Management Accounting Report: BTEC Unit 5, 2019/20, Finance

VerifiedAdded on 2023/01/10

|18

|4899

|40

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and techniques. It begins with an introduction to management accounting, its essential requirements, and the various systems used for decision-making, including price optimization, cost accounting, inventory management, and job costing. The report then examines different management accounting reports such as inventory management, accounts receivable, and performance reports, evaluating their benefits and the integration of these systems within an organizational process. The core of the report focuses on cost analysis, comparing and contrasting marginal and absorption costing methods for preparing income statements, along with an interpretation of the data. Furthermore, the report explores various planning tools used for budgetary control, analyzing their advantages and applications in preparing and forecasting budgets. Finally, the report addresses the adoption of management accounting systems to respond to financial problems and discusses the contribution of management accounting in achieving the sustainable success of an organization. The report uses Innocent Drinks as a case study to illustrate the practical application of these concepts.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1............................................................................................................................................3

Management accounting and essential requirements of management accounting systems...3

Management Accounting Reports:.........................................................................................5

Evaluation of benefits of explained MA systems:..................................................................6

Integration of management accounting system and report within organisational process:....6

TASK 2............................................................................................................................................7

Usage of the techniques of cost analysis to prepare income statement by using marginal and

absorption costing...................................................................................................................7

Accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents:...............................................................................................7

Interpretation of above data:...................................................................................................7

TASK 3............................................................................................................................................8

P4 Advantages of different planning tools used for budgetary control..................................8

Analyse the use of different planning tools and their application for preparing and forecasting

budgets ..................................................................................................................................9

TASK 4..........................................................................................................................................10

Adoption of management accounting systems to respond financial problems ...................10

Contribution of management accounting in sustainable success of the organisation while

responding financial problems.............................................................................................10

Application of planning tools to respond financial issue along with attainment of sustainable

success .................................................................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1............................................................................................................................................3

Management accounting and essential requirements of management accounting systems...3

Management Accounting Reports:.........................................................................................5

Evaluation of benefits of explained MA systems:..................................................................6

Integration of management accounting system and report within organisational process:....6

TASK 2............................................................................................................................................7

Usage of the techniques of cost analysis to prepare income statement by using marginal and

absorption costing...................................................................................................................7

Accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents:...............................................................................................7

Interpretation of above data:...................................................................................................7

TASK 3............................................................................................................................................8

P4 Advantages of different planning tools used for budgetary control..................................8

Analyse the use of different planning tools and their application for preparing and forecasting

budgets ..................................................................................................................................9

TASK 4..........................................................................................................................................10

Adoption of management accounting systems to respond financial problems ...................10

Contribution of management accounting in sustainable success of the organisation while

responding financial problems.............................................................................................10

Application of planning tools to respond financial issue along with attainment of sustainable

success .................................................................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Management accounting regards to term that involves an evaluation of inner management

enterprise practices that enable efficacious decision - making. This generally include the use of

accounting guidelines to establish finance and qualitative information that further assist in the

effectual controlling of entity's functions resulting in the achievement of objectives within a

set time-frame. This generally also classify as the cost-accounting which helps to assess

operating expenses and further assist in the compilation of annual results and represent the

operation of the organizational units of the corporation (DRURY, 2013). The study report

consists of comprehensive discussion about various elements of managerial accounting in

context of Innocent Drinks which is a corporation that produces smoothies and drinks offered in

supermarket chains, coffee houses as well as other stores. The corporation sells around above

two million of smoothies per week.

The study discusses the theory of managerial accounting and the basic requirements of

its various systems, the specific management accounting reporting approaches and the use of

acceptable cost analysis approaches in the preparing of marginal vs absorption costing income

statements. The study also goes on to discuss the benefits and shortcomings of multiple planning

tools within the context of budgetary controlling and application to MA systems for making

respond to various fiscal issues.

MAIN BODY

TASK 1

Management accounting and essential requirements of management accounting systems

Introduction: The managerial accounting involves the formulation of several types of

framework that help to maximise the performance enterprise and produce relevant

information for decision-making. The various systems that are configured in MA

mechanism are namely cost accounting, inventory management, job costing, price

optimisation etc. With the systematic implementation of MA mechanism and its frameworks, the

company needs to reinforce decision-making in order to produce predefined performance.

Management Accounting: This pertains to the approach of determining, recognizing,

interpreting, presenting and sharing financial reports in the fulfilment of targets of the entity.

These are often referring as the cost accounting (Management Accounting. 2018). Here ' key

Management accounting regards to term that involves an evaluation of inner management

enterprise practices that enable efficacious decision - making. This generally include the use of

accounting guidelines to establish finance and qualitative information that further assist in the

effectual controlling of entity's functions resulting in the achievement of objectives within a

set time-frame. This generally also classify as the cost-accounting which helps to assess

operating expenses and further assist in the compilation of annual results and represent the

operation of the organizational units of the corporation (DRURY, 2013). The study report

consists of comprehensive discussion about various elements of managerial accounting in

context of Innocent Drinks which is a corporation that produces smoothies and drinks offered in

supermarket chains, coffee houses as well as other stores. The corporation sells around above

two million of smoothies per week.

The study discusses the theory of managerial accounting and the basic requirements of

its various systems, the specific management accounting reporting approaches and the use of

acceptable cost analysis approaches in the preparing of marginal vs absorption costing income

statements. The study also goes on to discuss the benefits and shortcomings of multiple planning

tools within the context of budgetary controlling and application to MA systems for making

respond to various fiscal issues.

MAIN BODY

TASK 1

Management accounting and essential requirements of management accounting systems

Introduction: The managerial accounting involves the formulation of several types of

framework that help to maximise the performance enterprise and produce relevant

information for decision-making. The various systems that are configured in MA

mechanism are namely cost accounting, inventory management, job costing, price

optimisation etc. With the systematic implementation of MA mechanism and its frameworks, the

company needs to reinforce decision-making in order to produce predefined performance.

Management Accounting: This pertains to the approach of determining, recognizing,

interpreting, presenting and sharing financial reports in the fulfilment of targets of the entity.

These are often referring as the cost accounting (Management Accounting. 2018). Here ' key

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

distinction among financial accounting vs management accounting is management accounting

information is meant to allow administrators in an entity to making decisions, while financial

accounting designed to provide information to the entity's external stakeholders in an enterprise.

Management accounting systems: They are the mechanisms that the managerial

personnel use to collect statistics about the true operating capability of the various divisions of

the corporation. The various types of systems that are usually designed by upper management of

the company involve cost accounting, , stock management, job-costing system, price-

optimisation system etc. The core role that management of the entity seeks to execute by an

overview of the knowledge collected from the various accounts comprises planning,

coordination, monitoring and managerial decision-making (Chiu, Teoh and Tian, 2012). Here

below are certain systems which Innocent Drinks can apply, discussed below:

Price-optimisation System: Generally, a corporate entity's price optimization system is

being used to address the pricing models of the related goods along with approaches to

statistical analysis. With the implementation of such pricing measures in Innocent Drinks,

decision-makers of a corporate organization can effectively determine their current price

plans for products in line with new marketing scenarios. By applying this price-

optimisation system, company would be capable to develop major growth plans to

increase the existing level of income together with the fulfilment of the related

organisational goals.

Cost accounting system: This another significant system which considerably used in

case of Innocent Drinks in attempt to recognise and quantity aggregate production costs

incurred with assistance of thorough evaluation of multiple costs accrued towards each

stage in production of final product. This system require a controlled classification of

costs and allocation of costs to different aspects of organisation (Eierle and Schultze,

2013).

Inventory management system: This is most efficacious system which reduce the

managerial efforts towards management of wide array of inventories. This system require

detailed information and reports of multiple inventories including relevant classification

of each single inventory item. This system primarily offers assistive frameworks for

managing and handling of inventories. This facilitates managing officials with actual

information is meant to allow administrators in an entity to making decisions, while financial

accounting designed to provide information to the entity's external stakeholders in an enterprise.

Management accounting systems: They are the mechanisms that the managerial

personnel use to collect statistics about the true operating capability of the various divisions of

the corporation. The various types of systems that are usually designed by upper management of

the company involve cost accounting, , stock management, job-costing system, price-

optimisation system etc. The core role that management of the entity seeks to execute by an

overview of the knowledge collected from the various accounts comprises planning,

coordination, monitoring and managerial decision-making (Chiu, Teoh and Tian, 2012). Here

below are certain systems which Innocent Drinks can apply, discussed below:

Price-optimisation System: Generally, a corporate entity's price optimization system is

being used to address the pricing models of the related goods along with approaches to

statistical analysis. With the implementation of such pricing measures in Innocent Drinks,

decision-makers of a corporate organization can effectively determine their current price

plans for products in line with new marketing scenarios. By applying this price-

optimisation system, company would be capable to develop major growth plans to

increase the existing level of income together with the fulfilment of the related

organisational goals.

Cost accounting system: This another significant system which considerably used in

case of Innocent Drinks in attempt to recognise and quantity aggregate production costs

incurred with assistance of thorough evaluation of multiple costs accrued towards each

stage in production of final product. This system require a controlled classification of

costs and allocation of costs to different aspects of organisation (Eierle and Schultze,

2013).

Inventory management system: This is most efficacious system which reduce the

managerial efforts towards management of wide array of inventories. This system require

detailed information and reports of multiple inventories including relevant classification

of each single inventory item. This system primarily offers assistive frameworks for

managing and handling of inventories. This facilitates managing officials with actual

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

real-time tracking and monitoring of inventories. In Innocent Drinks, management can

apply this system to optimise inventories costs and in effective handling of inventories.

Job costing system: This MA framework allow management to effectively define all the

jobs within a manufacturing concern like Innocent Drink to specify specific jobs process

and then efficacious allocation of total costs incurred by entity to each defined job. This

system requires a reporting of all jobs along with details of costs incurred on different

jobs. This facilitates effective accountability within business entity's functions.

Essential requirements of Management Accounting systems:

Relevance- Knowledge is important to one and everyone. Financial management examines the

best instruments available with information relating to the action being taken, the choice and the

judgement method being used. By coming to terms with the requirements of shareholders, a most

important and valuable material for judgement is determined, compiled, and arranged for

assessment.

Value- The effects on valuation is forecast. Financial reporting administration relates the

company's practises to its underlying business strategy, which provides an in-depth view of the

broader macroeconomic situation. It entails assessing information along the course of value

development, estimating potential expectations, and reflecting on prices, investments, and the

possibility of opportunities for value generation.

Credibility- authority forms stewardship. Accountability and transparency help in making the

decision process much more purposeful. Trust and prosperity are improved by matching near-

term business priorities with long-term shareholder value. Strategy formulation professionals are

known to be legal, responsible, and aware of the company's principles, political needs, and

relational obligations.

Difference in management accounting and financial accounting:

Basis Management accounting Financial accounting

Necessary This accounting is not necessary for

businesses to carry out their

activities.

Though financial accounting is

important for businesses to enforce it.

Informatio

n

Such accounting contains economic

and non material.

In the other hand, only financial details

are used inside those accounts.

Rules and There is no clear role or legislation There are various kinds of laws and

apply this system to optimise inventories costs and in effective handling of inventories.

Job costing system: This MA framework allow management to effectively define all the

jobs within a manufacturing concern like Innocent Drink to specify specific jobs process

and then efficacious allocation of total costs incurred by entity to each defined job. This

system requires a reporting of all jobs along with details of costs incurred on different

jobs. This facilitates effective accountability within business entity's functions.

Essential requirements of Management Accounting systems:

Relevance- Knowledge is important to one and everyone. Financial management examines the

best instruments available with information relating to the action being taken, the choice and the

judgement method being used. By coming to terms with the requirements of shareholders, a most

important and valuable material for judgement is determined, compiled, and arranged for

assessment.

Value- The effects on valuation is forecast. Financial reporting administration relates the

company's practises to its underlying business strategy, which provides an in-depth view of the

broader macroeconomic situation. It entails assessing information along the course of value

development, estimating potential expectations, and reflecting on prices, investments, and the

possibility of opportunities for value generation.

Credibility- authority forms stewardship. Accountability and transparency help in making the

decision process much more purposeful. Trust and prosperity are improved by matching near-

term business priorities with long-term shareholder value. Strategy formulation professionals are

known to be legal, responsible, and aware of the company's principles, political needs, and

relational obligations.

Difference in management accounting and financial accounting:

Basis Management accounting Financial accounting

Necessary This accounting is not necessary for

businesses to carry out their

activities.

Though financial accounting is

important for businesses to enforce it.

Informatio

n

Such accounting contains economic

and non material.

In the other hand, only financial details

are used inside those accounts.

Rules and There is no clear role or legislation There are various kinds of laws and

regulation for the preparing of internal reporting

in this accounting.

legislation that need to be enforced in

this accounting process.

Outcome Internal plans are published under

this accounting as business needs are

prepared.

Financial records and documents are

drawn out in these accounts at the close

of the accounting year.

Management Accounting Reports:

Management Accounting Reports corresponds to a document that incorporates details

from processes examined about individual departments operations. This section discusses

numerous MA reports and their relevancies for Innocent Plc, as follows:

Inventory management report: It is kind of report that incorporates details regarding

inventory management. The central aim of such report is to strike an equilibrium between stock

expenditure and quality controls. This report would offer details to Innocent Drinks mostly on

quantity of materials which they have to prepare juices and smoothies at a specific time. The key

advantage of such a report to company is that it maintains certain level of stocks and raw

materials and has controls over excessive costs and expenditures that ultimately result

in enhancing of profit margins.

Accounts receivable report: As name revels this kind of report is primarily based on

reporting of balance of all the trade debtors. This is report that offers details on outstanding

customer invoices and outstanding accounts receivable by dates. Such a report is being used by

the Innocent Drinks to evaluate the late payments of their specific customers or debtors.

Furthermore, report also helps to look at credit term granted to them all and to assess how often

time has elapsed where payment is outstanding to these customers or trade debtors. The purpose

of such report is dictated by the actuality that this allow to tighten payment practices and retrieve

their due sum within timeline that results in company being financially stable (Granlund and

Lukka, 2017).

Performance report: This report contains details on results of something. This report

can be considered by the administration of the Innocent Drinks to assess real performance of

their staff and the progress of the respective units that are willing or unable to meet their

in this accounting.

legislation that need to be enforced in

this accounting process.

Outcome Internal plans are published under

this accounting as business needs are

prepared.

Financial records and documents are

drawn out in these accounts at the close

of the accounting year.

Management Accounting Reports:

Management Accounting Reports corresponds to a document that incorporates details

from processes examined about individual departments operations. This section discusses

numerous MA reports and their relevancies for Innocent Plc, as follows:

Inventory management report: It is kind of report that incorporates details regarding

inventory management. The central aim of such report is to strike an equilibrium between stock

expenditure and quality controls. This report would offer details to Innocent Drinks mostly on

quantity of materials which they have to prepare juices and smoothies at a specific time. The key

advantage of such a report to company is that it maintains certain level of stocks and raw

materials and has controls over excessive costs and expenditures that ultimately result

in enhancing of profit margins.

Accounts receivable report: As name revels this kind of report is primarily based on

reporting of balance of all the trade debtors. This is report that offers details on outstanding

customer invoices and outstanding accounts receivable by dates. Such a report is being used by

the Innocent Drinks to evaluate the late payments of their specific customers or debtors.

Furthermore, report also helps to look at credit term granted to them all and to assess how often

time has elapsed where payment is outstanding to these customers or trade debtors. The purpose

of such report is dictated by the actuality that this allow to tighten payment practices and retrieve

their due sum within timeline that results in company being financially stable (Granlund and

Lukka, 2017).

Performance report: This report contains details on results of something. This report

can be considered by the administration of the Innocent Drinks to assess real performance of

their staff and the progress of the respective units that are willing or unable to meet their

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

intended goals from their actual overall performance enterprise. The key advantage linked with

that same report is to assess the output deviation from the expectations and to take effective

corrective action. This intervention makes it possible to enhance the efficiency and

accomplishment of the goal.

Evaluation of benefits of explained MA systems:

Cost accounting system: In Innocent Plc this system would beneficial in assessing the

actual costs incurred in producing final product as well as to allocate areas accountable

for increasing costs.

Inventory management system: In Innocent Plc this is advantageous to adopt as it

enable management officials to minimise the overall inventories costs like warehousing,

storage, managing and handling etc.

Price optimisation system: It facilitate advantage of setting efficacious and productive

prices for its different products as well as to maintain profitability level.

Job costing system: This frameworks would be beneficial for Innocent Plc to place

accountability within the different job processes of organisation and assigning costs to

jobs to support quick decision-making (Ittner, 2014).

Integration of management accounting system and report within organisational process:

Corporate entities like Innocent Plc have numerous procedures, and that each procedure

has distinct task assigned to various individuals. As a consequence, the monitoring and control of

all procedures and operations is a complicated thing, hence it is important to

integrate different systems with organizational processes. This alignment allows managing staff

to keep track of every process as well as to coordinate processes in an organised way. As in Next

plc, various procedures related to inventory sorting, tracking, storage, loading etc. are

incorporated into inventory management framework, wherein every production supervisor is

responsible for monitoring and presenting all minor and main inventory information to top

executives in a structured manner. This encourage the key stakeholders of the entities to

completely match their preferences with the organization's policies in order to add economic

output within their work (Lääts and Haldma, 2012).

that same report is to assess the output deviation from the expectations and to take effective

corrective action. This intervention makes it possible to enhance the efficiency and

accomplishment of the goal.

Evaluation of benefits of explained MA systems:

Cost accounting system: In Innocent Plc this system would beneficial in assessing the

actual costs incurred in producing final product as well as to allocate areas accountable

for increasing costs.

Inventory management system: In Innocent Plc this is advantageous to adopt as it

enable management officials to minimise the overall inventories costs like warehousing,

storage, managing and handling etc.

Price optimisation system: It facilitate advantage of setting efficacious and productive

prices for its different products as well as to maintain profitability level.

Job costing system: This frameworks would be beneficial for Innocent Plc to place

accountability within the different job processes of organisation and assigning costs to

jobs to support quick decision-making (Ittner, 2014).

Integration of management accounting system and report within organisational process:

Corporate entities like Innocent Plc have numerous procedures, and that each procedure

has distinct task assigned to various individuals. As a consequence, the monitoring and control of

all procedures and operations is a complicated thing, hence it is important to

integrate different systems with organizational processes. This alignment allows managing staff

to keep track of every process as well as to coordinate processes in an organised way. As in Next

plc, various procedures related to inventory sorting, tracking, storage, loading etc. are

incorporated into inventory management framework, wherein every production supervisor is

responsible for monitoring and presenting all minor and main inventory information to top

executives in a structured manner. This encourage the key stakeholders of the entities to

completely match their preferences with the organization's policies in order to add economic

output within their work (Lääts and Haldma, 2012).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

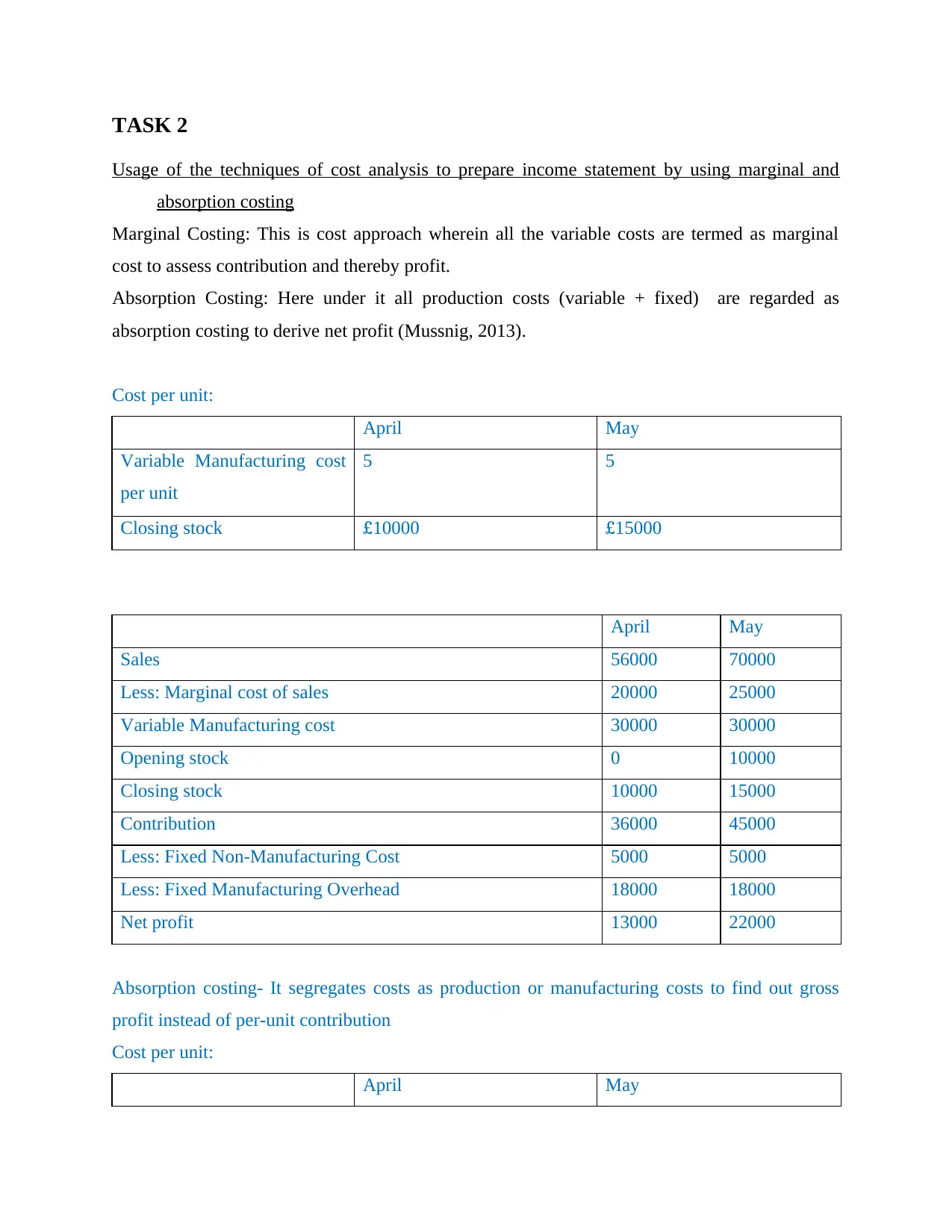

TASK 2

Usage of the techniques of cost analysis to prepare income statement by using marginal and

absorption costing

Marginal Costing: This is cost approach wherein all the variable costs are termed as marginal

cost to assess contribution and thereby profit.

Absorption Costing: Here under it all production costs (variable + fixed) are regarded as

absorption costing to derive net profit (Mussnig, 2013).

Cost per unit:

April May

Variable Manufacturing cost

per unit

5 5

Closing stock £10000 £15000

April May

Sales 56000 70000

Less: Marginal cost of sales 20000 25000

Variable Manufacturing cost 30000 30000

Opening stock 0 10000

Closing stock 10000 15000

Contribution 36000 45000

Less: Fixed Non-Manufacturing Cost 5000 5000

Less: Fixed Manufacturing Overhead 18000 18000

Net profit 13000 22000

Absorption costing- It segregates costs as production or manufacturing costs to find out gross

profit instead of per-unit contribution

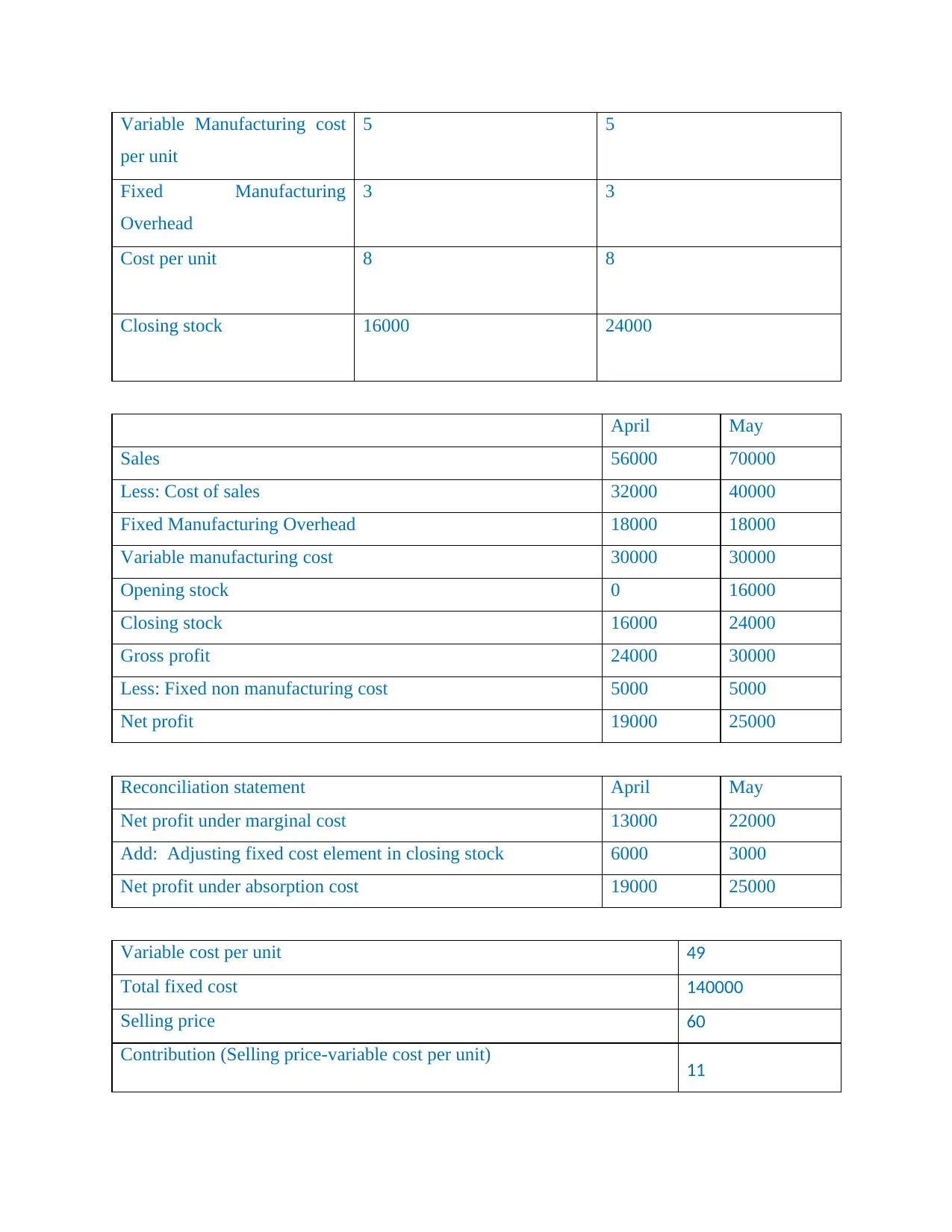

Cost per unit:

April May

Usage of the techniques of cost analysis to prepare income statement by using marginal and

absorption costing

Marginal Costing: This is cost approach wherein all the variable costs are termed as marginal

cost to assess contribution and thereby profit.

Absorption Costing: Here under it all production costs (variable + fixed) are regarded as

absorption costing to derive net profit (Mussnig, 2013).

Cost per unit:

April May

Variable Manufacturing cost

per unit

5 5

Closing stock £10000 £15000

April May

Sales 56000 70000

Less: Marginal cost of sales 20000 25000

Variable Manufacturing cost 30000 30000

Opening stock 0 10000

Closing stock 10000 15000

Contribution 36000 45000

Less: Fixed Non-Manufacturing Cost 5000 5000

Less: Fixed Manufacturing Overhead 18000 18000

Net profit 13000 22000

Absorption costing- It segregates costs as production or manufacturing costs to find out gross

profit instead of per-unit contribution

Cost per unit:

April May

Variable Manufacturing cost

per unit

5 5

Fixed Manufacturing

Overhead

3 3

Cost per unit 8 8

Closing stock 16000 24000

April May

Sales 56000 70000

Less: Cost of sales 32000 40000

Fixed Manufacturing Overhead 18000 18000

Variable manufacturing cost 30000 30000

Opening stock 0 16000

Closing stock 16000 24000

Gross profit 24000 30000

Less: Fixed non manufacturing cost 5000 5000

Net profit 19000 25000

Reconciliation statement April May

Net profit under marginal cost 13000 22000

Add: Adjusting fixed cost element in closing stock 6000 3000

Net profit under absorption cost 19000 25000

Variable cost per unit 49

Total fixed cost 140000

Selling price 60

Contribution (Selling price-variable cost per unit) 11

per unit

5 5

Fixed Manufacturing

Overhead

3 3

Cost per unit 8 8

Closing stock 16000 24000

April May

Sales 56000 70000

Less: Cost of sales 32000 40000

Fixed Manufacturing Overhead 18000 18000

Variable manufacturing cost 30000 30000

Opening stock 0 16000

Closing stock 16000 24000

Gross profit 24000 30000

Less: Fixed non manufacturing cost 5000 5000

Net profit 19000 25000

Reconciliation statement April May

Net profit under marginal cost 13000 22000

Add: Adjusting fixed cost element in closing stock 6000 3000

Net profit under absorption cost 19000 25000

Variable cost per unit 49

Total fixed cost 140000

Selling price 60

Contribution (Selling price-variable cost per unit) 11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

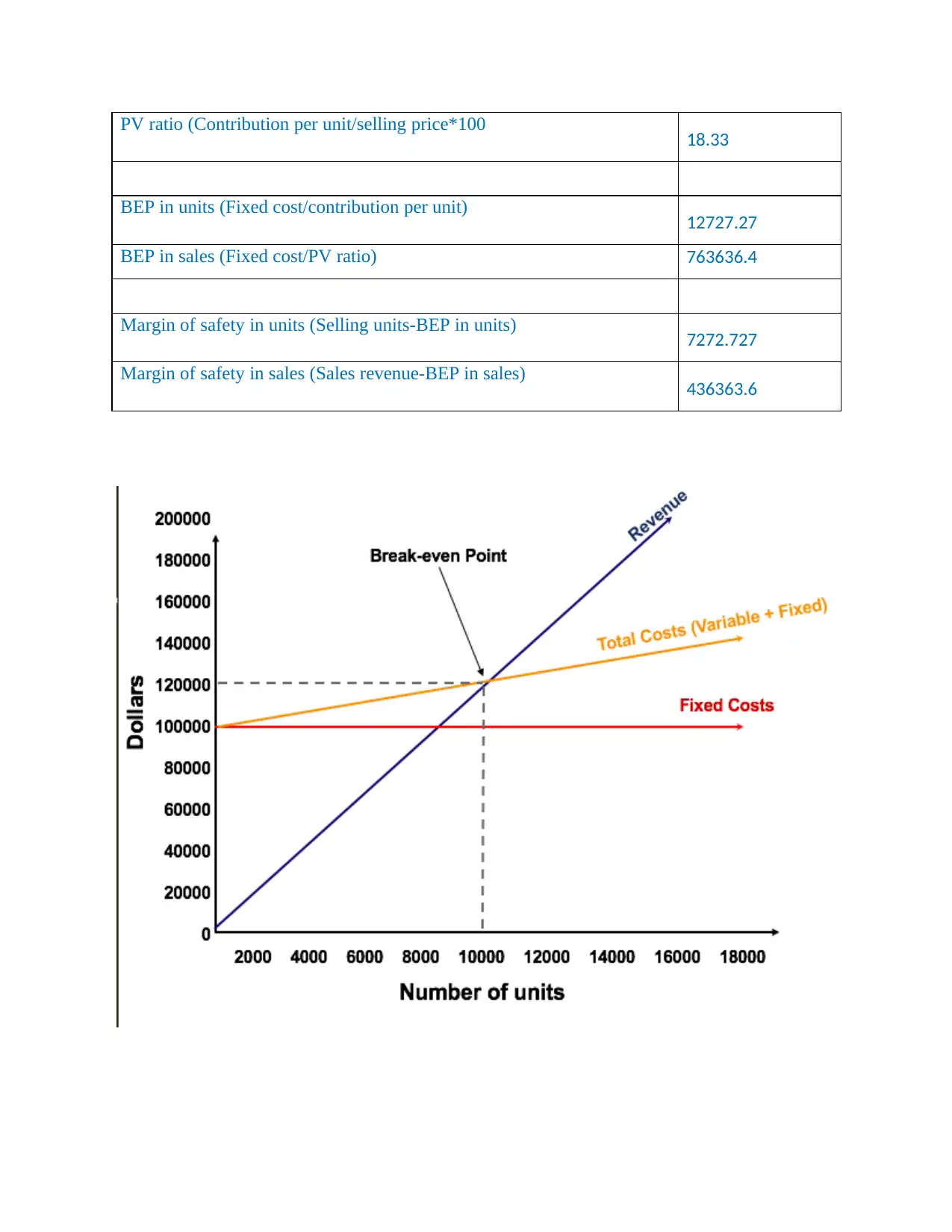

PV ratio (Contribution per unit/selling price*100 18.33

BEP in units (Fixed cost/contribution per unit) 12727.27

BEP in sales (Fixed cost/PV ratio) 763636.4

Margin of safety in units (Selling units-BEP in units) 7272.727

Margin of safety in sales (Sales revenue-BEP in sales) 436363.6

BEP in units (Fixed cost/contribution per unit) 12727.27

BEP in sales (Fixed cost/PV ratio) 763636.4

Margin of safety in units (Selling units-BEP in units) 7272.727

Margin of safety in sales (Sales revenue-BEP in sales) 436363.6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

P4 Advantages of different planning tools used for budgetary control

Budget and budgetary management are the instruments from which an entity will predict its

potential costs and revenues to expand sustainable manner. Different preparation methods are

evaluated in the following activities along with their benefits and demerits.

Budget and Budgetary control - Budget is the method where an enterprise is built to forecast

potential expenses from previous experiences. This approach allows to determine the conditions

of the future and makes correct plans.

Budgetary control is a strategy that means that the budget is planned in a way that makes for the

most precise financial plans are prepared. It's a methodology that contrasts estimates to real

results in order to identify differences (Morden, 2016).

Various planning tools used for budgetary control:

1. Production budget- For an appropriate accounting strategy, a production budget

introduces sets of units to be produced over a time frame. This is a substantial investment

plan that can assist a company by supplying reliable raw material statistics. In the

absence of an effective production budget, it can become difficult for companies to have

proper information about how much number of units need to be sold and needed

resources. Such as in Innocent drinks limited, their accountant prepares this budget that

enable to their production team to take corrective action of making suitable decisions for

purchasing of raw material as well as for production of new items (Myers, 2013).

Advantages Disadvantages

It encourages reducing output expense as

manufacturing is standardized. Initial

stock of goods become adequate to

handle. This is so because under it,

estimation of needed raw material is

provided that contributes to managers in

taking right decisions. For instance, in

Innocent drinks limited their managers

take corrective steps in order to buy

quantity of new raw material for further

production.

One of the biggest disadvantages to an

organization 's production expenditure

plan is that it requires more time and

money. Same as for above company, they

also face this issue of higher time

consumption as well as cost in order to

prepare this budget.

Example of production budget:

P4 Advantages of different planning tools used for budgetary control

Budget and budgetary management are the instruments from which an entity will predict its

potential costs and revenues to expand sustainable manner. Different preparation methods are

evaluated in the following activities along with their benefits and demerits.

Budget and Budgetary control - Budget is the method where an enterprise is built to forecast

potential expenses from previous experiences. This approach allows to determine the conditions

of the future and makes correct plans.

Budgetary control is a strategy that means that the budget is planned in a way that makes for the

most precise financial plans are prepared. It's a methodology that contrasts estimates to real

results in order to identify differences (Morden, 2016).

Various planning tools used for budgetary control:

1. Production budget- For an appropriate accounting strategy, a production budget

introduces sets of units to be produced over a time frame. This is a substantial investment

plan that can assist a company by supplying reliable raw material statistics. In the

absence of an effective production budget, it can become difficult for companies to have

proper information about how much number of units need to be sold and needed

resources. Such as in Innocent drinks limited, their accountant prepares this budget that

enable to their production team to take corrective action of making suitable decisions for

purchasing of raw material as well as for production of new items (Myers, 2013).

Advantages Disadvantages

It encourages reducing output expense as

manufacturing is standardized. Initial

stock of goods become adequate to

handle. This is so because under it,

estimation of needed raw material is

provided that contributes to managers in

taking right decisions. For instance, in

Innocent drinks limited their managers

take corrective steps in order to buy

quantity of new raw material for further

production.

One of the biggest disadvantages to an

organization 's production expenditure

plan is that it requires more time and

money. Same as for above company, they

also face this issue of higher time

consumption as well as cost in order to

prepare this budget.

Example of production budget:

2. Operational budget- In a corporate organization, an operating budget tracks all day-to-day

operations. The company chosen above can use this preparation strategy to manage its operating

costs and boost its working capital. It will become possible because under this all kinds of

activities and operations are predicted which helps to manager to prepare strategies like which

activities are complex and which ones are easier to perform. Same as the above budget, it also

has some limitations and benefits which are as follows:

Advantages Disadvantages

The budget allows companies to keep an eye

on all expenditures to efficiently control

expenditures and create financial savings.

Such as in above Innocent drinks limited,

they use this budget for managing different

kinds of activities and operations by help of it

(Namakonzi and Inanga, 2014).

This budget does not take into consideration

capital costs that often represent a distorted

picture of the profitability of the business.

3. Flexible budget: A flexible budget plan is an expense that changes or changes with changes in

measure or activity. The flexible spending plan is more advanced and useful than a static

financial plan. (The static expenditure amounts will remain unchanged. They will remain

unchanged from the amounts collected when the static financing plan was prepared and ratified.)

For costs that move by size or movement, consumption moves flexibly because variable

consumption involves a variable rate per unit of activity rather than a single fixed total amount.

To put it bluntly, the flexible financial plan is an increasingly valuable tool in estimating

management efficiency.

Advantages Disadvantages

It can help in business, costs and

calculating benefits at different levels of

This spending plan calls for talented

experts to tackle it. The reach of talented

operations. The company chosen above can use this preparation strategy to manage its operating

costs and boost its working capital. It will become possible because under this all kinds of

activities and operations are predicted which helps to manager to prepare strategies like which

activities are complex and which ones are easier to perform. Same as the above budget, it also

has some limitations and benefits which are as follows:

Advantages Disadvantages

The budget allows companies to keep an eye

on all expenditures to efficiently control

expenditures and create financial savings.

Such as in above Innocent drinks limited,

they use this budget for managing different

kinds of activities and operations by help of it

(Namakonzi and Inanga, 2014).

This budget does not take into consideration

capital costs that often represent a distorted

picture of the profitability of the business.

3. Flexible budget: A flexible budget plan is an expense that changes or changes with changes in

measure or activity. The flexible spending plan is more advanced and useful than a static

financial plan. (The static expenditure amounts will remain unchanged. They will remain

unchanged from the amounts collected when the static financing plan was prepared and ratified.)

For costs that move by size or movement, consumption moves flexibly because variable

consumption involves a variable rate per unit of activity rather than a single fixed total amount.

To put it bluntly, the flexible financial plan is an increasingly valuable tool in estimating

management efficiency.

Advantages Disadvantages

It can help in business, costs and

calculating benefits at different levels of

This spending plan calls for talented

experts to tackle it. The reach of talented

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.