Unit 5 Management Accounting Report for Tech (UK) Limited Analysis

VerifiedAdded on 2023/03/20

|13

|4272

|34

Report

AI Summary

This report, prepared for a Management Accounting assignment, delves into the core concepts and practical applications of management accounting within the context of Tech (UK) Limited. The report begins with an introduction to management accounting, emphasizing its importance for effective organizational management and decision-making. It explores various management accounting systems, including job costing, inventory management, pricing optimization, risk and financial management, and management information systems. The report then examines different methods used for management accounting reports, such as performance reports, inventory management reports, job cost reports, accounts receivable reports, and operational budget reports. A key section focuses on cost calculation techniques, including cost-volume-profit analysis, flexible budgeting, cost variance analysis, and marginal costing. The report also analyzes the advantages and disadvantages of planning tools for budgetary control. Finally, it compares how management accounting systems are used to respond to financial problems. The report concludes by summarizing the key findings and providing relevant references.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.................................................................................................................................3

TASK 1.................................................................................................................................................3

P1 Explain management accounting and essential requirement of different type of management

accounting system.............................................................................................................................3

P2 Different methods used for management accounting report.........................................................4

TASK 2.................................................................................................................................................6

P3 Calculate cost using appropriate technique for calculating profit.............................................6

TASK 3.................................................................................................................................................9

P4 Explain advantages and disadvantages of various type planning tools for budgetary control.......9

TASK 4...............................................................................................................................................10

P5 Compare ways how management accounting system is used to respond financial problem.......10

CONCLUSION...................................................................................................................................12

REFERENCES........................................................................................................................................13

INTRODUCTION.................................................................................................................................3

TASK 1.................................................................................................................................................3

P1 Explain management accounting and essential requirement of different type of management

accounting system.............................................................................................................................3

P2 Different methods used for management accounting report.........................................................4

TASK 2.................................................................................................................................................6

P3 Calculate cost using appropriate technique for calculating profit.............................................6

TASK 3.................................................................................................................................................9

P4 Explain advantages and disadvantages of various type planning tools for budgetary control.......9

TASK 4...............................................................................................................................................10

P5 Compare ways how management accounting system is used to respond financial problem.......10

CONCLUSION...................................................................................................................................12

REFERENCES........................................................................................................................................13

INTRODUCTION

Effective management and operation is based upon effective working management

and representation of reports and management. Management accounting is one of the

essential aspect organisational and business context (Wickramasinghe and Alawattage, 2012).

Various type of accounting policies and standards are followed by organisations subject to

effective management. This report is prepared to explain management accounting system and

essential requirement of different type of management accounting system. Various methods

for management accounting defined in this report. Cost technique are also defined in this

context. Advantages and disadvantages of various type of planning tools which are used in

budgetary control also defined in this context. How organisations are adapting management

accounting system to respond financial problems are also explained in this context. Tech

(UK) limited is opted organisation to elaborate the dynamics of management accounting.

TASK 1

P1 Explain management accounting and essential requirement of different type of

management accounting system

Management accounting is one of the essential aspect which is considered very useful

and effective in organisational

context. to make effective management and operation for better management and operation.

To make effective management and operation it is required to align All the departments and

sections of an organisation in such a manner so that managers become able to make strategies

and plans. Management accounting is also called as managerial accounting because this

accounting is very useful for managerial decisions and effective decision-making process.

Making plants, preparing Strategies for better forecasting analysing future threats and

opportunities in order to achieve core competence of organisations are main objective of

Management Accounting.

There is no any specific concept and principle are made for management accoutring.

Organisations set their own standards and accounting structures for better growth and

development of organisation. This is also called as internal accounting system. Management

accounting is adapted by organisations to analyse the make managerial strong and flexible

subject to opportunities and threats.

Proper planning, organising, staffing and effective communication structure are some

important feature for a successful organisation. Management accounting provides a

systematic order in order to record and manage the structure of organisation in effctive

manner. Various type of management accounting systems are used by organisations as per

business requirements and suitability. Management accounting system assist managers and

senior authority subject to choose better options and plants which remain associated with

growth and development of organisation. Different type of management accounting systems

are as follows:

Job Costing system: Analysing the cost of different type of sections and departments of

organisation is one of the main objective of a job costing system. This accounting system

helps to manage and comprise all over cost of different sections and departments of business.

It helps to determine the cost and profit of each department and helps to analyse the

performance of each department. This is considered as a process which remain associated

Effective management and operation is based upon effective working management

and representation of reports and management. Management accounting is one of the

essential aspect organisational and business context (Wickramasinghe and Alawattage, 2012).

Various type of accounting policies and standards are followed by organisations subject to

effective management. This report is prepared to explain management accounting system and

essential requirement of different type of management accounting system. Various methods

for management accounting defined in this report. Cost technique are also defined in this

context. Advantages and disadvantages of various type of planning tools which are used in

budgetary control also defined in this context. How organisations are adapting management

accounting system to respond financial problems are also explained in this context. Tech

(UK) limited is opted organisation to elaborate the dynamics of management accounting.

TASK 1

P1 Explain management accounting and essential requirement of different type of

management accounting system

Management accounting is one of the essential aspect which is considered very useful

and effective in organisational

context. to make effective management and operation for better management and operation.

To make effective management and operation it is required to align All the departments and

sections of an organisation in such a manner so that managers become able to make strategies

and plans. Management accounting is also called as managerial accounting because this

accounting is very useful for managerial decisions and effective decision-making process.

Making plants, preparing Strategies for better forecasting analysing future threats and

opportunities in order to achieve core competence of organisations are main objective of

Management Accounting.

There is no any specific concept and principle are made for management accoutring.

Organisations set their own standards and accounting structures for better growth and

development of organisation. This is also called as internal accounting system. Management

accounting is adapted by organisations to analyse the make managerial strong and flexible

subject to opportunities and threats.

Proper planning, organising, staffing and effective communication structure are some

important feature for a successful organisation. Management accounting provides a

systematic order in order to record and manage the structure of organisation in effctive

manner. Various type of management accounting systems are used by organisations as per

business requirements and suitability. Management accounting system assist managers and

senior authority subject to choose better options and plants which remain associated with

growth and development of organisation. Different type of management accounting systems

are as follows:

Job Costing system: Analysing the cost of different type of sections and departments of

organisation is one of the main objective of a job costing system. This accounting system

helps to manage and comprise all over cost of different sections and departments of business.

It helps to determine the cost and profit of each department and helps to analyse the

performance of each department. This is considered as a process which remain associated

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

with specific job centre or section (Lavia, López and Hiebl, 2014). This System considered

essential in respect of analysing results with accurate results. Information related to direct

material direct labour and direct expenses are some essential information which remain

associated with job costing system.

Inventory management system: Managing the level of inventories, economic order

quantity and effctive costing system subject to stock valuation are essential aspects

considered in inventory management system. It is required for any organisation that analyse

the cost of inventories in stock and manage the level of requirement for a particular duration.

This remain associated with the effective management and operation of departmental stores,

storages. There are some essential aspects which helps to analyse cost of inventories are also

some major aspect which remain essential for organisational growth and development.

Inventory management system assist managers to assign roles and responsibilities of store

manager and departmental manager for better optimisation. This accounting system not only

helps to manage the inventory levels but also helps to understand the lag in period for

manufacturing desired production units.

Pricing optimising system: this is one of the important management accounting system

which helps to control the cost and deciding the price of products and services of an

organisation. This accounting system remain essential in respect of decision making process.

All the essential aspects and elements are covered in this context which helps to analyse the

cost of product and deciding the price. With the help of this management system managers be

able to sort out the pricing strategies and optimise the price of products and services. prices is

optimised by considering cost controlling factors and aspects (Christ, 2014).

Risk and financial management: analysing associated risk and management is one

of the key aspect of risk and financial management. This is also remains essential as per

managers and senior level authority’s perspective. It is important for mangers to identify the

risk factors which remain affect the performance and growth of organisation. This

management accounting system basically helps to make importance financial and investment

decisions. Risk management system contains some computer based and system generated

information which assist managers to make best investment and financial plans.

Management information system: this accounting system is majorly used by large

business organisations. MIS system is considered one of the strategic system which helps to

analyse the performance and growth of organist ion in statistical form and order. There is

always some essential aspect remain associated with organisational performance and growth.

MIS system produces system generated information and details which are used to track

organisational performance and track the records in effective manner. Resolving complex

business situation subject to preparing more effective and accurate plans is main objective of

management information system.

P2 Different methods used for management accounting report

Reporting is one of the important part for any organisation. Management reports are

the part of making plans, preparing strategies and analysing plans for better growth and

development of organisation. Managements accounting reports helps to keep up to date

subject to track the performance of organization. Management accounting reports helps

mangers to track the records and transactions for a specific duration and time. Management

accounting reports summarise the information and detail in short form by which departmental

essential in respect of analysing results with accurate results. Information related to direct

material direct labour and direct expenses are some essential information which remain

associated with job costing system.

Inventory management system: Managing the level of inventories, economic order

quantity and effctive costing system subject to stock valuation are essential aspects

considered in inventory management system. It is required for any organisation that analyse

the cost of inventories in stock and manage the level of requirement for a particular duration.

This remain associated with the effective management and operation of departmental stores,

storages. There are some essential aspects which helps to analyse cost of inventories are also

some major aspect which remain essential for organisational growth and development.

Inventory management system assist managers to assign roles and responsibilities of store

manager and departmental manager for better optimisation. This accounting system not only

helps to manage the inventory levels but also helps to understand the lag in period for

manufacturing desired production units.

Pricing optimising system: this is one of the important management accounting system

which helps to control the cost and deciding the price of products and services of an

organisation. This accounting system remain essential in respect of decision making process.

All the essential aspects and elements are covered in this context which helps to analyse the

cost of product and deciding the price. With the help of this management system managers be

able to sort out the pricing strategies and optimise the price of products and services. prices is

optimised by considering cost controlling factors and aspects (Christ, 2014).

Risk and financial management: analysing associated risk and management is one

of the key aspect of risk and financial management. This is also remains essential as per

managers and senior level authority’s perspective. It is important for mangers to identify the

risk factors which remain affect the performance and growth of organisation. This

management accounting system basically helps to make importance financial and investment

decisions. Risk management system contains some computer based and system generated

information which assist managers to make best investment and financial plans.

Management information system: this accounting system is majorly used by large

business organisations. MIS system is considered one of the strategic system which helps to

analyse the performance and growth of organist ion in statistical form and order. There is

always some essential aspect remain associated with organisational performance and growth.

MIS system produces system generated information and details which are used to track

organisational performance and track the records in effective manner. Resolving complex

business situation subject to preparing more effective and accurate plans is main objective of

management information system.

P2 Different methods used for management accounting report

Reporting is one of the important part for any organisation. Management reports are

the part of making plans, preparing strategies and analysing plans for better growth and

development of organisation. Managements accounting reports helps to keep up to date

subject to track the performance of organization. Management accounting reports helps

mangers to track the records and transactions for a specific duration and time. Management

accounting reports summarise the information and detail in short form by which departmental

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and sectional information become easy to understand. Reports are prepared by accountants

and departmental manages. All the relevant information and sources are considered in one

single format subject to analyse essential factors of organisational performance and growth

(Moser, 2012).

Managements reports assist managers to understand the sectional performance of

organisation as well as helps to bifurcate the information in sectional figures. These reports

remain essential subject to getting information and details at primary level and stage.

Management reports make decision making process more smooth and easy for sustainable

growth and development of organisation. It remains essential for both mangers and seniors to

make important plans and strategies to overcome financial and non-financial problems of

organisation. Various type of methods is used subject to management accounting reports.

Major methods subject to management accounting reports are defined as follows:

Performance reports: these are the reports which are useful to record all the

transactions and events of operations and management for specific year. A summarised

information and details are published in the form of performance report. Individual

departmental information and details are analysed in this context subject to analyse individual

performance. All the sectional reports are consolidated at single point subject to determine

average performance and details of organisation. Actual performance of organisation is

evaluated with the budgeted performance of organisation. With these reports managers, be

able to find out performance affecting factors which impact the perfoamcnce of individual

and group. Performance affecting factors are tried to sorted out with the help of this

management system.

Inventory management reports: these are the reports which provides information

related to consumption, wastage, rate of production rate, average inventory in stock and in

production process. These information helps to analyse further raw material and supporting

sources for better organisational growth and development. This is one of the essential aspect

which remain associated with the management of inventory levels and operational and

management. Inventory reports provides entire information and details like how much closing

stock remain for carry forward next year. Inventory reports helps managers to evaluate the

factors and elements which increase the wastage level. With the help of inventory

management reports mangers become eligible to make plans and strategies to control wastage

and improve productivity as well as efficiency.

Job cost reports: analysing the cost of overall job canter and cost centre is one of the

main objective of job cost reports. These reports contain vital information related to

development and growth of an organisation. Overall cost depends upon cost measurement

tools and management which not only helps to analyse the overall cost of operations but also

helps to analyse the cost incurred at particular job centre. With the help of job cost reports

managers and senior level authorities be able to sort out plans and strategies subject to

effective management and growth. With the help of job cost repots budgetary control process

also can be easily managed (Hilton and Platt, 2013).

Accounts receivable reports: these are the records which helps to analyse the detail

and information related to debtors and customers. this is one of the essential aspect in resect

of managing debtors and customers of organisation. There is an information and report

produced by sales department of organisation. These reports contain that how much payment

and departmental manages. All the relevant information and sources are considered in one

single format subject to analyse essential factors of organisational performance and growth

(Moser, 2012).

Managements reports assist managers to understand the sectional performance of

organisation as well as helps to bifurcate the information in sectional figures. These reports

remain essential subject to getting information and details at primary level and stage.

Management reports make decision making process more smooth and easy for sustainable

growth and development of organisation. It remains essential for both mangers and seniors to

make important plans and strategies to overcome financial and non-financial problems of

organisation. Various type of methods is used subject to management accounting reports.

Major methods subject to management accounting reports are defined as follows:

Performance reports: these are the reports which are useful to record all the

transactions and events of operations and management for specific year. A summarised

information and details are published in the form of performance report. Individual

departmental information and details are analysed in this context subject to analyse individual

performance. All the sectional reports are consolidated at single point subject to determine

average performance and details of organisation. Actual performance of organisation is

evaluated with the budgeted performance of organisation. With these reports managers, be

able to find out performance affecting factors which impact the perfoamcnce of individual

and group. Performance affecting factors are tried to sorted out with the help of this

management system.

Inventory management reports: these are the reports which provides information

related to consumption, wastage, rate of production rate, average inventory in stock and in

production process. These information helps to analyse further raw material and supporting

sources for better organisational growth and development. This is one of the essential aspect

which remain associated with the management of inventory levels and operational and

management. Inventory reports provides entire information and details like how much closing

stock remain for carry forward next year. Inventory reports helps managers to evaluate the

factors and elements which increase the wastage level. With the help of inventory

management reports mangers become eligible to make plans and strategies to control wastage

and improve productivity as well as efficiency.

Job cost reports: analysing the cost of overall job canter and cost centre is one of the

main objective of job cost reports. These reports contain vital information related to

development and growth of an organisation. Overall cost depends upon cost measurement

tools and management which not only helps to analyse the overall cost of operations but also

helps to analyse the cost incurred at particular job centre. With the help of job cost reports

managers and senior level authorities be able to sort out plans and strategies subject to

effective management and growth. With the help of job cost repots budgetary control process

also can be easily managed (Hilton and Platt, 2013).

Accounts receivable reports: these are the records which helps to analyse the detail

and information related to debtors and customers. this is one of the essential aspect in resect

of managing debtors and customers of organisation. There is an information and report

produced by sales department of organisation. These reports contain that how much payment

is still remaining to get. These reports help to make credit policies for potential customers and

debtors effective managements and operations subject to unpaid customers are tackled by

account receivable reports. With the help of these reports lag in time of collecting payments

can be reduced easily.

Operational budget reports: this is also considered as overall report of producing

information and details. There are some essential aspects are covered subject to manage and

operate in vital form. Operational budgets help to reduce the level of administration and

operational activities. Operational budget reports contain information and details subject to

effective management and operation. All the income and expenditure which are incurred

during the year are considered in single format. Allocation and appropriation of financial

resources can be manged with the help of operational budget reports.

TASK 2

P3 Calculate cost using appropriate technique for calculating profit

Cost is one of the essential aspect in organisational context. There is various type of

nature of cost exists in organisational perspective such as production cost, operational cost,

and non-operational cost. organisations adopt various type of cost measurement tools and

techniques which helps to analyse the cost. Management accounting techniques are used to

control increased cost and reducing the factors which increase the production cost and non-

production cost. Various type of management accounting techniques is defined as follows:

Cost volume profit (CVP): this is one of the important pat of subject to modify and

rephrase the cost and volume structure of organisation. analysing the structure of organisation

subject to production cost and evaluation of profit with projected sales value.

Flexible budgeting: this technique is basically used to comprise the cost and adjust

the structure of organisation in systematic manner. This is one of the essential feature in order

to make flexible strategies and plans. This can be vary as per the change in output.

Cost variance: This technique basically used by organisations to Determine the

difference between actual and budgeted cost. This helps to compensate the difference which

occurs during the changes and measurement of cost analysis.

Marginal costing: this is one of the costing technique which helps to analyse the aspects of

all variable cost and production overheads which remain associated with production and

manufacturing process of marginal context. Marginal costing helps to analyse the cost of

overall production and manufacturing units. Direct material, direct labour and direct

expensed are key elements which are considered in marginal costing. This helps to analyse

the strategic decision which directly remain associated with production process. As per

decision making perspective marginal costing plays significant role. This costing remains the

part of unit costing (Becker, Ulrich and Staffel, 2011).

Abortion costing: absorption costing remains associated with overall cost of

organisation. This is also called as full costing calculation method which helps to analysing

and measured the cost of operations in sequential manner. All the direct and indirect parts are

also considered in this context subject to evaluating cost of product and services. This costing

technique remains relevant for absorption costing subject to higher profit. One drawback of

debtors effective managements and operations subject to unpaid customers are tackled by

account receivable reports. With the help of these reports lag in time of collecting payments

can be reduced easily.

Operational budget reports: this is also considered as overall report of producing

information and details. There are some essential aspects are covered subject to manage and

operate in vital form. Operational budgets help to reduce the level of administration and

operational activities. Operational budget reports contain information and details subject to

effective management and operation. All the income and expenditure which are incurred

during the year are considered in single format. Allocation and appropriation of financial

resources can be manged with the help of operational budget reports.

TASK 2

P3 Calculate cost using appropriate technique for calculating profit

Cost is one of the essential aspect in organisational context. There is various type of

nature of cost exists in organisational perspective such as production cost, operational cost,

and non-operational cost. organisations adopt various type of cost measurement tools and

techniques which helps to analyse the cost. Management accounting techniques are used to

control increased cost and reducing the factors which increase the production cost and non-

production cost. Various type of management accounting techniques is defined as follows:

Cost volume profit (CVP): this is one of the important pat of subject to modify and

rephrase the cost and volume structure of organisation. analysing the structure of organisation

subject to production cost and evaluation of profit with projected sales value.

Flexible budgeting: this technique is basically used to comprise the cost and adjust

the structure of organisation in systematic manner. This is one of the essential feature in order

to make flexible strategies and plans. This can be vary as per the change in output.

Cost variance: This technique basically used by organisations to Determine the

difference between actual and budgeted cost. This helps to compensate the difference which

occurs during the changes and measurement of cost analysis.

Marginal costing: this is one of the costing technique which helps to analyse the aspects of

all variable cost and production overheads which remain associated with production and

manufacturing process of marginal context. Marginal costing helps to analyse the cost of

overall production and manufacturing units. Direct material, direct labour and direct

expensed are key elements which are considered in marginal costing. This helps to analyse

the strategic decision which directly remain associated with production process. As per

decision making perspective marginal costing plays significant role. This costing remains the

part of unit costing (Becker, Ulrich and Staffel, 2011).

Abortion costing: absorption costing remains associated with overall cost of

organisation. This is also called as full costing calculation method which helps to analysing

and measured the cost of operations in sequential manner. All the direct and indirect parts are

also considered in this context subject to evaluating cost of product and services. This costing

technique remains relevant for absorption costing subject to higher profit. One drawback of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

this costing technique is that absorption costing do not remain the part of decision making

process.

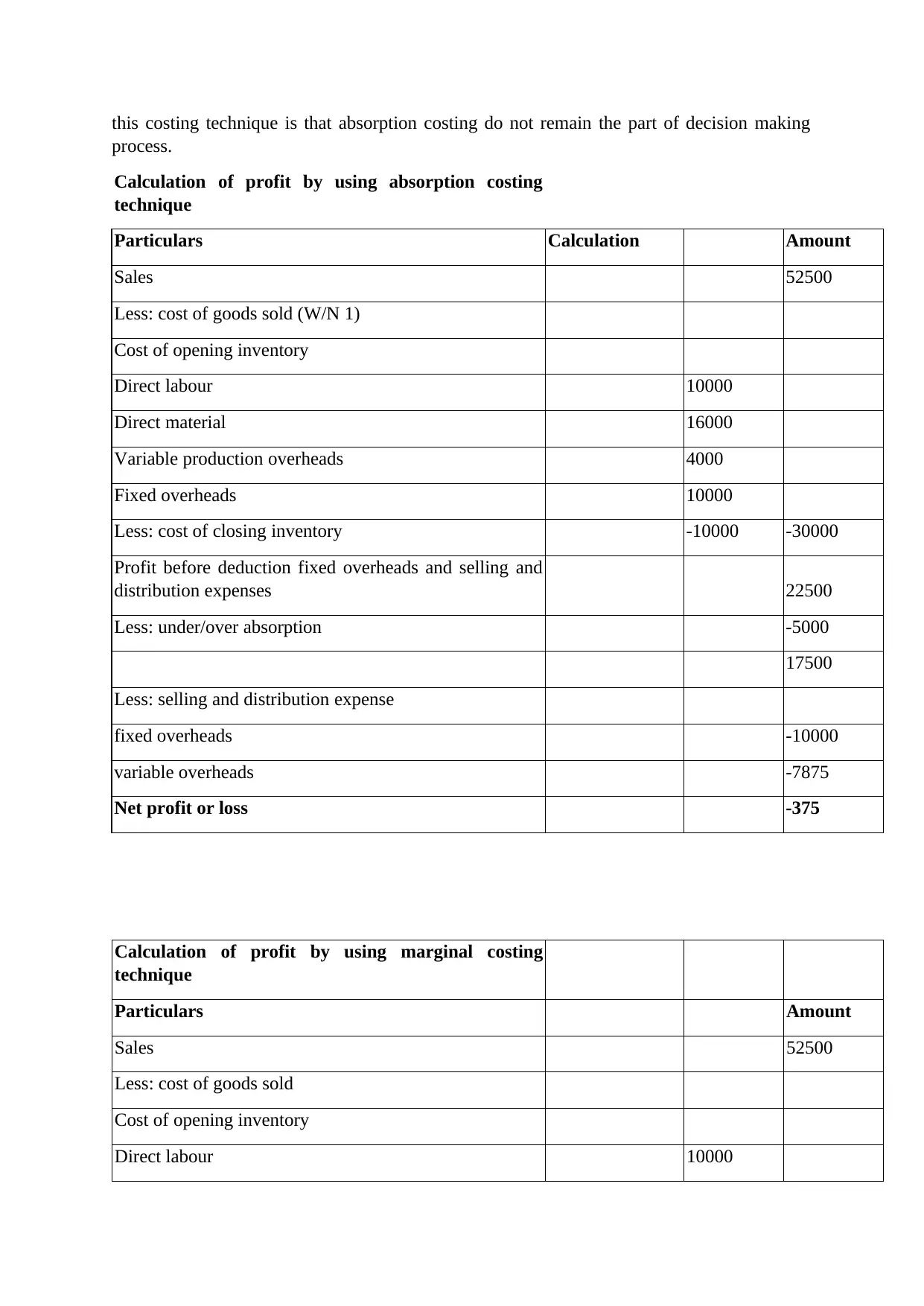

Calculation of profit by using absorption costing

technique

Particulars Calculation Amount

Sales 52500

Less: cost of goods sold (W/N 1)

Cost of opening inventory

Direct labour 10000

Direct material 16000

Variable production overheads 4000

Fixed overheads 10000

Less: cost of closing inventory -10000 -30000

Profit before deduction fixed overheads and selling and

distribution expenses 22500

Less: under/over absorption -5000

17500

Less: selling and distribution expense

fixed overheads -10000

variable overheads -7875

Net profit or loss -375

Calculation of profit by using marginal costing

technique

Particulars Amount

Sales 52500

Less: cost of goods sold

Cost of opening inventory

Direct labour 10000

process.

Calculation of profit by using absorption costing

technique

Particulars Calculation Amount

Sales 52500

Less: cost of goods sold (W/N 1)

Cost of opening inventory

Direct labour 10000

Direct material 16000

Variable production overheads 4000

Fixed overheads 10000

Less: cost of closing inventory -10000 -30000

Profit before deduction fixed overheads and selling and

distribution expenses 22500

Less: under/over absorption -5000

17500

Less: selling and distribution expense

fixed overheads -10000

variable overheads -7875

Net profit or loss -375

Calculation of profit by using marginal costing

technique

Particulars Amount

Sales 52500

Less: cost of goods sold

Cost of opening inventory

Direct labour 10000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Direct material 16000

Variable production overheads 4000

Less: cost of closing inventory (500*15) -7500 -22500

Profit before selling and distribution expenses 30000

Less: selling and distribution expense

variable overheads -7875

Net profit or loss 22125

Less: Fixed cost -25000

Profit/loss -2875

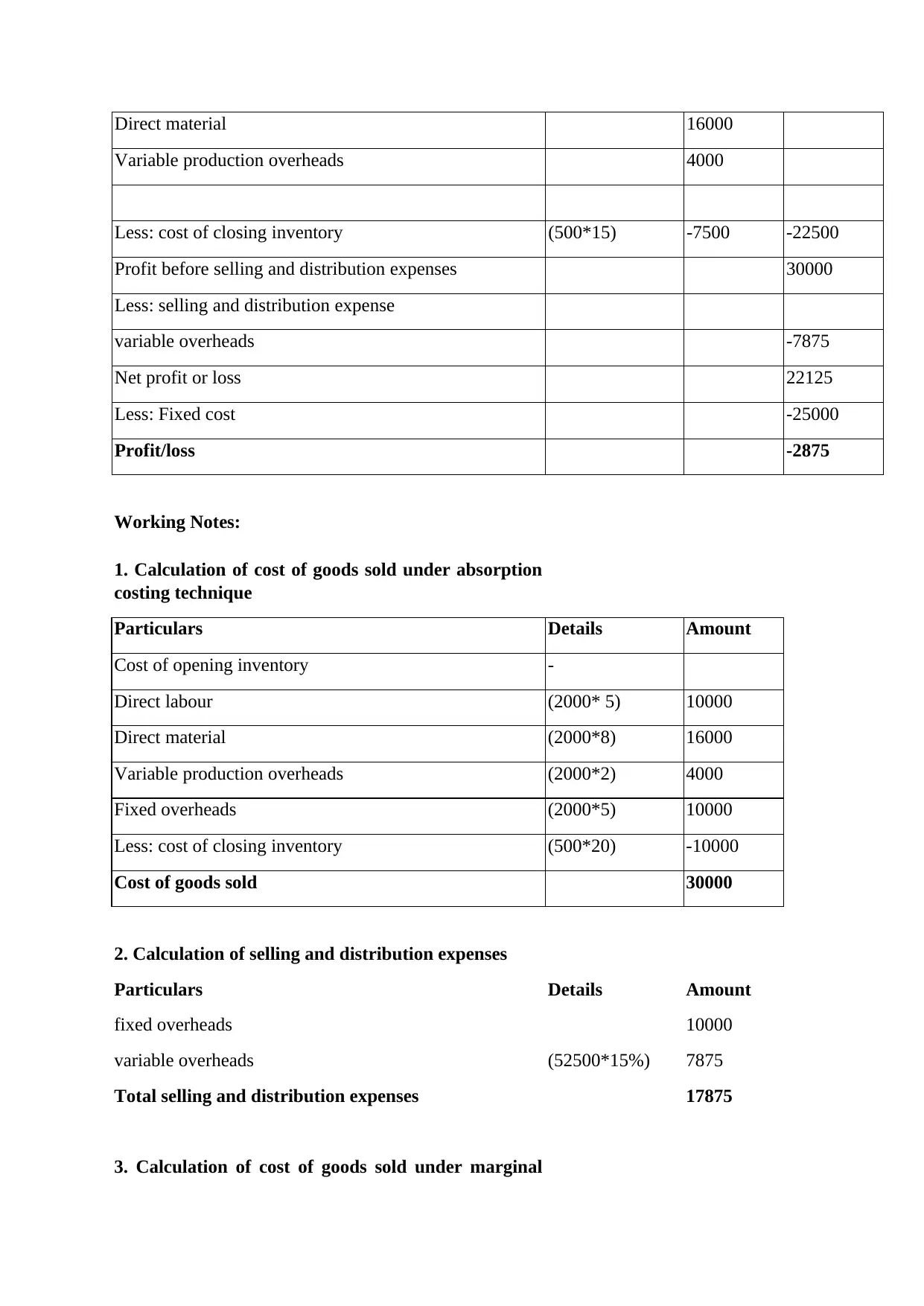

Working Notes:

1. Calculation of cost of goods sold under absorption

costing technique

Particulars Details Amount

Cost of opening inventory -

Direct labour (2000* 5) 10000

Direct material (2000*8) 16000

Variable production overheads (2000*2) 4000

Fixed overheads (2000*5) 10000

Less: cost of closing inventory (500*20) -10000

Cost of goods sold 30000

2. Calculation of selling and distribution expenses

Particulars Details Amount

fixed overheads 10000

variable overheads (52500*15%) 7875

Total selling and distribution expenses 17875

3. Calculation of cost of goods sold under marginal

Variable production overheads 4000

Less: cost of closing inventory (500*15) -7500 -22500

Profit before selling and distribution expenses 30000

Less: selling and distribution expense

variable overheads -7875

Net profit or loss 22125

Less: Fixed cost -25000

Profit/loss -2875

Working Notes:

1. Calculation of cost of goods sold under absorption

costing technique

Particulars Details Amount

Cost of opening inventory -

Direct labour (2000* 5) 10000

Direct material (2000*8) 16000

Variable production overheads (2000*2) 4000

Fixed overheads (2000*5) 10000

Less: cost of closing inventory (500*20) -10000

Cost of goods sold 30000

2. Calculation of selling and distribution expenses

Particulars Details Amount

fixed overheads 10000

variable overheads (52500*15%) 7875

Total selling and distribution expenses 17875

3. Calculation of cost of goods sold under marginal

costing technique

Particulars Details Amount

Cost of opening inventory -

Direct labour (2000* 5) 10000

Direct material (2000*8) 16000

Variable production overheads (2000*2) 4000

Less: cost of closing inventory (500*15) 7500

Cost of goods sold 22500

TASK 3

P4 Explain advantages and disadvantages of various type planning tools for budgetary control

Budgetary control is process which assist managerial operations towards achieving desired

aim and objective. Making budgets and framing the structure of organisation depends upon effective

management and growth of organisation. Various type of budgets are prepared under budgetary

control process such as:

Operational budget: this budget is prepared to take essential decisions and important

aspect subject to organisational growth and development. Accurate results are taken with the help

of operational budgets. It also decision-making process such as vital decision in increasing total

earning and expenses. Preparing strategies and plans for effective management is one of the key

aspect of operational budget.

Cash budget: this budget is prepared to analyse the requirement of cash during the year. It

is essential for organisation to analyse the cash requirement and utilise the amount of investment in

effective manner.

Various type of budgets is prepared by organisations subject to analyse income and expenditure

structure of organisation. Various type of planning tools are used in budgetary control process such

as;

ZERO based budging

Zero based budgeting is a method which is used to analyse all the expenses and Income

stage estimate for new period. This budgeting method is prepared on the basis of zero base which

contains zero expenditure and zero income generation sources at initial stage. Zero based budgeting

process starts at 0 and help to analyse the cost and expenditures which are incurred for periodic

events. There is one drawback of this budgeting process which is very complex subject to

understand that I am in a mix of estimated cost and expenditures (Eierle and Schultze, 2013).

Advantages:

This helps to analyses the cost from zero base.

Managers become eligible to make strategies plans at initial level.

Disadvantages:

Particulars Details Amount

Cost of opening inventory -

Direct labour (2000* 5) 10000

Direct material (2000*8) 16000

Variable production overheads (2000*2) 4000

Less: cost of closing inventory (500*15) 7500

Cost of goods sold 22500

TASK 3

P4 Explain advantages and disadvantages of various type planning tools for budgetary control

Budgetary control is process which assist managerial operations towards achieving desired

aim and objective. Making budgets and framing the structure of organisation depends upon effective

management and growth of organisation. Various type of budgets are prepared under budgetary

control process such as:

Operational budget: this budget is prepared to take essential decisions and important

aspect subject to organisational growth and development. Accurate results are taken with the help

of operational budgets. It also decision-making process such as vital decision in increasing total

earning and expenses. Preparing strategies and plans for effective management is one of the key

aspect of operational budget.

Cash budget: this budget is prepared to analyse the requirement of cash during the year. It

is essential for organisation to analyse the cash requirement and utilise the amount of investment in

effective manner.

Various type of budgets is prepared by organisations subject to analyse income and expenditure

structure of organisation. Various type of planning tools are used in budgetary control process such

as;

ZERO based budging

Zero based budgeting is a method which is used to analyse all the expenses and Income

stage estimate for new period. This budgeting method is prepared on the basis of zero base which

contains zero expenditure and zero income generation sources at initial stage. Zero based budgeting

process starts at 0 and help to analyse the cost and expenditures which are incurred for periodic

events. There is one drawback of this budgeting process which is very complex subject to

understand that I am in a mix of estimated cost and expenditures (Eierle and Schultze, 2013).

Advantages:

This helps to analyses the cost from zero base.

Managers become eligible to make strategies plans at initial level.

Disadvantages:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Level of budget starts at zero base even after not having extra cost

Lack of credible resources are found in respects of making budgets

Incremental budget: Method which is used in budgeting control and budgeting process. Allocation

and appropriation of resources remain based upon previous period or past events. This busting tool

also have to analyse Bustard results and actual results in respect of organisational performance.

Moreover, this budgeting tool helps managers and senior authority is to educate all the resources in

adequate manual so that competitive advantage can be achieved in effectively and efficiently. This

costing method used by Organisation in incremental situations when cost is not certain subject to

operations and management (Akbar, 2010).

Advantages:

Budgets remain stable accept incremental changes in cost and expenditure

Effects and impact can be easily seen by incremental changes

Coordination and combination between actual and busted results can be

achieved accurately.

Disadvantages:

This is the same process which is employed and used by organisation for

further period

Lack of innovative ideas and approaches found in this busting tool

Activiti based budgeting

This is also known as essential element of welding processes which is based upon system

design and transparency of figures. It provides a large overview of organisation subject to a locating

and appropriate in the resources for better performance and growth. This directly related to actual

activities which remain associated with operational and production processes.

Advantages:

It improvised local planning and forecasting structure of organization

Revenue structure is analyzed on the basis of actual activities

Disadvantages:

Time consuming and cost consuming busting process which may critical the

process of western control.

This also do not provide accurate results from effective forecasting process.

TASK 4

P5 Compare ways how management accounting system is used to respond financial problem

Management accounting refers to the interpretation and presenting the

accounting information which is required to plan a strategy of your business. The

information can be seek through cost accounting as well as financial accounting. This

helps a manager to perform a decision process for their businesses.

New condition and environment is evolve during the new market evolution so

information is said to be a tool to measure the performance of a business for a financial

Lack of credible resources are found in respects of making budgets

Incremental budget: Method which is used in budgeting control and budgeting process. Allocation

and appropriation of resources remain based upon previous period or past events. This busting tool

also have to analyse Bustard results and actual results in respect of organisational performance.

Moreover, this budgeting tool helps managers and senior authority is to educate all the resources in

adequate manual so that competitive advantage can be achieved in effectively and efficiently. This

costing method used by Organisation in incremental situations when cost is not certain subject to

operations and management (Akbar, 2010).

Advantages:

Budgets remain stable accept incremental changes in cost and expenditure

Effects and impact can be easily seen by incremental changes

Coordination and combination between actual and busted results can be

achieved accurately.

Disadvantages:

This is the same process which is employed and used by organisation for

further period

Lack of innovative ideas and approaches found in this busting tool

Activiti based budgeting

This is also known as essential element of welding processes which is based upon system

design and transparency of figures. It provides a large overview of organisation subject to a locating

and appropriate in the resources for better performance and growth. This directly related to actual

activities which remain associated with operational and production processes.

Advantages:

It improvised local planning and forecasting structure of organization

Revenue structure is analyzed on the basis of actual activities

Disadvantages:

Time consuming and cost consuming busting process which may critical the

process of western control.

This also do not provide accurate results from effective forecasting process.

TASK 4

P5 Compare ways how management accounting system is used to respond financial problem

Management accounting refers to the interpretation and presenting the

accounting information which is required to plan a strategy of your business. The

information can be seek through cost accounting as well as financial accounting. This

helps a manager to perform a decision process for their businesses.

New condition and environment is evolve during the new market evolution so

information is said to be a tool to measure the performance of a business for a financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

year and expert can take a help of this tool to analyze their strategies and plan to modify

the old strategies. Financial problems can be solved after some accounting calculations,

called as key performance indicators (Leitner, 2013). For long lasting success financial

tool can be analyzed. There are two types of indicators:-

Some of the financial indicators are:-

Ratios:-ratio can be said as the most preferred or suitable source of measuring the

sustainable success in your business. Some of the main ratios are:-

Profitability

Liquidity

Revenue

Solvency

turnover

This ratio can show the true picture of your business financial problems and help you

handle the consequences of your strategies.

Some of the non-financial indicators are: -

Management of human resources: - this non-financial is very important in today’s

environment because staff is the asset of the company and company always give them

benefits and award to contribute more effort to make a business fruitful.

Product and service quality: - for long term sustainability, it is required to look into the

product and the service quality which is very important or a key part of the business

and it is required in every company (Absorption costing. 2018).

Brand awareness: - It is important to look into the matter of the brand awareness

because it can be directly reflecting to the growth of the company. Perceived quality and

loyalty is very much important to brand awareness(Weygandt, Kimmel and Kieso,

2015).This non-financial indicator can help the businessman to think beyond its

competitors and gain an advantage over them.

The role of management accounting in sustainable success and management:-

Cost accounting and financial accounting can help the managers to take a

decision to have a sustainable development of the company in the market and

take an advantage over others.

Management accounting can help in the production or in the some important

matters of the business through information and facts which is relevant to the

strategies.

Sustainable issues can be reduced through this because it can be defined the way

to make a strategy to your business.

For this you have to maintain or imply a strategic planning for its financial return

in the future.

Performance management is the way to measure the true report of the analysis

done on the financial and non-financial indicators.

Analysis and interpretation of information sought from various resources to

ensure the sustainable growth in the future.

the old strategies. Financial problems can be solved after some accounting calculations,

called as key performance indicators (Leitner, 2013). For long lasting success financial

tool can be analyzed. There are two types of indicators:-

Some of the financial indicators are:-

Ratios:-ratio can be said as the most preferred or suitable source of measuring the

sustainable success in your business. Some of the main ratios are:-

Profitability

Liquidity

Revenue

Solvency

turnover

This ratio can show the true picture of your business financial problems and help you

handle the consequences of your strategies.

Some of the non-financial indicators are: -

Management of human resources: - this non-financial is very important in today’s

environment because staff is the asset of the company and company always give them

benefits and award to contribute more effort to make a business fruitful.

Product and service quality: - for long term sustainability, it is required to look into the

product and the service quality which is very important or a key part of the business

and it is required in every company (Absorption costing. 2018).

Brand awareness: - It is important to look into the matter of the brand awareness

because it can be directly reflecting to the growth of the company. Perceived quality and

loyalty is very much important to brand awareness(Weygandt, Kimmel and Kieso,

2015).This non-financial indicator can help the businessman to think beyond its

competitors and gain an advantage over them.

The role of management accounting in sustainable success and management:-

Cost accounting and financial accounting can help the managers to take a

decision to have a sustainable development of the company in the market and

take an advantage over others.

Management accounting can help in the production or in the some important

matters of the business through information and facts which is relevant to the

strategies.

Sustainable issues can be reduced through this because it can be defined the way

to make a strategy to your business.

For this you have to maintain or imply a strategic planning for its financial return

in the future.

Performance management is the way to measure the true report of the analysis

done on the financial and non-financial indicators.

Analysis and interpretation of information sought from various resources to

ensure the sustainable growth in the future.

CONCLUSION

This report is prepared to analyse and evaluate concept of management accounting

system with in the organisation. Management accounting systems are demonstrated subject to

organisational context. Concept of management accounting system in wider organisational

context is defined in this context. Various type of methods which are used to management

accounting reports are defined in this context. Range of management accounting techniques

are applied in wider context subject to analyse the cost of operation and management.

Importance and use of planning tools used in management accounting system also defined in

this context. Ways are compared that how organisations are adapting management accounting

system subject to respond financial problems.

This report is prepared to analyse and evaluate concept of management accounting

system with in the organisation. Management accounting systems are demonstrated subject to

organisational context. Concept of management accounting system in wider organisational

context is defined in this context. Various type of methods which are used to management

accounting reports are defined in this context. Range of management accounting techniques

are applied in wider context subject to analyse the cost of operation and management.

Importance and use of planning tools used in management accounting system also defined in

this context. Ways are compared that how organisations are adapting management accounting

system subject to respond financial problems.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.