Management Accounting for Cost and Control Assignment Solution

VerifiedAdded on 2020/03/01

|22

|1931

|34

Homework Assignment

AI Summary

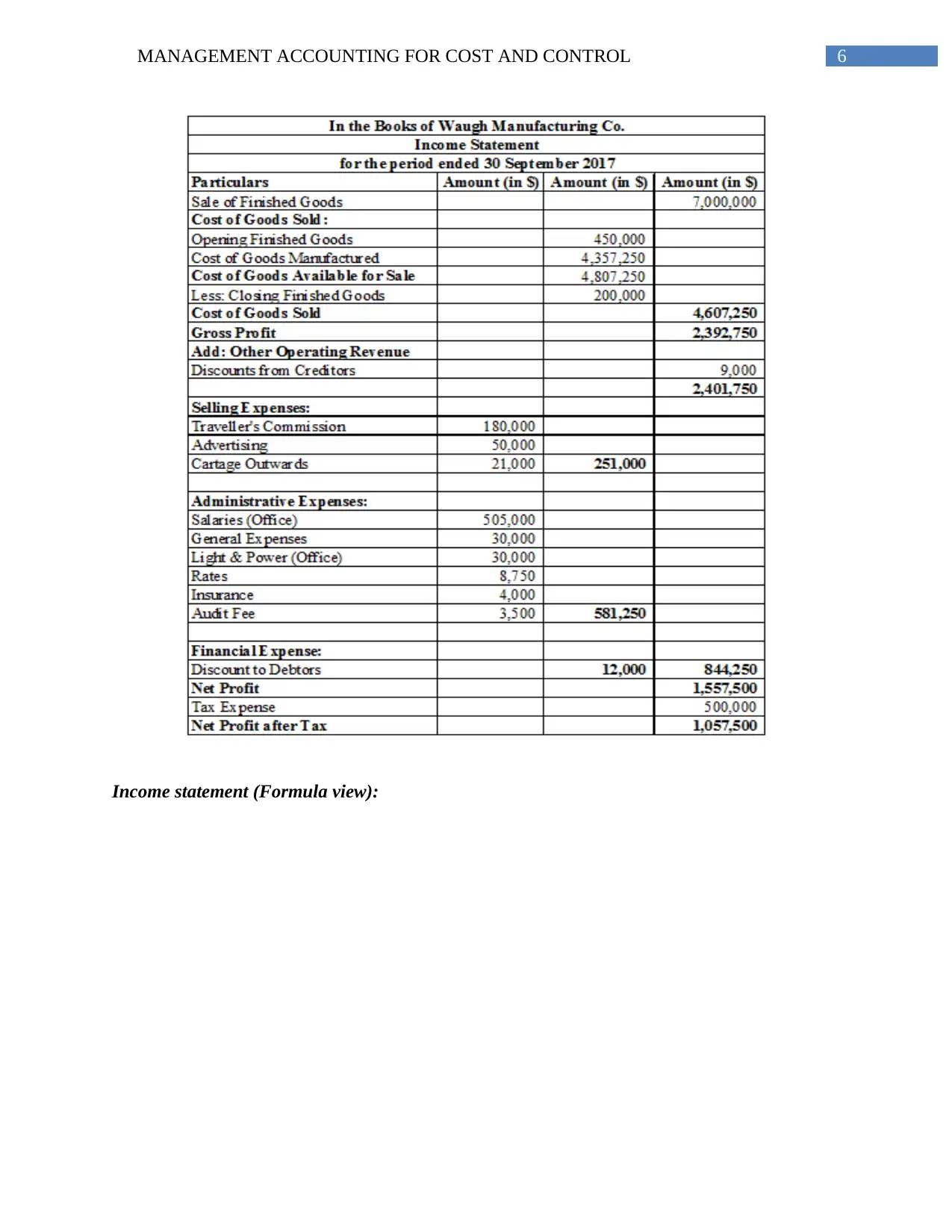

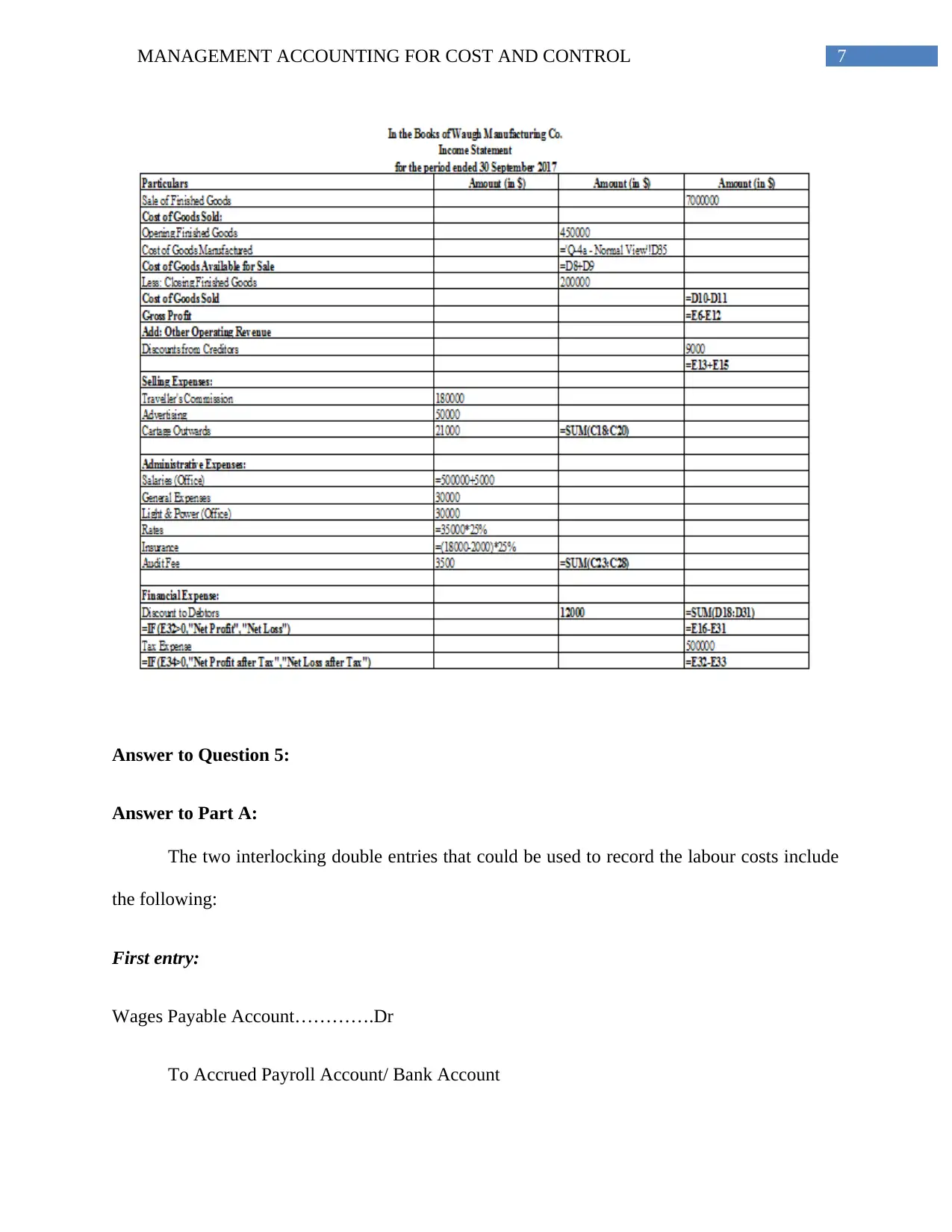

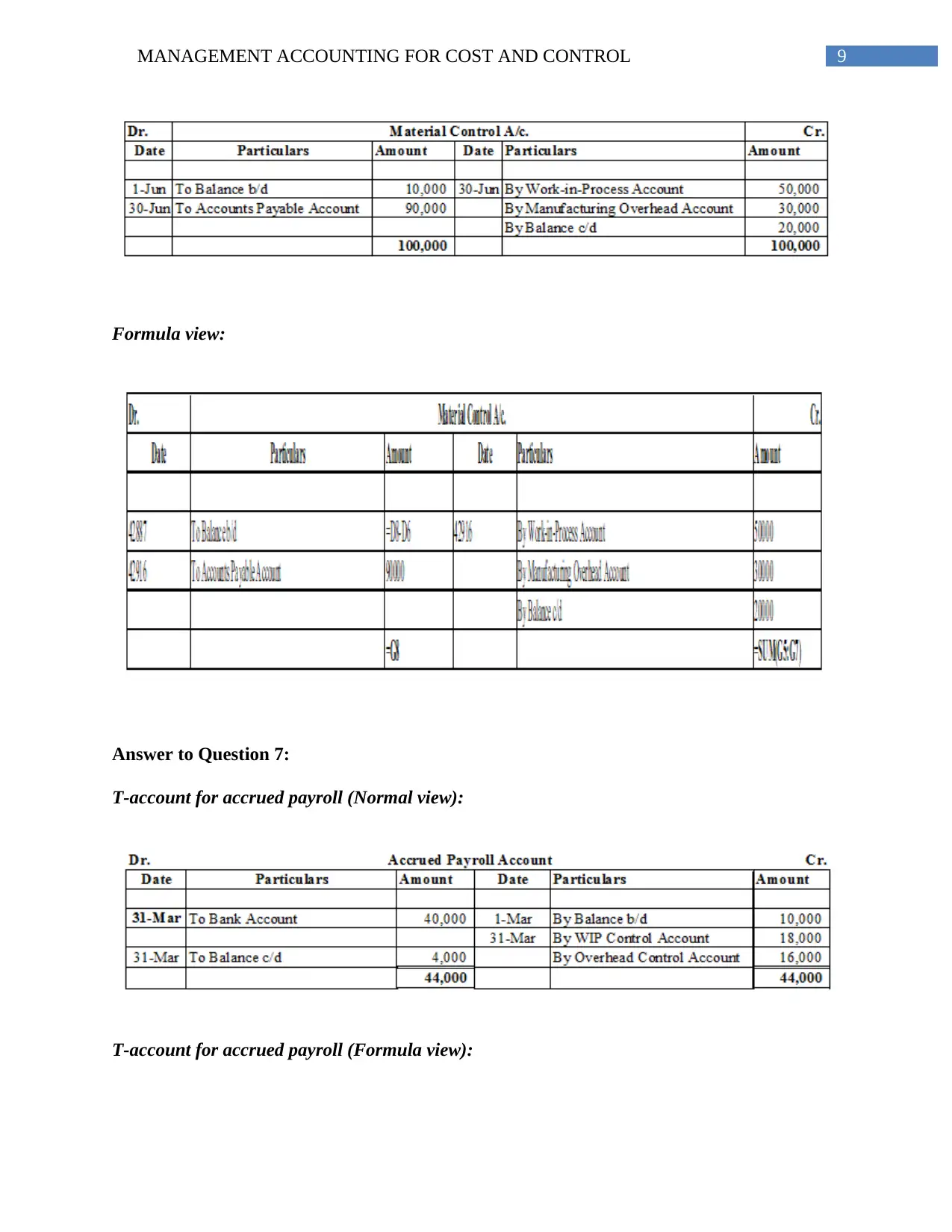

This document presents a detailed solution to a management accounting assignment, addressing key concepts such as budgeting, cost control, product costing, and activity-based costing. The assignment covers various aspects, including the purposes of management accounting reports, the role of control in achieving organizational goals, and the application of different costing methods. It includes calculations, journal entries, and T-accounts related to labor costs, overhead allocation, and service department cost allocation using direct, step, and reciprocal methods. The solution also provides a comparison between traditional costing and activity-based costing, emphasizing the benefits of the latter. References to relevant academic literature are included. Desklib provides past papers and solved assignments for students.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.