Analysis of Costing Methods for Management Accounting (ACC200)

VerifiedAdded on 2022/08/27

|10

|2441

|33

Homework Assignment

AI Summary

This assignment analyzes management accounting principles, focusing on the application of traditional costing and activity-based costing (ABC) methods. The student calculates predetermined overhead rates, determines product costs and selling prices for Kona and Malaysian coffee using both methods, and conducts a comparative analysis highlighting the differences between the two costing systems. The assignment includes detailed calculations, cost allocations, and a discussion on the suitability of each method for different business scenarios, with recommendations for pricing structures. The student also provides a clear comparison between Traditional Costing Method and Activity Based Costing Method. The document includes references to support the analysis.

Running head: INTRODUCTION TO MANAGEMENT ACCOUNTING

Introduction to Management Accounting

Name of the Student:

Name of the University:

Author Note

Introduction to Management Accounting

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1INTRODUCTION TO MANAGEMENT ACCOUNTING

Table of Contents

1a) Analysing the values for detecting the predetermined overhead rate of the

company:..................................................................................................................................2

1b) Understanding the pricing and selling price of Kona Coffee and Malaysian coffee

for 1kg:......................................................................................................................................2

2) Utilising the method of activity-based costing for deriving the prices of Kona

Coffee and Malaysian coffee:................................................................................................3

3a) Conduiting a comparative analysis on the results, while providing specific

clarification on the difference between traditional costing system and Activity based

costing system:........................................................................................................................5

3b) Providing appropriate recommendation for the overall pricing structure for the

products:...................................................................................................................................7

References:..............................................................................................................................9

Table of Contents

1a) Analysing the values for detecting the predetermined overhead rate of the

company:..................................................................................................................................2

1b) Understanding the pricing and selling price of Kona Coffee and Malaysian coffee

for 1kg:......................................................................................................................................2

2) Utilising the method of activity-based costing for deriving the prices of Kona

Coffee and Malaysian coffee:................................................................................................3

3a) Conduiting a comparative analysis on the results, while providing specific

clarification on the difference between traditional costing system and Activity based

costing system:........................................................................................................................5

3b) Providing appropriate recommendation for the overall pricing structure for the

products:...................................................................................................................................7

References:..............................................................................................................................9

2INTRODUCTION TO MANAGEMENT ACCOUNTING

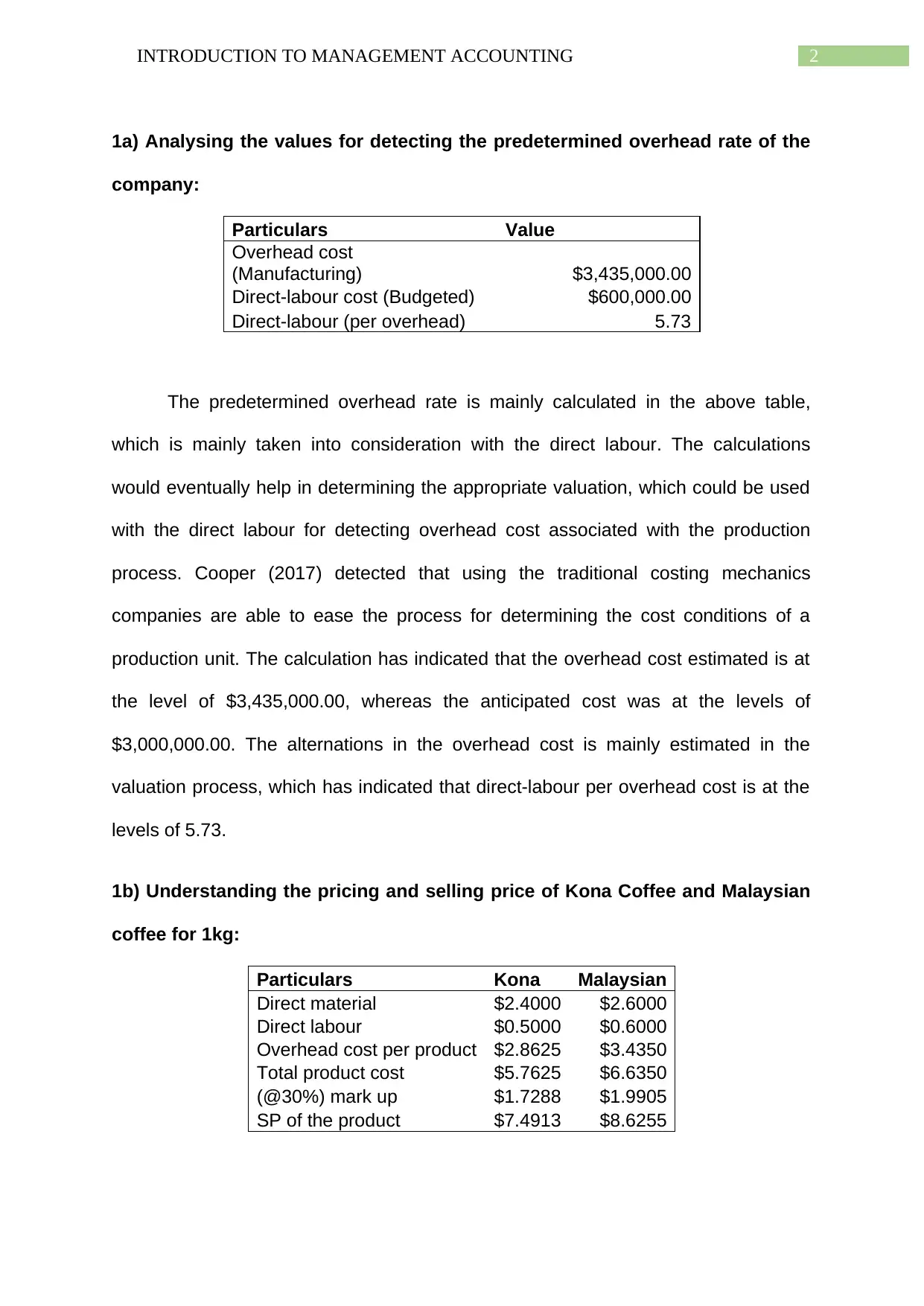

1a) Analysing the values for detecting the predetermined overhead rate of the

company:

Particulars Value

Overhead cost

(Manufacturing) $3,435,000.00

Direct-labour cost (Budgeted) $600,000.00

Direct-labour (per overhead) 5.73

The predetermined overhead rate is mainly calculated in the above table,

which is mainly taken into consideration with the direct labour. The calculations

would eventually help in determining the appropriate valuation, which could be used

with the direct labour for detecting overhead cost associated with the production

process. Cooper (2017) detected that using the traditional costing mechanics

companies are able to ease the process for determining the cost conditions of a

production unit. The calculation has indicated that the overhead cost estimated is at

the level of $3,435,000.00, whereas the anticipated cost was at the levels of

$3,000,000.00. The alternations in the overhead cost is mainly estimated in the

valuation process, which has indicated that direct-labour per overhead cost is at the

levels of 5.73.

1b) Understanding the pricing and selling price of Kona Coffee and Malaysian

coffee for 1kg:

Particulars Kona Malaysian

Direct material $2.4000 $2.6000

Direct labour $0.5000 $0.6000

Overhead cost per product $2.8625 $3.4350

Total product cost $5.7625 $6.6350

(@30%) mark up $1.7288 $1.9905

SP of the product $7.4913 $8.6255

1a) Analysing the values for detecting the predetermined overhead rate of the

company:

Particulars Value

Overhead cost

(Manufacturing) $3,435,000.00

Direct-labour cost (Budgeted) $600,000.00

Direct-labour (per overhead) 5.73

The predetermined overhead rate is mainly calculated in the above table,

which is mainly taken into consideration with the direct labour. The calculations

would eventually help in determining the appropriate valuation, which could be used

with the direct labour for detecting overhead cost associated with the production

process. Cooper (2017) detected that using the traditional costing mechanics

companies are able to ease the process for determining the cost conditions of a

production unit. The calculation has indicated that the overhead cost estimated is at

the level of $3,435,000.00, whereas the anticipated cost was at the levels of

$3,000,000.00. The alternations in the overhead cost is mainly estimated in the

valuation process, which has indicated that direct-labour per overhead cost is at the

levels of 5.73.

1b) Understanding the pricing and selling price of Kona Coffee and Malaysian

coffee for 1kg:

Particulars Kona Malaysian

Direct material $2.4000 $2.6000

Direct labour $0.5000 $0.6000

Overhead cost per product $2.8625 $3.4350

Total product cost $5.7625 $6.6350

(@30%) mark up $1.7288 $1.9905

SP of the product $7.4913 $8.6255

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3INTRODUCTION TO MANAGEMENT ACCOUNTING

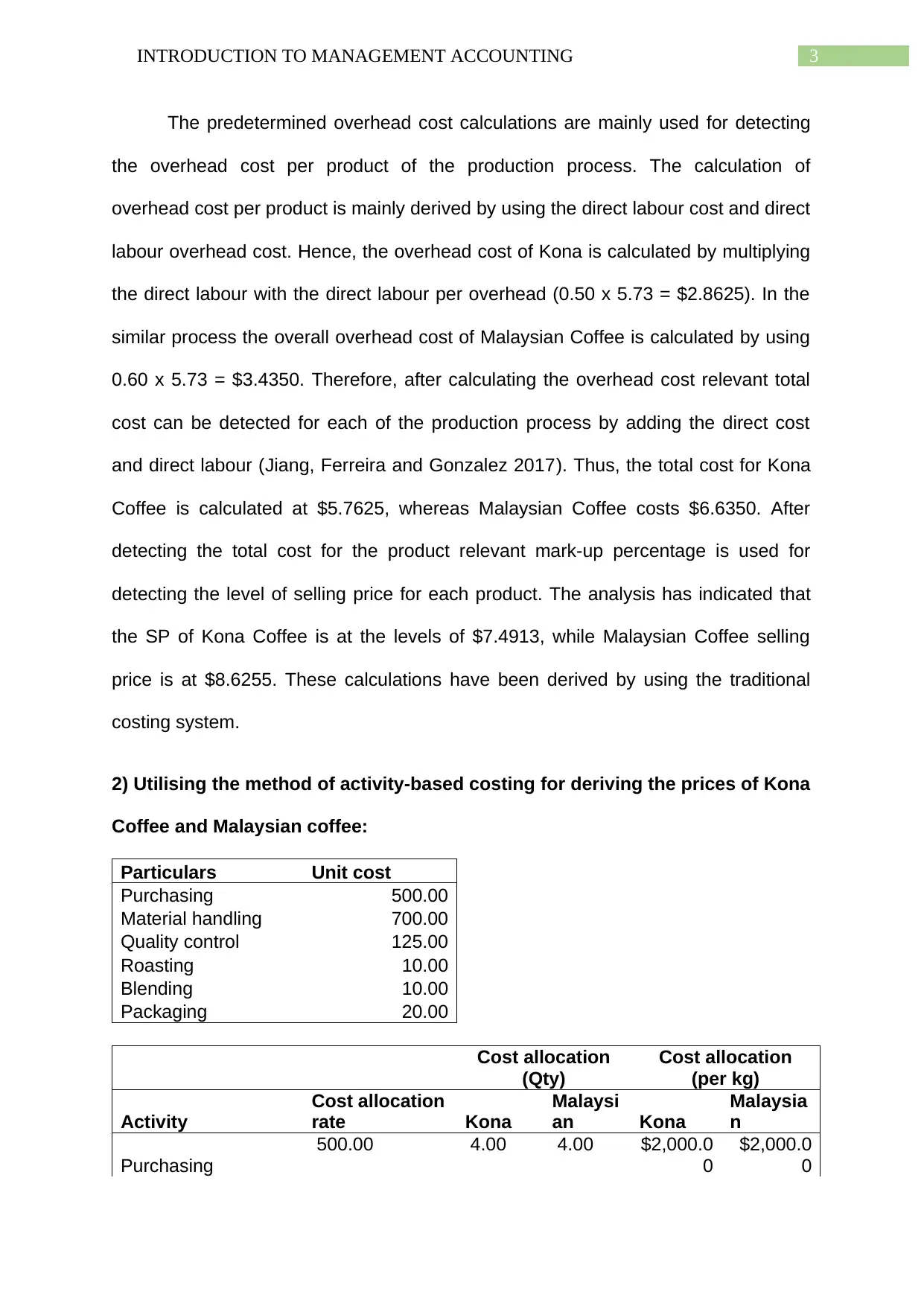

The predetermined overhead cost calculations are mainly used for detecting

the overhead cost per product of the production process. The calculation of

overhead cost per product is mainly derived by using the direct labour cost and direct

labour overhead cost. Hence, the overhead cost of Kona is calculated by multiplying

the direct labour with the direct labour per overhead (0.50 x 5.73 = $2.8625). In the

similar process the overall overhead cost of Malaysian Coffee is calculated by using

0.60 x 5.73 = $3.4350. Therefore, after calculating the overhead cost relevant total

cost can be detected for each of the production process by adding the direct cost

and direct labour (Jiang, Ferreira and Gonzalez 2017). Thus, the total cost for Kona

Coffee is calculated at $5.7625, whereas Malaysian Coffee costs $6.6350. After

detecting the total cost for the product relevant mark-up percentage is used for

detecting the level of selling price for each product. The analysis has indicated that

the SP of Kona Coffee is at the levels of $7.4913, while Malaysian Coffee selling

price is at $8.6255. These calculations have been derived by using the traditional

costing system.

2) Utilising the method of activity-based costing for deriving the prices of Kona

Coffee and Malaysian coffee:

Particulars Unit cost

Purchasing 500.00

Material handling 700.00

Quality control 125.00

Roasting 10.00

Blending 10.00

Packaging 20.00

Cost allocation

(Qty)

Cost allocation

(per kg)

Activity

Cost allocation

rate Kona

Malaysi

an Kona

Malaysia

n

Purchasing

500.00 4.00 4.00 $2,000.0

0

$2,000.0

0

The predetermined overhead cost calculations are mainly used for detecting

the overhead cost per product of the production process. The calculation of

overhead cost per product is mainly derived by using the direct labour cost and direct

labour overhead cost. Hence, the overhead cost of Kona is calculated by multiplying

the direct labour with the direct labour per overhead (0.50 x 5.73 = $2.8625). In the

similar process the overall overhead cost of Malaysian Coffee is calculated by using

0.60 x 5.73 = $3.4350. Therefore, after calculating the overhead cost relevant total

cost can be detected for each of the production process by adding the direct cost

and direct labour (Jiang, Ferreira and Gonzalez 2017). Thus, the total cost for Kona

Coffee is calculated at $5.7625, whereas Malaysian Coffee costs $6.6350. After

detecting the total cost for the product relevant mark-up percentage is used for

detecting the level of selling price for each product. The analysis has indicated that

the SP of Kona Coffee is at the levels of $7.4913, while Malaysian Coffee selling

price is at $8.6255. These calculations have been derived by using the traditional

costing system.

2) Utilising the method of activity-based costing for deriving the prices of Kona

Coffee and Malaysian coffee:

Particulars Unit cost

Purchasing 500.00

Material handling 700.00

Quality control 125.00

Roasting 10.00

Blending 10.00

Packaging 20.00

Cost allocation

(Qty)

Cost allocation

(per kg)

Activity

Cost allocation

rate Kona

Malaysi

an Kona

Malaysia

n

Purchasing

500.00 4.00 4.00 $2,000.0

0

$2,000.0

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4INTRODUCTION TO MANAGEMENT ACCOUNTING

Material handling

700.00 36.00 100.00 $25,200.

00

$70,000.

00

Quality control

125.00 4.00 10.00 $500.00 $1,250.0

0

Roasting

10.00 30.00

1,500.0

0

$300.00 $15,000.

00

Blending

10.00 15.00 750.00 $150.00 $7,500.0

0

Packaging

20.00 4.00 200.00 $80.00 $4,000.0

0

Total

$28,230.

00

$99,750.

00

Kilograms

$2,000.0

0

$100,000

.00

Cost per Kg

$14.115

0

$0.9975

Product cost Kona

Malaysi

an

Direct material $2.4000 $2.6000

Direct labour $0.5000 $0.6000

Overhead cost per

product

$14.1150 $0.9975

Product cost $17.0150 $4.1975

The calculations are mainly suggesting the level of pricing for both Kona and

Malaysian Coffee product under activity-based costing method. The values in the

above table have been calculated by using the ABC method by using different cost

pools and activities for deriving the prices that is associated with the production

process of both Kona and Malaysian Coffee. The per unit cost for all the activities

have been calculated, which is the cost pool that is used for assigning specific cost

to each product and detect the actual value of the product. Hence, after using the per

unit cost for each of the overhead activity the overall tables have been created for

assigning the cost of activity with the production units that is been conducted by the

company. The cost allocation for each of the activity is mainly based on production

units, which has been used for calculating the appropriate levels of values that could

Material handling

700.00 36.00 100.00 $25,200.

00

$70,000.

00

Quality control

125.00 4.00 10.00 $500.00 $1,250.0

0

Roasting

10.00 30.00

1,500.0

0

$300.00 $15,000.

00

Blending

10.00 15.00 750.00 $150.00 $7,500.0

0

Packaging

20.00 4.00 200.00 $80.00 $4,000.0

0

Total

$28,230.

00

$99,750.

00

Kilograms

$2,000.0

0

$100,000

.00

Cost per Kg

$14.115

0

$0.9975

Product cost Kona

Malaysi

an

Direct material $2.4000 $2.6000

Direct labour $0.5000 $0.6000

Overhead cost per

product

$14.1150 $0.9975

Product cost $17.0150 $4.1975

The calculations are mainly suggesting the level of pricing for both Kona and

Malaysian Coffee product under activity-based costing method. The values in the

above table have been calculated by using the ABC method by using different cost

pools and activities for deriving the prices that is associated with the production

process of both Kona and Malaysian Coffee. The per unit cost for all the activities

have been calculated, which is the cost pool that is used for assigning specific cost

to each product and detect the actual value of the product. Hence, after using the per

unit cost for each of the overhead activity the overall tables have been created for

assigning the cost of activity with the production units that is been conducted by the

company. The cost allocation for each of the activity is mainly based on production

units, which has been used for calculating the appropriate levels of values that could

5INTRODUCTION TO MANAGEMENT ACCOUNTING

be multiplied with the production units to derive the cost for the product ( Bichou

2015).

Therefore, from the calculations of ABC method, it is detected that the

overhead cost for Kona Coffee is at the levels of $14.1150, which would increase

total cost for the product at the levels of $17.0150 from 5.7625 derived in Traditional

Costing Method (TCM). Thus, the cost for Malaysian Coffee has mainly declined to

the levels of $4.1975, which was calculated at the levels of $8.6255 under TCM.

Hence, ABC method could be understood, as one of the effective measures that

could be used by companies for adequately detecting the expenses for producing a

particular product (Shepherd 2015).

3a) Conduiting a comparative analysis on the results, while providing specific

clarification on the difference between traditional costing system and Activity

based costing system:

The calculations that have been conducted for detecting the costing

conditions for Kona and Malaysian Coffee can be analysed on the basis of

comparative evaluation. This comparative analysis is mainly conducted on traditional

costing system and Activity based costing system. From the relevant analysis of the

calculations, it has been detected that both ABC and TCM has two different costing

mechanism, which provides two alternative costing conditions that the company

would be use to determine their selling price that suit their competitive needs. Rezaei

et al. (2016) indicated that with use of costing calculations, companies are able to

segregate different activities in their production process, which is essential for

understanding the contribution of each action. Hence, detection of the costing

be multiplied with the production units to derive the cost for the product ( Bichou

2015).

Therefore, from the calculations of ABC method, it is detected that the

overhead cost for Kona Coffee is at the levels of $14.1150, which would increase

total cost for the product at the levels of $17.0150 from 5.7625 derived in Traditional

Costing Method (TCM). Thus, the cost for Malaysian Coffee has mainly declined to

the levels of $4.1975, which was calculated at the levels of $8.6255 under TCM.

Hence, ABC method could be understood, as one of the effective measures that

could be used by companies for adequately detecting the expenses for producing a

particular product (Shepherd 2015).

3a) Conduiting a comparative analysis on the results, while providing specific

clarification on the difference between traditional costing system and Activity

based costing system:

The calculations that have been conducted for detecting the costing

conditions for Kona and Malaysian Coffee can be analysed on the basis of

comparative evaluation. This comparative analysis is mainly conducted on traditional

costing system and Activity based costing system. From the relevant analysis of the

calculations, it has been detected that both ABC and TCM has two different costing

mechanism, which provides two alternative costing conditions that the company

would be use to determine their selling price that suit their competitive needs. Rezaei

et al. (2016) indicated that with use of costing calculations, companies are able to

segregate different activities in their production process, which is essential for

understanding the contribution of each action. Hence, detection of the costing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6INTRODUCTION TO MANAGEMENT ACCOUNTING

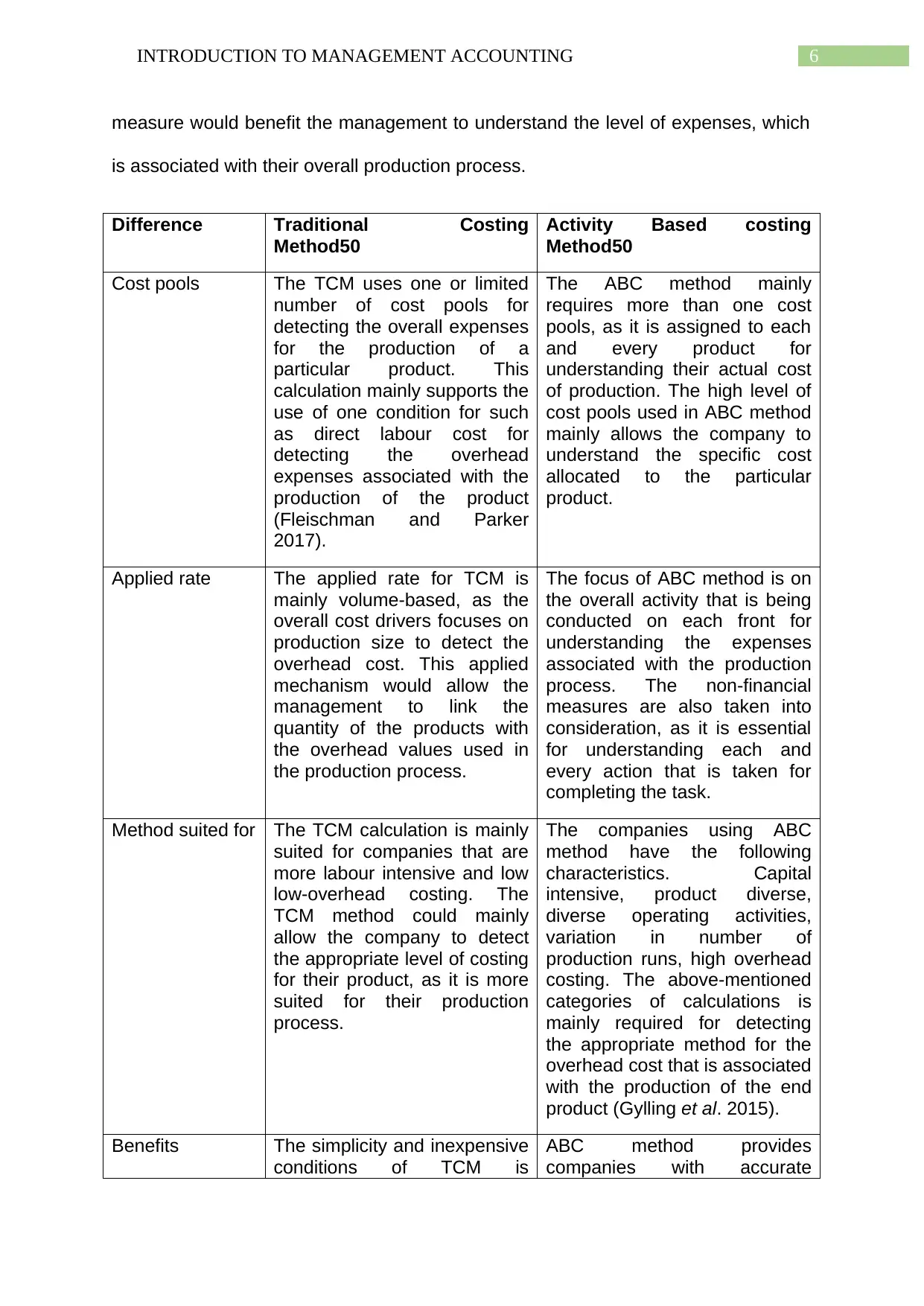

measure would benefit the management to understand the level of expenses, which

is associated with their overall production process.

Difference Traditional Costing

Method50

Activity Based costing

Method50

Cost pools The TCM uses one or limited

number of cost pools for

detecting the overall expenses

for the production of a

particular product. This

calculation mainly supports the

use of one condition for such

as direct labour cost for

detecting the overhead

expenses associated with the

production of the product

(Fleischman and Parker

2017).

The ABC method mainly

requires more than one cost

pools, as it is assigned to each

and every product for

understanding their actual cost

of production. The high level of

cost pools used in ABC method

mainly allows the company to

understand the specific cost

allocated to the particular

product.

Applied rate The applied rate for TCM is

mainly volume-based, as the

overall cost drivers focuses on

production size to detect the

overhead cost. This applied

mechanism would allow the

management to link the

quantity of the products with

the overhead values used in

the production process.

The focus of ABC method is on

the overall activity that is being

conducted on each front for

understanding the expenses

associated with the production

process. The non-financial

measures are also taken into

consideration, as it is essential

for understanding each and

every action that is taken for

completing the task.

Method suited for The TCM calculation is mainly

suited for companies that are

more labour intensive and low

low-overhead costing. The

TCM method could mainly

allow the company to detect

the appropriate level of costing

for their product, as it is more

suited for their production

process.

The companies using ABC

method have the following

characteristics. Capital

intensive, product diverse,

diverse operating activities,

variation in number of

production runs, high overhead

costing. The above-mentioned

categories of calculations is

mainly required for detecting

the appropriate method for the

overhead cost that is associated

with the production of the end

product (Gylling et al. 2015).

Benefits The simplicity and inexpensive

conditions of TCM is

ABC method provides

companies with accurate

measure would benefit the management to understand the level of expenses, which

is associated with their overall production process.

Difference Traditional Costing

Method50

Activity Based costing

Method50

Cost pools The TCM uses one or limited

number of cost pools for

detecting the overall expenses

for the production of a

particular product. This

calculation mainly supports the

use of one condition for such

as direct labour cost for

detecting the overhead

expenses associated with the

production of the product

(Fleischman and Parker

2017).

The ABC method mainly

requires more than one cost

pools, as it is assigned to each

and every product for

understanding their actual cost

of production. The high level of

cost pools used in ABC method

mainly allows the company to

understand the specific cost

allocated to the particular

product.

Applied rate The applied rate for TCM is

mainly volume-based, as the

overall cost drivers focuses on

production size to detect the

overhead cost. This applied

mechanism would allow the

management to link the

quantity of the products with

the overhead values used in

the production process.

The focus of ABC method is on

the overall activity that is being

conducted on each front for

understanding the expenses

associated with the production

process. The non-financial

measures are also taken into

consideration, as it is essential

for understanding each and

every action that is taken for

completing the task.

Method suited for The TCM calculation is mainly

suited for companies that are

more labour intensive and low

low-overhead costing. The

TCM method could mainly

allow the company to detect

the appropriate level of costing

for their product, as it is more

suited for their production

process.

The companies using ABC

method have the following

characteristics. Capital

intensive, product diverse,

diverse operating activities,

variation in number of

production runs, high overhead

costing. The above-mentioned

categories of calculations is

mainly required for detecting

the appropriate method for the

overhead cost that is associated

with the production of the end

product (Gylling et al. 2015).

Benefits The simplicity and inexpensive

conditions of TCM is

ABC method provides

companies with accurate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INTRODUCTION TO MANAGEMENT ACCOUNTING

considered as one of the

benefits for the organisation.

The companies using the TCM

method could determine the

actual cost associated with the

production process with ease,

as it does not have complex

calculations for deriving the

actual expenses for the

product.

product costing, and possible

elimination of non-value added

activities. This benefit directly

allows the organisation to

determine the appropriate level

of expenses that is associated

with the production process.

moreover, companies utilising

the method is able to

understanding the actual cost

that is associated with the

products.

Cost assignment The allocation of TCM is

relevantly based on overhead

cost, which is linked with the

department first and then with

the end products. The

calculations would mainly

enable the company to

understand the level of cost

that is directly based on the

overhead cost.

The cost assigning of ABC is

directly linked with the cost

pools, after which the product or

services are directly associated

with the expenses. The

company using the ABC

method would require a specific

cost pool for adjusting the total

overhead cost with their

expenses and determining the

accurate level of cost

associated with the product

process.

Focus The TCM is responsible for

focusing on managing the

costs of functional

departments or responsibilities

centres. Therefore, it could be

stated that with the

implementation of TCM

companies are able determine

the cost features that is

associated with the actual

expenses of the organisation

(Christopher 2016).

The ABC method focuses on

managing processes and

activities, which help in solving

the cross functional problems of

the production process. The

method would ensure that the

organisation is able to

understanding all the relevant

cost associated with their

production process even if they

are complicated in nature.

3b) Providing appropriate recommendation for the overall pricing structure for

the products:

Particulars Kona Malaysian

Total product cost under ABC method

$17.015

0 $4.1975

Total product cost under TCM $5.7625 $6.6350

considered as one of the

benefits for the organisation.

The companies using the TCM

method could determine the

actual cost associated with the

production process with ease,

as it does not have complex

calculations for deriving the

actual expenses for the

product.

product costing, and possible

elimination of non-value added

activities. This benefit directly

allows the organisation to

determine the appropriate level

of expenses that is associated

with the production process.

moreover, companies utilising

the method is able to

understanding the actual cost

that is associated with the

products.

Cost assignment The allocation of TCM is

relevantly based on overhead

cost, which is linked with the

department first and then with

the end products. The

calculations would mainly

enable the company to

understand the level of cost

that is directly based on the

overhead cost.

The cost assigning of ABC is

directly linked with the cost

pools, after which the product or

services are directly associated

with the expenses. The

company using the ABC

method would require a specific

cost pool for adjusting the total

overhead cost with their

expenses and determining the

accurate level of cost

associated with the product

process.

Focus The TCM is responsible for

focusing on managing the

costs of functional

departments or responsibilities

centres. Therefore, it could be

stated that with the

implementation of TCM

companies are able determine

the cost features that is

associated with the actual

expenses of the organisation

(Christopher 2016).

The ABC method focuses on

managing processes and

activities, which help in solving

the cross functional problems of

the production process. The

method would ensure that the

organisation is able to

understanding all the relevant

cost associated with their

production process even if they

are complicated in nature.

3b) Providing appropriate recommendation for the overall pricing structure for

the products:

Particulars Kona Malaysian

Total product cost under ABC method

$17.015

0 $4.1975

Total product cost under TCM $5.7625 $6.6350

8INTRODUCTION TO MANAGEMENT ACCOUNTING

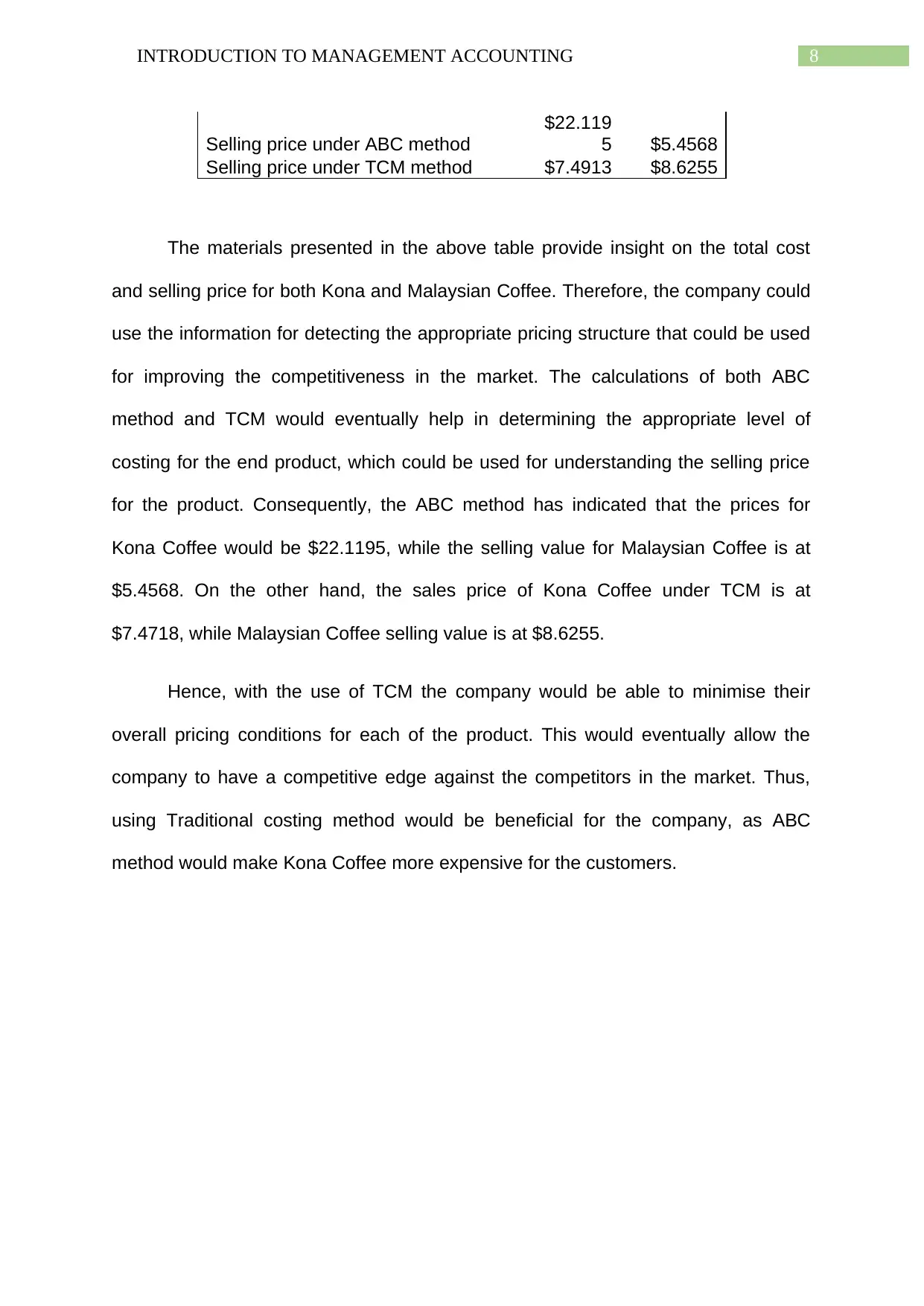

Selling price under ABC method

$22.119

5 $5.4568

Selling price under TCM method $7.4913 $8.6255

The materials presented in the above table provide insight on the total cost

and selling price for both Kona and Malaysian Coffee. Therefore, the company could

use the information for detecting the appropriate pricing structure that could be used

for improving the competitiveness in the market. The calculations of both ABC

method and TCM would eventually help in determining the appropriate level of

costing for the end product, which could be used for understanding the selling price

for the product. Consequently, the ABC method has indicated that the prices for

Kona Coffee would be $22.1195, while the selling value for Malaysian Coffee is at

$5.4568. On the other hand, the sales price of Kona Coffee under TCM is at

$7.4718, while Malaysian Coffee selling value is at $8.6255.

Hence, with the use of TCM the company would be able to minimise their

overall pricing conditions for each of the product. This would eventually allow the

company to have a competitive edge against the competitors in the market. Thus,

using Traditional costing method would be beneficial for the company, as ABC

method would make Kona Coffee more expensive for the customers.

Selling price under ABC method

$22.119

5 $5.4568

Selling price under TCM method $7.4913 $8.6255

The materials presented in the above table provide insight on the total cost

and selling price for both Kona and Malaysian Coffee. Therefore, the company could

use the information for detecting the appropriate pricing structure that could be used

for improving the competitiveness in the market. The calculations of both ABC

method and TCM would eventually help in determining the appropriate level of

costing for the end product, which could be used for understanding the selling price

for the product. Consequently, the ABC method has indicated that the prices for

Kona Coffee would be $22.1195, while the selling value for Malaysian Coffee is at

$5.4568. On the other hand, the sales price of Kona Coffee under TCM is at

$7.4718, while Malaysian Coffee selling value is at $8.6255.

Hence, with the use of TCM the company would be able to minimise their

overall pricing conditions for each of the product. This would eventually allow the

company to have a competitive edge against the competitors in the market. Thus,

using Traditional costing method would be beneficial for the company, as ABC

method would make Kona Coffee more expensive for the customers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9INTRODUCTION TO MANAGEMENT ACCOUNTING

References:

Bichou, K., 2015. The ISPS code and the cost of port compliance: an initial logistics

and supply chain framework for port security assessment and management. In Port

Management (pp. 109-137). Palgrave Macmillan, London.

Christopher, M., 2016. Logistics & supply chain management. Pearson UK.

Cooper, R., 2017. Target costing and value engineering. Routledge.

Fleischman, R.K. and Parker, L.D., 2017. What is Past is Prologue: Cost Accounting

in the British Industrial Revolution, 1760-1850. Routledge.

Gylling, M., Heikkilä, J., Jussila, K. and Saarinen, M., 2015. Making decisions on

offshore outsourcing and backshoring: A case study in the bicycle

industry. International Journal of Production Economics, 162, pp.92-100.

Jiang, S., Ferreira, J. and Gonzalez, M.C., 2017. Activity-based human mobility

patterns inferred from mobile phone data: A case study of Singapore. IEEE

Transactions on Big Data, 3(2), pp.208-219.

Rezaei, J., Nispeling, T., Sarkis, J. and Tavasszy, L., 2016. A supplier selection life

cycle approach integrating traditional and environmental criteria using the best worst

method. Journal of Cleaner Production, 135, pp.577-588.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting:

issues, concepts and practice. Routledge.

Shepherd, D.A., 2015. Party On! A call for entrepreneurship research that is more

interactive, activity based, cognitively hot, compassionate, and prosocial. Journal of

Business Venturing, 30(4), pp.489-507.

References:

Bichou, K., 2015. The ISPS code and the cost of port compliance: an initial logistics

and supply chain framework for port security assessment and management. In Port

Management (pp. 109-137). Palgrave Macmillan, London.

Christopher, M., 2016. Logistics & supply chain management. Pearson UK.

Cooper, R., 2017. Target costing and value engineering. Routledge.

Fleischman, R.K. and Parker, L.D., 2017. What is Past is Prologue: Cost Accounting

in the British Industrial Revolution, 1760-1850. Routledge.

Gylling, M., Heikkilä, J., Jussila, K. and Saarinen, M., 2015. Making decisions on

offshore outsourcing and backshoring: A case study in the bicycle

industry. International Journal of Production Economics, 162, pp.92-100.

Jiang, S., Ferreira, J. and Gonzalez, M.C., 2017. Activity-based human mobility

patterns inferred from mobile phone data: A case study of Singapore. IEEE

Transactions on Big Data, 3(2), pp.208-219.

Rezaei, J., Nispeling, T., Sarkis, J. and Tavasszy, L., 2016. A supplier selection life

cycle approach integrating traditional and environmental criteria using the best worst

method. Journal of Cleaner Production, 135, pp.577-588.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting:

issues, concepts and practice. Routledge.

Shepherd, D.A., 2015. Party On! A call for entrepreneurship research that is more

interactive, activity based, cognitively hot, compassionate, and prosocial. Journal of

Business Venturing, 30(4), pp.489-507.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.