Analysis of Management Accounting Systems Report - Aon Group

VerifiedAdded on 2021/02/19

|17

|4613

|15

Report

AI Summary

This report provides a comprehensive overview of management accounting systems, focusing on their application within the Aon Consulting Group and Grange Construction Materials. It explores the core principles, roles, and various systems like inventory management, cost accounting, and price optimization. The report delves into different types of management accounting reports, emphasizing their importance in decision-making. Furthermore, it examines costing techniques, including marginal and absorption costing, to prepare income statements. The report also analyzes planning tools used for budgetary control, comparing advantages and disadvantages. Finally, it compares how business entities apply management accounting systems to address financial problems, providing a holistic understanding of the subject matter.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Understanding

of

management accounting systems ..............................................................................................1

P2 Different kind of management accounting report..................................................................4

TASK 2............................................................................................................................................5

P3 Costing Techniques to prepare income statements................................................................5

TASK 3..........................................................................................................................................10

P4 Advantages and disadvantages of different types of planning tools used for budgetary

control.......................................................................................................................................10

TASK 4..........................................................................................................................................12

P5 Comparison of business entities applying management accounting systems for responding

different financial problems.....................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES................................................................................................................................1

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Understanding

of

management accounting systems ..............................................................................................1

P2 Different kind of management accounting report..................................................................4

TASK 2............................................................................................................................................5

P3 Costing Techniques to prepare income statements................................................................5

TASK 3..........................................................................................................................................10

P4 Advantages and disadvantages of different types of planning tools used for budgetary

control.......................................................................................................................................10

TASK 4..........................................................................................................................................12

P5 Comparison of business entities applying management accounting systems for responding

different financial problems.....................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES................................................................................................................................1

INTRODUCTION

In today,s economy there is a proper need of management in every sectors so that

available resources can be fully utilised and it easy for company to attain the desired results. In

business case, the concept related with identifying, classifying, grouping, reporting, analysing

and evaluating valuable financial information that support inner manager to make authentic

decision (Management Accounting, 2019). Aon consulting group one of the leading financial

company in UK that provides various consultancy services to its clients those have main

operation linked with construction, hospitality and retail industry. To better gain the

understanding of management accounting, Grange Construction Materials is selected. The

company deals in construction company and supply different kind of construction material to

large number of customer in UK.

In this report, several management accounting system with their importance and use in

responding to various financial problems, different report are discussed. In addition, valuable

costing method like absorption and marginal methods are used to prepare annual statements.

TASK 1

P1 Understanding of management accounting systems

Management accounting is related with systematic combination of valuable services that

are helpful in establishing a detail structure which provide authentic information about complete

performance of internal operation so that effective decision are made for future growth. In

general the procedure which provides financial data to managers within company in order to

make modification or improvement is know as management accounting.

Origin, role and principle of management accounting.

The concept of management accounting was originated in 1960s that mainly focus on

cost accounting that help the management to better analyse the overall performance and make

suitable changes (Collis and Hussey, 2017). There are some major principle that ease the process

of collecting information that are discussed below:

Influence: It enables to generate information that is influential to manager so they can

easily makes changes.

Relevance: It must be understood that all the facts and figures must be related to each

other so that better decision are made.

1

In today,s economy there is a proper need of management in every sectors so that

available resources can be fully utilised and it easy for company to attain the desired results. In

business case, the concept related with identifying, classifying, grouping, reporting, analysing

and evaluating valuable financial information that support inner manager to make authentic

decision (Management Accounting, 2019). Aon consulting group one of the leading financial

company in UK that provides various consultancy services to its clients those have main

operation linked with construction, hospitality and retail industry. To better gain the

understanding of management accounting, Grange Construction Materials is selected. The

company deals in construction company and supply different kind of construction material to

large number of customer in UK.

In this report, several management accounting system with their importance and use in

responding to various financial problems, different report are discussed. In addition, valuable

costing method like absorption and marginal methods are used to prepare annual statements.

TASK 1

P1 Understanding of management accounting systems

Management accounting is related with systematic combination of valuable services that

are helpful in establishing a detail structure which provide authentic information about complete

performance of internal operation so that effective decision are made for future growth. In

general the procedure which provides financial data to managers within company in order to

make modification or improvement is know as management accounting.

Origin, role and principle of management accounting.

The concept of management accounting was originated in 1960s that mainly focus on

cost accounting that help the management to better analyse the overall performance and make

suitable changes (Collis and Hussey, 2017). There are some major principle that ease the process

of collecting information that are discussed below:

Influence: It enables to generate information that is influential to manager so they can

easily makes changes.

Relevance: It must be understood that all the facts and figures must be related to each

other so that better decision are made.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Trust: The main motive is related with developing trust among manager and employees.

The main role of management accounting within company is to run tasks which help to

ensure financial aspects, handle all financial issues so that there can be better formulation of

strategy which support in growth and development.

Management Accounting Financial Accounting

The major objective of management

accounting to ascertain beneficial information

for internal managerial that can be used to

make vital decision for growth and success.

Financial accounting is refereed to the process

of preparing useful report that disclose the

financial performance of company to internal

and external parties.

Company are free to choose the option of

management accounting.

Companies are needed to flow the concept of

financial reporting that ease in better analysing

of total financial status and position.

Different procedure and system related with

management accounting importance to both

aspects that are qualitative and quantitative.

The process of financial accounting only

includes quantitative aspects.

In business scenario, the different kind of management accounting system are used by

manager of company in order to run and manage different useful operation and makes them run

profitable. There are various system each one have its own importance such as cost system help

to reduce cost and unprofitable activities, price system support to fix price etc. Some of the

useful system used by manager of Grange construction material are discussed below:

Inventory management system: This is related with maintaining a proper record of total

inventory held by company during entire production process (Demski, 2013). Manager of

respective company use this system to keep proper record of inward and outward flow of

inventory while providing useful services to desired customer group. It also provide strength to

supply chain as authentic report enables manager company to fulfil the demand of customer by

delivering required finished goods.

Cost accounting system: This system is related with managing and maintain cost related

with different operation within company. Manager of Grange construction material use this

system to determine the total cost incurred in different operation, maintain stock level and

production process. Thus it support in identifying the activities due to which there is huge

2

The main role of management accounting within company is to run tasks which help to

ensure financial aspects, handle all financial issues so that there can be better formulation of

strategy which support in growth and development.

Management Accounting Financial Accounting

The major objective of management

accounting to ascertain beneficial information

for internal managerial that can be used to

make vital decision for growth and success.

Financial accounting is refereed to the process

of preparing useful report that disclose the

financial performance of company to internal

and external parties.

Company are free to choose the option of

management accounting.

Companies are needed to flow the concept of

financial reporting that ease in better analysing

of total financial status and position.

Different procedure and system related with

management accounting importance to both

aspects that are qualitative and quantitative.

The process of financial accounting only

includes quantitative aspects.

In business scenario, the different kind of management accounting system are used by

manager of company in order to run and manage different useful operation and makes them run

profitable. There are various system each one have its own importance such as cost system help

to reduce cost and unprofitable activities, price system support to fix price etc. Some of the

useful system used by manager of Grange construction material are discussed below:

Inventory management system: This is related with maintaining a proper record of total

inventory held by company during entire production process (Demski, 2013). Manager of

respective company use this system to keep proper record of inward and outward flow of

inventory while providing useful services to desired customer group. It also provide strength to

supply chain as authentic report enables manager company to fulfil the demand of customer by

delivering required finished goods.

Cost accounting system: This system is related with managing and maintain cost related

with different operation within company. Manager of Grange construction material use this

system to determine the total cost incurred in different operation, maintain stock level and

production process. Thus it support in identifying the activities due to which there is huge

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expenses and results are not favourable and remove the unprofitable activities which help in

growing profit.

Price optimisation system: It is crucial for company to fix best price of there product so

that maximum number of customer can get benefit and co0mpany is able to increase profit by

good margin. By using the concept of price optimisation system manager of Grange construction

material are beneficial to set the best suitable price for their product so that more and more

customer can attain according to their requirement.

Job costing system: It is related with determining the cost incurred by companies on

different jobs that are involved in various useful operation of company (Kanellou and Spathis,

2013). In respective firm manager with the support of job costing method are helpful in defining

the total cost that is spend on large number of worker and ascertain the most profitable and

unprofitable job. This system support in increasing overall productivity as manage may invest

more in profitable activities.

Integration with company.

It is stated that proper and systematic integration of above presented management

systems aid in providing smooth and ease running of different organisation's operations.

Assorted systems assist in boosting the overall performance by giving necessary information

within specific time period. For example cost accounting systems help in preparation of cost

sheet and assessment of cost related with different process and inventory management system

support manager in increasing production level and increase profit by providing goods as per

demands.

Benefits of different system.

System Benefits

Cost Accounting system With the systematic support of this system manager are

able to help in determine of total cost that are included in

various business activities so that profit can be find out.

Inventory Management System This system support to maintain proper record of total

stock laying in warehouse so that demand can be fulfilled.

Job Costing system It help in ascertaining the total cost company utilised in

different job so that crucial decision are made.

3

growing profit.

Price optimisation system: It is crucial for company to fix best price of there product so

that maximum number of customer can get benefit and co0mpany is able to increase profit by

good margin. By using the concept of price optimisation system manager of Grange construction

material are beneficial to set the best suitable price for their product so that more and more

customer can attain according to their requirement.

Job costing system: It is related with determining the cost incurred by companies on

different jobs that are involved in various useful operation of company (Kanellou and Spathis,

2013). In respective firm manager with the support of job costing method are helpful in defining

the total cost that is spend on large number of worker and ascertain the most profitable and

unprofitable job. This system support in increasing overall productivity as manage may invest

more in profitable activities.

Integration with company.

It is stated that proper and systematic integration of above presented management

systems aid in providing smooth and ease running of different organisation's operations.

Assorted systems assist in boosting the overall performance by giving necessary information

within specific time period. For example cost accounting systems help in preparation of cost

sheet and assessment of cost related with different process and inventory management system

support manager in increasing production level and increase profit by providing goods as per

demands.

Benefits of different system.

System Benefits

Cost Accounting system With the systematic support of this system manager are

able to help in determine of total cost that are included in

various business activities so that profit can be find out.

Inventory Management System This system support to maintain proper record of total

stock laying in warehouse so that demand can be fulfilled.

Job Costing system It help in ascertaining the total cost company utilised in

different job so that crucial decision are made.

3

Price Optimisation System By using this method manager are able to set the best price

of product that support to increase customer base.

P2 Different kind of management accounting report.

It is essential for the company to prepare the relevant and accurate accounting report that

ease for manager to make valuable decision for future growth. As information must be reliable,

accurate containing all relevant facts and figure which focuses on developing plan that can be

crucial for improving the entire performance of company. There are some main features of

reports such as:

Reliable: The complete information contained within report must be reliable so that uses

can take meaningful decision can be taken for improvement.

Time to Time: It is crucial for the manager to prepare report on regular basis so that each

information can be presented within reports (Kihn and Näsi, 2017).

Manner to prepare information

It is important to present the information that have been obtained with the help of

different systems of management accounting. Thus it is stated that reports must be

understandable to interested parties because this data mainly consider financial information that

is not easily managerial personnel’s. So in order to provide an accurate interpretation of

information, it is necessary that information must be understandable. Also such information must

be in comparative form and comprehend to provide ease in decision-making process.

There are various crucial reports that are prepared by manager of Grange Construction

Materials in order to record each business happening that ease the process of decision making.

Some of the valuable reports that are prepared within company are discussed below:

Performance report: This report is mainly concerned with recording of overall

performance of different operation and employees working with company. It makes easy for the

manager to figure out the actual efficiencies of worker which enable in attainment of goals. In

Grange Construction Materials this report help to examine the total performance of each worker

and determine the lacking if any, so that proper plans are prepared for better improvement.

Accounts receivable reports: In order to increase the sales volume by good margin

manager used to sales valuable product of company on credit basis. With the help of this report

manage are able to prepare and maintain proper record of list of customer those have purchased

4

of product that support to increase customer base.

P2 Different kind of management accounting report.

It is essential for the company to prepare the relevant and accurate accounting report that

ease for manager to make valuable decision for future growth. As information must be reliable,

accurate containing all relevant facts and figure which focuses on developing plan that can be

crucial for improving the entire performance of company. There are some main features of

reports such as:

Reliable: The complete information contained within report must be reliable so that uses

can take meaningful decision can be taken for improvement.

Time to Time: It is crucial for the manager to prepare report on regular basis so that each

information can be presented within reports (Kihn and Näsi, 2017).

Manner to prepare information

It is important to present the information that have been obtained with the help of

different systems of management accounting. Thus it is stated that reports must be

understandable to interested parties because this data mainly consider financial information that

is not easily managerial personnel’s. So in order to provide an accurate interpretation of

information, it is necessary that information must be understandable. Also such information must

be in comparative form and comprehend to provide ease in decision-making process.

There are various crucial reports that are prepared by manager of Grange Construction

Materials in order to record each business happening that ease the process of decision making.

Some of the valuable reports that are prepared within company are discussed below:

Performance report: This report is mainly concerned with recording of overall

performance of different operation and employees working with company. It makes easy for the

manager to figure out the actual efficiencies of worker which enable in attainment of goals. In

Grange Construction Materials this report help to examine the total performance of each worker

and determine the lacking if any, so that proper plans are prepared for better improvement.

Accounts receivable reports: In order to increase the sales volume by good margin

manager used to sales valuable product of company on credit basis. With the help of this report

manage are able to prepare and maintain proper record of list of customer those have purchased

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

goods on credit basis. Accounts receivable report aid manager of respective company to send

regular message to respective customer which help in collecting the amount.

Inventory report: The main motive of preparing this report is to track the total raw

material available in warehouse, goods involved in production process and total quantity that are

ready for sales (Maher, Stickney and Weil, 2012). In Grange construction materials with the help

of this report manager are able to contain each and every detail related with stock of company.

Some common method for valuation of the stock in respective company used by manager are

LIFO and FIFO so that there can be proper identification of the closing value of stock.

TASK 2

P3 Costing Techniques to prepare income statements.

Cost is the summation of all the expenses incurred by an organisation in creation and

selling of a product or service from scratch to the final product sold. There are various types of

costs and Grange construction materials takes all these costs in its purview to decide prices for its

products. Some of them are direct cost, indirect cost, fixed cost, variable cost, operating cost,

opportunity cost etc. Cost analysis is the concept of establishing cost-output relationship.

Cost volume profit: It is the method which studies the impact of variation of cost and

volume have on operating profit. GCM analysts use this method to determine the break even

point for its products.

Flexible budgeting: It is budgeting technique used by the management of GCM to

allocate resources to its factors of production according to the variable expenditures and the

degree of variability.

Cost variance: It is a system devised to control the variance level from the actual

expected level.

Cost allocation: It is the process of allocating costs to different factors of production that

work together to create a product. GCM analysts use this technique in financial reporting to

spread costs to the relevant input areas. Prominent methods of cost allocation are :

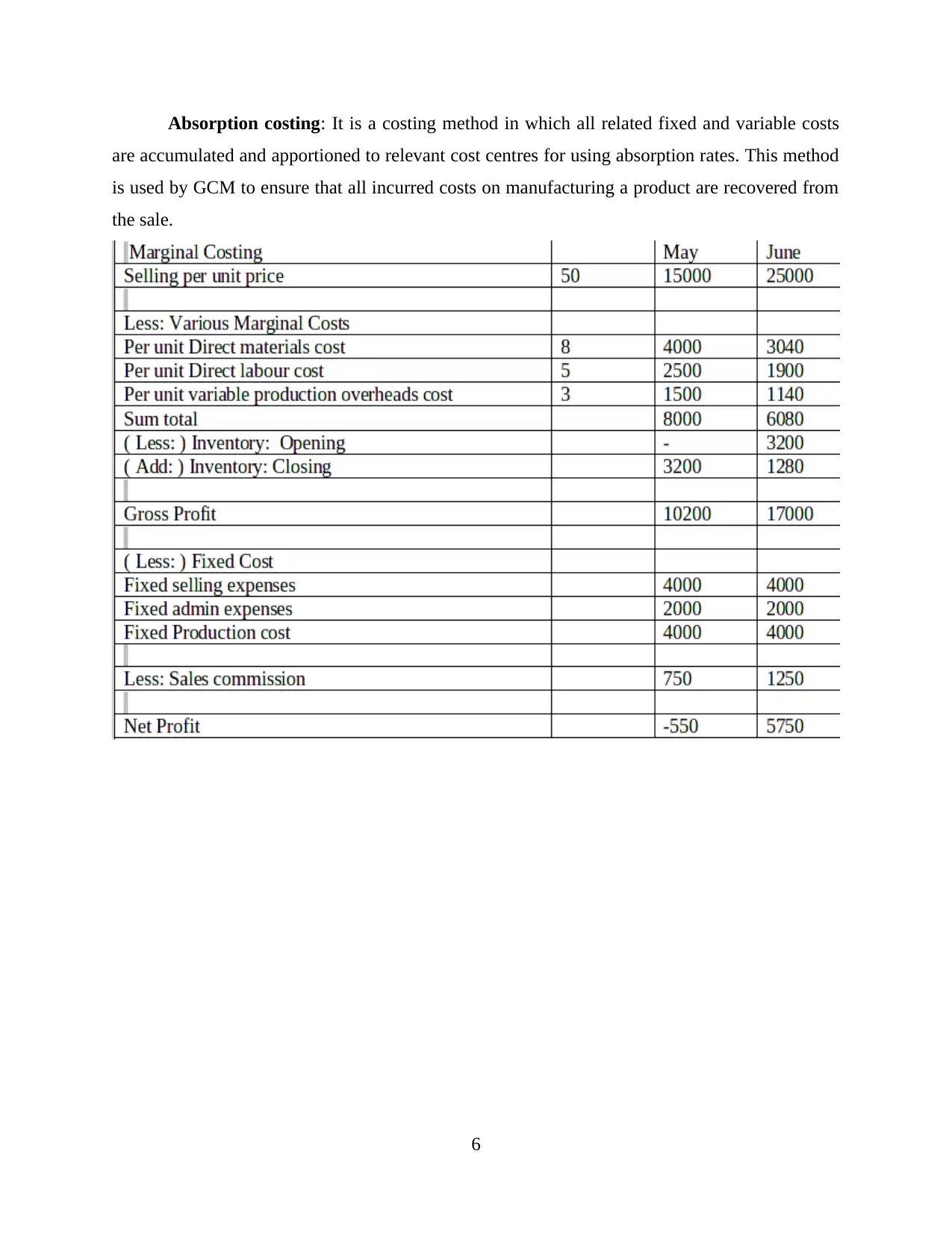

Marginal costing: It is a method under which all variable costs are taken as the cost of

the product and all fixed costs are taken as cost for the period. It takes only variable costs as cost

of the product (Malinić and Todorović, 2012).

5

regular message to respective customer which help in collecting the amount.

Inventory report: The main motive of preparing this report is to track the total raw

material available in warehouse, goods involved in production process and total quantity that are

ready for sales (Maher, Stickney and Weil, 2012). In Grange construction materials with the help

of this report manager are able to contain each and every detail related with stock of company.

Some common method for valuation of the stock in respective company used by manager are

LIFO and FIFO so that there can be proper identification of the closing value of stock.

TASK 2

P3 Costing Techniques to prepare income statements.

Cost is the summation of all the expenses incurred by an organisation in creation and

selling of a product or service from scratch to the final product sold. There are various types of

costs and Grange construction materials takes all these costs in its purview to decide prices for its

products. Some of them are direct cost, indirect cost, fixed cost, variable cost, operating cost,

opportunity cost etc. Cost analysis is the concept of establishing cost-output relationship.

Cost volume profit: It is the method which studies the impact of variation of cost and

volume have on operating profit. GCM analysts use this method to determine the break even

point for its products.

Flexible budgeting: It is budgeting technique used by the management of GCM to

allocate resources to its factors of production according to the variable expenditures and the

degree of variability.

Cost variance: It is a system devised to control the variance level from the actual

expected level.

Cost allocation: It is the process of allocating costs to different factors of production that

work together to create a product. GCM analysts use this technique in financial reporting to

spread costs to the relevant input areas. Prominent methods of cost allocation are :

Marginal costing: It is a method under which all variable costs are taken as the cost of

the product and all fixed costs are taken as cost for the period. It takes only variable costs as cost

of the product (Malinić and Todorović, 2012).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

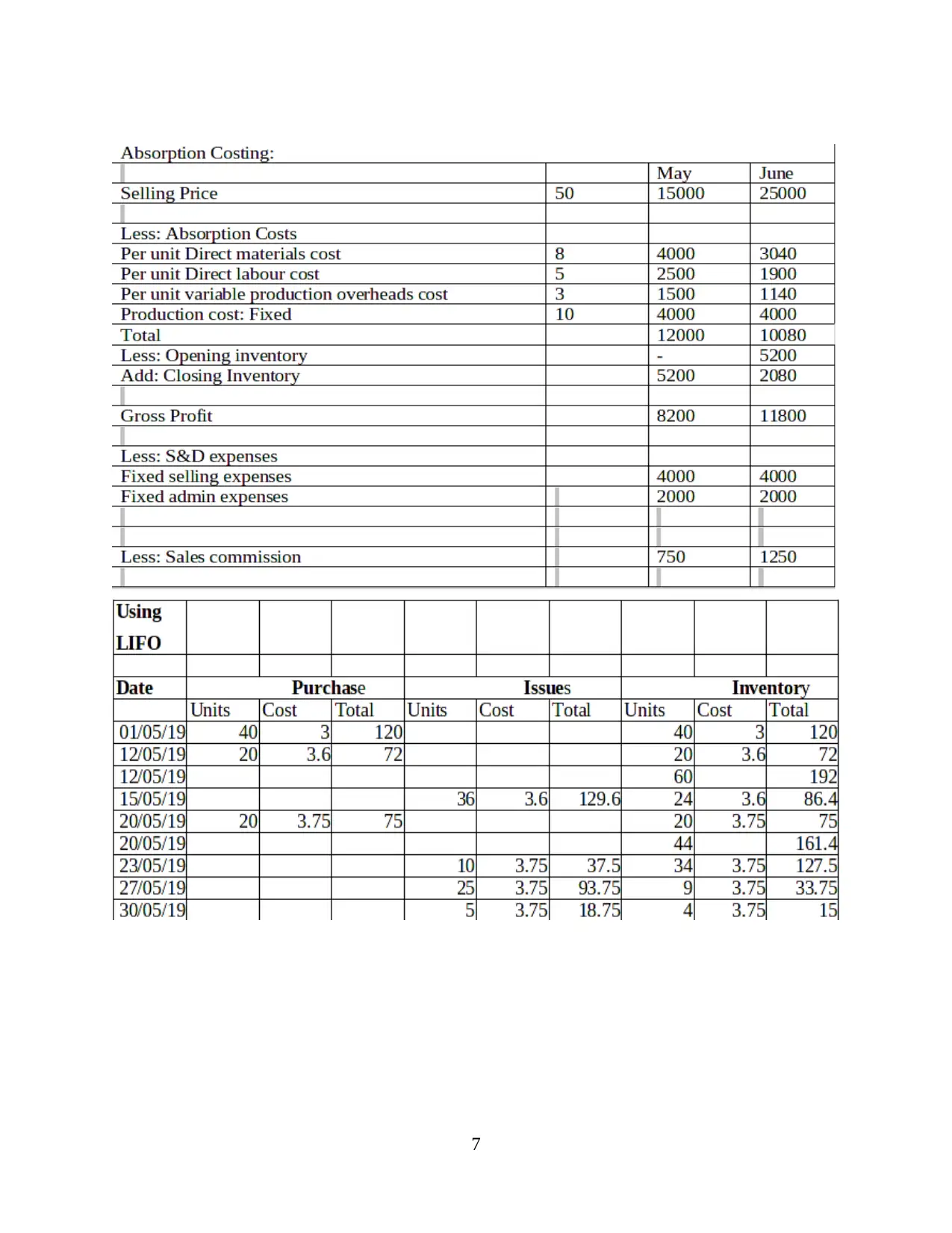

Absorption costing: It is a costing method in which all related fixed and variable costs

are accumulated and apportioned to relevant cost centres for using absorption rates. This method

is used by GCM to ensure that all incurred costs on manufacturing a product are recovered from

the sale.

6

are accumulated and apportioned to relevant cost centres for using absorption rates. This method

is used by GCM to ensure that all incurred costs on manufacturing a product are recovered from

the sale.

6

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

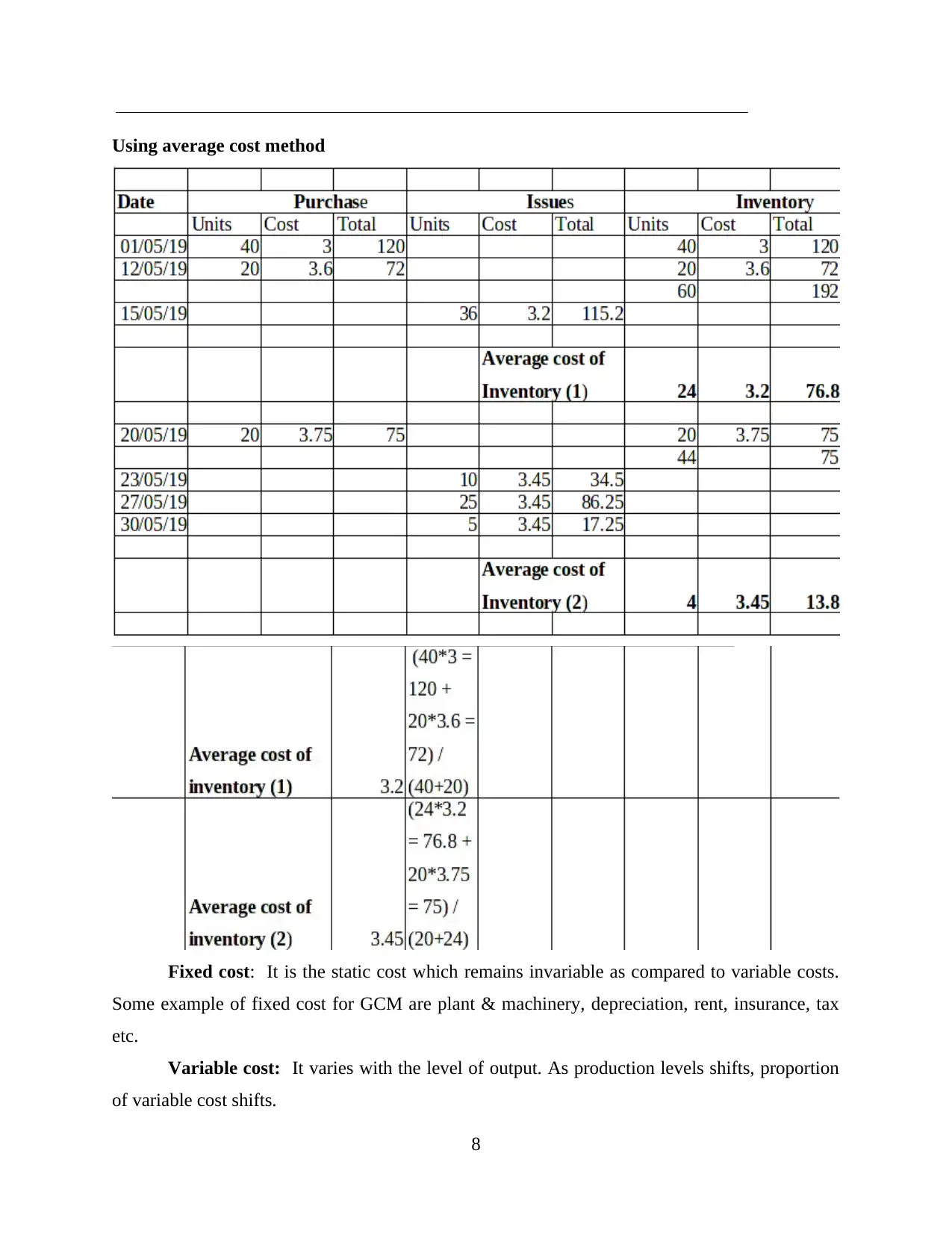

Using average cost method

Fixed cost: It is the static cost which remains invariable as compared to variable costs.

Some example of fixed cost for GCM are plant & machinery, depreciation, rent, insurance, tax

etc.

Variable cost: It varies with the level of output. As production levels shifts, proportion

of variable cost shifts.

8

Fixed cost: It is the static cost which remains invariable as compared to variable costs.

Some example of fixed cost for GCM are plant & machinery, depreciation, rent, insurance, tax

etc.

Variable cost: It varies with the level of output. As production levels shifts, proportion

of variable cost shifts.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Normal costing: It is used to derive the cost of a product. It covers factors like direct

labour, direct material, raw material and overheads.

Standard costing: It is used to to evaluate the variation between the actual results and

standards fixed for the cost as expected cost.

Activity based costing: It is a method of costing which assigns costs to all the factors

which goes into production. It considers all activities incidental to production inclusive.

Role of cost in price determination : Costing techniques allocates quantitative methods

to come to a price adding all fixed and variable inputs (McLaren, Appleyard and Mitchell,

2016).

Inventory cost: This is the cost related with the procurement, transportation and

supervision of inventory. It consists of costs like ordering cost, carrying cost, freight,

warehousing etc. It is used by GCM to determine expenses in managing stock at all times.

Benefit of reducing inventory cost is that it reduces the extra costs to the management

which can't be added to the product, hence would bear loss only. Reducing inventory would

mean more sales which is better sign for GCM.

Valuation methods: GCM has devised various methods to evaluate stock levels. Most

used one's are:

LIFO: Under this method costs of recent products which are purchased or produced is

considered as cost of goods sold. It means most recently produced goods will be sold first. It

stands as last in, first out.

FIFO: Under this method, costs of older inventory is considered first as cost of goods

sold irrespective of actual sale. It stands for first in , first out.

Overhead costs: These are the costs which are associated with day to day operations like

indirect material, indirect labour, and additional operating expenses which can't be assigned

directly to a given product or a cost centre. They are indirect in nature. GCM costing structure

has many overhead costs like manufacturing overhead, administration overhead, selling &

distribution overhead, fixed & variable overhead (Sadeghi and Jokar, 2014).

9

labour, direct material, raw material and overheads.

Standard costing: It is used to to evaluate the variation between the actual results and

standards fixed for the cost as expected cost.

Activity based costing: It is a method of costing which assigns costs to all the factors

which goes into production. It considers all activities incidental to production inclusive.

Role of cost in price determination : Costing techniques allocates quantitative methods

to come to a price adding all fixed and variable inputs (McLaren, Appleyard and Mitchell,

2016).

Inventory cost: This is the cost related with the procurement, transportation and

supervision of inventory. It consists of costs like ordering cost, carrying cost, freight,

warehousing etc. It is used by GCM to determine expenses in managing stock at all times.

Benefit of reducing inventory cost is that it reduces the extra costs to the management

which can't be added to the product, hence would bear loss only. Reducing inventory would

mean more sales which is better sign for GCM.

Valuation methods: GCM has devised various methods to evaluate stock levels. Most

used one's are:

LIFO: Under this method costs of recent products which are purchased or produced is

considered as cost of goods sold. It means most recently produced goods will be sold first. It

stands as last in, first out.

FIFO: Under this method, costs of older inventory is considered first as cost of goods

sold irrespective of actual sale. It stands for first in , first out.

Overhead costs: These are the costs which are associated with day to day operations like

indirect material, indirect labour, and additional operating expenses which can't be assigned

directly to a given product or a cost centre. They are indirect in nature. GCM costing structure

has many overhead costs like manufacturing overhead, administration overhead, selling &

distribution overhead, fixed & variable overhead (Sadeghi and Jokar, 2014).

9

TASK 3

P4 Advantages and disadvantages of different types of planning tools used for budgetary control

Budget: A budget is a formal financial statement which proposes monetary expenses and

incomes for a determined period. Process of creating a budget needs few systematic steps which

are as follows:

Examine the revenue situation.

Subtract fixed costs

Evaluate the persisting variable expenses.

Build a contingency fund for uncertain costs.

Prepare profit & loss statement.

Prepare an outline for a target budget.

Capital budget: It is a type of budget which is prepared for the fixed assets in an

organisation like plant & machinery, premises, research and development projects etc.

Advantages: Helps in understanding risks associated with a huge investment.

Helps to take long term strategic decisions.

Disadvantages: Long term and irreversible once taken.

High risk factor.

Operating budget: It is a statement which describes company's revenues, expenditures,

and costs for a given period of time.

Advantages: Helps in managing current expenses.

Creates financial reserves.

Disadvantages: May miss some important costs at times.

Adds extra cost burden.

Alternative methods of budgeting

Priority-Based budgeting: It is a budget based on the priority list from high to low based

on the subjective capacity (Tarmidi and et.al, 2014). All activities are set each time budget is

prepared.

Activity-Based budgeting: It is a budget which is mainly focused on activities that derives

cost to the company. It includes activities which are instrumental in making products.

Behavioural implications of budget

10

P4 Advantages and disadvantages of different types of planning tools used for budgetary control

Budget: A budget is a formal financial statement which proposes monetary expenses and

incomes for a determined period. Process of creating a budget needs few systematic steps which

are as follows:

Examine the revenue situation.

Subtract fixed costs

Evaluate the persisting variable expenses.

Build a contingency fund for uncertain costs.

Prepare profit & loss statement.

Prepare an outline for a target budget.

Capital budget: It is a type of budget which is prepared for the fixed assets in an

organisation like plant & machinery, premises, research and development projects etc.

Advantages: Helps in understanding risks associated with a huge investment.

Helps to take long term strategic decisions.

Disadvantages: Long term and irreversible once taken.

High risk factor.

Operating budget: It is a statement which describes company's revenues, expenditures,

and costs for a given period of time.

Advantages: Helps in managing current expenses.

Creates financial reserves.

Disadvantages: May miss some important costs at times.

Adds extra cost burden.

Alternative methods of budgeting

Priority-Based budgeting: It is a budget based on the priority list from high to low based

on the subjective capacity (Tarmidi and et.al, 2014). All activities are set each time budget is

prepared.

Activity-Based budgeting: It is a budget which is mainly focused on activities that derives

cost to the company. It includes activities which are instrumental in making products.

Behavioural implications of budget

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.