Management Accounting Assignment: Costing and Value Chain Analysis

VerifiedAdded on 2023/01/19

|14

|1652

|31

Report

AI Summary

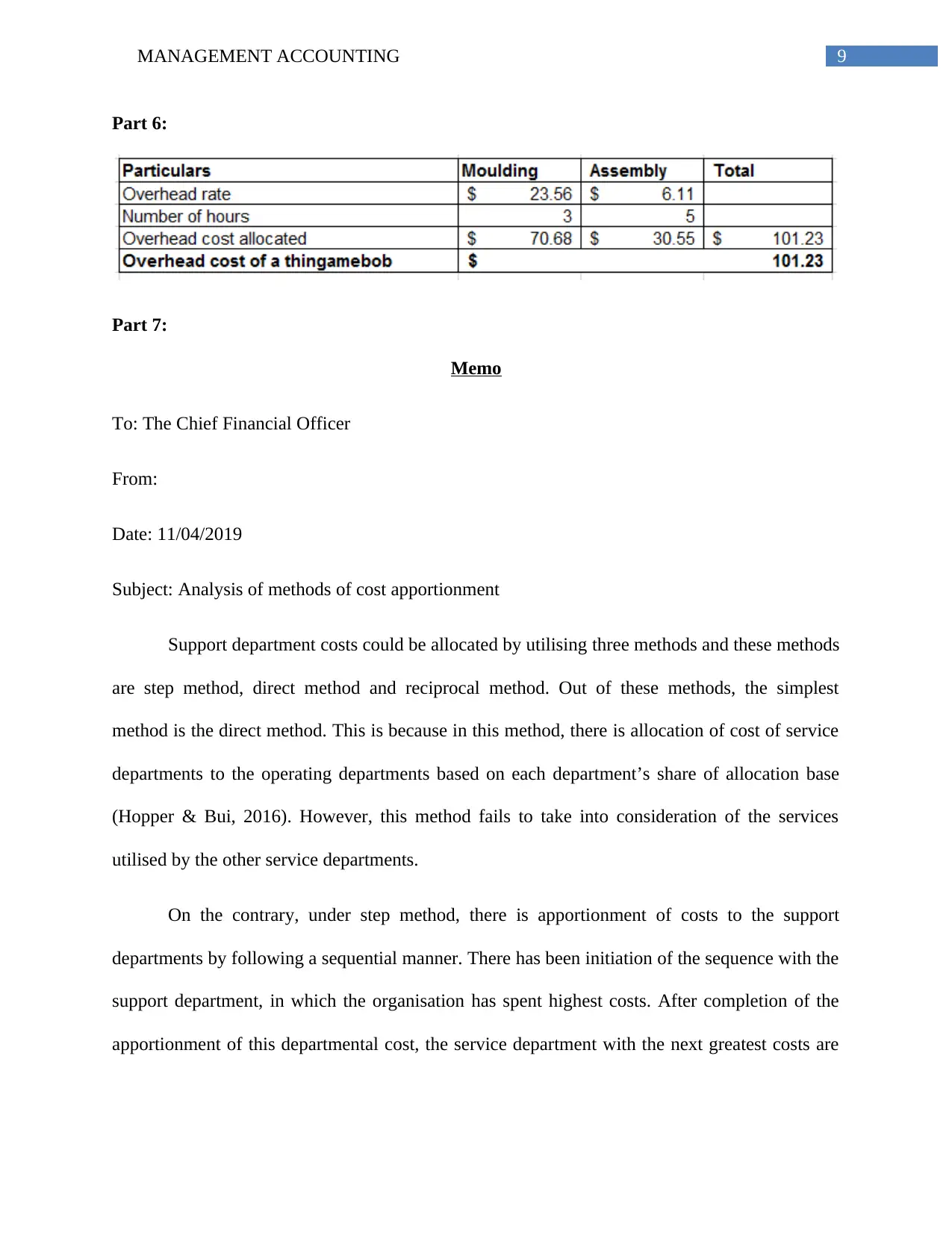

This management accounting report begins with a value chain analysis of Rio Tinto, evaluating its primary and secondary activities and identifying key management accounting issues. It then moves on to a cost of manufacturing statement, though specific details are not provided in the provided text. The report further explores cost allocation methods, comparing the direct, step-down, and reciprocal methods, concluding that the reciprocal method is the most effective due to its ability to account for interdepartmental services fully. The report also includes a memo analyzing the methods of cost apportionment. The assignment demonstrates the application of management accounting principles to real-world business scenarios, providing valuable insights into costing and cost allocation.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.