Management Accounting Report for Aon Consulting and Sewport Analysis

VerifiedAdded on 2021/02/20

|23

|4715

|364

Report

AI Summary

This report delves into the core concepts of management accounting, focusing on its application within Aon Consulting, a consultancy firm, and its client, Sewport, a designer clothing producer. The introduction establishes the role of management accounting in providing crucial insights for internal decision-making. Task 1 explores various management accounting systems, including cost accounting, inventory management, job costing, and price optimization, highlighting their benefits. It also examines different types of useful reports, such as management accounting reports, account receivable reports, budget reports, inventory management reports, and performance reports. Task 2 focuses on costing techniques, like cost-volume-profit analysis, flexible budgeting, cost variances, and marginal costing, used to prepare income statements and analyze financial performance. The report discusses the importance of these techniques in understanding and controlling costs, ultimately contributing to improved financial outcomes. Finally, the report concludes by summarizing the key findings and emphasizing the significance of management accounting in addressing financial issues and achieving organizational goals.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1Management accounting and different types of management accounting systems...........1

P2 Various types of useful reports..........................................................................................3

TASK 2............................................................................................................................................5

P3 Costing Techniques to prepare income statements...........................................................5

TASK 3..........................................................................................................................................10

P4 Advantages and disadvantage of different planning tool................................................10

TASK 4..........................................................................................................................................14

P5 Management accounting in response to overcome financial issues................................14

CONCLUSION..............................................................................................................................15

REFRENCES.................................................................................................................................17

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1Management accounting and different types of management accounting systems...........1

P2 Various types of useful reports..........................................................................................3

TASK 2............................................................................................................................................5

P3 Costing Techniques to prepare income statements...........................................................5

TASK 3..........................................................................................................................................10

P4 Advantages and disadvantage of different planning tool................................................10

TASK 4..........................................................................................................................................14

P5 Management accounting in response to overcome financial issues................................14

CONCLUSION..............................................................................................................................15

REFRENCES.................................................................................................................................17

INTRODUCTION

The concept of management accounting is relate with procedures that are deliberately

combines together in respect to give essential understanding and knowledge of business

operation to internal decision maker (Management Accounting, 2019). In general, the method of

determination, evaluation, examination, accumulation, interpretation and communication of

meaningful information that is further used by manager to measure, control and maximise the

best possible use of resources in order to increase profit, but overall to accomplish the business

strategy. In this project, Aon Consulting, is selected that is a average size consultancy firm that

is providing consultancy service to Sewport is selected that have main operation producing

designer cloths.

In scenario 1 of this assignment various reports and system of management accounting

are discussed. This reports also covers various costing methods in order to determine the net

profit and prepare income statement. On the other side in scenarios 2 various planning tool are

used to prepare budgets and management accounting system are implemented to overcome

financial issues.

TASK 1

P1Management accounting and different types of management accounting systems.

Management accounting: The concept of management accounting is related with

controlling, monitoring the business activities so business can be more efficient in the term of

effective planning and business action. It is a process that give financial information to

management of company so they can make accurate decision for better control of the organisation.

Some of the crucial kind of system are discussed below:

The concept of management accounting was started with the review of cost accounting

development from 1850 through and the use of double entry bookkeeping have been used for

more than 300 year by the very first time emerged as a recognized filed.

Principle of management accounting

The concept of management accounting is relate with procedures that are deliberately

combines together in respect to give essential understanding and knowledge of business

operation to internal decision maker (Management Accounting, 2019). In general, the method of

determination, evaluation, examination, accumulation, interpretation and communication of

meaningful information that is further used by manager to measure, control and maximise the

best possible use of resources in order to increase profit, but overall to accomplish the business

strategy. In this project, Aon Consulting, is selected that is a average size consultancy firm that

is providing consultancy service to Sewport is selected that have main operation producing

designer cloths.

In scenario 1 of this assignment various reports and system of management accounting

are discussed. This reports also covers various costing methods in order to determine the net

profit and prepare income statement. On the other side in scenarios 2 various planning tool are

used to prepare budgets and management accounting system are implemented to overcome

financial issues.

TASK 1

P1Management accounting and different types of management accounting systems.

Management accounting: The concept of management accounting is related with

controlling, monitoring the business activities so business can be more efficient in the term of

effective planning and business action. It is a process that give financial information to

management of company so they can make accurate decision for better control of the organisation.

Some of the crucial kind of system are discussed below:

The concept of management accounting was started with the review of cost accounting

development from 1850 through and the use of double entry bookkeeping have been used for

more than 300 year by the very first time emerged as a recognized filed.

Principle of management accounting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

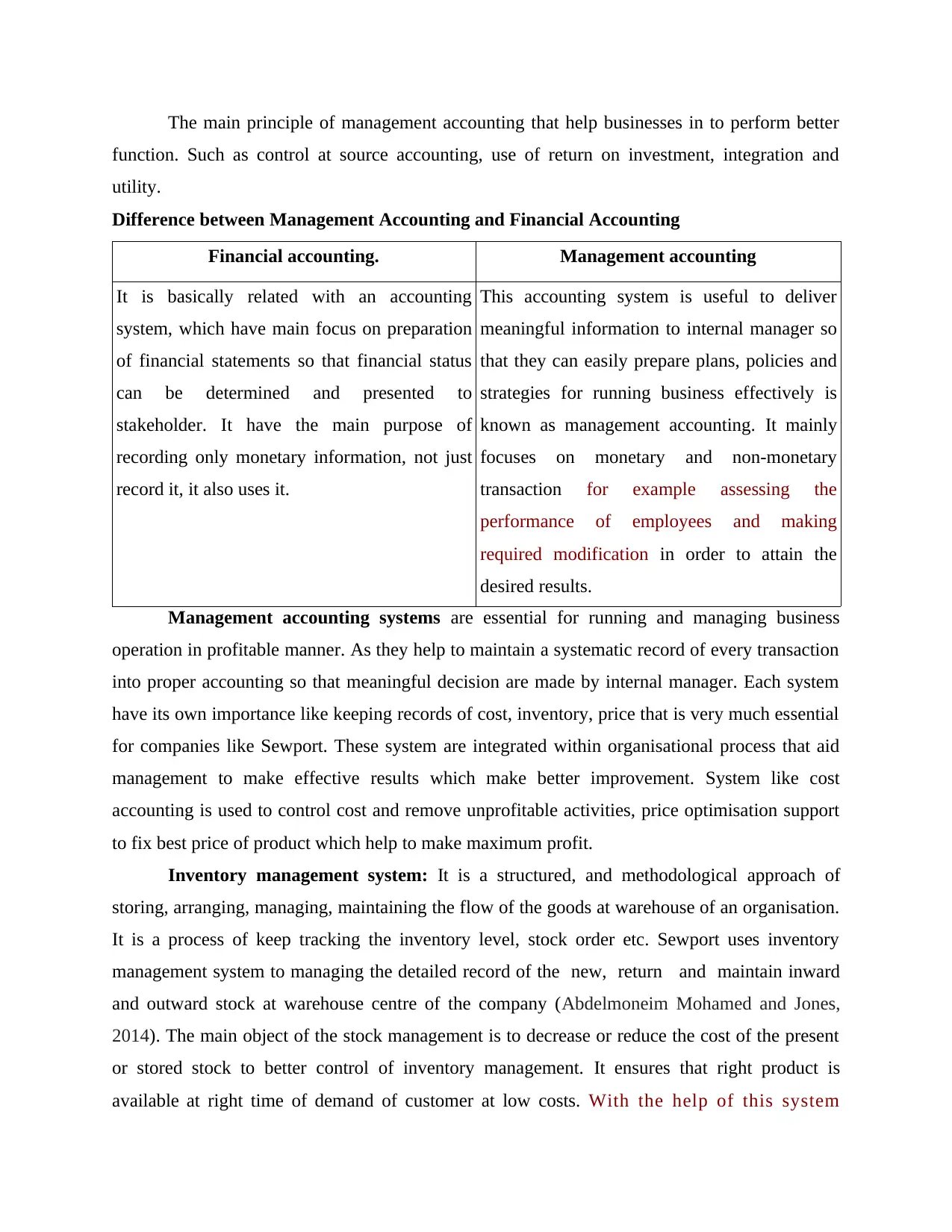

The main principle of management accounting that help businesses in to perform better

function. Such as control at source accounting, use of return on investment, integration and

utility.

Difference between Management Accounting and Financial Accounting

Financial accounting. Management accounting

It is basically related with an accounting

system, which have main focus on preparation

of financial statements so that financial status

can be determined and presented to

stakeholder. It have the main purpose of

recording only monetary information, not just

record it, it also uses it.

This accounting system is useful to deliver

meaningful information to internal manager so

that they can easily prepare plans, policies and

strategies for running business effectively is

known as management accounting. It mainly

focuses on monetary and non-monetary

transaction for example assessing the

performance of employees and making

required modification in order to attain the

desired results.

Management accounting systems are essential for running and managing business

operation in profitable manner. As they help to maintain a systematic record of every transaction

into proper accounting so that meaningful decision are made by internal manager. Each system

have its own importance like keeping records of cost, inventory, price that is very much essential

for companies like Sewport. These system are integrated within organisational process that aid

management to make effective results which make better improvement. System like cost

accounting is used to control cost and remove unprofitable activities, price optimisation support

to fix best price of product which help to make maximum profit.

Inventory management system: It is a structured, and methodological approach of

storing, arranging, managing, maintaining the flow of the goods at warehouse of an organisation.

It is a process of keep tracking the inventory level, stock order etc. Sewport uses inventory

management system to managing the detailed record of the new, return and maintain inward

and outward stock at warehouse centre of the company (Abdelmoneim Mohamed and Jones,

2014). The main object of the stock management is to decrease or reduce the cost of the present

or stored stock to better control of inventory management. It ensures that right product is

available at right time of demand of customer at low costs. With the help of this system

function. Such as control at source accounting, use of return on investment, integration and

utility.

Difference between Management Accounting and Financial Accounting

Financial accounting. Management accounting

It is basically related with an accounting

system, which have main focus on preparation

of financial statements so that financial status

can be determined and presented to

stakeholder. It have the main purpose of

recording only monetary information, not just

record it, it also uses it.

This accounting system is useful to deliver

meaningful information to internal manager so

that they can easily prepare plans, policies and

strategies for running business effectively is

known as management accounting. It mainly

focuses on monetary and non-monetary

transaction for example assessing the

performance of employees and making

required modification in order to attain the

desired results.

Management accounting systems are essential for running and managing business

operation in profitable manner. As they help to maintain a systematic record of every transaction

into proper accounting so that meaningful decision are made by internal manager. Each system

have its own importance like keeping records of cost, inventory, price that is very much essential

for companies like Sewport. These system are integrated within organisational process that aid

management to make effective results which make better improvement. System like cost

accounting is used to control cost and remove unprofitable activities, price optimisation support

to fix best price of product which help to make maximum profit.

Inventory management system: It is a structured, and methodological approach of

storing, arranging, managing, maintaining the flow of the goods at warehouse of an organisation.

It is a process of keep tracking the inventory level, stock order etc. Sewport uses inventory

management system to managing the detailed record of the new, return and maintain inward

and outward stock at warehouse centre of the company (Abdelmoneim Mohamed and Jones,

2014). The main object of the stock management is to decrease or reduce the cost of the present

or stored stock to better control of inventory management. It ensures that right product is

available at right time of demand of customer at low costs. With the help of this system

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

manager are able to modify their business strategy in order to maximise the

management of raw material and finished goods of company to make huge profit.

Cost accounting system: Sewport uses this report to monitor the production costs that

incurred at particular location. It also help to evaluate accurate cost of the inventory that help to

assess the total production cost for a specific time frame. Manager of respective firm are able to

control excess expenses due to which performance of other operation gets impacted, they are also

able to determine the non-profitable activities and remove them which ensure the proper

utilisation of resources to maximise profit margin. This system assess the input cost of material

at every step like raw material, work in progress and trading, delivering these goods at certain

price are helpful to maintaining the profit and cost control activities in the Sewport.

Job costing system: This system includes the process of assigning or gather the cost

associated manufacturing outcome of a particular units. Sewport normally using this method to

analyse the different items that are produced in same manufacturing unit are specifically

contrasting with each other and also each has its particular cost. The cost information from

warehouse department is also useful to determine the deciding maximum retail price that enables

Sewport to gain a reasonable profit (Bagautdinova, Kundakchyan and Malakhov, 2013).

Price optimisation system: This system of management accounting is practical model

that calculate how the product or item demand vary the price of the product at certain level.

Sewport decide the product price as per the basis of the production cost but it may vary on the

manufacturing scale of the unit. Price optimisation system can be used by the Sewport to decide

the price for particular customer division by imitating how a target customer will respond with

these price alteration in current market plan. With best suitable prices company are able to

increase sales volume and expand customer base to remain successful in competitive

environment.(Good)

Benefits of different system.

System Benefits

Cost Accounting system This system help in determination of cost by

dominating unpredicted expenses.

Inventory Management System It help company to gain reputation in market

due to its reliable supply.

management of raw material and finished goods of company to make huge profit.

Cost accounting system: Sewport uses this report to monitor the production costs that

incurred at particular location. It also help to evaluate accurate cost of the inventory that help to

assess the total production cost for a specific time frame. Manager of respective firm are able to

control excess expenses due to which performance of other operation gets impacted, they are also

able to determine the non-profitable activities and remove them which ensure the proper

utilisation of resources to maximise profit margin. This system assess the input cost of material

at every step like raw material, work in progress and trading, delivering these goods at certain

price are helpful to maintaining the profit and cost control activities in the Sewport.

Job costing system: This system includes the process of assigning or gather the cost

associated manufacturing outcome of a particular units. Sewport normally using this method to

analyse the different items that are produced in same manufacturing unit are specifically

contrasting with each other and also each has its particular cost. The cost information from

warehouse department is also useful to determine the deciding maximum retail price that enables

Sewport to gain a reasonable profit (Bagautdinova, Kundakchyan and Malakhov, 2013).

Price optimisation system: This system of management accounting is practical model

that calculate how the product or item demand vary the price of the product at certain level.

Sewport decide the product price as per the basis of the production cost but it may vary on the

manufacturing scale of the unit. Price optimisation system can be used by the Sewport to decide

the price for particular customer division by imitating how a target customer will respond with

these price alteration in current market plan. With best suitable prices company are able to

increase sales volume and expand customer base to remain successful in competitive

environment.(Good)

Benefits of different system.

System Benefits

Cost Accounting system This system help in determination of cost by

dominating unpredicted expenses.

Inventory Management System It help company to gain reputation in market

due to its reliable supply.

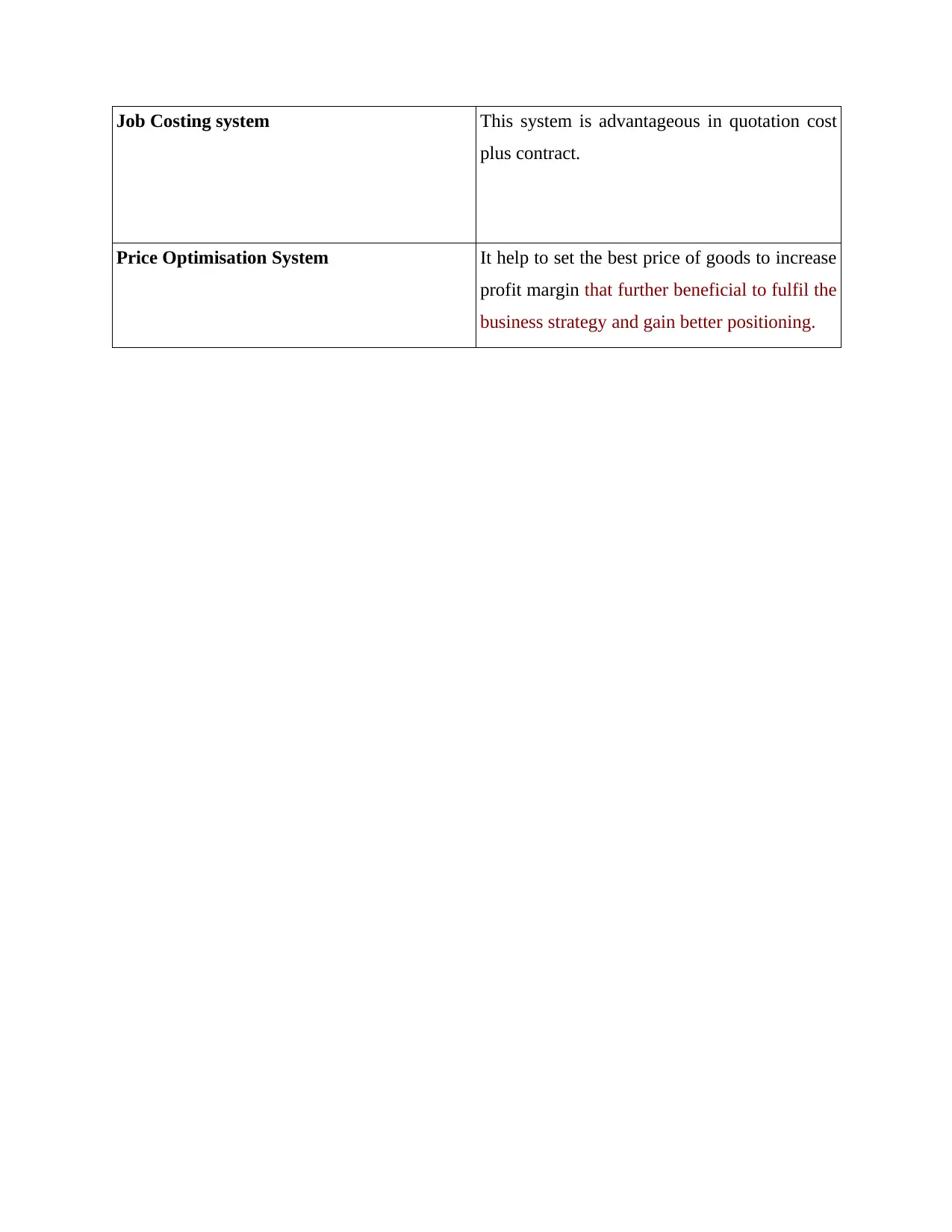

Job Costing system This system is advantageous in quotation cost

plus contract.

Price Optimisation System It help to set the best price of goods to increase

profit margin that further beneficial to fulfil the

business strategy and gain better positioning.

plus contract.

Price Optimisation System It help to set the best price of goods to increase

profit margin that further beneficial to fulfil the

business strategy and gain better positioning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P2 Various types of useful reports.

There are different methods used for management accounting reporting that are being

used in Sewport. These reports have meaningful characteristic which makes them relevant for

user such as:

Reliability: This means that all those items that are presented in report must be reliable

and can be verified or can be consistently used by investors and creditors in order to make

valuable investment or lending decision. It is that attribute which license users of data to count

upon it with assurance as representative of what it intent to represent.

Accuracy: The report presented for the period must be precise in all context so that any

types of error or misrepresentation's can be solved at initial stage.

The concepts of understandability states that information presented in financial reports

must be easy to read and understandable by user so that investment decision are made by

different interested stakeholder. In respective company, manager prepare all reports so that actual

performance can be easily understandable by the other stakeholder of company. These report are

essential for company as they provide the detail information about the overall financial position

of business which are defined underneath:

Management accounting reporting: This report is includes the detailed financial

information that provided by the head of the department to firm's manager in order to handling

day to day business activities (Bloomfield, 2015). Sewport uses this report to make short term

There are different methods used for management accounting reporting that are being

used in Sewport. These reports have meaningful characteristic which makes them relevant for

user such as:

Reliability: This means that all those items that are presented in report must be reliable

and can be verified or can be consistently used by investors and creditors in order to make

valuable investment or lending decision. It is that attribute which license users of data to count

upon it with assurance as representative of what it intent to represent.

Accuracy: The report presented for the period must be precise in all context so that any

types of error or misrepresentation's can be solved at initial stage.

The concepts of understandability states that information presented in financial reports

must be easy to read and understandable by user so that investment decision are made by

different interested stakeholder. In respective company, manager prepare all reports so that actual

performance can be easily understandable by the other stakeholder of company. These report are

essential for company as they provide the detail information about the overall financial position

of business which are defined underneath:

Management accounting reporting: This report is includes the detailed financial

information that provided by the head of the department to firm's manager in order to handling

day to day business activities (Bloomfield, 2015). Sewport uses this report to make short term

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial decision with the help of internal stakeholder in term of conducting the business

operations. These financial reports and information help to management in formulating and

implementing the business strategies.

Account receivable report: This report shows the unpaid customer list in books of

accounts of the organisation. In Sewport, account receivable report is initiated by the

management to determine the over due payment from its customers or how much amount need to

cover from debtors. This report provide strength to the credit policy of company as they can

make more sales on credit basis in case if customer are paying outstanding amount on accurate

date and time.

Budget report: This report is generated by the management of an organization to

compare the data related to estimation of the budget and actual result. Sewport company

basically prepare this report to verify the conducted business activities are able to perform as per

the set standard. In case of any deficit, proper action are made against those operational activities

due to which company was unable to produce budgeted targets.

Inventory management Report : This report is used to track the actual output of goods

sold, inward unit at warehouse, stock details, inventory level. Sewport management generates

this on quarterly basis to track the real time goods movement in the manufacturing units. There

are the certain method for valuation of the stock such as LIFO,FIFO and weighted average

method to identification of the closing stock value.

Performance report: This is detailed report which is being prepared by manager in

order to measure the efficiency and overall performance of particular functions, operation and

worker within an origination (Collis and Hussey, 2017). Sewport management formulated this

report to analysis the current performance with previous years data. This report is made to

analysis the achievement of workers in order to complete the given task in certain time period

and contribution made by them in achieving the business objects too.

TASK 2

P3 Costing Techniques to prepare income statements.

Cost is defined as an amount that which have to be paid by the buyer in order to buy

something for seller. In term of business cost in something that is usually a monetary valuation

of efforts, material and resources. There are different kind of cost that are needed to be consider

operations. These financial reports and information help to management in formulating and

implementing the business strategies.

Account receivable report: This report shows the unpaid customer list in books of

accounts of the organisation. In Sewport, account receivable report is initiated by the

management to determine the over due payment from its customers or how much amount need to

cover from debtors. This report provide strength to the credit policy of company as they can

make more sales on credit basis in case if customer are paying outstanding amount on accurate

date and time.

Budget report: This report is generated by the management of an organization to

compare the data related to estimation of the budget and actual result. Sewport company

basically prepare this report to verify the conducted business activities are able to perform as per

the set standard. In case of any deficit, proper action are made against those operational activities

due to which company was unable to produce budgeted targets.

Inventory management Report : This report is used to track the actual output of goods

sold, inward unit at warehouse, stock details, inventory level. Sewport management generates

this on quarterly basis to track the real time goods movement in the manufacturing units. There

are the certain method for valuation of the stock such as LIFO,FIFO and weighted average

method to identification of the closing stock value.

Performance report: This is detailed report which is being prepared by manager in

order to measure the efficiency and overall performance of particular functions, operation and

worker within an origination (Collis and Hussey, 2017). Sewport management formulated this

report to analysis the current performance with previous years data. This report is made to

analysis the achievement of workers in order to complete the given task in certain time period

and contribution made by them in achieving the business objects too.

TASK 2

P3 Costing Techniques to prepare income statements.

Cost is defined as an amount that which have to be paid by the buyer in order to buy

something for seller. In term of business cost in something that is usually a monetary valuation

of efforts, material and resources. There are different kind of cost that are needed to be consider

by Sewport such as Fixed, variable, Direct, indirect, product, period cost. Cost analysis is used

by manager to analyse the overall cost so that actual financial position of company can be

determined.

Cost-volume profit: It is one of the most valuable analyse that is used in Sewport to

ascertain the change in cost and volume of production which affect the production revenue and

net income. There are some assumption to made while performing this analysis Sales price,

variable price and total per unit is constant.

Flexible budgeting: It is related to the techniques that is used by management of

Sewport to see the impact of operation on different level of output so that profit can be

maximised.

Cost variances: It is related with the difference among the actual cost spend on different

operation and budgeted cost for specific period. This variance is consider to be main portion of

standard costing system that is used by Sewport.

Marginal costing: The above costing method is virtually linked to the substantive

method wherein marginal cost is invoiced to the maximum unit of cost, while on the other side

variable cost is write off over a given period of time toward overall contribution over a period. It

primarily means the increased cost used in the production of an extra item. The equation for

calculating costs of production to analyse the credible net revenue outcome for a particular time

span.

Absorption Costing: It is linked to the accounting techniques also recognized as

organizational or price accounting that use to provide all costs associated with both the

production of a particular product and product cost. it is crucial for internal GAAP disclosure. It

involves alike varied as well as fixed costs such as salaries, raw material costs and other

overheads linked to the price foundation of producing an item.

Cost allocation: It is related to methods of determining and assigning of cost to different

product within organization. In respective company it is used for financial reporting that aid to

spread cost between different section or stock items. There are different types of cost that are

elaborated below:

Fixed Cost: This kind of cost do not changes with the changes in the level of output and

are also know overheads cost. In case Sewport either manufacture 100 piece or 1000 piece these

cost are fixed same for the specific period.

by manager to analyse the overall cost so that actual financial position of company can be

determined.

Cost-volume profit: It is one of the most valuable analyse that is used in Sewport to

ascertain the change in cost and volume of production which affect the production revenue and

net income. There are some assumption to made while performing this analysis Sales price,

variable price and total per unit is constant.

Flexible budgeting: It is related to the techniques that is used by management of

Sewport to see the impact of operation on different level of output so that profit can be

maximised.

Cost variances: It is related with the difference among the actual cost spend on different

operation and budgeted cost for specific period. This variance is consider to be main portion of

standard costing system that is used by Sewport.

Marginal costing: The above costing method is virtually linked to the substantive

method wherein marginal cost is invoiced to the maximum unit of cost, while on the other side

variable cost is write off over a given period of time toward overall contribution over a period. It

primarily means the increased cost used in the production of an extra item. The equation for

calculating costs of production to analyse the credible net revenue outcome for a particular time

span.

Absorption Costing: It is linked to the accounting techniques also recognized as

organizational or price accounting that use to provide all costs associated with both the

production of a particular product and product cost. it is crucial for internal GAAP disclosure. It

involves alike varied as well as fixed costs such as salaries, raw material costs and other

overheads linked to the price foundation of producing an item.

Cost allocation: It is related to methods of determining and assigning of cost to different

product within organization. In respective company it is used for financial reporting that aid to

spread cost between different section or stock items. There are different types of cost that are

elaborated below:

Fixed Cost: This kind of cost do not changes with the changes in the level of output and

are also know overheads cost. In case Sewport either manufacture 100 piece or 1000 piece these

cost are fixed same for the specific period.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variable Cost: On the other side these cost changes with the fluctuation in the level of

production. In Sewport, cost of labour, material are variable cost that raise as the volume of

production increase.

Normal costing: It is used to mechanism the total cost of a commodity that includes the

respective components such as actual cost of material, labour. This methods is used in Sewport

to implement the actual cost to various goods and overheads rates.

Standard costing: It is related with substituting an awaited cost for an actual cost within

the annual reports. In Sewport, setting alternative variance is done to display the difference

among actual and expected costs.

Activity based costing: It is one of the best accounting process that identify and assigns

cost to each overheads function and then allocate these costs to respective goods of Sewport.

All these cost are helpful in fixing best possible price of product by controlling the

expenses incurred on manufacturing different cloths in Sewport.

Inventory cost: This type of costs are mainly connected with storage, procurements and

managing of goods within company. These are categorise in three crucial parts such as ordering

cost, carrying cost and out of stock or replenishment cost. It is very much important for Sewport

to reduce these cost as it increase the profit and make sure that saved amount in spend on other

crucial activities.

Valuation methods: There are different types of stock valuation methods that are

adopted by Sewport which increases the level of production and grow business (Bromiley and

et.al, 2015). Such as

LIFO: It is related with making of goods from the raw material that was brought last,

which help in clearing of storehouse and delivering goods at regular basis.

FIFO: This is related with manufacturing of goods from raw material that was first, so

that company production process keeps on going.

Overhead: This consider an ongoing business expenses that are not related with direct

labour or material that are used in creating valuable product. In context of Sewport some

overheads cost are rent, insurance, office supplies, salaries that are not related with product

specific.

Income statement under Marginal costing method for month of May & June

Particular May June

(in £) (in £)

production. In Sewport, cost of labour, material are variable cost that raise as the volume of

production increase.

Normal costing: It is used to mechanism the total cost of a commodity that includes the

respective components such as actual cost of material, labour. This methods is used in Sewport

to implement the actual cost to various goods and overheads rates.

Standard costing: It is related with substituting an awaited cost for an actual cost within

the annual reports. In Sewport, setting alternative variance is done to display the difference

among actual and expected costs.

Activity based costing: It is one of the best accounting process that identify and assigns

cost to each overheads function and then allocate these costs to respective goods of Sewport.

All these cost are helpful in fixing best possible price of product by controlling the

expenses incurred on manufacturing different cloths in Sewport.

Inventory cost: This type of costs are mainly connected with storage, procurements and

managing of goods within company. These are categorise in three crucial parts such as ordering

cost, carrying cost and out of stock or replenishment cost. It is very much important for Sewport

to reduce these cost as it increase the profit and make sure that saved amount in spend on other

crucial activities.

Valuation methods: There are different types of stock valuation methods that are

adopted by Sewport which increases the level of production and grow business (Bromiley and

et.al, 2015). Such as

LIFO: It is related with making of goods from the raw material that was brought last,

which help in clearing of storehouse and delivering goods at regular basis.

FIFO: This is related with manufacturing of goods from raw material that was first, so

that company production process keeps on going.

Overhead: This consider an ongoing business expenses that are not related with direct

labour or material that are used in creating valuable product. In context of Sewport some

overheads cost are rent, insurance, office supplies, salaries that are not related with product

specific.

Income statement under Marginal costing method for month of May & June

Particular May June

(in £) (in £)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

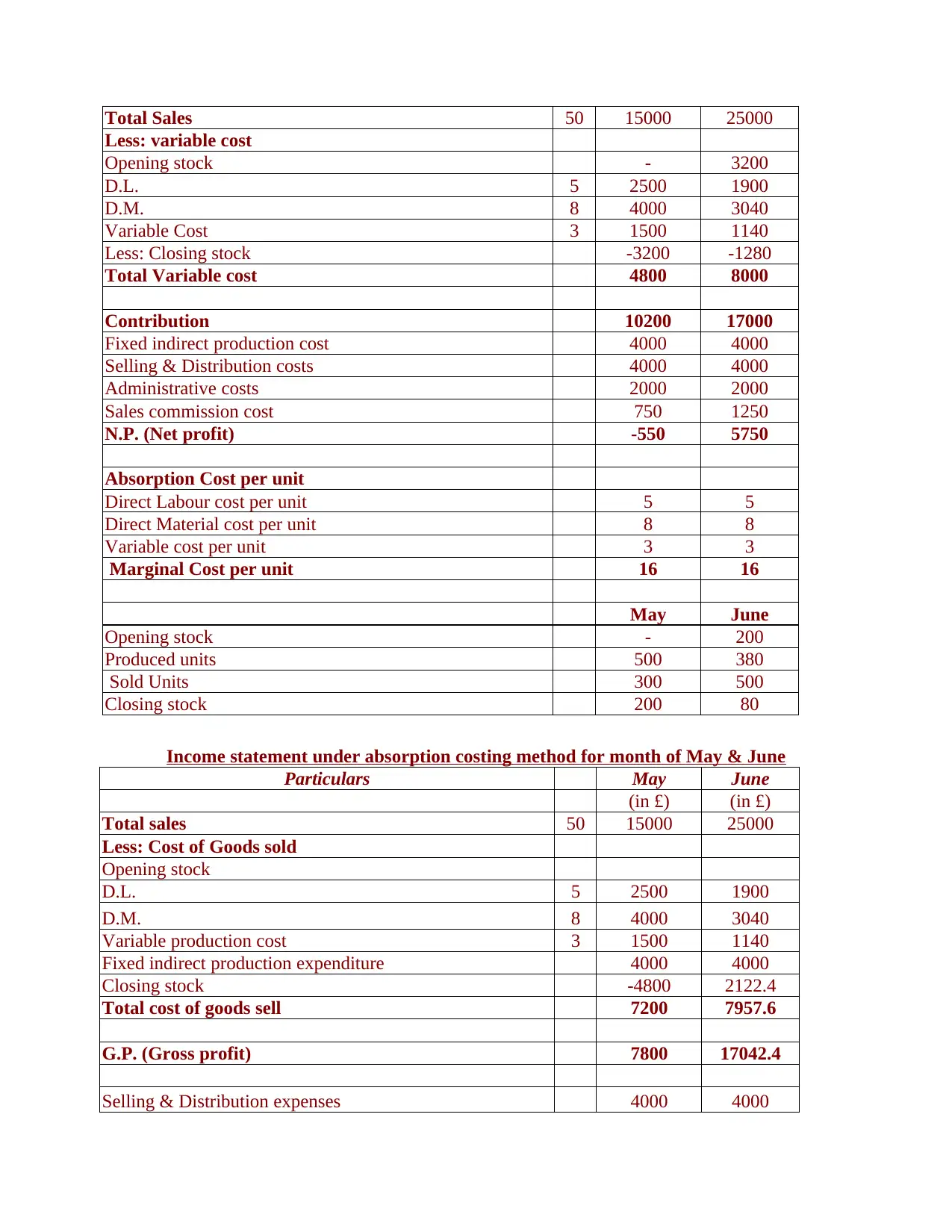

Total Sales 50 15000 25000

Less: variable cost

Opening stock - 3200

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable Cost 3 1500 1140

Less: Closing stock -3200 -1280

Total Variable cost 4800 8000

Contribution 10200 17000

Fixed indirect production cost 4000 4000

Selling & Distribution costs 4000 4000

Administrative costs 2000 2000

Sales commission cost 750 1250

N.P. (Net profit) -550 5750

Absorption Cost per unit

Direct Labour cost per unit 5 5

Direct Material cost per unit 8 8

Variable cost per unit 3 3

Marginal Cost per unit 16 16

May June

Opening stock - 200

Produced units 500 380

Sold Units 300 500

Closing stock 200 80

Income statement under absorption costing method for month of May & June

Particulars May June

(in £) (in £)

Total sales 50 15000 25000

Less: Cost of Goods sold

Opening stock

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable production cost 3 1500 1140

Fixed indirect production expenditure 4000 4000

Closing stock -4800 2122.4

Total cost of goods sell 7200 7957.6

G.P. (Gross profit) 7800 17042.4

Selling & Distribution expenses 4000 4000

Less: variable cost

Opening stock - 3200

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable Cost 3 1500 1140

Less: Closing stock -3200 -1280

Total Variable cost 4800 8000

Contribution 10200 17000

Fixed indirect production cost 4000 4000

Selling & Distribution costs 4000 4000

Administrative costs 2000 2000

Sales commission cost 750 1250

N.P. (Net profit) -550 5750

Absorption Cost per unit

Direct Labour cost per unit 5 5

Direct Material cost per unit 8 8

Variable cost per unit 3 3

Marginal Cost per unit 16 16

May June

Opening stock - 200

Produced units 500 380

Sold Units 300 500

Closing stock 200 80

Income statement under absorption costing method for month of May & June

Particulars May June

(in £) (in £)

Total sales 50 15000 25000

Less: Cost of Goods sold

Opening stock

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable production cost 3 1500 1140

Fixed indirect production expenditure 4000 4000

Closing stock -4800 2122.4

Total cost of goods sell 7200 7957.6

G.P. (Gross profit) 7800 17042.4

Selling & Distribution expenses 4000 4000

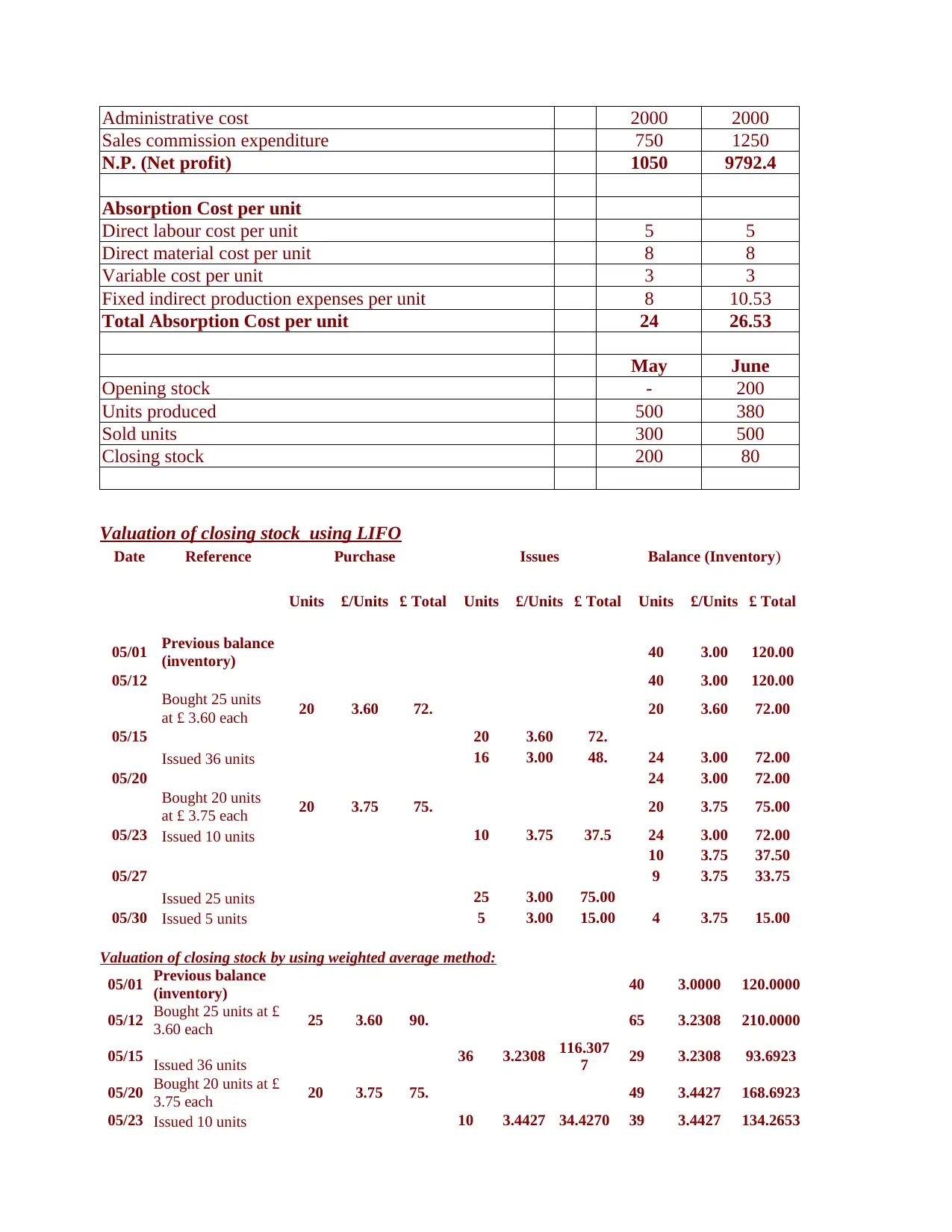

Administrative cost 2000 2000

Sales commission expenditure 750 1250

N.P. (Net profit) 1050 9792.4

Absorption Cost per unit

Direct labour cost per unit 5 5

Direct material cost per unit 8 8

Variable cost per unit 3 3

Fixed indirect production expenses per unit 8 10.53

Total Absorption Cost per unit 24 26.53

May June

Opening stock - 200

Units produced 500 380

Sold units 300 500

Closing stock 200 80

Valuation of closing stock using LIFO

Date Reference Purchase Issues Balance (Inventory)

Units £/Units £ Total Units £/Units £ Total Units £/Units £ Total

05/01 Previous balance

(inventory) 40 3.00 120.00

05/12 40 3.00 120.00

Bought 25 units

at £ 3.60 each 20 3.60 72. 20 3.60 72.00

05/15 20 3.60 72.

Issued 36 units 16 3.00 48. 24 3.00 72.00

05/20 24 3.00 72.00

Bought 20 units

at £ 3.75 each 20 3.75 75. 20 3.75 75.00

05/23 Issued 10 units 10 3.75 37.5 24 3.00 72.00

10 3.75 37.50

05/27 9 3.75 33.75

Issued 25 units 25 3.00 75.00

05/30 Issued 5 units 5 3.00 15.00 4 3.75 15.00

Valuation of closing stock by using weighted average method:

05/01 Previous balance

(inventory) 40 3.0000 120.0000

05/12 Bought 25 units at £

3.60 each 25 3.60 90. 65 3.2308 210.0000

05/15 Issued 36 units 36 3.2308 116.307

7 29 3.2308 93.6923

05/20 Bought 20 units at £

3.75 each 20 3.75 75. 49 3.4427 168.6923

05/23 Issued 10 units 10 3.4427 34.4270 39 3.4427 134.2653

Sales commission expenditure 750 1250

N.P. (Net profit) 1050 9792.4

Absorption Cost per unit

Direct labour cost per unit 5 5

Direct material cost per unit 8 8

Variable cost per unit 3 3

Fixed indirect production expenses per unit 8 10.53

Total Absorption Cost per unit 24 26.53

May June

Opening stock - 200

Units produced 500 380

Sold units 300 500

Closing stock 200 80

Valuation of closing stock using LIFO

Date Reference Purchase Issues Balance (Inventory)

Units £/Units £ Total Units £/Units £ Total Units £/Units £ Total

05/01 Previous balance

(inventory) 40 3.00 120.00

05/12 40 3.00 120.00

Bought 25 units

at £ 3.60 each 20 3.60 72. 20 3.60 72.00

05/15 20 3.60 72.

Issued 36 units 16 3.00 48. 24 3.00 72.00

05/20 24 3.00 72.00

Bought 20 units

at £ 3.75 each 20 3.75 75. 20 3.75 75.00

05/23 Issued 10 units 10 3.75 37.5 24 3.00 72.00

10 3.75 37.50

05/27 9 3.75 33.75

Issued 25 units 25 3.00 75.00

05/30 Issued 5 units 5 3.00 15.00 4 3.75 15.00

Valuation of closing stock by using weighted average method:

05/01 Previous balance

(inventory) 40 3.0000 120.0000

05/12 Bought 25 units at £

3.60 each 25 3.60 90. 65 3.2308 210.0000

05/15 Issued 36 units 36 3.2308 116.307

7 29 3.2308 93.6923

05/20 Bought 20 units at £

3.75 each 20 3.75 75. 49 3.4427 168.6923

05/23 Issued 10 units 10 3.4427 34.4270 39 3.4427 134.2653

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.