Management Accounting Report: Unit 5, MR College, Semester 1

VerifiedAdded on 2023/01/18

|16

|2938

|63

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles. Task 1 explores marginal and absorption costing, detailing their differences, applications, and impact on profit/loss figures. Task 2 delves into budgetary control, examining various planning tools like fixed, flexible, incremental, and zero-based budgets, along with variance analysis. The report evaluates the advantages and disadvantages of these tools, and analyzes their application in preparing and forecasting budgets. Furthermore, the report discusses how organizations like Tesco and Sainsbury use management accounting to address financial issues, incorporating both financial and non-financial performance indicators. The report concludes by evaluating how management accounting helps organizations respond to financial problems and achieve sustainable success, including the integration of sustainable practices and the use of management accounting tools.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING

Table of Contents

Task 1:.............................................................................................................................................2

Part B: Portfolio of calculations and comments..........................................................................2

Income statement using marginal costing and absorption costing for three years:.................2

Differences between marginal and absorption costing methods:............................................3

Use of marginal costing in a business:....................................................................................3

Reasons for difference in profit/loss figures under the two methods:.....................................4

Task 2:.............................................................................................................................................5

Part a:...........................................................................................................................................5

Part b:...........................................................................................................................................7

Part c:...........................................................................................................................................8

Part d:.........................................................................................................................................11

Part e:.........................................................................................................................................12

References:....................................................................................................................................14

Table of Contents

Task 1:.............................................................................................................................................2

Part B: Portfolio of calculations and comments..........................................................................2

Income statement using marginal costing and absorption costing for three years:.................2

Differences between marginal and absorption costing methods:............................................3

Use of marginal costing in a business:....................................................................................3

Reasons for difference in profit/loss figures under the two methods:.....................................4

Task 2:.............................................................................................................................................5

Part a:...........................................................................................................................................5

Part b:...........................................................................................................................................7

Part c:...........................................................................................................................................8

Part d:.........................................................................................................................................11

Part e:.........................................................................................................................................12

References:....................................................................................................................................14

2MANAGEMENT ACCOUNTING

Task 1:

Part B: Portfolio of calculations and comments

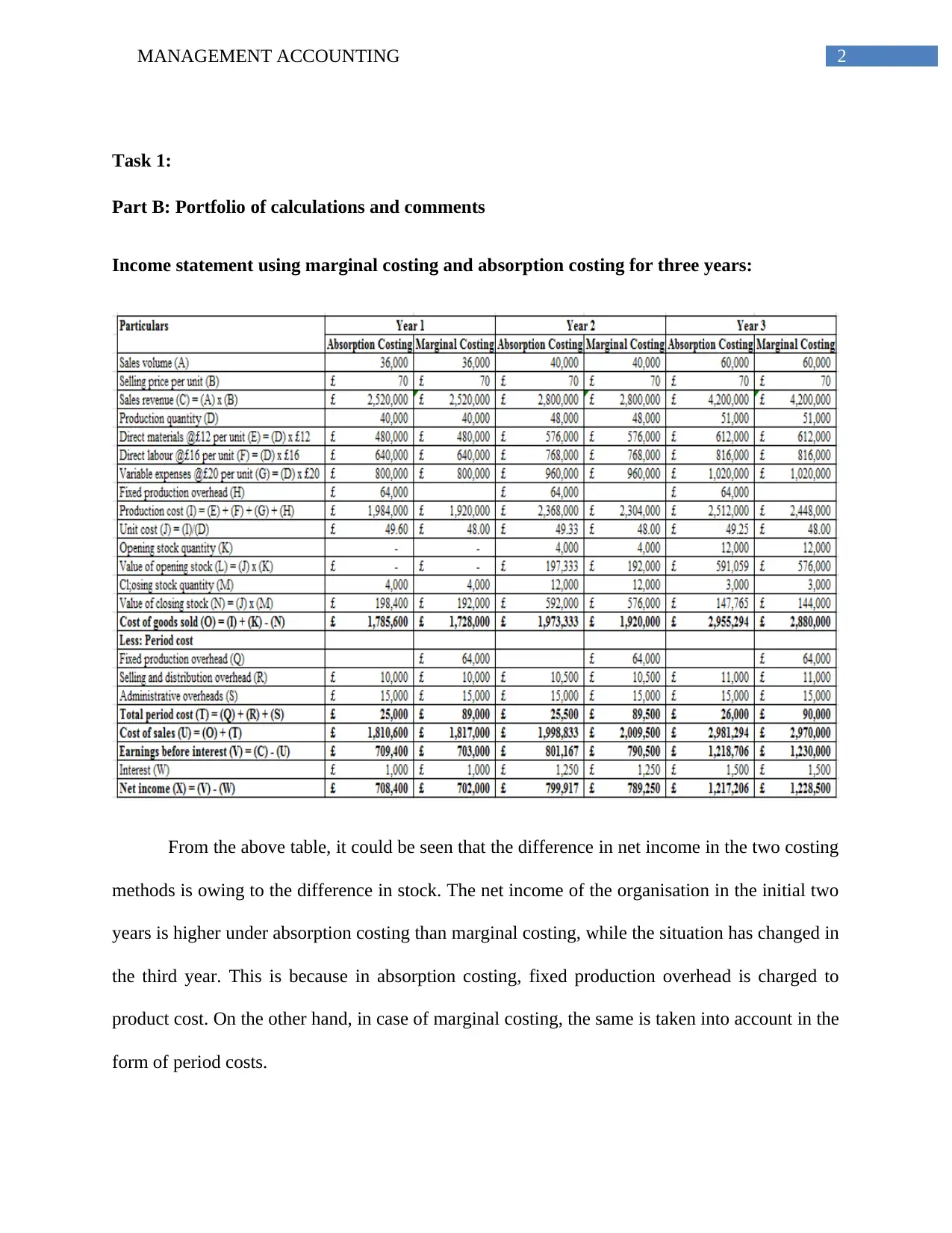

Income statement using marginal costing and absorption costing for three years:

From the above table, it could be seen that the difference in net income in the two costing

methods is owing to the difference in stock. The net income of the organisation in the initial two

years is higher under absorption costing than marginal costing, while the situation has changed in

the third year. This is because in absorption costing, fixed production overhead is charged to

product cost. On the other hand, in case of marginal costing, the same is taken into account in the

form of period costs.

Task 1:

Part B: Portfolio of calculations and comments

Income statement using marginal costing and absorption costing for three years:

From the above table, it could be seen that the difference in net income in the two costing

methods is owing to the difference in stock. The net income of the organisation in the initial two

years is higher under absorption costing than marginal costing, while the situation has changed in

the third year. This is because in absorption costing, fixed production overhead is charged to

product cost. On the other hand, in case of marginal costing, the same is taken into account in the

form of period costs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING

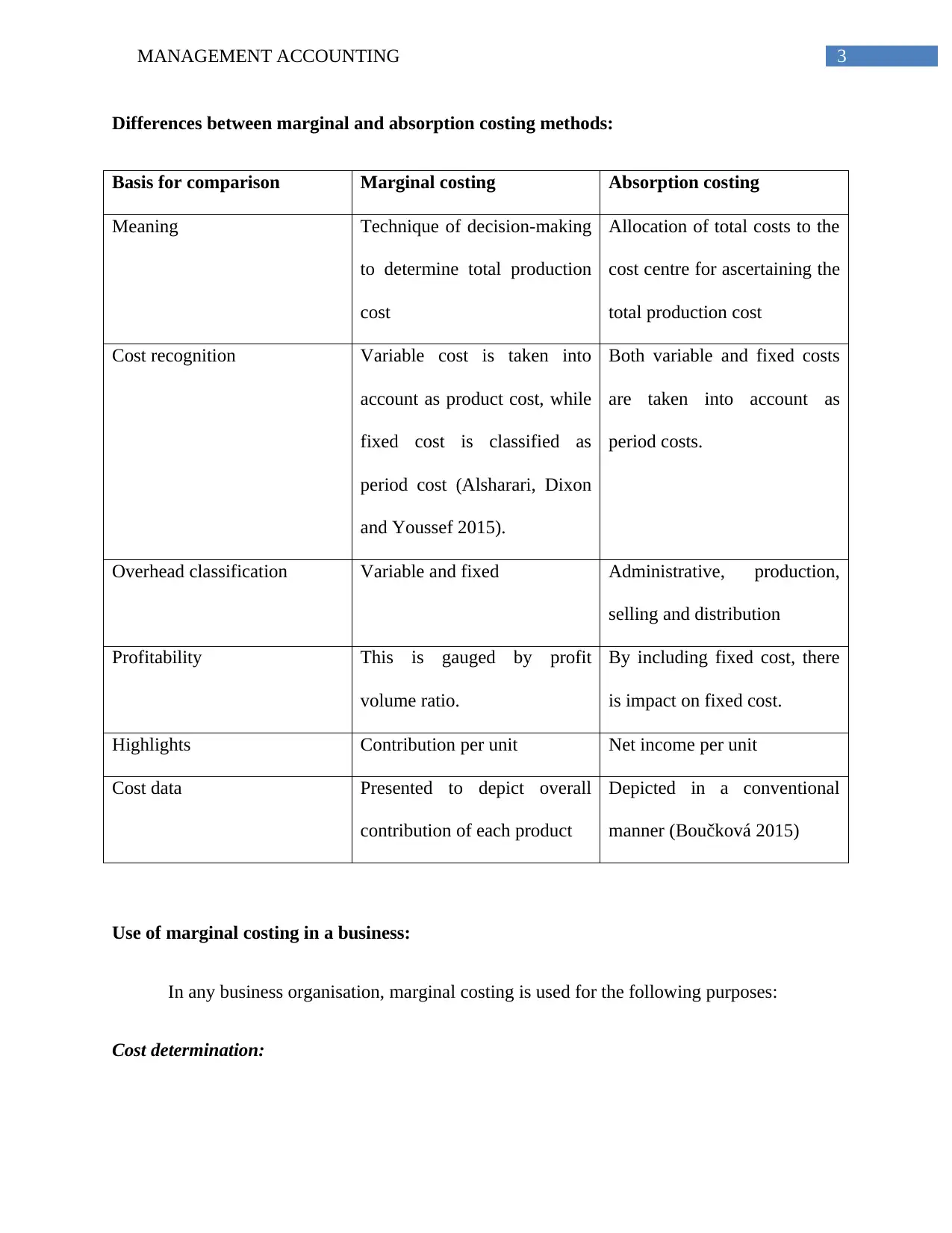

Differences between marginal and absorption costing methods:

Basis for comparison Marginal costing Absorption costing

Meaning Technique of decision-making

to determine total production

cost

Allocation of total costs to the

cost centre for ascertaining the

total production cost

Cost recognition Variable cost is taken into

account as product cost, while

fixed cost is classified as

period cost (Alsharari, Dixon

and Youssef 2015).

Both variable and fixed costs

are taken into account as

period costs.

Overhead classification Variable and fixed Administrative, production,

selling and distribution

Profitability This is gauged by profit

volume ratio.

By including fixed cost, there

is impact on fixed cost.

Highlights Contribution per unit Net income per unit

Cost data Presented to depict overall

contribution of each product

Depicted in a conventional

manner (Boučková 2015)

Use of marginal costing in a business:

In any business organisation, marginal costing is used for the following purposes:

Cost determination:

Differences between marginal and absorption costing methods:

Basis for comparison Marginal costing Absorption costing

Meaning Technique of decision-making

to determine total production

cost

Allocation of total costs to the

cost centre for ascertaining the

total production cost

Cost recognition Variable cost is taken into

account as product cost, while

fixed cost is classified as

period cost (Alsharari, Dixon

and Youssef 2015).

Both variable and fixed costs

are taken into account as

period costs.

Overhead classification Variable and fixed Administrative, production,

selling and distribution

Profitability This is gauged by profit

volume ratio.

By including fixed cost, there

is impact on fixed cost.

Highlights Contribution per unit Net income per unit

Cost data Presented to depict overall

contribution of each product

Depicted in a conventional

manner (Boučková 2015)

Use of marginal costing in a business:

In any business organisation, marginal costing is used for the following purposes:

Cost determination:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING

The technique of marginal costing assists in recording of costs and reporting as well. By

classifying costs into fixed and variable elements, it is easy to ascertain the job cost.

Cost control:

The statements of marginal costing could be understood easily by the management in

comparison to those depicted in accordance with absorption costing. The cost bifurcation into

variable and fixed costs allows the management in exercising control over the cost of production

and as a result, it affects efficiency (Bromwich and Scapens 2016). Although it is possible to

control variable costs at lower management levels, the top management only could control fixed

costs. In accordance with this technique, the management could analyse the cost behaviour at

different output and sales levels and thus, it exercises greater cost control.

Decision-making:

In the recent times, the management of an organisation is confronted with different

decision-making issues. Thus, the main criterion for choosing the suitable course of action is

profitability (Drury 2009). Some decision-making issues, which could be solved with the help of

marginal costing include product pricing, product mix, profit planning, make or buy decisions

and others.

Reasons for difference in profit/loss figures under the two methods:

In marginal costing, inventory is valued at the total variable production cost of a product

unit. On the other hand, absorption costing values inventory at the overall production cost of a

product unit (Dyson 2010). Therefore, there would be difference in inventory values at the start

and end of a period under the two costing methods. With the increase in inventory, higher profit

The technique of marginal costing assists in recording of costs and reporting as well. By

classifying costs into fixed and variable elements, it is easy to ascertain the job cost.

Cost control:

The statements of marginal costing could be understood easily by the management in

comparison to those depicted in accordance with absorption costing. The cost bifurcation into

variable and fixed costs allows the management in exercising control over the cost of production

and as a result, it affects efficiency (Bromwich and Scapens 2016). Although it is possible to

control variable costs at lower management levels, the top management only could control fixed

costs. In accordance with this technique, the management could analyse the cost behaviour at

different output and sales levels and thus, it exercises greater cost control.

Decision-making:

In the recent times, the management of an organisation is confronted with different

decision-making issues. Thus, the main criterion for choosing the suitable course of action is

profitability (Drury 2009). Some decision-making issues, which could be solved with the help of

marginal costing include product pricing, product mix, profit planning, make or buy decisions

and others.

Reasons for difference in profit/loss figures under the two methods:

In marginal costing, inventory is valued at the total variable production cost of a product

unit. On the other hand, absorption costing values inventory at the overall production cost of a

product unit (Dyson 2010). Therefore, there would be difference in inventory values at the start

and end of a period under the two costing methods. With the increase in inventory, higher profit

5MANAGEMENT ACCOUNTING

is recognised under absorption costing. On the other hand, when there is decline is inventory,

increased profit would be realised under marginal costing.

Task 2:

Part a:

There are different planning tools used for budgetary control, which are summarised

briefly as follows:

Fixed budgets:

Fixed budgets are dependent on the estimated level of output and revenue of an

organisation at the beginning of the accounting period. One major benefit of using fixed budgets

is the easy process of implementation, since static budgets are not needed to be updated

continually across the accounting periods. However, these budgets lack flexibility and if an

organisation develops budgets based on particular sales volume levels and the same increases, it

is not possible to assign additional resources (Horngren et al. 2016).

Flexible budgets:

Flexible budgets could be defined as those budgets, which adjust with changes in activity

or volume. For the costs varying with activity or volume, the flexible budget would adjust

automatically, since it includes a variable rate per activity unit rather than one fixed overall

amount. These budgets are highly useful in organisations, in which there is close alignment of

costs with the business activity like retail environment where it is possible to separate and treat

overheads in the form of fixed cost, while merchandise cost has direct association with revenues.

However, these budgets assume cost linearity and thus, they do not consider discounts for bulk

is recognised under absorption costing. On the other hand, when there is decline is inventory,

increased profit would be realised under marginal costing.

Task 2:

Part a:

There are different planning tools used for budgetary control, which are summarised

briefly as follows:

Fixed budgets:

Fixed budgets are dependent on the estimated level of output and revenue of an

organisation at the beginning of the accounting period. One major benefit of using fixed budgets

is the easy process of implementation, since static budgets are not needed to be updated

continually across the accounting periods. However, these budgets lack flexibility and if an

organisation develops budgets based on particular sales volume levels and the same increases, it

is not possible to assign additional resources (Horngren et al. 2016).

Flexible budgets:

Flexible budgets could be defined as those budgets, which adjust with changes in activity

or volume. For the costs varying with activity or volume, the flexible budget would adjust

automatically, since it includes a variable rate per activity unit rather than one fixed overall

amount. These budgets are highly useful in organisations, in which there is close alignment of

costs with the business activity like retail environment where it is possible to separate and treat

overheads in the form of fixed cost, while merchandise cost has direct association with revenues.

However, these budgets assume cost linearity and thus, they do not consider discounts for bulk

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING

orders of materials and labour costs would not behave in a linear manner unless a piecework

scheme is in place (Kamal 2015).

Incremental budgets:

Incremental budgets are those budgets developed using the budget of the previous period

or actual performance based on incremental amounts included for the new budget period. With

the help of incremental budgets, the managers could operate their departments consistently and it

is possible to avoid conflicts, if departments could be witnessed to be treated identically (Lavia

López and Hiebl 2014).

Zero-based budgets:

Zero-based budgets involve re-analysing all line items of the cash flow statement along

with validating that all expenditures are to be incurred by the particular department. With the

help of zero-based budgets, it becomes possible to identify opportunities and cost-effective

techniques of managing business operations by removing redundant or unessential activities

(Malina 2018). However, for preparing these budgets, there is need for high manpower and there

are many departments that might not have adequate time and human resources.

Variance analysis:

Variance analysis could be defined as the quantitative examination of the difference

between planned and actual behaviour. This analysis acts as a control mechanism by assisting the

managers in undertaking detailed, effective and forward-looking budgetary decisions. However,

budgeting exercise might be conducted loosely, which is bound to shift away from the actual

figures (Messner 2016).

orders of materials and labour costs would not behave in a linear manner unless a piecework

scheme is in place (Kamal 2015).

Incremental budgets:

Incremental budgets are those budgets developed using the budget of the previous period

or actual performance based on incremental amounts included for the new budget period. With

the help of incremental budgets, the managers could operate their departments consistently and it

is possible to avoid conflicts, if departments could be witnessed to be treated identically (Lavia

López and Hiebl 2014).

Zero-based budgets:

Zero-based budgets involve re-analysing all line items of the cash flow statement along

with validating that all expenditures are to be incurred by the particular department. With the

help of zero-based budgets, it becomes possible to identify opportunities and cost-effective

techniques of managing business operations by removing redundant or unessential activities

(Malina 2018). However, for preparing these budgets, there is need for high manpower and there

are many departments that might not have adequate time and human resources.

Variance analysis:

Variance analysis could be defined as the quantitative examination of the difference

between planned and actual behaviour. This analysis acts as a control mechanism by assisting the

managers in undertaking detailed, effective and forward-looking budgetary decisions. However,

budgeting exercise might be conducted loosely, which is bound to shift away from the actual

figures (Messner 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING

Part b:

By using fixed budget, it is possible to conduct variance analysis through which an

organisation could determine whether the budget is below or it has exceeded the original

estimations with the help of percentage and pounds. Thus, it is easy to plan for future years when

there is a comparison between the expected and the actual results (Nielsen, Mitchell and

Nørreklit 2015). In future, it is possible to adjust the budget down or up based on variance

percentages.

Flexible budget could be utilised more easily for updating a budget for which no

finalisation has been made on revenue or other activity figures. In this approach, the managers

provide the approval for all fixed costs and variable costs as part of revenues or other activity

measures. After this, the budgeting staffs finish the remaining part of the budget that flows

through formulas in flexible budget and expense levels are altered automatically.

Incremental budget is suitable to use, if the main cost drivers do not vary from year to

year. In this type of budget, the figures of each income and expense have started with the actual

numbers of the previous years and they are adjusted for inflation, growth in market and other

necessary factors. Thus, the previous year’s budget could be used as a benchmark after which the

management could add incremental amounts to the upcoming budget period (Otley 2016).

With the help of zero-based budgeting, higher-level strategic objectives could be

implemented into the budget process by tying them to particular functional areas of the firm, in

which it is possible to group costs initially, after which they could be gauged against past

outcomes and existing expectations. Thus, it assists in minimising costs by avoiding blanket rise

or fall in the budget of the prior period.

Part b:

By using fixed budget, it is possible to conduct variance analysis through which an

organisation could determine whether the budget is below or it has exceeded the original

estimations with the help of percentage and pounds. Thus, it is easy to plan for future years when

there is a comparison between the expected and the actual results (Nielsen, Mitchell and

Nørreklit 2015). In future, it is possible to adjust the budget down or up based on variance

percentages.

Flexible budget could be utilised more easily for updating a budget for which no

finalisation has been made on revenue or other activity figures. In this approach, the managers

provide the approval for all fixed costs and variable costs as part of revenues or other activity

measures. After this, the budgeting staffs finish the remaining part of the budget that flows

through formulas in flexible budget and expense levels are altered automatically.

Incremental budget is suitable to use, if the main cost drivers do not vary from year to

year. In this type of budget, the figures of each income and expense have started with the actual

numbers of the previous years and they are adjusted for inflation, growth in market and other

necessary factors. Thus, the previous year’s budget could be used as a benchmark after which the

management could add incremental amounts to the upcoming budget period (Otley 2016).

With the help of zero-based budgeting, higher-level strategic objectives could be

implemented into the budget process by tying them to particular functional areas of the firm, in

which it is possible to group costs initially, after which they could be gauged against past

outcomes and existing expectations. Thus, it assists in minimising costs by avoiding blanket rise

or fall in the budget of the prior period.

8MANAGEMENT ACCOUNTING

Variance analysis helps the management of an organisation in comparing the actual

results with the budgeted projections. When the budgetary variances are identified, the

management needs to find out the reasons behind such variances (Quattrone 2016). Thus, this

analysis is made for maintaining control of the business.

Part c:

There is evolvement of new business conditions over the years, in which information is

deemed to be the significant resource for gauging the firm performance along with identifying

the financial issues associated with variances found in standardised group of performance

indicators. This has resulted in different management accounting techniques setting benchmarks

and using main performance indicators for analysing firm performance reflecting the manner for

concentrating on long-term aspect of sustainability. By using budgetary control in planning and

executing different business activities, the organisations could concentrate on meeting the set

standards for the targeted outcomes for fulfilling the necessary business goals.

For this section, Tesco Plc and Sainsbury Plc are selected and these are the two giant

retailers operating in the UK retail sector. These two organisations use the following

performance indicators for solving their financial issues:

Financial indicators:

Basis Key Performance Indicators

(KPIs)

Use to identify financial

variances and issues

Solvency, debt and liquidity

ratio

Current ratio Capability of paying short-

term debts with current assets

Quick ratio Adequacy of liquid assets in

Variance analysis helps the management of an organisation in comparing the actual

results with the budgeted projections. When the budgetary variances are identified, the

management needs to find out the reasons behind such variances (Quattrone 2016). Thus, this

analysis is made for maintaining control of the business.

Part c:

There is evolvement of new business conditions over the years, in which information is

deemed to be the significant resource for gauging the firm performance along with identifying

the financial issues associated with variances found in standardised group of performance

indicators. This has resulted in different management accounting techniques setting benchmarks

and using main performance indicators for analysing firm performance reflecting the manner for

concentrating on long-term aspect of sustainability. By using budgetary control in planning and

executing different business activities, the organisations could concentrate on meeting the set

standards for the targeted outcomes for fulfilling the necessary business goals.

For this section, Tesco Plc and Sainsbury Plc are selected and these are the two giant

retailers operating in the UK retail sector. These two organisations use the following

performance indicators for solving their financial issues:

Financial indicators:

Basis Key Performance Indicators

(KPIs)

Use to identify financial

variances and issues

Solvency, debt and liquidity

ratio

Current ratio Capability of paying short-

term debts with current assets

Quick ratio Adequacy of liquid assets in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING

relation to short-term debt

Debt to equity Capital structure of a firm

representing the percent of

equity and debt for funding

assets

Working capital Capability of the organisation

in remaining solvent for

availing daily needs

Accounts payable to inventory Proportion of accounts

payable accrued to the

inventory level of the

organisation

Profitability ratios Gross margin Sales percentage left to incur

for covering its operating cost

in order to earn profit

Percentage of selling cost Used in goal-setting,

benchmarking and budgeting

Percentage of administrative

cost

Used in goal-setting,

benchmarking and budgeting

Percentage of operating cost Used in goal-setting,

benchmarking and budgeting

Percentage of finance cost Used in goal-setting,

benchmarking and budgeting

relation to short-term debt

Debt to equity Capital structure of a firm

representing the percent of

equity and debt for funding

assets

Working capital Capability of the organisation

in remaining solvent for

availing daily needs

Accounts payable to inventory Proportion of accounts

payable accrued to the

inventory level of the

organisation

Profitability ratios Gross margin Sales percentage left to incur

for covering its operating cost

in order to earn profit

Percentage of selling cost Used in goal-setting,

benchmarking and budgeting

Percentage of administrative

cost

Used in goal-setting,

benchmarking and budgeting

Percentage of operating cost Used in goal-setting,

benchmarking and budgeting

Percentage of finance cost Used in goal-setting,

benchmarking and budgeting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING

Net margin Denotes the net income earned

by the organisation

Revenue ratios Sales Provides detection of the part

of sales equation with the help

of customer relationship

management system providing

the knowledge required to

affect the same

Sales growth Measuring trends in sales and

its growth based on which

they undertake pricing

decisions (Shields 2015)

Non-financial indicators:

Human resource management In the current business environment, both

Tesco Plc and Sainsbury Plc have started to

view their staffs in the form of asset and they

consider the same as the significant influential

dynamic to ensure business success. This

comprises of acceptance of percentage of job

offers, competence surveys and others.

Product and service quality It has been identified that the issues recognised

in service or product quality of the two

Net margin Denotes the net income earned

by the organisation

Revenue ratios Sales Provides detection of the part

of sales equation with the help

of customer relationship

management system providing

the knowledge required to

affect the same

Sales growth Measuring trends in sales and

its growth based on which

they undertake pricing

decisions (Shields 2015)

Non-financial indicators:

Human resource management In the current business environment, both

Tesco Plc and Sainsbury Plc have started to

view their staffs in the form of asset and they

consider the same as the significant influential

dynamic to ensure business success. This

comprises of acceptance of percentage of job

offers, competence surveys and others.

Product and service quality It has been identified that the issues recognised

in service or product quality of the two

11MANAGEMENT ACCOUNTING

organisations have impact on their long-term

growth and this results in loss of future sales

and customer satisfaction (Van Der Stede

2015). Therefore, the organisations need to

contrast the same with competition and

satisfaction level of the customers.

Performance on these associated dimensions

has to be combined for depicting an overall

picture.

Company profile and brand awareness The measurement of company profile and

brand could signify future development and

growth (Wood and Sangster 2005). Therefore,

Tesco Plc and Sainsbury Plc are using

dimensions like increased loyalty, brand

awareness and perceived quality for generating

sales and lowering costs.

Part d:

For responding to financial problems, management accounting could help both Tesco Plc

and Sainsbury Plc in the following ways:

The managers would be needed for supporting sustainable and strategic goals with

policies and strategies to be developed

organisations have impact on their long-term

growth and this results in loss of future sales

and customer satisfaction (Van Der Stede

2015). Therefore, the organisations need to

contrast the same with competition and

satisfaction level of the customers.

Performance on these associated dimensions

has to be combined for depicting an overall

picture.

Company profile and brand awareness The measurement of company profile and

brand could signify future development and

growth (Wood and Sangster 2005). Therefore,

Tesco Plc and Sainsbury Plc are using

dimensions like increased loyalty, brand

awareness and perceived quality for generating

sales and lowering costs.

Part d:

For responding to financial problems, management accounting could help both Tesco Plc

and Sainsbury Plc in the following ways:

The managers would be needed for supporting sustainable and strategic goals with

policies and strategies to be developed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.