Icon College BTEC HND in Business Unit 5 Management Accounting Report

VerifiedAdded on 2023/01/16

|21

|5817

|92

Report

AI Summary

This report on management accounting covers key concepts and systems. It begins with an introduction to management accounting, explaining its role in organizational decision-making, and then dives into different types of management accounting systems such as cost accounting, inventory management, price optimization, and job costing. The report then explores various methods for reporting in management accounting, including budget reports, performance reports, and cost reports, highlighting their importance for internal stakeholders. Furthermore, the assignment examines the advantages and disadvantages of different planning tools used in budgetary control. Finally, the report provides a comparison of how different organizations adapt managerial accounting systems to address financial problems, providing a holistic view of the subject matter.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

LO1 .................................................................................................................................................1

Management Accounting and types of management accounting systems ..................................1

Different methods for reporting in management accounting ......................................................4

LO2..................................................................................................................................................7

Calculations of cost using different cost accounting accounting techniques...............................7

LO3..................................................................................................................................................9

Advantages and disadvantages of different planning tool...........................................................9

LO4................................................................................................................................................12

Comparison between organisations adapting managerial accounting systems for responding to

the financial problems. .............................................................................................................12

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................15

APPENDICES...............................................................................................................................18

INTRODUCTION...........................................................................................................................1

LO1 .................................................................................................................................................1

Management Accounting and types of management accounting systems ..................................1

Different methods for reporting in management accounting ......................................................4

LO2..................................................................................................................................................7

Calculations of cost using different cost accounting accounting techniques...............................7

LO3..................................................................................................................................................9

Advantages and disadvantages of different planning tool...........................................................9

LO4................................................................................................................................................12

Comparison between organisations adapting managerial accounting systems for responding to

the financial problems. .............................................................................................................12

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................15

APPENDICES...............................................................................................................................18

INTRODUCTION

Management accounting, managers use the provisions of accounting information in order

to better inform themselves before they decide matters within their organizations, which aids

their management and performance of control functions. This type of accounting system also

helps in knowing the needs and demands of business (Ax and Greve, 2017). The management

accountants are also being known as the value creators. These type of people are also engaged in

forecasting the future risks and challenges which is being associated with business. Risk included

can be financial. Assignment will explain management accounting and it will also provide

essential requirement for different type of management accounting system. It will also explain

different methods used for management accounting reporting. Study will also explain advantage

and disadvantage of different budgetary tools that can be used in budgetary control. It will also

compare how different organizations are adapting management accounting system so that they

can respond to financial problem.

LO1

Management Accounting and types of management accounting systems

Management accounting deals with application of the professional knowledge, concepts

and techniques for preparing accounting informations in a way that will help management of

company in formulation of policies and plans, controlling operations of organisations, optimal

use of the resources, decision making and disclosures to management and for safeguarding

assets. In simple terms, the management accounting could be understood as presentation and

processing of accounting as well as economic data. This helps in evaluating management's

performance, to formulate strategies, to make comparison, forecasting, budgeting etc.

Accounting is referred as process of identifying, measuring and interacting with data for

making the informed judgements and decisions by users of accounting information. Systems of

management accounting vary in application (Booth, 2018). Each system of managerial

accounting is framed for providing the useful information as required by the management for

effective decision making. There are different types of management accounting systems like cost

accounting, inventory management, price optimisation and job costing.

Types of management accounting systems.

Cost accounting systems

1

Management accounting, managers use the provisions of accounting information in order

to better inform themselves before they decide matters within their organizations, which aids

their management and performance of control functions. This type of accounting system also

helps in knowing the needs and demands of business (Ax and Greve, 2017). The management

accountants are also being known as the value creators. These type of people are also engaged in

forecasting the future risks and challenges which is being associated with business. Risk included

can be financial. Assignment will explain management accounting and it will also provide

essential requirement for different type of management accounting system. It will also explain

different methods used for management accounting reporting. Study will also explain advantage

and disadvantage of different budgetary tools that can be used in budgetary control. It will also

compare how different organizations are adapting management accounting system so that they

can respond to financial problem.

LO1

Management Accounting and types of management accounting systems

Management accounting deals with application of the professional knowledge, concepts

and techniques for preparing accounting informations in a way that will help management of

company in formulation of policies and plans, controlling operations of organisations, optimal

use of the resources, decision making and disclosures to management and for safeguarding

assets. In simple terms, the management accounting could be understood as presentation and

processing of accounting as well as economic data. This helps in evaluating management's

performance, to formulate strategies, to make comparison, forecasting, budgeting etc.

Accounting is referred as process of identifying, measuring and interacting with data for

making the informed judgements and decisions by users of accounting information. Systems of

management accounting vary in application (Booth, 2018). Each system of managerial

accounting is framed for providing the useful information as required by the management for

effective decision making. There are different types of management accounting systems like cost

accounting, inventory management, price optimisation and job costing.

Types of management accounting systems.

Cost accounting systems

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost accounting systems refers to a framework that is used by companies for estimating

the cost of products for the profitability analysis, cost control and inventory valuation. It

evaluates the performance of company and help managers of company in making decisions that

are based over costs related to manufacturing a product. Cost systems applies to every business

whether trading or manufacturing products or delivering services. Cost accounting is not same as

that of financial accounting. Cost accounting deals with cost with cost reduction and cost control

measures so that the profitability of company could be increased (Christ and Burritt, 2017). Cost

accounting is concerned with projected and actual outcomes. It helps manager in taking various

corrective steps for reducing the errors and gaps between the actual and budgeted results.

Cost accounting systems acts as guide for managers and executives working within

company so that decision can be taken for improving the efficiency and performance. Cost

accounting is mainly for the internal users of company. There are different types of cost

accounting systems available for manager of different business. Objective behind cost

accounting is of lowering costs of business operations by identifying and controlling them (Cost

accounting system, 2015).

Inventory Management System

Inventory management is combination of technologies, procedures and processes which

oversee maintenance and monitoring the products in stock and identify whether these products

are assets, supplies, raw material or the finished products. It is complex process specially for the

larger organisations where the basics of management system are same everywhere and in every

type of company. In this systems goods are received in the warehouses as raw materials or the

components. Inventory management system uses variety of information for keeping the track

records of goods as going through the processes, including serial numbers, lot numbers quantity,

cost and the dates of moving into the process.

Function are generally correlated and interlinked to each others. Inventory management is

a part of supply chain management of the business organisation. Inventory management is an

important function for the management of company that helps them to decide about the products

cycle. Managers of company strive for maintaining an optimum inventory levels meeting the

requirements and avoiding the impacts of mismanagement of inventory over financial figures

(Cooper, Ezzamel. and Qu, 2017). Companies use software of inventory management that

2

the cost of products for the profitability analysis, cost control and inventory valuation. It

evaluates the performance of company and help managers of company in making decisions that

are based over costs related to manufacturing a product. Cost systems applies to every business

whether trading or manufacturing products or delivering services. Cost accounting is not same as

that of financial accounting. Cost accounting deals with cost with cost reduction and cost control

measures so that the profitability of company could be increased (Christ and Burritt, 2017). Cost

accounting is concerned with projected and actual outcomes. It helps manager in taking various

corrective steps for reducing the errors and gaps between the actual and budgeted results.

Cost accounting systems acts as guide for managers and executives working within

company so that decision can be taken for improving the efficiency and performance. Cost

accounting is mainly for the internal users of company. There are different types of cost

accounting systems available for manager of different business. Objective behind cost

accounting is of lowering costs of business operations by identifying and controlling them (Cost

accounting system, 2015).

Inventory Management System

Inventory management is combination of technologies, procedures and processes which

oversee maintenance and monitoring the products in stock and identify whether these products

are assets, supplies, raw material or the finished products. It is complex process specially for the

larger organisations where the basics of management system are same everywhere and in every

type of company. In this systems goods are received in the warehouses as raw materials or the

components. Inventory management system uses variety of information for keeping the track

records of goods as going through the processes, including serial numbers, lot numbers quantity,

cost and the dates of moving into the process.

Function are generally correlated and interlinked to each others. Inventory management is

a part of supply chain management of the business organisation. Inventory management is an

important function for the management of company that helps them to decide about the products

cycle. Managers of company strive for maintaining an optimum inventory levels meeting the

requirements and avoiding the impacts of mismanagement of inventory over financial figures

(Cooper, Ezzamel. and Qu, 2017). Companies use software of inventory management that

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

provides the central database and reference point for inventory. These software have the ability

of analysing data, generating reports, forecasting the future demands and many more.

Price Optimisation System

It is a systems of mathematical programs which are used for calculating the variations in

demand at different level of prices. It then combines data with the cost and inventory

informations for recommending the price which will be improving the profits of company.

Optimization is used widely in pricing fields for describing applications used for setting the

prices. This is an optimization method which is used for decision making processes which

employs algorithms, data and software for making recommendations faster and better than the

humans (Dekker, 2016). Management of company after examining possible choices, make

predictions for the each outcome and select the best one that maximises the results of business.

Pricing optimisation examine all the possible pricing choices, make prediction over the revenues

and level of profit from each outcome. It is not limited to the use of automation for making

faster and better decisions. It deals with with finding the inputs which help in maximising the

outputs. The system aims at finding the optimum prices that will result in best margin and

revenue outcomes for every part of the business (Price optimisation system, 2017). Objective of

price optimisation is to provide the product at optimal prices at which organisations can earn

maximised revenues margins.

Job Costing System

This is system used for accumulating and assigning manufacturing cost of individual

output or unit. Job costing is used in organisations where the items manufactured are not similar

and have significant cost. There are variations in items manufactured, job costing requires each

item should have separate cost record. They also serve as subsidiary ledger for manager of

companies. This helps managers and of company to keep record of every job and to maintain

data that is relevant for the business operations. Job costing is an accounting methodology for

tracking the expenses of creating unique products. This helps managers in tracking the cost of

each job (Höglund and et.al., 2016). This is an efficient accounting technique used by various

business organisations as it helps them to run the business smoothly.

3

of analysing data, generating reports, forecasting the future demands and many more.

Price Optimisation System

It is a systems of mathematical programs which are used for calculating the variations in

demand at different level of prices. It then combines data with the cost and inventory

informations for recommending the price which will be improving the profits of company.

Optimization is used widely in pricing fields for describing applications used for setting the

prices. This is an optimization method which is used for decision making processes which

employs algorithms, data and software for making recommendations faster and better than the

humans (Dekker, 2016). Management of company after examining possible choices, make

predictions for the each outcome and select the best one that maximises the results of business.

Pricing optimisation examine all the possible pricing choices, make prediction over the revenues

and level of profit from each outcome. It is not limited to the use of automation for making

faster and better decisions. It deals with with finding the inputs which help in maximising the

outputs. The system aims at finding the optimum prices that will result in best margin and

revenue outcomes for every part of the business (Price optimisation system, 2017). Objective of

price optimisation is to provide the product at optimal prices at which organisations can earn

maximised revenues margins.

Job Costing System

This is system used for accumulating and assigning manufacturing cost of individual

output or unit. Job costing is used in organisations where the items manufactured are not similar

and have significant cost. There are variations in items manufactured, job costing requires each

item should have separate cost record. They also serve as subsidiary ledger for manager of

companies. This helps managers and of company to keep record of every job and to maintain

data that is relevant for the business operations. Job costing is an accounting methodology for

tracking the expenses of creating unique products. This helps managers in tracking the cost of

each job (Höglund and et.al., 2016). This is an efficient accounting technique used by various

business organisations as it helps them to run the business smoothly.

3

Different methods for reporting in management accounting

Management accounting lays emphasis over internal informations that are received

through financial accounting. Managerial accounting is used to control, plan and for making

decisions. Manager depends over financial statements like income statements, balance sheet and

the cash flow statements. These reporting statements are generally for external users where other

accounting reports also knows as managerial reports are for internal users for evaluating the

information of corporation. These reports include performance reports, budget reports and many

other. Management accounting is also known as managerial accounting (Maas, Schaltegger and

Crutzen, 2016). The report are prepared throughout the bookkeeping and accounting year as per

the requirements. Various critical decisions related to the business are based on these reports

therefore reports prepared should be authentic and carefully crafted by experts. Managers use

these reports for analysing and highlighting patterns and converting them into the useful

information. These reports have importance for the managers.

Budget Reports.

The budget reports in management accounting are critical for measuring the performance

of company and generated as whole for the small business and for department wise in large

organisations. Companies create budgets for understanding the schemes of business. The

estimates of the budgets are made on the basis of previous experiences. Budgets helps in making

the organisation prepared for the unforeseen situations that may arise. Budgets of company are

listed for all the sources of earning and expenditures. Budgetary report helps organisation to

remain in the budgeted level of expenditures and then achieving its goals and objectives. These

reports account for all the expenses that are required to be incurred for manufacturing the

products in an organisation. These managerial report guide the managers for planning and

deciding its future course of actions. If company do not prepares the budget reports than there

are possibilities that the company may not be able to control the cost of product. This will

increase the costing of products reducing the profit margins of products (Malmi, 2016).

Budgetary reports are prepared by every organisation for controlling the costs and forecasting the

revenues that may be generated by them selling the declared products. Budgetary reports are

prepared before the manufacturing of products. After the production budgetary report are

4

Management accounting lays emphasis over internal informations that are received

through financial accounting. Managerial accounting is used to control, plan and for making

decisions. Manager depends over financial statements like income statements, balance sheet and

the cash flow statements. These reporting statements are generally for external users where other

accounting reports also knows as managerial reports are for internal users for evaluating the

information of corporation. These reports include performance reports, budget reports and many

other. Management accounting is also known as managerial accounting (Maas, Schaltegger and

Crutzen, 2016). The report are prepared throughout the bookkeeping and accounting year as per

the requirements. Various critical decisions related to the business are based on these reports

therefore reports prepared should be authentic and carefully crafted by experts. Managers use

these reports for analysing and highlighting patterns and converting them into the useful

information. These reports have importance for the managers.

Budget Reports.

The budget reports in management accounting are critical for measuring the performance

of company and generated as whole for the small business and for department wise in large

organisations. Companies create budgets for understanding the schemes of business. The

estimates of the budgets are made on the basis of previous experiences. Budgets helps in making

the organisation prepared for the unforeseen situations that may arise. Budgets of company are

listed for all the sources of earning and expenditures. Budgetary report helps organisation to

remain in the budgeted level of expenditures and then achieving its goals and objectives. These

reports account for all the expenses that are required to be incurred for manufacturing the

products in an organisation. These managerial report guide the managers for planning and

deciding its future course of actions. If company do not prepares the budget reports than there

are possibilities that the company may not be able to control the cost of product. This will

increase the costing of products reducing the profit margins of products (Malmi, 2016).

Budgetary reports are prepared by every organisation for controlling the costs and forecasting the

revenues that may be generated by them selling the declared products. Budgetary reports are

prepared before the manufacturing of products. After the production budgetary report are

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

compared with the actual outcomes that are generated by company. This helps managers in

reducing the gaps between actual and budgeted output.

Performance Reports

As the name suggests performance reports are prepared by the management for knowing

the performance of company. The performance reports are framed for evaluating performance of

every employee to every activity being carried out in an organisation(Messner, 2016). Large

organisations also performance reports for the department. These performance report are used by

managers of the enterprise for making strategic decisions related to the future processes of

company. They undertake the corrective steps for increasing the efficiency and production of

enterprise. When management is available with the reports of individual performance of the

employees it helps management in rewarding them. Rewards and incentives helps management

in motivating the workforce increasing their efficiency and effectiveness. These reports helps in

measuring the performance of employees. These are often taken for knowing the insights of

operations undergoing within a company. If the performance is not up to the required levels in a

given capacity than it may take considerable steps in knowing the flaws that are affecting the

production and other activities (Performance reports, 2018). Performance reports are playing a

vital role in an organisation for keeping records and accurately measuring the effectiveness of the

decisions taken. The reports also enable the company to measure whether the strategies adopted

by company for enhancement is effective or in identifying the loopholes.

Cost Reports

Every product or article is manufactured by the organisation has cost associated with it.

These reports are prepared for identifying the cost of products or articles manufactured by

company. Cost of raw materials, labour, overhead and the added cost are taken into

consideration. Cost reports are the summarised report of all the above informations related to

manufacturing of product. The reports provide the managers with the capacity of realizing the

cost prices of different articles and their respective selling prices. Margins of profit are decided

by the organisations after monitoring the informations provided in these reports. Managers have

clear image and information related to all the costs that were occurred in the procurement and

production of articles (Otley, 2016). Cost report also include labour hour costs, inventory wastes

5

reducing the gaps between actual and budgeted output.

Performance Reports

As the name suggests performance reports are prepared by the management for knowing

the performance of company. The performance reports are framed for evaluating performance of

every employee to every activity being carried out in an organisation(Messner, 2016). Large

organisations also performance reports for the department. These performance report are used by

managers of the enterprise for making strategic decisions related to the future processes of

company. They undertake the corrective steps for increasing the efficiency and production of

enterprise. When management is available with the reports of individual performance of the

employees it helps management in rewarding them. Rewards and incentives helps management

in motivating the workforce increasing their efficiency and effectiveness. These reports helps in

measuring the performance of employees. These are often taken for knowing the insights of

operations undergoing within a company. If the performance is not up to the required levels in a

given capacity than it may take considerable steps in knowing the flaws that are affecting the

production and other activities (Performance reports, 2018). Performance reports are playing a

vital role in an organisation for keeping records and accurately measuring the effectiveness of the

decisions taken. The reports also enable the company to measure whether the strategies adopted

by company for enhancement is effective or in identifying the loopholes.

Cost Reports

Every product or article is manufactured by the organisation has cost associated with it.

These reports are prepared for identifying the cost of products or articles manufactured by

company. Cost of raw materials, labour, overhead and the added cost are taken into

consideration. Cost reports are the summarised report of all the above informations related to

manufacturing of product. The reports provide the managers with the capacity of realizing the

cost prices of different articles and their respective selling prices. Margins of profit are decided

by the organisations after monitoring the informations provided in these reports. Managers have

clear image and information related to all the costs that were occurred in the procurement and

production of articles (Otley, 2016). Cost report also include labour hour costs, inventory wastes

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and overhead costs. These reports are able to provide accurate understanding about all the

expenses that are necessary for optimum utilization of the available resources within the

organisation. Resources are scarce and it is important for companies to ensure that resources are

utilised in the best effective manner. Cost report also helps the management in making

comparisons between the current and previous outcomes. Costs reports contain every

information about the cost associated to the item produced. The reports also give per unit

costing of the products so that profit margin from unit can be identified(Cost reports, 2017).

These also helps in controlling the expenditure next time.

Managerial Accounting Report

Other reports that are not much known but are of significant importance to the

organisations. These reports include information report of the orders, project reports, analysis of

the competitor performance. These reports may be outsourced from professionals or prepared by

the internal management team (Pelz, 2019). Optimum course of actions depends over the

capabilities of managers in handling these reporting requirement. Reports are prepared by

organisations as per the information that is required by them for deciding about the future course

of action. Ideal choices differ with each company where the professionals skills and experience

for carrying out the task better and effectively. For attaining the best decisions managers of

company should have access over authentic and credible management accounting reports. A

managers should know the trends followed in the industry by its competitors. The cost

techniques used and adopted by them that is helping to achieve the level of profit margins

controlling the cost. Competitors analysis is essential for knowing the performance over similar

scale of productions. Projects reports relates to the specific project undertaken by the

organisation (Quattrone, 2016). Managers can focus over the particular projects and controls the

related operations. These reports are in addition to the other managerial reports that helps

management in setting the benchmark.

6

expenses that are necessary for optimum utilization of the available resources within the

organisation. Resources are scarce and it is important for companies to ensure that resources are

utilised in the best effective manner. Cost report also helps the management in making

comparisons between the current and previous outcomes. Costs reports contain every

information about the cost associated to the item produced. The reports also give per unit

costing of the products so that profit margin from unit can be identified(Cost reports, 2017).

These also helps in controlling the expenditure next time.

Managerial Accounting Report

Other reports that are not much known but are of significant importance to the

organisations. These reports include information report of the orders, project reports, analysis of

the competitor performance. These reports may be outsourced from professionals or prepared by

the internal management team (Pelz, 2019). Optimum course of actions depends over the

capabilities of managers in handling these reporting requirement. Reports are prepared by

organisations as per the information that is required by them for deciding about the future course

of action. Ideal choices differ with each company where the professionals skills and experience

for carrying out the task better and effectively. For attaining the best decisions managers of

company should have access over authentic and credible management accounting reports. A

managers should know the trends followed in the industry by its competitors. The cost

techniques used and adopted by them that is helping to achieve the level of profit margins

controlling the cost. Competitors analysis is essential for knowing the performance over similar

scale of productions. Projects reports relates to the specific project undertaken by the

organisation (Quattrone, 2016). Managers can focus over the particular projects and controls the

related operations. These reports are in addition to the other managerial reports that helps

management in setting the benchmark.

6

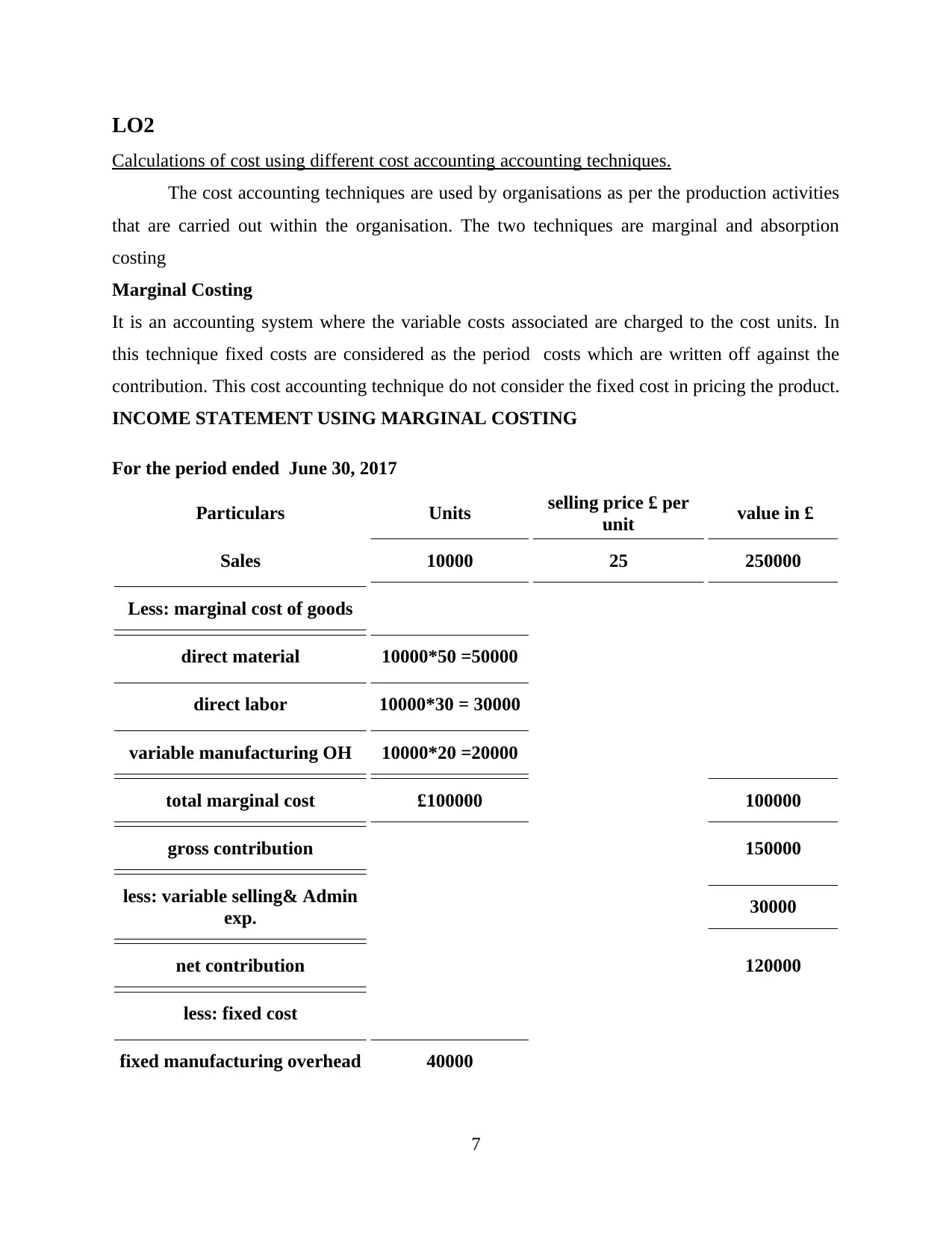

LO2

Calculations of cost using different cost accounting accounting techniques.

The cost accounting techniques are used by organisations as per the production activities

that are carried out within the organisation. The two techniques are marginal and absorption

costing

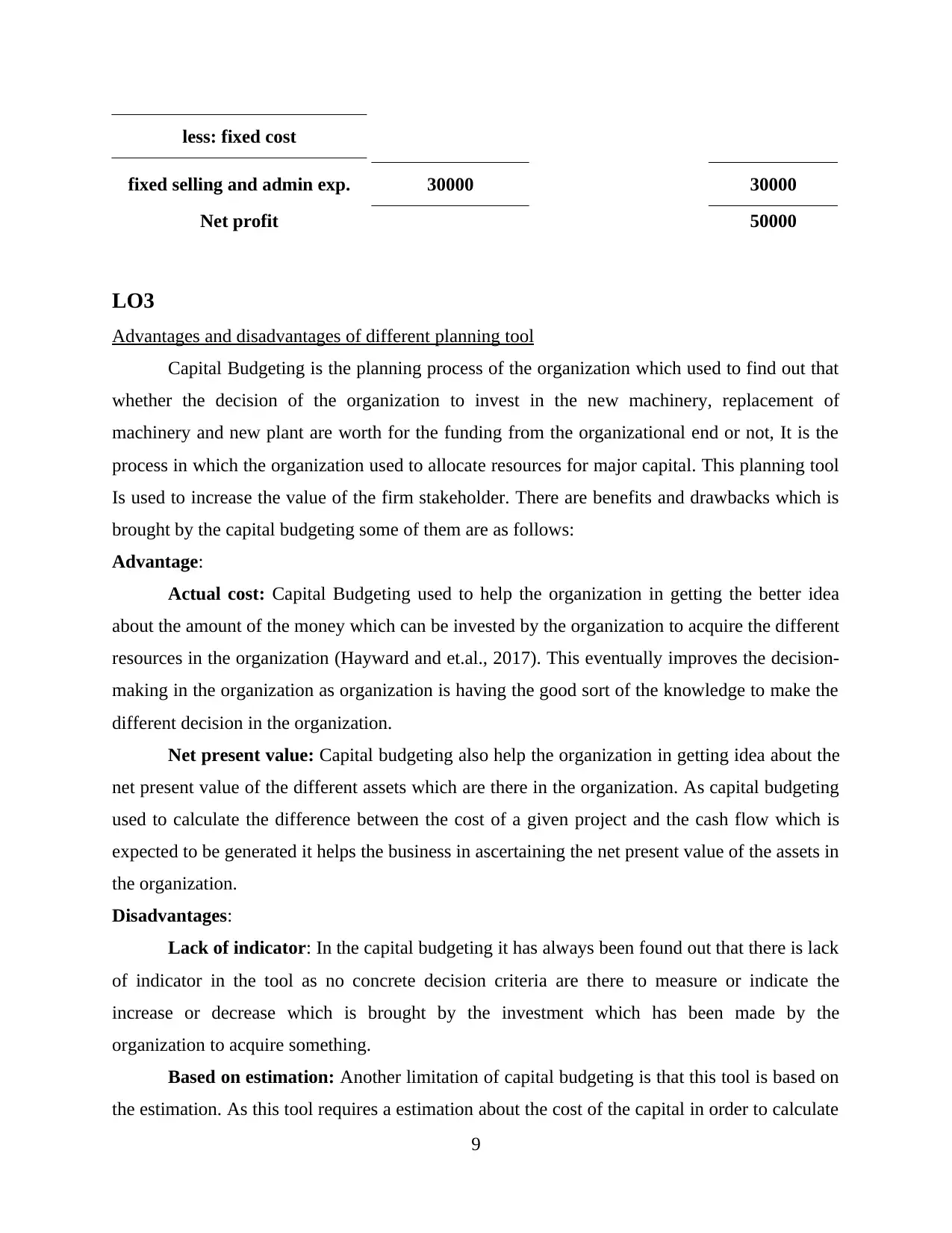

Marginal Costing

It is an accounting system where the variable costs associated are charged to the cost units. In

this technique fixed costs are considered as the period costs which are written off against the

contribution. This cost accounting technique do not consider the fixed cost in pricing the product.

INCOME STATEMENT USING MARGINAL COSTING

For the period ended June 30, 2017

Particulars Units selling price £ per

unit value in £

Sales 10000 25 250000

Less: marginal cost of goods

direct material 10000*50 =50000

direct labor 10000*30 = 30000

variable manufacturing OH 10000*20 =20000

total marginal cost £100000 100000

gross contribution 150000

less: variable selling& Admin

exp. 30000

net contribution 120000

less: fixed cost

fixed manufacturing overhead 40000

7

Calculations of cost using different cost accounting accounting techniques.

The cost accounting techniques are used by organisations as per the production activities

that are carried out within the organisation. The two techniques are marginal and absorption

costing

Marginal Costing

It is an accounting system where the variable costs associated are charged to the cost units. In

this technique fixed costs are considered as the period costs which are written off against the

contribution. This cost accounting technique do not consider the fixed cost in pricing the product.

INCOME STATEMENT USING MARGINAL COSTING

For the period ended June 30, 2017

Particulars Units selling price £ per

unit value in £

Sales 10000 25 250000

Less: marginal cost of goods

direct material 10000*50 =50000

direct labor 10000*30 = 30000

variable manufacturing OH 10000*20 =20000

total marginal cost £100000 100000

gross contribution 150000

less: variable selling& Admin

exp. 30000

net contribution 120000

less: fixed cost

fixed manufacturing overhead 40000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

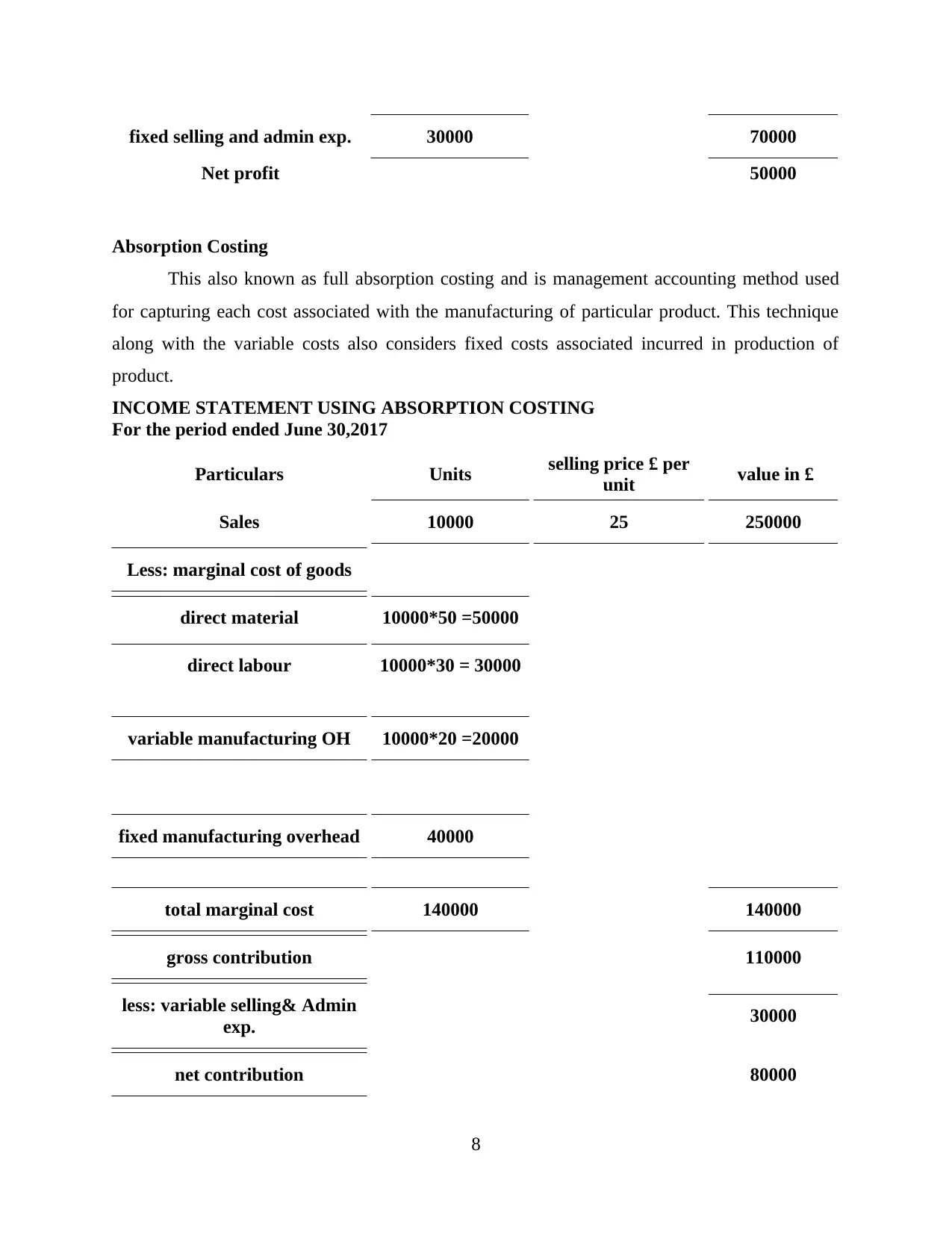

fixed selling and admin exp. 30000 70000

Net profit 50000

Absorption Costing

This also known as full absorption costing and is management accounting method used

for capturing each cost associated with the manufacturing of particular product. This technique

along with the variable costs also considers fixed costs associated incurred in production of

product.

INCOME STATEMENT USING ABSORPTION COSTING

For the period ended June 30,2017

Particulars Units selling price £ per

unit value in £

Sales 10000 25 250000

Less: marginal cost of goods

direct material 10000*50 =50000

direct labour 10000*30 = 30000

variable manufacturing OH 10000*20 =20000

fixed manufacturing overhead 40000

total marginal cost 140000 140000

gross contribution 110000

less: variable selling& Admin

exp. 30000

net contribution 80000

8

Net profit 50000

Absorption Costing

This also known as full absorption costing and is management accounting method used

for capturing each cost associated with the manufacturing of particular product. This technique

along with the variable costs also considers fixed costs associated incurred in production of

product.

INCOME STATEMENT USING ABSORPTION COSTING

For the period ended June 30,2017

Particulars Units selling price £ per

unit value in £

Sales 10000 25 250000

Less: marginal cost of goods

direct material 10000*50 =50000

direct labour 10000*30 = 30000

variable manufacturing OH 10000*20 =20000

fixed manufacturing overhead 40000

total marginal cost 140000 140000

gross contribution 110000

less: variable selling& Admin

exp. 30000

net contribution 80000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

less: fixed cost

fixed selling and admin exp. 30000 30000

Net profit 50000

LO3

Advantages and disadvantages of different planning tool

Capital Budgeting is the planning process of the organization which used to find out that

whether the decision of the organization to invest in the new machinery, replacement of

machinery and new plant are worth for the funding from the organizational end or not, It is the

process in which the organization used to allocate resources for major capital. This planning tool

Is used to increase the value of the firm stakeholder. There are benefits and drawbacks which is

brought by the capital budgeting some of them are as follows:

Advantage:

Actual cost: Capital Budgeting used to help the organization in getting the better idea

about the amount of the money which can be invested by the organization to acquire the different

resources in the organization (Hayward and et.al., 2017). This eventually improves the decision-

making in the organization as organization is having the good sort of the knowledge to make the

different decision in the organization.

Net present value: Capital budgeting also help the organization in getting idea about the

net present value of the different assets which are there in the organization. As capital budgeting

used to calculate the difference between the cost of a given project and the cash flow which is

expected to be generated it helps the business in ascertaining the net present value of the assets in

the organization.

Disadvantages:

Lack of indicator: In the capital budgeting it has always been found out that there is lack

of indicator in the tool as no concrete decision criteria are there to measure or indicate the

increase or decrease which is brought by the investment which has been made by the

organization to acquire something.

Based on estimation: Another limitation of capital budgeting is that this tool is based on

the estimation. As this tool requires a estimation about the cost of the capital in order to calculate

9

fixed selling and admin exp. 30000 30000

Net profit 50000

LO3

Advantages and disadvantages of different planning tool

Capital Budgeting is the planning process of the organization which used to find out that

whether the decision of the organization to invest in the new machinery, replacement of

machinery and new plant are worth for the funding from the organizational end or not, It is the

process in which the organization used to allocate resources for major capital. This planning tool

Is used to increase the value of the firm stakeholder. There are benefits and drawbacks which is

brought by the capital budgeting some of them are as follows:

Advantage:

Actual cost: Capital Budgeting used to help the organization in getting the better idea

about the amount of the money which can be invested by the organization to acquire the different

resources in the organization (Hayward and et.al., 2017). This eventually improves the decision-

making in the organization as organization is having the good sort of the knowledge to make the

different decision in the organization.

Net present value: Capital budgeting also help the organization in getting idea about the

net present value of the different assets which are there in the organization. As capital budgeting

used to calculate the difference between the cost of a given project and the cash flow which is

expected to be generated it helps the business in ascertaining the net present value of the assets in

the organization.

Disadvantages:

Lack of indicator: In the capital budgeting it has always been found out that there is lack

of indicator in the tool as no concrete decision criteria are there to measure or indicate the

increase or decrease which is brought by the investment which has been made by the

organization to acquire something.

Based on estimation: Another limitation of capital budgeting is that this tool is based on

the estimation. As this tool requires a estimation about the cost of the capital in order to calculate

9

the pay back and the net present value of the organization. Also, at the time this technique used

to ignore the cash flow beyond the payback period in the organization (Almazan Chen and

Titman, 2017).

Zero Based Budgeting

Zero based budgeting is the planning budgeting in which all the expenses of the

organization are justified for each new period in the organization. In this planning budgeting all

the thing are started from the zero and on the basis of the same budget are built around what is

need by the organization for upcoming period. Irrespective of the previous budget which was

made in the organization.

Advantages:

Allocation of the resource: Zero based planning budgeting tool is one of the best tool

for allocating the different resources in the organization. The reason behind the same is that this

planning tool used to analysis the needs and benefits and on the basis of the same used to allocate

the resources. This eventually used to increase the efficiency of the business performance in the

organization as the wastage of the resources are minimized in the organization.

Motivation and communication: This planning budgeting tool used to improve the level

of the motivation and the communication in the organization. This planning tool used to help the

employee in improving the level of the motivation because this tool used to give them more

initiative and responsibility in the decision-making (Oraka, Sopekan and Udeh, 2016). Also, this

tool help the organization in improving the communication and coordination at the time of

making the different decision in the organization.

Disadvantages:

Time consuming: This is the biggest disadvantage of using Zero based budgeting as the

planning tool. As this tool used to consume a good amount of the time for the manager to define

the necessary expenditure on the time. As this tool is overdependent on the same it used to

consume the good amount of the time for the organization to give a result of the same.

Requires manpower and knowledge: Also as this budget planning tool is very difficult

to understand it requires a good amount of the knowledge and organization require the external

employee in the organization for carry out the same. This eventually used to increase the cost of

the company as recruitment cost of the company used to rise. Also, to build the knowledge

10

to ignore the cash flow beyond the payback period in the organization (Almazan Chen and

Titman, 2017).

Zero Based Budgeting

Zero based budgeting is the planning budgeting in which all the expenses of the

organization are justified for each new period in the organization. In this planning budgeting all

the thing are started from the zero and on the basis of the same budget are built around what is

need by the organization for upcoming period. Irrespective of the previous budget which was

made in the organization.

Advantages:

Allocation of the resource: Zero based planning budgeting tool is one of the best tool

for allocating the different resources in the organization. The reason behind the same is that this

planning tool used to analysis the needs and benefits and on the basis of the same used to allocate

the resources. This eventually used to increase the efficiency of the business performance in the

organization as the wastage of the resources are minimized in the organization.

Motivation and communication: This planning budgeting tool used to improve the level

of the motivation and the communication in the organization. This planning tool used to help the

employee in improving the level of the motivation because this tool used to give them more

initiative and responsibility in the decision-making (Oraka, Sopekan and Udeh, 2016). Also, this

tool help the organization in improving the communication and coordination at the time of

making the different decision in the organization.

Disadvantages:

Time consuming: This is the biggest disadvantage of using Zero based budgeting as the

planning tool. As this tool used to consume a good amount of the time for the manager to define

the necessary expenditure on the time. As this tool is overdependent on the same it used to

consume the good amount of the time for the organization to give a result of the same.

Requires manpower and knowledge: Also as this budget planning tool is very difficult

to understand it requires a good amount of the knowledge and organization require the external

employee in the organization for carry out the same. This eventually used to increase the cost of

the company as recruitment cost of the company used to rise. Also, to build the knowledge

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.