Analysis and Application of Management Accounting Techniques

VerifiedAdded on 2023/06/15

|9

|2082

|69

Report

AI Summary

This report provides a comprehensive overview of management accounting, its integration with management accounting reporting systems, and the benefits of its application within an organizational context. It explains the principles of management accounting, emphasizing the importance of integrating management accounting systems. The report also details various techniques and methods used for management accounting reporting, such as margin analysis, constraint analysis, capital budgeting, and trend analysis. Furthermore, it includes the preparation and interpretation of income statements using marginal and absorption costing techniques. The study concludes that management accounting is crucial for providing insights that help management in analyzing, interpreting, and making informed decisions, thereby enhancing financial management and control within a company. Desklib offers a wide range of study resources, including solved assignments and past papers, to support students in their academic endeavors.

Application of

Management

Accounting

Management

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

Management Accounting and Its Integration with Management Accounting Reporting System.

.....................................................................................................................................................4

An evaluation of the benefits of the Management Accounting systems and their application

within an organisational context..................................................................................................4

An explanation of the principles of management accounting and why it is important to

integrate management accounting systems within an organisation. You are also asked to

provide an explanation of different techniques and methods used for management accounting

reporting.......................................................................................................................................5

Different Techniques and Methods Used For Management Accounting Reporting...................6

Prepare and interpret accurate income statements for the company using a range of

management accounting techniques, such as marginal and absorption costs..............................7

Profit statements using Absorption costing.............................................................................7

Profit statements using Marginal costing................................................................................8

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

Books & Journals.........................................................................................................................9

Introduction......................................................................................................................................3

Management Accounting and Its Integration with Management Accounting Reporting System.

.....................................................................................................................................................4

An evaluation of the benefits of the Management Accounting systems and their application

within an organisational context..................................................................................................4

An explanation of the principles of management accounting and why it is important to

integrate management accounting systems within an organisation. You are also asked to

provide an explanation of different techniques and methods used for management accounting

reporting.......................................................................................................................................5

Different Techniques and Methods Used For Management Accounting Reporting...................6

Prepare and interpret accurate income statements for the company using a range of

management accounting techniques, such as marginal and absorption costs..............................7

Profit statements using Absorption costing.............................................................................7

Profit statements using Marginal costing................................................................................8

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

Books & Journals.........................................................................................................................9

Introduction

Management accounting is a type of management accounting that encompasses the process of

presenting financial data as well as all of the resources needed by an organization's manager to

make decisions. This accounting system provides statistical data that assists managers in doing

various tasks such as making better and more accurate decisions and controlling corporate

activity. Managerial accounting is primarily employed by the organization's internal team,

making it a distinct concept from financial accounting. It aids in the development of executive

financial statements in order to make short and long-term decisions in order to achieve

organisational objectives. It also aids managers in determining product or service prices by

supplying all relevant information such as market conditions, profitability, and so on.

Management accounting is a type of management accounting that encompasses the process of

presenting financial data as well as all of the resources needed by an organization's manager to

make decisions. This accounting system provides statistical data that assists managers in doing

various tasks such as making better and more accurate decisions and controlling corporate

activity. Managerial accounting is primarily employed by the organization's internal team,

making it a distinct concept from financial accounting. It aids in the development of executive

financial statements in order to make short and long-term decisions in order to achieve

organisational objectives. It also aids managers in determining product or service prices by

supplying all relevant information such as market conditions, profitability, and so on.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting and Its Integration with Management Accounting Reporting System.

Management accounting is the ability to recognize, measuring, analysing, summarizing, and

evaluating data presented to managers in order for them to make key company choices. One of

the main goals is to keep track of the costs involved with the production of goods or services for

the organization. Managerial accounting delivers quantitative and qualitative data on operational

and financial performance to businesses (Xie, 2019). While accounting information is concerned

with how creditors and others use this information to evaluate performance by making choices,

managerial accounting is concerned with how owners, managers, and employees use it

internally. The systems that organisations build to control and plan operations and support good

decision-making are referred to as a firm's accounting management system. Standard finance

reporting has aspects that make it valuable to both shareholders and creditors while also limiting

its applicability to a wider audience. Financial statements, which are only focused on historical

financial outcomes, are created in a standard format from period to period and contain identical

information across business sub-groups. Management accounting is an important concept which

is used by almost all the companies in order to manage the use of money in a planned and

efficient way (Phornlaphatrachakorn, 2019). The management accounting system and

management accounting reporting is related to each other because they are interdependent on

each other. In context to Synergy Manufacturing Ltd., an effective management accounting

reporting system should be developed and maintained so that the accounting system should also

be used in a proper manner. This will ultimately help in improvising the company's performance.

It is highly important for this organization to use the integration if the management accounting

and the management accounting reporting system in an effective way so that the organization can

achieve the organization goal in an effective manner.

An evaluation of the benefits of the Management Accounting systems and their application

within an organisational context.

Some benefits of management accounting with their applications are mentioned below:

Management Accounting System Benefit Application

Cost accounting system Measuring and improving

efficiency.

With the use of cost accounting

system, Synergy Manufacturing

Ltd., can measure its efficiency

Management accounting is the ability to recognize, measuring, analysing, summarizing, and

evaluating data presented to managers in order for them to make key company choices. One of

the main goals is to keep track of the costs involved with the production of goods or services for

the organization. Managerial accounting delivers quantitative and qualitative data on operational

and financial performance to businesses (Xie, 2019). While accounting information is concerned

with how creditors and others use this information to evaluate performance by making choices,

managerial accounting is concerned with how owners, managers, and employees use it

internally. The systems that organisations build to control and plan operations and support good

decision-making are referred to as a firm's accounting management system. Standard finance

reporting has aspects that make it valuable to both shareholders and creditors while also limiting

its applicability to a wider audience. Financial statements, which are only focused on historical

financial outcomes, are created in a standard format from period to period and contain identical

information across business sub-groups. Management accounting is an important concept which

is used by almost all the companies in order to manage the use of money in a planned and

efficient way (Phornlaphatrachakorn, 2019). The management accounting system and

management accounting reporting is related to each other because they are interdependent on

each other. In context to Synergy Manufacturing Ltd., an effective management accounting

reporting system should be developed and maintained so that the accounting system should also

be used in a proper manner. This will ultimately help in improvising the company's performance.

It is highly important for this organization to use the integration if the management accounting

and the management accounting reporting system in an effective way so that the organization can

achieve the organization goal in an effective manner.

An evaluation of the benefits of the Management Accounting systems and their application

within an organisational context.

Some benefits of management accounting with their applications are mentioned below:

Management Accounting System Benefit Application

Cost accounting system Measuring and improving

efficiency.

With the use of cost accounting

system, Synergy Manufacturing

Ltd., can measure its efficiency

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

in relation to cost, time, efforts

etc. It can also compare the actual

figures with the economy

standards to increase its

efficiency levels.

Inventory Management

System

Avoiding stock outs and excess

stocks.

A better planning and

management of inventory system

will help Synergy

Manufacturing Ltd., to avoid

the stock outs as well as the

wastage of the food stock.

Job Order Cost Accounting

System

Keep track of individuals

and team performance.

This accounting system will

benefit the managers of Synergy

Manufacturing Ltd., to keep a

check on the performance in

order to maintain high level of

efficiency and productivity.

An explanation of the principles of management accounting and why it is important to integrate

management accounting systems within an organisation. You are also asked to provide an

explanation of different techniques and methods used for management accounting

reporting.

Management accounting principles (MAP) were created to help integrated reporting enhance

management information objectives, internal operations, financial application, customer value,

and capacity utilisation in order to meet corporate goals in the most efficient way possible (Scott,

2019). There are various importance of the principles of management accounting and they are

mentioned below in different points:

Planning: Financial and non-financial information is delivered to management at regular

intervals, such as weekly or fortnightly, in management accounting. Forecasts, budgets,

and in-depth analysis are included in this presentation. As a result, it aids management in

the planning of corporate activities.

etc. It can also compare the actual

figures with the economy

standards to increase its

efficiency levels.

Inventory Management

System

Avoiding stock outs and excess

stocks.

A better planning and

management of inventory system

will help Synergy

Manufacturing Ltd., to avoid

the stock outs as well as the

wastage of the food stock.

Job Order Cost Accounting

System

Keep track of individuals

and team performance.

This accounting system will

benefit the managers of Synergy

Manufacturing Ltd., to keep a

check on the performance in

order to maintain high level of

efficiency and productivity.

An explanation of the principles of management accounting and why it is important to integrate

management accounting systems within an organisation. You are also asked to provide an

explanation of different techniques and methods used for management accounting

reporting.

Management accounting principles (MAP) were created to help integrated reporting enhance

management information objectives, internal operations, financial application, customer value,

and capacity utilisation in order to meet corporate goals in the most efficient way possible (Scott,

2019). There are various importance of the principles of management accounting and they are

mentioned below in different points:

Planning: Financial and non-financial information is delivered to management at regular

intervals, such as weekly or fortnightly, in management accounting. Forecasts, budgets,

and in-depth analysis are included in this presentation. As a result, it aids management in

the planning of corporate activities.

Making decisions: Management accounting is used for decision-making since it provides

numerous charts, projections, and analyses. This helps in keeping a high level of

efficiency along with the essence of effectivity.

Recognize warning indications of an issue early on: Because the accounts are supplied

at regular periods, management may detect if a product is performing poorly early on.

This will help overcome limits early on and prevent losses in the future (Saeidi and

Othman, 2017).

Management at the strategic level: Management can make recommendations on

whether to keep a product or change the sales approach based on the facts supplied in

management accounting. Because management accounting is not governed by any laws,

management can determine which areas deserve additional research and investigation and

develop plans appropriately.

Different Techniques and Methods Used For Management Accounting Reporting

Management accounting reporting is regarded as a vital and necessary component of any

business. It essentially paints a picture of how well a company is operating. This is a method of

showcasing a company's current financial situation across a certain time period (Krishnan, 2020).

Accounting records are used to compile all financial information relating to the organisation.

Additionally, these reports aid in the making of critical business decisions. Management

accounting reporting can be done in a variety of ways, as listed below:

• Margin analysis: The most significant analysis in managerial accounting is the margin

analysis. This analysis aids in establishing the break-even level so that production

processes can be optimised. It is primarily concerned with determining the best sales mix

for the company's goods. It is crucial in determining what additional advantages can be

obtained using the same resources and actions. The corporation uses margin analysis as a

way of management accounting reporting in order to optimize profitability.

Analysis of Constraints: This form of study focuses on the bottlenecks that exist within

a company. Because bottlenecks have complete power over a company's profitability, an

organization's focus should be on maximising bottleneck utilisation. The profitability will

be unaffected if the focus is kept on other aspects. Bottlenecks can be found almost

anywhere, thus it's a vital idea to understand (Burritt and Christ, 2017).

numerous charts, projections, and analyses. This helps in keeping a high level of

efficiency along with the essence of effectivity.

Recognize warning indications of an issue early on: Because the accounts are supplied

at regular periods, management may detect if a product is performing poorly early on.

This will help overcome limits early on and prevent losses in the future (Saeidi and

Othman, 2017).

Management at the strategic level: Management can make recommendations on

whether to keep a product or change the sales approach based on the facts supplied in

management accounting. Because management accounting is not governed by any laws,

management can determine which areas deserve additional research and investigation and

develop plans appropriately.

Different Techniques and Methods Used For Management Accounting Reporting

Management accounting reporting is regarded as a vital and necessary component of any

business. It essentially paints a picture of how well a company is operating. This is a method of

showcasing a company's current financial situation across a certain time period (Krishnan, 2020).

Accounting records are used to compile all financial information relating to the organisation.

Additionally, these reports aid in the making of critical business decisions. Management

accounting reporting can be done in a variety of ways, as listed below:

• Margin analysis: The most significant analysis in managerial accounting is the margin

analysis. This analysis aids in establishing the break-even level so that production

processes can be optimised. It is primarily concerned with determining the best sales mix

for the company's goods. It is crucial in determining what additional advantages can be

obtained using the same resources and actions. The corporation uses margin analysis as a

way of management accounting reporting in order to optimize profitability.

Analysis of Constraints: This form of study focuses on the bottlenecks that exist within

a company. Because bottlenecks have complete power over a company's profitability, an

organization's focus should be on maximising bottleneck utilisation. The profitability will

be unaffected if the focus is kept on other aspects. Bottlenecks can be found almost

anywhere, thus it's a vital idea to understand (Burritt and Christ, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Capital Budgeting: This strategy is concerned with the examination of information that

is extremely important in making decisions about capital expenditures. It primarily entails

the computation of NPV (Net Present Value) and IRR (Internal Rate of Return), which

aids finance managers in making capital budgeting decisions.

Trend analysis and forecasting: This is a strategy or a procedure for predicting current

trends based on historical trend data. This study is based on past data, which aids in

anticipating future patterns. This essentially focuses on present trends in order to

anticipate future ones through comparative research. It also contains a number of tactics

that might aid an organisation in determining current and upcoming trends through

forecasting (Hutaibat and Alhatabat, 2020).

Prepare and interpret accurate income statements for the company using a range of management

accounting techniques, such as marginal and absorption costs.

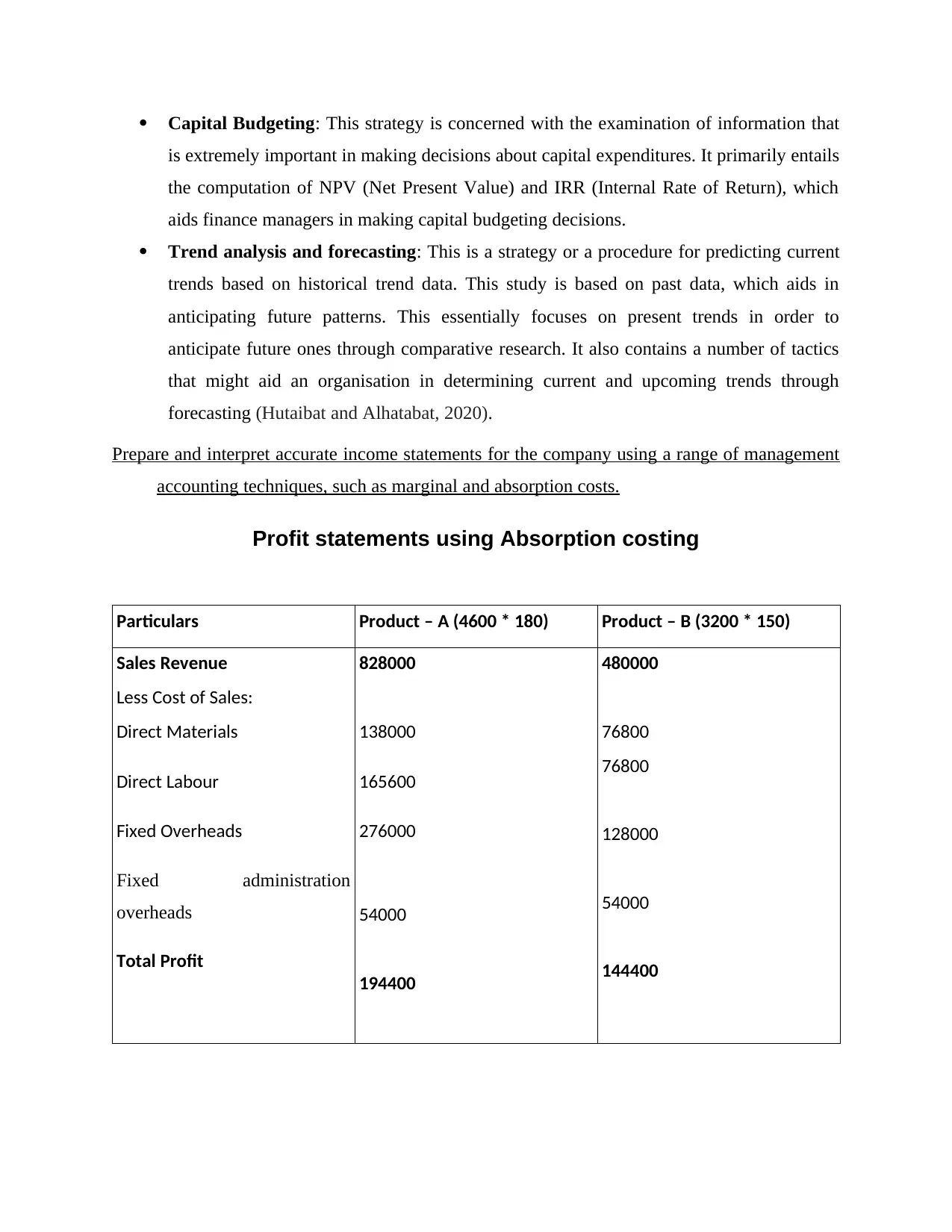

Profit statements using Absorption costing

Particulars Product – A (4600 * 180) Product – B (3200 * 150)

Sales Revenue

Less Cost of Sales:

Direct Materials

Direct Labour

Fixed Overheads

Fixed administration

overheads

Total Profit

828000

138000

165600

276000

54000

194400

480000

76800

76800

128000

54000

144400

is extremely important in making decisions about capital expenditures. It primarily entails

the computation of NPV (Net Present Value) and IRR (Internal Rate of Return), which

aids finance managers in making capital budgeting decisions.

Trend analysis and forecasting: This is a strategy or a procedure for predicting current

trends based on historical trend data. This study is based on past data, which aids in

anticipating future patterns. This essentially focuses on present trends in order to

anticipate future ones through comparative research. It also contains a number of tactics

that might aid an organisation in determining current and upcoming trends through

forecasting (Hutaibat and Alhatabat, 2020).

Prepare and interpret accurate income statements for the company using a range of management

accounting techniques, such as marginal and absorption costs.

Profit statements using Absorption costing

Particulars Product – A (4600 * 180) Product – B (3200 * 150)

Sales Revenue

Less Cost of Sales:

Direct Materials

Direct Labour

Fixed Overheads

Fixed administration

overheads

Total Profit

828000

138000

165600

276000

54000

194400

480000

76800

76800

128000

54000

144400

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

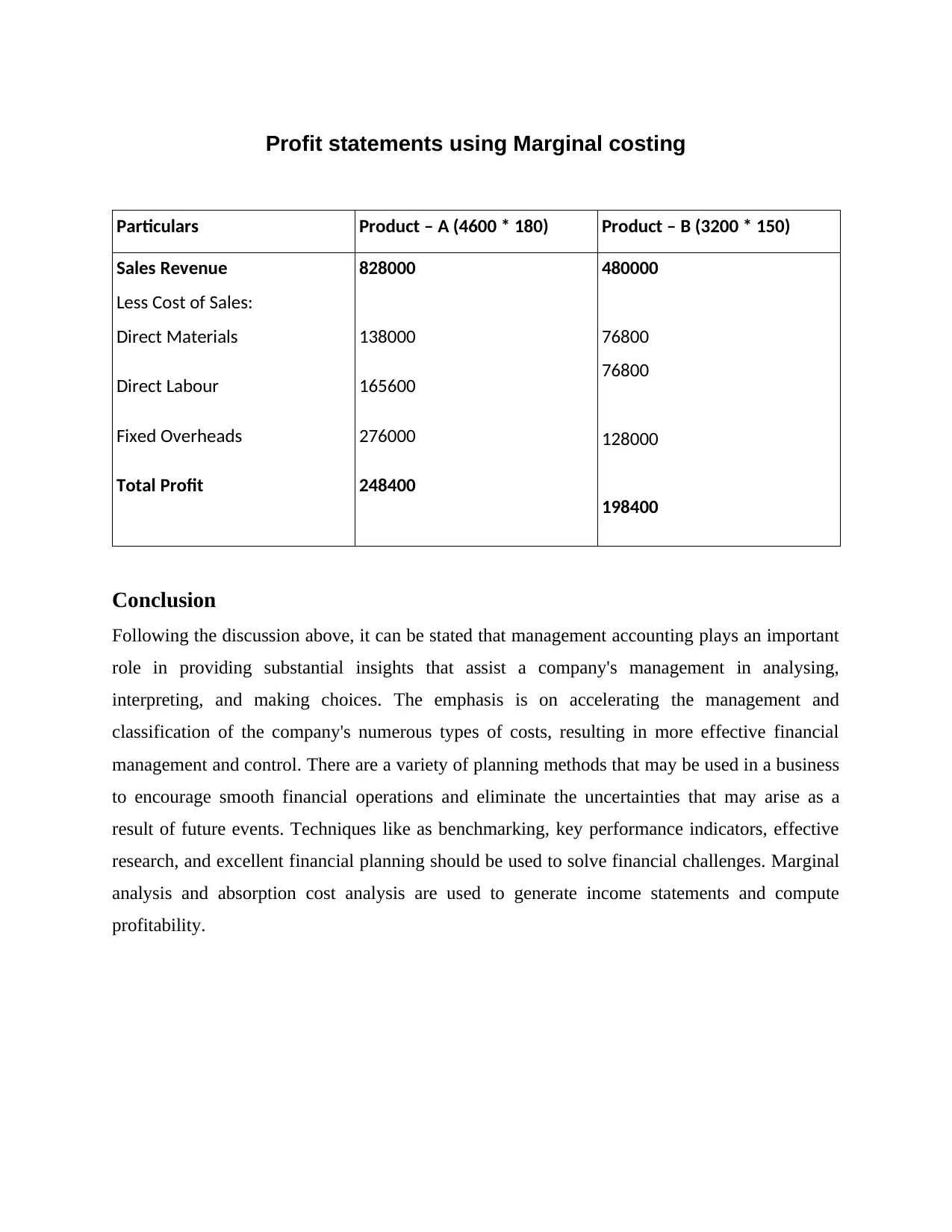

Profit statements using Marginal costing

Particulars Product – A (4600 * 180) Product – B (3200 * 150)

Sales Revenue

Less Cost of Sales:

Direct Materials

Direct Labour

Fixed Overheads

Total Profit

828000

138000

165600

276000

248400

480000

76800

76800

128000

198400

Conclusion

Following the discussion above, it can be stated that management accounting plays an important

role in providing substantial insights that assist a company's management in analysing,

interpreting, and making choices. The emphasis is on accelerating the management and

classification of the company's numerous types of costs, resulting in more effective financial

management and control. There are a variety of planning methods that may be used in a business

to encourage smooth financial operations and eliminate the uncertainties that may arise as a

result of future events. Techniques like as benchmarking, key performance indicators, effective

research, and excellent financial planning should be used to solve financial challenges. Marginal

analysis and absorption cost analysis are used to generate income statements and compute

profitability.

Particulars Product – A (4600 * 180) Product – B (3200 * 150)

Sales Revenue

Less Cost of Sales:

Direct Materials

Direct Labour

Fixed Overheads

Total Profit

828000

138000

165600

276000

248400

480000

76800

76800

128000

198400

Conclusion

Following the discussion above, it can be stated that management accounting plays an important

role in providing substantial insights that assist a company's management in analysing,

interpreting, and making choices. The emphasis is on accelerating the management and

classification of the company's numerous types of costs, resulting in more effective financial

management and control. There are a variety of planning methods that may be used in a business

to encourage smooth financial operations and eliminate the uncertainties that may arise as a

result of future events. Techniques like as benchmarking, key performance indicators, effective

research, and excellent financial planning should be used to solve financial challenges. Marginal

analysis and absorption cost analysis are used to generate income statements and compute

profitability.

References

Books & Journals

Xie, B., 2019. Westliche Management-Accounting-Instrumente in China. Springer Fachmedien

Wiesbaden.

Phornlaphatrachakorn, K., 2019. Influences of strategic management accounting on firm

profitability of information and communication technology businesses in

Thailand. International Journal of Business Excellence, 17(2), pp.131-153.

Scott, P., 2019. Introduction to Management Accounting. Oxford University Press, USA.

Saeidi, S. P. and Othman, M. S. H., 2017. The mediating role of process and product innovation

in the relationship between environmental management accounting and firm's financial

performance. International Journal of Business Innovation and Research, 14(4), pp.421-

438.

Krishnan, R., 2020. Across the Great Divide: Bridging the Gap between Economics-and

Sociology-Based Research on Management Accounting. Journal of Management

Accounting Research, 32(2), pp.21-25.

Burritt, R. L. and Christ, K. L., 2017. The need for monetary information within corporate water

accounting. Journal of environmental management, 201, pp.72-81.

Hutaibat, K. and Alhatabat, Z., 2020. Management accounting practices’ adoption in UK

universities. Journal of Further and Higher Education, 44(8), pp.1024-1038.

Samuel, S., 2018. A conceptual framework for teaching management accounting. Journal of

Accounting Education, 44, pp.25-34.

Avelé, D., 2021. Between management accounting tools and analysis of the performance of

municipal public services: a case study. African Journal of Economic and Sustainable

Development, 8(4), pp.319-339.

(Xie, 2019)(Phornlaphatrachakorn, 2019)(Scott, 2019)(Saeidi and Othman, 2017)(Krishnan,

2020)(Burritt and Christ, 2017)(Hutaibat and Alhatabat, 2020)(Samuel, 2018)(Avelé, 2021)

Books & Journals

Xie, B., 2019. Westliche Management-Accounting-Instrumente in China. Springer Fachmedien

Wiesbaden.

Phornlaphatrachakorn, K., 2019. Influences of strategic management accounting on firm

profitability of information and communication technology businesses in

Thailand. International Journal of Business Excellence, 17(2), pp.131-153.

Scott, P., 2019. Introduction to Management Accounting. Oxford University Press, USA.

Saeidi, S. P. and Othman, M. S. H., 2017. The mediating role of process and product innovation

in the relationship between environmental management accounting and firm's financial

performance. International Journal of Business Innovation and Research, 14(4), pp.421-

438.

Krishnan, R., 2020. Across the Great Divide: Bridging the Gap between Economics-and

Sociology-Based Research on Management Accounting. Journal of Management

Accounting Research, 32(2), pp.21-25.

Burritt, R. L. and Christ, K. L., 2017. The need for monetary information within corporate water

accounting. Journal of environmental management, 201, pp.72-81.

Hutaibat, K. and Alhatabat, Z., 2020. Management accounting practices’ adoption in UK

universities. Journal of Further and Higher Education, 44(8), pp.1024-1038.

Samuel, S., 2018. A conceptual framework for teaching management accounting. Journal of

Accounting Education, 44, pp.25-34.

Avelé, D., 2021. Between management accounting tools and analysis of the performance of

municipal public services: a case study. African Journal of Economic and Sustainable

Development, 8(4), pp.319-339.

(Xie, 2019)(Phornlaphatrachakorn, 2019)(Scott, 2019)(Saeidi and Othman, 2017)(Krishnan,

2020)(Burritt and Christ, 2017)(Hutaibat and Alhatabat, 2020)(Samuel, 2018)(Avelé, 2021)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.