University Cost Accounting: Management and Control Assignment

VerifiedAdded on 2019/12/28

|11

|2596

|205

Homework Assignment

AI Summary

This assignment solution delves into key aspects of management accounting, specifically focusing on cost and control. It begins by defining the elements of cost, differentiating between direct and indirect materials, labor, and overheads. The solution then explores different costing techniques, including the recording of costs and the use of averaging techniques for inventory management. It further examines cost concepts like prime cost, product cost, and conversion cost. A significant portion of the assignment is dedicated to a manufacturing statement and profitability statement, illustrating how costs are calculated and profits are determined. The solution also addresses the treatment of overtime payments and provides journal entries for material control and accrued payroll. Finally, it compares traditional costing with activity-based costing (ABC), highlighting the advantages and disadvantages of each approach, and concludes with a detailed explanation of different overhead allocation methods, including direct, step-down, and reciprocal methods, providing calculations for each.

MANAGEMENT

ACCOUNTING FOR

COST AND CONTROL

ACCOUNTING FOR

COST AND CONTROL

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

ASSIGNMENT 1.............................................................................................................................3

QUESTION 1..................................................................................................................................3

QUESTION 2..................................................................................................................................3

QUESTION 3..................................................................................................................................4

QUESTION 4..................................................................................................................................5

QUESTION 5..................................................................................................................................6

QUESTION 6..................................................................................................................................6

QUESTION 7..................................................................................................................................7

QUESTION 9..................................................................................................................................8

QUESTION 10................................................................................................................................8

REFERENCES..............................................................................................................................11

ASSIGNMENT 1.............................................................................................................................3

QUESTION 1..................................................................................................................................3

QUESTION 2..................................................................................................................................3

QUESTION 3..................................................................................................................................4

QUESTION 4..................................................................................................................................5

QUESTION 5..................................................................................................................................6

QUESTION 6..................................................................................................................................6

QUESTION 7..................................................................................................................................7

QUESTION 9..................................................................................................................................8

QUESTION 10................................................................................................................................8

REFERENCES..............................................................................................................................11

ASSIGNMENT 1

Costing is an important part at the workplace. It helps in determining the actual price of

the product as well as the cost which is incur in the product, so better and effective cost

management different approaches are to be used. In the present report the whole discussion is

based on the major cost elements which are helpful in making the cost of a product. Along with

that all such factors and techniques which are beneficial in making cost effective are also be

considered. Also the cost which is incurred on the manufacturing plants are taken into points.

QUESTION 1

ELEMENTS OF COST

MATERIAL- Material cost is the tangible goods used in producing the project. This cost

can be direct or indirect. Direct material is quantifiable and can be traced and indirect material is

unquantifiable and cannot be traced.

For example – A company producing furniture may consider wood as a direct material because it

can be quantified.

LABOUR- Wages and salaries paid to the employees involved in manufacturing are

called as labour the cost can be divided into direct and indirect labour cost (Höglund and et.al.,

2016). Labour cost includes wages paid and indirect costs include other wages and incentives but

are not traceable.

For example-Wages for line managers are considered to be the direct cost.

OVERHEAD- Overhead cost is those cost that are related to production but are not

classified as direct or indirect cost. Common overheads includes depreciation on machinery,

factory equipment etc.

For example- Indirect material and Indirect labour

QUESTION 2

There are many products at workplace whose recording is must they helps in estimating a

proper balance for each and every material in a factory but for averaging technique small

business uses this approach for their business. Basically it can be said that recording cost is for

large business organisation but average techniques is for the small business.

The three best examples of using recording cost techniques are:

Costing is an important part at the workplace. It helps in determining the actual price of

the product as well as the cost which is incur in the product, so better and effective cost

management different approaches are to be used. In the present report the whole discussion is

based on the major cost elements which are helpful in making the cost of a product. Along with

that all such factors and techniques which are beneficial in making cost effective are also be

considered. Also the cost which is incurred on the manufacturing plants are taken into points.

QUESTION 1

ELEMENTS OF COST

MATERIAL- Material cost is the tangible goods used in producing the project. This cost

can be direct or indirect. Direct material is quantifiable and can be traced and indirect material is

unquantifiable and cannot be traced.

For example – A company producing furniture may consider wood as a direct material because it

can be quantified.

LABOUR- Wages and salaries paid to the employees involved in manufacturing are

called as labour the cost can be divided into direct and indirect labour cost (Höglund and et.al.,

2016). Labour cost includes wages paid and indirect costs include other wages and incentives but

are not traceable.

For example-Wages for line managers are considered to be the direct cost.

OVERHEAD- Overhead cost is those cost that are related to production but are not

classified as direct or indirect cost. Common overheads includes depreciation on machinery,

factory equipment etc.

For example- Indirect material and Indirect labour

QUESTION 2

There are many products at workplace whose recording is must they helps in estimating a

proper balance for each and every material in a factory but for averaging technique small

business uses this approach for their business. Basically it can be said that recording cost is for

large business organisation but average techniques is for the small business.

The three best examples of using recording cost techniques are:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1. Land and building: This method is used just for the purpose of calculating the

depreciation of the assets (Kaplan and Atkinson, 2015). With the help of calculating

proper depreciation on assets it helps in getting the actual value of the fixed assets.

2. Plant and machinery: These are used with aim of manufacturing goods and products. So,

this is important for a business to maintain proper record of each and every valuables of

the organisation.

The three best examples of average techniques are as follow:

1. Grocery store: They maintain their stock just for getting the proper knowledgeable about

their products and inventory. This is one of the best way for calculating the actual stock

value in the store. So, that all things can be stored properly.

2. Small business enterprises: The average technique is used by the small business because

it helps them in manage their stock and also helps in reducing the cost of the production.

Because they use their previous year stock for the current year (Lapsley and Rekers,

2017).

3. Small firms: They manage their accounts and calculate the cost which is incurred on the

production.

QUESTION 3

Cost concepts

Prime cost: It comprises the direct costs of all the essential elements like direct material,

direct labour and direct overheads.

Product cost: This comprises payments or expenditures incurred to produce goods or

service i.e. direct material and labour, consumables, factory overheads and so on.

Period cost: As name implies, it is closely related to the fixed passage of time like selling

expense.

Conversion cost: It refers to the cost of labour and overheads that are necessary to

convert raw material into finished goods known as conversion cost (Nuhu, Baird and Bala

Appuhamilage, 2017).

Inventoriable cost: All the expenses which firm incur to get the material into a situation

of ready for sale are called inventoriable costs. It consists of material, labour and both the fixed

& variable overheads.

depreciation of the assets (Kaplan and Atkinson, 2015). With the help of calculating

proper depreciation on assets it helps in getting the actual value of the fixed assets.

2. Plant and machinery: These are used with aim of manufacturing goods and products. So,

this is important for a business to maintain proper record of each and every valuables of

the organisation.

The three best examples of average techniques are as follow:

1. Grocery store: They maintain their stock just for getting the proper knowledgeable about

their products and inventory. This is one of the best way for calculating the actual stock

value in the store. So, that all things can be stored properly.

2. Small business enterprises: The average technique is used by the small business because

it helps them in manage their stock and also helps in reducing the cost of the production.

Because they use their previous year stock for the current year (Lapsley and Rekers,

2017).

3. Small firms: They manage their accounts and calculate the cost which is incurred on the

production.

QUESTION 3

Cost concepts

Prime cost: It comprises the direct costs of all the essential elements like direct material,

direct labour and direct overheads.

Product cost: This comprises payments or expenditures incurred to produce goods or

service i.e. direct material and labour, consumables, factory overheads and so on.

Period cost: As name implies, it is closely related to the fixed passage of time like selling

expense.

Conversion cost: It refers to the cost of labour and overheads that are necessary to

convert raw material into finished goods known as conversion cost (Nuhu, Baird and Bala

Appuhamilage, 2017).

Inventoriable cost: All the expenses which firm incur to get the material into a situation

of ready for sale are called inventoriable costs. It consists of material, labour and both the fixed

& variable overheads.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

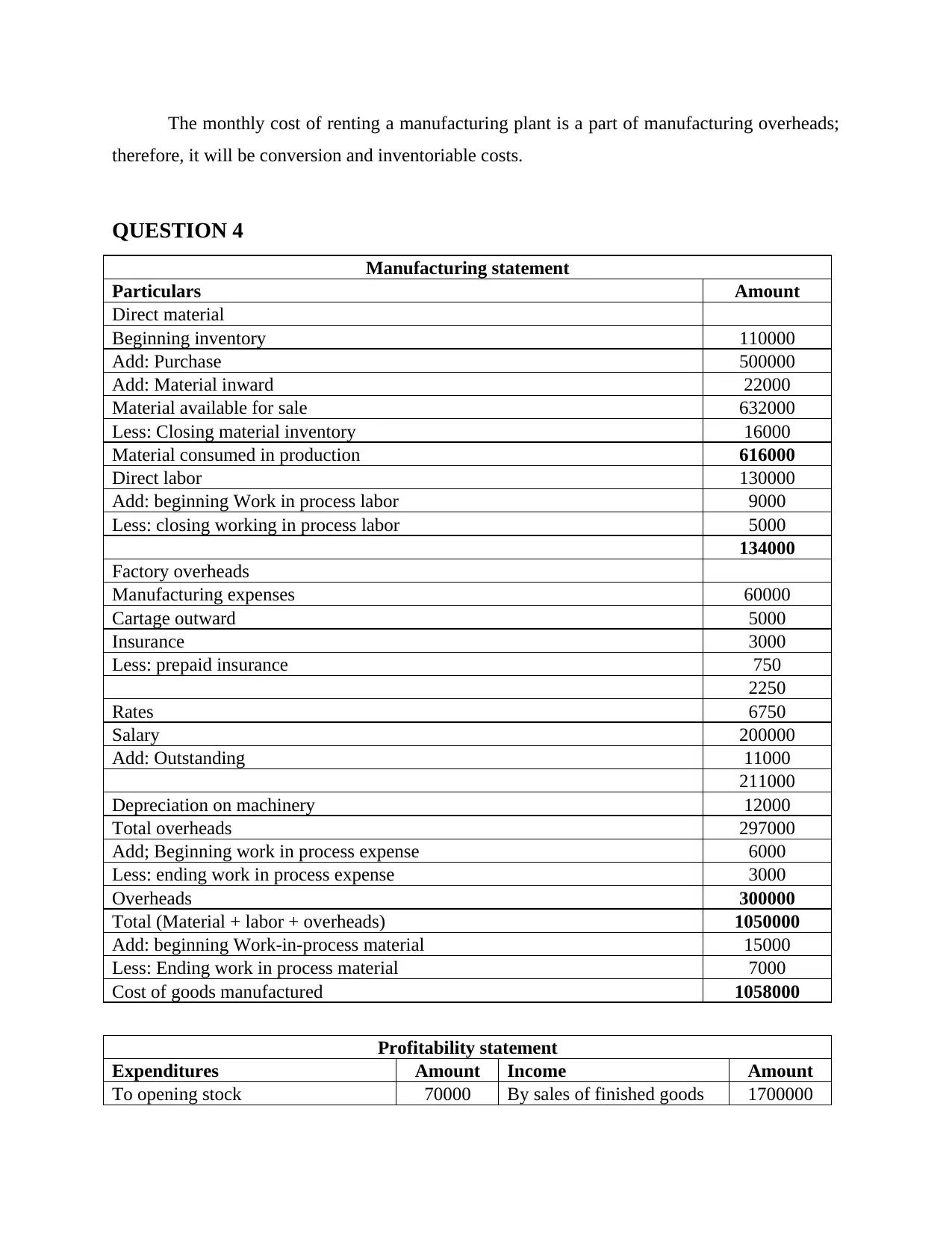

The monthly cost of renting a manufacturing plant is a part of manufacturing overheads;

therefore, it will be conversion and inventoriable costs.

QUESTION 4

Manufacturing statement

Particulars Amount

Direct material

Beginning inventory 110000

Add: Purchase 500000

Add: Material inward 22000

Material available for sale 632000

Less: Closing material inventory 16000

Material consumed in production 616000

Direct labor 130000

Add: beginning Work in process labor 9000

Less: closing working in process labor 5000

134000

Factory overheads

Manufacturing expenses 60000

Cartage outward 5000

Insurance 3000

Less: prepaid insurance 750

2250

Rates 6750

Salary 200000

Add: Outstanding 11000

211000

Depreciation on machinery 12000

Total overheads 297000

Add; Beginning work in process expense 6000

Less: ending work in process expense 3000

Overheads 300000

Total (Material + labor + overheads) 1050000

Add: beginning Work-in-process material 15000

Less: Ending work in process material 7000

Cost of goods manufactured 1058000

Profitability statement

Expenditures Amount Income Amount

To opening stock 70000 By sales of finished goods 1700000

therefore, it will be conversion and inventoriable costs.

QUESTION 4

Manufacturing statement

Particulars Amount

Direct material

Beginning inventory 110000

Add: Purchase 500000

Add: Material inward 22000

Material available for sale 632000

Less: Closing material inventory 16000

Material consumed in production 616000

Direct labor 130000

Add: beginning Work in process labor 9000

Less: closing working in process labor 5000

134000

Factory overheads

Manufacturing expenses 60000

Cartage outward 5000

Insurance 3000

Less: prepaid insurance 750

2250

Rates 6750

Salary 200000

Add: Outstanding 11000

211000

Depreciation on machinery 12000

Total overheads 297000

Add; Beginning work in process expense 6000

Less: ending work in process expense 3000

Overheads 300000

Total (Material + labor + overheads) 1050000

Add: beginning Work-in-process material 15000

Less: Ending work in process material 7000

Cost of goods manufactured 1058000

Profitability statement

Expenditures Amount Income Amount

To opening stock 70000 By sales of finished goods 1700000

To cost of goods manufactured 1058000 By closing stock 25000

To gross profit (b/f) 597000

1725000 1725000

To discount 6000 By gross profit b/d 597000

To advertisement 12000 By discount receipts 4000

To audit fees 3000

To rates 2250

To insurance (25%) 1000

Less: Prepaid (25%) 250 750

To light and power 12000

To general expense 9000

To salary 100000

Add: Accrued salary 700 100700

To sales commission 40000

To tax expense 50000

To net profit (Balance figure) 365300

601000 601000

QUESTION 5

Overtime payments should not be considered as a direct labour and always considered as

a part of indirect labour. Overtime refers to the amount paid by the company for the extra work

performed by the workers (Schroeder, Clark and Cathey, 2016). It is treated as an indirect cost of

labour while figuring out the cost of manufacturing. For instance, a worker worked for 51 hours

exceeded the normal working hours 48 and the normal wages rate is 8GBP/hour whereas the

work performed in excess to 48 hour will be paid at 12GBP. Thus, it will be treated as follows:

Direct labor (51*8GBP) = 408GBP

Manufacturing overheads (3 hours *4GBP) = 12GBP

Total cost = 420GBP

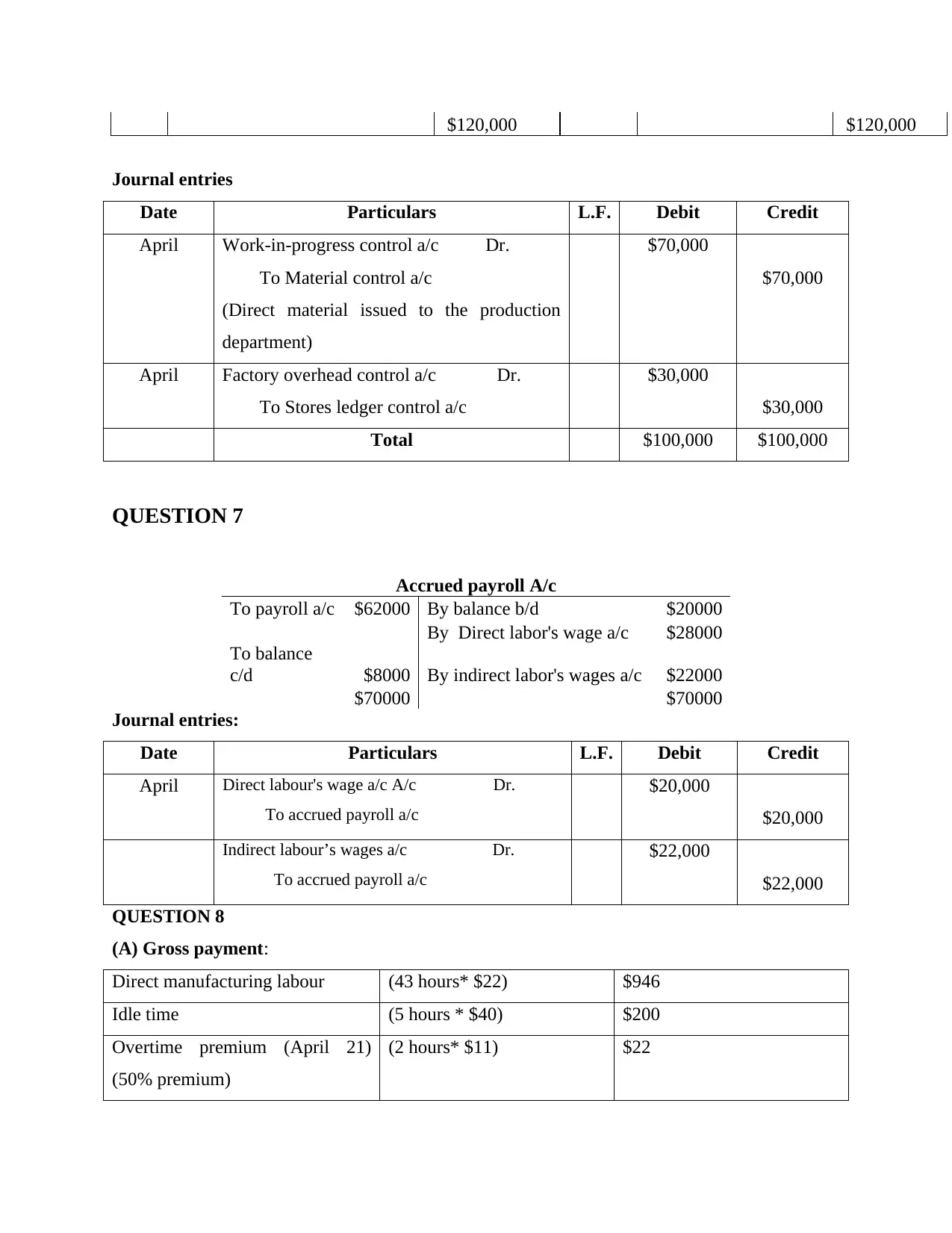

QUESTION 6

Material control account

1st

April To balance b/d $40,000.00

By work in progress

control a/c $70,000.00

To General ledger control a/c

(b/f) (material purchase) $ 80,000.00

By factory overhead

control a/c $30,000.00

30th

April By balance c/d $20,000.00

To gross profit (b/f) 597000

1725000 1725000

To discount 6000 By gross profit b/d 597000

To advertisement 12000 By discount receipts 4000

To audit fees 3000

To rates 2250

To insurance (25%) 1000

Less: Prepaid (25%) 250 750

To light and power 12000

To general expense 9000

To salary 100000

Add: Accrued salary 700 100700

To sales commission 40000

To tax expense 50000

To net profit (Balance figure) 365300

601000 601000

QUESTION 5

Overtime payments should not be considered as a direct labour and always considered as

a part of indirect labour. Overtime refers to the amount paid by the company for the extra work

performed by the workers (Schroeder, Clark and Cathey, 2016). It is treated as an indirect cost of

labour while figuring out the cost of manufacturing. For instance, a worker worked for 51 hours

exceeded the normal working hours 48 and the normal wages rate is 8GBP/hour whereas the

work performed in excess to 48 hour will be paid at 12GBP. Thus, it will be treated as follows:

Direct labor (51*8GBP) = 408GBP

Manufacturing overheads (3 hours *4GBP) = 12GBP

Total cost = 420GBP

QUESTION 6

Material control account

1st

April To balance b/d $40,000.00

By work in progress

control a/c $70,000.00

To General ledger control a/c

(b/f) (material purchase) $ 80,000.00

By factory overhead

control a/c $30,000.00

30th

April By balance c/d $20,000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

$120,000 $120,000

Journal entries

Date Particulars L.F. Debit Credit

April Work-in-progress control a/c Dr.

To Material control a/c

(Direct material issued to the production

department)

$70,000

$70,000

April Factory overhead control a/c Dr.

To Stores ledger control a/c

$30,000

$30,000

Total $100,000 $100,000

QUESTION 7

Accrued payroll A/c

To payroll a/c $62000 By balance b/d $20000

By Direct labor's wage a/c $28000

To balance

c/d $8000 By indirect labor's wages a/c $22000

$70000 $70000

Journal entries:

Date Particulars L.F. Debit Credit

April Direct labour's wage a/c A/c Dr.

To accrued payroll a/c

$20,000

$20,000

Indirect labour’s wages a/c Dr.

To accrued payroll a/c

$22,000

$22,000

QUESTION 8

(A) Gross payment:

Direct manufacturing labour (43 hours* $22) $946

Idle time (5 hours * $40) $200

Overtime premium (April 21)

(50% premium)

(2 hours* $11) $22

Journal entries

Date Particulars L.F. Debit Credit

April Work-in-progress control a/c Dr.

To Material control a/c

(Direct material issued to the production

department)

$70,000

$70,000

April Factory overhead control a/c Dr.

To Stores ledger control a/c

$30,000

$30,000

Total $100,000 $100,000

QUESTION 7

Accrued payroll A/c

To payroll a/c $62000 By balance b/d $20000

By Direct labor's wage a/c $28000

To balance

c/d $8000 By indirect labor's wages a/c $22000

$70000 $70000

Journal entries:

Date Particulars L.F. Debit Credit

April Direct labour's wage a/c A/c Dr.

To accrued payroll a/c

$20,000

$20,000

Indirect labour’s wages a/c Dr.

To accrued payroll a/c

$22,000

$22,000

QUESTION 8

(A) Gross payment:

Direct manufacturing labour (43 hours* $22) $946

Idle time (5 hours * $40) $200

Overtime premium (April 21)

(50% premium)

(2 hours* $11) $22

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

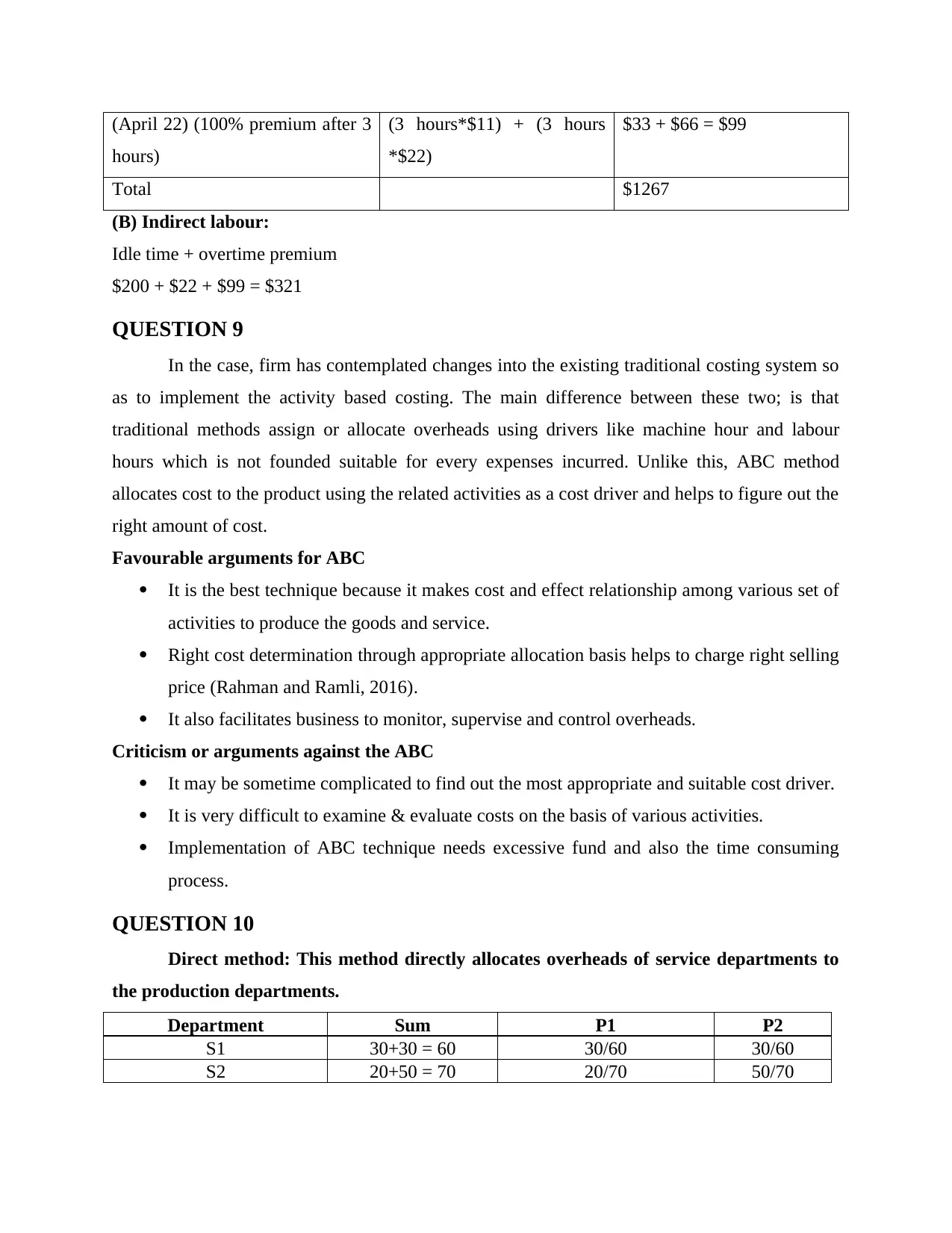

(April 22) (100% premium after 3

hours)

(3 hours*$11) + (3 hours

*$22)

$33 + $66 = $99

Total $1267

(B) Indirect labour:

Idle time + overtime premium

$200 + $22 + $99 = $321

QUESTION 9

In the case, firm has contemplated changes into the existing traditional costing system so

as to implement the activity based costing. The main difference between these two; is that

traditional methods assign or allocate overheads using drivers like machine hour and labour

hours which is not founded suitable for every expenses incurred. Unlike this, ABC method

allocates cost to the product using the related activities as a cost driver and helps to figure out the

right amount of cost.

Favourable arguments for ABC

It is the best technique because it makes cost and effect relationship among various set of

activities to produce the goods and service.

Right cost determination through appropriate allocation basis helps to charge right selling

price (Rahman and Ramli, 2016).

It also facilitates business to monitor, supervise and control overheads.

Criticism or arguments against the ABC

It may be sometime complicated to find out the most appropriate and suitable cost driver.

It is very difficult to examine & evaluate costs on the basis of various activities.

Implementation of ABC technique needs excessive fund and also the time consuming

process.

QUESTION 10

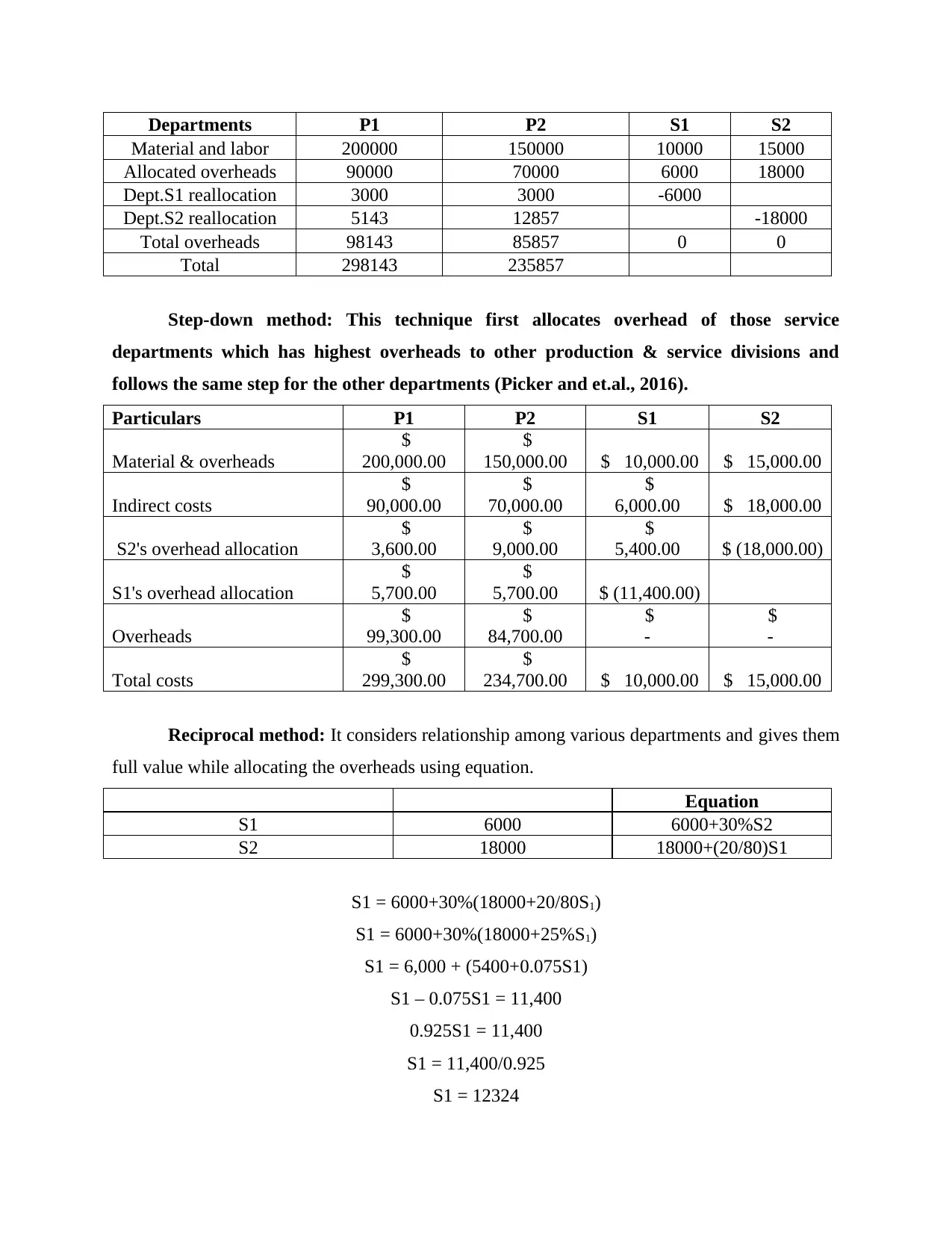

Direct method: This method directly allocates overheads of service departments to

the production departments.

Department Sum P1 P2

S1 30+30 = 60 30/60 30/60

S2 20+50 = 70 20/70 50/70

hours)

(3 hours*$11) + (3 hours

*$22)

$33 + $66 = $99

Total $1267

(B) Indirect labour:

Idle time + overtime premium

$200 + $22 + $99 = $321

QUESTION 9

In the case, firm has contemplated changes into the existing traditional costing system so

as to implement the activity based costing. The main difference between these two; is that

traditional methods assign or allocate overheads using drivers like machine hour and labour

hours which is not founded suitable for every expenses incurred. Unlike this, ABC method

allocates cost to the product using the related activities as a cost driver and helps to figure out the

right amount of cost.

Favourable arguments for ABC

It is the best technique because it makes cost and effect relationship among various set of

activities to produce the goods and service.

Right cost determination through appropriate allocation basis helps to charge right selling

price (Rahman and Ramli, 2016).

It also facilitates business to monitor, supervise and control overheads.

Criticism or arguments against the ABC

It may be sometime complicated to find out the most appropriate and suitable cost driver.

It is very difficult to examine & evaluate costs on the basis of various activities.

Implementation of ABC technique needs excessive fund and also the time consuming

process.

QUESTION 10

Direct method: This method directly allocates overheads of service departments to

the production departments.

Department Sum P1 P2

S1 30+30 = 60 30/60 30/60

S2 20+50 = 70 20/70 50/70

Departments P1 P2 S1 S2

Material and labor 200000 150000 10000 15000

Allocated overheads 90000 70000 6000 18000

Dept.S1 reallocation 3000 3000 -6000

Dept.S2 reallocation 5143 12857 -18000

Total overheads 98143 85857 0 0

Total 298143 235857

Step-down method: This technique first allocates overhead of those service

departments which has highest overheads to other production & service divisions and

follows the same step for the other departments (Picker and et.al., 2016).

Particulars P1 P2 S1 S2

Material & overheads

$

200,000.00

$

150,000.00 $ 10,000.00 $ 15,000.00

Indirect costs

$

90,000.00

$

70,000.00

$

6,000.00 $ 18,000.00

S2's overhead allocation

$

3,600.00

$

9,000.00

$

5,400.00 $ (18,000.00)

S1's overhead allocation

$

5,700.00

$

5,700.00 $ (11,400.00)

Overheads

$

99,300.00

$

84,700.00

$

-

$

-

Total costs

$

299,300.00

$

234,700.00 $ 10,000.00 $ 15,000.00

Reciprocal method: It considers relationship among various departments and gives them

full value while allocating the overheads using equation.

Equation

S1 6000 6000+30%S2

S2 18000 18000+(20/80)S1

S1 = 6000+30%(18000+20/80S1)

S1 = 6000+30%(18000+25%S1)

S1 = 6,000 + (5400+0.075S1)

S1 – 0.075S1 = 11,400

0.925S1 = 11,400

S1 = 11,400/0.925

S1 = 12324

Material and labor 200000 150000 10000 15000

Allocated overheads 90000 70000 6000 18000

Dept.S1 reallocation 3000 3000 -6000

Dept.S2 reallocation 5143 12857 -18000

Total overheads 98143 85857 0 0

Total 298143 235857

Step-down method: This technique first allocates overhead of those service

departments which has highest overheads to other production & service divisions and

follows the same step for the other departments (Picker and et.al., 2016).

Particulars P1 P2 S1 S2

Material & overheads

$

200,000.00

$

150,000.00 $ 10,000.00 $ 15,000.00

Indirect costs

$

90,000.00

$

70,000.00

$

6,000.00 $ 18,000.00

S2's overhead allocation

$

3,600.00

$

9,000.00

$

5,400.00 $ (18,000.00)

S1's overhead allocation

$

5,700.00

$

5,700.00 $ (11,400.00)

Overheads

$

99,300.00

$

84,700.00

$

-

$

-

Total costs

$

299,300.00

$

234,700.00 $ 10,000.00 $ 15,000.00

Reciprocal method: It considers relationship among various departments and gives them

full value while allocating the overheads using equation.

Equation

S1 6000 6000+30%S2

S2 18000 18000+(20/80)S1

S1 = 6000+30%(18000+20/80S1)

S1 = 6000+30%(18000+25%S1)

S1 = 6,000 + (5400+0.075S1)

S1 – 0.075S1 = 11,400

0.925S1 = 11,400

S1 = 11,400/0.925

S1 = 12324

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

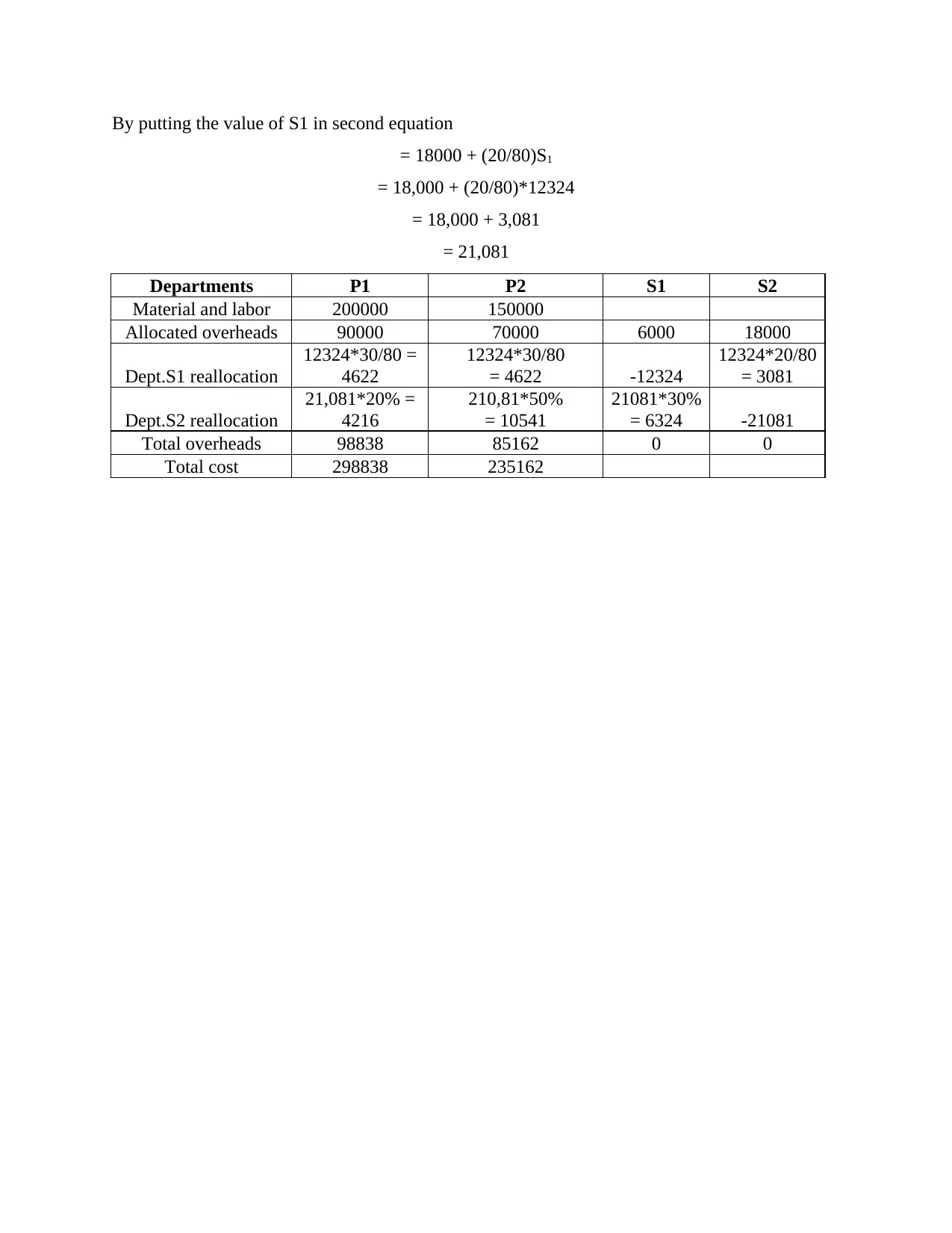

By putting the value of S1 in second equation

= 18000 + (20/80)S1

= 18,000 + (20/80)*12324

= 18,000 + 3,081

= 21,081

Departments P1 P2 S1 S2

Material and labor 200000 150000

Allocated overheads 90000 70000 6000 18000

Dept.S1 reallocation

12324*30/80 =

4622

12324*30/80

= 4622 -12324

12324*20/80

= 3081

Dept.S2 reallocation

21,081*20% =

4216

210,81*50%

= 10541

21081*30%

= 6324 -21081

Total overheads 98838 85162 0 0

Total cost 298838 235162

= 18000 + (20/80)S1

= 18,000 + (20/80)*12324

= 18,000 + 3,081

= 21,081

Departments P1 P2 S1 S2

Material and labor 200000 150000

Allocated overheads 90000 70000 6000 18000

Dept.S1 reallocation

12324*30/80 =

4622

12324*30/80

= 4622 -12324

12324*20/80

= 3081

Dept.S2 reallocation

21,081*20% =

4216

210,81*50%

= 10541

21081*30%

= 6324 -21081

Total overheads 98838 85162 0 0

Total cost 298838 235162

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Höglund, L. and et.al., 2016. Management accounting of control practices: a matter of and for

strategy. Inthe 9TH INTERNATIONAL EIASM PUBLIC SECTOR CONFERENCE, held

in LISBON, PORTUGAL, SEPTEMBER 6-8, 2016. 12(3). pp.12-39.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Lapsley, I. and Rekers, J.V., 2017. The relevance of strategic management accounting to popular

culture: The world of West End Musicals. Management Accounting Research.

Nuhu, N.A., Baird, K. and Bala Appuhamilage, A., 2017. The adoption and success of

contemporary management accounting practices in the public sector. Asian Review of

Accounting. 25(1). pp.10-46.

Picker, R. and et.al., 2016. Applying international financial reporting standards. John Wiley &

Sons.

Rahman, N.A.A. and Ramli, A., 2016. Entrepreneurial Orientation, Strategic Management

Accounting Practices, Innovation, and Firm Performance: Craft Industry Perspective. In

Proceedings of the ASEAN Entrepreneurship Conference 2014. Springer Singapore.

10(3). pp.179-191

Schroeder, R.G., Clark, M.W. and Cathey, J.M., 2016. Financial Accounting Theory and

Analysis: Text and Cases: Text and Cases. Wiley Global Education.

Books and Journals

Höglund, L. and et.al., 2016. Management accounting of control practices: a matter of and for

strategy. Inthe 9TH INTERNATIONAL EIASM PUBLIC SECTOR CONFERENCE, held

in LISBON, PORTUGAL, SEPTEMBER 6-8, 2016. 12(3). pp.12-39.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Lapsley, I. and Rekers, J.V., 2017. The relevance of strategic management accounting to popular

culture: The world of West End Musicals. Management Accounting Research.

Nuhu, N.A., Baird, K. and Bala Appuhamilage, A., 2017. The adoption and success of

contemporary management accounting practices in the public sector. Asian Review of

Accounting. 25(1). pp.10-46.

Picker, R. and et.al., 2016. Applying international financial reporting standards. John Wiley &

Sons.

Rahman, N.A.A. and Ramli, A., 2016. Entrepreneurial Orientation, Strategic Management

Accounting Practices, Innovation, and Firm Performance: Craft Industry Perspective. In

Proceedings of the ASEAN Entrepreneurship Conference 2014. Springer Singapore.

10(3). pp.179-191

Schroeder, R.G., Clark, M.W. and Cathey, J.M., 2016. Financial Accounting Theory and

Analysis: Text and Cases: Text and Cases. Wiley Global Education.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.