Management Accounting Assignment: Weighted Average vs FIFO Analysis

VerifiedAdded on 2022/09/22

|18

|2186

|20

Homework Assignment

AI Summary

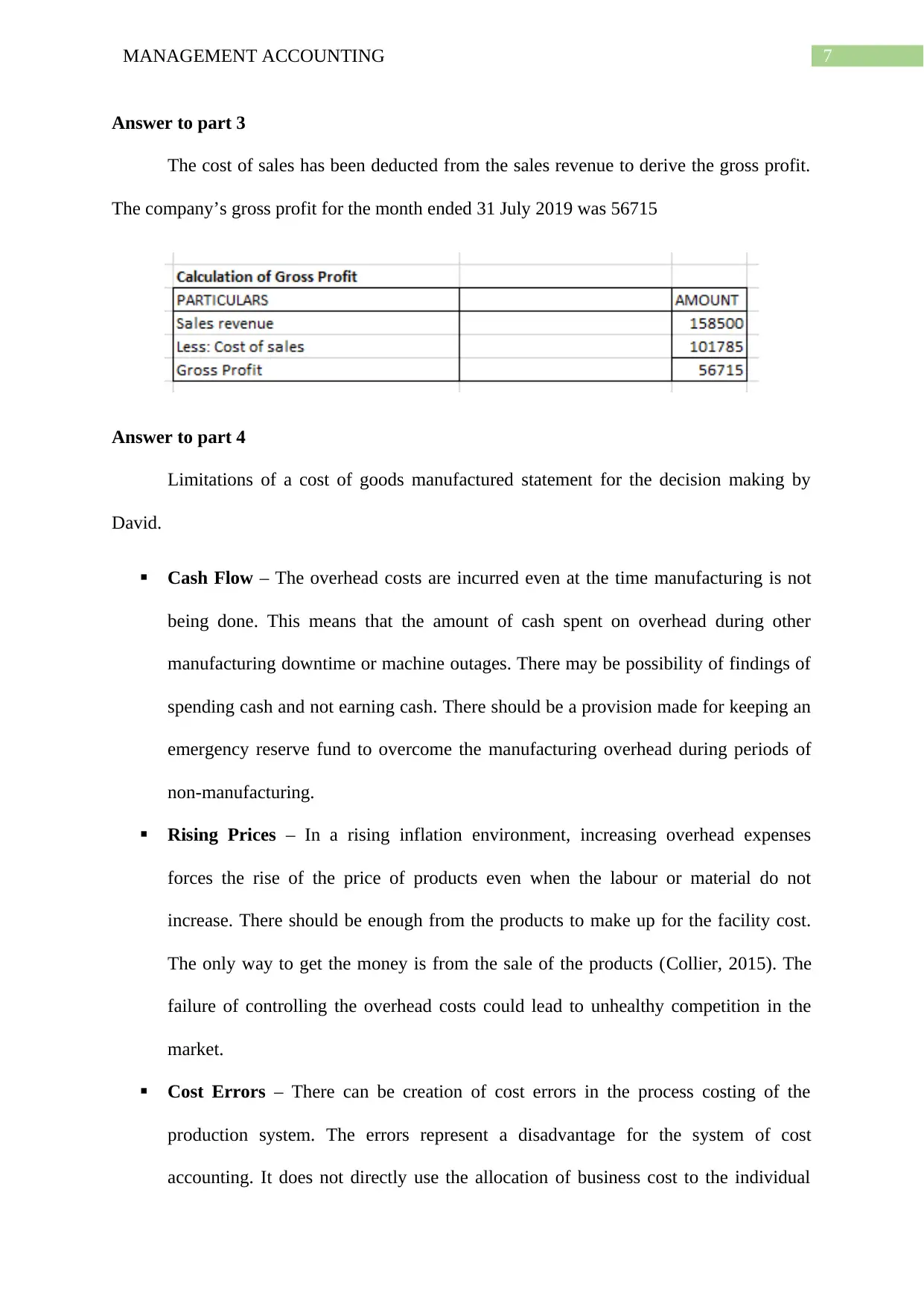

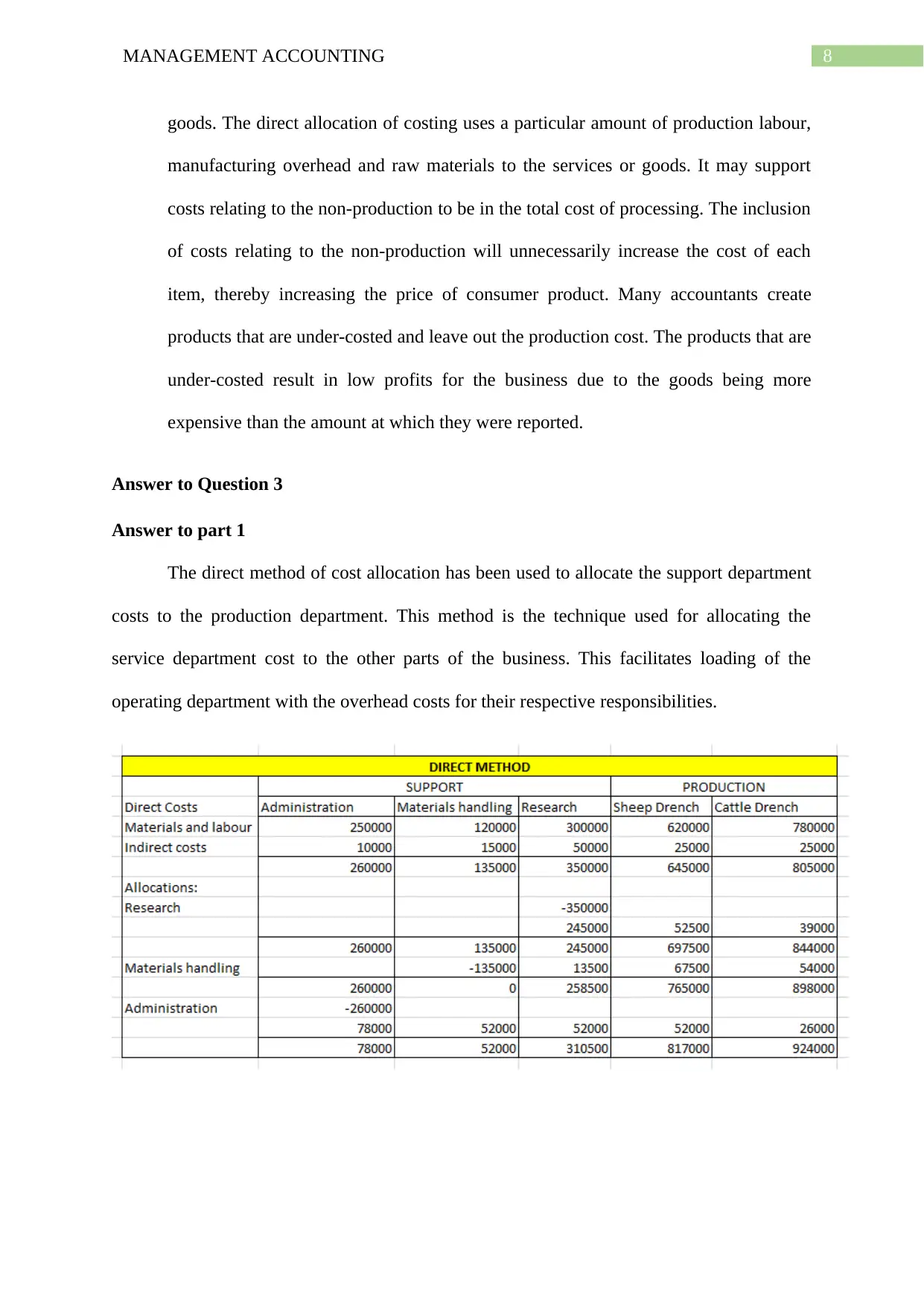

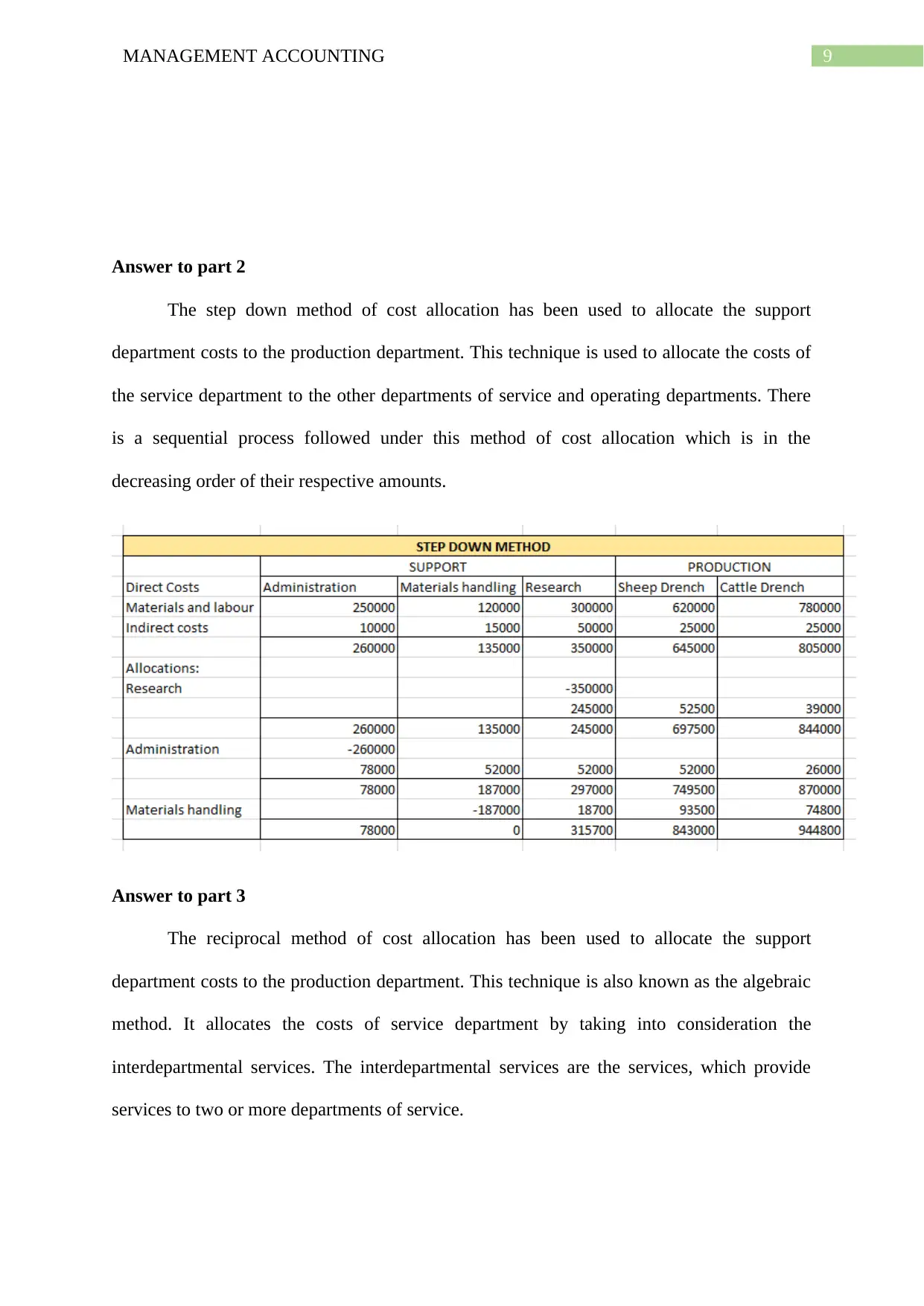

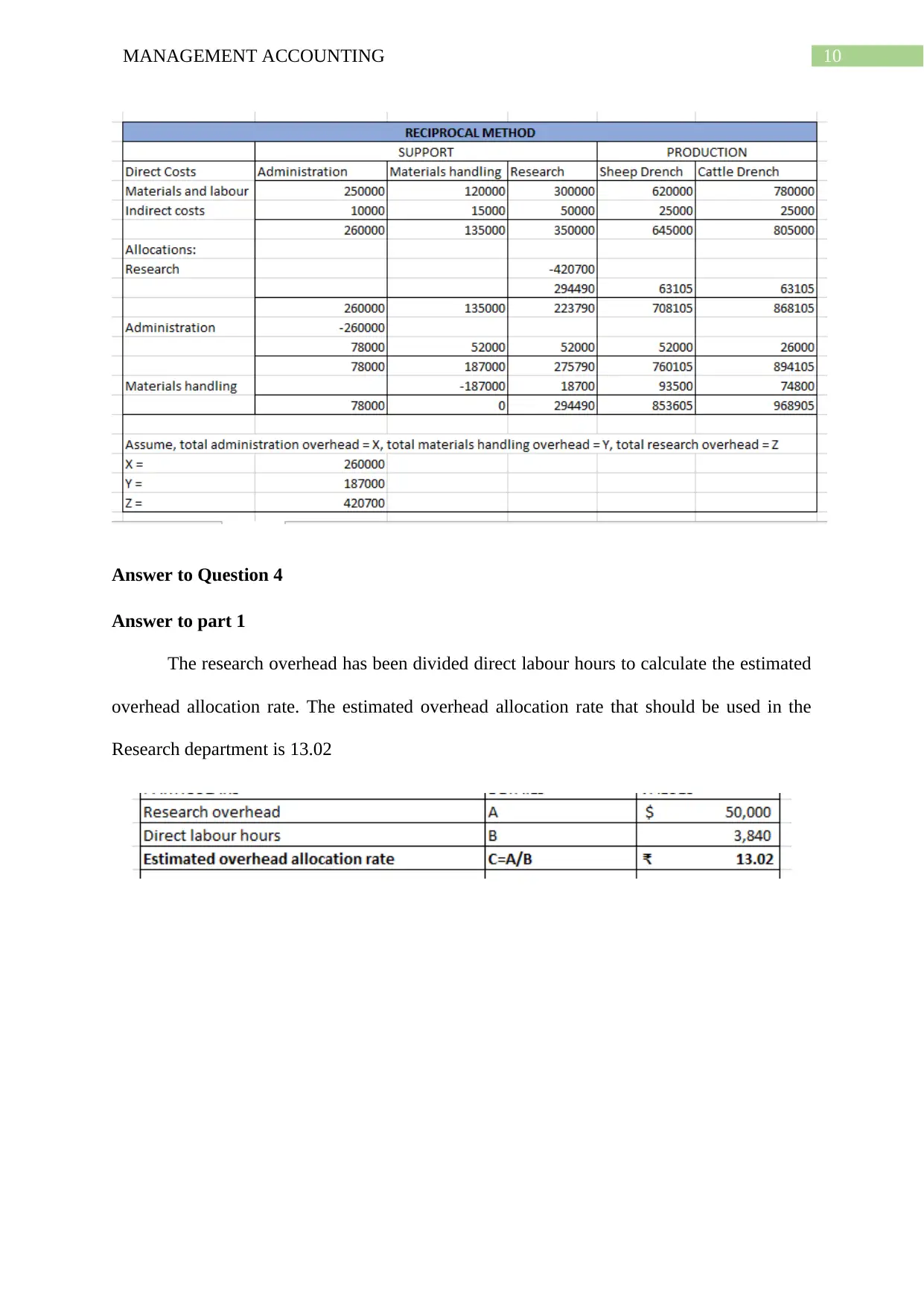

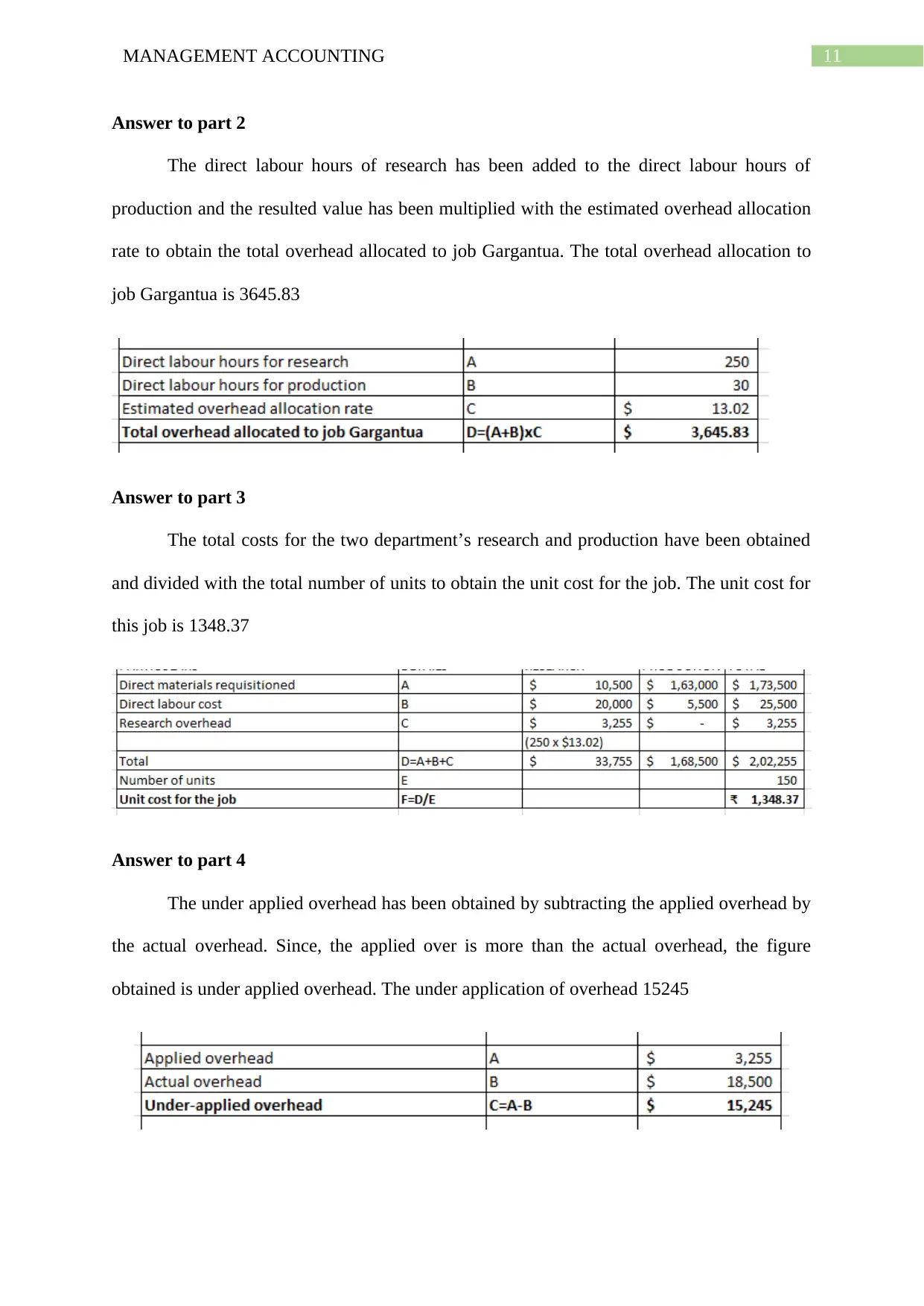

This document provides a comprehensive solution to a management accounting assignment based on a case study of Farm Organic Ltd, a company producing organic drenches for livestock. The assignment covers key concepts such as value chain analysis, cost of goods manufactured statements, cost of sales, and the limitations of such statements. It delves into various cost allocation methods, including direct, step-down, and reciprocal methods, along with overhead allocation rate calculations. The solution analyzes job costing, under-applied overhead, and corresponding journal entries. Furthermore, it meticulously calculates the cost of goods transferred out using both weighted average and FIFO methods, followed by journal entries for production costs in different departments. The assignment concludes with a comparison of the costs derived from these two methods, offering a detailed understanding of the impact of different costing approaches on financial reporting and decision-making.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.