Management Accounting Assignment: Cost Analysis and Job Costing Report

VerifiedAdded on 2023/01/17

|15

|1716

|85

Report

AI Summary

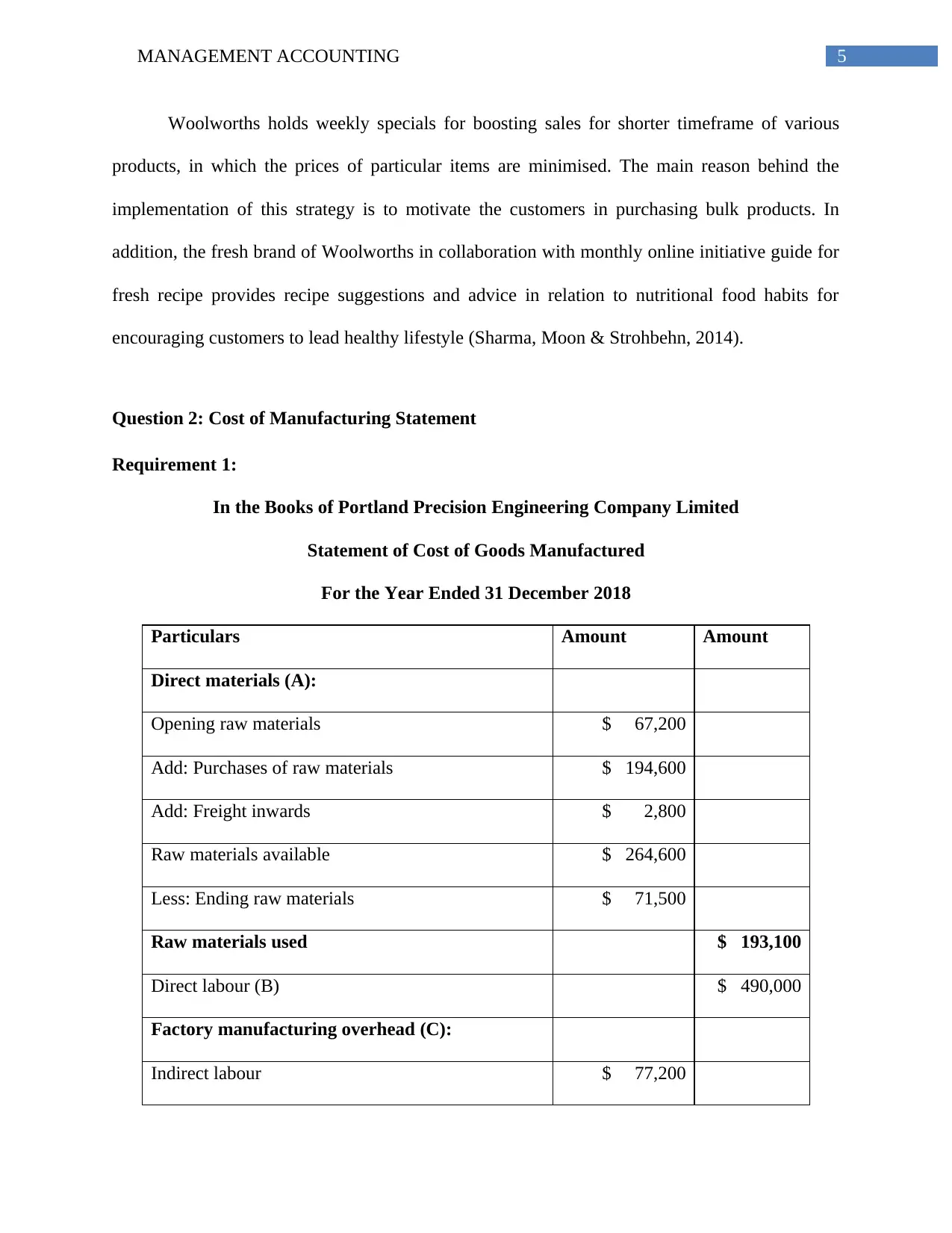

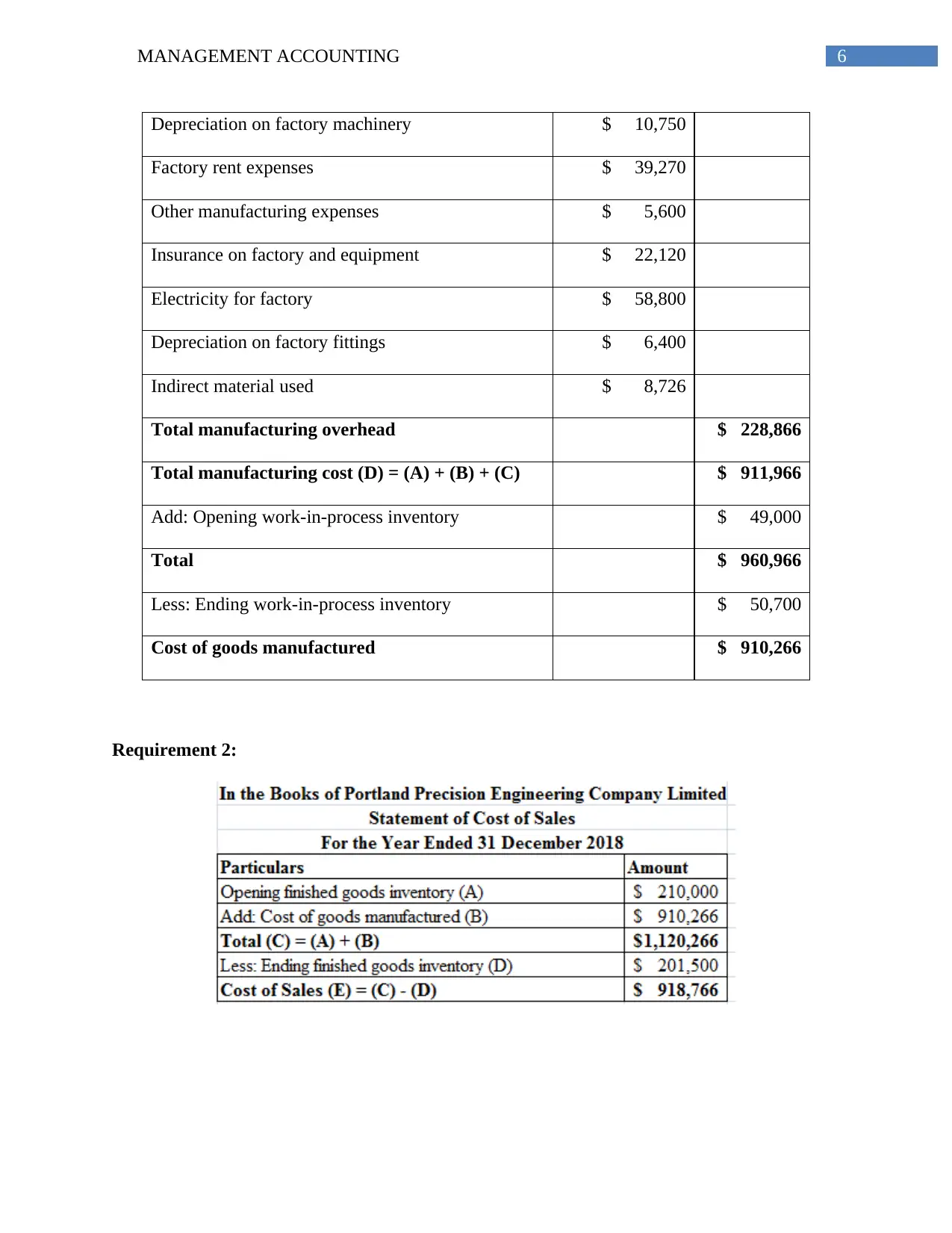

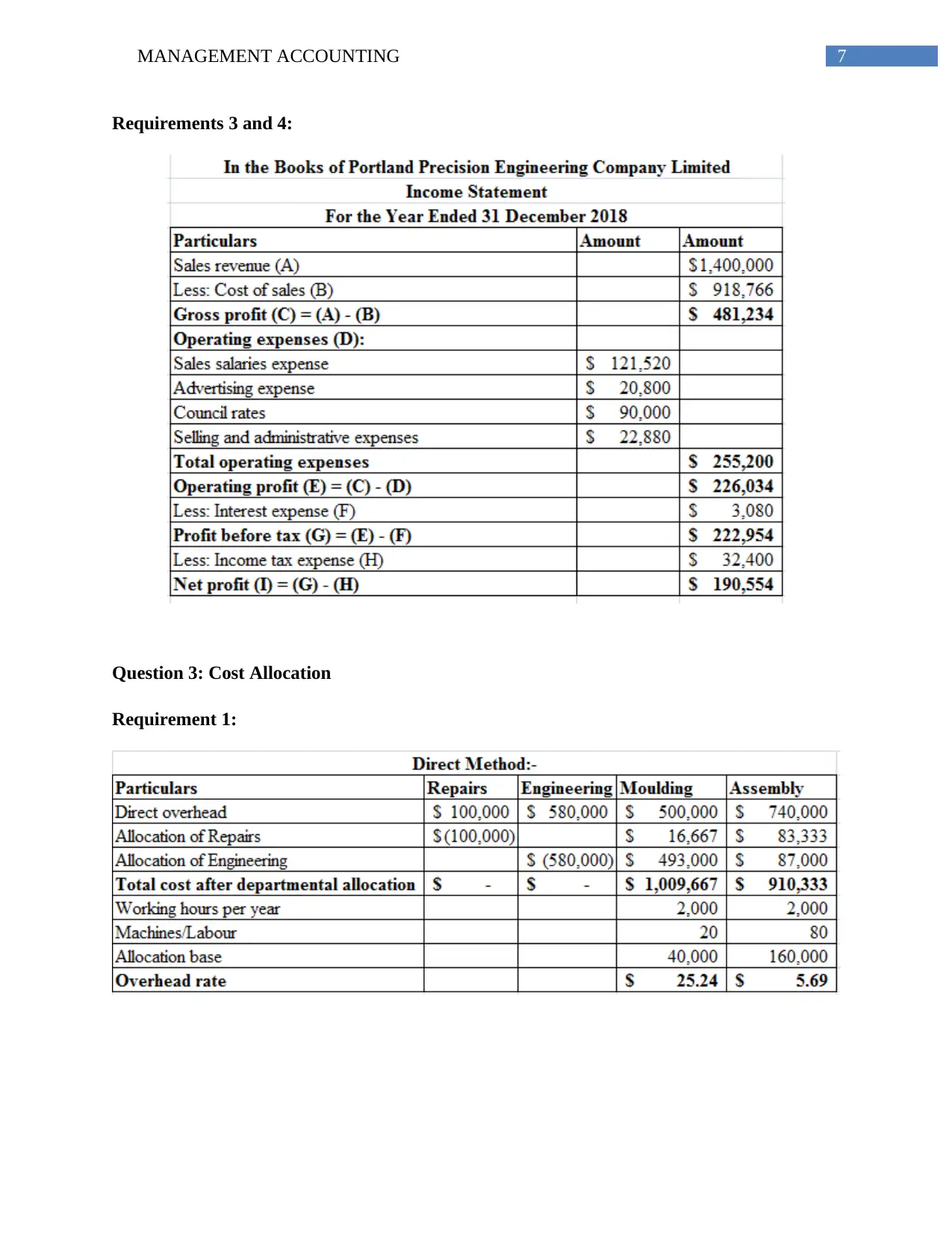

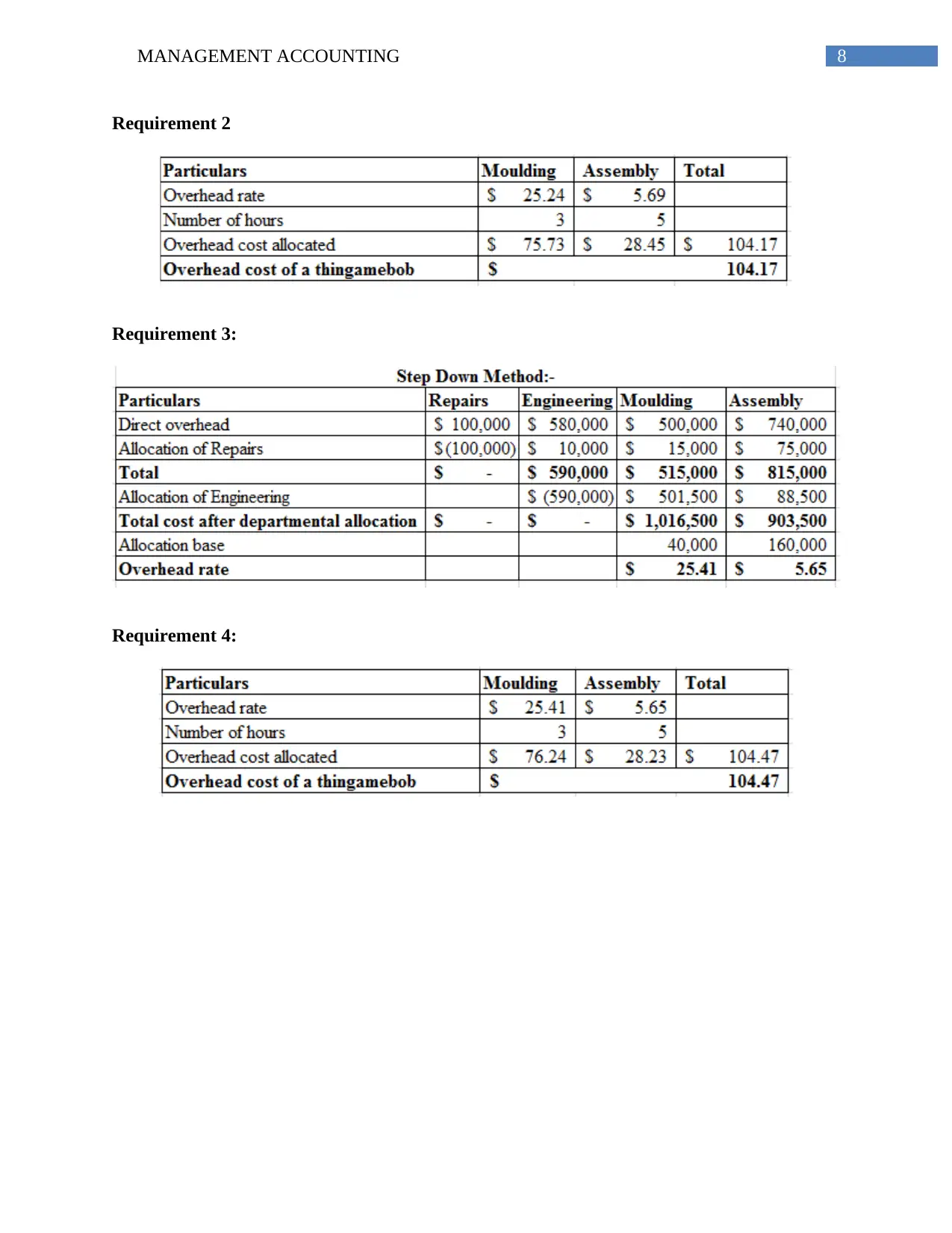

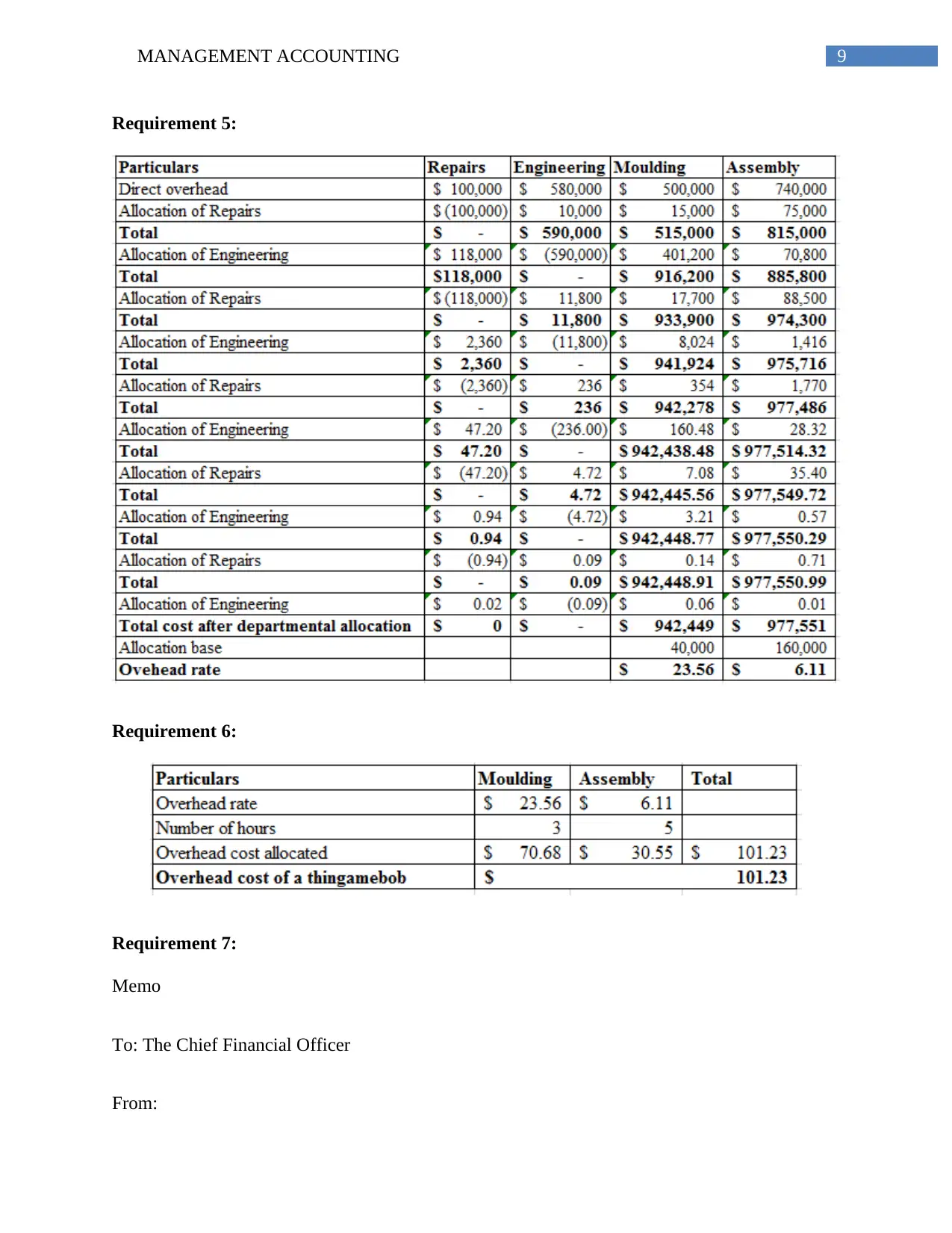

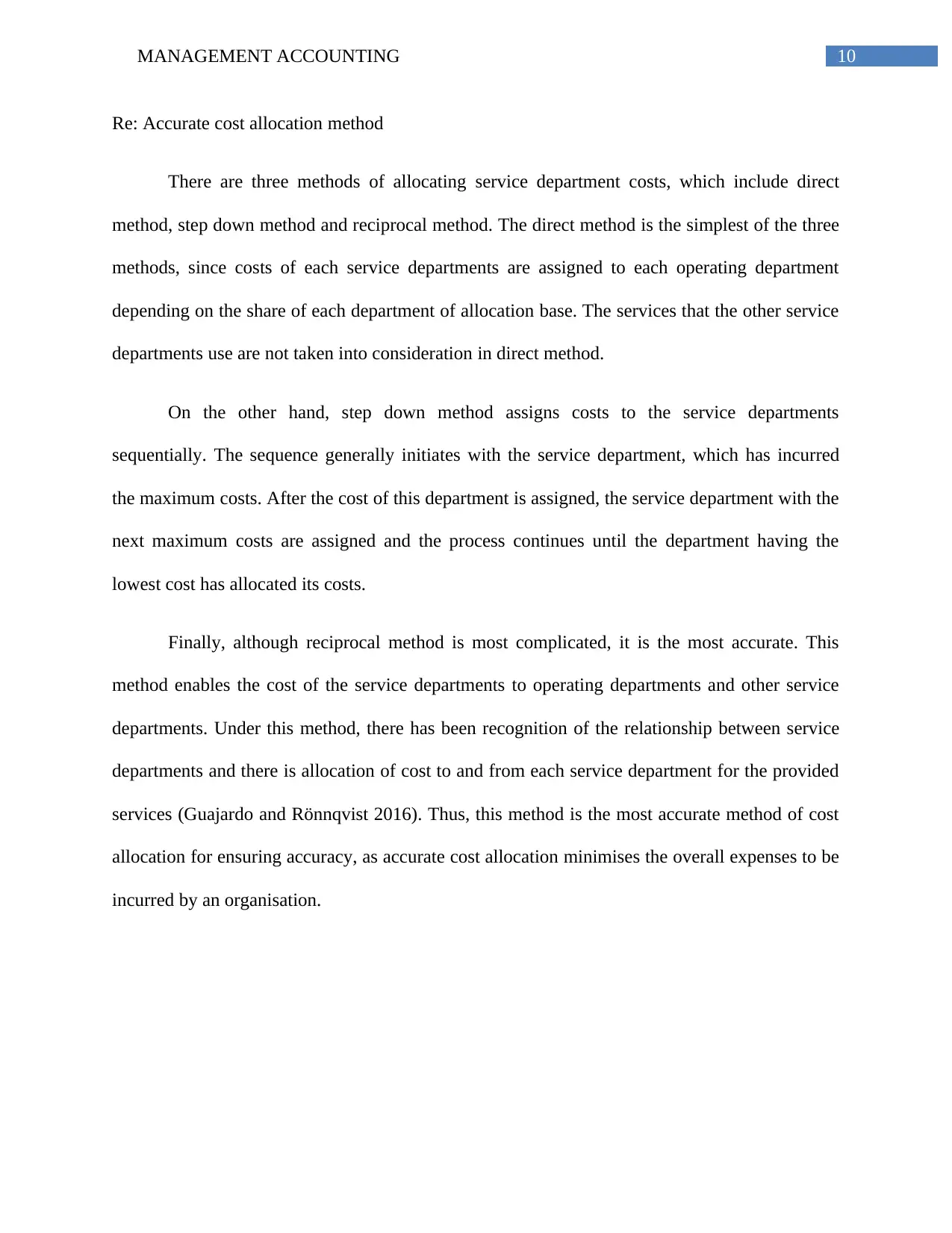

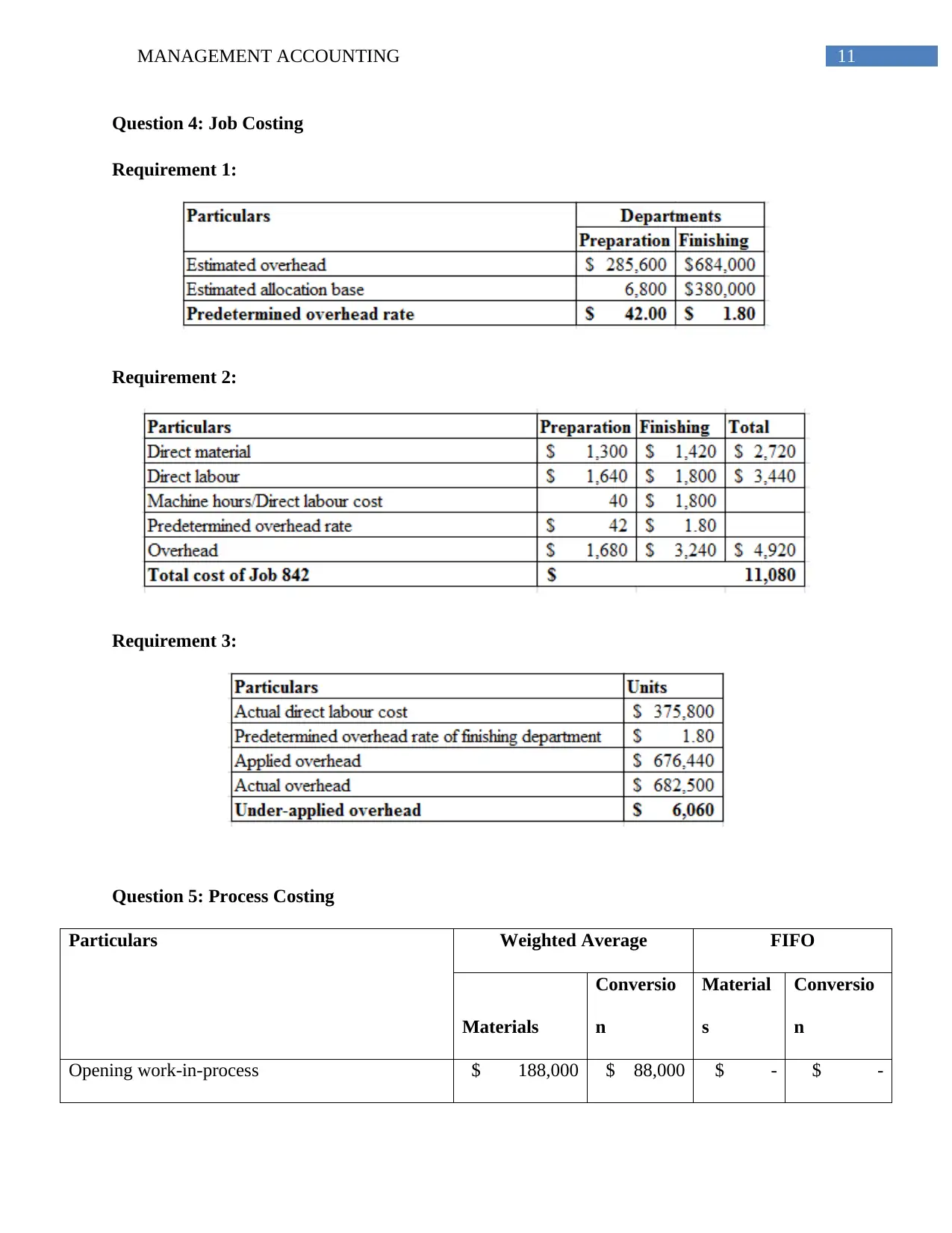

This management accounting assignment comprehensively addresses key concepts through a series of questions. The report begins with a value chain analysis of Woolworths Group Limited, evaluating its inbound logistics, operations, and marketing/sales strategies. The assignment then presents a detailed cost of manufacturing statement for Portland Precision Engineering Company Limited, followed by cost allocation analysis, exploring direct, step-down, and reciprocal methods. Job costing and process costing problems are solved, with the weighted average method applied in the process costing section. The assignment demonstrates an understanding of various costing techniques and their applications in financial analysis, providing valuable insights into management accounting principles.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.