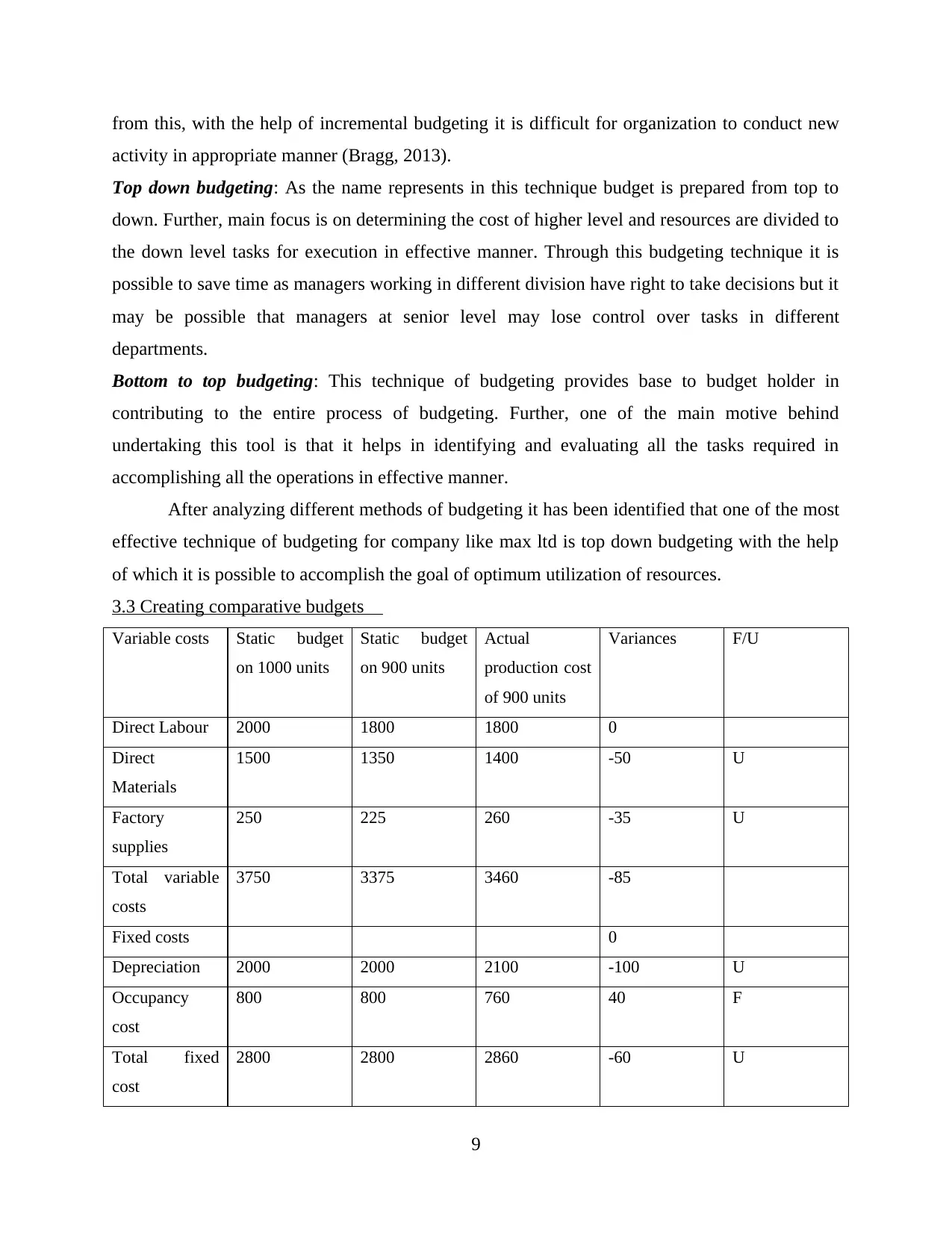

3.3 Creating comparative budgets

Variable costs Static budget

on 1000 units

Static budget

on 900 units

Actual

production cost

of 900 units

Variances F/U

Direct Labour 2000 1800 1800 0

Direct

Materials

1500 1350 1400 -50 U

Factory

supplies

250 225 260 -35 U

Total variable

costs

3750 3375 3460 -85

Fixed costs 0

Depreciation 2000 2000 2100 -100 U

Occupancy

cost

800 800 760 40 F

Total fixed

cost

2800 2800 2860 -60 U

9

activity in appropriate manner (Bragg, 2013).

Top down budgeting: As the name represents in this technique budget is prepared from top to

down. Further, main focus is on determining the cost of higher level and resources are divided to

the down level tasks for execution in effective manner. Through this budgeting technique it is

possible to save time as managers working in different division have right to take decisions but it

may be possible that managers at senior level may lose control over tasks in different

departments.

Bottom to top budgeting: This technique of budgeting provides base to budget holder in

contributing to the entire process of budgeting. Further, one of the main motive behind

undertaking this tool is that it helps in identifying and evaluating all the tasks required in

accomplishing all the operations in effective manner.

After analyzing different methods of budgeting it has been identified that one of the most

effective technique of budgeting for company like max ltd is top down budgeting with the help

of which it is possible to accomplish the goal of optimum utilization of resources.

3.3 Creating comparative budgets

Variable costs Static budget

on 1000 units

Static budget

on 900 units

Actual

production cost

of 900 units

Variances F/U

Direct Labour 2000 1800 1800 0

Direct

Materials

1500 1350 1400 -50 U

Factory

supplies

250 225 260 -35 U

Total variable

costs

3750 3375 3460 -85

Fixed costs 0

Depreciation 2000 2000 2100 -100 U

Occupancy

cost

800 800 760 40 F

Total fixed

cost

2800 2800 2860 -60 U

9

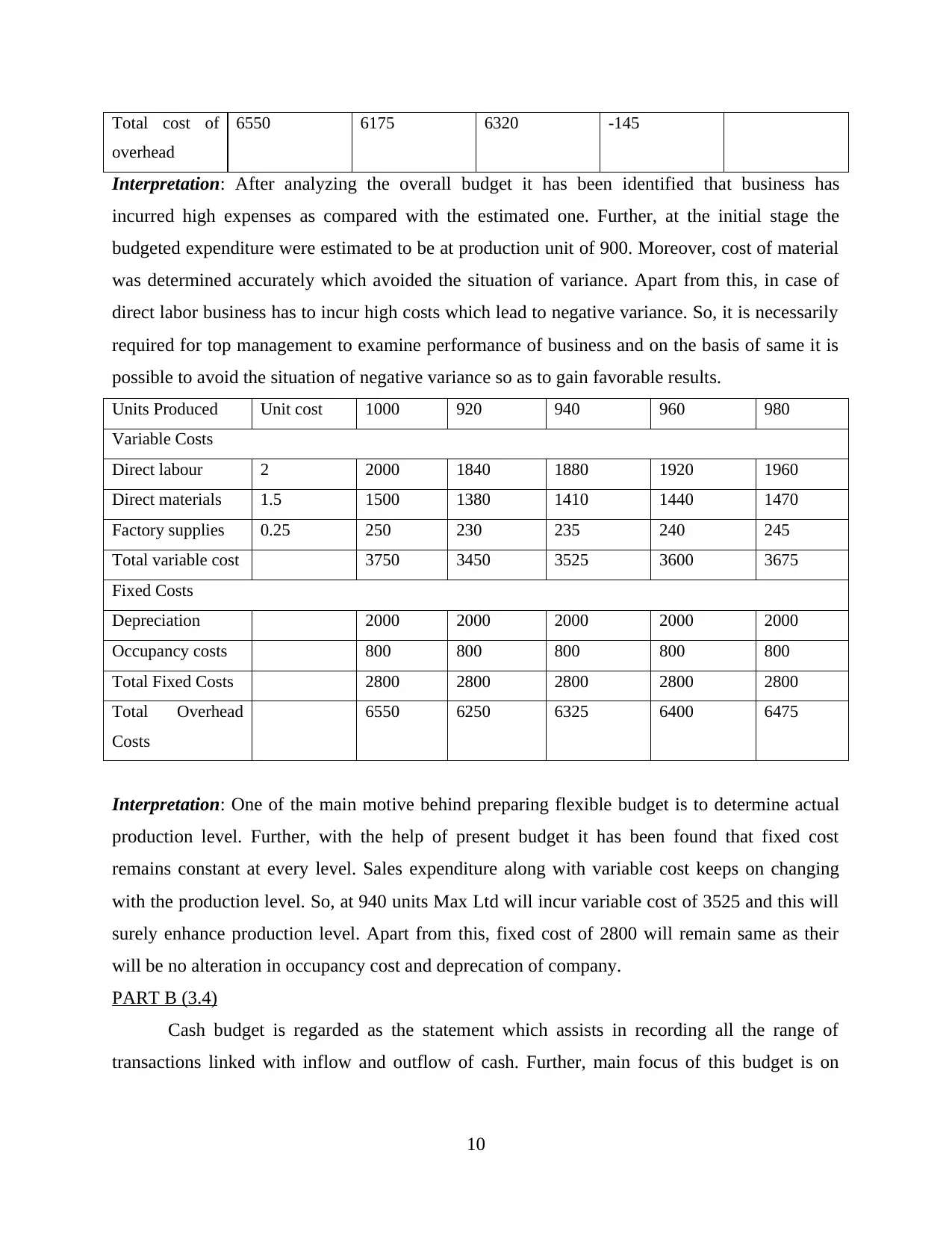

Total cost of

overhead

6550 6175 6320 -145

Interpretation: After analyzing the overall budget it has been identified that business has

incurred high expenses as compared with the estimated one. Further, at the initial stage the

budgeted expenditure were estimated to be at production unit of 900. Moreover, cost of material

was determined accurately which avoided the situation of variance. Apart from this, in case of

direct labor business has to incur high costs which lead to negative variance. So, it is necessarily

required for top management to examine performance of business and on the basis of same it is

possible to avoid the situation of negative variance so as to gain favorable results.

Units Produced Unit cost 1000 920 940 960 980

Variable Costs

Direct labour 2 2000 1840 1880 1920 1960

Direct materials 1.5 1500 1380 1410 1440 1470

Factory supplies 0.25 250 230 235 240 245

Total variable cost 3750 3450 3525 3600 3675

Fixed Costs

Depreciation 2000 2000 2000 2000 2000

Occupancy costs 800 800 800 800 800

Total Fixed Costs 2800 2800 2800 2800 2800

Total Overhead

Costs

6550 6250 6325 6400 6475

Interpretation: One of the main motive behind preparing flexible budget is to determine actual

production level. Further, with the help of present budget it has been found that fixed cost

remains constant at every level. Sales expenditure along with variable cost keeps on changing

with the production level. So, at 940 units Max Ltd will incur variable cost of 3525 and this will

surely enhance production level. Apart from this, fixed cost of 2800 will remain same as their

will be no alteration in occupancy cost and deprecation of company.

PART B (3.4)

Cash budget is regarded as the statement which assists in recording all the range of

transactions linked with inflow and outflow of cash. Further, main focus of this budget is on

10

overhead

6550 6175 6320 -145

Interpretation: After analyzing the overall budget it has been identified that business has

incurred high expenses as compared with the estimated one. Further, at the initial stage the

budgeted expenditure were estimated to be at production unit of 900. Moreover, cost of material

was determined accurately which avoided the situation of variance. Apart from this, in case of

direct labor business has to incur high costs which lead to negative variance. So, it is necessarily

required for top management to examine performance of business and on the basis of same it is

possible to avoid the situation of negative variance so as to gain favorable results.

Units Produced Unit cost 1000 920 940 960 980

Variable Costs

Direct labour 2 2000 1840 1880 1920 1960

Direct materials 1.5 1500 1380 1410 1440 1470

Factory supplies 0.25 250 230 235 240 245

Total variable cost 3750 3450 3525 3600 3675

Fixed Costs

Depreciation 2000 2000 2000 2000 2000

Occupancy costs 800 800 800 800 800

Total Fixed Costs 2800 2800 2800 2800 2800

Total Overhead

Costs

6550 6250 6325 6400 6475

Interpretation: One of the main motive behind preparing flexible budget is to determine actual

production level. Further, with the help of present budget it has been found that fixed cost

remains constant at every level. Sales expenditure along with variable cost keeps on changing

with the production level. So, at 940 units Max Ltd will incur variable cost of 3525 and this will

surely enhance production level. Apart from this, fixed cost of 2800 will remain same as their

will be no alteration in occupancy cost and deprecation of company.

PART B (3.4)

Cash budget is regarded as the statement which assists in recording all the range of

transactions linked with inflow and outflow of cash. Further, main focus of this budget is on

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.