Analysis of Costing Methods and Selling Price Determination

VerifiedAdded on 2022/08/20

|8

|1515

|24

Homework Assignment

AI Summary

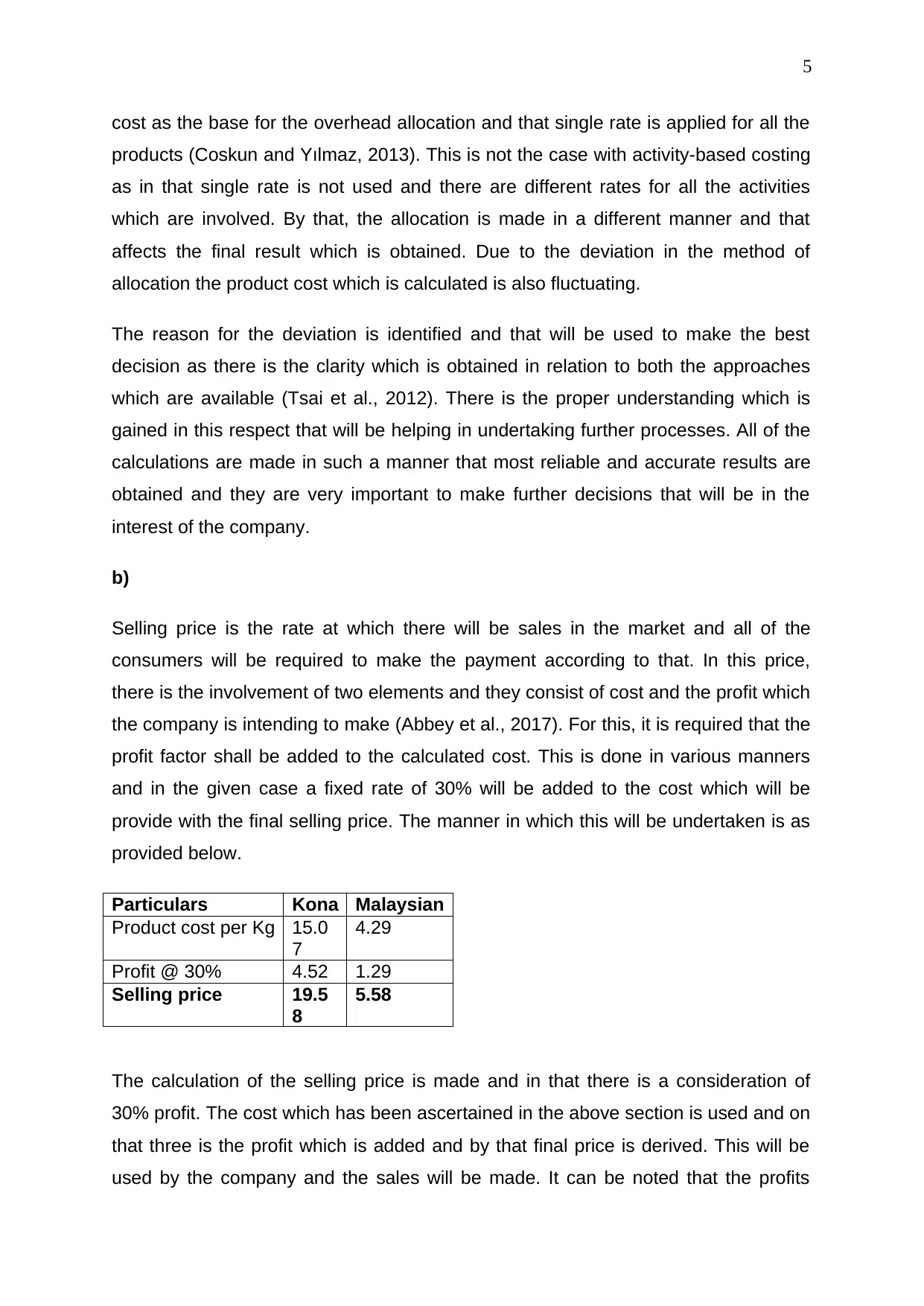

This assignment delves into the principles of management accounting, focusing on cost ascertainment and pricing strategies. It begins by introducing activity-based costing (ABC) as a superior method compared to traditional costing, detailing the steps involved, including identifying activities, cost drivers, and calculating cost per driver. The assignment then calculates product costs for Kona and Malaysian coffee using ABC. A comparison is made between traditional costing and ABC, highlighting the deviations in product costs and the reasons behind them. The assignment concludes by determining the selling price for each coffee type, incorporating a 30% profit margin, and emphasizing the importance of ABC for informed management decisions. References to relevant academic sources are also provided.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.