Management Accounting Report: Decision Making for ASDA Stores

VerifiedAdded on 2020/06/04

|18

|4746

|57

Report

AI Summary

This report, prepared by a Management Accounting Officer, provides a detailed analysis of various management accounting systems (MAS) and their applications within ASDA Stores. It explores different MAS types, including Traditional, Lean, Throughput, and Transfer systems, highlighting their roles in financial reporting and decision-making. The report examines different management accounting reporting methods, such as budget reports, accounts receivable aging reports, job cost reports, inventory and manufacturing reports, income statements, and cash flow statements, explaining their significance and practical implementation for ASDA Stores. Furthermore, the report delves into absorption costing and marginal costing methods, illustrating their use in income statement analysis. It also discusses the merits and demerits of planning tools for budgetary control and emphasizes the importance of management accounting in solving financial problems, offering case analyses to support the application of these techniques. The report's primary objective is to identify effective accounting methods like profit analysis, marginal costing, and absorption costing, enabling ASDA Stores to make informed business decisions.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Report on management accounting system and its different types required for management

.....................................................................................................................................................1

P2 Different methods of Management accounting reporting......................................................4

TASK 2............................................................................................................................................7

P3 Calculation of absorption costing and marginal costing in identifying income statements. .7

TASK 3..........................................................................................................................................11

P4 A report on merits and demerits of various planning tools of budgetary control................11

P5 Use of management accounting system to solve financial problem....................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Report on management accounting system and its different types required for management

.....................................................................................................................................................1

P2 Different methods of Management accounting reporting......................................................4

TASK 2............................................................................................................................................7

P3 Calculation of absorption costing and marginal costing in identifying income statements. .7

TASK 3..........................................................................................................................................11

P4 A report on merits and demerits of various planning tools of budgetary control................11

P5 Use of management accounting system to solve financial problem....................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

From: Management accounting officer

To: General manager of ASDA Stores

Sub: Management accounting system

In this report, being a Management Accounting Officer, details of the variety of MAS

that assist ASDA Stores in make the proper decision while choosing the best alternatives has

explained by me. Different types of Management Accounting Systems such as Traditional, Lean,

Throughput and Transfer systems are the part of this report.

INTRODUCTION

MAS or management accounting is a enterprise learning and transformation process in

which practical application of accounting techniques while making report is done (Bac, 2013).

These reports show the financial health of an organisation in meeting its future estimation plans.

Management accounting plays several roles like analysing, planning, implementation and

controlling programme designs (Banerjee, 2010). It helps management in knowing their financial

status. These financial reports also help management in making decisions.

In this assignment, Asda Stores Ltd. is considered for application of management

accounting strategies. This company is British supermarket distributor and its headquarter is in

Leeds, West Yorkshire. It was founded in 1965 (source: asdasecure).

Various methods and types of management accounting has been discussed in report to

General manager. Merits and demerits of planning tools has also been explained to support

budgetary control process. Case analyses of two different scenario's have been done to execute

accounting techniques into it. The study of these different scenario's will help management of

chosen company in proper application of these tools discussed in report for better decision-

making.

Main objective of this report is to identify different ways of using accounting methods

such as profit analysis, marginal costing and absorption costing for company.

TASK 1

P1

Management Accounting System:

1

To: General manager of ASDA Stores

Sub: Management accounting system

In this report, being a Management Accounting Officer, details of the variety of MAS

that assist ASDA Stores in make the proper decision while choosing the best alternatives has

explained by me. Different types of Management Accounting Systems such as Traditional, Lean,

Throughput and Transfer systems are the part of this report.

INTRODUCTION

MAS or management accounting is a enterprise learning and transformation process in

which practical application of accounting techniques while making report is done (Bac, 2013).

These reports show the financial health of an organisation in meeting its future estimation plans.

Management accounting plays several roles like analysing, planning, implementation and

controlling programme designs (Banerjee, 2010). It helps management in knowing their financial

status. These financial reports also help management in making decisions.

In this assignment, Asda Stores Ltd. is considered for application of management

accounting strategies. This company is British supermarket distributor and its headquarter is in

Leeds, West Yorkshire. It was founded in 1965 (source: asdasecure).

Various methods and types of management accounting has been discussed in report to

General manager. Merits and demerits of planning tools has also been explained to support

budgetary control process. Case analyses of two different scenario's have been done to execute

accounting techniques into it. The study of these different scenario's will help management of

chosen company in proper application of these tools discussed in report for better decision-

making.

Main objective of this report is to identify different ways of using accounting methods

such as profit analysis, marginal costing and absorption costing for company.

TASK 1

P1

Management Accounting System:

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The MAS contains all the provisions that provide accounting information to the managers

(Bennett and James, 2017). Data's collected through this system helps in making decisions to

resolve many issues of an organisation. It consists guidelines for making financial and non-

financial decisions. It is mainly considered by Investors, creditors and operational managers.

These users have different purposes to consider accounting information. It is based on their

requirements.

There are various management accounting systems which are used in order to make certain

objectives.

Cost Accounting system: This is also known as lean accounting system. Cost accounting

system is the main tool which are used in order to make sustainable development. However, it

can be stated that the cost accounting system is an effective technique which produce goods in a

reasonable manner. This can be said that the management accounting system is the most

effective tool that can be used for lowering the cost of production of goods. It involves the

revolutionary technique in which it focuses on the cost reducing strategy. Whenever it is

necessary to make decisions, this system provides immediate information to the accounting

managers.

Stock Administration system: It is a main system that assist in keeping control over stock of

an enterprise. Inventory management system helps the company to gain the sustainable

development in an appropriate way. With the help of IMS, company can effectively manage

their working capital and cited company can make their decisions effectively about the

Inventory Management System.

Job Costing system: This is the job costing system which are used in order to assign

production cost to an individual product or batch. Normally, this can be said that the job order

costing is the tool which is used only when the goods produced are separately different from

each other.

Price optimisation system: This is the tool under which the management accountant officer

will optimise the price so that the company could use their objectives in an appropriate way.

although, this is the most important tool of the business that can be used by the company in

order to implement their business objectives. POS helps the company to fix their price in an

effective manner. which would help out to make their business decisions for the long run.

2

(Bennett and James, 2017). Data's collected through this system helps in making decisions to

resolve many issues of an organisation. It consists guidelines for making financial and non-

financial decisions. It is mainly considered by Investors, creditors and operational managers.

These users have different purposes to consider accounting information. It is based on their

requirements.

There are various management accounting systems which are used in order to make certain

objectives.

Cost Accounting system: This is also known as lean accounting system. Cost accounting

system is the main tool which are used in order to make sustainable development. However, it

can be stated that the cost accounting system is an effective technique which produce goods in a

reasonable manner. This can be said that the management accounting system is the most

effective tool that can be used for lowering the cost of production of goods. It involves the

revolutionary technique in which it focuses on the cost reducing strategy. Whenever it is

necessary to make decisions, this system provides immediate information to the accounting

managers.

Stock Administration system: It is a main system that assist in keeping control over stock of

an enterprise. Inventory management system helps the company to gain the sustainable

development in an appropriate way. With the help of IMS, company can effectively manage

their working capital and cited company can make their decisions effectively about the

Inventory Management System.

Job Costing system: This is the job costing system which are used in order to assign

production cost to an individual product or batch. Normally, this can be said that the job order

costing is the tool which is used only when the goods produced are separately different from

each other.

Price optimisation system: This is the tool under which the management accountant officer

will optimise the price so that the company could use their objectives in an appropriate way.

although, this is the most important tool of the business that can be used by the company in

order to implement their business objectives. POS helps the company to fix their price in an

effective manner. which would help out to make their business decisions for the long run.

2

P2

From: Management accounting officer

To: G.M. of ASDA Stores

Sub: Management accounting report

In this report, the process of decision-making has been explained to various methods of

accounting reporting to assist ASDA Stores. Apart from this, the use of these methods has also

been mentioned as per the company's requirement.

Introduction to Management accounting report

Management accounting reports tells about financial position and status of a company. It

shows the how efficiently company is performing as compared to other companies (Chiarini

and Vagnoni, 2015). This is done at the last of each accounting period or it can be present at the

time of demand, such as directors can also ask for monthly, weekly or even daily reports.

Advantages of M.A reports

This system assist in future prediction.

This aids in decision making or buying.

It predicts coming cash flow of business from various sources.

This assist in knowing the difference in labour, content and results of possessions

It help organisation in studying the rate of rate required to run the business.

Different methods of MA report

Budget Report: It is a system of MA reporting of organization, management can learn

how to analyse the performance of a company through evaluating budget report

3

Methods of Management Accounting ReportMethods of Management Accounting Report

Accounts receivable

Aging Report

Job costs Reports

Income statement

report

Cash flow reportBudget Report

Inventory reports

From: Management accounting officer

To: G.M. of ASDA Stores

Sub: Management accounting report

In this report, the process of decision-making has been explained to various methods of

accounting reporting to assist ASDA Stores. Apart from this, the use of these methods has also

been mentioned as per the company's requirement.

Introduction to Management accounting report

Management accounting reports tells about financial position and status of a company. It

shows the how efficiently company is performing as compared to other companies (Chiarini

and Vagnoni, 2015). This is done at the last of each accounting period or it can be present at the

time of demand, such as directors can also ask for monthly, weekly or even daily reports.

Advantages of M.A reports

This system assist in future prediction.

This aids in decision making or buying.

It predicts coming cash flow of business from various sources.

This assist in knowing the difference in labour, content and results of possessions

It help organisation in studying the rate of rate required to run the business.

Different methods of MA report

Budget Report: It is a system of MA reporting of organization, management can learn

how to analyse the performance of a company through evaluating budget report

3

Methods of Management Accounting ReportMethods of Management Accounting Report

Accounts receivable

Aging Report

Job costs Reports

Income statement

report

Cash flow reportBudget Report

Inventory reports

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Chiarini, 2012.). This report helps the company in controlling additional costs on some

departments. It also compares the performance of each department on the basis of their

cost allocated in budget reports. Under this technique, an approximated budget for that

particular period has been made, this estimate is based on the trend of actual expenses.

Owners and managers can also use budget reports for allocation of incentives among

their employees, budget reports analyse robust analytical skills and skills to create

useful management accounting reports. Overall, this is fundamental reports in

managerial accounting. It helps businesses in control costs in enterprises.

Accounts receivable Ageing Report: This reporting method of management

accounting for any business is very important, which sells its products on credit.

Generally credit is given in different categories such as 30, 60 and 90 days. It is

necessary for a company to refer this report at the time of making credit policies for

buyers of their product.

Job costs Reports: This method of management accounting provides a report that

shows expenditure for a particular project. These costs correspond to an estimate

revenue to analyse job profits. This method classifies high earning areas of the business,

rather than focusing on the allocation of funds to these areas rather than waste money

and cost rather than using the money in low-income areas. Job Costing is also used to

identify expenses of work-in-progress or unfinished projects to eliminate wastes before

completion.

Inventory and manufacturing reports: This method of management accounting is

useful for companies that produce physical products such as manufacturing industries.

The Inventory and Manufacturing report helps in collecting data on inventory cost,

labor and other upper part of the production process. Manufacturing companies can use

the managerial accounting report to make their operations more efficient

Income statement report: These statements consists of trading and profit and loss

account which is prepared at the end of every year (DRURY, 2013). It helps a company

in knowing how much profit and loss is left with the company after pay off all its

expenses. It is transferred to retained earnings account of a company.

Cash Flow statement report: This report helps the business to know how much cash is

available in a business and how much it could be earned in future. Overall, it tells about

4

departments. It also compares the performance of each department on the basis of their

cost allocated in budget reports. Under this technique, an approximated budget for that

particular period has been made, this estimate is based on the trend of actual expenses.

Owners and managers can also use budget reports for allocation of incentives among

their employees, budget reports analyse robust analytical skills and skills to create

useful management accounting reports. Overall, this is fundamental reports in

managerial accounting. It helps businesses in control costs in enterprises.

Accounts receivable Ageing Report: This reporting method of management

accounting for any business is very important, which sells its products on credit.

Generally credit is given in different categories such as 30, 60 and 90 days. It is

necessary for a company to refer this report at the time of making credit policies for

buyers of their product.

Job costs Reports: This method of management accounting provides a report that

shows expenditure for a particular project. These costs correspond to an estimate

revenue to analyse job profits. This method classifies high earning areas of the business,

rather than focusing on the allocation of funds to these areas rather than waste money

and cost rather than using the money in low-income areas. Job Costing is also used to

identify expenses of work-in-progress or unfinished projects to eliminate wastes before

completion.

Inventory and manufacturing reports: This method of management accounting is

useful for companies that produce physical products such as manufacturing industries.

The Inventory and Manufacturing report helps in collecting data on inventory cost,

labor and other upper part of the production process. Manufacturing companies can use

the managerial accounting report to make their operations more efficient

Income statement report: These statements consists of trading and profit and loss

account which is prepared at the end of every year (DRURY, 2013). It helps a company

in knowing how much profit and loss is left with the company after pay off all its

expenses. It is transferred to retained earnings account of a company.

Cash Flow statement report: This report helps the business to know how much cash is

available in a business and how much it could be earned in future. Overall, it tells about

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the trade's liquidity.

This method could be applied by ASDA Stores in following ways:

Budget Report: ASDA Stores can use the budget report to analyse the difference

between estimated and actual data. More deviation refers to the inability of a company

to manage its costs, where less variance means that the company is using its resources

without wasting its resources. It can be understood through this illustration: ASDA

Stores sales budget is 500 units and company able to achieve selling 600 units. This

difference is known as under budget as company estimates lesser than actual. This under

budget affects in non-meeting of actual demand.

Accounts receivable Aging Report: Through the application of this type of report,

ASDA Stores could know how much period requires to receive the total amount from its

debtors. For instance, If the debtor is moving from last year, the efficiency of the

working capital of the companies will be affected due to the low cash available for a

business. Therefore, this report can be implemented to control the extra blockage of

cash among debtors.

Job costs Reports: After the application of this method, ASDA Stores can know which

activity consumes more cash. For example, in the given example, the company has

production, sales and distribution costs. These different costs generate a job-related cost

on the basis of activities. .

Inventory and manufacturing reports: In this type of reporting method, managers

applied this to know how much stock of ASDA Stores is blocked in manufacturing

process. These reports represent the working capital statement and the progress of a

company. For example, information about a company's stock and closing stock is

required to meet the demand of a product for information.

Income statement report: This report is known to show how much profit has been left

with the ASDA Stores after payment of all expenses, interests, taxes and payments. For

example, the company records the net profit amount of £ 9300 over a year. This means

that it has only managed to earn that amount.

Cash flow statement report: ASDA Stores can implement this method to find the

liquidity of its business through the analysis of cash flow statement reports. For

example, the company's net profit is £ 9.3 billion, which is accumulated. This means

5

This method could be applied by ASDA Stores in following ways:

Budget Report: ASDA Stores can use the budget report to analyse the difference

between estimated and actual data. More deviation refers to the inability of a company

to manage its costs, where less variance means that the company is using its resources

without wasting its resources. It can be understood through this illustration: ASDA

Stores sales budget is 500 units and company able to achieve selling 600 units. This

difference is known as under budget as company estimates lesser than actual. This under

budget affects in non-meeting of actual demand.

Accounts receivable Aging Report: Through the application of this type of report,

ASDA Stores could know how much period requires to receive the total amount from its

debtors. For instance, If the debtor is moving from last year, the efficiency of the

working capital of the companies will be affected due to the low cash available for a

business. Therefore, this report can be implemented to control the extra blockage of

cash among debtors.

Job costs Reports: After the application of this method, ASDA Stores can know which

activity consumes more cash. For example, in the given example, the company has

production, sales and distribution costs. These different costs generate a job-related cost

on the basis of activities. .

Inventory and manufacturing reports: In this type of reporting method, managers

applied this to know how much stock of ASDA Stores is blocked in manufacturing

process. These reports represent the working capital statement and the progress of a

company. For example, information about a company's stock and closing stock is

required to meet the demand of a product for information.

Income statement report: This report is known to show how much profit has been left

with the ASDA Stores after payment of all expenses, interests, taxes and payments. For

example, the company records the net profit amount of £ 9300 over a year. This means

that it has only managed to earn that amount.

Cash flow statement report: ASDA Stores can implement this method to find the

liquidity of its business through the analysis of cash flow statement reports. For

example, the company's net profit is £ 9.3 billion, which is accumulated. This means

5

that the business is not earned in cash. So, the business may know how much actual

cash has been left with this report.

CONCLUSION

This depends on the requirement of ASDA Stores which type of report is required. Each

reporting method has its own use and significance, to obtain the liquidity of a business, the cash

flow statement report is useful. Income Statement helps the business to know how much money

it makes with the business in order to invest in expansion activities and business maintenance.

Budget report estimates are based on estimation. According to it, rotour plc is required for

allocation of funds between different departments.

TASK 2

P3 Calculation of absorption costing and marginal costing in identifying income statements

Marginal costing: In this type of costing method, expenses and revenues are break down

into per unit basis. According to this costing method, business should produce products until its

costs per unit is more than its price per unit (Håkansson, Kraus and Lind, 2010). For example:

To know the impact of profit with change in sales units, company requires per unit price. It can

produce its products until price of the product is more than its costs. But after utilising excess

production limit, for any new production fixed cost of company would increase which makes

excess of costs over its price.

Absorption Costing: This is a method for evaluating the inventory, here, the distribution

expenditure is distributed among the various departments to know how much cost has to pay for

each department. For example, let's assume that the ASDA Stores has two departments that are

selling & distribution and production. Suppose that the staff of these two departments eat in a

canteen the cost of the canteen is itself developed by the company itself. Therefore, the cost of

canteen is not direct cost, but it supports both departments to run a business. Therefore, the

methods of absorption have suggested to distribute the canteen expenditure among these two

departments to get the actual value.

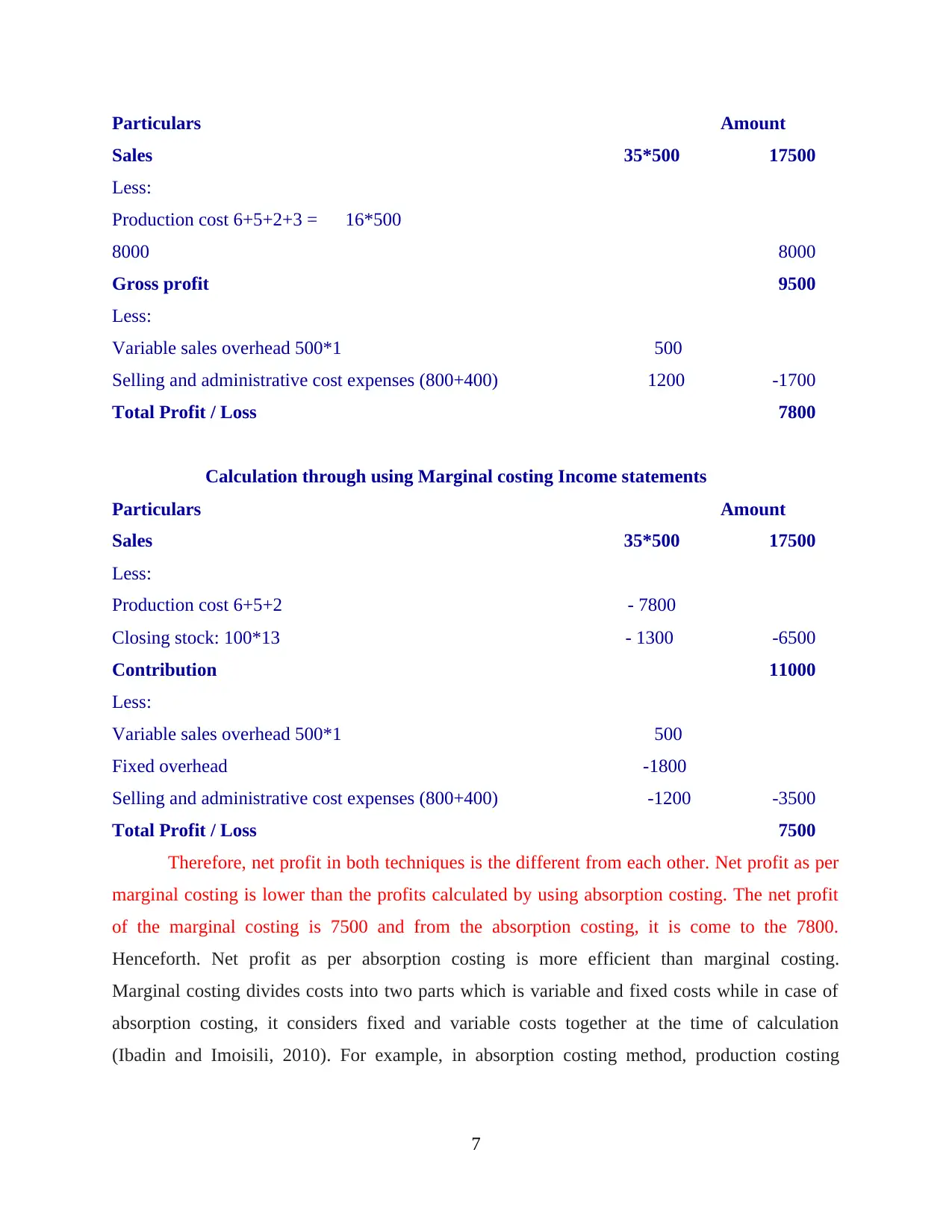

Below is the table in which calculation of Income statement with marginal costing and

absorption costing is Computation of Net profit by using absorption costing

Income statements

6

cash has been left with this report.

CONCLUSION

This depends on the requirement of ASDA Stores which type of report is required. Each

reporting method has its own use and significance, to obtain the liquidity of a business, the cash

flow statement report is useful. Income Statement helps the business to know how much money

it makes with the business in order to invest in expansion activities and business maintenance.

Budget report estimates are based on estimation. According to it, rotour plc is required for

allocation of funds between different departments.

TASK 2

P3 Calculation of absorption costing and marginal costing in identifying income statements

Marginal costing: In this type of costing method, expenses and revenues are break down

into per unit basis. According to this costing method, business should produce products until its

costs per unit is more than its price per unit (Håkansson, Kraus and Lind, 2010). For example:

To know the impact of profit with change in sales units, company requires per unit price. It can

produce its products until price of the product is more than its costs. But after utilising excess

production limit, for any new production fixed cost of company would increase which makes

excess of costs over its price.

Absorption Costing: This is a method for evaluating the inventory, here, the distribution

expenditure is distributed among the various departments to know how much cost has to pay for

each department. For example, let's assume that the ASDA Stores has two departments that are

selling & distribution and production. Suppose that the staff of these two departments eat in a

canteen the cost of the canteen is itself developed by the company itself. Therefore, the cost of

canteen is not direct cost, but it supports both departments to run a business. Therefore, the

methods of absorption have suggested to distribute the canteen expenditure among these two

departments to get the actual value.

Below is the table in which calculation of Income statement with marginal costing and

absorption costing is Computation of Net profit by using absorption costing

Income statements

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

Calculation through using Marginal costing Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

Therefore, net profit in both techniques is the different from each other. Net profit as per

marginal costing is lower than the profits calculated by using absorption costing. The net profit

of the marginal costing is 7500 and from the absorption costing, it is come to the 7800.

Henceforth. Net profit as per absorption costing is more efficient than marginal costing.

Marginal costing divides costs into two parts which is variable and fixed costs while in case of

absorption costing, it considers fixed and variable costs together at the time of calculation

(Ibadin and Imoisili, 2010). For example, in absorption costing method, production costing

7

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

Calculation through using Marginal costing Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

Therefore, net profit in both techniques is the different from each other. Net profit as per

marginal costing is lower than the profits calculated by using absorption costing. The net profit

of the marginal costing is 7500 and from the absorption costing, it is come to the 7800.

Henceforth. Net profit as per absorption costing is more efficient than marginal costing.

Marginal costing divides costs into two parts which is variable and fixed costs while in case of

absorption costing, it considers fixed and variable costs together at the time of calculation

(Ibadin and Imoisili, 2010). For example, in absorption costing method, production costing

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

includes both variable and fixed costs of production and Selling & distribution costs contains

both variable and fixed overhead of administration expenses.

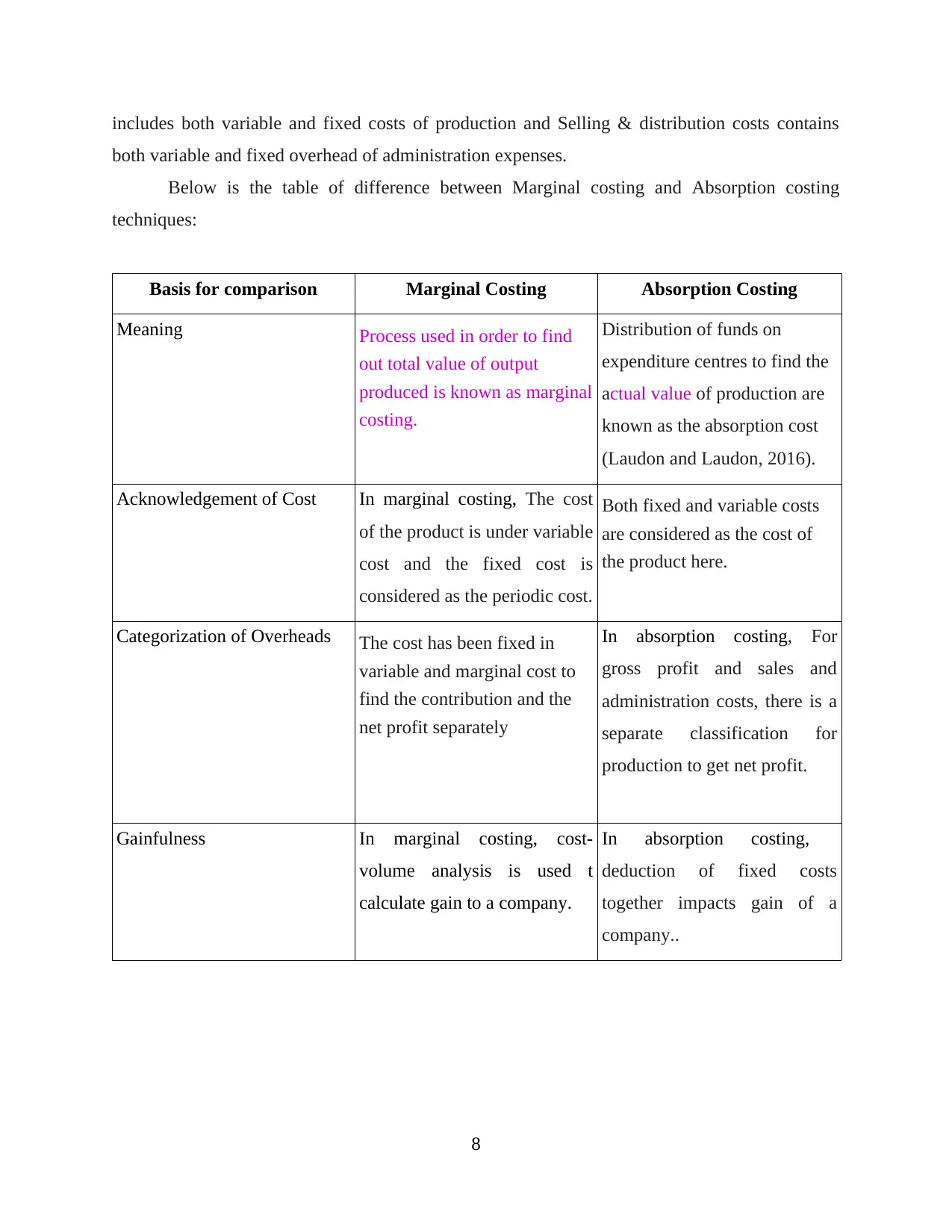

Below is the table of difference between Marginal costing and Absorption costing

techniques:

Basis for comparison Marginal Costing Absorption Costing

Meaning Process used in order to find

out total value of output

produced is known as marginal

costing.

Distribution of funds on

expenditure centres to find the

actual value of production are

known as the absorption cost

(Laudon and Laudon, 2016).

Acknowledgement of Cost In marginal costing, The cost

of the product is under variable

cost and the fixed cost is

considered as the periodic cost.

Both fixed and variable costs

are considered as the cost of

the product here.

Categorization of Overheads The cost has been fixed in

variable and marginal cost to

find the contribution and the

net profit separately

In absorption costing, For

gross profit and sales and

administration costs, there is a

separate classification for

production to get net profit.

Gainfulness In marginal costing, cost-

volume analysis is used t

calculate gain to a company.

In absorption costing,

deduction of fixed costs

together impacts gain of a

company..

8

both variable and fixed overhead of administration expenses.

Below is the table of difference between Marginal costing and Absorption costing

techniques:

Basis for comparison Marginal Costing Absorption Costing

Meaning Process used in order to find

out total value of output

produced is known as marginal

costing.

Distribution of funds on

expenditure centres to find the

actual value of production are

known as the absorption cost

(Laudon and Laudon, 2016).

Acknowledgement of Cost In marginal costing, The cost

of the product is under variable

cost and the fixed cost is

considered as the periodic cost.

Both fixed and variable costs

are considered as the cost of

the product here.

Categorization of Overheads The cost has been fixed in

variable and marginal cost to

find the contribution and the

net profit separately

In absorption costing, For

gross profit and sales and

administration costs, there is a

separate classification for

production to get net profit.

Gainfulness In marginal costing, cost-

volume analysis is used t

calculate gain to a company.

In absorption costing,

deduction of fixed costs

together impacts gain of a

company..

8

Expenditure per Unit Opening and closing stock of a

company doesn't affect the

calculation of Marginal costing

in finding cost per unit of a

product.

Opening and closing stock

directly affects the absorption

costing while calculating total

expenditure absorbed in

production process.

Detail Here, the main purpose of

marginal costing is to calculate

contribution per unit.

The purpose of absorption

costing is to calculate net profit

and gross profit of a company.

Cost Information In order to final out the cost of

every commodity data

associated to cost is presented.

This is prepared in a traditional

way to present the cost of the

data.

Absorption Costing: It accepts the costs that can be completely absorbed in the

production process (Lavia López and Hiebl, 2014). The goal of the cost of absorption is to

recover overheads so that the total time and effort eaten in the manufacture of products and

services can be reflected. It is calculated after considering following factors given below:

Appointment and allotments of overheads: In this phase, the overhead is allocated and

divided. It includes overhead expenditure directly separated from the production

department.

Rebuilding Service Cost Center Overheads: Service cost centers or departments are

not directly involved in the production activity of the products, thus their fixed overhead

charges can be distributed to the production departments on the basis of their cost. For

example, rebuilding of costs on the basis of services provided by canteen, stores, health

department and conflict resolution department can be done. As these departments

contributes in supporting production houses which helps company in smoothly running

its business operations.

Absorption of overheads: Overhead absorption is a method in which the costs of

overheads are included in the total cost of the product. It is defined as charge per unit cost

per production as per calculation based on the total number of production units. Overhead

absorption rate by the number of units of available absorption products can be identified

9

company doesn't affect the

calculation of Marginal costing

in finding cost per unit of a

product.

Opening and closing stock

directly affects the absorption

costing while calculating total

expenditure absorbed in

production process.

Detail Here, the main purpose of

marginal costing is to calculate

contribution per unit.

The purpose of absorption

costing is to calculate net profit

and gross profit of a company.

Cost Information In order to final out the cost of

every commodity data

associated to cost is presented.

This is prepared in a traditional

way to present the cost of the

data.

Absorption Costing: It accepts the costs that can be completely absorbed in the

production process (Lavia López and Hiebl, 2014). The goal of the cost of absorption is to

recover overheads so that the total time and effort eaten in the manufacture of products and

services can be reflected. It is calculated after considering following factors given below:

Appointment and allotments of overheads: In this phase, the overhead is allocated and

divided. It includes overhead expenditure directly separated from the production

department.

Rebuilding Service Cost Center Overheads: Service cost centers or departments are

not directly involved in the production activity of the products, thus their fixed overhead

charges can be distributed to the production departments on the basis of their cost. For

example, rebuilding of costs on the basis of services provided by canteen, stores, health

department and conflict resolution department can be done. As these departments

contributes in supporting production houses which helps company in smoothly running

its business operations.

Absorption of overheads: Overhead absorption is a method in which the costs of

overheads are included in the total cost of the product. It is defined as charge per unit cost

per production as per calculation based on the total number of production units. Overhead

absorption rate by the number of units of available absorption products can be identified

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.