Management Accounting Systems and Techniques for Aridri Company

VerifiedAdded on 2020/12/09

|17

|4666

|346

Report

AI Summary

This report provides a comprehensive overview of management accounting systems and techniques, focusing on their application within the context of a manufacturing company, Aridri. The report begins with an introduction to management accounting, its types, and its significance for business planning and control, particularly for small organizations. It then delves into specific methods, including price optimization, job costing, cost accounting, and inventory management systems, highlighting their benefits. The report further examines management accounting reporting, covering budgeting, job cost, and inventory reports, alongside their integration within organizational processes. A key section of the report focuses on cost calculations, preparing income statements using both marginal and absorption costing methods, and includes a break-even analysis. The report also analyzes different planning tools for budgetary control, evaluating their advantages and disadvantages, and explores how organizations adapt management accounting systems to resolve financial problems, culminating in an evaluation of how planning tools respond to solve financial problems.

Management Accounting

Systems & Techniques

Systems & Techniques

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its different types....................................................................1

P2 Methods for management accounting Reporting...................................................................3

M1 Benefits of management accounting system........................................................................4

D1 Critical evaluation on management accounting report integrated within organisational

process.........................................................................................................................................4

TASK 2............................................................................................................................................4

P3 Cost calculations to prepare an income statement ................................................................4

M2 A range of management accounting techniques...................................................................7

D2 Analysis and Interpretation of data.......................................................................................8

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of different types of planning tools for budgetary control...8

M3 Analysis on use of different planning tool for preparing and forecasting budgets...............9

TASK 4............................................................................................................................................9

P5 Comparison on how organizations are adapting management accounting system to resolve

financial problems.......................................................................................................................9

M4 Analysis on how management accounting lead to sustainable success..............................11

D3 Evaluation of how planning tools respond to solve financial problems.............................12

CONCLUSION..............................................................................................................................12

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its different types....................................................................1

P2 Methods for management accounting Reporting...................................................................3

M1 Benefits of management accounting system........................................................................4

D1 Critical evaluation on management accounting report integrated within organisational

process.........................................................................................................................................4

TASK 2............................................................................................................................................4

P3 Cost calculations to prepare an income statement ................................................................4

M2 A range of management accounting techniques...................................................................7

D2 Analysis and Interpretation of data.......................................................................................8

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of different types of planning tools for budgetary control...8

M3 Analysis on use of different planning tool for preparing and forecasting budgets...............9

TASK 4............................................................................................................................................9

P5 Comparison on how organizations are adapting management accounting system to resolve

financial problems.......................................................................................................................9

M4 Analysis on how management accounting lead to sustainable success..............................11

D3 Evaluation of how planning tools respond to solve financial problems.............................12

CONCLUSION..............................................................................................................................12

REFERENCE.................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting refers to a process of preparing reports and accounts in a

company. It provides necessary information which is used for further planning and controlling

decisions. In context with small organizations, this concept helps in monitoring business

performance (Kumarasiri and Jubb, 2016). The present report is going to make a discussion

about management accounting with its various methods like planning and measurement tools.

For this purpose, Aridri is taken, which deals in manufacturing sector and engage business in

hand dryer production.

This assignment highlights use of different planning tools for budgetary controls, which

further help in preparing and forecasting budget of company. An explanation about different

managerial accounting reports like budget, job cost, inventory and more is also given. Along

with this, an income statement is prepared on the basis of calculations of costs by using

absorption and marginal costing methods. A comparison is also made to show how companies

under small sector use management accounting system for resolving financial issues.

TASK 1

P1 Management accounting and its different types

The concept of Management accounting can be defined as process of preparing report

by which performance of business can be analysed. It provides timely and accurate information

to managers of company so that they can take short-term and long-term decisions accordingly.

Moreover, it determines, analyses, measures, interprets as well as communicates information that

makes an organisation able to achieve their set goals. In an organisation, management accounting

plays different role like forecasting the future and cash flows, making decisions, understanding

performance variances and analyse rate of return (Pavlatos, 2015). In context with Aridri, as it

deals business in small sector of UK so, it is necessary for managers of this company to timely

prepare such reports. It will help in managing accounts and preparing budget in appropriate

manner.

Aridri is considered as first hand dryer manufacturing company in the world, which

receives Quiet MarkTM from Noise Abatement Society. It uses unique and latest technologies in

production field which extend lifespan of hand dryer products. So, to enhance and create more

value of business, this enterprise uses management accounting system. In this regard, an

1

Management accounting refers to a process of preparing reports and accounts in a

company. It provides necessary information which is used for further planning and controlling

decisions. In context with small organizations, this concept helps in monitoring business

performance (Kumarasiri and Jubb, 2016). The present report is going to make a discussion

about management accounting with its various methods like planning and measurement tools.

For this purpose, Aridri is taken, which deals in manufacturing sector and engage business in

hand dryer production.

This assignment highlights use of different planning tools for budgetary controls, which

further help in preparing and forecasting budget of company. An explanation about different

managerial accounting reports like budget, job cost, inventory and more is also given. Along

with this, an income statement is prepared on the basis of calculations of costs by using

absorption and marginal costing methods. A comparison is also made to show how companies

under small sector use management accounting system for resolving financial issues.

TASK 1

P1 Management accounting and its different types

The concept of Management accounting can be defined as process of preparing report

by which performance of business can be analysed. It provides timely and accurate information

to managers of company so that they can take short-term and long-term decisions accordingly.

Moreover, it determines, analyses, measures, interprets as well as communicates information that

makes an organisation able to achieve their set goals. In an organisation, management accounting

plays different role like forecasting the future and cash flows, making decisions, understanding

performance variances and analyse rate of return (Pavlatos, 2015). In context with Aridri, as it

deals business in small sector of UK so, it is necessary for managers of this company to timely

prepare such reports. It will help in managing accounts and preparing budget in appropriate

manner.

Aridri is considered as first hand dryer manufacturing company in the world, which

receives Quiet MarkTM from Noise Abatement Society. It uses unique and latest technologies in

production field which extend lifespan of hand dryer products. So, to enhance and create more

value of business, this enterprise uses management accounting system. In this regard, an

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

explanation of different types of management accounting system and its importance is given as

beneath:

Price optimising system: This system is generally used for determining how demand of

a product will fluctuate at different-different price strategies (Christ and Burritt, 2017). It is also

used to control price of raw materials and other resources for increasing efficiency of production.

Therefore, managers of Aridri used this system of management accounting to evaluate how to

retain loyal customers. Moreover, it also aids them in determining pricing structures for initial,

promotional and discount pricing. Along with this, pricing optimisation also assist Aridri in

selling short life-cycle products first which are subjected to seasonal and fashion trends.

Job costing system: This system of management accounting help to find out each unit

cost of product. (Banker and et. al., 2014). But it is generally used when manufactured goods are

significantly different from each other. Managers of Aridri use this process to maintain record of

each unit of product. It include following procedure:- Receive enquiry- For placing order, customer used to look out first on quality of material

and price rate. Estimate price- It is usually done by accountant who estimate price of each unit by

identifying taste and preference of customers. Order receive- If consumers give assurance for price, then they order will be placed

accordingly. Production order- It is placed for starting the process of production. Cost recording- Each and every aspect related to cost is recorded in production process.

Completion of job- After completion, report will provide to accounts department of

company for final costing of job.

Cost accounting system: This system provides a framework by which Aridri can

estimate cost of different products for analysing profitability and inventory valuation. In

manufacturing sector, different types of cost contribute for producing an output. Therefore, this

concept involves two methodologies of cost accounting that are- job and process costing.

Inventory management system: This concept is concerned with management of stock

and inventories in an enterprise. Therefore, organisational process of a company can be

integrated by using inventory management system. It will help in achieving efficient and

effective flow of inventory. In context with Aridri, it uses this management accounting system

2

beneath:

Price optimising system: This system is generally used for determining how demand of

a product will fluctuate at different-different price strategies (Christ and Burritt, 2017). It is also

used to control price of raw materials and other resources for increasing efficiency of production.

Therefore, managers of Aridri used this system of management accounting to evaluate how to

retain loyal customers. Moreover, it also aids them in determining pricing structures for initial,

promotional and discount pricing. Along with this, pricing optimisation also assist Aridri in

selling short life-cycle products first which are subjected to seasonal and fashion trends.

Job costing system: This system of management accounting help to find out each unit

cost of product. (Banker and et. al., 2014). But it is generally used when manufactured goods are

significantly different from each other. Managers of Aridri use this process to maintain record of

each unit of product. It include following procedure:- Receive enquiry- For placing order, customer used to look out first on quality of material

and price rate. Estimate price- It is usually done by accountant who estimate price of each unit by

identifying taste and preference of customers. Order receive- If consumers give assurance for price, then they order will be placed

accordingly. Production order- It is placed for starting the process of production. Cost recording- Each and every aspect related to cost is recorded in production process.

Completion of job- After completion, report will provide to accounts department of

company for final costing of job.

Cost accounting system: This system provides a framework by which Aridri can

estimate cost of different products for analysing profitability and inventory valuation. In

manufacturing sector, different types of cost contribute for producing an output. Therefore, this

concept involves two methodologies of cost accounting that are- job and process costing.

Inventory management system: This concept is concerned with management of stock

and inventories in an enterprise. Therefore, organisational process of a company can be

integrated by using inventory management system. It will help in achieving efficient and

effective flow of inventory. In context with Aridri, it uses this management accounting system

2

with aim to generate high return profitability by minimising the total cost of inventories. This

accounting system includes many methods like LIFO (Last in first out), FIFO (First-In First-Out)

and prioritise with ABC. Managers of Aridri use ABC analysis in order to focus on those

products which provide more profit for business. In this era, products of A category required

more and regular attention because impact of them is financially significant. Similarly, B and C

category include moderate and low-value products respectively which have a high frequency of

sales.

P2 Methods for management accounting Reporting

Accounting reports are most crucial part in business which helps in determining how

company is performing. This concept assists small organizations to monitor the performance of

business (Jack, 2015). In this regard, managers of a firm can prepare different reports either in

quarterly, weekly or monthly basis. It provide accurate and reliable statistical information so

management can take decision according to it. In context with Aridri, different types of

management accounting reports and their benefits for business are discussed in following

manner:-

Budgeting report: This report sets out the plan for analysing performance of different

departments and control costs. Estimated budget of a company is usually based on actual

expenses. So, managers of Aridri design this report to analyse and compare how close budgeted

performance of business during a financial period was to the actual one.

Job cost reports: It is concerned with determining expenses, costs and profitability of

each job in manufacturing process. This report provides crucial information to a company about

its current status of a particular job. As Aridri deals in manufacturing field and use a wide range

of raw materials for producing high quality of hand dryer products. So, using job cost report, it

can control addition expenses so that efficiency of production can be increased.

Inventory and manufacturing report: This kind of management accounting report is

generally used by manufacturing and construction companies (Smith, Brännström and Jansson,

2015). It includes information about labour cost, wastages and each unit overhead costs.

Therefore, employers of Aridri prepare this report to see opportunities by which they can make

improvement in manufacturing process.

3

accounting system includes many methods like LIFO (Last in first out), FIFO (First-In First-Out)

and prioritise with ABC. Managers of Aridri use ABC analysis in order to focus on those

products which provide more profit for business. In this era, products of A category required

more and regular attention because impact of them is financially significant. Similarly, B and C

category include moderate and low-value products respectively which have a high frequency of

sales.

P2 Methods for management accounting Reporting

Accounting reports are most crucial part in business which helps in determining how

company is performing. This concept assists small organizations to monitor the performance of

business (Jack, 2015). In this regard, managers of a firm can prepare different reports either in

quarterly, weekly or monthly basis. It provide accurate and reliable statistical information so

management can take decision according to it. In context with Aridri, different types of

management accounting reports and their benefits for business are discussed in following

manner:-

Budgeting report: This report sets out the plan for analysing performance of different

departments and control costs. Estimated budget of a company is usually based on actual

expenses. So, managers of Aridri design this report to analyse and compare how close budgeted

performance of business during a financial period was to the actual one.

Job cost reports: It is concerned with determining expenses, costs and profitability of

each job in manufacturing process. This report provides crucial information to a company about

its current status of a particular job. As Aridri deals in manufacturing field and use a wide range

of raw materials for producing high quality of hand dryer products. So, using job cost report, it

can control addition expenses so that efficiency of production can be increased.

Inventory and manufacturing report: This kind of management accounting report is

generally used by manufacturing and construction companies (Smith, Brännström and Jansson,

2015). It includes information about labour cost, wastages and each unit overhead costs.

Therefore, employers of Aridri prepare this report to see opportunities by which they can make

improvement in manufacturing process.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

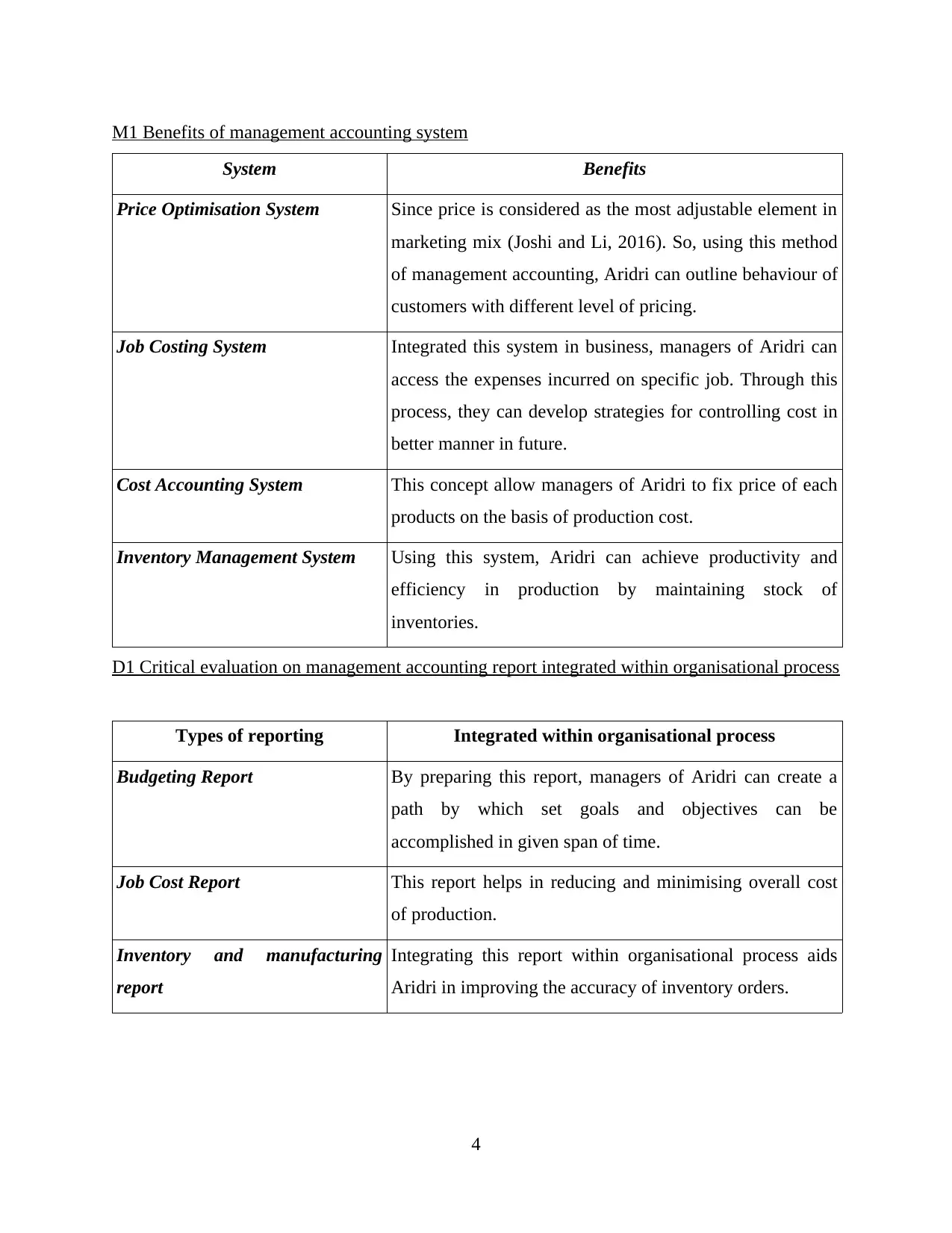

M1 Benefits of management accounting system

System Benefits

Price Optimisation System Since price is considered as the most adjustable element in

marketing mix (Joshi and Li, 2016). So, using this method

of management accounting, Aridri can outline behaviour of

customers with different level of pricing.

Job Costing System Integrated this system in business, managers of Aridri can

access the expenses incurred on specific job. Through this

process, they can develop strategies for controlling cost in

better manner in future.

Cost Accounting System This concept allow managers of Aridri to fix price of each

products on the basis of production cost.

Inventory Management System Using this system, Aridri can achieve productivity and

efficiency in production by maintaining stock of

inventories.

D1 Critical evaluation on management accounting report integrated within organisational process

Types of reporting Integrated within organisational process

Budgeting Report By preparing this report, managers of Aridri can create a

path by which set goals and objectives can be

accomplished in given span of time.

Job Cost Report This report helps in reducing and minimising overall cost

of production.

Inventory and manufacturing

report

Integrating this report within organisational process aids

Aridri in improving the accuracy of inventory orders.

4

System Benefits

Price Optimisation System Since price is considered as the most adjustable element in

marketing mix (Joshi and Li, 2016). So, using this method

of management accounting, Aridri can outline behaviour of

customers with different level of pricing.

Job Costing System Integrated this system in business, managers of Aridri can

access the expenses incurred on specific job. Through this

process, they can develop strategies for controlling cost in

better manner in future.

Cost Accounting System This concept allow managers of Aridri to fix price of each

products on the basis of production cost.

Inventory Management System Using this system, Aridri can achieve productivity and

efficiency in production by maintaining stock of

inventories.

D1 Critical evaluation on management accounting report integrated within organisational process

Types of reporting Integrated within organisational process

Budgeting Report By preparing this report, managers of Aridri can create a

path by which set goals and objectives can be

accomplished in given span of time.

Job Cost Report This report helps in reducing and minimising overall cost

of production.

Inventory and manufacturing

report

Integrating this report within organisational process aids

Aridri in improving the accuracy of inventory orders.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

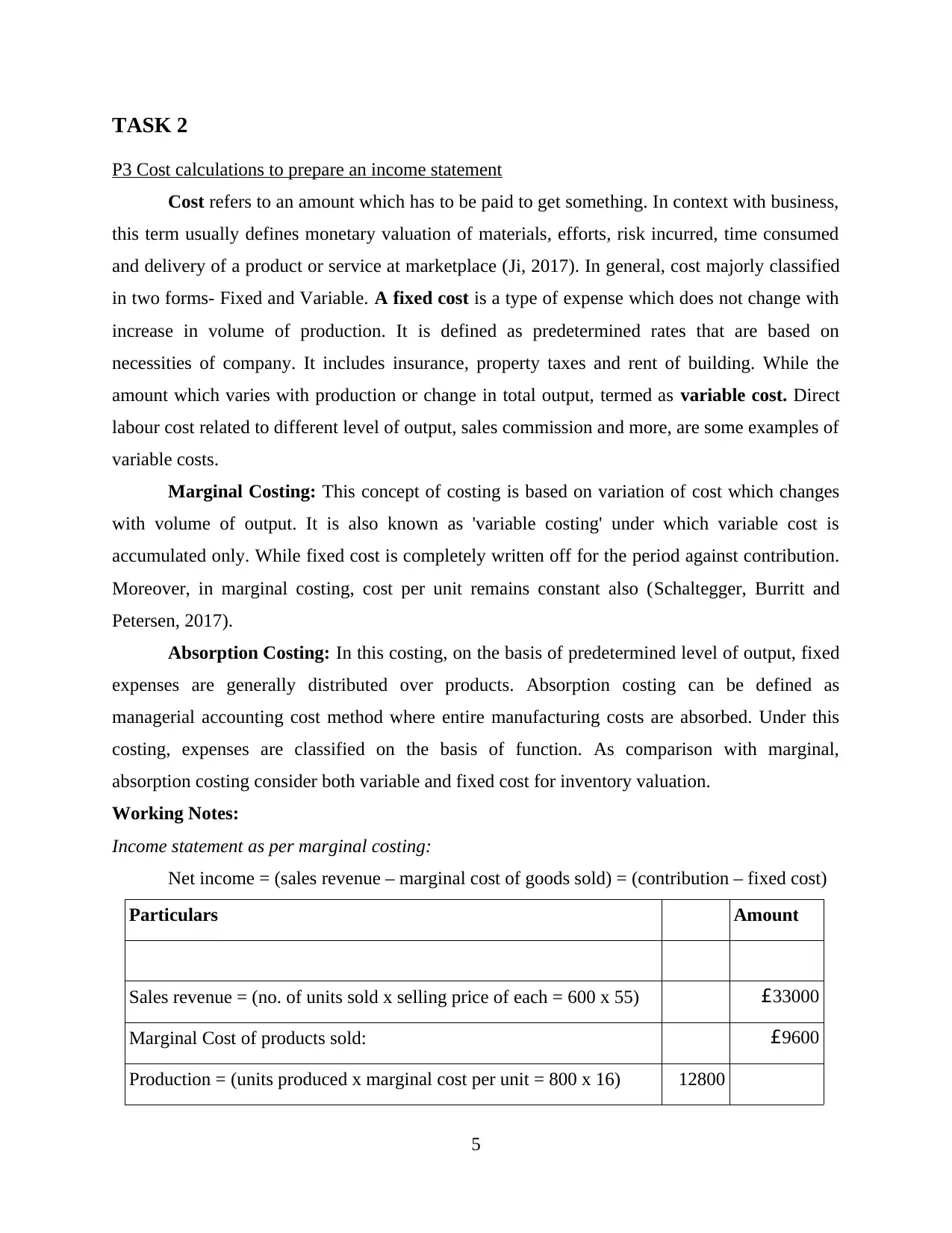

P3 Cost calculations to prepare an income statement

Cost refers to an amount which has to be paid to get something. In context with business,

this term usually defines monetary valuation of materials, efforts, risk incurred, time consumed

and delivery of a product or service at marketplace (Ji, 2017). In general, cost majorly classified

in two forms- Fixed and Variable. A fixed cost is a type of expense which does not change with

increase in volume of production. It is defined as predetermined rates that are based on

necessities of company. It includes insurance, property taxes and rent of building. While the

amount which varies with production or change in total output, termed as variable cost. Direct

labour cost related to different level of output, sales commission and more, are some examples of

variable costs.

Marginal Costing: This concept of costing is based on variation of cost which changes

with volume of output. It is also known as 'variable costing' under which variable cost is

accumulated only. While fixed cost is completely written off for the period against contribution.

Moreover, in marginal costing, cost per unit remains constant also (Schaltegger, Burritt and

Petersen, 2017).

Absorption Costing: In this costing, on the basis of predetermined level of output, fixed

expenses are generally distributed over products. Absorption costing can be defined as

managerial accounting cost method where entire manufacturing costs are absorbed. Under this

costing, expenses are classified on the basis of function. As comparison with marginal,

absorption costing consider both variable and fixed cost for inventory valuation.

Working Notes:

Income statement as per marginal costing:

Net income = (sales revenue – marginal cost of goods sold) = (contribution – fixed cost)

Particulars Amount

Sales revenue = (no. of units sold x selling price of each = 600 x 55) £33000

Marginal Cost of products sold: £9600

Production = (units produced x marginal cost per unit = 800 x 16) 12800

5

P3 Cost calculations to prepare an income statement

Cost refers to an amount which has to be paid to get something. In context with business,

this term usually defines monetary valuation of materials, efforts, risk incurred, time consumed

and delivery of a product or service at marketplace (Ji, 2017). In general, cost majorly classified

in two forms- Fixed and Variable. A fixed cost is a type of expense which does not change with

increase in volume of production. It is defined as predetermined rates that are based on

necessities of company. It includes insurance, property taxes and rent of building. While the

amount which varies with production or change in total output, termed as variable cost. Direct

labour cost related to different level of output, sales commission and more, are some examples of

variable costs.

Marginal Costing: This concept of costing is based on variation of cost which changes

with volume of output. It is also known as 'variable costing' under which variable cost is

accumulated only. While fixed cost is completely written off for the period against contribution.

Moreover, in marginal costing, cost per unit remains constant also (Schaltegger, Burritt and

Petersen, 2017).

Absorption Costing: In this costing, on the basis of predetermined level of output, fixed

expenses are generally distributed over products. Absorption costing can be defined as

managerial accounting cost method where entire manufacturing costs are absorbed. Under this

costing, expenses are classified on the basis of function. As comparison with marginal,

absorption costing consider both variable and fixed cost for inventory valuation.

Working Notes:

Income statement as per marginal costing:

Net income = (sales revenue – marginal cost of goods sold) = (contribution – fixed cost)

Particulars Amount

Sales revenue = (no. of units sold x selling price of each = 600 x 55) £33000

Marginal Cost of products sold: £9600

Production = (units produced x marginal cost per unit = 800 x 16) 12800

5

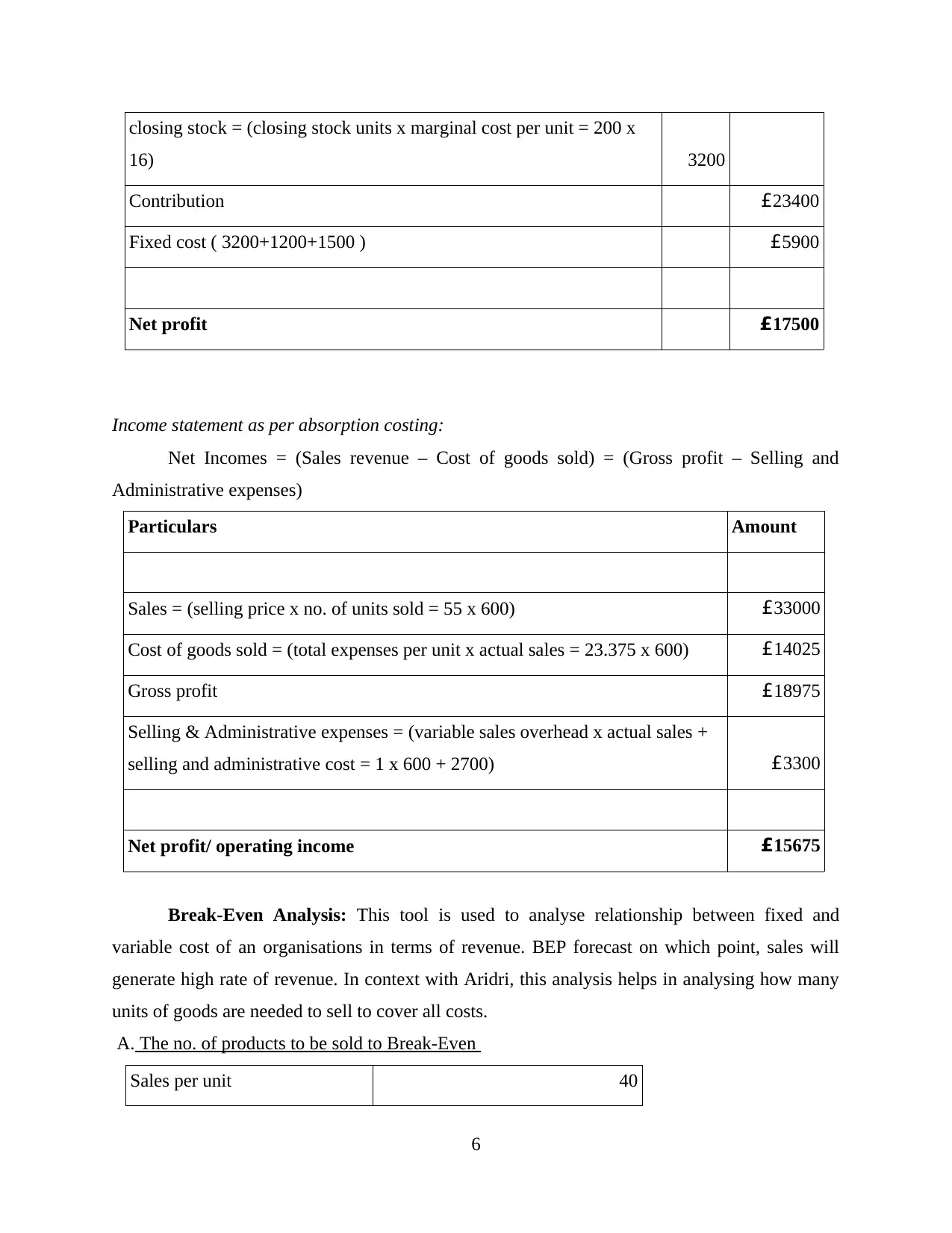

closing stock = (closing stock units x marginal cost per unit = 200 x

16) 3200

Contribution £23400

Fixed cost ( 3200+1200+1500 ) £5900

Net profit £17500

Income statement as per absorption costing:

Net Incomes = (Sales revenue – Cost of goods sold) = (Gross profit – Selling and

Administrative expenses)

Particulars Amount

Sales = (selling price x no. of units sold = 55 x 600) £33000

Cost of goods sold = (total expenses per unit x actual sales = 23.375 x 600) £14025

Gross profit £18975

Selling & Administrative expenses = (variable sales overhead x actual sales +

selling and administrative cost = 1 x 600 + 2700) £3300

Net profit/ operating income £15675

Break-Even Analysis: This tool is used to analyse relationship between fixed and

variable cost of an organisations in terms of revenue. BEP forecast on which point, sales will

generate high rate of revenue. In context with Aridri, this analysis helps in analysing how many

units of goods are needed to sell to cover all costs.

A. The no. of products to be sold to Break-Even

Sales per unit 40

6

16) 3200

Contribution £23400

Fixed cost ( 3200+1200+1500 ) £5900

Net profit £17500

Income statement as per absorption costing:

Net Incomes = (Sales revenue – Cost of goods sold) = (Gross profit – Selling and

Administrative expenses)

Particulars Amount

Sales = (selling price x no. of units sold = 55 x 600) £33000

Cost of goods sold = (total expenses per unit x actual sales = 23.375 x 600) £14025

Gross profit £18975

Selling & Administrative expenses = (variable sales overhead x actual sales +

selling and administrative cost = 1 x 600 + 2700) £3300

Net profit/ operating income £15675

Break-Even Analysis: This tool is used to analyse relationship between fixed and

variable cost of an organisations in terms of revenue. BEP forecast on which point, sales will

generate high rate of revenue. In context with Aridri, this analysis helps in analysing how many

units of goods are needed to sell to cover all costs.

A. The no. of products to be sold to Break-Even

Sales per unit 40

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

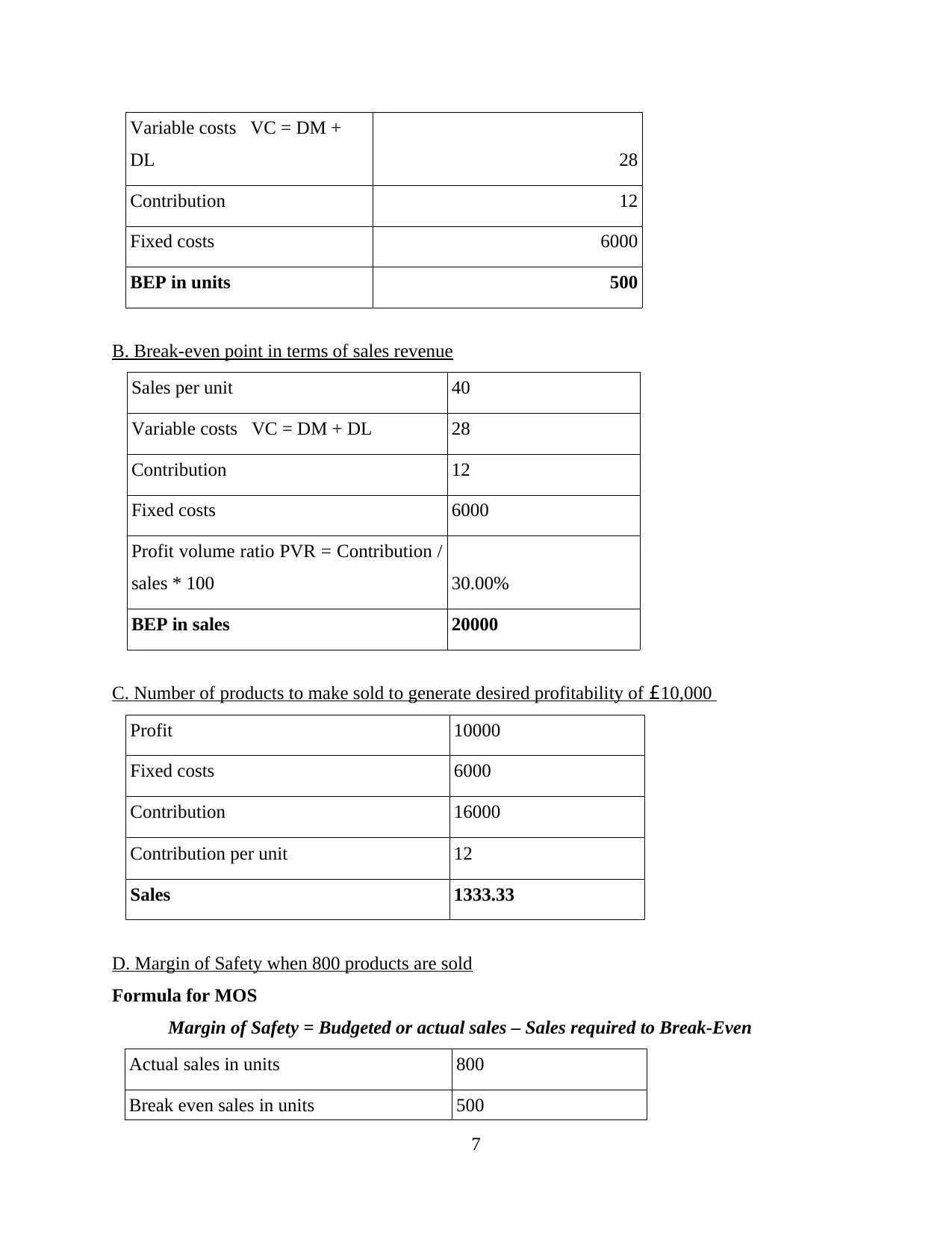

Variable costs VC = DM +

DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

B. Break-even point in terms of sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

BEP in sales 20000

C. Number of products to make sold to generate desired profitability of £10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

D. Margin of Safety when 800 products are sold

Formula for MOS

Margin of Safety = Budgeted or actual sales – Sales required to Break-Even

Actual sales in units 800

Break even sales in units 500

7

DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

B. Break-even point in terms of sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

BEP in sales 20000

C. Number of products to make sold to generate desired profitability of £10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

D. Margin of Safety when 800 products are sold

Formula for MOS

Margin of Safety = Budgeted or actual sales – Sales required to Break-Even

Actual sales in units 800

Break even sales in units 500

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Margin of safety 37.5

Margin of safety (MOS)- It reflects the exact difference between break-even and actual

or budgeted sales of an enterprise. In other words, sales revenue that goes beyond BEP is

considered as margin of safety. As per above calculation, when actual sales of Aridri is 800 units

and break-even sales is 500 units then in that case, margin of safety will be obtained as 37.5

units.

M2 A range of management accounting techniques

There is a wide range of management accounting techniques are available which helps a

company in gathering internal information. So, using such techniques, managers of Aridri can

prepare reports which further facilitate in taking proper decisions. Some major techniques used

by this enterprise are:-

Standard Costing: It is a technique of recording accounting transactions which further

used in analyzing the difference between standard and actual cost.

Marginal Costing: Accountant of Aridri use this technique for decision making,

controlling cost and maximizing profitability.

D2 Analysis and Interpretation of data

It has analyzed from above data that techniques of management accounting use different-

different methods for calculating the per unit cost of products. In absorption costing, all costs are

utilized for calculation. While in marginal costing, only variable cost is used and fixed cost is

written off to the contribution. Thus, in this regard, net operating income as per absorption and

marginal costing, come out as £15675 and £17500 respectively for Aridri Ltd.

TASK 3

P4 Advantages and disadvantages of different types of planning tools for budgetary control

Budgetary control is considered as a process by which a company can control its

expenses and finance (Maskell, Baggaley and Grasso, 2016). This concept involves a procedure

of comparing budget to actual outcome. It has a potential to aid an organization to reach its

specific goal in predetermined time by offering several advantages. It includes coordinating all

8

Margin of safety (MOS)- It reflects the exact difference between break-even and actual

or budgeted sales of an enterprise. In other words, sales revenue that goes beyond BEP is

considered as margin of safety. As per above calculation, when actual sales of Aridri is 800 units

and break-even sales is 500 units then in that case, margin of safety will be obtained as 37.5

units.

M2 A range of management accounting techniques

There is a wide range of management accounting techniques are available which helps a

company in gathering internal information. So, using such techniques, managers of Aridri can

prepare reports which further facilitate in taking proper decisions. Some major techniques used

by this enterprise are:-

Standard Costing: It is a technique of recording accounting transactions which further

used in analyzing the difference between standard and actual cost.

Marginal Costing: Accountant of Aridri use this technique for decision making,

controlling cost and maximizing profitability.

D2 Analysis and Interpretation of data

It has analyzed from above data that techniques of management accounting use different-

different methods for calculating the per unit cost of products. In absorption costing, all costs are

utilized for calculation. While in marginal costing, only variable cost is used and fixed cost is

written off to the contribution. Thus, in this regard, net operating income as per absorption and

marginal costing, come out as £15675 and £17500 respectively for Aridri Ltd.

TASK 3

P4 Advantages and disadvantages of different types of planning tools for budgetary control

Budgetary control is considered as a process by which a company can control its

expenses and finance (Maskell, Baggaley and Grasso, 2016). This concept involves a procedure

of comparing budget to actual outcome. It has a potential to aid an organization to reach its

specific goal in predetermined time by offering several advantages. It includes coordinating all

8

activities of departments, translating strategic plans into actions and more. With respect to Aridri

Limited, concept of budgetary controls helps in regulating its entire activities as per

predetermined target and objectives. One of the main advantages of practicing budgetary control

is to gain opportunity by which changes in business can be made. It helps in moving business on

next level and keeping on track of success as well.

As due to dynamic nature of business, there are different type of risk occurred at

workplace which affect budget of a company. It includes natural disasters, failure in technology,

global events such as pandemic (swine flu, influenza), climatic changes and more. As Aridri

Limited deals in small sector so, controlling budget is its major concern. Therefore, to handle

such issues and manage risks as well, there are different type of planning tools available for

budgetary controls like:-

Forecasting Planning Tool- Planning is considered as mapping out the direction of

organisational for attaining desired goals. In this regard, planning for future refers to a major

activity of a company. Therefore, forecasting tool is used for predicting uncertain future demand

of a company. In context with Aridri Ltd., using this tool, it can manage risks by developing

strategies to recover from situations which might happen in future.

Advantage Disadvantages

Aridri Ltd. can apply forecasting methods for

to anticipate potential risks and issues which

might arise in upcoming years.

For small companies, it is rarely possible to

forecast future in accurate manner. So, making

decisions for forecasting is financially ruin for

them.

Contingency Planning Tools- It refers to a course of action which is designed in to aid

an organisation in responding to a future situation in an effective manner (D'Onza, Greco and

Allegrini, 2016). This plan outlined seven steps to overcome from such issues which may or

many not happen in future. It includes developing the contingency planning policy; conducting

business impact analysis; identifying preventive controls; formulating strategies; preparing plan;

testing plan and last is maintenance the same. Thus, by conducting all these phases, Aridri can

prevent itself from future problems easily as well as respond more effectively.

Advantage Disadvantages

9

Limited, concept of budgetary controls helps in regulating its entire activities as per

predetermined target and objectives. One of the main advantages of practicing budgetary control

is to gain opportunity by which changes in business can be made. It helps in moving business on

next level and keeping on track of success as well.

As due to dynamic nature of business, there are different type of risk occurred at

workplace which affect budget of a company. It includes natural disasters, failure in technology,

global events such as pandemic (swine flu, influenza), climatic changes and more. As Aridri

Limited deals in small sector so, controlling budget is its major concern. Therefore, to handle

such issues and manage risks as well, there are different type of planning tools available for

budgetary controls like:-

Forecasting Planning Tool- Planning is considered as mapping out the direction of

organisational for attaining desired goals. In this regard, planning for future refers to a major

activity of a company. Therefore, forecasting tool is used for predicting uncertain future demand

of a company. In context with Aridri Ltd., using this tool, it can manage risks by developing

strategies to recover from situations which might happen in future.

Advantage Disadvantages

Aridri Ltd. can apply forecasting methods for

to anticipate potential risks and issues which

might arise in upcoming years.

For small companies, it is rarely possible to

forecast future in accurate manner. So, making

decisions for forecasting is financially ruin for

them.

Contingency Planning Tools- It refers to a course of action which is designed in to aid

an organisation in responding to a future situation in an effective manner (D'Onza, Greco and

Allegrini, 2016). This plan outlined seven steps to overcome from such issues which may or

many not happen in future. It includes developing the contingency planning policy; conducting

business impact analysis; identifying preventive controls; formulating strategies; preparing plan;

testing plan and last is maintenance the same. Thus, by conducting all these phases, Aridri can

prevent itself from future problems easily as well as respond more effectively.

Advantage Disadvantages

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.