Analyzing Management Accounting Systems: Tools and Techniques

VerifiedAdded on 2020/10/04

|20

|5966

|49

Essay

AI Summary

Management accounting plays a pivotal role in providing financial information that aids management decision-making. This essay explores the intricate components of Management Accounting Systems by examining essential tools such as Inventory Management, Job-Costing, Price-Optimization, and Cost Accounting. Each tool serves distinct functions; for instance, Inventory Management ensures optimal stock levels to prevent overstocking or stockouts. Meanwhile, Job-Costing provides detailed cost insights into specific projects or jobs, facilitating more accurate pricing and profitability analysis. Additionally, the essay discusses Price-Optimization techniques that help businesses set competitive prices while maximizing profits. Cost Accounting is highlighted as a crucial aspect for tracking expenses and managing budgets efficiently. Furthermore, various budgetary control methods such as financial and operating budgets are reviewed to understand their roles in planning and controlling organizational resources. Non-monetary budgets and the differentiation between fixed and variable budgets are also discussed to provide a holistic view of budgeting practices within management accounting. The essay concludes by emphasizing how these tools collectively support strategic decision-making, thereby enhancing overall business performance.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Report to General Manager regarding concept of management accounting and

requirements of their types to company......................................................................................1

P2 Report to General manager regarding explanation of methods of management accounting

reports..........................................................................................................................................4

TASK 2............................................................................................................................................7

P3 Difference between Marginal costing and Absorption costing and calculation of Income

statement through these methods:...............................................................................................7

TASK 3..........................................................................................................................................11

P4 Report to General manager regarding advantages and disadvantage of different types of

planning tools for budgetary control.........................................................................................11

P5 Uses of management accounting system in solving financial problems..............................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Report to General Manager regarding concept of management accounting and

requirements of their types to company......................................................................................1

P2 Report to General manager regarding explanation of methods of management accounting

reports..........................................................................................................................................4

TASK 2............................................................................................................................................7

P3 Difference between Marginal costing and Absorption costing and calculation of Income

statement through these methods:...............................................................................................7

TASK 3..........................................................................................................................................11

P4 Report to General manager regarding advantages and disadvantage of different types of

planning tools for budgetary control.........................................................................................11

P5 Uses of management accounting system in solving financial problems..............................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

A management accounting system gathers financial informations from operations of the

business like sales data, movement in inventories and changes in the costs of raw materials

(Banerjee, 2010). These useful informations than converted into valuable reports by management

accounting systems.

Bizdaq was established in 2015 with less than 10 employees, it comes under business

sales sectors. This company gives marketplace for sale and its annual turnover is near to

£100,000.

In this assignment, various types of management accounting systems have been

discussed. Advantages and disadvantages of budget control will support Bizdaq in making a

choice between different methods of budgetary-control. This assignment contains case study

which has two scenario's. First scenario has focus on accounting techniques implementation for

business, while second scenario consists of resolution techniques to reduce the impact of

financial issues. A report has been written to General manager, to convince him for adopting

different techniques of budgetary-control to solve Bizdaq's financial issues.

The main objective of this report is to explain application techniques of management

accounting tools like profit analysis, marginal costing and absorption costing methods.

TASK 1

P1 Report to General Manager regarding concept of management accounting and requirements

of their types to company

From: Management accounting officer

To: General manager of Bizdaq

Sub: Management accounting system

This report contains management accounting system meaning and its different types. It's basic

uses for company is also explained. The main purpose of this report is to explain management

about how it would support company in decision-making process.

Management Accounting System:

An accounting management system uses operational data and makes reports which is

valuable like sales analyses report, Inventory costs which is stocked and comparison report

between budgeted and actual expenses (Bebbington, Unerman and O'Dwyer, 2014). For

1

A management accounting system gathers financial informations from operations of the

business like sales data, movement in inventories and changes in the costs of raw materials

(Banerjee, 2010). These useful informations than converted into valuable reports by management

accounting systems.

Bizdaq was established in 2015 with less than 10 employees, it comes under business

sales sectors. This company gives marketplace for sale and its annual turnover is near to

£100,000.

In this assignment, various types of management accounting systems have been

discussed. Advantages and disadvantages of budget control will support Bizdaq in making a

choice between different methods of budgetary-control. This assignment contains case study

which has two scenario's. First scenario has focus on accounting techniques implementation for

business, while second scenario consists of resolution techniques to reduce the impact of

financial issues. A report has been written to General manager, to convince him for adopting

different techniques of budgetary-control to solve Bizdaq's financial issues.

The main objective of this report is to explain application techniques of management

accounting tools like profit analysis, marginal costing and absorption costing methods.

TASK 1

P1 Report to General Manager regarding concept of management accounting and requirements

of their types to company

From: Management accounting officer

To: General manager of Bizdaq

Sub: Management accounting system

This report contains management accounting system meaning and its different types. It's basic

uses for company is also explained. The main purpose of this report is to explain management

about how it would support company in decision-making process.

Management Accounting System:

An accounting management system uses operational data and makes reports which is

valuable like sales analyses report, Inventory costs which is stocked and comparison report

between budgeted and actual expenses (Bebbington, Unerman and O'Dwyer, 2014). For

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

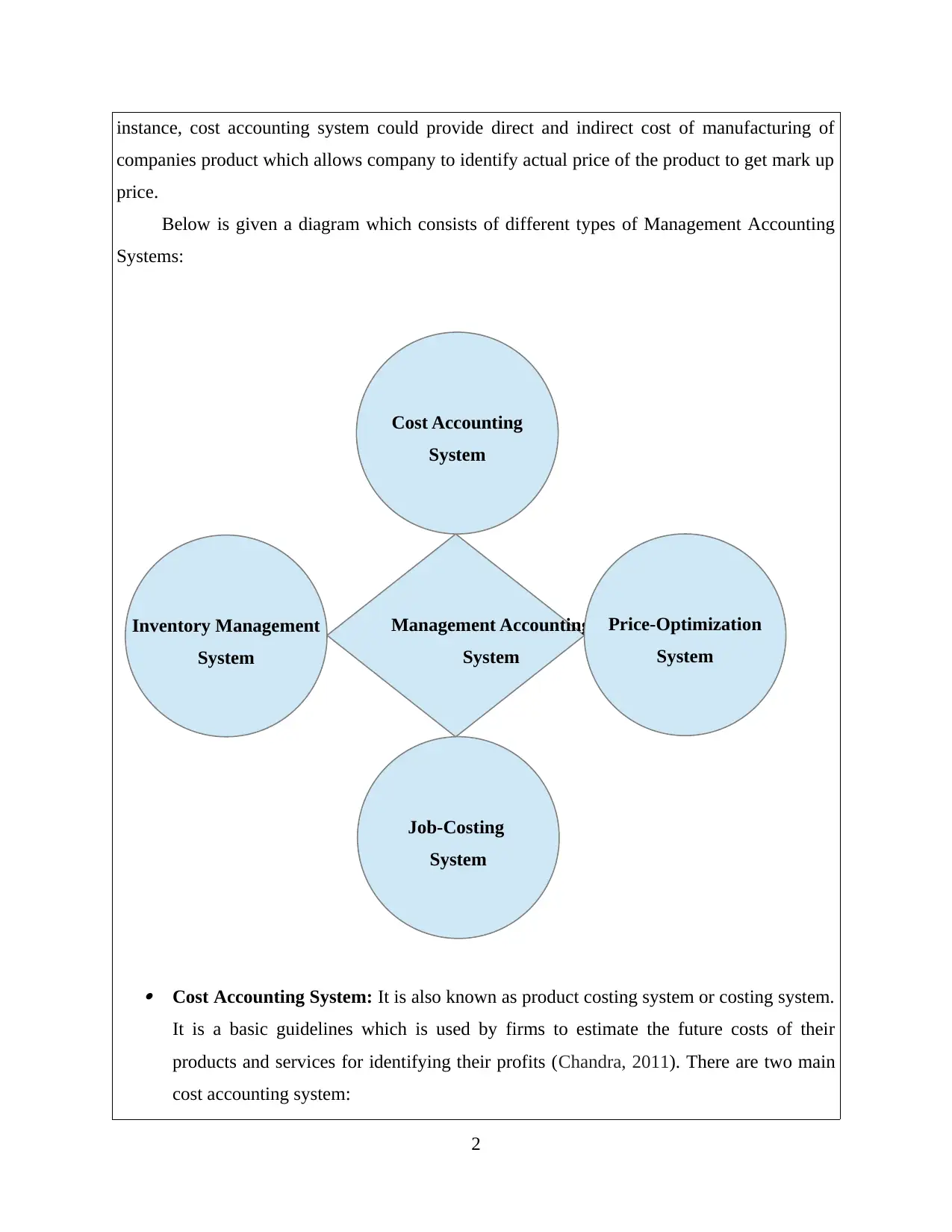

instance, cost accounting system could provide direct and indirect cost of manufacturing of

companies product which allows company to identify actual price of the product to get mark up

price.

Below is given a diagram which consists of different types of Management Accounting

Systems:

Cost Accounting System: It is also known as product costing system or costing system.

It is a basic guidelines which is used by firms to estimate the future costs of their

products and services for identifying their profits (Chandra, 2011). There are two main

cost accounting system:

2

Management Accounting

System

Inventory Management

System

Job-Costing

System

Price-Optimization

System

Cost Accounting

System

companies product which allows company to identify actual price of the product to get mark up

price.

Below is given a diagram which consists of different types of Management Accounting

Systems:

Cost Accounting System: It is also known as product costing system or costing system.

It is a basic guidelines which is used by firms to estimate the future costs of their

products and services for identifying their profits (Chandra, 2011). There are two main

cost accounting system:

2

Management Accounting

System

Inventory Management

System

Job-Costing

System

Price-Optimization

System

Cost Accounting

System

◦ Job Order Costing: These type of cost accounting systems identifies manufacturing

costs for each job separately (Chapman, 2011). It is useful for those firms which are

into producing unique products or receiving special orders like niche furniture

producer, high cost air surveillance system, etc.

◦ Process Costing: These type of cost accounting system identifies manufacturing

costs for each process separately. It's useful for different departmental process like

oil refineries, chemical producers, etc.

Some times firms uses combination of both systems which is also known as hybrid

cost accounting system.

Benefits: Bizdaq could be benefited through this accounting system, as through this

method company might know about the products which are profitable or not profitable for firm.

Also a product costing system would help company in estimating the value of closing materials

inventory, work-in-progress and finished goods inventory for preparation of financial statement.

Inventory Management System: An Inventory management system consists of

combination of the uses of desktop software, barcode scanners, barcode printers and

mobile devices to arrange the management of inventory like goods, consumables,

supplies, stock, etc (Christ and Burritt, 2013). Inventory management is important

because it control works of operations by tracking two main functions of companies

warehouses which is; Receiving incoming goods and shipping outgoing inventories.

The main objective of inventory control is to identify present inventory levels and

minimizing under-stock and over-stock accordingly.

Benefits: It could be useful for Bizdaq to manage its inventory because through Inventory

management system, company could create purchase orders, receive and deliver inventories,

creates sales orders, shipping inventories, calculates turnover of physical inventories and

schedule reports. Inventory management system could also help Bizdaq in improving bottom

line, accuracy of inventories and workflow of the company.

Job Costing System: This type of management accounting system involves process of

collecting informations related to the costs attached to specific production or service job

(Damodaran, 2012). This data might be required by management to submit cost related

informations to their clients. Job costing systems gathers three types of data's which is

Direct materials, Direct labour and Overhead costs.

3

costs for each job separately (Chapman, 2011). It is useful for those firms which are

into producing unique products or receiving special orders like niche furniture

producer, high cost air surveillance system, etc.

◦ Process Costing: These type of cost accounting system identifies manufacturing

costs for each process separately. It's useful for different departmental process like

oil refineries, chemical producers, etc.

Some times firms uses combination of both systems which is also known as hybrid

cost accounting system.

Benefits: Bizdaq could be benefited through this accounting system, as through this

method company might know about the products which are profitable or not profitable for firm.

Also a product costing system would help company in estimating the value of closing materials

inventory, work-in-progress and finished goods inventory for preparation of financial statement.

Inventory Management System: An Inventory management system consists of

combination of the uses of desktop software, barcode scanners, barcode printers and

mobile devices to arrange the management of inventory like goods, consumables,

supplies, stock, etc (Christ and Burritt, 2013). Inventory management is important

because it control works of operations by tracking two main functions of companies

warehouses which is; Receiving incoming goods and shipping outgoing inventories.

The main objective of inventory control is to identify present inventory levels and

minimizing under-stock and over-stock accordingly.

Benefits: It could be useful for Bizdaq to manage its inventory because through Inventory

management system, company could create purchase orders, receive and deliver inventories,

creates sales orders, shipping inventories, calculates turnover of physical inventories and

schedule reports. Inventory management system could also help Bizdaq in improving bottom

line, accuracy of inventories and workflow of the company.

Job Costing System: This type of management accounting system involves process of

collecting informations related to the costs attached to specific production or service job

(Damodaran, 2012). This data might be required by management to submit cost related

informations to their clients. Job costing systems gathers three types of data's which is

Direct materials, Direct labour and Overhead costs.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Benefits: It is useful for Bizdaq because it could help company in modify informations

according to the requirements of customer. As clients only allows to charge certain costs to their

jobs.

Price-Optimization System: These systems are mathematical programs which

calculates variance of demands at different level of prices and combines the data

information on costs and inventory levels to suggests prices for earning profits (David,

2011). Price-Optimization system works on three critical pricing elements like price

strategy of a company, value of product for buyer and sellers and strategies of

management to control profitability elements.

Benefits: It would help Bizdaq in determining starting prices, promotion pricing and

discount pricing.

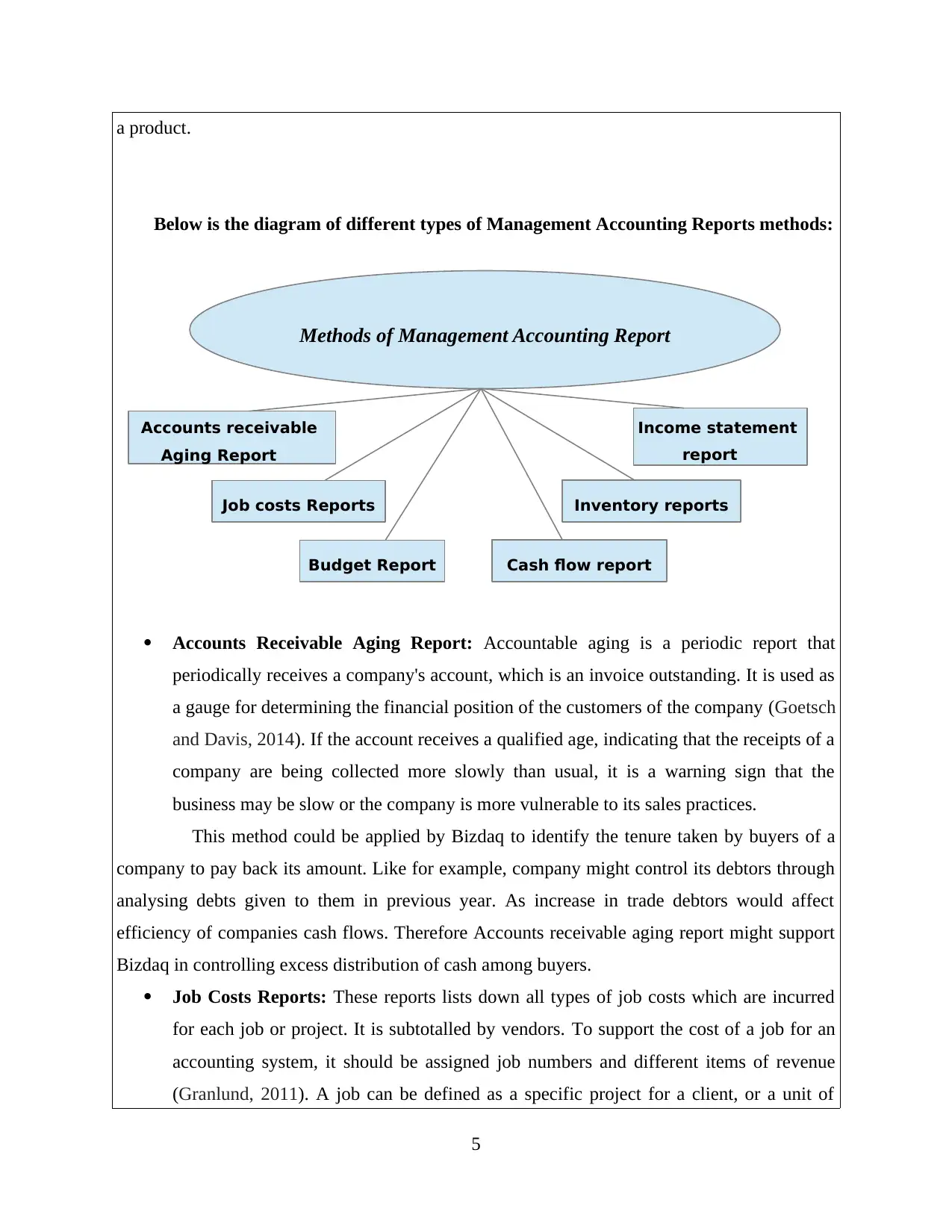

P2 Report to General manager regarding explanation of methods of management accounting

reports

From: Management accounting officer

To: General manager of Bizdaq

Sub: Management accounting report

The objective of this report is to explain different methods of reporting in accounting

management process and to describe the possible applications of these reports to support

company for appropriate decision-making process.

Management Accounting Report

These management accounting reports supports business in determining performance of

the company. It is usually created at the end of every year and used by top management to know

financial status of the company in a market (Eastman, 2012). It gives guidelines to a manager to

modify some process to increase or improve performance of a company.

Management accounting report is also important because it supports company in

estimating future costs in advance, it helps in making budgets, make or buy decisions, reacts

against variances in financial performance of a company. It determines which factors is not

performing well. For instance variable costing and marginal costing methods identifies per unit

cost of machineries, labour, materials and variable overheads to know exact production costs of

4

according to the requirements of customer. As clients only allows to charge certain costs to their

jobs.

Price-Optimization System: These systems are mathematical programs which

calculates variance of demands at different level of prices and combines the data

information on costs and inventory levels to suggests prices for earning profits (David,

2011). Price-Optimization system works on three critical pricing elements like price

strategy of a company, value of product for buyer and sellers and strategies of

management to control profitability elements.

Benefits: It would help Bizdaq in determining starting prices, promotion pricing and

discount pricing.

P2 Report to General manager regarding explanation of methods of management accounting

reports

From: Management accounting officer

To: General manager of Bizdaq

Sub: Management accounting report

The objective of this report is to explain different methods of reporting in accounting

management process and to describe the possible applications of these reports to support

company for appropriate decision-making process.

Management Accounting Report

These management accounting reports supports business in determining performance of

the company. It is usually created at the end of every year and used by top management to know

financial status of the company in a market (Eastman, 2012). It gives guidelines to a manager to

modify some process to increase or improve performance of a company.

Management accounting report is also important because it supports company in

estimating future costs in advance, it helps in making budgets, make or buy decisions, reacts

against variances in financial performance of a company. It determines which factors is not

performing well. For instance variable costing and marginal costing methods identifies per unit

cost of machineries, labour, materials and variable overheads to know exact production costs of

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

a product.

Below is the diagram of different types of Management Accounting Reports methods:

Accounts Receivable Aging Report: Accountable aging is a periodic report that

periodically receives a company's account, which is an invoice outstanding. It is used as

a gauge for determining the financial position of the customers of the company (Goetsch

and Davis, 2014). If the account receives a qualified age, indicating that the receipts of a

company are being collected more slowly than usual, it is a warning sign that the

business may be slow or the company is more vulnerable to its sales practices.

This method could be applied by Bizdaq to identify the tenure taken by buyers of a

company to pay back its amount. Like for example, company might control its debtors through

analysing debts given to them in previous year. As increase in trade debtors would affect

efficiency of companies cash flows. Therefore Accounts receivable aging report might support

Bizdaq in controlling excess distribution of cash among buyers.

Job Costs Reports: These reports lists down all types of job costs which are incurred

for each job or project. It is subtotalled by vendors. To support the cost of a job for an

accounting system, it should be assigned job numbers and different items of revenue

(Granlund, 2011). A job can be defined as a specific project for a client, or a unit of

5

Methods of Management Accounting Report

Accounts receivable

Aging Report

Job costs Reports

Income statement

report

Cash flow reportBudget Report

Inventory reports

Below is the diagram of different types of Management Accounting Reports methods:

Accounts Receivable Aging Report: Accountable aging is a periodic report that

periodically receives a company's account, which is an invoice outstanding. It is used as

a gauge for determining the financial position of the customers of the company (Goetsch

and Davis, 2014). If the account receives a qualified age, indicating that the receipts of a

company are being collected more slowly than usual, it is a warning sign that the

business may be slow or the company is more vulnerable to its sales practices.

This method could be applied by Bizdaq to identify the tenure taken by buyers of a

company to pay back its amount. Like for example, company might control its debtors through

analysing debts given to them in previous year. As increase in trade debtors would affect

efficiency of companies cash flows. Therefore Accounts receivable aging report might support

Bizdaq in controlling excess distribution of cash among buyers.

Job Costs Reports: These reports lists down all types of job costs which are incurred

for each job or project. It is subtotalled by vendors. To support the cost of a job for an

accounting system, it should be assigned job numbers and different items of revenue

(Granlund, 2011). A job can be defined as a specific project for a client, or a unit of

5

Methods of Management Accounting Report

Accounts receivable

Aging Report

Job costs Reports

Income statement

report

Cash flow reportBudget Report

Inventory reports

manufactured product or a batch of units of the same type, which are produced

simultaneously.

The application of Job Costing Reports might support Bizdaq in identifying those

activities which are consumed lots of cash. Through this reporting method company could

modify informations according to the requirements of customer. As clients only allows to

charge certain costs to their jobs.

Budget Reports: To support the cost of the job for the accounting system, it should be

assigned the number of jobs and different items of revenue. A job can be defined as a

specific project for the customer, or a batch of units of the same product or the same

type of units which are produced simultaneously (Kimmel, Weygandt and Kieso, 2010).

According to the report of this budget, the estimate should be based on the previous

trends of actual expenditure, revenue and prices. This organization also helps in the

distribution of incentives among its employees. Budget reports are generally limited to

the reporter's strong analytical and assessment skills. Financial status, income and

expenditure data can be modified on a regular basis by a company. Financial data is

usually recorded in the budget report, which is also known as the financial report, it has

been written and written based on the requirements of a company.

Application: Through application of budget reports, Bizdaq would get a support in

analysing the variances between budgeted and actual costs. As more deviation reflects

inefficiency of a company to manage demands and supply of a product, while less variances

indicates that Bizdaq is very well utilising its resources and successfully eliminating the extra

wastes.

Cash Flow Statement Report: In management accounting reports, this types is also

known as statement of cash flows. Cash flow statement is a financial statement which

tracks the changes of balance sheet and Profit&loss accounts (Linoff and Berry, 2011).

It determines how much cash is inflows and outflows from operating, investment and

financial activities.

Application: Bizdaq could apply this reporting method, in order to obtain the liquidity of

its business through analysis of cash flow statement reports, for example, the net profit of the

company is £9300 according to the direct cost, which has been earned which means that it is

actually in exchange for cash Not earned by business. Therefore, the realization of how much

6

simultaneously.

The application of Job Costing Reports might support Bizdaq in identifying those

activities which are consumed lots of cash. Through this reporting method company could

modify informations according to the requirements of customer. As clients only allows to

charge certain costs to their jobs.

Budget Reports: To support the cost of the job for the accounting system, it should be

assigned the number of jobs and different items of revenue. A job can be defined as a

specific project for the customer, or a batch of units of the same product or the same

type of units which are produced simultaneously (Kimmel, Weygandt and Kieso, 2010).

According to the report of this budget, the estimate should be based on the previous

trends of actual expenditure, revenue and prices. This organization also helps in the

distribution of incentives among its employees. Budget reports are generally limited to

the reporter's strong analytical and assessment skills. Financial status, income and

expenditure data can be modified on a regular basis by a company. Financial data is

usually recorded in the budget report, which is also known as the financial report, it has

been written and written based on the requirements of a company.

Application: Through application of budget reports, Bizdaq would get a support in

analysing the variances between budgeted and actual costs. As more deviation reflects

inefficiency of a company to manage demands and supply of a product, while less variances

indicates that Bizdaq is very well utilising its resources and successfully eliminating the extra

wastes.

Cash Flow Statement Report: In management accounting reports, this types is also

known as statement of cash flows. Cash flow statement is a financial statement which

tracks the changes of balance sheet and Profit&loss accounts (Linoff and Berry, 2011).

It determines how much cash is inflows and outflows from operating, investment and

financial activities.

Application: Bizdaq could apply this reporting method, in order to obtain the liquidity of

its business through analysis of cash flow statement reports, for example, the net profit of the

company is £9300 according to the direct cost, which has been earned which means that it is

actually in exchange for cash Not earned by business. Therefore, the realization of how much

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

cash is survived with the report of cash flow, helps in identifying.

CONCLUSION

After analysing key points of above report it can be concluded that, it is always a smart

business decision that select Management Accounting Reporting System which integrates with

the company's financial accounting system. This eliminates redundancy and increases the

timeliness of the management report. With precise, timely information, management can make

informed decisions about operating commodities like cost reduction, increase in production

time, increase in hand list, and increasing marketing budget. Businesses with a management

accounting system have a definite benefit in organizing the capital, to reduce costs and increase

the expansion of the future.

TASK 2

P3 Difference between Marginal costing and Absorption costing and calculation of Income

statement through these methods:

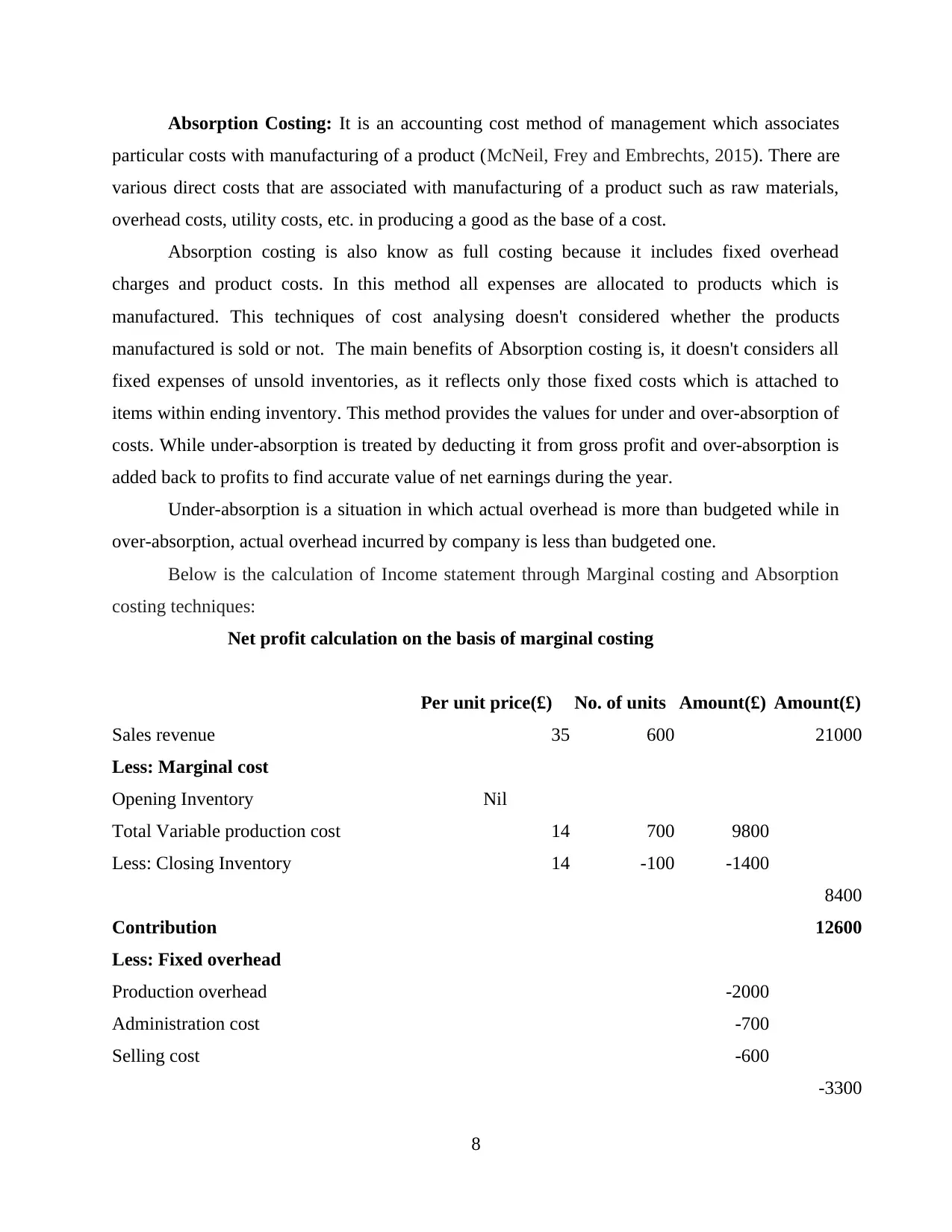

Marginal Costing: Its calculation is based on marginal costs of a product. The marginal

cost of a product is variable cost of it, whereas the marginal production cost of a product is sum

of its direct materials cost, direct labour cost, direct expenses cost and variable production

overhead costs per unit (Macintosh and Quattrone, 2010). This indicates that, total variables

costs would rise with the increase in volume of production and sales of business.

On the other hand, fixed costs are those expenses that remains same for year and it is not

affected by volume of production and sales. Marginal cost of production are the costs per unit of

product which is produced by the company and it can be avoided if firm is not producing units.

Like for example, suppose production cost of 100 units is £1000 and if company manufactures

101 units than cost of product is increased to £1010, that means per unit cost of production is

£10. Hence, company can avoid this additional cost of £10 by not producing one extra units.

Marginal costing is an accounting system where variable costs are added to costs per

units. Fixed costs are charged against contribution to determine exact profits earned by company

during a year. Variable costs are those which are changes with the output of units produced. This

method is also known as principal costing techniques which is helpful for companies in decision-

making.

7

CONCLUSION

After analysing key points of above report it can be concluded that, it is always a smart

business decision that select Management Accounting Reporting System which integrates with

the company's financial accounting system. This eliminates redundancy and increases the

timeliness of the management report. With precise, timely information, management can make

informed decisions about operating commodities like cost reduction, increase in production

time, increase in hand list, and increasing marketing budget. Businesses with a management

accounting system have a definite benefit in organizing the capital, to reduce costs and increase

the expansion of the future.

TASK 2

P3 Difference between Marginal costing and Absorption costing and calculation of Income

statement through these methods:

Marginal Costing: Its calculation is based on marginal costs of a product. The marginal

cost of a product is variable cost of it, whereas the marginal production cost of a product is sum

of its direct materials cost, direct labour cost, direct expenses cost and variable production

overhead costs per unit (Macintosh and Quattrone, 2010). This indicates that, total variables

costs would rise with the increase in volume of production and sales of business.

On the other hand, fixed costs are those expenses that remains same for year and it is not

affected by volume of production and sales. Marginal cost of production are the costs per unit of

product which is produced by the company and it can be avoided if firm is not producing units.

Like for example, suppose production cost of 100 units is £1000 and if company manufactures

101 units than cost of product is increased to £1010, that means per unit cost of production is

£10. Hence, company can avoid this additional cost of £10 by not producing one extra units.

Marginal costing is an accounting system where variable costs are added to costs per

units. Fixed costs are charged against contribution to determine exact profits earned by company

during a year. Variable costs are those which are changes with the output of units produced. This

method is also known as principal costing techniques which is helpful for companies in decision-

making.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Absorption Costing: It is an accounting cost method of management which associates

particular costs with manufacturing of a product (McNeil, Frey and Embrechts, 2015). There are

various direct costs that are associated with manufacturing of a product such as raw materials,

overhead costs, utility costs, etc. in producing a good as the base of a cost.

Absorption costing is also know as full costing because it includes fixed overhead

charges and product costs. In this method all expenses are allocated to products which is

manufactured. This techniques of cost analysing doesn't considered whether the products

manufactured is sold or not. The main benefits of Absorption costing is, it doesn't considers all

fixed expenses of unsold inventories, as it reflects only those fixed costs which is attached to

items within ending inventory. This method provides the values for under and over-absorption of

costs. While under-absorption is treated by deducting it from gross profit and over-absorption is

added back to profits to find accurate value of net earnings during the year.

Under-absorption is a situation in which actual overhead is more than budgeted while in

over-absorption, actual overhead incurred by company is less than budgeted one.

Below is the calculation of Income statement through Marginal costing and Absorption

costing techniques:

Net profit calculation on the basis of marginal costing

Per unit price(£) No. of units Amount(£) Amount(£)

Sales revenue 35 600 21000

Less: Marginal cost

Opening Inventory Nil

Total Variable production cost 14 700 9800

Less: Closing Inventory 14 -100 -1400

8400

Contribution 12600

Less: Fixed overhead

Production overhead -2000

Administration cost -700

Selling cost -600

-3300

8

particular costs with manufacturing of a product (McNeil, Frey and Embrechts, 2015). There are

various direct costs that are associated with manufacturing of a product such as raw materials,

overhead costs, utility costs, etc. in producing a good as the base of a cost.

Absorption costing is also know as full costing because it includes fixed overhead

charges and product costs. In this method all expenses are allocated to products which is

manufactured. This techniques of cost analysing doesn't considered whether the products

manufactured is sold or not. The main benefits of Absorption costing is, it doesn't considers all

fixed expenses of unsold inventories, as it reflects only those fixed costs which is attached to

items within ending inventory. This method provides the values for under and over-absorption of

costs. While under-absorption is treated by deducting it from gross profit and over-absorption is

added back to profits to find accurate value of net earnings during the year.

Under-absorption is a situation in which actual overhead is more than budgeted while in

over-absorption, actual overhead incurred by company is less than budgeted one.

Below is the calculation of Income statement through Marginal costing and Absorption

costing techniques:

Net profit calculation on the basis of marginal costing

Per unit price(£) No. of units Amount(£) Amount(£)

Sales revenue 35 600 21000

Less: Marginal cost

Opening Inventory Nil

Total Variable production cost 14 700 9800

Less: Closing Inventory 14 -100 -1400

8400

Contribution 12600

Less: Fixed overhead

Production overhead -2000

Administration cost -700

Selling cost -600

-3300

8

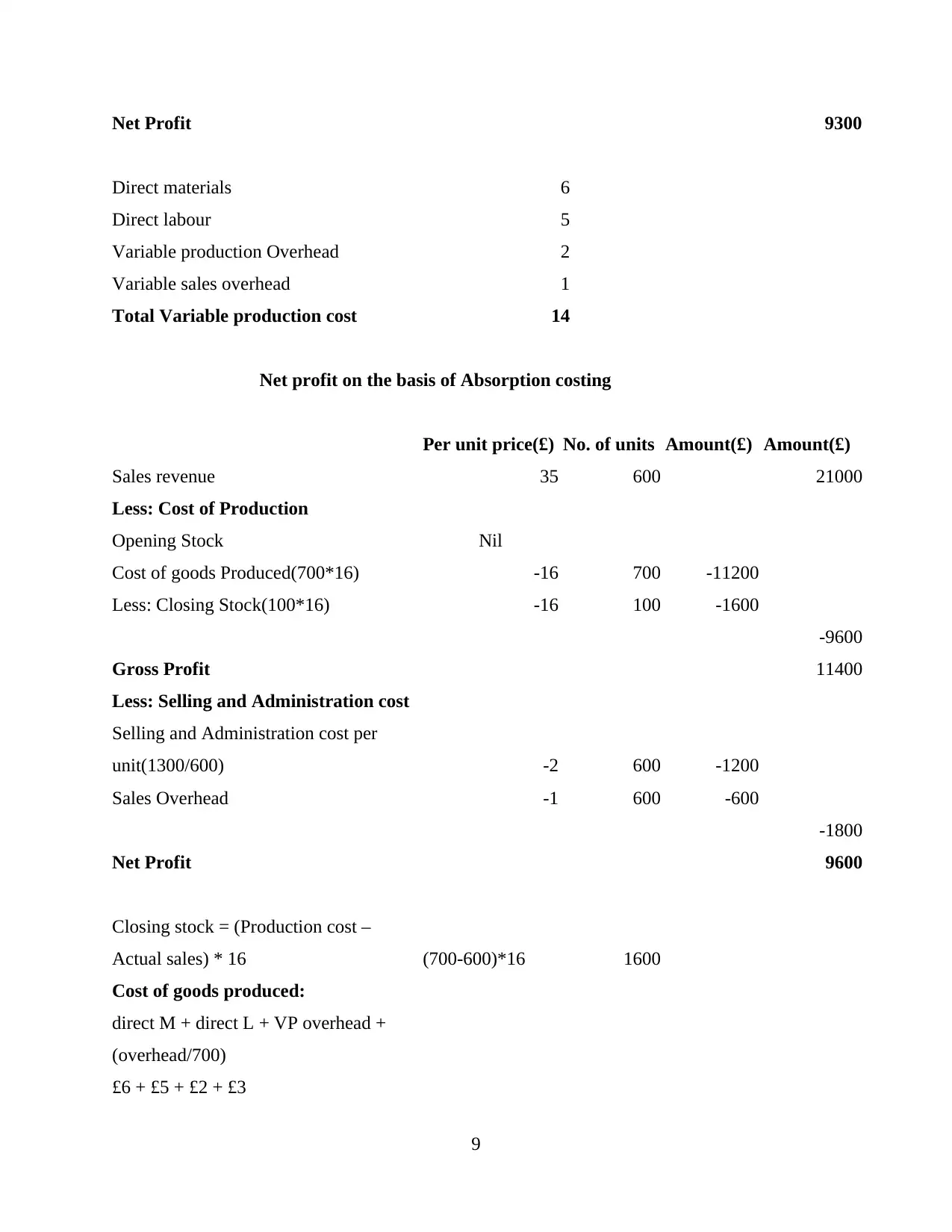

Net Profit 9300

Direct materials 6

Direct labour 5

Variable production Overhead 2

Variable sales overhead 1

Total Variable production cost 14

Net profit on the basis of Absorption costing

Per unit price(£) No. of units Amount(£) Amount(£)

Sales revenue 35 600 21000

Less: Cost of Production

Opening Stock Nil

Cost of goods Produced(700*16) -16 700 -11200

Less: Closing Stock(100*16) -16 100 -1600

-9600

Gross Profit 11400

Less: Selling and Administration cost

Selling and Administration cost per

unit(1300/600) -2 600 -1200

Sales Overhead -1 600 -600

-1800

Net Profit 9600

Closing stock = (Production cost –

Actual sales) * 16 (700-600)*16 1600

Cost of goods produced:

direct M + direct L + VP overhead +

(overhead/700)

£6 + £5 + £2 + £3

9

Direct materials 6

Direct labour 5

Variable production Overhead 2

Variable sales overhead 1

Total Variable production cost 14

Net profit on the basis of Absorption costing

Per unit price(£) No. of units Amount(£) Amount(£)

Sales revenue 35 600 21000

Less: Cost of Production

Opening Stock Nil

Cost of goods Produced(700*16) -16 700 -11200

Less: Closing Stock(100*16) -16 100 -1600

-9600

Gross Profit 11400

Less: Selling and Administration cost

Selling and Administration cost per

unit(1300/600) -2 600 -1200

Sales Overhead -1 600 -600

-1800

Net Profit 9600

Closing stock = (Production cost –

Actual sales) * 16 (700-600)*16 1600

Cost of goods produced:

direct M + direct L + VP overhead +

(overhead/700)

£6 + £5 + £2 + £3

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.