Management Accounting Report: Systems, Techniques, and Challenges

VerifiedAdded on 2023/01/11

|15

|4586

|39

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within the context of Cream Ltd, a medium-sized UK company specializing in desserts. The report begins by defining management accounting and its essential systems, including cost accounting, inventory management, price optimization, and job order costing. It then details various management accounting reporting methods such as account receivable aging reports, budget reports, performance reports, and inventory management reports. The analysis extends to the application and benefits of these systems, along with an examination of how these systems are integrated into organizational processes. The report further explores different costing techniques, including marginal and absorption costing, and discusses the application of management accounting techniques like standard and historical costing. Planning tools for budgetary control are also analyzed. Finally, the report addresses the use of management accounting in responding to financial issues, analyzing techniques used to deal with financial challenges. The report provides a detailed exploration of how management accounting is used to aid business decision-making within Cream Ltd.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Description of management accounting and its systems along with their essential

requirements................................................................................................................................1

P2 List of method which are used by companies to report information of management

accounting....................................................................................................................................2

M1 Application and benefits of management accounting systems used by companies..............4

D1 Analysis of the way in which systems and reporting of management accounting is

integrated with organisational processes.....................................................................................4

TASK 2............................................................................................................................................5

P3 Use of different costing techniques to determine cost and profits.........................................5

M2 Application of range of management accounting techniques...............................................7

D2 Interpretation of data..............................................................................................................7

TASK 3............................................................................................................................................7

P4 Analysis of different types of planning tools used in budgetary control................................7

M3 Use of different planning tools and their application to prepare budget and forecasts.........8

TASK 4............................................................................................................................................9

P5 Use of management accounting in responding financial issues.............................................9

M4 Analysis of techniques which are used by companies to deal with financial challenges....11

D3 Use of planning tools to deal with financial challenges......................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Description of management accounting and its systems along with their essential

requirements................................................................................................................................1

P2 List of method which are used by companies to report information of management

accounting....................................................................................................................................2

M1 Application and benefits of management accounting systems used by companies..............4

D1 Analysis of the way in which systems and reporting of management accounting is

integrated with organisational processes.....................................................................................4

TASK 2............................................................................................................................................5

P3 Use of different costing techniques to determine cost and profits.........................................5

M2 Application of range of management accounting techniques...............................................7

D2 Interpretation of data..............................................................................................................7

TASK 3............................................................................................................................................7

P4 Analysis of different types of planning tools used in budgetary control................................7

M3 Use of different planning tools and their application to prepare budget and forecasts.........8

TASK 4............................................................................................................................................9

P5 Use of management accounting in responding financial issues.............................................9

M4 Analysis of techniques which are used by companies to deal with financial challenges....11

D3 Use of planning tools to deal with financial challenges......................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is an approach which is used by managers to keep track record

of internal reports of the business. It guides employees and other internal stakeholders to make

sure that their entity is performing good or not in the market. For all the companies it is very

important to make sure that they are able to meet the predetermined goals or not and for this

purpose they are required to be aware of the concept of management accounting (Alyousef and

Mickan, 2016). While planning to enhance or improve performance it facilitates managers to

formulate strategic decisions for future. This assignment is based upon Cream Ltd which is a

medium sized company of UK and offer doughnuts, waffles and ice-creams to the customers.

Present report is focused with different topics which are management accounting systems, its

report, accounting techniques to calculate cost, planning tools for budgetary control etc. Along

with this, comparison of organisations on the basis of use of management accounting techniques

to deal with finance related problems is also covered in this project.

TASK 1

P1 Description of management accounting and its systems along with their essential

requirements

Management accounting is a technique which is mainly used for the purpose of recording

information of organisational activities that are performed for the purpose of meeting long-term

business goals. It is very important for all the companies to make sure that they are focused with

it so that effective strategies for future could be formulated. Managers of Creams Ltd are also

using it as they want to make sure that business is executed in systematic manner. For this

purpose, various types of systems are used by them. Description of them along with essential

requirements of them:

Cost accounting system: It is a management accounting system which is used by

companies for the purpose of recording information of cost which have taken place during the

accounting year. With the help of it, managers in Creams Ltd get aware of the expenses which

are arising while carrying out operations so it is used by them. The essential requirement of it for

the entity is that it guides the management to analyse costs and arrange funds accordingly to

meet them (Aouni, McGillis and Abdulkarim, 2017).

1

Management accounting is an approach which is used by managers to keep track record

of internal reports of the business. It guides employees and other internal stakeholders to make

sure that their entity is performing good or not in the market. For all the companies it is very

important to make sure that they are able to meet the predetermined goals or not and for this

purpose they are required to be aware of the concept of management accounting (Alyousef and

Mickan, 2016). While planning to enhance or improve performance it facilitates managers to

formulate strategic decisions for future. This assignment is based upon Cream Ltd which is a

medium sized company of UK and offer doughnuts, waffles and ice-creams to the customers.

Present report is focused with different topics which are management accounting systems, its

report, accounting techniques to calculate cost, planning tools for budgetary control etc. Along

with this, comparison of organisations on the basis of use of management accounting techniques

to deal with finance related problems is also covered in this project.

TASK 1

P1 Description of management accounting and its systems along with their essential

requirements

Management accounting is a technique which is mainly used for the purpose of recording

information of organisational activities that are performed for the purpose of meeting long-term

business goals. It is very important for all the companies to make sure that they are focused with

it so that effective strategies for future could be formulated. Managers of Creams Ltd are also

using it as they want to make sure that business is executed in systematic manner. For this

purpose, various types of systems are used by them. Description of them along with essential

requirements of them:

Cost accounting system: It is a management accounting system which is used by

companies for the purpose of recording information of cost which have taken place during the

accounting year. With the help of it, managers in Creams Ltd get aware of the expenses which

are arising while carrying out operations so it is used by them. The essential requirement of it for

the entity is that it guides the management to analyse costs and arrange funds accordingly to

meet them (Aouni, McGillis and Abdulkarim, 2017).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management system: All the companies which are making any type of

product or item use it so that details regarding the stock which is used to carry out operations

could be kept. In Creams Ltd. it is utilised by the management to make sure that the enterprise is

able to meet requirements of all the customers regarding doughnuts, waffles and ice creams by

managing the items that are required to make them. There are three types of it which could be

used by entities according to their requirements. All of them are as follows:

LIFO: When this inventory management system is used by enterprises then they make

sure that recently bought items are used to make products.

FIFO: If it is used by companies then already purchased goods are used to make the

final product.

AVCO: In this system of inventory management the goods are used for business on the

basis of their average cost.

From all the above described systems of inventory management first in first out method is

used in Creams Ltd. Its essential requirement for the company is to use fresh and good quality

goods to make all the items ordered by the customers (Arunruangsirilert and Chonglerttham,

2017).

Price optimisation system: All the organisations which are focused with meeting the

long-term business goals by attracting large number of customers use it because it helps them to

set appropriate price for all the products that are sold by them. In order to determine the right

price for all the items that are sold by Creams Ltd to its customers this system is used by the

entity. It is essentially required for the organisation because it can help to decide best suitable

price for all the items that can help to meet expectations of customers.

Job order costing system: When entities want to keep track record of all the activities

that are performed by them then it is used as it is highly focused with performing all the jobs

according to specifications of customers. In Creams Ltd. it is used by management so that the

managers can record the requirements of clients separately and try to meet them all. It is very

important for the enterprise to use it as it facilitates to meet the demand of targeted audience

(Bedford and Speklé, 2018).

P2 List of method which are used by companies to report information of management accounting

When an organisation records information of all its activities in different reports then it is

known as management accounting reporting. While formulating strategies for future it is very

2

product or item use it so that details regarding the stock which is used to carry out operations

could be kept. In Creams Ltd. it is utilised by the management to make sure that the enterprise is

able to meet requirements of all the customers regarding doughnuts, waffles and ice creams by

managing the items that are required to make them. There are three types of it which could be

used by entities according to their requirements. All of them are as follows:

LIFO: When this inventory management system is used by enterprises then they make

sure that recently bought items are used to make products.

FIFO: If it is used by companies then already purchased goods are used to make the

final product.

AVCO: In this system of inventory management the goods are used for business on the

basis of their average cost.

From all the above described systems of inventory management first in first out method is

used in Creams Ltd. Its essential requirement for the company is to use fresh and good quality

goods to make all the items ordered by the customers (Arunruangsirilert and Chonglerttham,

2017).

Price optimisation system: All the organisations which are focused with meeting the

long-term business goals by attracting large number of customers use it because it helps them to

set appropriate price for all the products that are sold by them. In order to determine the right

price for all the items that are sold by Creams Ltd to its customers this system is used by the

entity. It is essentially required for the organisation because it can help to decide best suitable

price for all the items that can help to meet expectations of customers.

Job order costing system: When entities want to keep track record of all the activities

that are performed by them then it is used as it is highly focused with performing all the jobs

according to specifications of customers. In Creams Ltd. it is used by management so that the

managers can record the requirements of clients separately and try to meet them all. It is very

important for the enterprise to use it as it facilitates to meet the demand of targeted audience

(Bedford and Speklé, 2018).

P2 List of method which are used by companies to report information of management accounting

When an organisation records information of all its activities in different reports then it is

known as management accounting reporting. While formulating strategies for future it is very

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

important to analyse all the internal report so that best options for performing operational

activities in future could be determined and selected. There are various methods or report that are

used for management accounting reporting in Creams Ltd. These are used by the managers to

make sure that they are having detailed and accurate information of all the activities of

organisation. Discussion of all of them is as follows:

Account receivable aging report: Some of the companies which are offering credit

facilities to the customers generate their report to keep information about them. Managers of

Creams Ltd use it to record the same details and make sure that they get all the payments from

the credit clients on time. It is beneficial for the entity because with the help of it, the owed

amount which is not yet paid by the debtors could be determined and they could be asked to

make the payment as soon as possible (Black, 2017).

Budget report: It can be defined as a report which is focused with recording information

of funds that are required to be allocated to different departments of the company so that they

can meet the obligations that are set by management for them. Managers of Creams Ltd. also

formulate it in order to make sure that appropriate amount is assigned to all the functional units

which are working for benefit of the organisation. It is very beneficial for the entity because with

the help of it all the pre-planned activities are carried out smoothly (Charifzadeh and Taschner,

2017).

Performance report: It is very important for all the business entities to keep track record

of performance of business so that timely modifications could be made in the strategies. This

type of information is recorded in performance report and it also keep the details of presentation

of employees. Creams Ltd. is creating it to make sure that it performs well in the market and the

staff members who are contributing in its growth get benefits for their contribution. The main

advantage of using is that it helps in motivating employees by providing them incentives

according to tehri performance. Apart from this it also helps to make efforts to improve the

position of company by making changes in the strategies (Dávila, 2019).

Inventory management report: It is mainly formulated by such companies that are

selling some tangible items to the customers so that information of goods could be kept in

records. Creams Ltd. use it to analyse that it is able to keep the sufficient items that are required

to meet the expectations or orders of customers regarding Doughnuts, Waffles and Ice creams. It

3

activities in future could be determined and selected. There are various methods or report that are

used for management accounting reporting in Creams Ltd. These are used by the managers to

make sure that they are having detailed and accurate information of all the activities of

organisation. Discussion of all of them is as follows:

Account receivable aging report: Some of the companies which are offering credit

facilities to the customers generate their report to keep information about them. Managers of

Creams Ltd use it to record the same details and make sure that they get all the payments from

the credit clients on time. It is beneficial for the entity because with the help of it, the owed

amount which is not yet paid by the debtors could be determined and they could be asked to

make the payment as soon as possible (Black, 2017).

Budget report: It can be defined as a report which is focused with recording information

of funds that are required to be allocated to different departments of the company so that they

can meet the obligations that are set by management for them. Managers of Creams Ltd. also

formulate it in order to make sure that appropriate amount is assigned to all the functional units

which are working for benefit of the organisation. It is very beneficial for the entity because with

the help of it all the pre-planned activities are carried out smoothly (Charifzadeh and Taschner,

2017).

Performance report: It is very important for all the business entities to keep track record

of performance of business so that timely modifications could be made in the strategies. This

type of information is recorded in performance report and it also keep the details of presentation

of employees. Creams Ltd. is creating it to make sure that it performs well in the market and the

staff members who are contributing in its growth get benefits for their contribution. The main

advantage of using is that it helps in motivating employees by providing them incentives

according to tehri performance. Apart from this it also helps to make efforts to improve the

position of company by making changes in the strategies (Dávila, 2019).

Inventory management report: It is mainly formulated by such companies that are

selling some tangible items to the customers so that information of goods could be kept in

records. Creams Ltd. use it to analyse that it is able to keep the sufficient items that are required

to meet the expectations or orders of customers regarding Doughnuts, Waffles and Ice creams. It

3

is advantageous for the enterprise because with the help of it, possibility of lack of goods to meet

expectation of customers could be ignored.

M1 Application and benefits of management accounting systems used by companies

There are various types of management accounting systems which are used by Creams Ltd.

Application and benefit of all of them are as follows:

Inventory management system: In Creams Ltd it is used by the managers as it helps

them to make sure that they use inventory properly for meeting requirements of

customers.

Cost accounting system: It is applied within Creams Ltd because with the help of it the

managers can determine the costs of all the activities and make arrangements of funds to

meet them.

Job order costing system: This management accounting system benefits Creams Ltd by

analyse the cost of all the activities that are performed according to specifications of

customers therefore it is used within the entity.

Price optimisation system: Managers of Creams Ltd are using this system as it helps

them to analyse the best price for its products that can help to meet expectations of

customers.

D1 Analysis of the way in which systems and reporting of management accounting is integrated

with organisational processes

Creams Ltd. is a medium sized entity of United Kingdom which is dealing in different

types of deserts such as doughnuts, waffles and ice creams. In order to perform the operations

properly the entity uses different management accounting systems such as cost accounting,

inventory management, job order costing and price optimisation. On the other hand, different

report such as performance, account receivable, budget and inventory management are also

generated by the managers. All of them are integrated with the organisational processes. For

example, account receivable helps to formulate or tighten the credit policies by analysing the

outstanding amount by the defaulters. Price optimisation system is used to formulate pricing

policies to meet the expectations of customers.

4

expectation of customers could be ignored.

M1 Application and benefits of management accounting systems used by companies

There are various types of management accounting systems which are used by Creams Ltd.

Application and benefit of all of them are as follows:

Inventory management system: In Creams Ltd it is used by the managers as it helps

them to make sure that they use inventory properly for meeting requirements of

customers.

Cost accounting system: It is applied within Creams Ltd because with the help of it the

managers can determine the costs of all the activities and make arrangements of funds to

meet them.

Job order costing system: This management accounting system benefits Creams Ltd by

analyse the cost of all the activities that are performed according to specifications of

customers therefore it is used within the entity.

Price optimisation system: Managers of Creams Ltd are using this system as it helps

them to analyse the best price for its products that can help to meet expectations of

customers.

D1 Analysis of the way in which systems and reporting of management accounting is integrated

with organisational processes

Creams Ltd. is a medium sized entity of United Kingdom which is dealing in different

types of deserts such as doughnuts, waffles and ice creams. In order to perform the operations

properly the entity uses different management accounting systems such as cost accounting,

inventory management, job order costing and price optimisation. On the other hand, different

report such as performance, account receivable, budget and inventory management are also

generated by the managers. All of them are integrated with the organisational processes. For

example, account receivable helps to formulate or tighten the credit policies by analysing the

outstanding amount by the defaulters. Price optimisation system is used to formulate pricing

policies to meet the expectations of customers.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

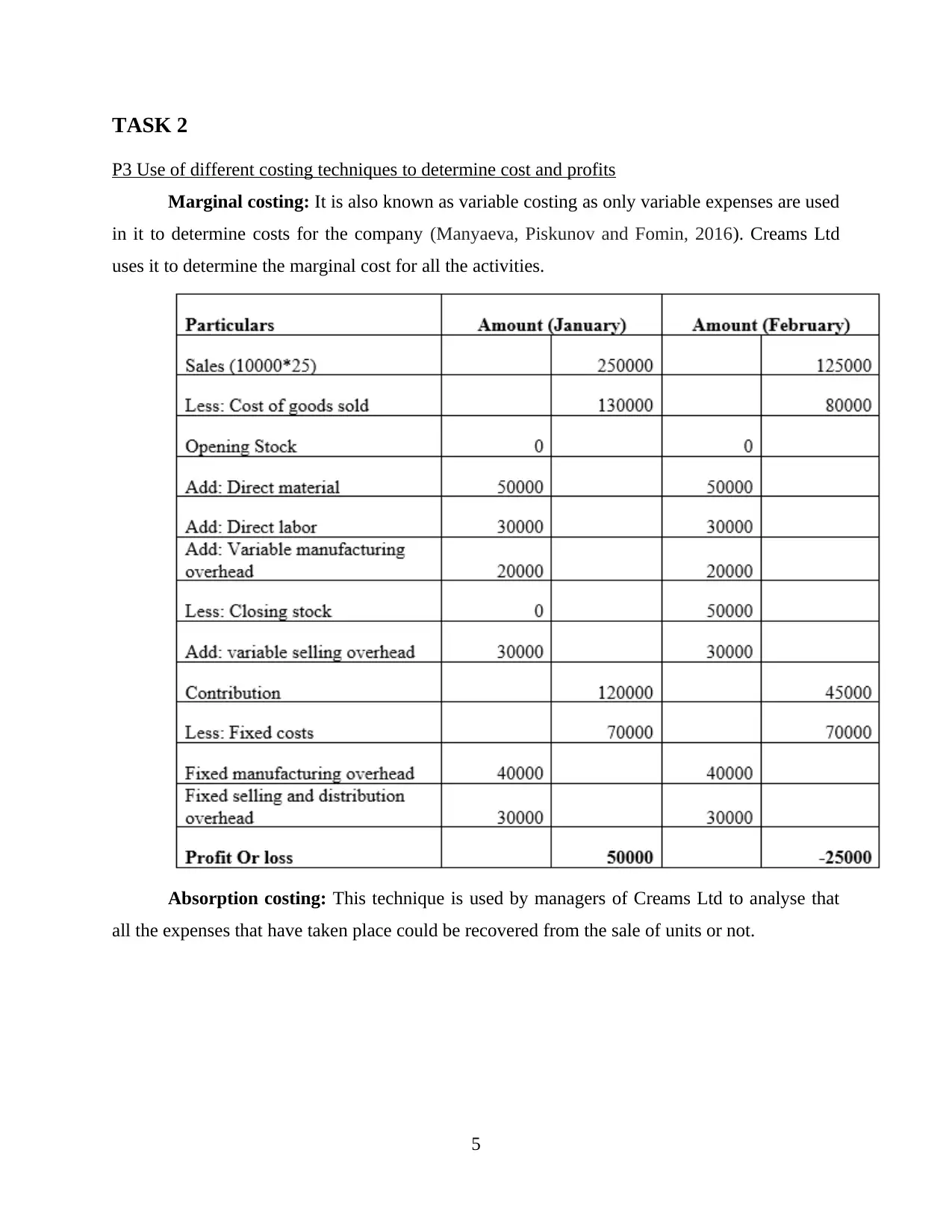

P3 Use of different costing techniques to determine cost and profits

Marginal costing: It is also known as variable costing as only variable expenses are used

in it to determine costs for the company (Manyaeva, Piskunov and Fomin, 2016). Creams Ltd

uses it to determine the marginal cost for all the activities.

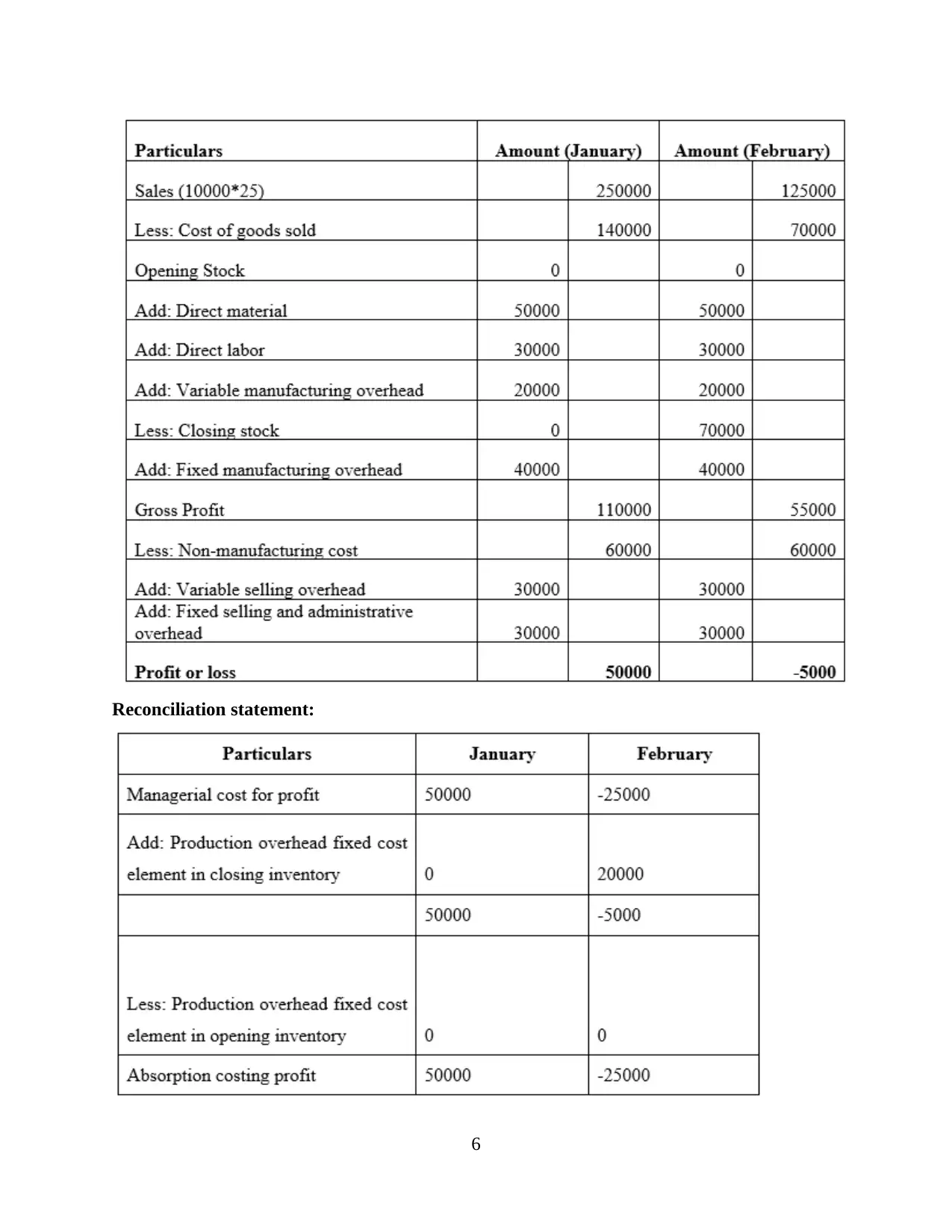

Absorption costing: This technique is used by managers of Creams Ltd to analyse that

all the expenses that have taken place could be recovered from the sale of units or not.

5

P3 Use of different costing techniques to determine cost and profits

Marginal costing: It is also known as variable costing as only variable expenses are used

in it to determine costs for the company (Manyaeva, Piskunov and Fomin, 2016). Creams Ltd

uses it to determine the marginal cost for all the activities.

Absorption costing: This technique is used by managers of Creams Ltd to analyse that

all the expenses that have taken place could be recovered from the sale of units or not.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Reconciliation statement:

6

6

M2 Application of range of management accounting techniques

Creams Ltd. can apply various types of management accounting techniques to formulate

the income statements and analyse profits along with costs. Description of some of the is as

follows:

Standard costing: This technique is used by companies to analyse that they are able to

meet the predetermined standards or not. In Creams Ltd. it could be used to assess that the

standards that are set by the entity for meeting long term business goals are met or not. Apart

from this, it can also be used to analyse variance between the budgeted and actual figures.

Historical costing: This costing technique states that all the entities should evaluate the

assets on their actual cost rather than the market price as it can help to analyse their accurate

value. By using it Creams Ltd will also be able to record all the assets in their actual value in the

books.

D2 Interpretation of data

From the income statement of marginal costing it has been determined that when it will be

used by the company then the total profits for January will be 50000 and for February t will

result in loss of 25000. On the other hand, absorption costing will create profits of 50000 for

January and for February the losses will be 5000.

TASK 3

P4 Analysis of different types of planning tools used in budgetary control

Budget is an essential element which is required to be focused by all the organisations to

maintain the performance of company. In order to make sure that all the activities are performed

properly it is very important for the top-level managers to make sure that they are managing

budgets and assigning appropriate funds to different divisions of company. While planning to

reduce overspending of funds budgetary control is focused (Mueller and Trost, 2017). In Creams

Ltd different types of planning tools are used by the management which are discussed below:

Flexible budget: It is a budget in which modifications could be made according to

changes in the money spent on different activities. It is used by managers of Creams Ltd. to be

updated about the latest expenses that are made by the entity.

Advantages: It is very sophisticated and useful as compared to other budgets as it

provides accurate information about position of the company. It is also beneficial to

7

Creams Ltd. can apply various types of management accounting techniques to formulate

the income statements and analyse profits along with costs. Description of some of the is as

follows:

Standard costing: This technique is used by companies to analyse that they are able to

meet the predetermined standards or not. In Creams Ltd. it could be used to assess that the

standards that are set by the entity for meeting long term business goals are met or not. Apart

from this, it can also be used to analyse variance between the budgeted and actual figures.

Historical costing: This costing technique states that all the entities should evaluate the

assets on their actual cost rather than the market price as it can help to analyse their accurate

value. By using it Creams Ltd will also be able to record all the assets in their actual value in the

books.

D2 Interpretation of data

From the income statement of marginal costing it has been determined that when it will be

used by the company then the total profits for January will be 50000 and for February t will

result in loss of 25000. On the other hand, absorption costing will create profits of 50000 for

January and for February the losses will be 5000.

TASK 3

P4 Analysis of different types of planning tools used in budgetary control

Budget is an essential element which is required to be focused by all the organisations to

maintain the performance of company. In order to make sure that all the activities are performed

properly it is very important for the top-level managers to make sure that they are managing

budgets and assigning appropriate funds to different divisions of company. While planning to

reduce overspending of funds budgetary control is focused (Mueller and Trost, 2017). In Creams

Ltd different types of planning tools are used by the management which are discussed below:

Flexible budget: It is a budget in which modifications could be made according to

changes in the money spent on different activities. It is used by managers of Creams Ltd. to be

updated about the latest expenses that are made by the entity.

Advantages: It is very sophisticated and useful as compared to other budgets as it

provides accurate information about position of the company. It is also beneficial to

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

determine the actual sales level after modifications so that estimation of future sales

could be performed.

Disadvantages: The time required to prepare is very high as continuous modifications

made in it according to the changes in expenses and sales level. Apart from this, it is very

confusing as it has multiple figures to reflect the organisational data.

Zero based budget: It is mainly used by companies to analyse the accurate transactions

and other expenses that are made in a specific year as it starts with a zero balance. In Cream Ltd.

managers are using it to make sure that they estimate the future expenses properly or not by

analysing the records of this budget (Nielsen, 2018).

Advantages: It helps to allocate the funds effectively to all the divisions according to

requirements. It also helps to detect the inflated budget so that possibility of negative

impact of them upon business could be reduced.

Disadvantages: When the entity is not able to estimate the future income then it will be

very difficult to make this budget. In order to prepare it proper experience is required for

which the entities are required to hire a skilled manager which costs very high.

Activity-based budget: This type of budget is focused with the recording of information

of all the activities which are resulting in costs for the entity (Phan, Baird and Su, 2017).

Mangers of Creams Ltd. are using it to determine cost of different activities that are performed

by them so that appropriate funds could be allocated to them according to their requirements.

Advantages: With the help of it, all the activities which are unnecessary could eliminated

so that cost of business could be saved. It also facilitates to gain competitive advantage in

the market.

Disadvantages: The major drawback of activity-based budget is that it is very costly

method to implement and very expensive as compare to the traditional method of

preparing budgets. On the other hand, technical details are also required to maintain the

costs in this method.

M3 Use of different planning tools and their application to prepare budget and forecasts

Managers of Creams Ltd are using different types of planning tools for the purpose of

maintaining budgets and prepare them. These are flexible, zero based and activity-based budget.

All of them are used in budgetary control so that non-essential exploitation of budget could be

controlled. All these planning tools help to analyse the requirements of the business and then

8

could be performed.

Disadvantages: The time required to prepare is very high as continuous modifications

made in it according to the changes in expenses and sales level. Apart from this, it is very

confusing as it has multiple figures to reflect the organisational data.

Zero based budget: It is mainly used by companies to analyse the accurate transactions

and other expenses that are made in a specific year as it starts with a zero balance. In Cream Ltd.

managers are using it to make sure that they estimate the future expenses properly or not by

analysing the records of this budget (Nielsen, 2018).

Advantages: It helps to allocate the funds effectively to all the divisions according to

requirements. It also helps to detect the inflated budget so that possibility of negative

impact of them upon business could be reduced.

Disadvantages: When the entity is not able to estimate the future income then it will be

very difficult to make this budget. In order to prepare it proper experience is required for

which the entities are required to hire a skilled manager which costs very high.

Activity-based budget: This type of budget is focused with the recording of information

of all the activities which are resulting in costs for the entity (Phan, Baird and Su, 2017).

Mangers of Creams Ltd. are using it to determine cost of different activities that are performed

by them so that appropriate funds could be allocated to them according to their requirements.

Advantages: With the help of it, all the activities which are unnecessary could eliminated

so that cost of business could be saved. It also facilitates to gain competitive advantage in

the market.

Disadvantages: The major drawback of activity-based budget is that it is very costly

method to implement and very expensive as compare to the traditional method of

preparing budgets. On the other hand, technical details are also required to maintain the

costs in this method.

M3 Use of different planning tools and their application to prepare budget and forecasts

Managers of Creams Ltd are using different types of planning tools for the purpose of

maintaining budgets and prepare them. These are flexible, zero based and activity-based budget.

All of them are used in budgetary control so that non-essential exploitation of budget could be

controlled. All these planning tools help to analyse the requirements of the business and then

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

allocate funds accordingly. With the help of them long term business goals could be met which

help to grow the business. For example, activity-based budget help to analyse the requirement of

different activities and then the managers can assign monetary resources of them so that all the

predetermined objectives of the company could be accomplished successfully.

TASK 4

P5 Use of management accounting in responding financial issues

When an organisation is not having sufficient funds to meet obligations of business then

it results in financial challenges. It is very important for all the companies to deal with all of

them properly so that possibility of their negative impact upon the business could be reduced.

Some specific finance related problems that are faced by Creams Ltd. are as follows:

Improper money management system: This problem takes place when accounting

professional of an organisation are not able to manage the funds properly by using right

principles, rules and regulations of accounting. In Creams Ltd this problem is creating financial

issues because of it the managers are not aware of actual funds that are available for future

activities (Sedevich-Fons, L., 2018).

Insufficient funds for operations because of delayed payments from debtors: When

an entity is not able to receive the owed amount from the clients on time then it may also result

in financial issues which will affect the execution of operations. Some of the customers of

Creams Ltd. are not able to make payments on time and due to this the entity is facing the

challenges related to availability of finance.

In order to identify and respond to all the above described financial problems the

managers of Creams Ltd are using following techniques:

Benchmarking: This technique is mainly used for comparison of an entity with another

one so that the elements that are resulting in business issues could be identified properly. In

Creams Ltd it is used by the managers for the purpose of identifying the problem of delayed

payments from the debtors so that sufficient funds for operations could be arranged. It guides the

managers to determine the major errors in the credit policies by comparing it with a competitor

and the make changes in it (Shields and Shelleman, 2016).

Key performance indicator: It is also a technique which is used to identify the issues

for business. With the help of it, errors in the management of business could be determined by

9

help to grow the business. For example, activity-based budget help to analyse the requirement of

different activities and then the managers can assign monetary resources of them so that all the

predetermined objectives of the company could be accomplished successfully.

TASK 4

P5 Use of management accounting in responding financial issues

When an organisation is not having sufficient funds to meet obligations of business then

it results in financial challenges. It is very important for all the companies to deal with all of

them properly so that possibility of their negative impact upon the business could be reduced.

Some specific finance related problems that are faced by Creams Ltd. are as follows:

Improper money management system: This problem takes place when accounting

professional of an organisation are not able to manage the funds properly by using right

principles, rules and regulations of accounting. In Creams Ltd this problem is creating financial

issues because of it the managers are not aware of actual funds that are available for future

activities (Sedevich-Fons, L., 2018).

Insufficient funds for operations because of delayed payments from debtors: When

an entity is not able to receive the owed amount from the clients on time then it may also result

in financial issues which will affect the execution of operations. Some of the customers of

Creams Ltd. are not able to make payments on time and due to this the entity is facing the

challenges related to availability of finance.

In order to identify and respond to all the above described financial problems the

managers of Creams Ltd are using following techniques:

Benchmarking: This technique is mainly used for comparison of an entity with another

one so that the elements that are resulting in business issues could be identified properly. In

Creams Ltd it is used by the managers for the purpose of identifying the problem of delayed

payments from the debtors so that sufficient funds for operations could be arranged. It guides the

managers to determine the major errors in the credit policies by comparing it with a competitor

and the make changes in it (Shields and Shelleman, 2016).

Key performance indicator: It is also a technique which is used to identify the issues

for business. With the help of it, errors in the management of business could be determined by

9

evaluating success or failure of business projects. There are two main types of it which are as

follows:

Financial KPI: It is highly focused with the identification of financial problems that are

affecting business in negative manner.

Non-Financial KPI: This KPI is used by companies to analyse mistakes in non-financial

activities such as supply chain, distribution management etc.

From both of KPIs the managers in Creams Ltd are using financial KPI to identify the

problem of improper money management as it will help them to analyse it properly and analyse

the issues which are making it weaker (Sugahara, Daidj and Ushio, 2017).

Financial governance: This technique is mainly focused with principles, rules and

regulations that should be focused by the organisations to carry out operational smoothly. While

planning to deal with the financial challenges that are faced by the organisation. With the help of

it, they try to formulate all the accounts according to specific rules and regulations which will

help to respond the problems properly.

Comparison:

Creams Ltd. Madame Waffle

The managers of the company are using cost

accounting system of management accounting

so that they can deal with the problem of

improper money management. With the help of

it they try to manage the costs properly and

respond to the business challenge (Tucker and

Lawson, 2016).

Managers within the entity are using job order

costing to deal with the problem of lack of

funds for operations as it guides them to

analyse requirements of all the activities and

arrange funding for the same.

In order to deal with the problem of late

payments from clients the entity is using price

optimisation system so that appropriate price

for all the products could be set and the

willingness of them for asking credit could be

reduced.

The enterprise is dealing with the problem of

weak management of inventory and to deal

with it the managers are using inventory

management system which helps to manage

stock properly (Yigitbasioglu, 2016).

10

follows:

Financial KPI: It is highly focused with the identification of financial problems that are

affecting business in negative manner.

Non-Financial KPI: This KPI is used by companies to analyse mistakes in non-financial

activities such as supply chain, distribution management etc.

From both of KPIs the managers in Creams Ltd are using financial KPI to identify the

problem of improper money management as it will help them to analyse it properly and analyse

the issues which are making it weaker (Sugahara, Daidj and Ushio, 2017).

Financial governance: This technique is mainly focused with principles, rules and

regulations that should be focused by the organisations to carry out operational smoothly. While

planning to deal with the financial challenges that are faced by the organisation. With the help of

it, they try to formulate all the accounts according to specific rules and regulations which will

help to respond the problems properly.

Comparison:

Creams Ltd. Madame Waffle

The managers of the company are using cost

accounting system of management accounting

so that they can deal with the problem of

improper money management. With the help of

it they try to manage the costs properly and

respond to the business challenge (Tucker and

Lawson, 2016).

Managers within the entity are using job order

costing to deal with the problem of lack of

funds for operations as it guides them to

analyse requirements of all the activities and

arrange funding for the same.

In order to deal with the problem of late

payments from clients the entity is using price

optimisation system so that appropriate price

for all the products could be set and the

willingness of them for asking credit could be

reduced.

The enterprise is dealing with the problem of

weak management of inventory and to deal

with it the managers are using inventory

management system which helps to manage

stock properly (Yigitbasioglu, 2016).

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.