Management Accounting Report: Cost Analysis and Reporting for SMEs

VerifiedAdded on 2020/01/28

|16

|5198

|482

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and practices, using Portfolio Payroll Limited, a London-based SME, as a case study. The introduction establishes the significance of management accounting in today's competitive business environment, differentiating it from financial accounting and highlighting its role in internal decision-making. Task 1 delves into the requirements of management accounting systems for SMEs, discussing the importance of planning, decision-making, and control, along with methods for management accounting reporting, including financial planning, financial statement analysis, and budgetary control. The benefits and usage of management accounting systems, such as traditional cost accounting, lean accounting, and transfer pricing, are also explored. Task 2 focuses on cost calculation methods, specifically marginal and absorption costing, providing advantages, and disadvantages of each. The report covers topics like financial planning, cost analysis, and reporting methods to improve the operational efficiency of a business. The report concludes by summarizing the key findings and emphasizes the importance of effective management accounting for business success and expansion. References are provided for further reading.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

TASK 2.................................................................................................................................................6

TASK 3...............................................................................................................................................10

TASK 4...............................................................................................................................................13

CONCLUSION..................................................................................................................................15

REFERENCES...................................................................................................................................17

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

TASK 2.................................................................................................................................................6

TASK 3...............................................................................................................................................10

TASK 4...............................................................................................................................................13

CONCLUSION..................................................................................................................................15

REFERENCES...................................................................................................................................17

INTRODUCTION

Management accounting is the process of managing reports and accounts that helps in

providing accurate and timely financial and statistical information obtained by the managers in

order to record day to day short term decisions. Unlikely financial accounting helps in producing

annual reports that is mainly useful for external stakeholders and thus they use the accounts in terms

of generating monthly or weekly reports for business internal audiences such as departmental

managers (Christ and et.al., 2017). However, such reports are introduces in regard to identify the

amount of available cash, sales revenue generated, inventory in hand and raw material etc. It is also

beneficial in terms of trend charts, variance analysis and other statistical information so that data

could be collected in terms of improving business performance. In the present report the small

medium enterprise taken is Portfolio payroll limited. It is situated in london aand started in 2002.

The number of employee in portfolio payroll limited is 50 and revenue generated by them in 2016 is

11.1 million.The report has primary focus on management accounting and also indicate the

requirement for small business enterprises to use management accounting system for further

expansion. Methods for management accounting reporting are also discussed for better

understanding.

TASK 1

P1 Management accounting and Requirement of management accounting systems

In current scenario organizations are facing fierce competition, to sustain and survive.

Managers have to use and create the accounting provisions in order to perform better. Management

accounting includes planning, decision making, controlling and providing expertise in financial

reporting so that organizational goals can be achieve smoothly. Management accounting use by

managers within the organization and provide information for their use. Management accounting

emphasize decision which affects the future of the organization, it also emphasize relevancy of

activity with business, timeliness and proper report of particular segment (Deegan, 2013).

Portfolio payroll limited a London based employment agency also consider management

accounting in their operational activity. AS portfolio payroll is small and medium enterprise so their

objectives and mission are more vulnerable to achieve, it makes compulsory for them to use

management accounting activities. Concept of target costing allows them to timely monitor the

needs and possibilities of consumers, on the basis of this the direction become prudent to improve

enterprise activity.

An accounting system is an important tool whose existence is undoubtedly necessary. A

small medium enterprise should be always in a position where they have information about what

Management accounting is the process of managing reports and accounts that helps in

providing accurate and timely financial and statistical information obtained by the managers in

order to record day to day short term decisions. Unlikely financial accounting helps in producing

annual reports that is mainly useful for external stakeholders and thus they use the accounts in terms

of generating monthly or weekly reports for business internal audiences such as departmental

managers (Christ and et.al., 2017). However, such reports are introduces in regard to identify the

amount of available cash, sales revenue generated, inventory in hand and raw material etc. It is also

beneficial in terms of trend charts, variance analysis and other statistical information so that data

could be collected in terms of improving business performance. In the present report the small

medium enterprise taken is Portfolio payroll limited. It is situated in london aand started in 2002.

The number of employee in portfolio payroll limited is 50 and revenue generated by them in 2016 is

11.1 million.The report has primary focus on management accounting and also indicate the

requirement for small business enterprises to use management accounting system for further

expansion. Methods for management accounting reporting are also discussed for better

understanding.

TASK 1

P1 Management accounting and Requirement of management accounting systems

In current scenario organizations are facing fierce competition, to sustain and survive.

Managers have to use and create the accounting provisions in order to perform better. Management

accounting includes planning, decision making, controlling and providing expertise in financial

reporting so that organizational goals can be achieve smoothly. Management accounting use by

managers within the organization and provide information for their use. Management accounting

emphasize decision which affects the future of the organization, it also emphasize relevancy of

activity with business, timeliness and proper report of particular segment (Deegan, 2013).

Portfolio payroll limited a London based employment agency also consider management

accounting in their operational activity. AS portfolio payroll is small and medium enterprise so their

objectives and mission are more vulnerable to achieve, it makes compulsory for them to use

management accounting activities. Concept of target costing allows them to timely monitor the

needs and possibilities of consumers, on the basis of this the direction become prudent to improve

enterprise activity.

An accounting system is an important tool whose existence is undoubtedly necessary. A

small medium enterprise should be always in a position where they have information about what

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

they owns and what they owe, whether they are generating any profit or not. Whether they are in a

position to meet all their long term commitments, Gathering all the information can be a crucial task

for an small business enterprise, here management accounting systems came into the existence.

Management accounting systems collects all the financial data from business operations such as

sales data, track the cost associated with the production of goods and services, shifts occurrence in

inventory and changes in raw material costs and then convert all the information in a way that it can

be analysed (DRURY, 2013).

It is always consider as smart decision to go after that management accounting system which

integrates with the organization's financial system. For allocate the cost related to direct labour,

direct material and manufacturing overhead the common management accounting system used are

job order or process costing method.

Lean accounting is one of the widely used management accounting system technique, rather

than focusing only on the cost factor lean accounting is useful in making strategy for reducing cost

and eliminate waste.

Transfer pricing is another method comes under management accounting system umbrella,

In these method companies will cost goods as they move or transfer in different departments

because each product transfer to different departments adding significant cost to thje product.

Depending on the type of the project and work and the time sensitivity of the information

management may required reports quarterly, monthly, weekly or even daily (Fullerton, Kennedy

and Widener, 2013). Budget reports are also the part of the small business as they provide the

information about over all performance. The account receivables aging reports are use to managing

cash flow for companies that extend credit to their customer. Job cost reports are used for figure out

the expenses for a specific project or task.

P2 Methods used for management accounting reporting

Competitiveness among the enterprises are substantially increasing, for cop-up with it there

are various methods, concepts and techniques are use for reporting in managerial accounting.

Portfolio payroll limited uses ample of management accounting reporting techniques to comply

with their strategic goals and objectives, the method use by payment payroll limited is following

below-

Financial planning method is come into the existence right after enterprise vision and

objectives have been set. By the use of these method enterprise try to determine how a business will

afford to achieve goals and objectives. Effective financial planning consist with both long term ansd

short term objectives of the enterprise (Zimmerman and Yahya-Zadeh, 2011). Formulating financial

policies, assess the business environment, quantify the amount of resources required to achive

position to meet all their long term commitments, Gathering all the information can be a crucial task

for an small business enterprise, here management accounting systems came into the existence.

Management accounting systems collects all the financial data from business operations such as

sales data, track the cost associated with the production of goods and services, shifts occurrence in

inventory and changes in raw material costs and then convert all the information in a way that it can

be analysed (DRURY, 2013).

It is always consider as smart decision to go after that management accounting system which

integrates with the organization's financial system. For allocate the cost related to direct labour,

direct material and manufacturing overhead the common management accounting system used are

job order or process costing method.

Lean accounting is one of the widely used management accounting system technique, rather

than focusing only on the cost factor lean accounting is useful in making strategy for reducing cost

and eliminate waste.

Transfer pricing is another method comes under management accounting system umbrella,

In these method companies will cost goods as they move or transfer in different departments

because each product transfer to different departments adding significant cost to thje product.

Depending on the type of the project and work and the time sensitivity of the information

management may required reports quarterly, monthly, weekly or even daily (Fullerton, Kennedy

and Widener, 2013). Budget reports are also the part of the small business as they provide the

information about over all performance. The account receivables aging reports are use to managing

cash flow for companies that extend credit to their customer. Job cost reports are used for figure out

the expenses for a specific project or task.

P2 Methods used for management accounting reporting

Competitiveness among the enterprises are substantially increasing, for cop-up with it there

are various methods, concepts and techniques are use for reporting in managerial accounting.

Portfolio payroll limited uses ample of management accounting reporting techniques to comply

with their strategic goals and objectives, the method use by payment payroll limited is following

below-

Financial planning method is come into the existence right after enterprise vision and

objectives have been set. By the use of these method enterprise try to determine how a business will

afford to achieve goals and objectives. Effective financial planning consist with both long term ansd

short term objectives of the enterprise (Zimmerman and Yahya-Zadeh, 2011). Formulating financial

policies, assess the business environment, quantify the amount of resources required to achive

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

objectives, setting budget and identify the risk and issues that may be occurred are the major area

where an enterprise financial planning focus on. The other method which used in management

accounting reporting is analysis of the financial statement, by the use of it payment payroll figure

out the significance of financial data and forecast it for achieve and set the future goals.

Historical cost accounting methods use by portfolio payroll for determine the past data to the

management relating to the cost of each job. Generally accepted accounting principles (GAAP) is a

basic way to figure out the result of historical cost accounting.

Standard costing is widely use method for management account reporting and also consider

by the portfolio payroll. It is use for the calculation and analysis of variance to reduce the adverse

event which happen in the past. Compare the actual with the standard cost is an element which use

in standard costing (Mistry, Sharma and Low, 2014).

Budgetary control method use for the planning and control of the various activities of the

business. It is a tool for directing the enterprise in a desired direction for achieving satisfying return

on the investment.

Fund flow statement tool use for allocate any change in the financial statement of an

enterprise. Portfolio payroll use fund flow statement for figure out the most favourable way in

which they can use the fund which is there in the enterprise.

Portfolio payroll limited use cash flow statement for determining the cash inflow and

outflow of the enterprise. It is useful for cash control because it give detailed information about

sources of cash inflows and uses of cash outflows for the enterprise in a particular period of time

(Kastberg and Siverbo, 2016).

By the use of revaluation accounting portfolio payroll limited assures the preservation and

maintenance of the capital within the enterprise. It brings the information about changes which

occurred at the time of the preparation of financial statements in the mind of the accounting

managers.

The management accountant use statistical and graphical presentation techniques to make

information more meaningful and user friendly. Master charts, charts of sale, Earning investment

charts, Linear programming, statistical quality control etc. Tools are used for proper decision

making (Ibarrondo-Dávila, López-Alonso and Rubio-Gámez, 2015).

Communication and decision making tools are also use by the portfolio payroll limited as a

management accounting reporting methods for enabling themselves to carry out the functions of

planning, controlling and implementing.

M1 Benefits and usage of management accounting system

By the means of suing various management accounting system that benefits that are being

gained are enumerated in the manner stated as below:

where an enterprise financial planning focus on. The other method which used in management

accounting reporting is analysis of the financial statement, by the use of it payment payroll figure

out the significance of financial data and forecast it for achieve and set the future goals.

Historical cost accounting methods use by portfolio payroll for determine the past data to the

management relating to the cost of each job. Generally accepted accounting principles (GAAP) is a

basic way to figure out the result of historical cost accounting.

Standard costing is widely use method for management account reporting and also consider

by the portfolio payroll. It is use for the calculation and analysis of variance to reduce the adverse

event which happen in the past. Compare the actual with the standard cost is an element which use

in standard costing (Mistry, Sharma and Low, 2014).

Budgetary control method use for the planning and control of the various activities of the

business. It is a tool for directing the enterprise in a desired direction for achieving satisfying return

on the investment.

Fund flow statement tool use for allocate any change in the financial statement of an

enterprise. Portfolio payroll use fund flow statement for figure out the most favourable way in

which they can use the fund which is there in the enterprise.

Portfolio payroll limited use cash flow statement for determining the cash inflow and

outflow of the enterprise. It is useful for cash control because it give detailed information about

sources of cash inflows and uses of cash outflows for the enterprise in a particular period of time

(Kastberg and Siverbo, 2016).

By the use of revaluation accounting portfolio payroll limited assures the preservation and

maintenance of the capital within the enterprise. It brings the information about changes which

occurred at the time of the preparation of financial statements in the mind of the accounting

managers.

The management accountant use statistical and graphical presentation techniques to make

information more meaningful and user friendly. Master charts, charts of sale, Earning investment

charts, Linear programming, statistical quality control etc. Tools are used for proper decision

making (Ibarrondo-Dávila, López-Alonso and Rubio-Gámez, 2015).

Communication and decision making tools are also use by the portfolio payroll limited as a

management accounting reporting methods for enabling themselves to carry out the functions of

planning, controlling and implementing.

M1 Benefits and usage of management accounting system

By the means of suing various management accounting system that benefits that are being

gained are enumerated in the manner stated as below:

Traditional cost accounting: The major advantage of utilizing traditional cost accounting system is

that it assist in effective execution of specific system so that it assist in determination of the cost of

the goods which are being sold by Portfolio payroll limited. Therefore it also act as an aid in

gaining advantage from suitable cost allocation and therefore associated with material, labour as

well as overheads.This system asssit in attaining critical information with respect to determination

of final price of Portfolio payroll limited that are being sold to the target market (Upping and Oliver,

2016).

Lean accounting: The advantage of utilizing the lean accounting is that it leads to assessment that is

less complex and attain critical data with respect to comparing it with traditional accounting. By the

means of conducting this application results in attained in terms of acquiring needed data in

Portfolio payroll limited. Thus this leads to enhancing the performance of the organization in the

market.

Transfer pricing: Through the assistance of such kind of management system assistance is offered in

benefitting business with respect to determination of the cost that is associated with movement of

the products. However this systems act as aid in determination of the total cost of product that is

manufactured by Portfolio payroll limited that includes all the expenses which are associated with

producing the product (Jamil, Mohamed and Ali, 2015).

D1 Usage of management accounting system and reporting in the business

By means of conducting the management accounting system it is advantages for Portfolio

payroll limited to make integration and conduct suitable outcomes so that financial activities in the

business can be managed in an effective manner. However it assists in management of the business

decisions therefore growth can be enhanced and success can be attained. Portfolio payroll limited.

make utilization of suitable management of the accounting system that leads to management of the

financial decisions so that suitable decisions can be taken with respect achievement of desired

targets. The manager of business is required to lay emphasis on bringing enhancement in the

operational and therefore leads to reducing the cost included in operating the firm so that higher

return can be attained (Klychova, Zakirova and Valieva, 2015). However use of appropriate

management system leads to reporting in the organization. Therefore use of effective management

accounting system leads to reporting in the business. Such results in improvising the organizational

performance with respect to development of suitable budget and therefore makes evaluation of the

outcomes in attaining success.

TASK 2

P3 Calculation of the cost by means of suitable tools of analyzing the costs for preparing an income

statement of marginal and absorption costing

By means of determining the cost assistance it offered to the firm in enhancing the

managerial decisions. Therefore it leads to conducting the functions of the business that results in

that it assist in effective execution of specific system so that it assist in determination of the cost of

the goods which are being sold by Portfolio payroll limited. Therefore it also act as an aid in

gaining advantage from suitable cost allocation and therefore associated with material, labour as

well as overheads.This system asssit in attaining critical information with respect to determination

of final price of Portfolio payroll limited that are being sold to the target market (Upping and Oliver,

2016).

Lean accounting: The advantage of utilizing the lean accounting is that it leads to assessment that is

less complex and attain critical data with respect to comparing it with traditional accounting. By the

means of conducting this application results in attained in terms of acquiring needed data in

Portfolio payroll limited. Thus this leads to enhancing the performance of the organization in the

market.

Transfer pricing: Through the assistance of such kind of management system assistance is offered in

benefitting business with respect to determination of the cost that is associated with movement of

the products. However this systems act as aid in determination of the total cost of product that is

manufactured by Portfolio payroll limited that includes all the expenses which are associated with

producing the product (Jamil, Mohamed and Ali, 2015).

D1 Usage of management accounting system and reporting in the business

By means of conducting the management accounting system it is advantages for Portfolio

payroll limited to make integration and conduct suitable outcomes so that financial activities in the

business can be managed in an effective manner. However it assists in management of the business

decisions therefore growth can be enhanced and success can be attained. Portfolio payroll limited.

make utilization of suitable management of the accounting system that leads to management of the

financial decisions so that suitable decisions can be taken with respect achievement of desired

targets. The manager of business is required to lay emphasis on bringing enhancement in the

operational and therefore leads to reducing the cost included in operating the firm so that higher

return can be attained (Klychova, Zakirova and Valieva, 2015). However use of appropriate

management system leads to reporting in the organization. Therefore use of effective management

accounting system leads to reporting in the business. Such results in improvising the organizational

performance with respect to development of suitable budget and therefore makes evaluation of the

outcomes in attaining success.

TASK 2

P3 Calculation of the cost by means of suitable tools of analyzing the costs for preparing an income

statement of marginal and absorption costing

By means of determining the cost assistance it offered to the firm in enhancing the

managerial decisions. Therefore it leads to conducting the functions of the business that results in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

determination of the cost engaged with carrying out organizational operations. In addition to this

determination of ineffective costs leads to influencing pricing decision. It includes distinctive tools

that are being utilized by the business with respect to determination of costs and identification of

marginal costing, absorption costing as well as other methods with respect to calculation of the

costs that are enumerated in the manner as under:

Marginal costing: This method is regarded as effective that assist in charging variable cost per unit

of the products are being manufactured by Portfolio payroll limited (Ahmad, 2015). Thus makes

computation of total contribution when fixed cost is charged in full towards the contribution of

attaining net profit. Thus it is effective for the firm in determining total cost that is regarded as

periodical cost and does not make allocation of such in carrying out whole production.

Advantages

It makes elimination of entire absorption of the fixed costs and leads to avoiding important

adjustment so that results can be achieved. Another demerit of this is that organization charges fixed

expenses in relation to attainment of periodical costs.

Disadvantages

The demerit it possesses is that it makes creation of problems in order to segregate the fixed as well

as variable costs. Along with this it makes assessment of the real world case and determines the

semi variable cost that is eliminated totally (Gopalakrishnan, Libby and Swenson, 2015).

Application of marginal costing

Calculation of production cost Budgeted Actual

Direct material 3600.00 4200.00

Direct labor 3000.00 3500.00

Variable production overheads 1200.00 1400.00

Total cost of production 7800.00 9100.00

Add: Beginning inventory

less: closing inventory 1950.00 1300.00

Cost of sale 5850.00 7800.00

Cost of sale/unit 13 13

Marginal costing profitability statement

Particulars Budgeted Actual

Sales 14000 21000

less: Cost of sales (see above) 5850.00 7800.00

Variable sales overheads 450 600

Total variable cost (TVC) 6300.00 8400.00

Contribution 7700.00 12600.00

Less: Fixed expenditures

Administrative overheads 800 700

Selling cost 400 600

Total fixed cost (TFC) 1200 1300

determination of ineffective costs leads to influencing pricing decision. It includes distinctive tools

that are being utilized by the business with respect to determination of costs and identification of

marginal costing, absorption costing as well as other methods with respect to calculation of the

costs that are enumerated in the manner as under:

Marginal costing: This method is regarded as effective that assist in charging variable cost per unit

of the products are being manufactured by Portfolio payroll limited (Ahmad, 2015). Thus makes

computation of total contribution when fixed cost is charged in full towards the contribution of

attaining net profit. Thus it is effective for the firm in determining total cost that is regarded as

periodical cost and does not make allocation of such in carrying out whole production.

Advantages

It makes elimination of entire absorption of the fixed costs and leads to avoiding important

adjustment so that results can be achieved. Another demerit of this is that organization charges fixed

expenses in relation to attainment of periodical costs.

Disadvantages

The demerit it possesses is that it makes creation of problems in order to segregate the fixed as well

as variable costs. Along with this it makes assessment of the real world case and determines the

semi variable cost that is eliminated totally (Gopalakrishnan, Libby and Swenson, 2015).

Application of marginal costing

Calculation of production cost Budgeted Actual

Direct material 3600.00 4200.00

Direct labor 3000.00 3500.00

Variable production overheads 1200.00 1400.00

Total cost of production 7800.00 9100.00

Add: Beginning inventory

less: closing inventory 1950.00 1300.00

Cost of sale 5850.00 7800.00

Cost of sale/unit 13 13

Marginal costing profitability statement

Particulars Budgeted Actual

Sales 14000 21000

less: Cost of sales (see above) 5850.00 7800.00

Variable sales overheads 450 600

Total variable cost (TVC) 6300.00 8400.00

Contribution 7700.00 12600.00

Less: Fixed expenditures

Administrative overheads 800 700

Selling cost 400 600

Total fixed cost (TFC) 1200 1300

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net profitability 6500.00 11300.00

Profitability per unit 14.44 18.83

Absorption costing: This kind of costing act as an aid in making determination of the total costs that

leads to assessment of the fixed overheads that is included in the total production costs. Therefore

such includes variable expenses. This is comprised of various expenses such as fixed variable,

direct as well as indirect so that company’s total cost can be determined.

Advantages

The main advantage of absorption costing is that it is valuing inventory including the closing

system of inventory. In addition to this it act as an aid in determining needed adjustments for over

absorption in relation to controlling cost. Absorption costing is regarded as the best manner with

which assistance is offered in making determination of the total costs as well as profitability on

particular job (Chenhall and Moers, 2015).

Disadvantages

This has lack of usefulness towards making decisions regarding pricing. Along with this it is does

not assist cost control.

Difference among marginal and absorption costing

Marginal costing is regarded as the tool that assists in valuation of the inventory at variable cost of

production. On the other hand marginal costing is effective in measurement of the inventory value

at full costing. Whereas by conducting under variable costing, assistance in offered in valuation of

the inventory (Christ and et.al., 2017).

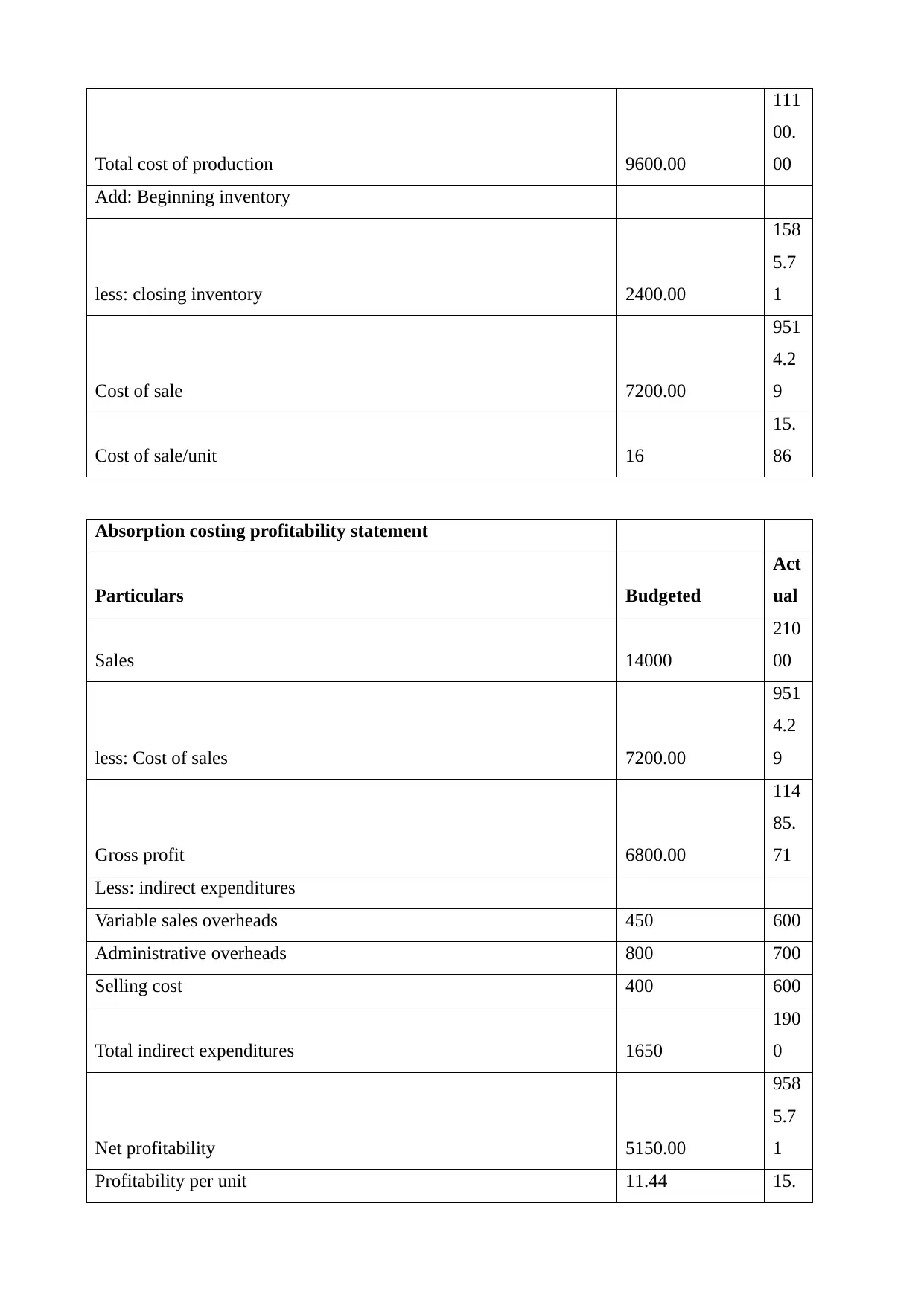

Application of absorption costing

Calculation of production cost Budgeted

Act

ual

Direct material 3600.00

420

0.0

0

Direct labor 3000.00

350

0.0

0

Variable production overheads 1200.00

140

0.0

0

Fixed production overheads 1800.00

200

0.0

0

Profitability per unit 14.44 18.83

Absorption costing: This kind of costing act as an aid in making determination of the total costs that

leads to assessment of the fixed overheads that is included in the total production costs. Therefore

such includes variable expenses. This is comprised of various expenses such as fixed variable,

direct as well as indirect so that company’s total cost can be determined.

Advantages

The main advantage of absorption costing is that it is valuing inventory including the closing

system of inventory. In addition to this it act as an aid in determining needed adjustments for over

absorption in relation to controlling cost. Absorption costing is regarded as the best manner with

which assistance is offered in making determination of the total costs as well as profitability on

particular job (Chenhall and Moers, 2015).

Disadvantages

This has lack of usefulness towards making decisions regarding pricing. Along with this it is does

not assist cost control.

Difference among marginal and absorption costing

Marginal costing is regarded as the tool that assists in valuation of the inventory at variable cost of

production. On the other hand marginal costing is effective in measurement of the inventory value

at full costing. Whereas by conducting under variable costing, assistance in offered in valuation of

the inventory (Christ and et.al., 2017).

Application of absorption costing

Calculation of production cost Budgeted

Act

ual

Direct material 3600.00

420

0.0

0

Direct labor 3000.00

350

0.0

0

Variable production overheads 1200.00

140

0.0

0

Fixed production overheads 1800.00

200

0.0

0

Total cost of production 9600.00

111

00.

00

Add: Beginning inventory

less: closing inventory 2400.00

158

5.7

1

Cost of sale 7200.00

951

4.2

9

Cost of sale/unit 16

15.

86

Absorption costing profitability statement

Particulars Budgeted

Act

ual

Sales 14000

210

00

less: Cost of sales 7200.00

951

4.2

9

Gross profit 6800.00

114

85.

71

Less: indirect expenditures

Variable sales overheads 450 600

Administrative overheads 800 700

Selling cost 400 600

Total indirect expenditures 1650

190

0

Net profitability 5150.00

958

5.7

1

Profitability per unit 11.44 15.

111

00.

00

Add: Beginning inventory

less: closing inventory 2400.00

158

5.7

1

Cost of sale 7200.00

951

4.2

9

Cost of sale/unit 16

15.

86

Absorption costing profitability statement

Particulars Budgeted

Act

ual

Sales 14000

210

00

less: Cost of sales 7200.00

951

4.2

9

Gross profit 6800.00

114

85.

71

Less: indirect expenditures

Variable sales overheads 450 600

Administrative overheads 800 700

Selling cost 400 600

Total indirect expenditures 1650

190

0

Net profitability 5150.00

958

5.7

1

Profitability per unit 11.44 15.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

98

Interpretation

It can be interpreted by the means of analysis that determination of actual cost of production assist

in evaluating under variable and full costing that is determined to 11100 and 7800. Moreover the net

profit can be computed to 9585.71 and 11300. Thus in this relation assessment of such it is

comparatively higher for the sake of determining the marginal cost because of lower cost of sales.

M2 Application of range of management accounting tools

Through determination of above tools it has been determined that marginal costing as well

as variable costing are important. Therefore it is being used by Portfolio Payroll limited. By using

variable costing as management account tool determination of the cost of production is done in

relation to considering variable cost in the products. Full costing act as an aid in evaluation of the

cost through measurement of the total as well as fixed cost.

D2 Production of financial reports and interpretation of data

To: Board of directors of Portfolio Payroll limited

From: Accountant officer

Date: 15th April 2017

Subject: Cost report

By the means of cost evaluation in both the methods it is being reported that firm includes marginal

costing, actual profitability is determined at high level to 11300. On the other hand while

conducting full costing method outcomes is in form of value that is 9585.71 which is considered

low (Deegan, 2013).

TASK 3

P4 Advantages and Disadvantages of different types of planning tools used in budgetary control

Budgetary control is a process of analyzing the result of the budget once organization

implement it. In budgetary control actual results are compared with the estimated budget.

Enterprises uses various tool for proper planning of budgetory control.

Variance analysis

Variance analysis concerns with evaluation of performances by means of variance between

budget amount, planned amount or standard amount or the actual amount incurred sold. Variance

anlysis figure out the sources of actual values to budget differences.

Advantages

Variance analysis is an excellent tool for the performance measurement of an enterprise

Responsibility accounting can be exercised by the use of variance analysis

Interpretation

It can be interpreted by the means of analysis that determination of actual cost of production assist

in evaluating under variable and full costing that is determined to 11100 and 7800. Moreover the net

profit can be computed to 9585.71 and 11300. Thus in this relation assessment of such it is

comparatively higher for the sake of determining the marginal cost because of lower cost of sales.

M2 Application of range of management accounting tools

Through determination of above tools it has been determined that marginal costing as well

as variable costing are important. Therefore it is being used by Portfolio Payroll limited. By using

variable costing as management account tool determination of the cost of production is done in

relation to considering variable cost in the products. Full costing act as an aid in evaluation of the

cost through measurement of the total as well as fixed cost.

D2 Production of financial reports and interpretation of data

To: Board of directors of Portfolio Payroll limited

From: Accountant officer

Date: 15th April 2017

Subject: Cost report

By the means of cost evaluation in both the methods it is being reported that firm includes marginal

costing, actual profitability is determined at high level to 11300. On the other hand while

conducting full costing method outcomes is in form of value that is 9585.71 which is considered

low (Deegan, 2013).

TASK 3

P4 Advantages and Disadvantages of different types of planning tools used in budgetary control

Budgetary control is a process of analyzing the result of the budget once organization

implement it. In budgetary control actual results are compared with the estimated budget.

Enterprises uses various tool for proper planning of budgetory control.

Variance analysis

Variance analysis concerns with evaluation of performances by means of variance between

budget amount, planned amount or standard amount or the actual amount incurred sold. Variance

anlysis figure out the sources of actual values to budget differences.

Advantages

Variance analysis is an excellent tool for the performance measurement of an enterprise

Responsibility accounting can be exercised by the use of variance analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Draws attention of management where planned activity is different from actual one

(Quattrone, 2016)

Disadvantages

Main focus on the past result without looking at the future

Clueless or not understanding about the drivers behind the performance

Variance create pressure to build excess work in process and finished goods inventories

Responsibility accounting

Responsibility accounting is a budgetary planning tool and technique which consist revenue,

cost and profit information at the level of those individual managers who are responsible for them.

Responsibility accounting allows the company and each manager of a responsibility center to

receive monthly feedback on the manager performance (Saladrigues and Tena, 2017).

Advantages

It establishes a sound mechanism within the enterprise for controlling

It creates responsible nature within the enterprise which exaggerate the work competency

Encourage proper budgeting with that actual achievement can be compared

Responsibility accounting increase the interest and awareness of the officers

Exclusion of unnecessary task simplifies the structure

Disadvantages

Proper delegation of work and responsibility increase the workload

Classification of expenses need to consider for further analysis which make tasks more

difficult

Managers may require additional classification if the responsibility reports are differents

from existing routine (Zimmerman and Yahya-Zadeh, 2011)

Zero base budgeting

As the name itself explaining the Zero base budgeting start from the zero level, every

function within the organization is analyzed according to their need and cost.Zero-base budgeting

provide a direction to top strategic goals so that they can be implemented well in the budget process

(Marginal and absorption costing. 2016).

Advantages

(Quattrone, 2016)

Disadvantages

Main focus on the past result without looking at the future

Clueless or not understanding about the drivers behind the performance

Variance create pressure to build excess work in process and finished goods inventories

Responsibility accounting

Responsibility accounting is a budgetary planning tool and technique which consist revenue,

cost and profit information at the level of those individual managers who are responsible for them.

Responsibility accounting allows the company and each manager of a responsibility center to

receive monthly feedback on the manager performance (Saladrigues and Tena, 2017).

Advantages

It establishes a sound mechanism within the enterprise for controlling

It creates responsible nature within the enterprise which exaggerate the work competency

Encourage proper budgeting with that actual achievement can be compared

Responsibility accounting increase the interest and awareness of the officers

Exclusion of unnecessary task simplifies the structure

Disadvantages

Proper delegation of work and responsibility increase the workload

Classification of expenses need to consider for further analysis which make tasks more

difficult

Managers may require additional classification if the responsibility reports are differents

from existing routine (Zimmerman and Yahya-Zadeh, 2011)

Zero base budgeting

As the name itself explaining the Zero base budgeting start from the zero level, every

function within the organization is analyzed according to their need and cost.Zero-base budgeting

provide a direction to top strategic goals so that they can be implemented well in the budget process

(Marginal and absorption costing. 2016).

Advantages

It provides a systematic way to the organization for evaluating programmes of activities and

operations

It allows enterprise to allocate resources as according to priority

There is no need for complete recycling of budget inputs as elements are already priortize

Long term plans and goals can easily linked with the budget by the use of zero base

budgeting (Christ and et.al., 2017)

Disadvantages

Implementation process may encountered with problem in the case of unsupportive top

management

Fixation process for decision package is cumbersome

Ranking of decision package may encounter problems

Break-even analysis

Break even analysis entitles with the examination of the margin safety for the enterprise. It is

useful in determining the production level in the sales process or also determine the financial

fluctuation within the enterprise (Deegan, 2013).

Advantages

Provide the results for budgetary level process

Predict the effect of changes

Predict the effect of cost and efficiency changes on profitability

Disadvantages

Assume the sale price is constant at all level of output within the enterprise

Assume production and sale are same within the enterprise

Time consuming process to prepare charts for the analysis

M3 Using various planning tools and applying for budget forecasting

By means of conducting the tools related with planning the firm is assisted towards using

Zero based budgeting and therefore it reflects realistic figures so that future goals can be achieved.

However budget has to be constructed in relation to conducting specific activity. Therefore

determining the volume so that flexible approach can be assessed with respect to making evaluation

of the production in order to make suitable comparison (DRURY, 2013).

D3 Planning tools to solve financial problems

By the means of utilizing planning tool assistance offered to financial manager of the company in

operations

It allows enterprise to allocate resources as according to priority

There is no need for complete recycling of budget inputs as elements are already priortize

Long term plans and goals can easily linked with the budget by the use of zero base

budgeting (Christ and et.al., 2017)

Disadvantages

Implementation process may encountered with problem in the case of unsupportive top

management

Fixation process for decision package is cumbersome

Ranking of decision package may encounter problems

Break-even analysis

Break even analysis entitles with the examination of the margin safety for the enterprise. It is

useful in determining the production level in the sales process or also determine the financial

fluctuation within the enterprise (Deegan, 2013).

Advantages

Provide the results for budgetary level process

Predict the effect of changes

Predict the effect of cost and efficiency changes on profitability

Disadvantages

Assume the sale price is constant at all level of output within the enterprise

Assume production and sale are same within the enterprise

Time consuming process to prepare charts for the analysis

M3 Using various planning tools and applying for budget forecasting

By means of conducting the tools related with planning the firm is assisted towards using

Zero based budgeting and therefore it reflects realistic figures so that future goals can be achieved.

However budget has to be constructed in relation to conducting specific activity. Therefore

determining the volume so that flexible approach can be assessed with respect to making evaluation

of the production in order to make suitable comparison (DRURY, 2013).

D3 Planning tools to solve financial problems

By the means of utilizing planning tool assistance offered to financial manager of the company in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.