Capital Joinery Ltd - Management Accounting Report and Analysis

VerifiedAdded on 2022/12/29

|19

|4672

|76

Report

AI Summary

This report provides a comprehensive overview of management accounting principles, focusing on their practical application within Capital Joinery Ltd. It begins by defining management accounting and exploring various systems, including job costing, inventory management, cost accounting, and price optimization. The report then delves into the methods used for management accounting reports, such as account receivable reports, budget reports, performance reports, and cost managerial accounting reports. It examines the benefits of these systems. The core of the report analyzes costing techniques, including marginal costing, absorption costing, and standard costing, with detailed calculations and reconciliations. Furthermore, it investigates the benefits and drawbacks of planning tools used for budgetary control. Finally, the report discusses the use of management accounting tools in resolving financial problems and leading organizational success. The document provides practical examples and calculations to illustrate each concept, offering valuable insights into the application of management accounting within a real-world business context.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Brief description regarding various types of systems of management accounting................3

P2 Methods used for management accounting reports...............................................................4

M1 Benefits of management accounting system........................................................................5

TASK 2............................................................................................................................................7

P3 Calculation of cost by using management accounting techniques.........................................7

M2 Uses of management accounting techniques for formulate reports....................................11

TASK 3..........................................................................................................................................11

P4 Brief description regarding benefits & drawbacks of planning tools used for budgetary

control.......................................................................................................................................11

M3 Uses of planning tools for forecasting budgets..................................................................13

TASK 4..........................................................................................................................................13

P5 Brief explanation of use of management accounting tools for resolve financial problem. .13

M4 Use of management accounting tools for lead organization success by solving issue

related with financial problem..................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Brief description regarding various types of systems of management accounting................3

P2 Methods used for management accounting reports...............................................................4

M1 Benefits of management accounting system........................................................................5

TASK 2............................................................................................................................................7

P3 Calculation of cost by using management accounting techniques.........................................7

M2 Uses of management accounting techniques for formulate reports....................................11

TASK 3..........................................................................................................................................11

P4 Brief description regarding benefits & drawbacks of planning tools used for budgetary

control.......................................................................................................................................11

M3 Uses of planning tools for forecasting budgets..................................................................13

TASK 4..........................................................................................................................................13

P5 Brief explanation of use of management accounting tools for resolve financial problem. .13

M4 Use of management accounting tools for lead organization success by solving issue

related with financial problem..................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting is essential branch of accounting which apply by manager for

decision making purpose. In order to understand this concept Capital Joinery Ltd has been

taken. This organization is situated in UK, it is medium size business entity which provides best

quality of furniture, doors, window facilitates to their customers. This report includes the

relevance of different types of managerial accounting system as well as use of various

management accounting report for formulation of budget. This report also define how cost

calculate by using different technique and benefits of various planning tools. It is also showcase

use of benchmarking, and other technique of management accounting to solve monetary issue.

TASK 1

P1 Brief description regarding various types of systems of management accounting.

Management accounting: This term is combination of 2 essential word of running

business. One is management and other is accounting. Management is define as art of getting

things done by others. Accounting is procedure in which business transaction are collect,

analysis, record and present in effective manner. Management accounting is part of management

procedure which help in recording transaction in such a way which useful for managers in

decision making procedure (Anand, Balakrishnan and Labro, 2019).

There will be many types of system which used by manager in order to re4cord their

transaction following are define below Job costing system-based: This system is implemented by business entities in order to

calculate or measure cost required for fulfill demand of each business customers. Their

will be different types of cost assign by organizations in order to complete their particular

or specific job. Capital Joinery Ltd used job costing system in order to assign or

calculate job. Inventory management system: Stock is consider as most essential element of

organization. Success of business entity depend on how effective organization manage

their inventory. There various kinds of tools which help in manage, control and evaluate

maximum, minimum number of order required to fulfil demand of customers. Capital

Joinery Ltd use ABC, JIT,EOQ, LIFO and FIFO technique through which they can able

Management accounting is essential branch of accounting which apply by manager for

decision making purpose. In order to understand this concept Capital Joinery Ltd has been

taken. This organization is situated in UK, it is medium size business entity which provides best

quality of furniture, doors, window facilitates to their customers. This report includes the

relevance of different types of managerial accounting system as well as use of various

management accounting report for formulation of budget. This report also define how cost

calculate by using different technique and benefits of various planning tools. It is also showcase

use of benchmarking, and other technique of management accounting to solve monetary issue.

TASK 1

P1 Brief description regarding various types of systems of management accounting.

Management accounting: This term is combination of 2 essential word of running

business. One is management and other is accounting. Management is define as art of getting

things done by others. Accounting is procedure in which business transaction are collect,

analysis, record and present in effective manner. Management accounting is part of management

procedure which help in recording transaction in such a way which useful for managers in

decision making procedure (Anand, Balakrishnan and Labro, 2019).

There will be many types of system which used by manager in order to re4cord their

transaction following are define below Job costing system-based: This system is implemented by business entities in order to

calculate or measure cost required for fulfill demand of each business customers. Their

will be different types of cost assign by organizations in order to complete their particular

or specific job. Capital Joinery Ltd used job costing system in order to assign or

calculate job. Inventory management system: Stock is consider as most essential element of

organization. Success of business entity depend on how effective organization manage

their inventory. There various kinds of tools which help in manage, control and evaluate

maximum, minimum number of order required to fulfil demand of customers. Capital

Joinery Ltd use ABC, JIT,EOQ, LIFO and FIFO technique through which they can able

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to understand requirement of stock at the time of supplying finished goods for selling

purpose. Cost accounting system: This system is implemented by manager in order to calculated

final cost required for run or operate business cycle. There will be many technique or

tools which useful to determine cost and profit generate by selling business units. Cost

accounting system is implemented by Capital Joinery Ltd in order to systematically

recognize total cost organization bear to make products as well as run their day to day

business activities. They generally use marginal, absorption, standard costing tools

which useful in accurately determine cost of business activities (Anderson, 2017, Baard

and Dumay, 2020).

Price optimization system:This system is implemented by managers in order to

determine rate of price. As it is consider as factor which useful to generate profit. Thus

manager needs to choose their price rate which help in generate profit by satisfying

demand o0f customers. There will be many methods which manager of Capital Joinery

Ltd use to determine their price rate which includes, price penetration, price skimming,

price premium and discounting price method. Manager on the basis of stage of running

business cycle need to select and choose price method which useful in attain business

profits.

P2 Methods used for management accounting reports

Management Accounting Report

Management Accounting Report determine the financial status of a company. These

reports includes financial information right from records of accounting, transaction details,

profitability of a product, operating cost and regional sales over a period of time. With the help

of of these reports an organisation can plan, take decisions, regulate operations and also measure

the performance.

Types of Management Accounting Reports:

Account Receivable Report: It is a crucial element for any organisation that provide

credits to its customers. Managers can easily find out the defaulters by knowing there

remaining balance and they can change there credit policies accordingly. Separate

categories are formed for product and services whose payment are 30, 60, and 90 days

delayed. As in UK people are comfortable to purchase on credit basis, due to this Capital

purpose. Cost accounting system: This system is implemented by manager in order to calculated

final cost required for run or operate business cycle. There will be many technique or

tools which useful to determine cost and profit generate by selling business units. Cost

accounting system is implemented by Capital Joinery Ltd in order to systematically

recognize total cost organization bear to make products as well as run their day to day

business activities. They generally use marginal, absorption, standard costing tools

which useful in accurately determine cost of business activities (Anderson, 2017, Baard

and Dumay, 2020).

Price optimization system:This system is implemented by managers in order to

determine rate of price. As it is consider as factor which useful to generate profit. Thus

manager needs to choose their price rate which help in generate profit by satisfying

demand o0f customers. There will be many methods which manager of Capital Joinery

Ltd use to determine their price rate which includes, price penetration, price skimming,

price premium and discounting price method. Manager on the basis of stage of running

business cycle need to select and choose price method which useful in attain business

profits.

P2 Methods used for management accounting reports

Management Accounting Report

Management Accounting Report determine the financial status of a company. These

reports includes financial information right from records of accounting, transaction details,

profitability of a product, operating cost and regional sales over a period of time. With the help

of of these reports an organisation can plan, take decisions, regulate operations and also measure

the performance.

Types of Management Accounting Reports:

Account Receivable Report: It is a crucial element for any organisation that provide

credits to its customers. Managers can easily find out the defaulters by knowing there

remaining balance and they can change there credit policies accordingly. Separate

categories are formed for product and services whose payment are 30, 60, and 90 days

delayed. As in UK people are comfortable to purchase on credit basis, due to this Capital

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Joinery providing there articles on credit. It keeps a record on balancing figure and deal

with customers accordingly. Capital Joinery changes its credit policy according to the

credit worth of the customers

Budget Report: Theses reports helps to analyse the performance of company by

comparing them with past records. Prior years income and expenditures are considered

while estimating the budget for a period. Capital Joinery has budgeted the expenses in

advance regarding exporting of woods, which helps them to cut exporting cost and make

more profit. Good tools are used as compared to last year at low cost as they have find

new suppliers. Performance Report: It is determine the outcome of an activity and work performance

of every employee or of over all company. This reports helps the manager to form

strategic decisions about future aspects. It maintain the accuracy about the performance

of an organisation. Capital Joinery with help of performance report consistently

performing well. By measuring there performance Capital Joinery has now increase its

net worth and has maintain to utilise the full efficiency of its employees. Performance

report provides them structure for future, on the other hand they have maintain the

quantity of woods. They have introduce different technology in there work with keeping

in mind the needs of there customers (Christensen, Skærbæk and Tryggestad, 2019) . Cost Managerial Accounting Report: This report consider all the cost that are incurred

in manufacturing the articles. Profit margins are determine by taking overhead, labour,

raw material cost and other cost that are taken in deliberation. All these totals are divided

by amount of articles produced. Capital Joinery maintained records of cost of wood,

exporting cost, labour cost and other raw materials such as clocks, iron pipes. This cost

keeping helps it to determine there total expenses and what cost they can set for there

windows, casements etc.

M1 Benefits of management accounting system.

Management accounting system Benefits and essential requirement of theses

system

Job costing system-based: Capital Joinery use this system in order to

with customers accordingly. Capital Joinery changes its credit policy according to the

credit worth of the customers

Budget Report: Theses reports helps to analyse the performance of company by

comparing them with past records. Prior years income and expenditures are considered

while estimating the budget for a period. Capital Joinery has budgeted the expenses in

advance regarding exporting of woods, which helps them to cut exporting cost and make

more profit. Good tools are used as compared to last year at low cost as they have find

new suppliers. Performance Report: It is determine the outcome of an activity and work performance

of every employee or of over all company. This reports helps the manager to form

strategic decisions about future aspects. It maintain the accuracy about the performance

of an organisation. Capital Joinery with help of performance report consistently

performing well. By measuring there performance Capital Joinery has now increase its

net worth and has maintain to utilise the full efficiency of its employees. Performance

report provides them structure for future, on the other hand they have maintain the

quantity of woods. They have introduce different technology in there work with keeping

in mind the needs of there customers (Christensen, Skærbæk and Tryggestad, 2019) . Cost Managerial Accounting Report: This report consider all the cost that are incurred

in manufacturing the articles. Profit margins are determine by taking overhead, labour,

raw material cost and other cost that are taken in deliberation. All these totals are divided

by amount of articles produced. Capital Joinery maintained records of cost of wood,

exporting cost, labour cost and other raw materials such as clocks, iron pipes. This cost

keeping helps it to determine there total expenses and what cost they can set for there

windows, casements etc.

M1 Benefits of management accounting system.

Management accounting system Benefits and essential requirement of theses

system

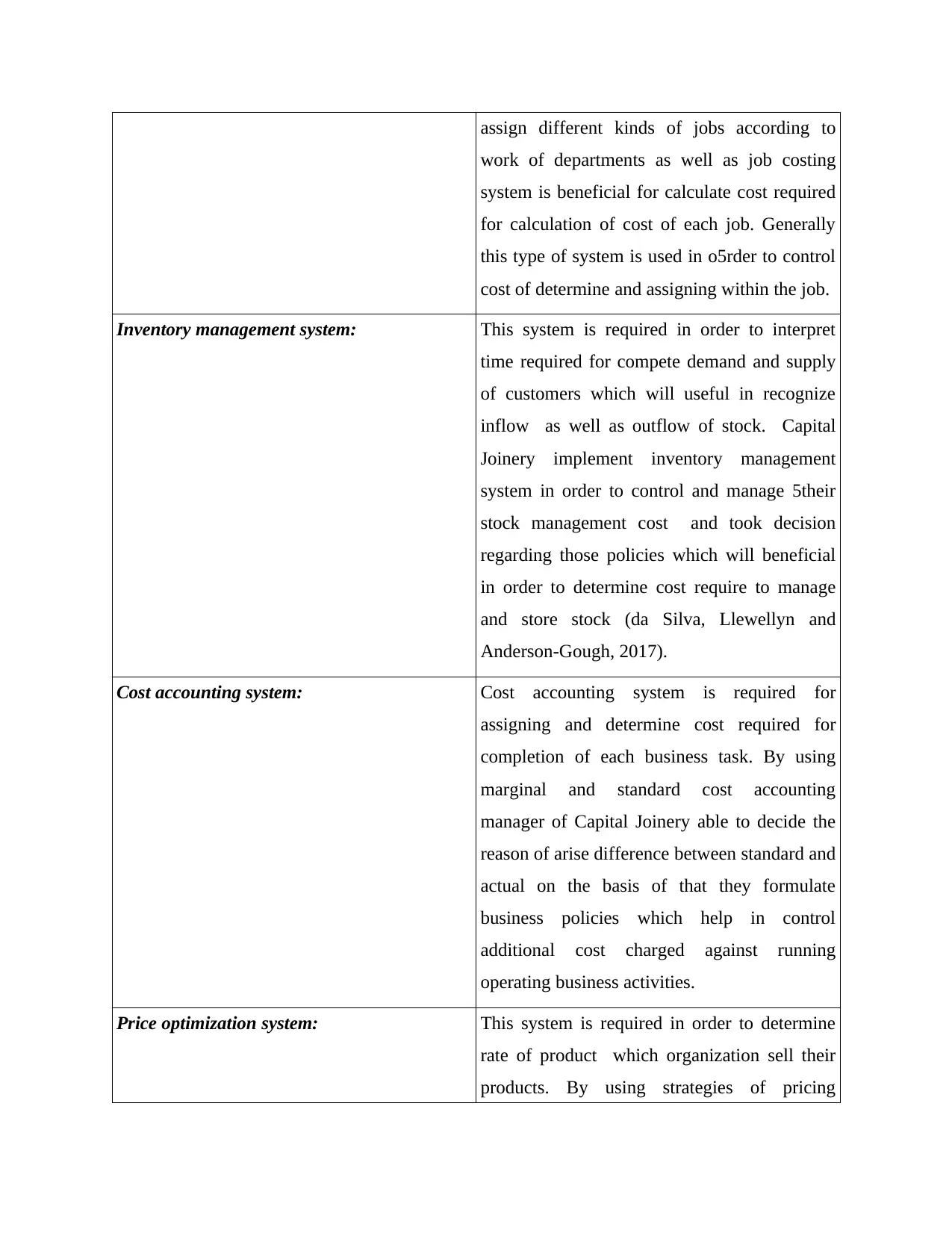

Job costing system-based: Capital Joinery use this system in order to

assign different kinds of jobs according to

work of departments as well as job costing

system is beneficial for calculate cost required

for calculation of cost of each job. Generally

this type of system is used in o5rder to control

cost of determine and assigning within the job.

Inventory management system: This system is required in order to interpret

time required for compete demand and supply

of customers which will useful in recognize

inflow as well as outflow of stock. Capital

Joinery implement inventory management

system in order to control and manage 5their

stock management cost and took decision

regarding those policies which will beneficial

in order to determine cost require to manage

and store stock (da Silva, Llewellyn and

Anderson-Gough, 2017).

Cost accounting system: Cost accounting system is required for

assigning and determine cost required for

completion of each business task. By using

marginal and standard cost accounting

manager of Capital Joinery able to decide the

reason of arise difference between standard and

actual on the basis of that they formulate

business policies which help in control

additional cost charged against running

operating business activities.

Price optimization system: This system is required in order to determine

rate of product which organization sell their

products. By using strategies of pricing

work of departments as well as job costing

system is beneficial for calculate cost required

for calculation of cost of each job. Generally

this type of system is used in o5rder to control

cost of determine and assigning within the job.

Inventory management system: This system is required in order to interpret

time required for compete demand and supply

of customers which will useful in recognize

inflow as well as outflow of stock. Capital

Joinery implement inventory management

system in order to control and manage 5their

stock management cost and took decision

regarding those policies which will beneficial

in order to determine cost require to manage

and store stock (da Silva, Llewellyn and

Anderson-Gough, 2017).

Cost accounting system: Cost accounting system is required for

assigning and determine cost required for

completion of each business task. By using

marginal and standard cost accounting

manager of Capital Joinery able to decide the

reason of arise difference between standard and

actual on the basis of that they formulate

business policies which help in control

additional cost charged against running

operating business activities.

Price optimization system: This system is required in order to determine

rate of product which organization sell their

products. By using strategies of pricing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Capital Joinery able to generate profits by

selling their products at high price. They use

price penetration strategy which is beneficial in

attaining their business goals.

TASK 2

P3 Calculation of cost by using management accounting techniques.

Costing techniques: The procedure which help in analysis cost required for running

business activities is known as costing. Business entities have many options in order to recognize

cost of each business transaction (Durocher, Bujaki and Brouard, 2016).

Marginal costing: This technique is useful in calculate cost by determining relation

between profit and variable cost. This technique is also known as variable costing procedure. In

which only variable cost is consider in order to recognize profit and cost required for run

business activities.

marginal costing

Particulars May June

Sales 25000.. 18750..

Less: Variable costs

Sales commission 500.. 375..

Manufacturing cost 2000... 1500..

Direct material 6000.. 4500..

Direct labour 4000.. 3000..

Total cost 12500. 9375..

Contribution 12500. 9375..

Less: Fixed cost

Fixed selling 1000.. 1000..

Fixed production overhead 2000.. 2000..

selling their products at high price. They use

price penetration strategy which is beneficial in

attaining their business goals.

TASK 2

P3 Calculation of cost by using management accounting techniques.

Costing techniques: The procedure which help in analysis cost required for running

business activities is known as costing. Business entities have many options in order to recognize

cost of each business transaction (Durocher, Bujaki and Brouard, 2016).

Marginal costing: This technique is useful in calculate cost by determining relation

between profit and variable cost. This technique is also known as variable costing procedure. In

which only variable cost is consider in order to recognize profit and cost required for run

business activities.

marginal costing

Particulars May June

Sales 25000.. 18750..

Less: Variable costs

Sales commission 500.. 375..

Manufacturing cost 2000... 1500..

Direct material 6000.. 4500..

Direct labour 4000.. 3000..

Total cost 12500. 9375..

Contribution 12500. 9375..

Less: Fixed cost

Fixed selling 1000.. 1000..

Fixed production overhead 2000.. 2000..

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed administration 3000.. 3000..

Net profit 6500. 3375..

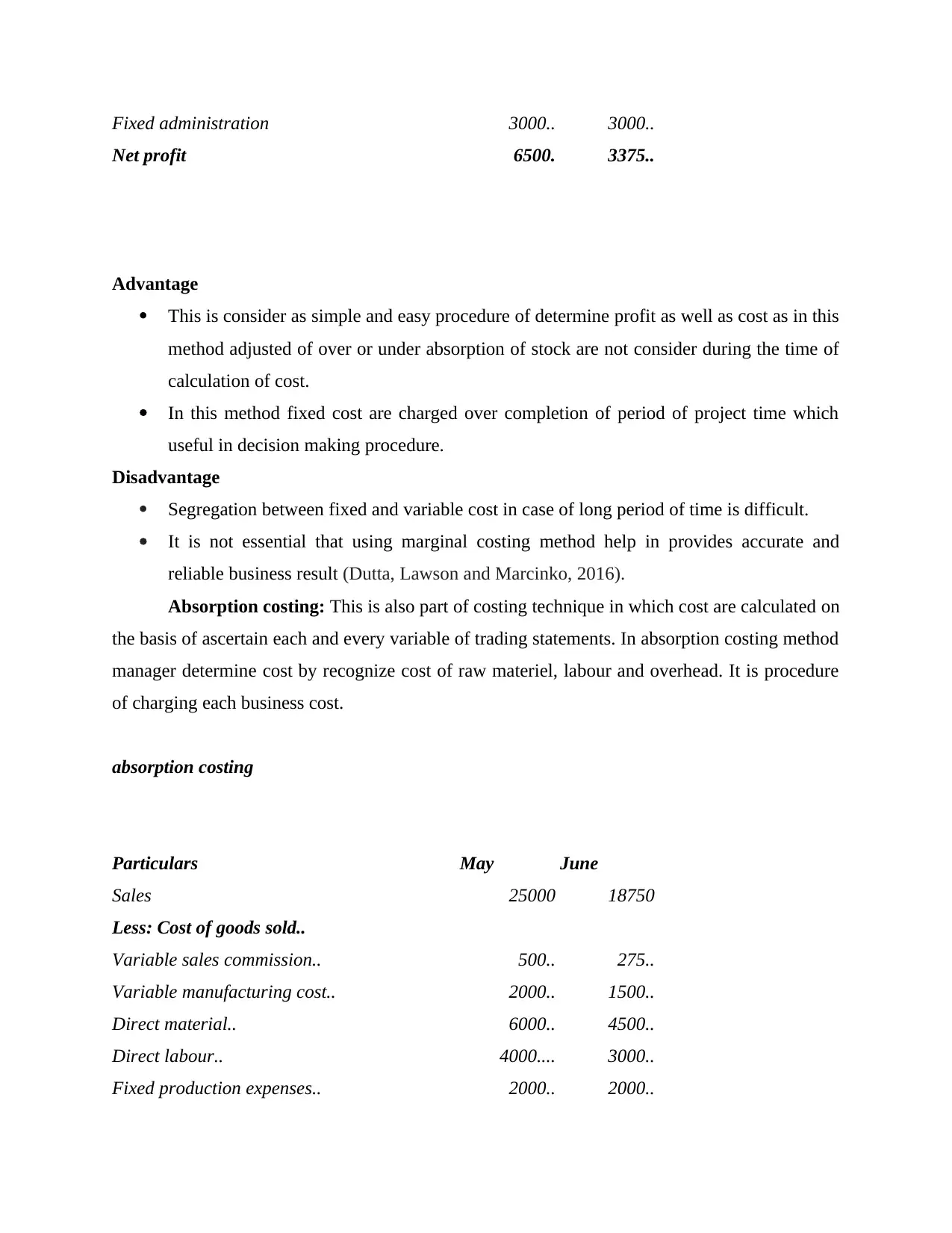

Advantage

This is consider as simple and easy procedure of determine profit as well as cost as in this

method adjusted of over or under absorption of stock are not consider during the time of

calculation of cost.

In this method fixed cost are charged over completion of period of project time which

useful in decision making procedure.

Disadvantage

Segregation between fixed and variable cost in case of long period of time is difficult.

It is not essential that using marginal costing method help in provides accurate and

reliable business result (Dutta, Lawson and Marcinko, 2016).

Absorption costing: This is also part of costing technique in which cost are calculated on

the basis of ascertain each and every variable of trading statements. In absorption costing method

manager determine cost by recognize cost of raw materiel, labour and overhead. It is procedure

of charging each business cost.

absorption costing

Particulars May June

Sales 25000 18750

Less: Cost of goods sold..

Variable sales commission.. 500.. 275..

Variable manufacturing cost.. 2000.. 1500..

Direct material.. 6000.. 4500..

Direct labour.. 4000.... 3000..

Fixed production expenses.. 2000.. 2000..

Net profit 6500. 3375..

Advantage

This is consider as simple and easy procedure of determine profit as well as cost as in this

method adjusted of over or under absorption of stock are not consider during the time of

calculation of cost.

In this method fixed cost are charged over completion of period of project time which

useful in decision making procedure.

Disadvantage

Segregation between fixed and variable cost in case of long period of time is difficult.

It is not essential that using marginal costing method help in provides accurate and

reliable business result (Dutta, Lawson and Marcinko, 2016).

Absorption costing: This is also part of costing technique in which cost are calculated on

the basis of ascertain each and every variable of trading statements. In absorption costing method

manager determine cost by recognize cost of raw materiel, labour and overhead. It is procedure

of charging each business cost.

absorption costing

Particulars May June

Sales 25000 18750

Less: Cost of goods sold..

Variable sales commission.. 500.. 275..

Variable manufacturing cost.. 2000.. 1500..

Direct material.. 6000.. 4500..

Direct labour.. 4000.... 3000..

Fixed production expenses.. 2000.. 2000..

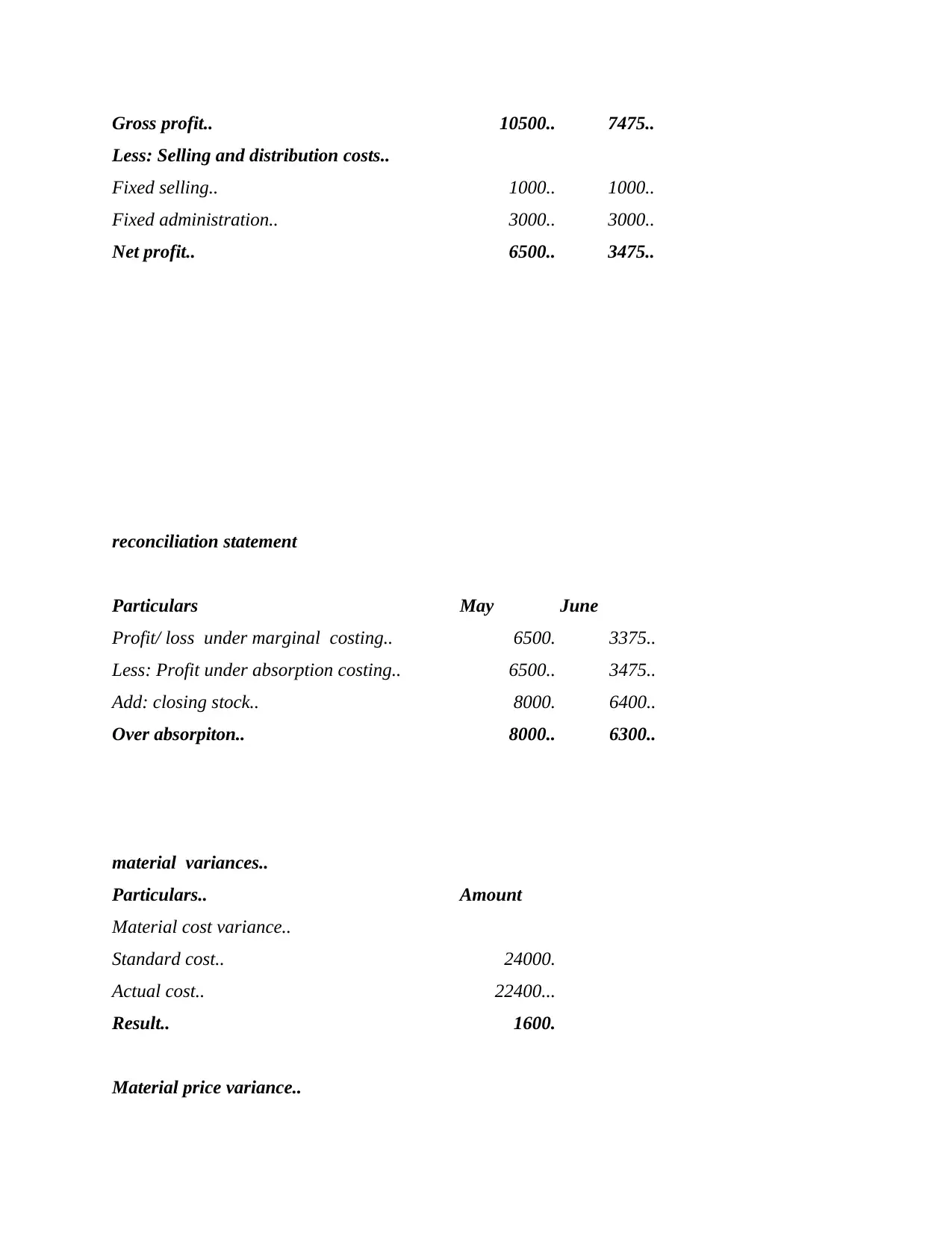

Gross profit.. 10500.. 7475..

Less: Selling and distribution costs..

Fixed selling.. 1000.. 1000..

Fixed administration.. 3000.. 3000..

Net profit.. 6500.. 3475..

reconciliation statement

Particulars May June

Profit/ loss under marginal costing.. 6500. 3375..

Less: Profit under absorption costing.. 6500.. 3475..

Add: closing stock.. 8000. 6400..

Over absorpiton.. 8000.. 6300..

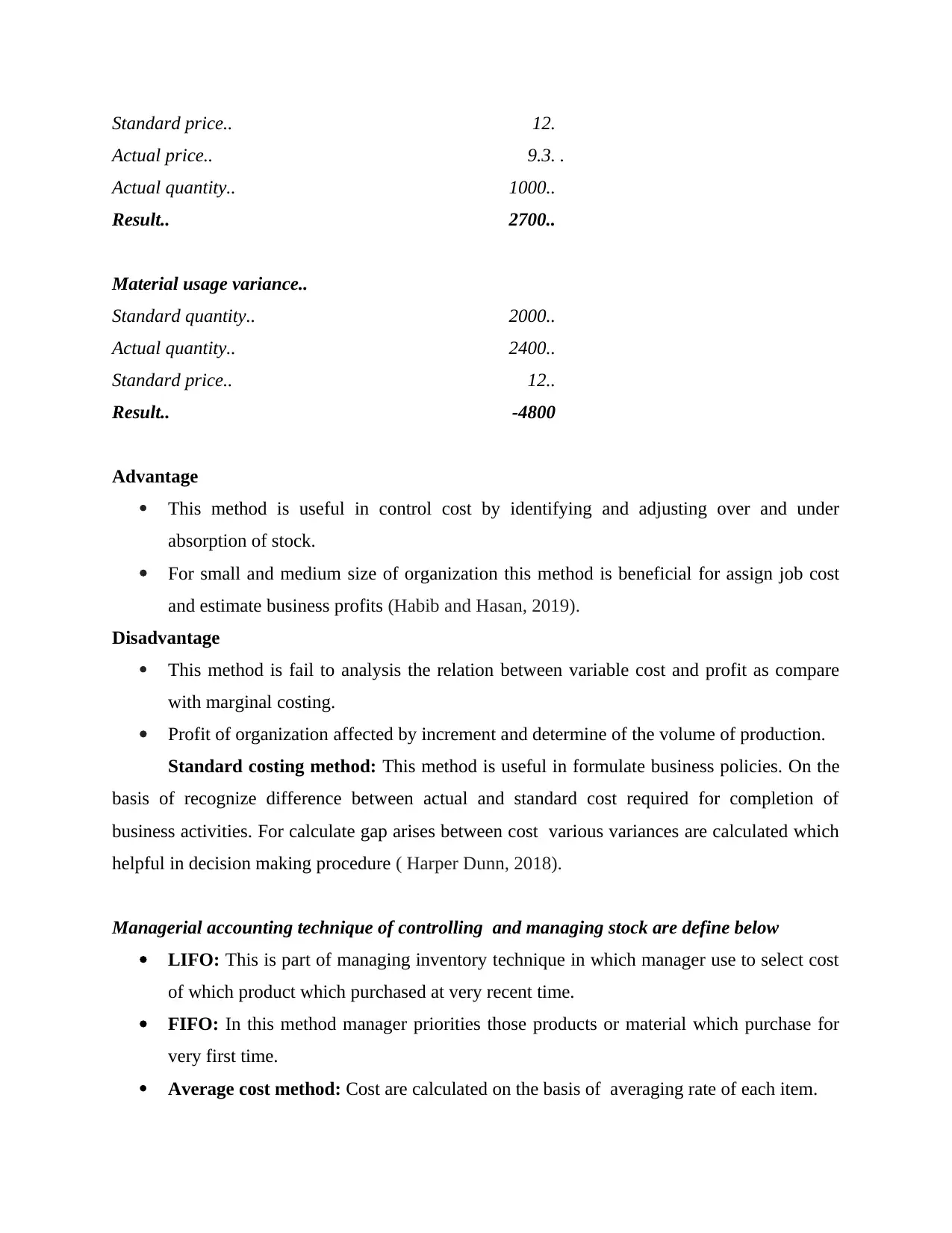

material variances..

Particulars.. Amount

Material cost variance..

Standard cost.. 24000.

Actual cost.. 22400...

Result.. 1600.

Material price variance..

Less: Selling and distribution costs..

Fixed selling.. 1000.. 1000..

Fixed administration.. 3000.. 3000..

Net profit.. 6500.. 3475..

reconciliation statement

Particulars May June

Profit/ loss under marginal costing.. 6500. 3375..

Less: Profit under absorption costing.. 6500.. 3475..

Add: closing stock.. 8000. 6400..

Over absorpiton.. 8000.. 6300..

material variances..

Particulars.. Amount

Material cost variance..

Standard cost.. 24000.

Actual cost.. 22400...

Result.. 1600.

Material price variance..

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Standard price.. 12.

Actual price.. 9.3. .

Actual quantity.. 1000..

Result.. 2700..

Material usage variance..

Standard quantity.. 2000..

Actual quantity.. 2400..

Standard price.. 12..

Result.. -4800

Advantage

This method is useful in control cost by identifying and adjusting over and under

absorption of stock.

For small and medium size of organization this method is beneficial for assign job cost

and estimate business profits (Habib and Hasan, 2019).

Disadvantage

This method is fail to analysis the relation between variable cost and profit as compare

with marginal costing.

Profit of organization affected by increment and determine of the volume of production.

Standard costing method: This method is useful in formulate business policies. On the

basis of recognize difference between actual and standard cost required for completion of

business activities. For calculate gap arises between cost various variances are calculated which

helpful in decision making procedure ( Harper Dunn, 2018).

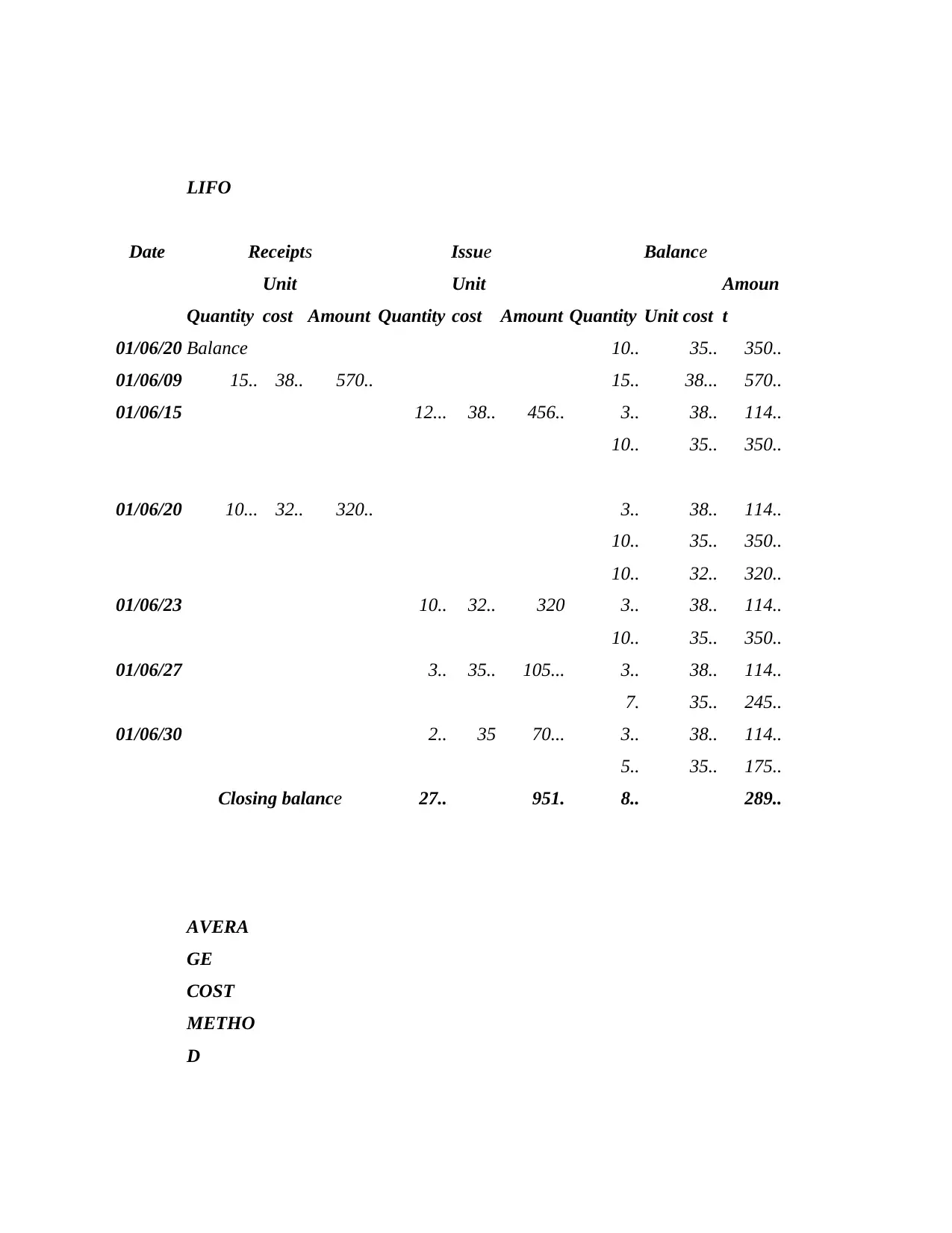

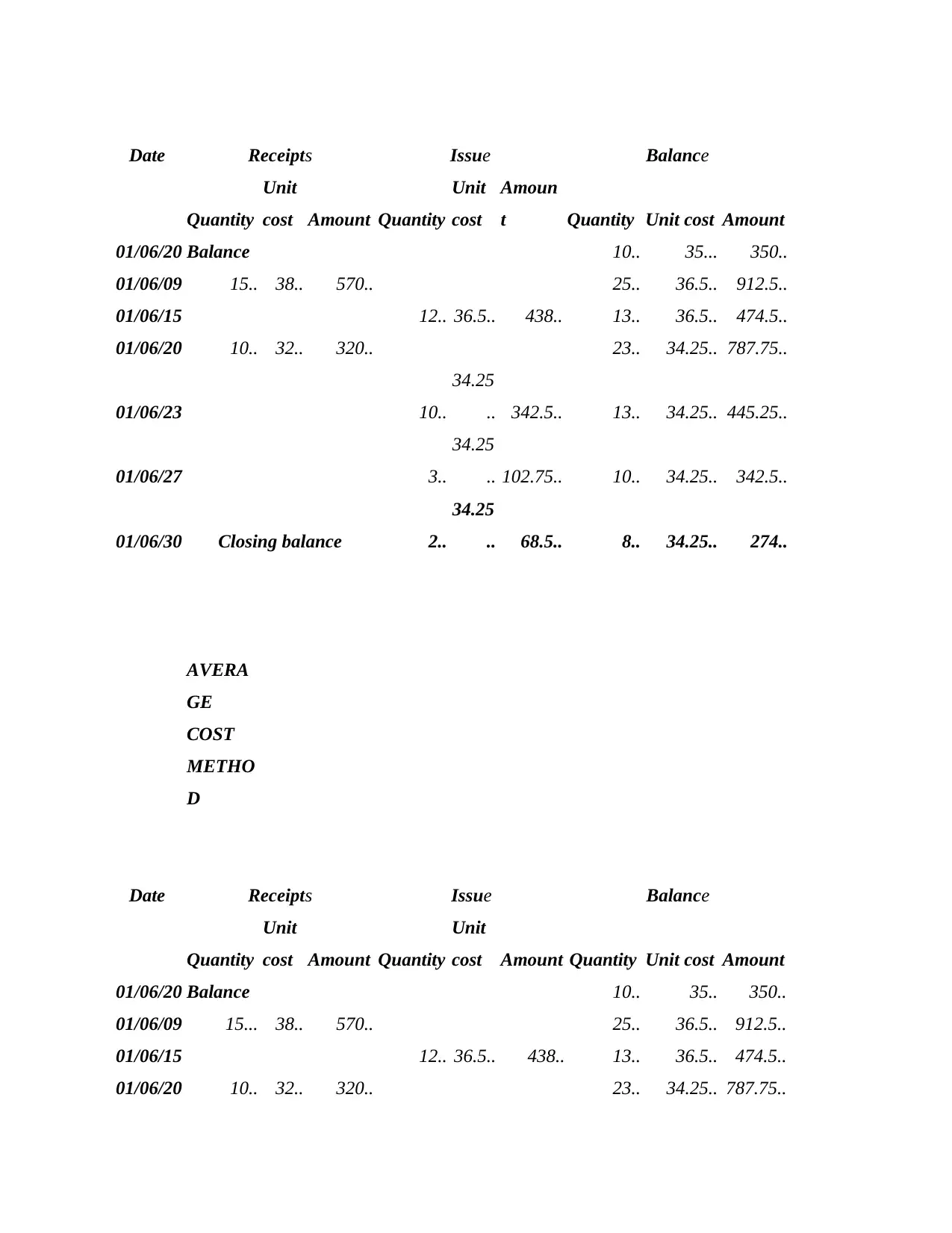

Managerial accounting technique of controlling and managing stock are define below

LIFO: This is part of managing inventory technique in which manager use to select cost

of which product which purchased at very recent time.

FIFO: In this method manager priorities those products or material which purchase for

very first time.

Average cost method: Cost are calculated on the basis of averaging rate of each item.

Actual price.. 9.3. .

Actual quantity.. 1000..

Result.. 2700..

Material usage variance..

Standard quantity.. 2000..

Actual quantity.. 2400..

Standard price.. 12..

Result.. -4800

Advantage

This method is useful in control cost by identifying and adjusting over and under

absorption of stock.

For small and medium size of organization this method is beneficial for assign job cost

and estimate business profits (Habib and Hasan, 2019).

Disadvantage

This method is fail to analysis the relation between variable cost and profit as compare

with marginal costing.

Profit of organization affected by increment and determine of the volume of production.

Standard costing method: This method is useful in formulate business policies. On the

basis of recognize difference between actual and standard cost required for completion of

business activities. For calculate gap arises between cost various variances are calculated which

helpful in decision making procedure ( Harper Dunn, 2018).

Managerial accounting technique of controlling and managing stock are define below

LIFO: This is part of managing inventory technique in which manager use to select cost

of which product which purchased at very recent time.

FIFO: In this method manager priorities those products or material which purchase for

very first time.

Average cost method: Cost are calculated on the basis of averaging rate of each item.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LIFO

Date Receipts Issue Balance

Quantity

Unit

cost Amount Quantity

Unit

cost Amount Quantity Unit cost

Amoun

t

01/06/20 Balance 10.. 35.. 350..

01/06/09 15.. 38.. 570.. 15.. 38... 570..

01/06/15 12... 38.. 456.. 3.. 38.. 114..

10.. 35.. 350..

01/06/20 10... 32.. 320.. 3.. 38.. 114..

10.. 35.. 350..

10.. 32.. 320..

01/06/23 10.. 32.. 320 3.. 38.. 114..

10.. 35.. 350..

01/06/27 3.. 35.. 105... 3.. 38.. 114..

7. 35.. 245..

01/06/30 2.. 35 70... 3.. 38.. 114..

5.. 35.. 175..

Closing balance 27.. 951. 8.. 289..

AVERA

GE

COST

METHO

D

Date Receipts Issue Balance

Quantity

Unit

cost Amount Quantity

Unit

cost Amount Quantity Unit cost

Amoun

t

01/06/20 Balance 10.. 35.. 350..

01/06/09 15.. 38.. 570.. 15.. 38... 570..

01/06/15 12... 38.. 456.. 3.. 38.. 114..

10.. 35.. 350..

01/06/20 10... 32.. 320.. 3.. 38.. 114..

10.. 35.. 350..

10.. 32.. 320..

01/06/23 10.. 32.. 320 3.. 38.. 114..

10.. 35.. 350..

01/06/27 3.. 35.. 105... 3.. 38.. 114..

7. 35.. 245..

01/06/30 2.. 35 70... 3.. 38.. 114..

5.. 35.. 175..

Closing balance 27.. 951. 8.. 289..

AVERA

GE

COST

METHO

D

Date Receipts Issue Balance

Quantity

Unit

cost Amount Quantity

Unit

cost

Amoun

t Quantity Unit cost Amount

01/06/20 Balance 10.. 35... 350..

01/06/09 15.. 38.. 570.. 25.. 36.5.. 912.5..

01/06/15 12.. 36.5.. 438.. 13.. 36.5.. 474.5..

01/06/20 10.. 32.. 320.. 23.. 34.25.. 787.75..

01/06/23 10..

34.25

.. 342.5.. 13.. 34.25.. 445.25..

01/06/27 3..

34.25

.. 102.75.. 10.. 34.25.. 342.5..

01/06/30 Closing balance 2..

34.25

.. 68.5.. 8.. 34.25.. 274..

AVERA

GE

COST

METHO

D

Date Receipts Issue Balance

Quantity

Unit

cost Amount Quantity

Unit

cost Amount Quantity Unit cost Amount

01/06/20 Balance 10.. 35.. 350..

01/06/09 15... 38.. 570.. 25.. 36.5.. 912.5..

01/06/15 12.. 36.5.. 438.. 13.. 36.5.. 474.5..

01/06/20 10.. 32.. 320.. 23.. 34.25.. 787.75..

Quantity

Unit

cost Amount Quantity

Unit

cost

Amoun

t Quantity Unit cost Amount

01/06/20 Balance 10.. 35... 350..

01/06/09 15.. 38.. 570.. 25.. 36.5.. 912.5..

01/06/15 12.. 36.5.. 438.. 13.. 36.5.. 474.5..

01/06/20 10.. 32.. 320.. 23.. 34.25.. 787.75..

01/06/23 10..

34.25

.. 342.5.. 13.. 34.25.. 445.25..

01/06/27 3..

34.25

.. 102.75.. 10.. 34.25.. 342.5..

01/06/30 Closing balance 2..

34.25

.. 68.5.. 8.. 34.25.. 274..

AVERA

GE

COST

METHO

D

Date Receipts Issue Balance

Quantity

Unit

cost Amount Quantity

Unit

cost Amount Quantity Unit cost Amount

01/06/20 Balance 10.. 35.. 350..

01/06/09 15... 38.. 570.. 25.. 36.5.. 912.5..

01/06/15 12.. 36.5.. 438.. 13.. 36.5.. 474.5..

01/06/20 10.. 32.. 320.. 23.. 34.25.. 787.75..

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.