Open Polytechnic 71202 Management Accounting Assignment 1 Solution

VerifiedAdded on 2023/04/23

|19

|3305

|132

Homework Assignment

AI Summary

This document presents a comprehensive solution to Management Accounting Assignment 1, covering a range of topics. The solution begins with a detailed analysis of short answer questions, including calculations related to schedules of goods manufactured, cost of job, equivalent units, allocation of costs, and Economic Order Quantity (EOQ). The assignment then delves into activity-based costing (ABC), requiring the preparation of profit statements, allocation of overhead costs, calculation of activity rates, and a comparison of traditional and ABC methods. Furthermore, the solution includes budgeting exercises, such as sales, production, direct material purchases, and cash budgets. Finally, the assignment concludes with a standard costing section, incorporating variance analysis for direct materials, direct labor, and overheads. The solution provides all necessary calculations and interpretations to address the assignment's requirements effectively.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

QUESTION 1...................................................................................................................................4

A): Schedule of goods manufactured for the period ending 31st march 2018.............................6

B): Complete the table.................................................................................................................7

C) (i) Calculation of total cost of job X10...................................................................................7

(ii) Undervaluation and over-valuation........................................................................................8

D): (i) Schedule of Equivalent unit..............................................................................................8

(ii): Total cost of finished goods..................................................................................................8

(iii) Total cost of finished good for the month of November......................................................8

(e): Allocation of cost to support department to manufacturing line 1 and 2.............................9

(f):(i) Calculation for EOQ..........................................................................................................9

(ii): Interpretation.......................................................................................................................10

(g): Allocate the joint manufacturing cost.................................................................................10

QUESTION 2.................................................................................................................................10

(a) Preparation of profit statement...........................................................................................10

(b): Allocation of the overhead cost to each activity.................................................................11

(c): Activity rate for each activity cost pool..............................................................................11

(d): Calculate the total overhead cost.........................................................................................12

(e): Preparing a profit statement................................................................................................13

(f): Indication of the activity based costing information...........................................................13

QUESTION 3.................................................................................................................................13

(a) (I) Sales Budget for the period ending December 2019.......................................................13

(a) (ii) Production Budget for the period ending December 2019.............................................14

(a) (iii) Direct material purchases Budget for the period ending December 2019.....................14

(b): Cash Budget for the period ending December 2019...........................................................16

QUESTION 4.................................................................................................................................16

(a): Use of Historic data.............................................................................................................16

(b): Difference............................................................................................................................17

(c) (i): Direct material variance..................................................................................................17

(ii): Calculation for direct labour rate variance..........................................................................17

Table of Contents.............................................................................................................................2

QUESTION 1...................................................................................................................................4

A): Schedule of goods manufactured for the period ending 31st march 2018.............................6

B): Complete the table.................................................................................................................7

C) (i) Calculation of total cost of job X10...................................................................................7

(ii) Undervaluation and over-valuation........................................................................................8

D): (i) Schedule of Equivalent unit..............................................................................................8

(ii): Total cost of finished goods..................................................................................................8

(iii) Total cost of finished good for the month of November......................................................8

(e): Allocation of cost to support department to manufacturing line 1 and 2.............................9

(f):(i) Calculation for EOQ..........................................................................................................9

(ii): Interpretation.......................................................................................................................10

(g): Allocate the joint manufacturing cost.................................................................................10

QUESTION 2.................................................................................................................................10

(a) Preparation of profit statement...........................................................................................10

(b): Allocation of the overhead cost to each activity.................................................................11

(c): Activity rate for each activity cost pool..............................................................................11

(d): Calculate the total overhead cost.........................................................................................12

(e): Preparing a profit statement................................................................................................13

(f): Indication of the activity based costing information...........................................................13

QUESTION 3.................................................................................................................................13

(a) (I) Sales Budget for the period ending December 2019.......................................................13

(a) (ii) Production Budget for the period ending December 2019.............................................14

(a) (iii) Direct material purchases Budget for the period ending December 2019.....................14

(b): Cash Budget for the period ending December 2019...........................................................16

QUESTION 4.................................................................................................................................16

(a): Use of Historic data.............................................................................................................16

(b): Difference............................................................................................................................17

(c) (i): Direct material variance..................................................................................................17

(ii): Calculation for direct labour rate variance..........................................................................17

(iii): Variable overhead spending...............................................................................................17

(iv): Fixed overhead volume variance.......................................................................................17

REFERENCES..............................................................................................................................19

3

(iv): Fixed overhead volume variance.......................................................................................17

REFERENCES..............................................................................................................................19

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

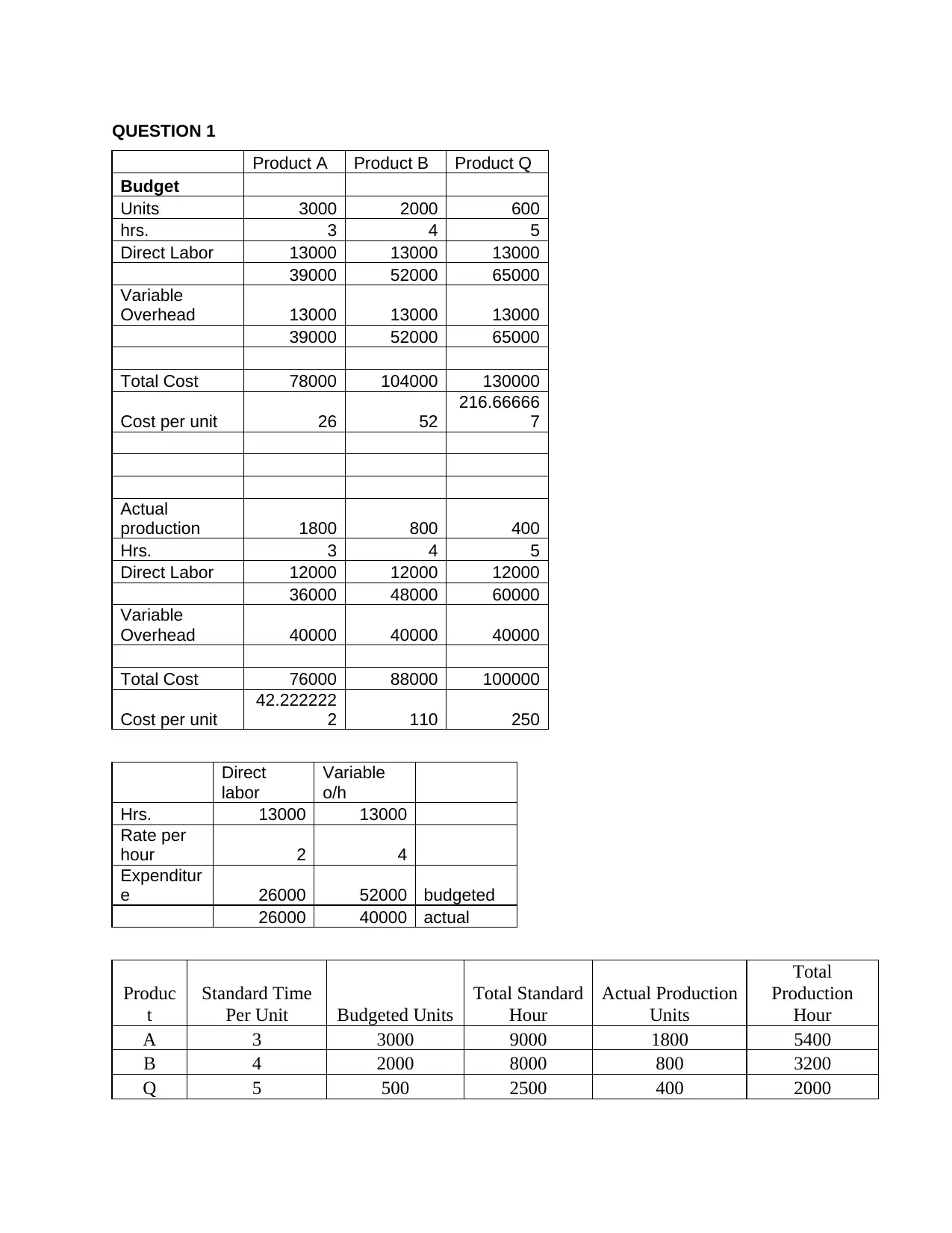

QUESTION 1

Product A Product B Product Q

Budget

Units 3000 2000 600

hrs. 3 4 5

Direct Labor 13000 13000 13000

39000 52000 65000

Variable

Overhead 13000 13000 13000

39000 52000 65000

Total Cost 78000 104000 130000

Cost per unit 26 52

216.66666

7

Actual

production 1800 800 400

Hrs. 3 4 5

Direct Labor 12000 12000 12000

36000 48000 60000

Variable

Overhead 40000 40000 40000

Total Cost 76000 88000 100000

Cost per unit

42.222222

2 110 250

Direct

labor

Variable

o/h

Hrs. 13000 13000

Rate per

hour 2 4

Expenditur

e 26000 52000 budgeted

26000 40000 actual

Produc

t

Standard Time

Per Unit Budgeted Units

Total Standard

Hour

Actual Production

Units

Total

Production

Hour

A 3 3000 9000 1800 5400

B 4 2000 8000 800 3200

Q 5 500 2500 400 2000

Product A Product B Product Q

Budget

Units 3000 2000 600

hrs. 3 4 5

Direct Labor 13000 13000 13000

39000 52000 65000

Variable

Overhead 13000 13000 13000

39000 52000 65000

Total Cost 78000 104000 130000

Cost per unit 26 52

216.66666

7

Actual

production 1800 800 400

Hrs. 3 4 5

Direct Labor 12000 12000 12000

36000 48000 60000

Variable

Overhead 40000 40000 40000

Total Cost 76000 88000 100000

Cost per unit

42.222222

2 110 250

Direct

labor

Variable

o/h

Hrs. 13000 13000

Rate per

hour 2 4

Expenditur

e 26000 52000 budgeted

26000 40000 actual

Produc

t

Standard Time

Per Unit Budgeted Units

Total Standard

Hour

Actual Production

Units

Total

Production

Hour

A 3 3000 9000 1800 5400

B 4 2000 8000 800 3200

Q 5 500 2500 400 2000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

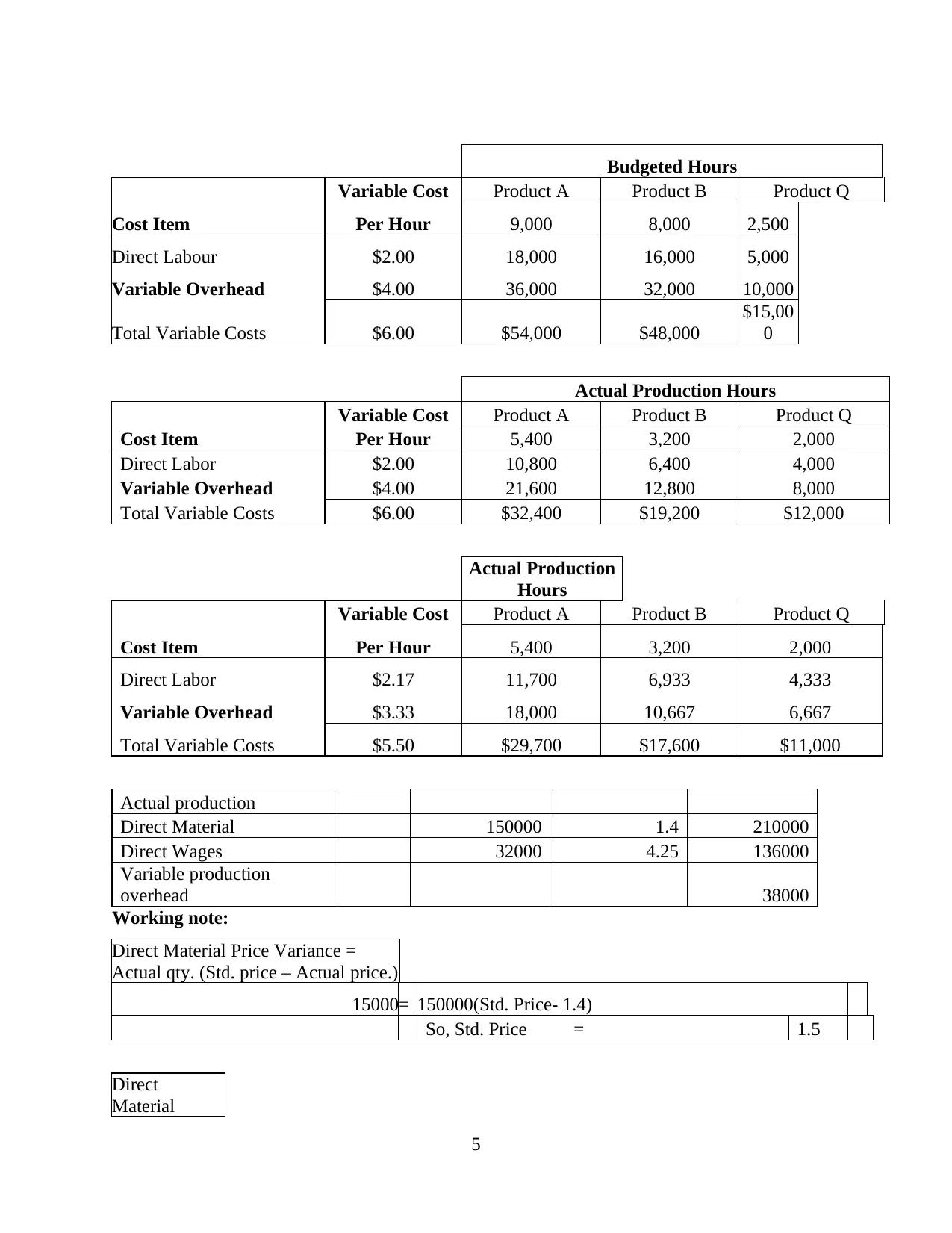

Budgeted Hours

Variable Cost Product A Product B Product Q

Cost Item Per Hour 9,000 8,000 2,500

Direct Labour $2.00 18,000 16,000 5,000

Variable Overhead $4.00 36,000 32,000 10,000

Total Variable Costs $6.00 $54,000 $48,000

$15,00

0

Actual Production Hours

Variable Cost Product A Product B Product Q

Cost Item Per Hour 5,400 3,200 2,000

Direct Labor $2.00 10,800 6,400 4,000

Variable Overhead $4.00 21,600 12,800 8,000

Total Variable Costs $6.00 $32,400 $19,200 $12,000

Actual Production

Hours

Variable Cost Product A Product B Product Q

Cost Item Per Hour 5,400 3,200 2,000

Direct Labor $2.17 11,700 6,933 4,333

Variable Overhead $3.33 18,000 10,667 6,667

Total Variable Costs $5.50 $29,700 $17,600 $11,000

Actual production

Direct Material 150000 1.4 210000

Direct Wages 32000 4.25 136000

Variable production

overhead 38000

Working note:

Direct Material Price Variance =

Actual qty. (Std. price – Actual price.)

15000= 150000(Std. Price- 1.4)

So, Std. Price = 1.5

Direct

Material

5

Variable Cost Product A Product B Product Q

Cost Item Per Hour 9,000 8,000 2,500

Direct Labour $2.00 18,000 16,000 5,000

Variable Overhead $4.00 36,000 32,000 10,000

Total Variable Costs $6.00 $54,000 $48,000

$15,00

0

Actual Production Hours

Variable Cost Product A Product B Product Q

Cost Item Per Hour 5,400 3,200 2,000

Direct Labor $2.00 10,800 6,400 4,000

Variable Overhead $4.00 21,600 12,800 8,000

Total Variable Costs $6.00 $32,400 $19,200 $12,000

Actual Production

Hours

Variable Cost Product A Product B Product Q

Cost Item Per Hour 5,400 3,200 2,000

Direct Labor $2.17 11,700 6,933 4,333

Variable Overhead $3.33 18,000 10,667 6,667

Total Variable Costs $5.50 $29,700 $17,600 $11,000

Actual production

Direct Material 150000 1.4 210000

Direct Wages 32000 4.25 136000

Variable production

overhead 38000

Working note:

Direct Material Price Variance =

Actual qty. (Std. price – Actual price.)

15000= 150000(Std. Price- 1.4)

So, Std. Price = 1.5

Direct

Material

5

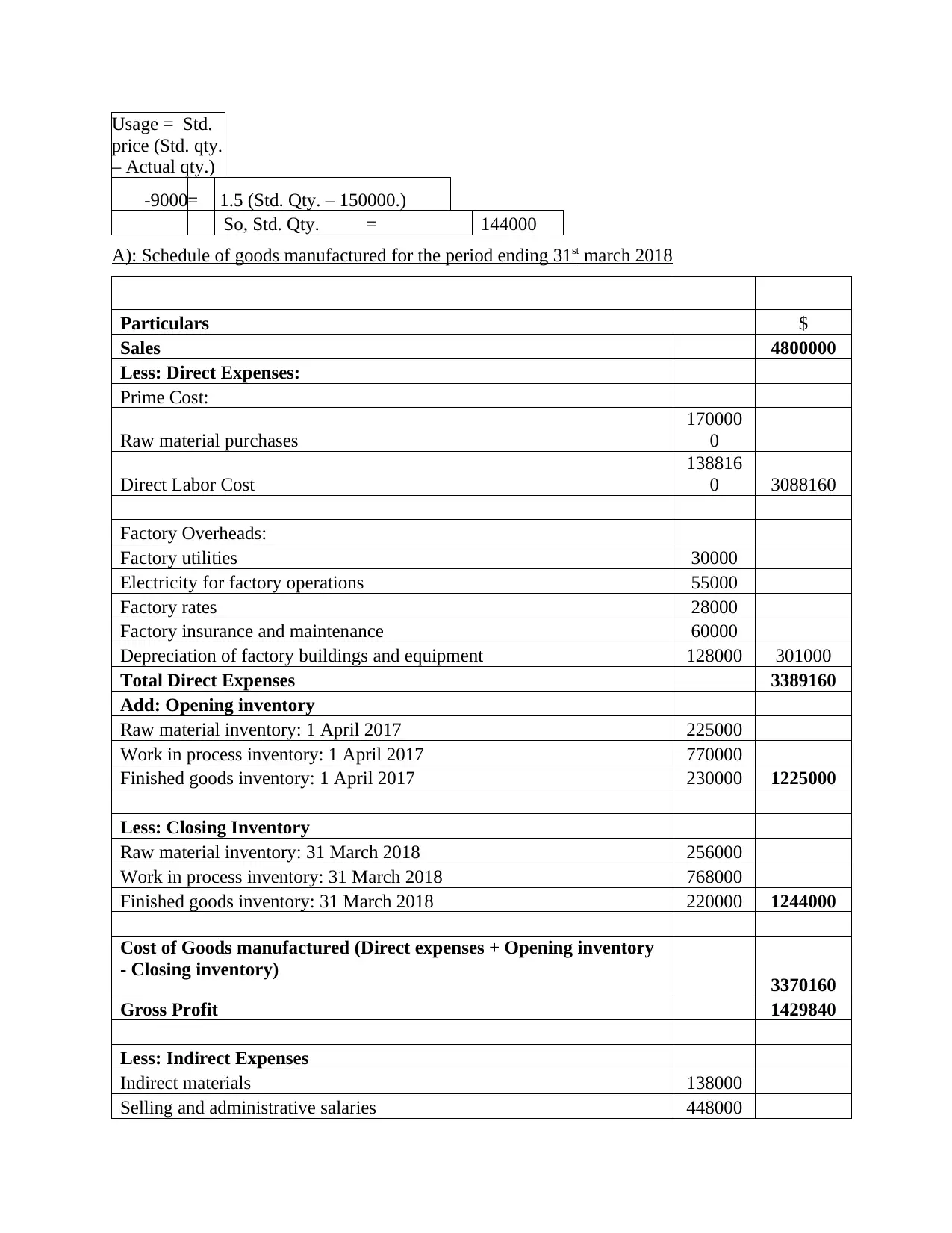

Usage = Std.

price (Std. qty.

– Actual qty.)

-9000= 1.5 (Std. Qty. – 150000.)

So, Std. Qty. = 144000

A): Schedule of goods manufactured for the period ending 31st march 2018

Particulars $

Sales 4800000

Less: Direct Expenses:

Prime Cost:

Raw material purchases

170000

0

Direct Labor Cost

138816

0 3088160

Factory Overheads:

Factory utilities 30000

Electricity for factory operations 55000

Factory rates 28000

Factory insurance and maintenance 60000

Depreciation of factory buildings and equipment 128000 301000

Total Direct Expenses 3389160

Add: Opening inventory

Raw material inventory: 1 April 2017 225000

Work in process inventory: 1 April 2017 770000

Finished goods inventory: 1 April 2017 230000 1225000

Less: Closing Inventory

Raw material inventory: 31 March 2018 256000

Work in process inventory: 31 March 2018 768000

Finished goods inventory: 31 March 2018 220000 1244000

Cost of Goods manufactured (Direct expenses + Opening inventory

- Closing inventory) 3370160

Gross Profit 1429840

Less: Indirect Expenses

Indirect materials 138000

Selling and administrative salaries 448000

price (Std. qty.

– Actual qty.)

-9000= 1.5 (Std. Qty. – 150000.)

So, Std. Qty. = 144000

A): Schedule of goods manufactured for the period ending 31st march 2018

Particulars $

Sales 4800000

Less: Direct Expenses:

Prime Cost:

Raw material purchases

170000

0

Direct Labor Cost

138816

0 3088160

Factory Overheads:

Factory utilities 30000

Electricity for factory operations 55000

Factory rates 28000

Factory insurance and maintenance 60000

Depreciation of factory buildings and equipment 128000 301000

Total Direct Expenses 3389160

Add: Opening inventory

Raw material inventory: 1 April 2017 225000

Work in process inventory: 1 April 2017 770000

Finished goods inventory: 1 April 2017 230000 1225000

Less: Closing Inventory

Raw material inventory: 31 March 2018 256000

Work in process inventory: 31 March 2018 768000

Finished goods inventory: 31 March 2018 220000 1244000

Cost of Goods manufactured (Direct expenses + Opening inventory

- Closing inventory) 3370160

Gross Profit 1429840

Less: Indirect Expenses

Indirect materials 138000

Selling and administrative salaries 448000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Delivery and distribution costs 72000

Advertising costs 40000

Depreciation on administrative buildings and equipment 51000

Electricity for sales and administration offices 27000

Other selling and administration expenses 260000 1036000

Net Profit 393840

B): Complete the table

Units 20000 25000 30000

Total variable cost

120000

0 1500000 1800000

Per unit variable cost 60 60 60

Total fixed cost 800000 800000 800000

Per unit fixed cost 40 32

26.666666

67

Total cost

200000

0 2300000 2600000

Total per unit cost 100 92

86.666666

67

C) (i) Calculation of total cost of job X10

Budgete

d Actual

Total manufacturing overhead cost 1200000

Labour Hours 40000

Prime Cost:

Raw material 140500

Direct Labour Cost 61200

Other manufacturing overhead 48500

Indirect Costs:

Indirect labour Cost 9000

Indirect materials 21500

Total Cost of Job X10 280700

(ii) Undervaluation and over-valuation

Actual manufacturing overheard = 21500+48500+9000=79000

Budgeting manufacturing overhead =1200000/40000*3400=102000

7

Advertising costs 40000

Depreciation on administrative buildings and equipment 51000

Electricity for sales and administration offices 27000

Other selling and administration expenses 260000 1036000

Net Profit 393840

B): Complete the table

Units 20000 25000 30000

Total variable cost

120000

0 1500000 1800000

Per unit variable cost 60 60 60

Total fixed cost 800000 800000 800000

Per unit fixed cost 40 32

26.666666

67

Total cost

200000

0 2300000 2600000

Total per unit cost 100 92

86.666666

67

C) (i) Calculation of total cost of job X10

Budgete

d Actual

Total manufacturing overhead cost 1200000

Labour Hours 40000

Prime Cost:

Raw material 140500

Direct Labour Cost 61200

Other manufacturing overhead 48500

Indirect Costs:

Indirect labour Cost 9000

Indirect materials 21500

Total Cost of Job X10 280700

(ii) Undervaluation and over-valuation

Actual manufacturing overheard = 21500+48500+9000=79000

Budgeting manufacturing overhead =1200000/40000*3400=102000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

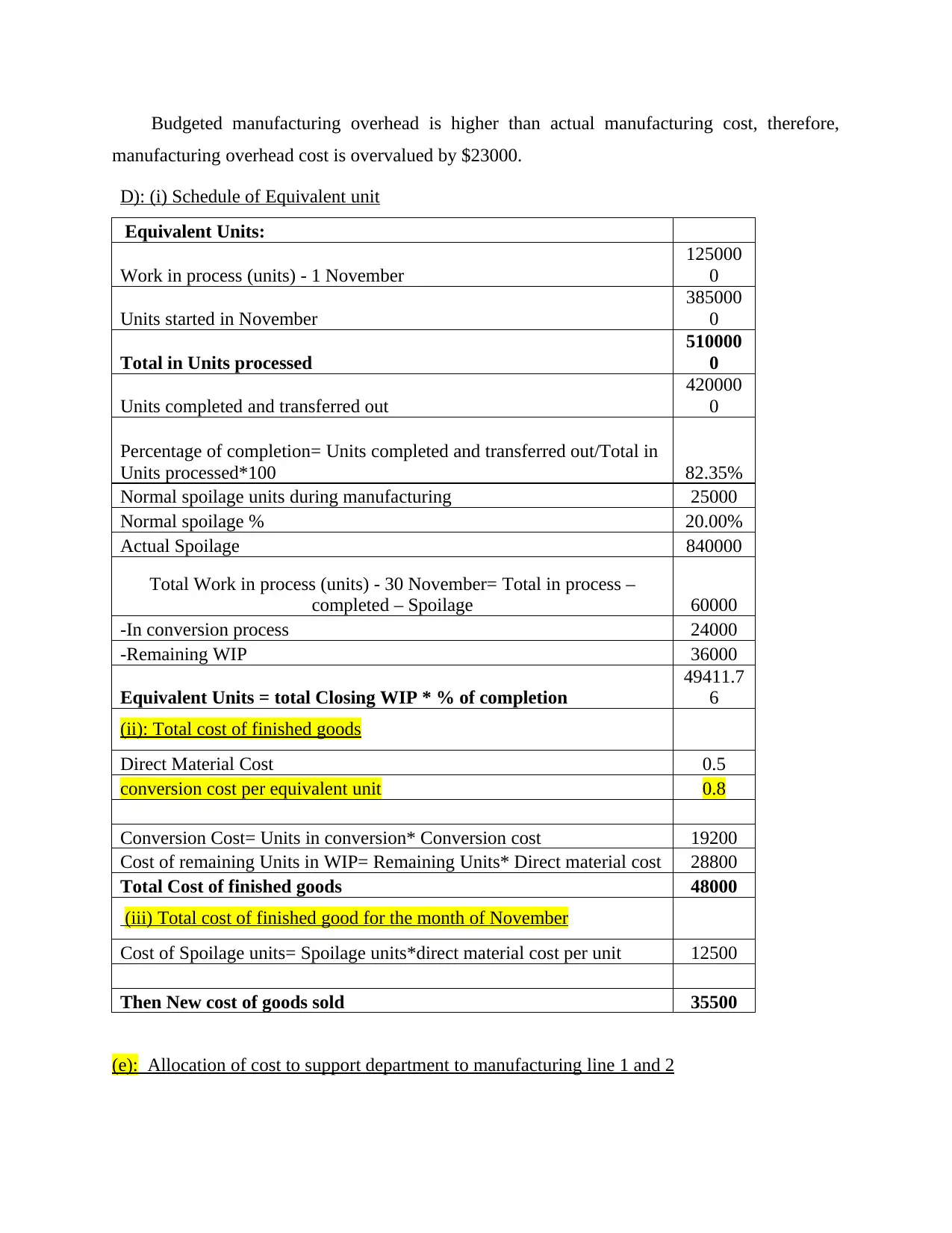

Budgeted manufacturing overhead is higher than actual manufacturing cost, therefore,

manufacturing overhead cost is overvalued by $23000.

D): (i) Schedule of Equivalent unit

Equivalent Units:

Work in process (units) - 1 November

125000

0

Units started in November

385000

0

Total in Units processed

510000

0

Units completed and transferred out

420000

0

Percentage of completion= Units completed and transferred out/Total in

Units processed*100 82.35%

Normal spoilage units during manufacturing 25000

Normal spoilage % 20.00%

Actual Spoilage 840000

Total Work in process (units) - 30 November= Total in process –

completed – Spoilage 60000

-In conversion process 24000

-Remaining WIP 36000

Equivalent Units = total Closing WIP * % of completion

49411.7

6

(ii): Total cost of finished goods

Direct Material Cost 0.5

conversion cost per equivalent unit 0.8

Conversion Cost= Units in conversion* Conversion cost 19200

Cost of remaining Units in WIP= Remaining Units* Direct material cost 28800

Total Cost of finished goods 48000

(iii) Total cost of finished good for the month of November

Cost of Spoilage units= Spoilage units*direct material cost per unit 12500

Then New cost of goods sold 35500

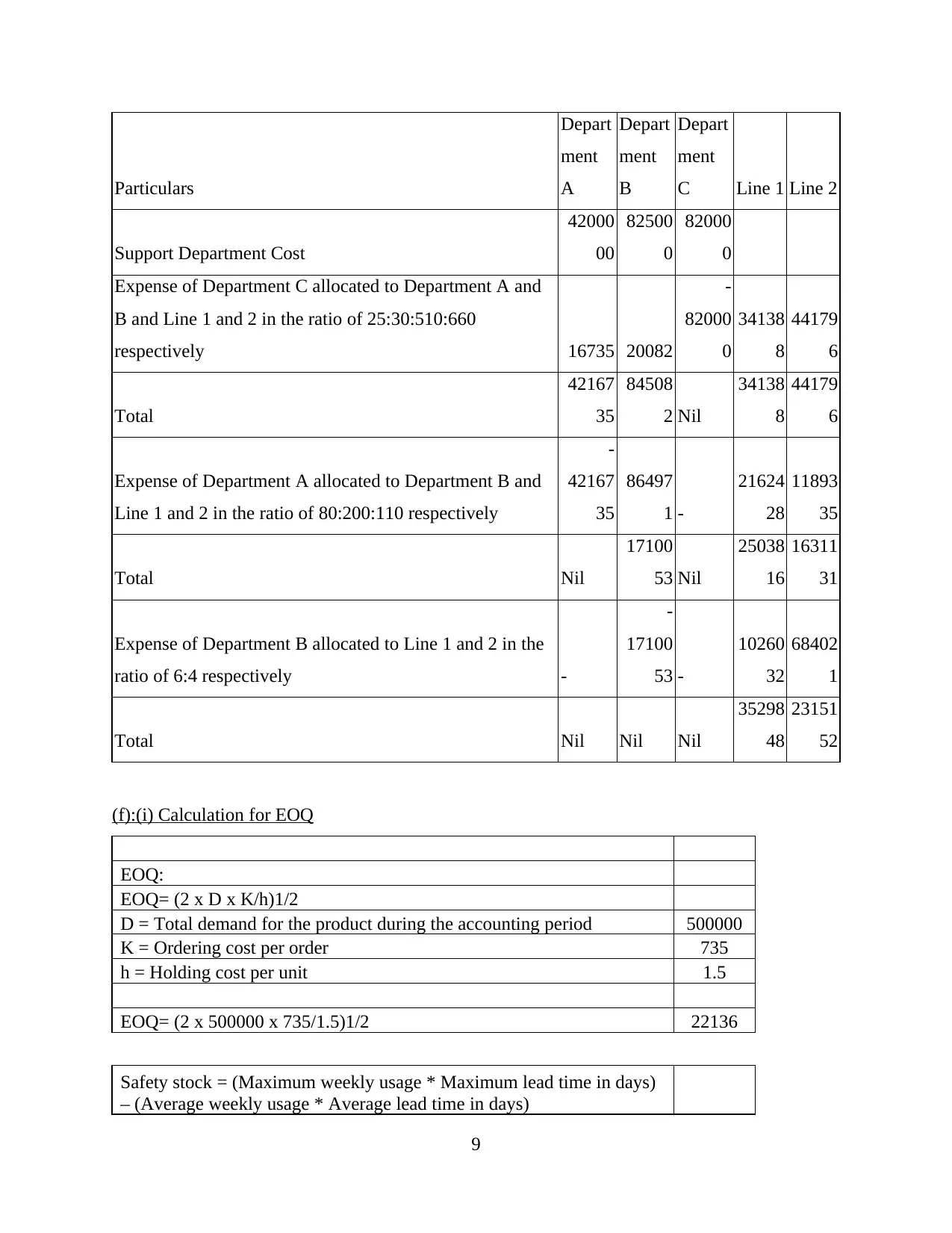

(e): Allocation of cost to support department to manufacturing line 1 and 2

manufacturing overhead cost is overvalued by $23000.

D): (i) Schedule of Equivalent unit

Equivalent Units:

Work in process (units) - 1 November

125000

0

Units started in November

385000

0

Total in Units processed

510000

0

Units completed and transferred out

420000

0

Percentage of completion= Units completed and transferred out/Total in

Units processed*100 82.35%

Normal spoilage units during manufacturing 25000

Normal spoilage % 20.00%

Actual Spoilage 840000

Total Work in process (units) - 30 November= Total in process –

completed – Spoilage 60000

-In conversion process 24000

-Remaining WIP 36000

Equivalent Units = total Closing WIP * % of completion

49411.7

6

(ii): Total cost of finished goods

Direct Material Cost 0.5

conversion cost per equivalent unit 0.8

Conversion Cost= Units in conversion* Conversion cost 19200

Cost of remaining Units in WIP= Remaining Units* Direct material cost 28800

Total Cost of finished goods 48000

(iii) Total cost of finished good for the month of November

Cost of Spoilage units= Spoilage units*direct material cost per unit 12500

Then New cost of goods sold 35500

(e): Allocation of cost to support department to manufacturing line 1 and 2

Particulars

Depart

ment

A

Depart

ment

B

Depart

ment

C Line 1 Line 2

Support Department Cost

42000

00

82500

0

82000

0

Expense of Department C allocated to Department A and

B and Line 1 and 2 in the ratio of 25:30:510:660

respectively 16735 20082

-

82000

0

34138

8

44179

6

Total

42167

35

84508

2 Nil

34138

8

44179

6

Expense of Department A allocated to Department B and

Line 1 and 2 in the ratio of 80:200:110 respectively

-

42167

35

86497

1 -

21624

28

11893

35

Total Nil

17100

53 Nil

25038

16

16311

31

Expense of Department B allocated to Line 1 and 2 in the

ratio of 6:4 respectively -

-

17100

53 -

10260

32

68402

1

Total Nil Nil Nil

35298

48

23151

52

(f):(i) Calculation for EOQ

EOQ:

EOQ= (2 x D x K/h)1/2

D = Total demand for the product during the accounting period 500000

K = Ordering cost per order 735

h = Holding cost per unit 1.5

EOQ= (2 x 500000 x 735/1.5)1/2 22136

Safety stock = (Maximum weekly usage * Maximum lead time in days)

– (Average weekly usage * Average lead time in days)

9

Depart

ment

A

Depart

ment

B

Depart

ment

C Line 1 Line 2

Support Department Cost

42000

00

82500

0

82000

0

Expense of Department C allocated to Department A and

B and Line 1 and 2 in the ratio of 25:30:510:660

respectively 16735 20082

-

82000

0

34138

8

44179

6

Total

42167

35

84508

2 Nil

34138

8

44179

6

Expense of Department A allocated to Department B and

Line 1 and 2 in the ratio of 80:200:110 respectively

-

42167

35

86497

1 -

21624

28

11893

35

Total Nil

17100

53 Nil

25038

16

16311

31

Expense of Department B allocated to Line 1 and 2 in the

ratio of 6:4 respectively -

-

17100

53 -

10260

32

68402

1

Total Nil Nil Nil

35298

48

23151

52

(f):(i) Calculation for EOQ

EOQ:

EOQ= (2 x D x K/h)1/2

D = Total demand for the product during the accounting period 500000

K = Ordering cost per order 735

h = Holding cost per unit 1.5

EOQ= (2 x 500000 x 735/1.5)1/2 22136

Safety stock = (Maximum weekly usage * Maximum lead time in days)

– (Average weekly usage * Average lead time in days)

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

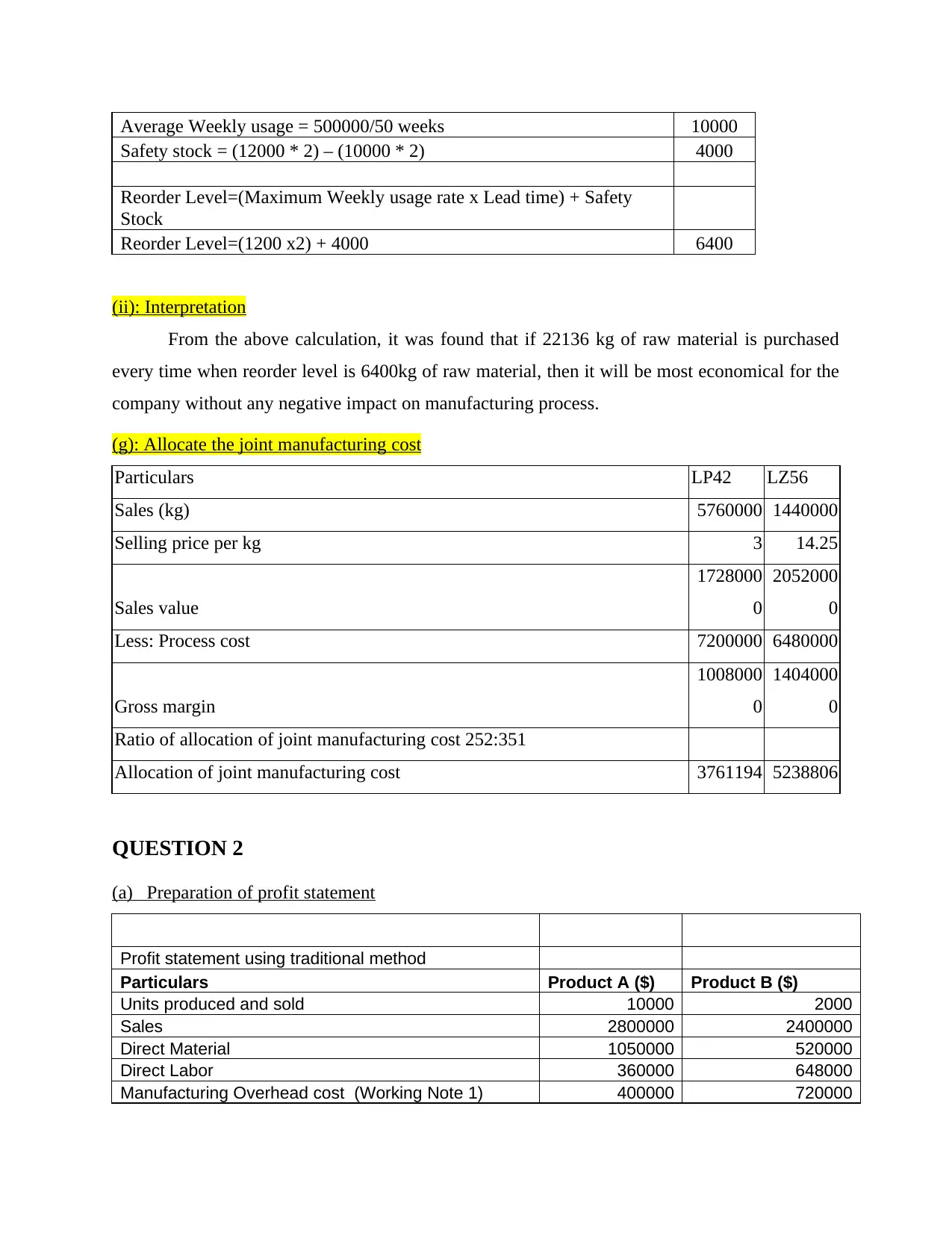

Average Weekly usage = 500000/50 weeks 10000

Safety stock = (12000 * 2) – (10000 * 2) 4000

Reorder Level=(Maximum Weekly usage rate x Lead time) + Safety

Stock

Reorder Level=(1200 x2) + 4000 6400

(ii): Interpretation

From the above calculation, it was found that if 22136 kg of raw material is purchased

every time when reorder level is 6400kg of raw material, then it will be most economical for the

company without any negative impact on manufacturing process.

(g): Allocate the joint manufacturing cost

Particulars LP42 LZ56

Sales (kg) 5760000 1440000

Selling price per kg 3 14.25

Sales value

1728000

0

2052000

0

Less: Process cost 7200000 6480000

Gross margin

1008000

0

1404000

0

Ratio of allocation of joint manufacturing cost 252:351

Allocation of joint manufacturing cost 3761194 5238806

QUESTION 2

(a) Preparation of profit statement

Profit statement using traditional method

Particulars Product A ($) Product B ($)

Units produced and sold 10000 2000

Sales 2800000 2400000

Direct Material 1050000 520000

Direct Labor 360000 648000

Manufacturing Overhead cost (Working Note 1) 400000 720000

Safety stock = (12000 * 2) – (10000 * 2) 4000

Reorder Level=(Maximum Weekly usage rate x Lead time) + Safety

Stock

Reorder Level=(1200 x2) + 4000 6400

(ii): Interpretation

From the above calculation, it was found that if 22136 kg of raw material is purchased

every time when reorder level is 6400kg of raw material, then it will be most economical for the

company without any negative impact on manufacturing process.

(g): Allocate the joint manufacturing cost

Particulars LP42 LZ56

Sales (kg) 5760000 1440000

Selling price per kg 3 14.25

Sales value

1728000

0

2052000

0

Less: Process cost 7200000 6480000

Gross margin

1008000

0

1404000

0

Ratio of allocation of joint manufacturing cost 252:351

Allocation of joint manufacturing cost 3761194 5238806

QUESTION 2

(a) Preparation of profit statement

Profit statement using traditional method

Particulars Product A ($) Product B ($)

Units produced and sold 10000 2000

Sales 2800000 2400000

Direct Material 1050000 520000

Direct Labor 360000 648000

Manufacturing Overhead cost (Working Note 1) 400000 720000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

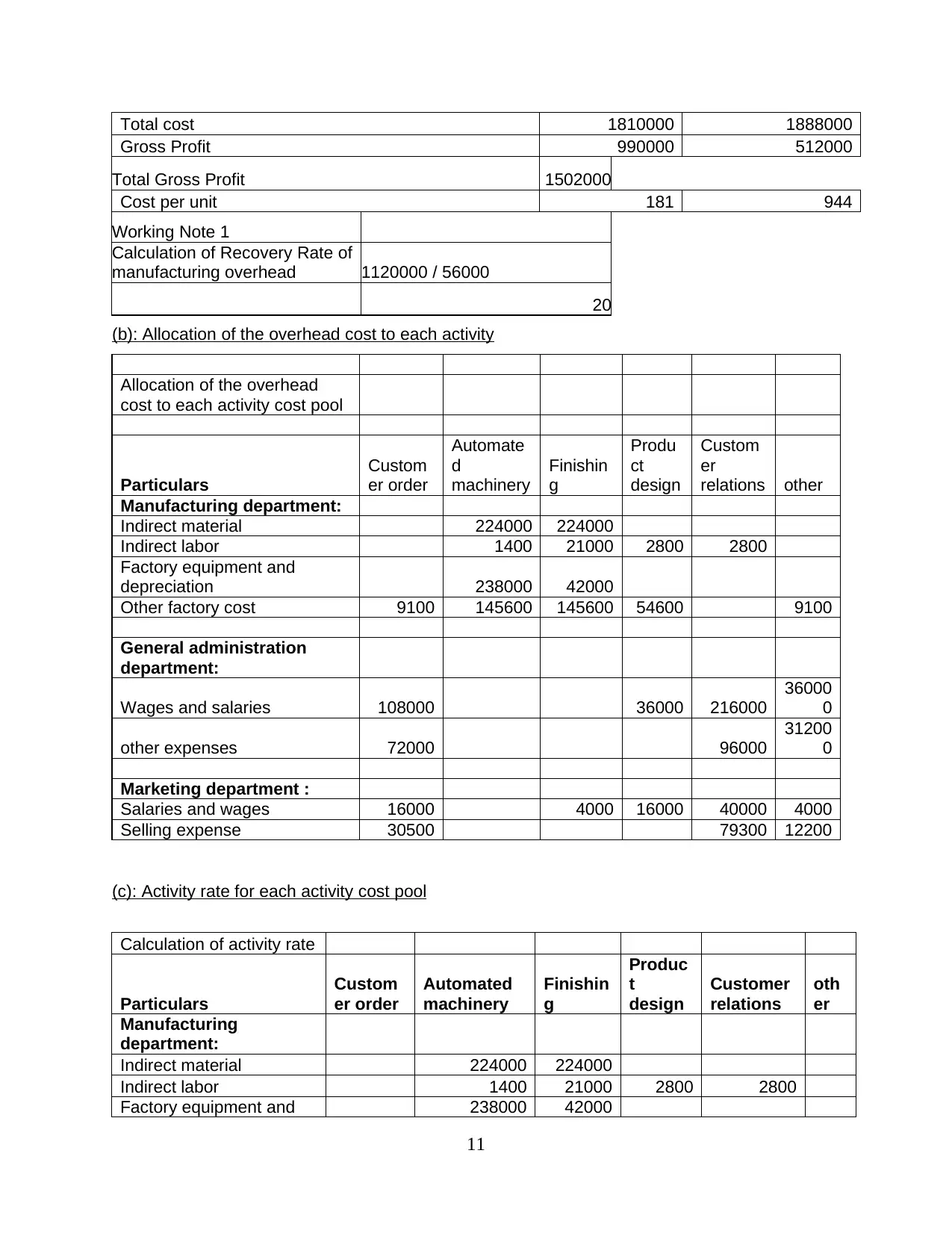

Total cost 1810000 1888000

Gross Profit 990000 512000

Total Gross Profit 1502000

Cost per unit 181 944

Working Note 1

Calculation of Recovery Rate of

manufacturing overhead 1120000 / 56000

20

(b): Allocation of the overhead cost to each activity

Allocation of the overhead

cost to each activity cost pool

Particulars

Custom

er order

Automate

d

machinery

Finishin

g

Produ

ct

design

Custom

er

relations other

Manufacturing department:

Indirect material 224000 224000

Indirect labor 1400 21000 2800 2800

Factory equipment and

depreciation 238000 42000

Other factory cost 9100 145600 145600 54600 9100

General administration

department:

Wages and salaries 108000 36000 216000

36000

0

other expenses 72000 96000

31200

0

Marketing department :

Salaries and wages 16000 4000 16000 40000 4000

Selling expense 30500 79300 12200

(c): Activity rate for each activity cost pool

Calculation of activity rate

Particulars

Custom

er order

Automated

machinery

Finishin

g

Produc

t

design

Customer

relations

oth

er

Manufacturing

department:

Indirect material 224000 224000

Indirect labor 1400 21000 2800 2800

Factory equipment and 238000 42000

11

Gross Profit 990000 512000

Total Gross Profit 1502000

Cost per unit 181 944

Working Note 1

Calculation of Recovery Rate of

manufacturing overhead 1120000 / 56000

20

(b): Allocation of the overhead cost to each activity

Allocation of the overhead

cost to each activity cost pool

Particulars

Custom

er order

Automate

d

machinery

Finishin

g

Produ

ct

design

Custom

er

relations other

Manufacturing department:

Indirect material 224000 224000

Indirect labor 1400 21000 2800 2800

Factory equipment and

depreciation 238000 42000

Other factory cost 9100 145600 145600 54600 9100

General administration

department:

Wages and salaries 108000 36000 216000

36000

0

other expenses 72000 96000

31200

0

Marketing department :

Salaries and wages 16000 4000 16000 40000 4000

Selling expense 30500 79300 12200

(c): Activity rate for each activity cost pool

Calculation of activity rate

Particulars

Custom

er order

Automated

machinery

Finishin

g

Produc

t

design

Customer

relations

oth

er

Manufacturing

department:

Indirect material 224000 224000

Indirect labor 1400 21000 2800 2800

Factory equipment and 238000 42000

11

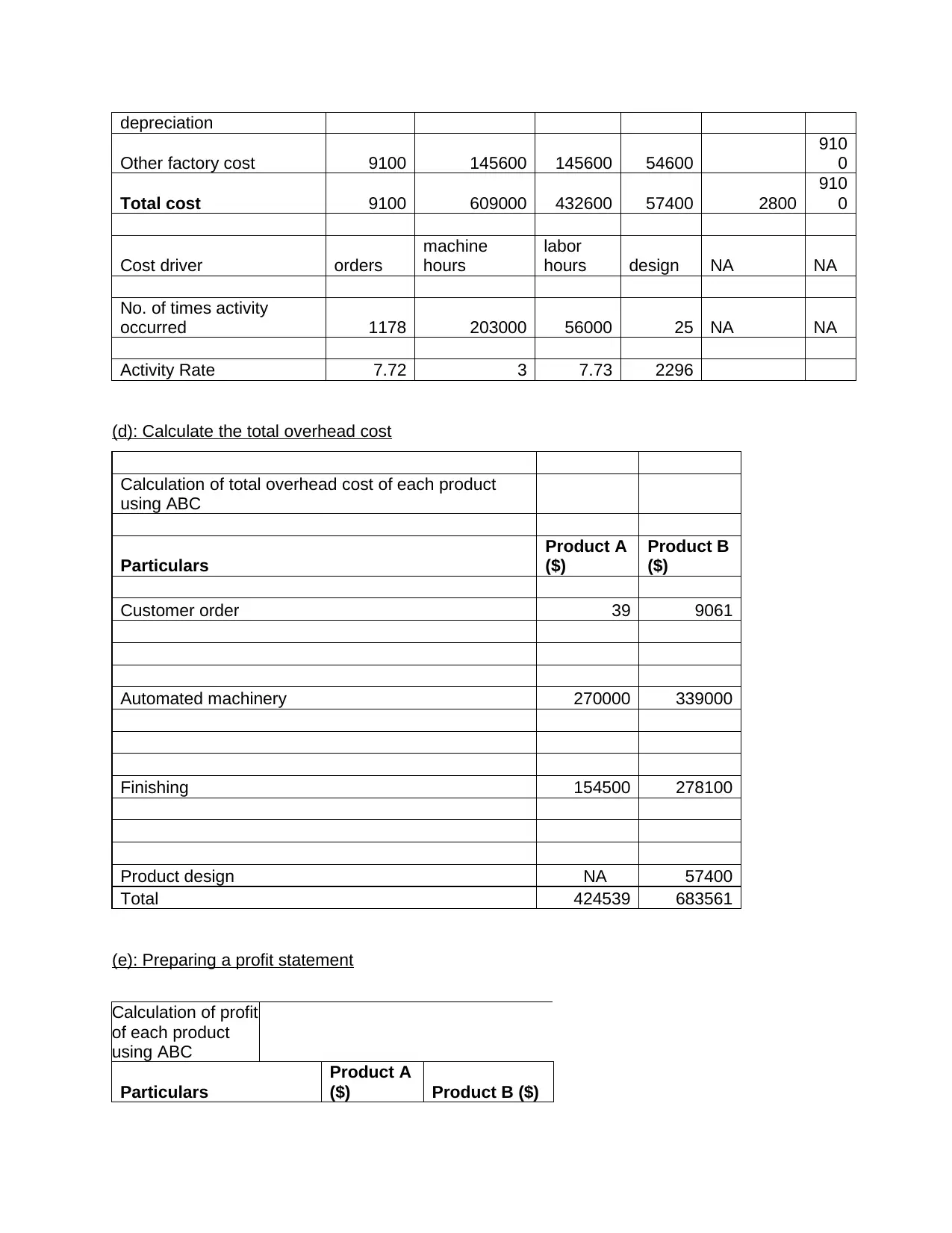

depreciation

Other factory cost 9100 145600 145600 54600

910

0

Total cost 9100 609000 432600 57400 2800

910

0

Cost driver orders

machine

hours

labor

hours design NA NA

No. of times activity

occurred 1178 203000 56000 25 NA NA

Activity Rate 7.72 3 7.73 2296

(d): Calculate the total overhead cost

Calculation of total overhead cost of each product

using ABC

Particulars

Product A

($)

Product B

($)

Customer order 39 9061

Automated machinery 270000 339000

Finishing 154500 278100

Product design NA 57400

Total 424539 683561

(e): Preparing a profit statement

Calculation of profit

of each product

using ABC

Particulars

Product A

($) Product B ($)

Other factory cost 9100 145600 145600 54600

910

0

Total cost 9100 609000 432600 57400 2800

910

0

Cost driver orders

machine

hours

labor

hours design NA NA

No. of times activity

occurred 1178 203000 56000 25 NA NA

Activity Rate 7.72 3 7.73 2296

(d): Calculate the total overhead cost

Calculation of total overhead cost of each product

using ABC

Particulars

Product A

($)

Product B

($)

Customer order 39 9061

Automated machinery 270000 339000

Finishing 154500 278100

Product design NA 57400

Total 424539 683561

(e): Preparing a profit statement

Calculation of profit

of each product

using ABC

Particulars

Product A

($) Product B ($)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.