Higher National Diploma: Management Accounting Report, Unit 5, 2023

VerifiedAdded on 2022/12/27

|18

|4717

|35

Report

AI Summary

This report delves into the realm of management accounting, utilizing Connect Catering Service as a practical context. It begins by defining management accounting and exploring various management accounting systems, such as price optimization, inventory management, job order costing, and cost accounting systems. The report then examines different methods of management accounting reporting, including performance, budget, accounts receivable, and inventory management reporting, along with their advantages and applications. A significant portion of the report is dedicated to cost calculations, comparing marginal and absorption costing methods. Furthermore, it discusses planning tools used for budgetary control, highlighting their advantages and disadvantages. Finally, the report concludes with a comparative analysis of Connect Catering Service and a competitor, Rusty and Roses Catering Service, evaluating their responses to financial problems and the management accounting systems employed.

Unit 5 – Management

Accounting

1

Accounting

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

MAIN BODY...................................................................................................................................3

Task 1 ..............................................................................................................................................3

P1 Management accounting and different types of management accounting systems...............3

P2 Different methods of management accounting reporting......................................................5

Task 2...............................................................................................................................................7

P3 Calculation of costs...............................................................................................................7

Task 3.............................................................................................................................................11

P4 Advantages and disadvantages of different planning tools used for budgetary control .....11

Task 4.............................................................................................................................................13

P5 Comparison between two firms in adapting MAS to respond to financial problems .........13

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

2

Introduction......................................................................................................................................3

MAIN BODY...................................................................................................................................3

Task 1 ..............................................................................................................................................3

P1 Management accounting and different types of management accounting systems...............3

P2 Different methods of management accounting reporting......................................................5

Task 2...............................................................................................................................................7

P3 Calculation of costs...............................................................................................................7

Task 3.............................................................................................................................................11

P4 Advantages and disadvantages of different planning tools used for budgetary control .....11

Task 4.............................................................................................................................................13

P5 Comparison between two firms in adapting MAS to respond to financial problems .........13

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

2

Introduction

Management of an organisation requires different sets of financial and non-financial

information to reach to the conclusions that can enable them to make informed decisions about

the affairs of the firm. These information are made available to the management in the form of

various reports that have been generated using various management accounting systems

(Rozhkova, Blinova and Rozhkova, 2017). Therefore, it can be said that financial accounting

deals with only information of financial nature while management accounting deals with

information of both financial and non-financial nature. Further, users of financial information are

both external and internal stakeholders while users of managerial accounting information are

only internal to organisation.

This report has been developed taking Connect Catering Service as context to evaluate

different aspects and practices related to management accounting concerned with the company.

Connect Catering Service is based in Oxfordshire, UK and is a family owned and operated

catering firm. To begin with, management accounting and different types of management

accounting systems have been discussed in the report. In addition, various reports developed out

of those management accounting systems have also been elucidated. Further, a practical

demonstration of cost problem have been illustrated and also, statements of income have been

prepared using absorption costing and marginal costing. In the next part of the report, planning

tools for budgetary control have been discussed and finally, a comparison have been drawn up

between Connect Catering Service and its competitor Rusty and Roses Catering Service to

evaluate financial problems faced by the two firms and different management accounting

systems used by the two to overcome those problems.

MAIN BODY

Task 1

P1 Management accounting and different types of management accounting systems

Management accounting: This is process of report preparation with financial details that

help managers of organisation take effective decisions in long or short run (Malik and et.

al.,2021). In relation with Connect catering services, main aim of company leaders is to forecast

future plans, cash flows, understand performance variances and determining return rates on

existing or future investments.

3

Management of an organisation requires different sets of financial and non-financial

information to reach to the conclusions that can enable them to make informed decisions about

the affairs of the firm. These information are made available to the management in the form of

various reports that have been generated using various management accounting systems

(Rozhkova, Blinova and Rozhkova, 2017). Therefore, it can be said that financial accounting

deals with only information of financial nature while management accounting deals with

information of both financial and non-financial nature. Further, users of financial information are

both external and internal stakeholders while users of managerial accounting information are

only internal to organisation.

This report has been developed taking Connect Catering Service as context to evaluate

different aspects and practices related to management accounting concerned with the company.

Connect Catering Service is based in Oxfordshire, UK and is a family owned and operated

catering firm. To begin with, management accounting and different types of management

accounting systems have been discussed in the report. In addition, various reports developed out

of those management accounting systems have also been elucidated. Further, a practical

demonstration of cost problem have been illustrated and also, statements of income have been

prepared using absorption costing and marginal costing. In the next part of the report, planning

tools for budgetary control have been discussed and finally, a comparison have been drawn up

between Connect Catering Service and its competitor Rusty and Roses Catering Service to

evaluate financial problems faced by the two firms and different management accounting

systems used by the two to overcome those problems.

MAIN BODY

Task 1

P1 Management accounting and different types of management accounting systems

Management accounting: This is process of report preparation with financial details that

help managers of organisation take effective decisions in long or short run (Malik and et.

al.,2021). In relation with Connect catering services, main aim of company leaders is to forecast

future plans, cash flows, understand performance variances and determining return rates on

existing or future investments.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting systems in management: These are systems adopted within chosen firm

internally for providing critical information to company managers. In relation to Connect

catering services, these system also known as cost accounting systems are utilized by managers

for determining, analysing, interpreting and communicating appropriate information to users

helping them achieve business goal objectives.

Price optimisation system: Following system help market researchers decide price of

their manufactured products with mathematical accuracy. In context with Connect catering

services, this system help managers identify market demand and accordingly create pricing

strategies such as premium, skimming, economic value and penetration.

Inventory management system: This form of system is a combination of organisational

procedures and technology to monitor stock inventory of chosen firm (Libby and Salterio, 2019).

In relation with Connect catering services, various form of inventory management software's are

adopted by managers to apply following methods:

AVCO(Average cost method): This method help managers allot costs to stock

items based on total goods purchased within a specific time period. This is also

known as weighted average method as it is used by chosen entity to determine

cost of quantity goods over certain period monthly, yearly or on regular basis.

LIFO(Last in first out method): This method is used by managers when they

have to use fresh stocks entered in books recently (Quinn and Strauss, 2017). In

relation with Connect catering services, recent products are calculated first by

accountants of firm to assume actual cost of goods sold currently.

FIFO(First in first out method): This method is mainly used by enterprise to use

products registered earlier. Under this method older products are first sold by

company present in stock inventory. In relevance with Connect caterers, have

adopted this food storage system to distribute older items first for streamlining

inventory practices and keep recent products preserved.

Job order costing system: This system deals with accumulation and assigning of

manufacturing costs as per individual units (Kumarasiri, 2017). In context of Connect catering

services, uses this system of accounting to decide price of every product manufactured with

reasonable rate for consumers in market. Job order costing is calculated with following elements

that consist of direct material, labour and estimated overheads.

4

internally for providing critical information to company managers. In relation to Connect

catering services, these system also known as cost accounting systems are utilized by managers

for determining, analysing, interpreting and communicating appropriate information to users

helping them achieve business goal objectives.

Price optimisation system: Following system help market researchers decide price of

their manufactured products with mathematical accuracy. In context with Connect catering

services, this system help managers identify market demand and accordingly create pricing

strategies such as premium, skimming, economic value and penetration.

Inventory management system: This form of system is a combination of organisational

procedures and technology to monitor stock inventory of chosen firm (Libby and Salterio, 2019).

In relation with Connect catering services, various form of inventory management software's are

adopted by managers to apply following methods:

AVCO(Average cost method): This method help managers allot costs to stock

items based on total goods purchased within a specific time period. This is also

known as weighted average method as it is used by chosen entity to determine

cost of quantity goods over certain period monthly, yearly or on regular basis.

LIFO(Last in first out method): This method is used by managers when they

have to use fresh stocks entered in books recently (Quinn and Strauss, 2017). In

relation with Connect catering services, recent products are calculated first by

accountants of firm to assume actual cost of goods sold currently.

FIFO(First in first out method): This method is mainly used by enterprise to use

products registered earlier. Under this method older products are first sold by

company present in stock inventory. In relevance with Connect caterers, have

adopted this food storage system to distribute older items first for streamlining

inventory practices and keep recent products preserved.

Job order costing system: This system deals with accumulation and assigning of

manufacturing costs as per individual units (Kumarasiri, 2017). In context of Connect catering

services, uses this system of accounting to decide price of every product manufactured with

reasonable rate for consumers in market. Job order costing is calculated with following elements

that consist of direct material, labour and estimated overheads.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost accounting system: Cost system of accounting is utilized by manufacturers of

organisation to track stock flows within inventory management system. Managers of

organisations such as Connect catering services use this accounting to analyse cost of production

activities with systematic track of raw material.

There are a lot of uses and application of above discussed accounting systems to

effectively carry on activities of manufacturing, production and inventory management within an

organisation discussed below.

P2 Different methods of management accounting reporting

Management accounting reporting is a process of producing internal reports by

stakeholders of organisation in form of periodic statements or mathematical calculations.

Managers use accounting reporting to manage basic operations running within company

internally (De Boer, Brouwers and Koetzier, 2019). Connect catering services create different

form of reports consisting of accounting records and financial data. This data comprise of

various transactions, profit of products sold, regional goods sold and cost during company

operations.

Performance reporting: This form of reporting is used by company superiors to set

baselines for allotted projects to employees at workplace (Schaltegger, 2020). Organisations such

as Connect catering services create performance reports for utilizing useful resources of

communicating project to others in group. Chosen firm accountants also forecast management

progress in construction of various plans by use of these performance reports.

Budget reporting: This is a written blueprint that show costs or revenues that are going to

be managed by company owners or staff employees. The main purpose behind formulation of

these budget reports in context of Connect caterers is to know actual spending of business as

compared toe profits earned.

Accounts receivable report: This is a periodic report that is created according to time

length of outstanding invoices. Main focus of manager behind formulation of these reports is to

determine financial health of company (Bennett and James,2017). In relation with chosen entity,

there are various key performance indicators that are focussed upon in accounts receivable

reports consisting of daily sales, outstanding payments, turnover ratio, revised invoices, bad-

debts, staff productivity and credit percentage etc.

5

organisation to track stock flows within inventory management system. Managers of

organisations such as Connect catering services use this accounting to analyse cost of production

activities with systematic track of raw material.

There are a lot of uses and application of above discussed accounting systems to

effectively carry on activities of manufacturing, production and inventory management within an

organisation discussed below.

P2 Different methods of management accounting reporting

Management accounting reporting is a process of producing internal reports by

stakeholders of organisation in form of periodic statements or mathematical calculations.

Managers use accounting reporting to manage basic operations running within company

internally (De Boer, Brouwers and Koetzier, 2019). Connect catering services create different

form of reports consisting of accounting records and financial data. This data comprise of

various transactions, profit of products sold, regional goods sold and cost during company

operations.

Performance reporting: This form of reporting is used by company superiors to set

baselines for allotted projects to employees at workplace (Schaltegger, 2020). Organisations such

as Connect catering services create performance reports for utilizing useful resources of

communicating project to others in group. Chosen firm accountants also forecast management

progress in construction of various plans by use of these performance reports.

Budget reporting: This is a written blueprint that show costs or revenues that are going to

be managed by company owners or staff employees. The main purpose behind formulation of

these budget reports in context of Connect caterers is to know actual spending of business as

compared toe profits earned.

Accounts receivable report: This is a periodic report that is created according to time

length of outstanding invoices. Main focus of manager behind formulation of these reports is to

determine financial health of company (Bennett and James,2017). In relation with chosen entity,

there are various key performance indicators that are focussed upon in accounts receivable

reports consisting of daily sales, outstanding payments, turnover ratio, revised invoices, bad-

debts, staff productivity and credit percentage etc.

5

Inventory management reporting: Inventory is unit of products that are preserved for

sale in future by retailer of organisation. Stock inventory are of various types categorised into

raw material,unfinished goods, in transit goods and cycle inventories etc.. In relation to Connect

catering services, managers create various type of reports fro inventory management such as in-

hand stocks, low stocks, product performance, benchmark variances etc.

Advantage and use of above discussed accounting systems in relevance with chosen

organisation:

Management accounting system Advantages and application

Price optimisation system Use: Chosen firm use this accounting system

to set price for their manufactured products as

per consumer preferences within reasonable

rates (Song and et. al., 2019).

Benefit: This system is helpful in market

analysis of competitive firms sand substitute

products based on their existing price rates.

Inventory management system Use: This system is utilized to maintain stocks

and monitor track record of every product

within organisation.

Benefit: This help chosen firm keep up to date

information of product details and transactional

information helping them reduce duplication of

activities, decrease red tap-ism, eliminate

wastage of resources etc.

Job order costing system Use: Following accounting system use this

system to monitor costs within manufacturing

process of goods or service production

(Amahalu, Nweze and Chinyere, 2017).

Benefit: Connect catering services have

advantage of analysing individual profit reports

on basis of performance, benchmarks, measure

6

sale in future by retailer of organisation. Stock inventory are of various types categorised into

raw material,unfinished goods, in transit goods and cycle inventories etc.. In relation to Connect

catering services, managers create various type of reports fro inventory management such as in-

hand stocks, low stocks, product performance, benchmark variances etc.

Advantage and use of above discussed accounting systems in relevance with chosen

organisation:

Management accounting system Advantages and application

Price optimisation system Use: Chosen firm use this accounting system

to set price for their manufactured products as

per consumer preferences within reasonable

rates (Song and et. al., 2019).

Benefit: This system is helpful in market

analysis of competitive firms sand substitute

products based on their existing price rates.

Inventory management system Use: This system is utilized to maintain stocks

and monitor track record of every product

within organisation.

Benefit: This help chosen firm keep up to date

information of product details and transactional

information helping them reduce duplication of

activities, decrease red tap-ism, eliminate

wastage of resources etc.

Job order costing system Use: Following accounting system use this

system to monitor costs within manufacturing

process of goods or service production

(Amahalu, Nweze and Chinyere, 2017).

Benefit: Connect catering services have

advantage of analysing individual profit reports

on basis of performance, benchmarks, measure

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

indirect cost expenditures etc.

Cost accounting system Use: Selected firm apply this accounting

technique to compare goods & services with

their cost prices in market. It help manager

know efficiency level of product cost as

compared to its competitive goods in industry.

Benefit: This is a flexible method of

determining costs. The system benefits chosen

entity with presentation of cost data of every

product, ascertain profits from every activity,

systematic record product costs.

Management accounting system and reporting process integration within

organisational context: Main purpose of every organisation behind regulating various

operational activities is profit maximisation. In order to achieve long term goal of organisation

such as Connect catering services it is important for manager to conduct systematic processes

with use of appropriate accounting systems (Xueyi, 2017). For example, cost accounting method

is a simple and flexible way of differentiating various costs into variable, dependent, independent

or fixed costs etc. Also price optimizing accounting system is useful for creating performance,

budget and inventory reports helping manager keep track of every product detail available for

sale or stock. Performance report also help manager know best performers from employees that

help leaders motivate them to give their best in achievement of organisational objectives.

Task 2

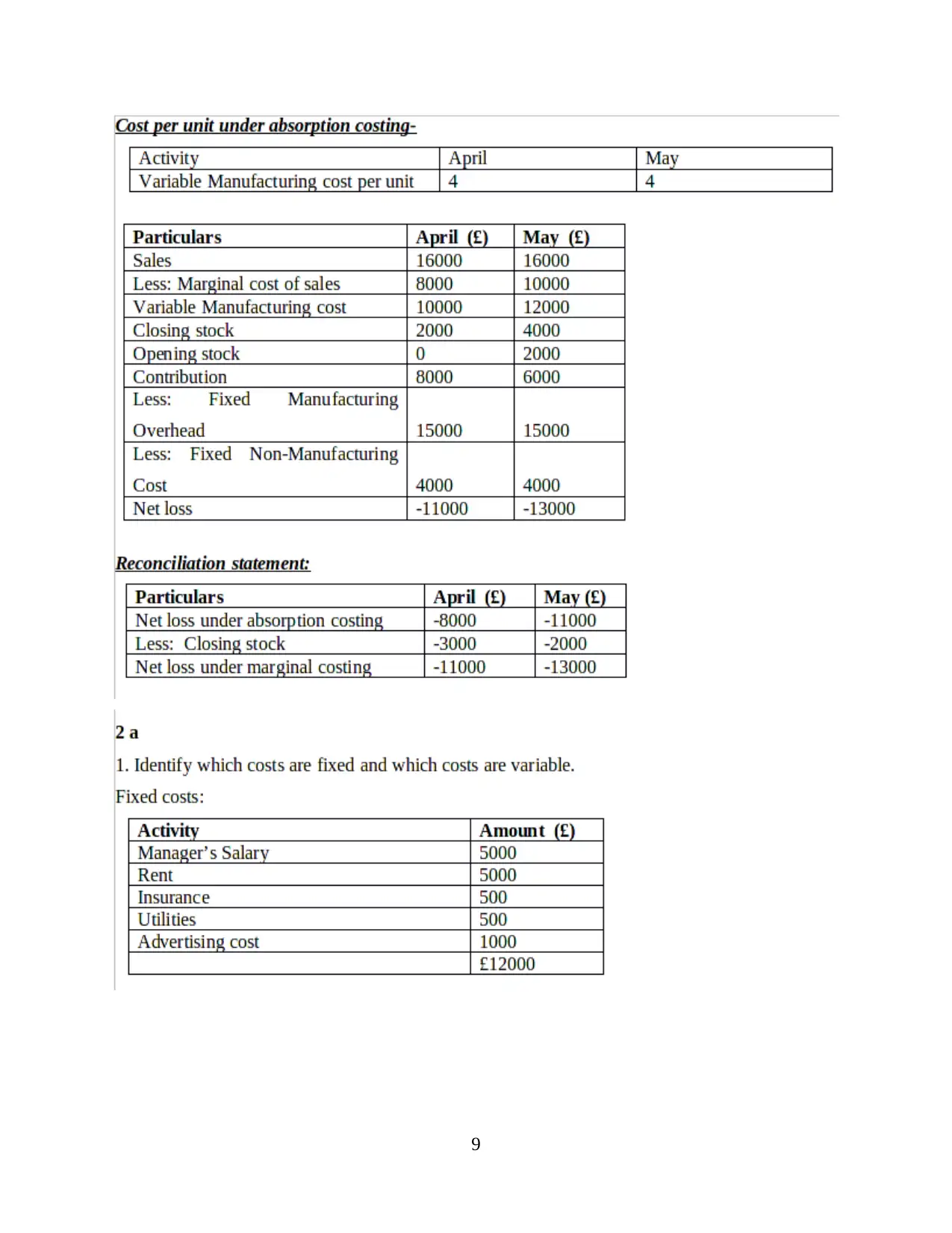

P3 Calculation of costs

Marginal costing system: This costing system is adopted by Connect catering services to

determine additional units of production according to extra cost units (Álvarez, Adhikari and

Mejía, 2021). Marginal costing technique is helpful for chosen firm to analyse optimum

production quantity.

Absorption costing system: This system is used by Connect catering services to

determine overall cost overheads derived from activities of manufacturing & production. This

7

Cost accounting system Use: Selected firm apply this accounting

technique to compare goods & services with

their cost prices in market. It help manager

know efficiency level of product cost as

compared to its competitive goods in industry.

Benefit: This is a flexible method of

determining costs. The system benefits chosen

entity with presentation of cost data of every

product, ascertain profits from every activity,

systematic record product costs.

Management accounting system and reporting process integration within

organisational context: Main purpose of every organisation behind regulating various

operational activities is profit maximisation. In order to achieve long term goal of organisation

such as Connect catering services it is important for manager to conduct systematic processes

with use of appropriate accounting systems (Xueyi, 2017). For example, cost accounting method

is a simple and flexible way of differentiating various costs into variable, dependent, independent

or fixed costs etc. Also price optimizing accounting system is useful for creating performance,

budget and inventory reports helping manager keep track of every product detail available for

sale or stock. Performance report also help manager know best performers from employees that

help leaders motivate them to give their best in achievement of organisational objectives.

Task 2

P3 Calculation of costs

Marginal costing system: This costing system is adopted by Connect catering services to

determine additional units of production according to extra cost units (Álvarez, Adhikari and

Mejía, 2021). Marginal costing technique is helpful for chosen firm to analyse optimum

production quantity.

Absorption costing system: This system is used by Connect catering services to

determine overall cost overheads derived from activities of manufacturing & production. This

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

technique is useful for managers to recover costs of sales by absorbing maximum expenses from

selling same units.

Application of appropriate management accounting techniques for creating financial

statement with final accounts:In order to know actual business position, Connect catering

services have used various accounting techniques for regulating company operations.

Standard costing: This process is used by accountants of chosen organisation to know

actual differences between set budget cost standards with actual cost incurred. Following

technique is useful for Connect caterers to know reason behind cost variances occurred between

standard and actual costs.

Normal costing: This technique is used by Connect catering services to know actual

value of products derived from manufacturing or production within organisation (Adler,2018).

Managers apply this technique for allocating cost resources in correct way.

Historical costing: This is traditional form of accounting technique used to analyse assets

and liabilities as well as record them in financial accounts with their original value. Chosen firm

uses this tool to know real financial position of organisation in competition market.

8

selling same units.

Application of appropriate management accounting techniques for creating financial

statement with final accounts:In order to know actual business position, Connect catering

services have used various accounting techniques for regulating company operations.

Standard costing: This process is used by accountants of chosen organisation to know

actual differences between set budget cost standards with actual cost incurred. Following

technique is useful for Connect caterers to know reason behind cost variances occurred between

standard and actual costs.

Normal costing: This technique is used by Connect catering services to know actual

value of products derived from manufacturing or production within organisation (Adler,2018).

Managers apply this technique for allocating cost resources in correct way.

Historical costing: This is traditional form of accounting technique used to analyse assets

and liabilities as well as record them in financial accounts with their original value. Chosen firm

uses this tool to know real financial position of organisation in competition market.

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 3

P4 Advantages and disadvantages of different planning tools used for budgetary control

Planning tools refers to those tools or techniques that are used managers to facilitate

effective planning and decision-making (Shil, Hoque and Akter, 2019). Main purpose behind

deploying planning tools are to ensure that business operations are planned and performed

according to the strategical goals and objectives as decided in accordance with the mission,

vision and values of the organisation. These planing tools also acts as standards for controlling

function as well. Management deploys various kinds of planning tools to improve performance

of the different kinds of organisational processes. One such process is the development of

budgets by managers of Connect Catering Service, which are not only planning tools but also act

as standards for controlling function, hence are called as budgetary controls.

Budgets are forecast statement that are based on the historical figures but are itself

futuristic. In other words, budgets are estimated future statement of respective income,

expenditure or capital on the basis of past performance. These budgets act as standards for

monitoring and controlling function further. Actual performance is compared against budgeted

estimates to find out the variances. These variances are deviation that are capable of impacting

11

P4 Advantages and disadvantages of different planning tools used for budgetary control

Planning tools refers to those tools or techniques that are used managers to facilitate

effective planning and decision-making (Shil, Hoque and Akter, 2019). Main purpose behind

deploying planning tools are to ensure that business operations are planned and performed

according to the strategical goals and objectives as decided in accordance with the mission,

vision and values of the organisation. These planing tools also acts as standards for controlling

function as well. Management deploys various kinds of planning tools to improve performance

of the different kinds of organisational processes. One such process is the development of

budgets by managers of Connect Catering Service, which are not only planning tools but also act

as standards for controlling function, hence are called as budgetary controls.

Budgets are forecast statement that are based on the historical figures but are itself

futuristic. In other words, budgets are estimated future statement of respective income,

expenditure or capital on the basis of past performance. These budgets act as standards for

monitoring and controlling function further. Actual performance is compared against budgeted

estimates to find out the variances. These variances are deviation that are capable of impacting

11

operations, profitability and financial management of the firm. Therefore, in order to mitigate

and eliminate such chances, corrective actions are taken to remove the negative deviations

occurred from the standards. Organisations prepare various operational and capital budgets to

prepare a master budget which act as guiding agent for the operations of the respective period for

the organisation. Connect Catering Services can use below mentioned planning tools to prepare

the further mentioned budgets:

Management by Objective (MBO)

It is a planning technique which objectifies to clearly define the targets that are aimed by

company in order to achieve success and growth (Tucker and Schaltegger, 2016). These aims

must be developed in agreement with both management and employees so that they can be

achieved actually. For example, management of Connect Catering Services want to achieve a

20% increase in sales-volume. They can then create SMART goals related to it before preparing

sales budgets for the period and prepare the budget accordingly. This budget can then further act

as standard against which actual performance would be reviewed and corrective actions be taken.

This would enable company to facilitate better planning, coordination and utilisation of its

resources but on the other hand, since the planning for future would be based on historical data,

it is not appropriate to develop a perfect framework in a cost efficient manner.

Benchmarking

It is a planning tool which targets to improve performance of the company at par with the

best performance in the industry in which the company operates (Weygandt, Kimmel and Kieso,

2020). It aims to plan for both short-term and long term for the company. For example, with the

help of benchmarking tool, managers of Connect Catering Services realise that there is need for

improvement in their cash planning . They can therefore, develop cash budgets accordingly to

improve their performance further. It would benefit company by determining the lag in its

performance and further suggesting improvements that can make it best in the industry.

However, these are again based on unpredictable future and cannot help plan future in accuracy

to make company best in the industry. Also, it is a costly technique and is able to disrupt

financial management of smaller firms.

Cash Budget

It is a budgetary statement for estimation of inflow and outflow of cash and cash

equivalents of a firm in a defined period. It helps management in ensuring efficient financial

12

and eliminate such chances, corrective actions are taken to remove the negative deviations

occurred from the standards. Organisations prepare various operational and capital budgets to

prepare a master budget which act as guiding agent for the operations of the respective period for

the organisation. Connect Catering Services can use below mentioned planning tools to prepare

the further mentioned budgets:

Management by Objective (MBO)

It is a planning technique which objectifies to clearly define the targets that are aimed by

company in order to achieve success and growth (Tucker and Schaltegger, 2016). These aims

must be developed in agreement with both management and employees so that they can be

achieved actually. For example, management of Connect Catering Services want to achieve a

20% increase in sales-volume. They can then create SMART goals related to it before preparing

sales budgets for the period and prepare the budget accordingly. This budget can then further act

as standard against which actual performance would be reviewed and corrective actions be taken.

This would enable company to facilitate better planning, coordination and utilisation of its

resources but on the other hand, since the planning for future would be based on historical data,

it is not appropriate to develop a perfect framework in a cost efficient manner.

Benchmarking

It is a planning tool which targets to improve performance of the company at par with the

best performance in the industry in which the company operates (Weygandt, Kimmel and Kieso,

2020). It aims to plan for both short-term and long term for the company. For example, with the

help of benchmarking tool, managers of Connect Catering Services realise that there is need for

improvement in their cash planning . They can therefore, develop cash budgets accordingly to

improve their performance further. It would benefit company by determining the lag in its

performance and further suggesting improvements that can make it best in the industry.

However, these are again based on unpredictable future and cannot help plan future in accuracy

to make company best in the industry. Also, it is a costly technique and is able to disrupt

financial management of smaller firms.

Cash Budget

It is a budgetary statement for estimation of inflow and outflow of cash and cash

equivalents of a firm in a defined period. It helps management in ensuring efficient financial

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.