Kensington College: Management Accounting Systems and its Applications

VerifiedAdded on 2023/01/17

|18

|5329

|26

Report

AI Summary

This report provides a comprehensive analysis of management accounting systems and their practical applications. It begins by defining management accounting and its crucial requirements, including different types of management accounting systems such as job costing, price optimization, inventory management, and cost accounting systems. The report then elaborates on various management accounting reporting methods, including inventory management reports, budget reports, performance reports, and accounts receivable aging reports. Furthermore, it delves into the computation of costs for preparing income statements using marginal and absorption costing techniques, including detailed calculations. The report also explores the assets and detriments of various planning tools used in management accounting. Finally, it draws analogies among firms for the adoption of management accounting systems in responding to financial problems, offering a complete overview of the subject matter.

Management Accounting

Systems and its Applications

Systems and its Applications

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Define management accounting and their crucial requirements of their types.................1

P2 Elaborate methods of management accounting reporting.................................................3

TASK 2............................................................................................................................................4

P3 Computation of costs for preparation of income statement through marginal and absorption

costs........................................................................................................................................4

TASK 3..........................................................................................................................................10

P4 Assets and detriment of various kinds of planning tools................................................10

TASK 4..........................................................................................................................................13

P5 Analogy among firms for adoption of management accounting system for responding to

financial................................................................................................................................13

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Define management accounting and their crucial requirements of their types.................1

P2 Elaborate methods of management accounting reporting.................................................3

TASK 2............................................................................................................................................4

P3 Computation of costs for preparation of income statement through marginal and absorption

costs........................................................................................................................................4

TASK 3..........................................................................................................................................10

P4 Assets and detriment of various kinds of planning tools................................................10

TASK 4..........................................................................................................................................13

P5 Analogy among firms for adoption of management accounting system for responding to

financial................................................................................................................................13

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

INTRODUCTION

Management or managerial accounting refers to process of furnishing financial resources

as well as information to the managers for formulation of decisions. Management accounting

aims at usage of statistical data for building up accurate and efficacious decision, management of

enterprise, development and business activities. Basically, this denotes application of knowledge

and professional skills for preparation of information related with accounting and finance

(Harrison and Lock, 2017). In addition to this, it aids firm within development of planning,

control of operations and planning for them accordingly. To understand the concept of

management accounting, Berkeley Partnership was brought in 1990. They render diverse to their

client firms in the form of independent management consultants. Essentra packaging is one of

their client who is a manufacturing organisation and deals within tear tapes. This deals with

management accounting their types and methods for their reporting. In addition to this, different

costs have been calculated and merits and demerits of planning tools have been illustrated.

Furthermore, comparison has been shown among accounting systems to financial issues.

TASK 1

P1 Define management accounting and their crucial requirements of their types.

The process of preparation of accounts and reports which render precise, timely statistical

and financial information needed by managers for taking short term decisions with respect to day

to day decisions is referred to management accounting. This will assist Essentra packaging to

build up policies and plans according to activities they have to carry out. It will aid them for

carrying out performance analysis by creating hypothesis of strategies, budgeting, forecasting

and many others. Generally, it comprises of presenting information related with accounting.

There are wide range of assets that are being offered by management accounting and can be

utilised by Essentra packaging to attain their goals in an appropriate manner (Chiarini and

Vagnoni, 2015).

Management accounting system refers to internal systems which are used by organisation

for evaluation and measurement of performance. Essentra packaging can make use of these

systems to formulate policies for each department depending upon their performance so that

affirmative results can can be attained. This will enable management to have precise information

and decisions can build up accordingly. Thus, it is necessary for Essentra packaging to make use

1

Management or managerial accounting refers to process of furnishing financial resources

as well as information to the managers for formulation of decisions. Management accounting

aims at usage of statistical data for building up accurate and efficacious decision, management of

enterprise, development and business activities. Basically, this denotes application of knowledge

and professional skills for preparation of information related with accounting and finance

(Harrison and Lock, 2017). In addition to this, it aids firm within development of planning,

control of operations and planning for them accordingly. To understand the concept of

management accounting, Berkeley Partnership was brought in 1990. They render diverse to their

client firms in the form of independent management consultants. Essentra packaging is one of

their client who is a manufacturing organisation and deals within tear tapes. This deals with

management accounting their types and methods for their reporting. In addition to this, different

costs have been calculated and merits and demerits of planning tools have been illustrated.

Furthermore, comparison has been shown among accounting systems to financial issues.

TASK 1

P1 Define management accounting and their crucial requirements of their types.

The process of preparation of accounts and reports which render precise, timely statistical

and financial information needed by managers for taking short term decisions with respect to day

to day decisions is referred to management accounting. This will assist Essentra packaging to

build up policies and plans according to activities they have to carry out. It will aid them for

carrying out performance analysis by creating hypothesis of strategies, budgeting, forecasting

and many others. Generally, it comprises of presenting information related with accounting.

There are wide range of assets that are being offered by management accounting and can be

utilised by Essentra packaging to attain their goals in an appropriate manner (Chiarini and

Vagnoni, 2015).

Management accounting system refers to internal systems which are used by organisation

for evaluation and measurement of performance. Essentra packaging can make use of these

systems to formulate policies for each department depending upon their performance so that

affirmative results can can be attained. This will enable management to have precise information

and decisions can build up accordingly. Thus, it is necessary for Essentra packaging to make use

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of this tool as it deals with both financial and non-financial data that will assist them within

carrying out their business operations.

Firms can make use of management accounting systems as per their requirements and

demand of the situation. For an instance Essentra packaging can make use costing accounting

system with respect to management of their inventory. Price optimisation system can be applied

by them for furnishing framework for determining prices of their commodities. Similarly

different systems serves diverse purposes and can be utilised accordingly.

Management accounting system was brought in England during industrial revolution.

This involves various operations through which issues related with financial problems can be

sorted out (Armitage, Webb and Glynn, 2016). Principle of management accounting deals with

creating an influence as well as build up trust so that operations of organisation can be oriented

and synchronised.

Difference between management and financial accounting

Management accounting Financial accounting

It is utilised by Essentra Packaging for carrying

out their internal operations. Figures and facts

are confidential and are being utilised for

formulating decisions.

Reporting is carried out for public view, all

facts, figures and amounts are are publicly

disclosed.

In this case there are not specified format or

pattern for reporting. Figures are illustrated as

per target audiences and may not comprise

information according to requirements.

With respect to this universal reporting

standards associated with accounting are being

used such as GAAP, IFRS, etc. that can be

understood by individuals easily.

Essentra packaging can have financial and

non-financial data by its usage in their reports

according to requirements.

They aims at firms financial data (Financial

accounting vs Management Accounting, 2019).

No formal audit structure is needed in such

kind of reporting.

In this case reports are initially audited and

then they are being reported or published.

Types of management accounting system

2

carrying out their business operations.

Firms can make use of management accounting systems as per their requirements and

demand of the situation. For an instance Essentra packaging can make use costing accounting

system with respect to management of their inventory. Price optimisation system can be applied

by them for furnishing framework for determining prices of their commodities. Similarly

different systems serves diverse purposes and can be utilised accordingly.

Management accounting system was brought in England during industrial revolution.

This involves various operations through which issues related with financial problems can be

sorted out (Armitage, Webb and Glynn, 2016). Principle of management accounting deals with

creating an influence as well as build up trust so that operations of organisation can be oriented

and synchronised.

Difference between management and financial accounting

Management accounting Financial accounting

It is utilised by Essentra Packaging for carrying

out their internal operations. Figures and facts

are confidential and are being utilised for

formulating decisions.

Reporting is carried out for public view, all

facts, figures and amounts are are publicly

disclosed.

In this case there are not specified format or

pattern for reporting. Figures are illustrated as

per target audiences and may not comprise

information according to requirements.

With respect to this universal reporting

standards associated with accounting are being

used such as GAAP, IFRS, etc. that can be

understood by individuals easily.

Essentra packaging can have financial and

non-financial data by its usage in their reports

according to requirements.

They aims at firms financial data (Financial

accounting vs Management Accounting, 2019).

No formal audit structure is needed in such

kind of reporting.

In this case reports are initially audited and

then they are being reported or published.

Types of management accounting system

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job costing system: In this case firm is liable for evaluation of entire expenditure that

will take place while carrying out any specified task. Organisation can conduct their activities

through complete data that has been incurred with respect to cost associated with peculiar

accounting time frame. Through this Essentra packaging can gather information related with

assigned job in terms of cost associated with each. This will lead firm to estimate overall cost

associated so that profits can be anticipated.

Price optimisation system: Within competitive market, it is crucial for firm to set prices

for their services or products within a defined format as this will aid them within improvisation

of overall profits. Organisation needs to identify market prices as well as demands of customers

within effectual way (Otley, 2016). This will assist them to evaluate attitude of customers,

preferences and tastes for product. It will have affirmative impact on overall sales of Essentra

packaging that will lead them to have enhanced profit for their services or products.

Inventory management system: Within firm there exists two crucial functions they are

production along with manufacturing that manages stock, inventory and also track structure of

organisation. This will assist Essentra packaging to check their inventory in a precise manner

along with this wastage will also be minimised and will lead them to have enhanced profit

margin. To improvise productivity organisation can build up strategies for this to ensure

optimum usage resources in suitable manner.

Cost accounting system: This denotes a framework that is being utilised by organisation

for estimation of cost associated with their products for inventory valuation, cost control and

profitability analysis. It is one of essential aspect as estimation of exact cost of products is

difficult for profitable activities. Essentra packaging must address products that can lead them to

have improvised profits but it is only possible when cost of services is accurately anticipated. It

denotes that it will enable firm to track their inventory flow with respect to various stages that

are associated with production (Appelbaum and et. al., 2017). Firm can make its usage for

recognition, allocation, classification, aggregation and reporting their costs so that comparison

can be carried out among costs.

P2 Elaborate methods of management accounting reporting

The process that gives guidelines to higher executives for building up decisions with

respect to their operations is referred to as management accounting reporting. Essentra packaging

3

will take place while carrying out any specified task. Organisation can conduct their activities

through complete data that has been incurred with respect to cost associated with peculiar

accounting time frame. Through this Essentra packaging can gather information related with

assigned job in terms of cost associated with each. This will lead firm to estimate overall cost

associated so that profits can be anticipated.

Price optimisation system: Within competitive market, it is crucial for firm to set prices

for their services or products within a defined format as this will aid them within improvisation

of overall profits. Organisation needs to identify market prices as well as demands of customers

within effectual way (Otley, 2016). This will assist them to evaluate attitude of customers,

preferences and tastes for product. It will have affirmative impact on overall sales of Essentra

packaging that will lead them to have enhanced profit for their services or products.

Inventory management system: Within firm there exists two crucial functions they are

production along with manufacturing that manages stock, inventory and also track structure of

organisation. This will assist Essentra packaging to check their inventory in a precise manner

along with this wastage will also be minimised and will lead them to have enhanced profit

margin. To improvise productivity organisation can build up strategies for this to ensure

optimum usage resources in suitable manner.

Cost accounting system: This denotes a framework that is being utilised by organisation

for estimation of cost associated with their products for inventory valuation, cost control and

profitability analysis. It is one of essential aspect as estimation of exact cost of products is

difficult for profitable activities. Essentra packaging must address products that can lead them to

have improvised profits but it is only possible when cost of services is accurately anticipated. It

denotes that it will enable firm to track their inventory flow with respect to various stages that

are associated with production (Appelbaum and et. al., 2017). Firm can make its usage for

recognition, allocation, classification, aggregation and reporting their costs so that comparison

can be carried out among costs.

P2 Elaborate methods of management accounting reporting

The process that gives guidelines to higher executives for building up decisions with

respect to their operations is referred to as management accounting reporting. Essentra packaging

3

can opt for these reports for analysing performance of their employees. Few reports are

explained beneath:

Inventory management report: This is one of the most crucial activity which is related

with building up reports so that they can have entire information about inventory. Essentra

packaging needs to identify various perspectives that are related to storage cost, closing of stocks

and many others. In addition to this, these reports deliver details about stocks and methods that

can be utilised by them for this. This aims at maintaining balance in between services that are

delivered to customers and management of inventory.

Budget Report: Essentra packaging have to furnish reports related with production in

context of future as this will assist them to carry out their operations in standardised manner.

Basically, it renders information about incentives that are being to their amount as this will boost

up their morale to perform their operations in an amplified manner (Alsharari, Dixon and

Youssef, 2015). It will aid firm to ensure that overall performance can be improvised in terms of

ways operations are being carried out.

Performance report: They are being carried out to measure performance of employees.

It involves detailed statements about incentives that are given to employees. This will help

Essentra packaging to inspire employees as it will lead them to identify overall profits they have

gained and also build up strategies by which they can amplify their growth. It will also assist

management to identify what improvisation do they need to make so that performance of

employees can be enhanced.

Accounts receivable ageing report: It will render important data in context of invoices

that are given to customers related with credits. This leads Essentra packaging to determine

amount that is to be paid along with credit memos. It is a tool that leads organisation to yield

favourable outcome in context of effectiveness of credits along with their gatherings & payments

overdue (Azudin and Mansor, 2018).

TASK 2

P3 Computation of costs for preparation of income statement through marginal and absorption

costs.

Cost denotes overall expenses that occurred while performing operations and activities

within premises of organisation. It is divided into various sections, they can be either variable,

4

explained beneath:

Inventory management report: This is one of the most crucial activity which is related

with building up reports so that they can have entire information about inventory. Essentra

packaging needs to identify various perspectives that are related to storage cost, closing of stocks

and many others. In addition to this, these reports deliver details about stocks and methods that

can be utilised by them for this. This aims at maintaining balance in between services that are

delivered to customers and management of inventory.

Budget Report: Essentra packaging have to furnish reports related with production in

context of future as this will assist them to carry out their operations in standardised manner.

Basically, it renders information about incentives that are being to their amount as this will boost

up their morale to perform their operations in an amplified manner (Alsharari, Dixon and

Youssef, 2015). It will aid firm to ensure that overall performance can be improvised in terms of

ways operations are being carried out.

Performance report: They are being carried out to measure performance of employees.

It involves detailed statements about incentives that are given to employees. This will help

Essentra packaging to inspire employees as it will lead them to identify overall profits they have

gained and also build up strategies by which they can amplify their growth. It will also assist

management to identify what improvisation do they need to make so that performance of

employees can be enhanced.

Accounts receivable ageing report: It will render important data in context of invoices

that are given to customers related with credits. This leads Essentra packaging to determine

amount that is to be paid along with credit memos. It is a tool that leads organisation to yield

favourable outcome in context of effectiveness of credits along with their gatherings & payments

overdue (Azudin and Mansor, 2018).

TASK 2

P3 Computation of costs for preparation of income statement through marginal and absorption

costs.

Cost denotes overall expenses that occurred while performing operations and activities

within premises of organisation. It is divided into various sections, they can be either variable,

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

fixed, indirect or direct. Essentra packaging have different kinds of cost that occurs while they

are carrying out their operations. For an instance cost of raw materials, labour, suppliers and

many others. This denotes complete processes that are being associated with computation of

entire cost. It will enable the management to identify cost of individual operations.

Cost volume profit analysis: It is a analysis technique which deals with determination of

divergence among cost and profits that are furnished by carrying out specified operations. Its

objective is to analyse financial situations of firms in context of divergence in between assorted

factors.

Flexible budgeting: This is defined as budgeting techniques in which values related with

overall budget can be altered with respect to volumes that have been produced and sales that

incurred (Spraakman and et. al., 2015). Essentra packaging can make use of these methods for

analysing overall impact of sales that took over a certain frame of time.

Cost variance: This is referred to method that exemplify alterations that took place

within cost in comparison of existent cost that is occurring. Essentra packaging need to

determine divergence in between calculated as well as existing cost with respect to

manufacturing.

Absorption & marginal costing:

Absorption costing: This method involves expenses related with costs in terms of

production of relevant services or products by taking into consideration Generally Accepted

Accounting Principles (GAAP) for external reporting. This involves both fixed as well as

variable cost of products or services that are delivered by Essentra packaging to their customers.

This costing is utilised for costing strategies with respect to administration and bookkeeping that

works in an effective manner that will leads business towards growth. Furthermore, variable &

fixed cost, materials cost and compensation will lead to increase within costing (Sledgianowski,

Gomaa and Tan, 2017). It will assist management of firm to formulate effectual strategies for

overcoming situations that took place while firm carry out their operations. In this emphasis will

be on cost that has been absorbed along with technical tools that can be taken into account by

management of organisation.

5

are carrying out their operations. For an instance cost of raw materials, labour, suppliers and

many others. This denotes complete processes that are being associated with computation of

entire cost. It will enable the management to identify cost of individual operations.

Cost volume profit analysis: It is a analysis technique which deals with determination of

divergence among cost and profits that are furnished by carrying out specified operations. Its

objective is to analyse financial situations of firms in context of divergence in between assorted

factors.

Flexible budgeting: This is defined as budgeting techniques in which values related with

overall budget can be altered with respect to volumes that have been produced and sales that

incurred (Spraakman and et. al., 2015). Essentra packaging can make use of these methods for

analysing overall impact of sales that took over a certain frame of time.

Cost variance: This is referred to method that exemplify alterations that took place

within cost in comparison of existent cost that is occurring. Essentra packaging need to

determine divergence in between calculated as well as existing cost with respect to

manufacturing.

Absorption & marginal costing:

Absorption costing: This method involves expenses related with costs in terms of

production of relevant services or products by taking into consideration Generally Accepted

Accounting Principles (GAAP) for external reporting. This involves both fixed as well as

variable cost of products or services that are delivered by Essentra packaging to their customers.

This costing is utilised for costing strategies with respect to administration and bookkeeping that

works in an effective manner that will leads business towards growth. Furthermore, variable &

fixed cost, materials cost and compensation will lead to increase within costing (Sledgianowski,

Gomaa and Tan, 2017). It will assist management of firm to formulate effectual strategies for

overcoming situations that took place while firm carry out their operations. In this emphasis will

be on cost that has been absorbed along with technical tools that can be taken into account by

management of organisation.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

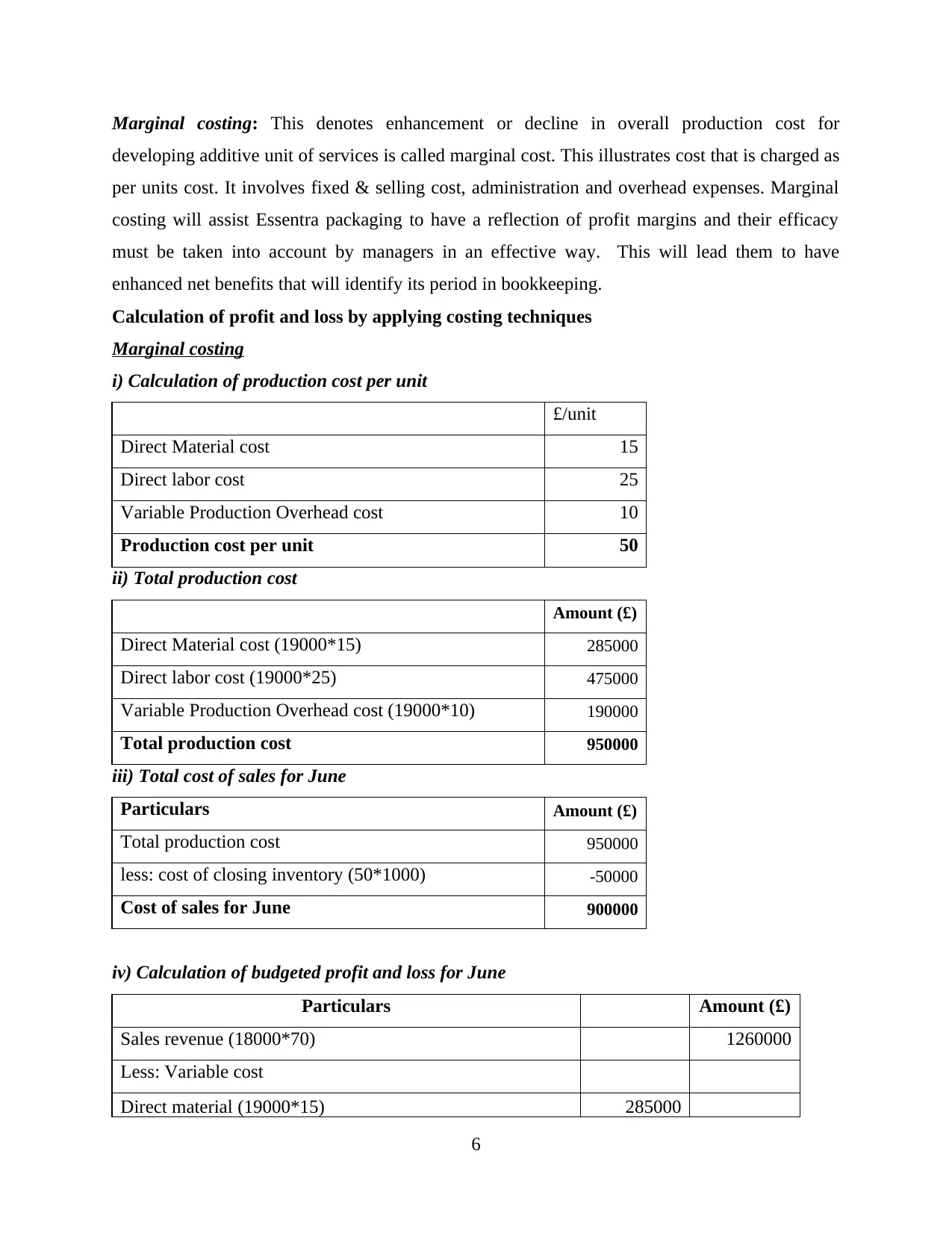

Marginal costing: This denotes enhancement or decline in overall production cost for

developing additive unit of services is called marginal cost. This illustrates cost that is charged as

per units cost. It involves fixed & selling cost, administration and overhead expenses. Marginal

costing will assist Essentra packaging to have a reflection of profit margins and their efficacy

must be taken into account by managers in an effective way. This will lead them to have

enhanced net benefits that will identify its period in bookkeeping.

Calculation of profit and loss by applying costing techniques

Marginal costing

i) Calculation of production cost per unit

£/unit

Direct Material cost 15

Direct labor cost 25

Variable Production Overhead cost 10

Production cost per unit 50

ii) Total production cost

Amount (£)

Direct Material cost (19000*15) 285000

Direct labor cost (19000*25) 475000

Variable Production Overhead cost (19000*10) 190000

Total production cost 950000

iii) Total cost of sales for June

Particulars Amount (£)

Total production cost 950000

less: cost of closing inventory (50*1000) -50000

Cost of sales for June 900000

iv) Calculation of budgeted profit and loss for June

Particulars Amount (£)

Sales revenue (18000*70) 1260000

Less: Variable cost

Direct material (19000*15) 285000

6

developing additive unit of services is called marginal cost. This illustrates cost that is charged as

per units cost. It involves fixed & selling cost, administration and overhead expenses. Marginal

costing will assist Essentra packaging to have a reflection of profit margins and their efficacy

must be taken into account by managers in an effective way. This will lead them to have

enhanced net benefits that will identify its period in bookkeeping.

Calculation of profit and loss by applying costing techniques

Marginal costing

i) Calculation of production cost per unit

£/unit

Direct Material cost 15

Direct labor cost 25

Variable Production Overhead cost 10

Production cost per unit 50

ii) Total production cost

Amount (£)

Direct Material cost (19000*15) 285000

Direct labor cost (19000*25) 475000

Variable Production Overhead cost (19000*10) 190000

Total production cost 950000

iii) Total cost of sales for June

Particulars Amount (£)

Total production cost 950000

less: cost of closing inventory (50*1000) -50000

Cost of sales for June 900000

iv) Calculation of budgeted profit and loss for June

Particulars Amount (£)

Sales revenue (18000*70) 1260000

Less: Variable cost

Direct material (19000*15) 285000

6

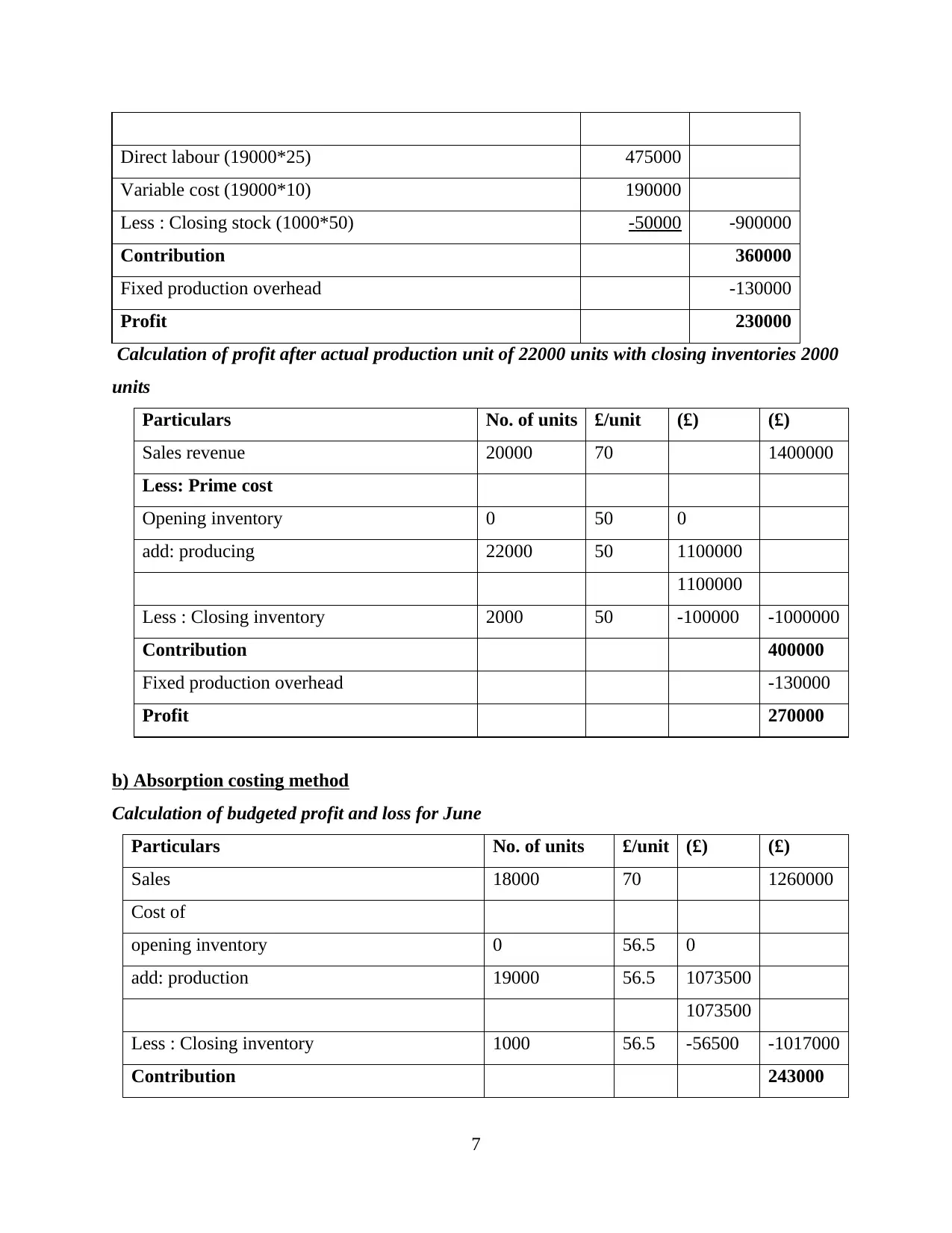

Direct labour (19000*25) 475000

Variable cost (19000*10) 190000

Less : Closing stock (1000*50) -50000 -900000

Contribution 360000

Fixed production overhead -130000

Profit 230000

Calculation of profit after actual production unit of 22000 units with closing inventories 2000

units

Particulars No. of units £/unit (£) (£)

Sales revenue 20000 70 1400000

Less: Prime cost

Opening inventory 0 50 0

add: producing 22000 50 1100000

1100000

Less : Closing inventory 2000 50 -100000 -1000000

Contribution 400000

Fixed production overhead -130000

Profit 270000

b) Absorption costing method

Calculation of budgeted profit and loss for June

Particulars No. of units £/unit (£) (£)

Sales 18000 70 1260000

Cost of

opening inventory 0 56.5 0

add: production 19000 56.5 1073500

1073500

Less : Closing inventory 1000 56.5 -56500 -1017000

Contribution 243000

7

Variable cost (19000*10) 190000

Less : Closing stock (1000*50) -50000 -900000

Contribution 360000

Fixed production overhead -130000

Profit 230000

Calculation of profit after actual production unit of 22000 units with closing inventories 2000

units

Particulars No. of units £/unit (£) (£)

Sales revenue 20000 70 1400000

Less: Prime cost

Opening inventory 0 50 0

add: producing 22000 50 1100000

1100000

Less : Closing inventory 2000 50 -100000 -1000000

Contribution 400000

Fixed production overhead -130000

Profit 270000

b) Absorption costing method

Calculation of budgeted profit and loss for June

Particulars No. of units £/unit (£) (£)

Sales 18000 70 1260000

Cost of

opening inventory 0 56.5 0

add: production 19000 56.5 1073500

1073500

Less : Closing inventory 1000 56.5 -56500 -1017000

Contribution 243000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

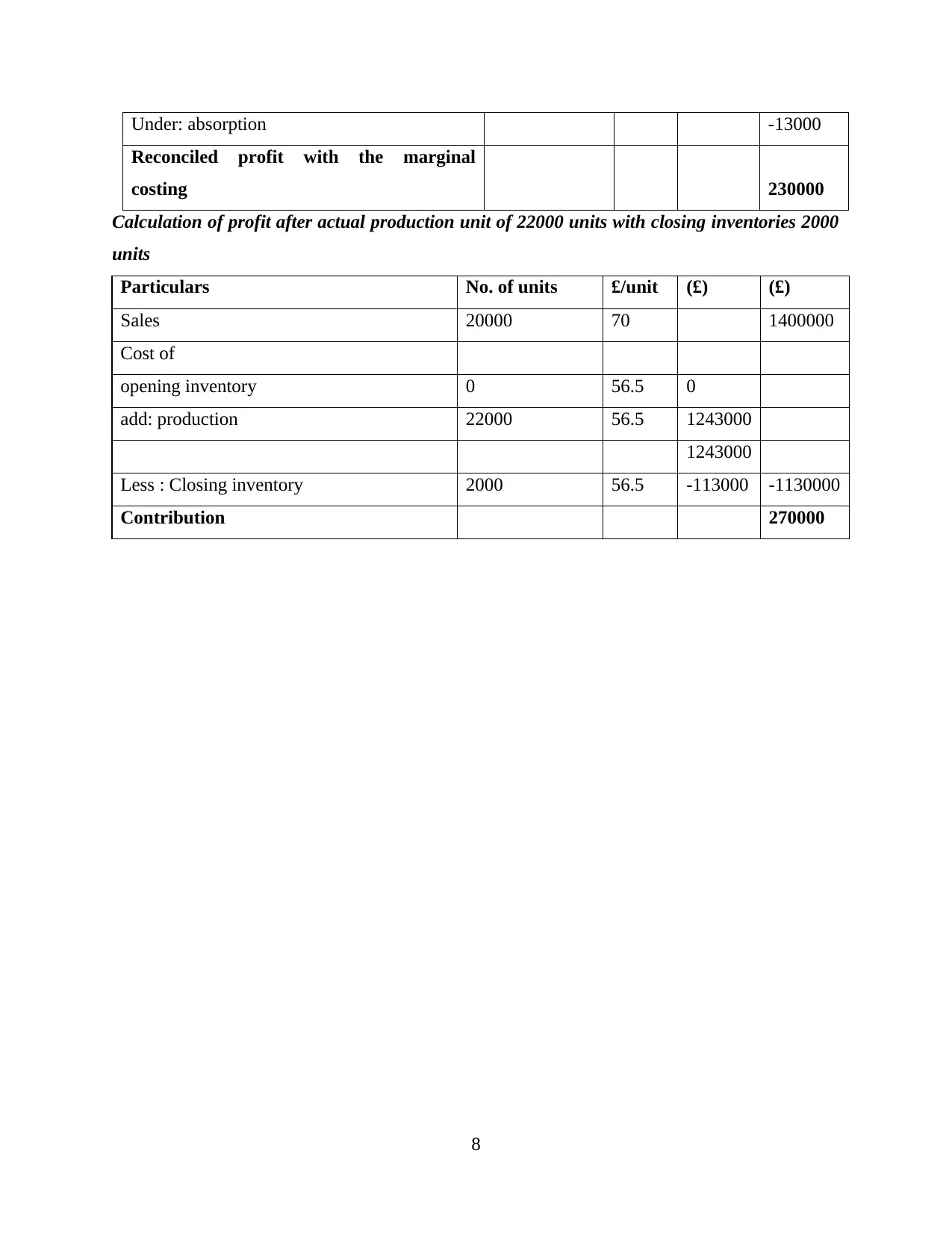

Under: absorption -13000

Reconciled profit with the marginal

costing 230000

Calculation of profit after actual production unit of 22000 units with closing inventories 2000

units

Particulars No. of units £/unit (£) (£)

Sales 20000 70 1400000

Cost of

opening inventory 0 56.5 0

add: production 22000 56.5 1243000

1243000

Less : Closing inventory 2000 56.5 -113000 -1130000

Contribution 270000

8

Reconciled profit with the marginal

costing 230000

Calculation of profit after actual production unit of 22000 units with closing inventories 2000

units

Particulars No. of units £/unit (£) (£)

Sales 20000 70 1400000

Cost of

opening inventory 0 56.5 0

add: production 22000 56.5 1243000

1243000

Less : Closing inventory 2000 56.5 -113000 -1130000

Contribution 270000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost allocation: It is referred to process of allocation of overheads according to activities that

have been performed. An example can be taken, Essentra packaging allot expenditure according

to various activities that are being related with process of manufacturing.

Fixed cost: The cost which do not modify with decrease or increase in amount related

services or products that are being offered is referred to as fixed cost (Aldehayyat and Maan,

2013). Generally, it denotes overall expenditure or cost that are given by Essentra packaging for

carrying out their operations.

Variable cost: The corporate expenses which are altered with respect production output

proportion is referred to as variable cost. It inclines or declines in context of production within

firm's volume, as it increases with improvisation in production and declines if production rate

falls down. With respect to Essentra packaging cost of materials along with variable overheads

will be included in this.

Normal costing: This comprises of cost of products in context of material cost, labour

cost and various others that takes place in organisation while they (Essentra packaging) are

delivering their services.

Standard costing: It refers to standardised cost which is anticipated in context of future

perspectives for furnishing various operations. This takes place in comparison to actual

performances that are being rendered by firm (Anandarajan, Anandarajan and Srinivasan, 2012).

For example, Essentra packaging makes use of costing to measure direct costs related with this.

Activity based costing: This refers to accounting method that can be utilised by firms for

determination of cost with respect to overhead operations along with their products. They

completely depends on activities or operations and costing systems are defined as per that.

Inventory cost: This comprises of cost related with ordering, delivering, storage and

various other activities to which firm is liable to carry out. Essentra packaging can identify costs

associated with inventory for management of overall expenses that took place and are occurring.

Valuation methods:

LIFO: This illustrates cash flow assumptions and is abbreviation of last in first out. This

method can be used by Essentra packaging to take inventory which is amendable for making a

record of items that are initially sold by them. The costs associated with latest products that were

produced outgo first according to costs of goods sold (COGS). For example, manufacturing team

of Essentra packaging opts for usage of raw materials that came at last.

9

have been performed. An example can be taken, Essentra packaging allot expenditure according

to various activities that are being related with process of manufacturing.

Fixed cost: The cost which do not modify with decrease or increase in amount related

services or products that are being offered is referred to as fixed cost (Aldehayyat and Maan,

2013). Generally, it denotes overall expenditure or cost that are given by Essentra packaging for

carrying out their operations.

Variable cost: The corporate expenses which are altered with respect production output

proportion is referred to as variable cost. It inclines or declines in context of production within

firm's volume, as it increases with improvisation in production and declines if production rate

falls down. With respect to Essentra packaging cost of materials along with variable overheads

will be included in this.

Normal costing: This comprises of cost of products in context of material cost, labour

cost and various others that takes place in organisation while they (Essentra packaging) are

delivering their services.

Standard costing: It refers to standardised cost which is anticipated in context of future

perspectives for furnishing various operations. This takes place in comparison to actual

performances that are being rendered by firm (Anandarajan, Anandarajan and Srinivasan, 2012).

For example, Essentra packaging makes use of costing to measure direct costs related with this.

Activity based costing: This refers to accounting method that can be utilised by firms for

determination of cost with respect to overhead operations along with their products. They

completely depends on activities or operations and costing systems are defined as per that.

Inventory cost: This comprises of cost related with ordering, delivering, storage and

various other activities to which firm is liable to carry out. Essentra packaging can identify costs

associated with inventory for management of overall expenses that took place and are occurring.

Valuation methods:

LIFO: This illustrates cash flow assumptions and is abbreviation of last in first out. This

method can be used by Essentra packaging to take inventory which is amendable for making a

record of items that are initially sold by them. The costs associated with latest products that were

produced outgo first according to costs of goods sold (COGS). For example, manufacturing team

of Essentra packaging opts for usage of raw materials that came at last.

9

FIFO: It stands for first in first out and is associated with costs of goods which are being

sold out along with values associated with inventory. In this case, older cost will be taken into

consideration as initial costs (Christ and Burritt, 2013). This cost will be eliminated from balance

sheet and will take place as a initial cost which will be present as first cost in the income

statements. For an example, Essentra Ltd make use of raw materials which were brought at

initial stage so that their quality is not compromised with passage of time.

Overhead: This denotes expense that is associated with labour and material cost. They

are fixed for an instance salary.

TASK 3

P4 Assets and detriment of various kinds of planning tools.

Budget is defined as the financial plan for specified periods. This involves quantities of

the resources, cost and expenditure, liabilities, cash flows and many others. Moreover, this is

utilised for forecasting financial outcomes as well as position of company for upcoming duration.

The manager of the organisation prepare budget as per the long term objectives in order to

achieve success. Essentra packaging managers formulates several types budget for analysing that

whole sections are using financial resources effective and efficiently or not. For controlling

excess expenditure of funds, it concentrate upon budgetary control. This is considered as the

procedures to set financial as well as performance targets for particular time duration for

attaining growth and success (Cohen and Karatzimas, 2013).

For preparing the budgets manager of Essentra packaging explain objectives and

accumulate relevant information in respect of firm's needs. Then gathered data are examined

through them for measuring its accuracy. After analysis, it prepare budgets consequently as well

as represent that in front of senior executives for taking its approval. So, when it get approved

thereafter managers execute that on company. These steps are obeyed in respective organisation

for preparing the budget in efficacious way.

Zero based budgeting:

This is considered as the budget that initiate from scratch. This guides managers of the

company to justify all the expenditure that take place at the time of performing activities of the

enterprises. Within Essentra packaging, this is prepared through management for analysing the

10

sold out along with values associated with inventory. In this case, older cost will be taken into

consideration as initial costs (Christ and Burritt, 2013). This cost will be eliminated from balance

sheet and will take place as a initial cost which will be present as first cost in the income

statements. For an example, Essentra Ltd make use of raw materials which were brought at

initial stage so that their quality is not compromised with passage of time.

Overhead: This denotes expense that is associated with labour and material cost. They

are fixed for an instance salary.

TASK 3

P4 Assets and detriment of various kinds of planning tools.

Budget is defined as the financial plan for specified periods. This involves quantities of

the resources, cost and expenditure, liabilities, cash flows and many others. Moreover, this is

utilised for forecasting financial outcomes as well as position of company for upcoming duration.

The manager of the organisation prepare budget as per the long term objectives in order to

achieve success. Essentra packaging managers formulates several types budget for analysing that

whole sections are using financial resources effective and efficiently or not. For controlling

excess expenditure of funds, it concentrate upon budgetary control. This is considered as the

procedures to set financial as well as performance targets for particular time duration for

attaining growth and success (Cohen and Karatzimas, 2013).

For preparing the budgets manager of Essentra packaging explain objectives and

accumulate relevant information in respect of firm's needs. Then gathered data are examined

through them for measuring its accuracy. After analysis, it prepare budgets consequently as well

as represent that in front of senior executives for taking its approval. So, when it get approved

thereafter managers execute that on company. These steps are obeyed in respective organisation

for preparing the budget in efficacious way.

Zero based budgeting:

This is considered as the budget that initiate from scratch. This guides managers of the

company to justify all the expenditure that take place at the time of performing activities of the

enterprises. Within Essentra packaging, this is prepared through management for analysing the

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.