Analysis of Management Accounting Techniques: Prime Furniture Report

VerifiedAdded on 2022/12/23

|12

|3172

|38

Report

AI Summary

This management accounting report provides a comprehensive overview of key concepts and techniques relevant to business students. The report begins with an introduction to management accounting and its essential components, including cost-accounting, inventory management, job costing, and price optimization systems. It then explores different types of management accounting reporting, such as budget reports, performance reports, and cost management reports. The report delves into cost calculation using both marginal and absorption costing techniques, including income statements and profit reconciliation statements. Furthermore, the report examines the advantages and disadvantages of various planning tools utilized in budgetary control, including zero-based budgeting, capital budgeting, and pricing strategies. Finally, the report compares how organizations respond to financial problems. The report utilizes Prime Furniture as a case study to illustrate the practical application of these concepts.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

P1 Management accounting & management accounting system essentials...........................3

P2 Types of Management accounting reporting.....................................................................4

Task 2...............................................................................................................................................5

P3 Cost calculation using different costing techniques..........................................................5

Task 3...............................................................................................................................................7

P4 Advantages & disadvantages types of planning tools used in budgetary control.............7

Task 4...............................................................................................................................................9

P5 Comparison between organisations while responding to financial problems...................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

P1 Management accounting & management accounting system essentials...........................3

P2 Types of Management accounting reporting.....................................................................4

Task 2...............................................................................................................................................5

P3 Cost calculation using different costing techniques..........................................................5

Task 3...............................................................................................................................................7

P4 Advantages & disadvantages types of planning tools used in budgetary control.............7

Task 4...............................................................................................................................................9

P5 Comparison between organisations while responding to financial problems...................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Introduction

Management accounting is a unique tool which has been using by management of a

company to assist in decision making which is made by top level management. It is considered

as provision for related financial & non-financial decision making data to related managerial

personnel. It is somehow different from financial management as management accounting is

more concerned about decision making where as financial management is related to financial

position of an organisation. Management accounting is referred to identification, accumulation,

measurement, preparation, analysis and interpretation as well as communication of certain

information which assists managers for fulfilment of organisational objectives. In this respect,

management accounting techniques are being discussed in reference to Prime Furniture which is

one of most developing company which is based in East London, UK.

Task 1

P1 Management accounting & management accounting system essentials

Cost-accounting system: It is a concept which suggests assessment of cost related elements

in order to aid in decision making for long term growth and sustainability of an organisation

(Alawattage and Wickramasinghe, 2018). It is considered as one of effective technique

which helps in identification of cost structure of an entity so that cost could be minimised

and profits could be maximised in such reference. Cost plays significant role in organisation

development as it is important to reduce higher incurring cost so that it will be easier to

attain ultimate profitability by an organisation.

Benefits: It helps in disclosing organisational profitable and non-profitable activities

which is being involved in business operations. It also guides in future policy strategies

so that cost effectiveness could be given adequate emphasis.

Inventory management system: It refers to a process in which products are tracked through

entire supply chain which starts from purchasing of raw items, production goods and

ultimate sale to customers (Álvarez and et. al., 2021). This approach is used to manage

inventory system in an organisation with help of effective approaches. It is important for

business organisation to track & control flow of goods which are being part of its supply

chain in order to promote healthy supply chain system.

Management accounting is a unique tool which has been using by management of a

company to assist in decision making which is made by top level management. It is considered

as provision for related financial & non-financial decision making data to related managerial

personnel. It is somehow different from financial management as management accounting is

more concerned about decision making where as financial management is related to financial

position of an organisation. Management accounting is referred to identification, accumulation,

measurement, preparation, analysis and interpretation as well as communication of certain

information which assists managers for fulfilment of organisational objectives. In this respect,

management accounting techniques are being discussed in reference to Prime Furniture which is

one of most developing company which is based in East London, UK.

Task 1

P1 Management accounting & management accounting system essentials

Cost-accounting system: It is a concept which suggests assessment of cost related elements

in order to aid in decision making for long term growth and sustainability of an organisation

(Alawattage and Wickramasinghe, 2018). It is considered as one of effective technique

which helps in identification of cost structure of an entity so that cost could be minimised

and profits could be maximised in such reference. Cost plays significant role in organisation

development as it is important to reduce higher incurring cost so that it will be easier to

attain ultimate profitability by an organisation.

Benefits: It helps in disclosing organisational profitable and non-profitable activities

which is being involved in business operations. It also guides in future policy strategies

so that cost effectiveness could be given adequate emphasis.

Inventory management system: It refers to a process in which products are tracked through

entire supply chain which starts from purchasing of raw items, production goods and

ultimate sale to customers (Álvarez and et. al., 2021). This approach is used to manage

inventory system in an organisation with help of effective approaches. It is important for

business organisation to track & control flow of goods which are being part of its supply

chain in order to promote healthy supply chain system.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Benefits: It is effective approach towards cost-reduction and monitoring of stock balance

so that excess stock and stock out situations could be regulated.

Job costing system: It is a technique which is used in accumulation of cost related

information which is associated with specified service job or production centre. It is referred

to basic cost value which is applied to individual projects or jobs in an organisation.

Through this method, it becomes easier to identify cost structure of each activity in an

organisation so that efficiency could be achieved for long lasting period.

Benefits: This approach is helpful in identification of accurate profits which is attained

from each operation in an organisation. Also it monitors cost of items through production

procedures. This technique also identifies performance of employees in regard to each

business operations so that loopholes could be identified and effective techniques could

be utilized to eliminate such loophole (Amirshenava and Osanloo, 2018).

Price optimization system: It is most effective technique which is used in order to identify

reason of fluctuations in prices due to changing demands of customers. It is used to

influence pricing for different customer units in order to identify the way customers will

respond to changing price levels in a market (Coyte, 2019). It is very beneficial technique

for an organisation in order to attain profitability and productivity in an organisation. There

are also various benefits of price optimisation system which can be analysed as below.

Benefits: It benefits an organisation to achieve ultimate financial advantage through price

optimisation in reference to its products and service so that maximum profits could be

attained for long lasting period.

P2 Types of Management accounting reporting

Budget Report: It describes comparison of actual results of business operations to

forecasted data in order to identify key areas of improvement so that corrective actions

could be taken for further modification in such areas. Budget is basically formulated in

order to regulate cost structure of an organisation of that maximum profitability can be

achieved (Duggan, 2018). It is one of most used technique in order to control financial

results of an organisation based operations. There are several benefits of budgeting such

as it helps in reviewing future based profitability, planning for such profitability and

performance evaluation so that efficiency could be achieved for ultimate success of an

so that excess stock and stock out situations could be regulated.

Job costing system: It is a technique which is used in accumulation of cost related

information which is associated with specified service job or production centre. It is referred

to basic cost value which is applied to individual projects or jobs in an organisation.

Through this method, it becomes easier to identify cost structure of each activity in an

organisation so that efficiency could be achieved for long lasting period.

Benefits: This approach is helpful in identification of accurate profits which is attained

from each operation in an organisation. Also it monitors cost of items through production

procedures. This technique also identifies performance of employees in regard to each

business operations so that loopholes could be identified and effective techniques could

be utilized to eliminate such loophole (Amirshenava and Osanloo, 2018).

Price optimization system: It is most effective technique which is used in order to identify

reason of fluctuations in prices due to changing demands of customers. It is used to

influence pricing for different customer units in order to identify the way customers will

respond to changing price levels in a market (Coyte, 2019). It is very beneficial technique

for an organisation in order to attain profitability and productivity in an organisation. There

are also various benefits of price optimisation system which can be analysed as below.

Benefits: It benefits an organisation to achieve ultimate financial advantage through price

optimisation in reference to its products and service so that maximum profits could be

attained for long lasting period.

P2 Types of Management accounting reporting

Budget Report: It describes comparison of actual results of business operations to

forecasted data in order to identify key areas of improvement so that corrective actions

could be taken for further modification in such areas. Budget is basically formulated in

order to regulate cost structure of an organisation of that maximum profitability can be

achieved (Duggan, 2018). It is one of most used technique in order to control financial

results of an organisation based operations. There are several benefits of budgeting such

as it helps in reviewing future based profitability, planning for such profitability and

performance evaluation so that efficiency could be achieved for ultimate success of an

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organisation for long term. Also adequate cash allocation could be made so that activities

will be able to operate in smooth manner to achieve productivity.

Performance Report: Business performance report facilitates management to identify

and understand prevailing and potential growth segments in an organisation so that

forecasted performance could be achieved by the company. Business organisation is

required to continuously track performance and efficiency of business operations to

implement effective strategies so that sustainable growth can be achieved. It is therefore

important for an organisation to use performance reports so that efficiency and

productivity of business operations could be identified for further improvement or

modification in such area. It is one of the most beneficial reporting formats which have

vast usage in terms of performance evaluation in regard to organisation. Therefore

organisation should formulate use of such report so that maximum benefits can be

achieved by an organisation (Flaah, 2020).

Cost management Report: This is defined as procedure of planning as well as

controlling of business cost structure by using cost effective and cost reduction

techniques in this concern. It is one of the most effective techniques in order to eliminate

excess cost which is being incurred by an organisation in order to meet forecasted profit

requirement for long sustainable period. It is also said to be integral part of business

organisation which aids in decision making in relation to cost related matters so that

efficiency could be achieved and profitability will be promoted. There are certain benefits

of this reporting such as it establishes accountability of each cost by people who have

performed such task to which such cost is associated. It is helpful form of reporting

which should be used for achieving business efficiency and productivity in relation to

cost structure of a business entity. It is therefore needs to be implemented by an

organisation in its business reports in order to facilitate managers for ultimate decision

making in this regard. (Ghasemi and et. al., 2019).

Task 2

P3 Cost calculation using different costing techniques

will be able to operate in smooth manner to achieve productivity.

Performance Report: Business performance report facilitates management to identify

and understand prevailing and potential growth segments in an organisation so that

forecasted performance could be achieved by the company. Business organisation is

required to continuously track performance and efficiency of business operations to

implement effective strategies so that sustainable growth can be achieved. It is therefore

important for an organisation to use performance reports so that efficiency and

productivity of business operations could be identified for further improvement or

modification in such area. It is one of the most beneficial reporting formats which have

vast usage in terms of performance evaluation in regard to organisation. Therefore

organisation should formulate use of such report so that maximum benefits can be

achieved by an organisation (Flaah, 2020).

Cost management Report: This is defined as procedure of planning as well as

controlling of business cost structure by using cost effective and cost reduction

techniques in this concern. It is one of the most effective techniques in order to eliminate

excess cost which is being incurred by an organisation in order to meet forecasted profit

requirement for long sustainable period. It is also said to be integral part of business

organisation which aids in decision making in relation to cost related matters so that

efficiency could be achieved and profitability will be promoted. There are certain benefits

of this reporting such as it establishes accountability of each cost by people who have

performed such task to which such cost is associated. It is helpful form of reporting

which should be used for achieving business efficiency and productivity in relation to

cost structure of a business entity. It is therefore needs to be implemented by an

organisation in its business reports in order to facilitate managers for ultimate decision

making in this regard. (Ghasemi and et. al., 2019).

Task 2

P3 Cost calculation using different costing techniques

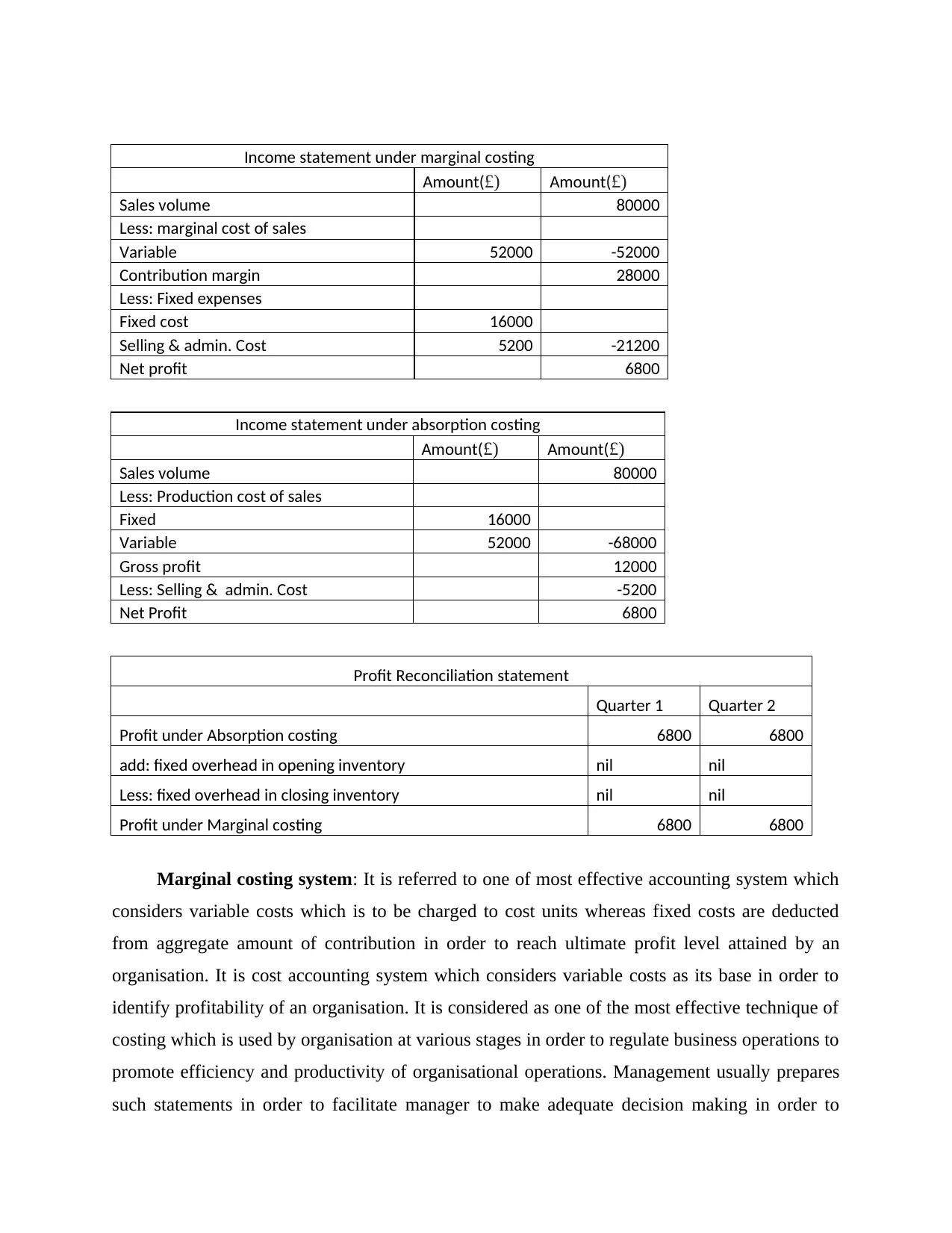

Income statement under marginal costing

Amount(£) Amount(£)

Sales volume 80000

Less: marginal cost of sales

Variable 52000 -52000

Contribution margin 28000

Less: Fixed expenses

Fixed cost 16000

Selling & admin. Cost 5200 -21200

Net profit 6800

Income statement under absorption costing

Amount(£) Amount(£)

Sales volume 80000

Less: Production cost of sales

Fixed 16000

Variable 52000 -68000

Gross profit 12000

Less: Selling & admin. Cost -5200

Net Profit 6800

Profit Reconciliation statement

Quarter 1 Quarter 2

Profit under Absorption costing 6800 6800

add: fixed overhead in opening inventory nil nil

Less: fixed overhead in closing inventory nil nil

Profit under Marginal costing 6800 6800

Marginal costing system: It is referred to one of most effective accounting system which

considers variable costs which is to be charged to cost units whereas fixed costs are deducted

from aggregate amount of contribution in order to reach ultimate profit level attained by an

organisation. It is cost accounting system which considers variable costs as its base in order to

identify profitability of an organisation. It is considered as one of the most effective technique of

costing which is used by organisation at various stages in order to regulate business operations to

promote efficiency and productivity of organisational operations. Management usually prepares

such statements in order to facilitate manager to make adequate decision making in order to

Amount(£) Amount(£)

Sales volume 80000

Less: marginal cost of sales

Variable 52000 -52000

Contribution margin 28000

Less: Fixed expenses

Fixed cost 16000

Selling & admin. Cost 5200 -21200

Net profit 6800

Income statement under absorption costing

Amount(£) Amount(£)

Sales volume 80000

Less: Production cost of sales

Fixed 16000

Variable 52000 -68000

Gross profit 12000

Less: Selling & admin. Cost -5200

Net Profit 6800

Profit Reconciliation statement

Quarter 1 Quarter 2

Profit under Absorption costing 6800 6800

add: fixed overhead in opening inventory nil nil

Less: fixed overhead in closing inventory nil nil

Profit under Marginal costing 6800 6800

Marginal costing system: It is referred to one of most effective accounting system which

considers variable costs which is to be charged to cost units whereas fixed costs are deducted

from aggregate amount of contribution in order to reach ultimate profit level attained by an

organisation. It is cost accounting system which considers variable costs as its base in order to

identify profitability of an organisation. It is considered as one of the most effective technique of

costing which is used by organisation at various stages in order to regulate business operations to

promote efficiency and productivity of organisational operations. Management usually prepares

such statements in order to facilitate manager to make adequate decision making in order to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

achieve ultimate success towards market expansion and other factors. Therefore, it is

considerably important technique which needs to be formulised so that managers will be able to

produce appropriate decisions towards business future growth prospects. It should be considered

by organisations in terms of increasing profitability and sustainability for long term basis (Libby

and Salterio, 2019).

Absorption costing system: This approach is combination of different costs including

fixed, variables and others through which company’s profit is been calculated for the given

period of time. It varies from marginal costing as it considers fixed cost to allocate at each unit of

product manufactured in given period. It considers both fixed and variable cost in production of

production in specific period. This costing structure includes both direct and indirect cost for

calculation of profits. Various indirect and direct costs include material, labour, factory cost,

administration expenditure, and insurance and so on. Various organisations include this approach

of costing in order to reach profit which is being generated by an organisation from day to day

activities. It is one of the effective approaches of cost management which has been used towards

profit maximisation and cost reduction for promoting efficiency of an organisation. It is very

helpful in decision making process made by managers in respect of an organisation for ultimate

success. Therefore, it is important to adopt adequate cost technique by an organisation in order to

promote healthy decision making and efficiency of procedures of business operations (McShane,

2018).

Task 3

P4 Advantages & disadvantages types of planning tools used in budgetary control

Zero based Budgeting: It is a type of budget which is prepared from the scratch or zero

bases. It required justifying each & every expense of business operations before adding

such expense in budget forecast. It is newly established form of budget which is also

known as modern budgeting technique which is helpful in building cost structure for

future prospect (Myers, 2019). Generally budgets are based on historical or past data of

an organisation through which future cost is being forecasted in order to eliminate

unnecessary expenditure and promote profitability for long lasting period. But in this type

of budget, historical data is not considered while development of budget. It starts budget

considerably important technique which needs to be formulised so that managers will be able to

produce appropriate decisions towards business future growth prospects. It should be considered

by organisations in terms of increasing profitability and sustainability for long term basis (Libby

and Salterio, 2019).

Absorption costing system: This approach is combination of different costs including

fixed, variables and others through which company’s profit is been calculated for the given

period of time. It varies from marginal costing as it considers fixed cost to allocate at each unit of

product manufactured in given period. It considers both fixed and variable cost in production of

production in specific period. This costing structure includes both direct and indirect cost for

calculation of profits. Various indirect and direct costs include material, labour, factory cost,

administration expenditure, and insurance and so on. Various organisations include this approach

of costing in order to reach profit which is being generated by an organisation from day to day

activities. It is one of the effective approaches of cost management which has been used towards

profit maximisation and cost reduction for promoting efficiency of an organisation. It is very

helpful in decision making process made by managers in respect of an organisation for ultimate

success. Therefore, it is important to adopt adequate cost technique by an organisation in order to

promote healthy decision making and efficiency of procedures of business operations (McShane,

2018).

Task 3

P4 Advantages & disadvantages types of planning tools used in budgetary control

Zero based Budgeting: It is a type of budget which is prepared from the scratch or zero

bases. It required justifying each & every expense of business operations before adding

such expense in budget forecast. It is newly established form of budget which is also

known as modern budgeting technique which is helpful in building cost structure for

future prospect (Myers, 2019). Generally budgets are based on historical or past data of

an organisation through which future cost is being forecasted in order to eliminate

unnecessary expenditure and promote profitability for long lasting period. But in this type

of budget, historical data is not considered while development of budget. It starts budget

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

from zero base and reduce cost which could incur in further business operations in order

to promote efficiency and productivity of business organisation.

Advantages: This technique is considered as cost centric, prioritizes allocation of

resources efficiently and strengthen growth and & transparency of business operations

with adequate decision making.

Disadvantages: Being modern approach of budgeting it might be complex at several

times and lacks proper understanding of situation as well as little expensive as compared

to other approaches of budgeting.

Capital budgeting: It is a method which is used in order to determine the fixed asset

purchase it is to be considered or to be rejected in order to conduct smooth flow of

business operations (Nartey and et. al., 2020). It is capital asset centric approach so that

expenditure to be made in such regard can be regulated in effective manner. It is one of

the most effective approach of budgeting which does not consider operating expenditure

but focuses over capital expenditure which needs to be carried out by an organisation for

ultimate profitability and to fulfil need and requirement of organisation.

Advantages: It is beneficial technique which identifies risks being involved in an

investment and most appropriate investment opportunity to be adopted by an organisation

for long term sustainability.

Disadvantages: Though it is very beneficial yet it lacks certainty as it is base on

assumption and future forecasts in reference to a business unit for long term basis.

Pricing strategies: It is one of most effective approach which provides different pricing

strategies which needs to be adopted by an organisation for long term market

sustainability and enhancing market share for long term basis. There are various pricing

strategies such as cost plus pricing, price skimming, competitive pricing and so on. These

pricing policies are helpful in determining which price strategy will be most effective for

business organisation in order to attract maximum of customers and enhance profitability

for long lasting period (Pandey and Gupta, 2020).

Advantages: various pricing strategies such as cost plus policy are easy to implement and

understand and therefore it is mostly adopted by organisation to promote long term

profitability. It is important to adopt appropriate pricing strategy in order to become most

successful venture.

to promote efficiency and productivity of business organisation.

Advantages: This technique is considered as cost centric, prioritizes allocation of

resources efficiently and strengthen growth and & transparency of business operations

with adequate decision making.

Disadvantages: Being modern approach of budgeting it might be complex at several

times and lacks proper understanding of situation as well as little expensive as compared

to other approaches of budgeting.

Capital budgeting: It is a method which is used in order to determine the fixed asset

purchase it is to be considered or to be rejected in order to conduct smooth flow of

business operations (Nartey and et. al., 2020). It is capital asset centric approach so that

expenditure to be made in such regard can be regulated in effective manner. It is one of

the most effective approach of budgeting which does not consider operating expenditure

but focuses over capital expenditure which needs to be carried out by an organisation for

ultimate profitability and to fulfil need and requirement of organisation.

Advantages: It is beneficial technique which identifies risks being involved in an

investment and most appropriate investment opportunity to be adopted by an organisation

for long term sustainability.

Disadvantages: Though it is very beneficial yet it lacks certainty as it is base on

assumption and future forecasts in reference to a business unit for long term basis.

Pricing strategies: It is one of most effective approach which provides different pricing

strategies which needs to be adopted by an organisation for long term market

sustainability and enhancing market share for long term basis. There are various pricing

strategies such as cost plus pricing, price skimming, competitive pricing and so on. These

pricing policies are helpful in determining which price strategy will be most effective for

business organisation in order to attract maximum of customers and enhance profitability

for long lasting period (Pandey and Gupta, 2020).

Advantages: various pricing strategies such as cost plus policy are easy to implement and

understand and therefore it is mostly adopted by organisation to promote long term

profitability. It is important to adopt appropriate pricing strategy in order to become most

successful venture.

Disadvantages: In cost pricing approach major drawback is said to be higher pricing due

to which overall sale of products would be reduced which can lead to losses or reduced

profit-margins.

Variance analysis: It is a procedure in which summary of deviation between actual

performance and forecasted performance is being produced before managers in order to

promote effective and efficient decision making. It is most important technique which

needs to be established by organisations in order to produce ultimate improvement

decision making which needs to be made for rectification of such deviation between

actual and forecasted performance of an organisation during specific period of time.

Advantages: It is helpful in elimination of errors or deviations in actual and budgeted

performance which will promote efficiency in business operations (Tucker, 2019).

Disadvantages: Though it is very beneficial yet it is complex while formulating it in order

to reach such deviation in the performance of an organisation.

Task 4

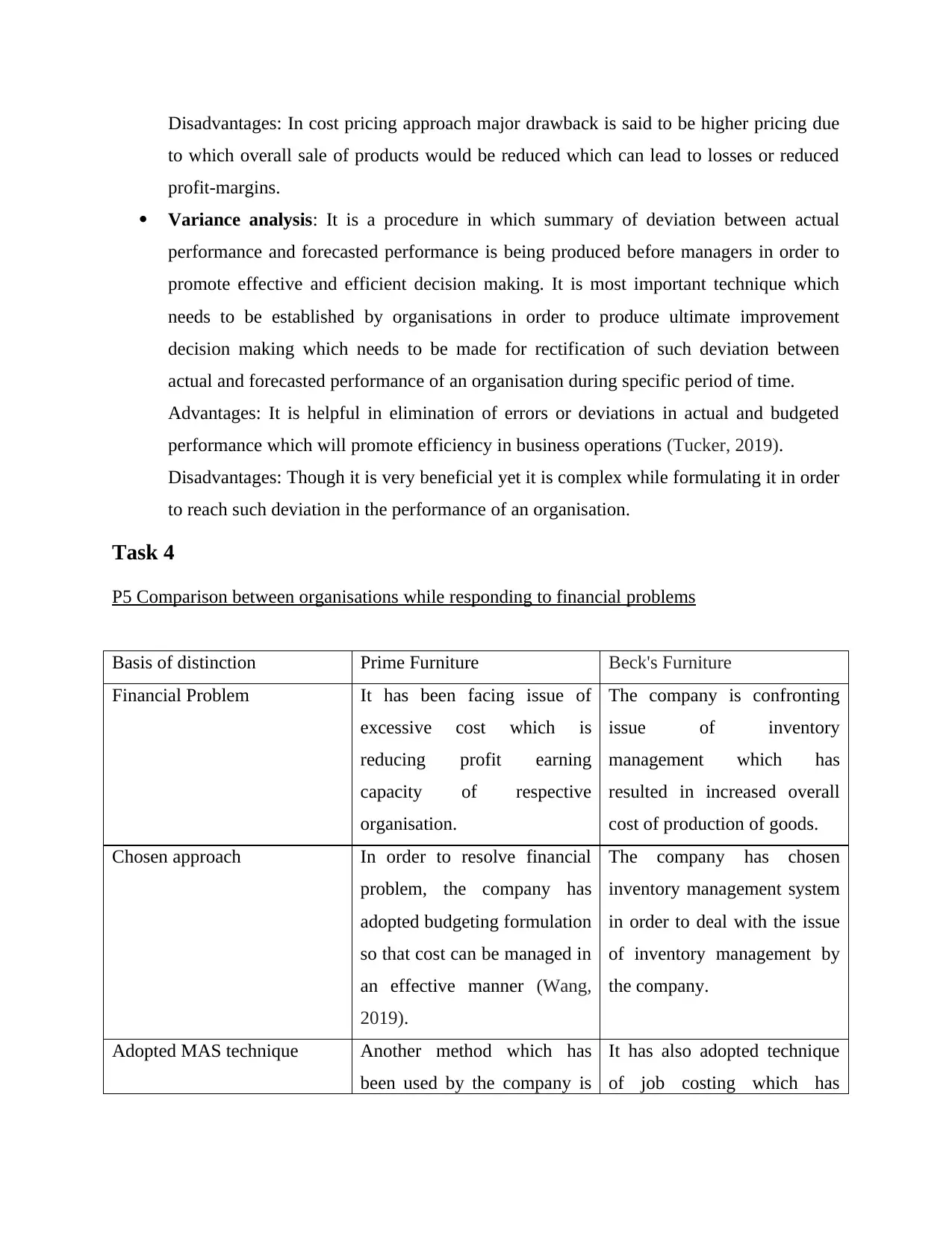

P5 Comparison between organisations while responding to financial problems

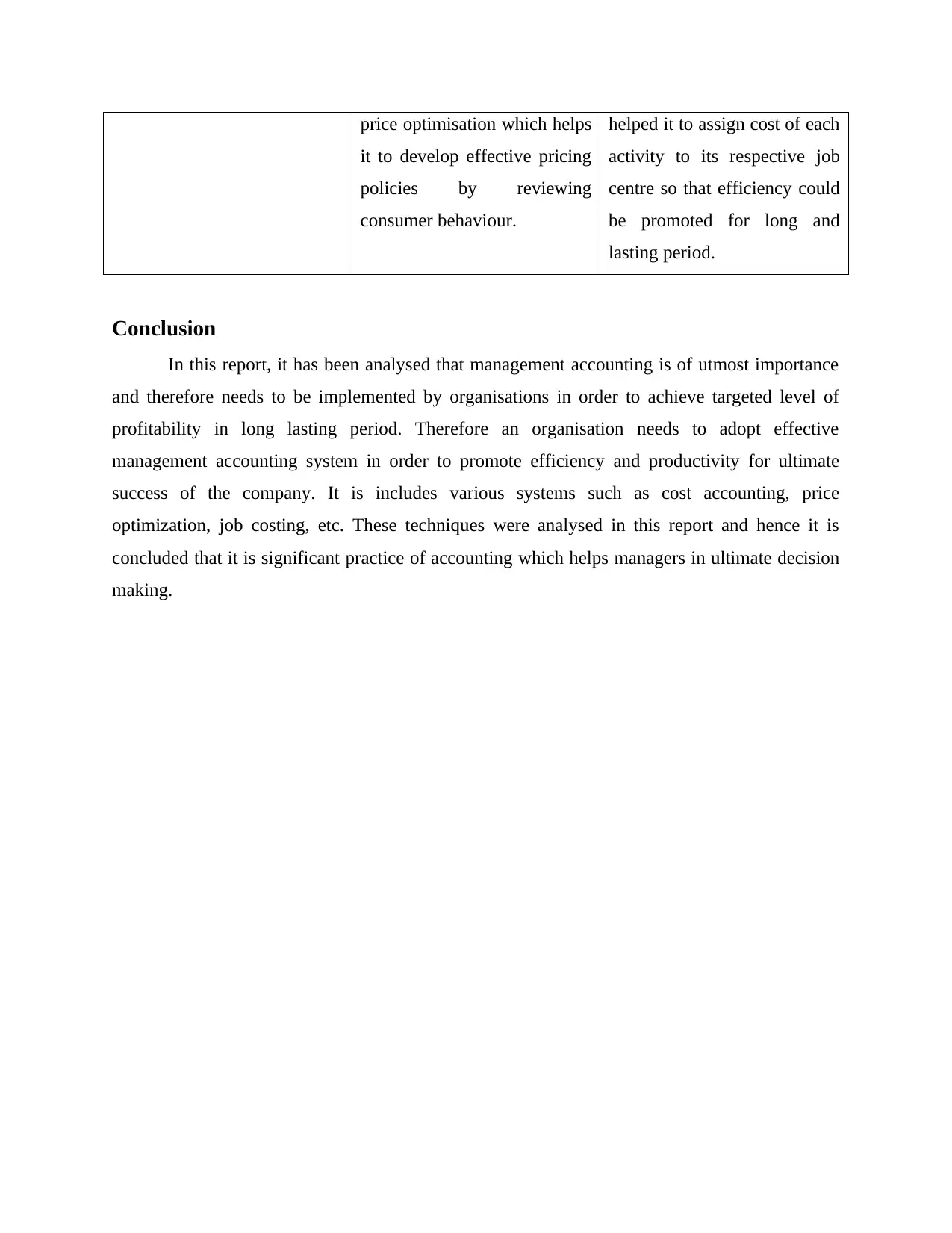

Basis of distinction Prime Furniture Beck's Furniture

Financial Problem It has been facing issue of

excessive cost which is

reducing profit earning

capacity of respective

organisation.

The company is confronting

issue of inventory

management which has

resulted in increased overall

cost of production of goods.

Chosen approach In order to resolve financial

problem, the company has

adopted budgeting formulation

so that cost can be managed in

an effective manner (Wang,

2019).

The company has chosen

inventory management system

in order to deal with the issue

of inventory management by

the company.

Adopted MAS technique Another method which has

been used by the company is

It has also adopted technique

of job costing which has

to which overall sale of products would be reduced which can lead to losses or reduced

profit-margins.

Variance analysis: It is a procedure in which summary of deviation between actual

performance and forecasted performance is being produced before managers in order to

promote effective and efficient decision making. It is most important technique which

needs to be established by organisations in order to produce ultimate improvement

decision making which needs to be made for rectification of such deviation between

actual and forecasted performance of an organisation during specific period of time.

Advantages: It is helpful in elimination of errors or deviations in actual and budgeted

performance which will promote efficiency in business operations (Tucker, 2019).

Disadvantages: Though it is very beneficial yet it is complex while formulating it in order

to reach such deviation in the performance of an organisation.

Task 4

P5 Comparison between organisations while responding to financial problems

Basis of distinction Prime Furniture Beck's Furniture

Financial Problem It has been facing issue of

excessive cost which is

reducing profit earning

capacity of respective

organisation.

The company is confronting

issue of inventory

management which has

resulted in increased overall

cost of production of goods.

Chosen approach In order to resolve financial

problem, the company has

adopted budgeting formulation

so that cost can be managed in

an effective manner (Wang,

2019).

The company has chosen

inventory management system

in order to deal with the issue

of inventory management by

the company.

Adopted MAS technique Another method which has

been used by the company is

It has also adopted technique

of job costing which has

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

price optimisation which helps

it to develop effective pricing

policies by reviewing

consumer behaviour.

helped it to assign cost of each

activity to its respective job

centre so that efficiency could

be promoted for long and

lasting period.

Conclusion

In this report, it has been analysed that management accounting is of utmost importance

and therefore needs to be implemented by organisations in order to achieve targeted level of

profitability in long lasting period. Therefore an organisation needs to adopt effective

management accounting system in order to promote efficiency and productivity for ultimate

success of the company. It is includes various systems such as cost accounting, price

optimization, job costing, etc. These techniques were analysed in this report and hence it is

concluded that it is significant practice of accounting which helps managers in ultimate decision

making.

it to develop effective pricing

policies by reviewing

consumer behaviour.

helped it to assign cost of each

activity to its respective job

centre so that efficiency could

be promoted for long and

lasting period.

Conclusion

In this report, it has been analysed that management accounting is of utmost importance

and therefore needs to be implemented by organisations in order to achieve targeted level of

profitability in long lasting period. Therefore an organisation needs to adopt effective

management accounting system in order to promote efficiency and productivity for ultimate

success of the company. It is includes various systems such as cost accounting, price

optimization, job costing, etc. These techniques were analysed in this report and hence it is

concluded that it is significant practice of accounting which helps managers in ultimate decision

making.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Books and journals

Alawattage, C. and Wickramasinghe, D., 2018. Strategizing Management Accounting: Liberal

Origins and Neoliberal Trends. Routledge.

Álvarez, C.B. and et. al., 2021. Management accounting practices and efficiency in a Colombian

multi-utility conglomerate. Journal of Accounting in Emerging Economies.

Amirshenava, S. and Osanloo, M., 2018. Mine closure risk management: an integration of 3D

risk model and MCDM techniques. Journal of cleaner production. 184. pp.389-401.

Coyte, R., 2019. Enabling management control systems, situated learning and intellectual capital

development. Accounting, Auditing & Accountability Journal.

Duggan, K.J., 2018. Creating mixed model value streams: practical lean techniques for building

to demand. CRC Press.

Flaah, H.J., 2020. A suggested model for the application of resource consumption accounting

approach in the oil refining industry Applied study in south refineries

company. Managerial Studies Journal. 13(27).

Ghasemi, R. and et. al., 2019. The effectiveness of management accounting systems: evidence

from financial organizations in Iran. Journal of Accounting in Emerging Economies.

Libby, T. and Salterio, S.E., 2019. Deception in management accounting experimental

research:“A tricky issue” revisited. Journal of Management Accounting Research. 31(2).

pp.143-158.

McShane, M., 2018. Enterprise risk management: history and a design science proposal. The

Journal of Risk Finance.

Myers, M.D., 2019. Qualitative research in business and management. Sage.

Nartey, E. and et. al., 2020. The contingency effects of supply chain integration on management

control system design and operational performance of hospitals in Ghana. Journal of

Accounting in Emerging Economies.

Pandey, A. and Gupta, R., 2020. A structural equation model of financial accounting practices

and use of it impacting msmes performance: Moderation by entrepreneurial

skills. JIMS8M: The Journal of Indian Management & Strategy. 25(3). pp.21-30.

Books and journals

Alawattage, C. and Wickramasinghe, D., 2018. Strategizing Management Accounting: Liberal

Origins and Neoliberal Trends. Routledge.

Álvarez, C.B. and et. al., 2021. Management accounting practices and efficiency in a Colombian

multi-utility conglomerate. Journal of Accounting in Emerging Economies.

Amirshenava, S. and Osanloo, M., 2018. Mine closure risk management: an integration of 3D

risk model and MCDM techniques. Journal of cleaner production. 184. pp.389-401.

Coyte, R., 2019. Enabling management control systems, situated learning and intellectual capital

development. Accounting, Auditing & Accountability Journal.

Duggan, K.J., 2018. Creating mixed model value streams: practical lean techniques for building

to demand. CRC Press.

Flaah, H.J., 2020. A suggested model for the application of resource consumption accounting

approach in the oil refining industry Applied study in south refineries

company. Managerial Studies Journal. 13(27).

Ghasemi, R. and et. al., 2019. The effectiveness of management accounting systems: evidence

from financial organizations in Iran. Journal of Accounting in Emerging Economies.

Libby, T. and Salterio, S.E., 2019. Deception in management accounting experimental

research:“A tricky issue” revisited. Journal of Management Accounting Research. 31(2).

pp.143-158.

McShane, M., 2018. Enterprise risk management: history and a design science proposal. The

Journal of Risk Finance.

Myers, M.D., 2019. Qualitative research in business and management. Sage.

Nartey, E. and et. al., 2020. The contingency effects of supply chain integration on management

control system design and operational performance of hospitals in Ghana. Journal of

Accounting in Emerging Economies.

Pandey, A. and Gupta, R., 2020. A structural equation model of financial accounting practices

and use of it impacting msmes performance: Moderation by entrepreneurial

skills. JIMS8M: The Journal of Indian Management & Strategy. 25(3). pp.21-30.

Tucker, B.P., 2019. Heard it through the grapevine: conceptualizing informal control through the

lens of social network theory. Journal of Management Accounting Research. 31(1).

pp.219-245.

Wang, T., 2019. Integration of Financial Accounting and Management Accounting. World

Scientific Research Journal. 5(11). pp.191-195.

lens of social network theory. Journal of Management Accounting Research. 31(1).

pp.219-245.

Wang, T., 2019. Integration of Financial Accounting and Management Accounting. World

Scientific Research Journal. 5(11). pp.191-195.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.