Management Accounting Assignment Solution - Cost and Profit Analysis

VerifiedAdded on 2020/03/15

|16

|2155

|47

Homework Assignment

AI Summary

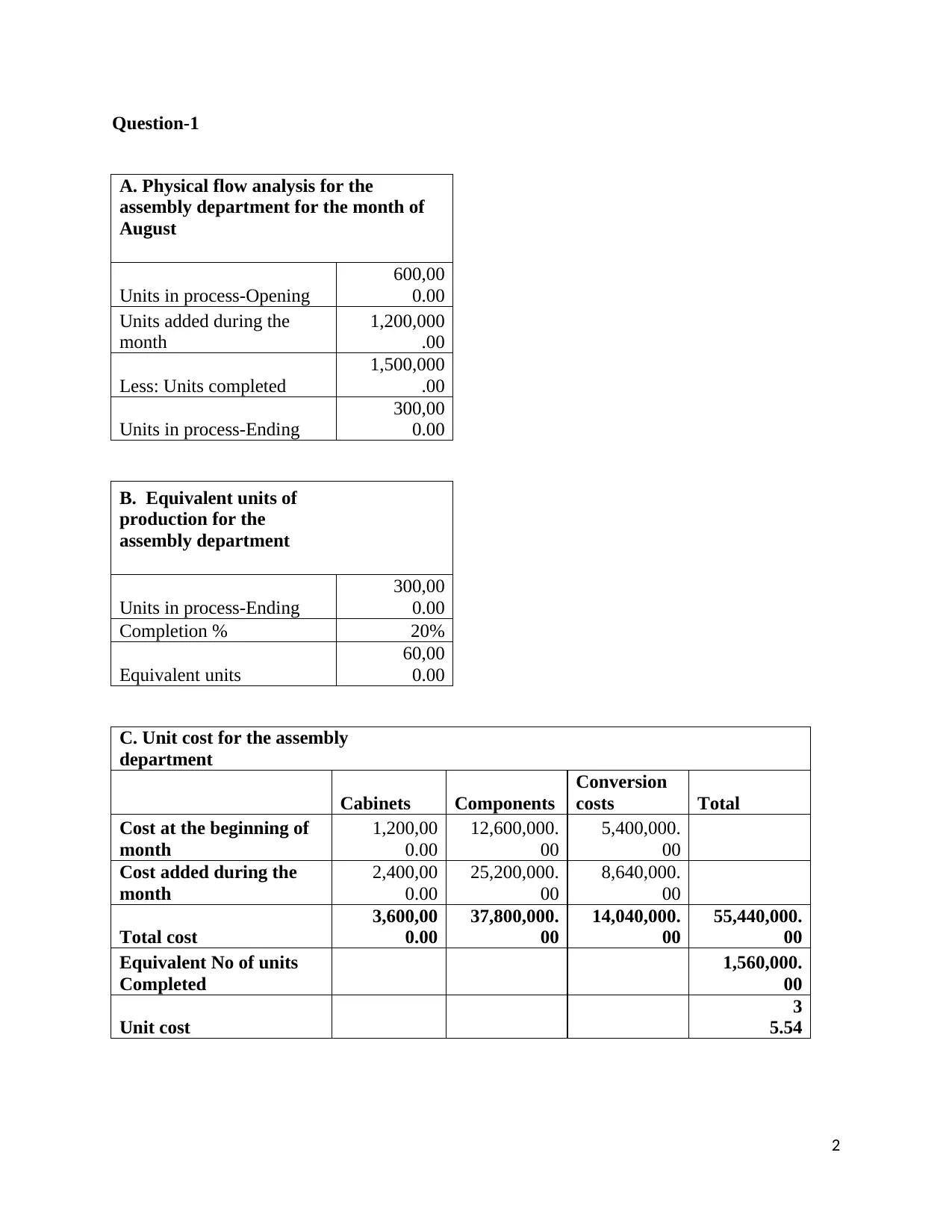

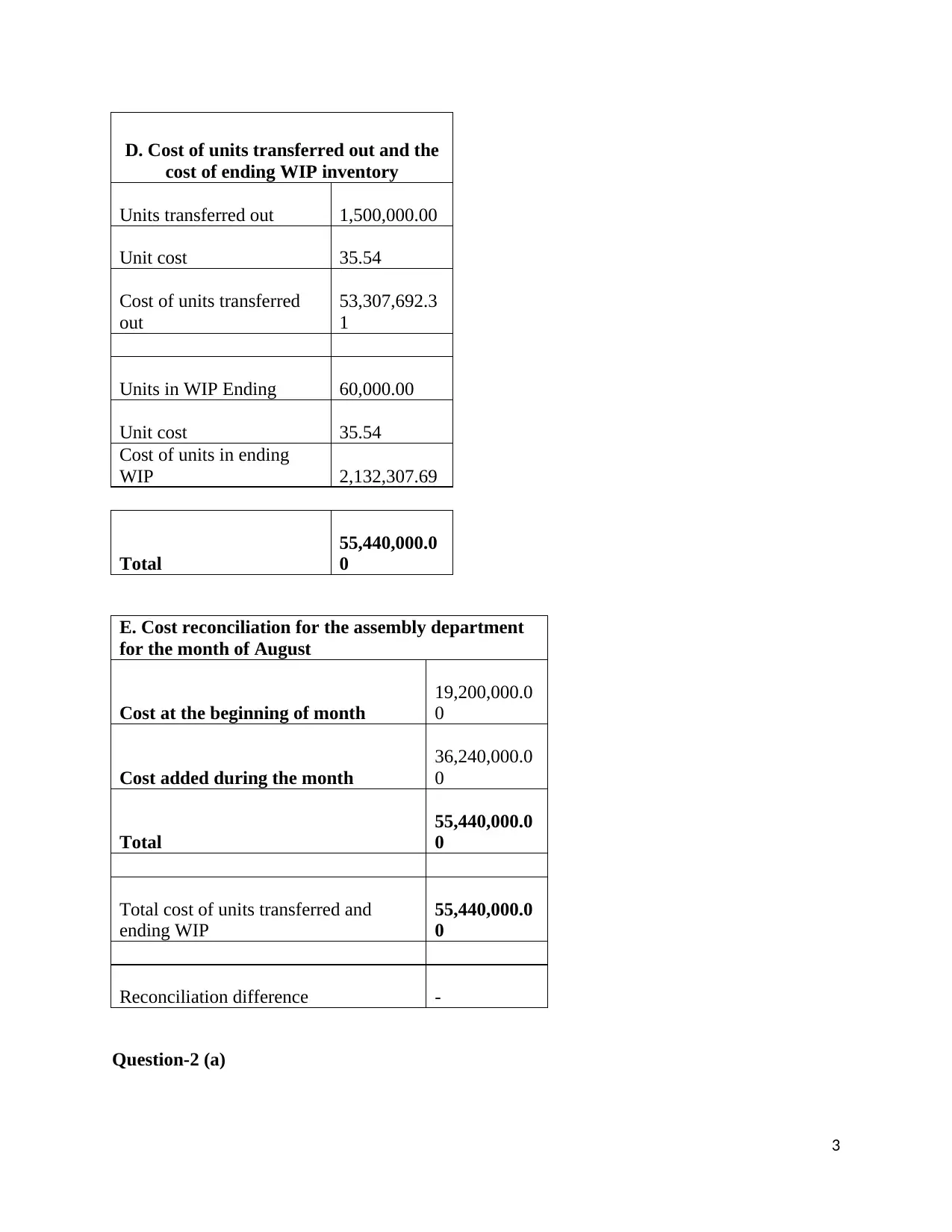

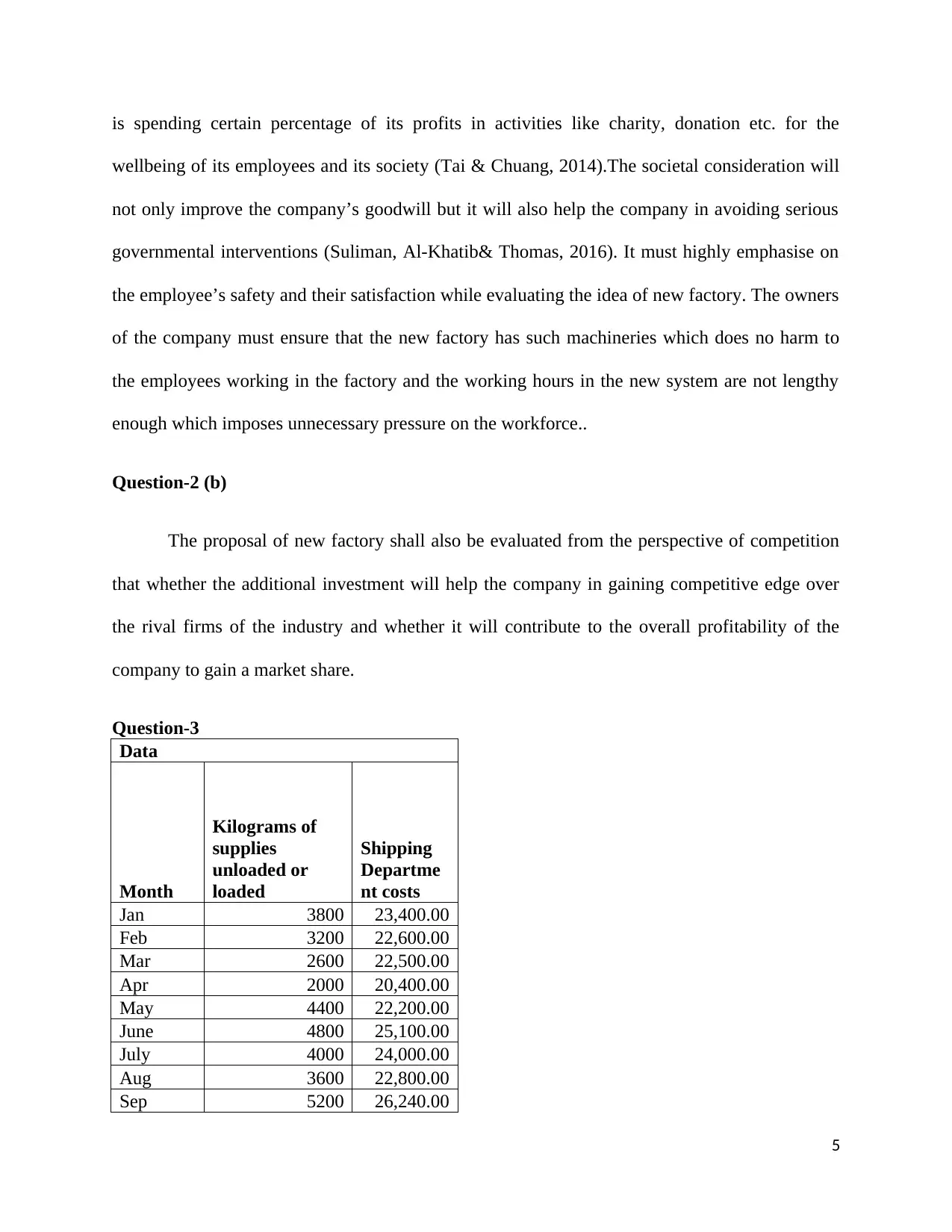

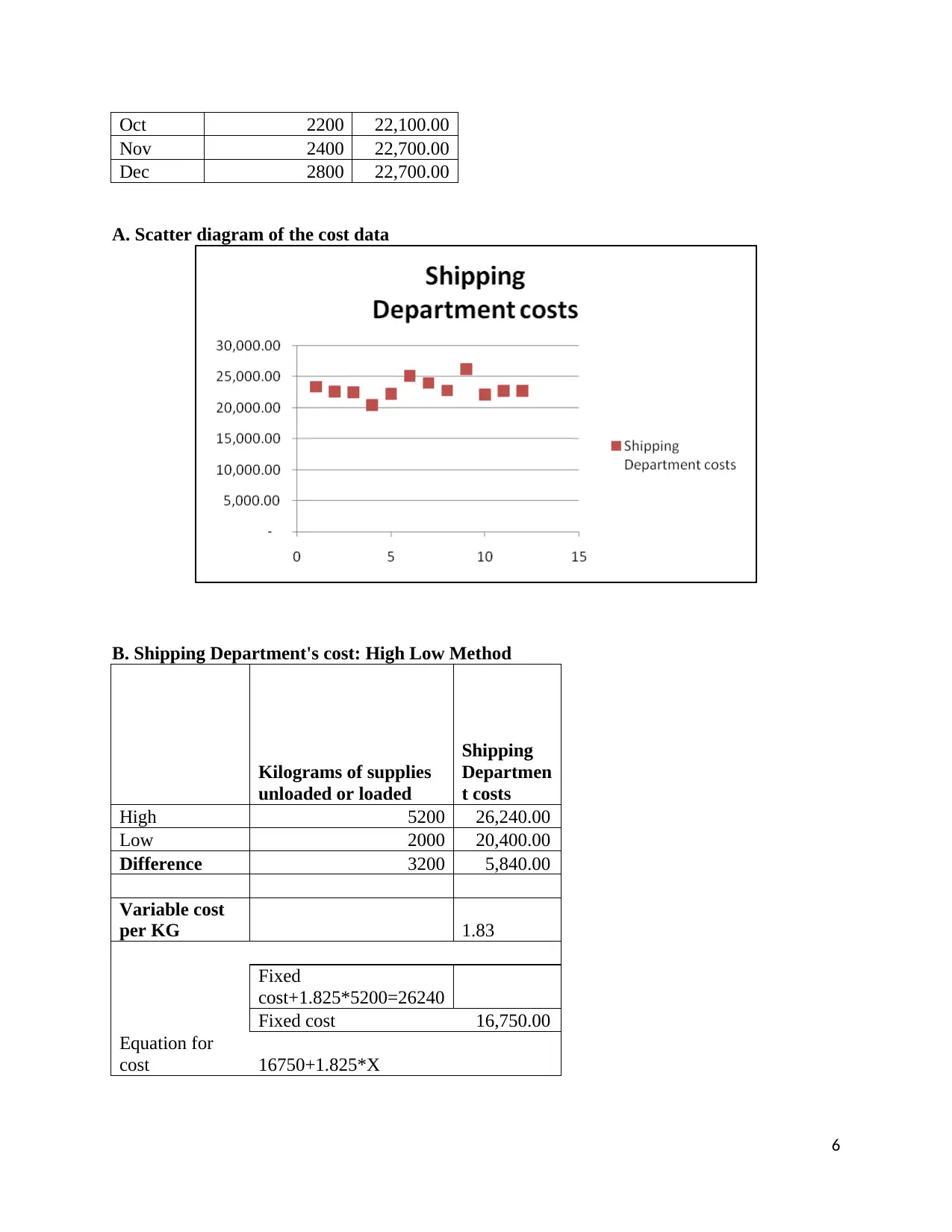

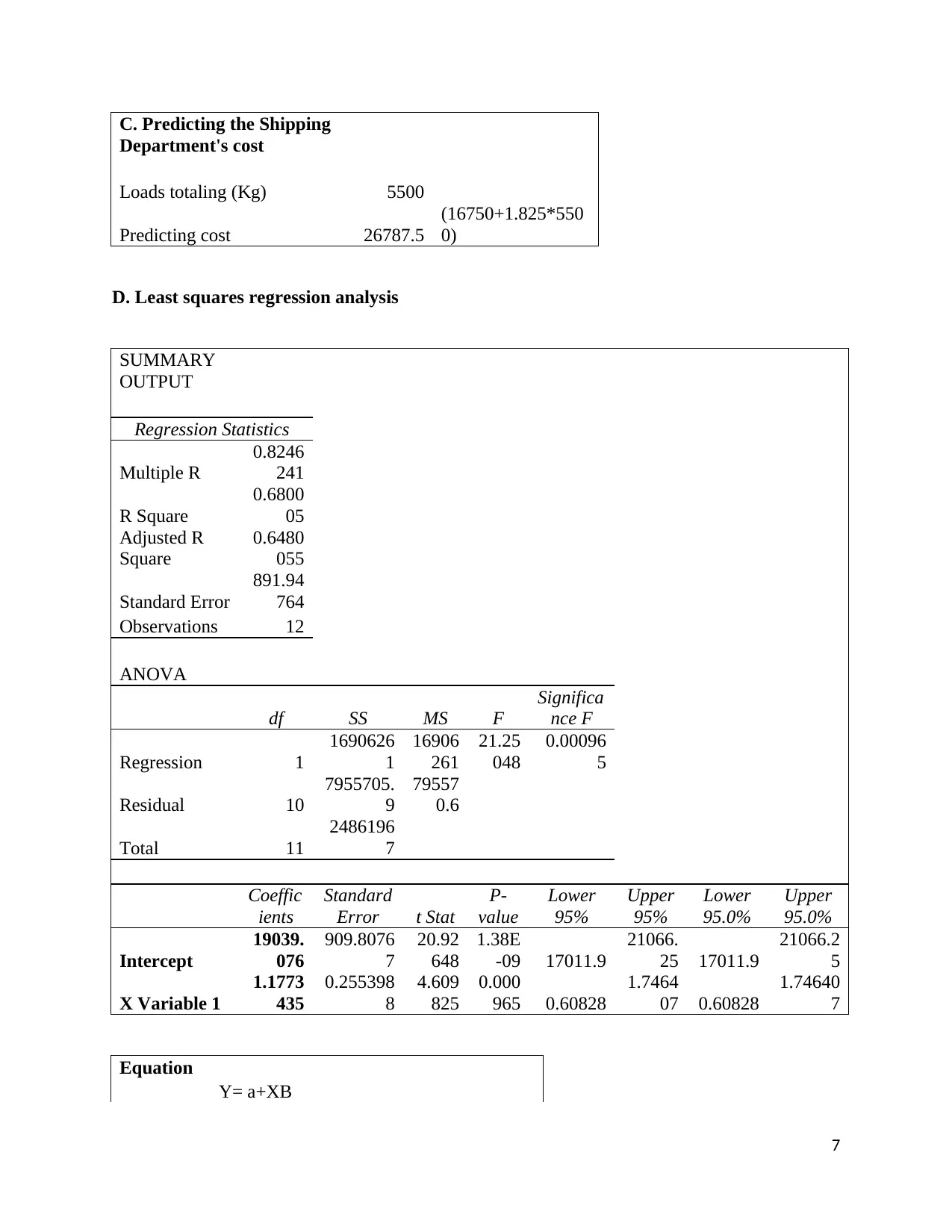

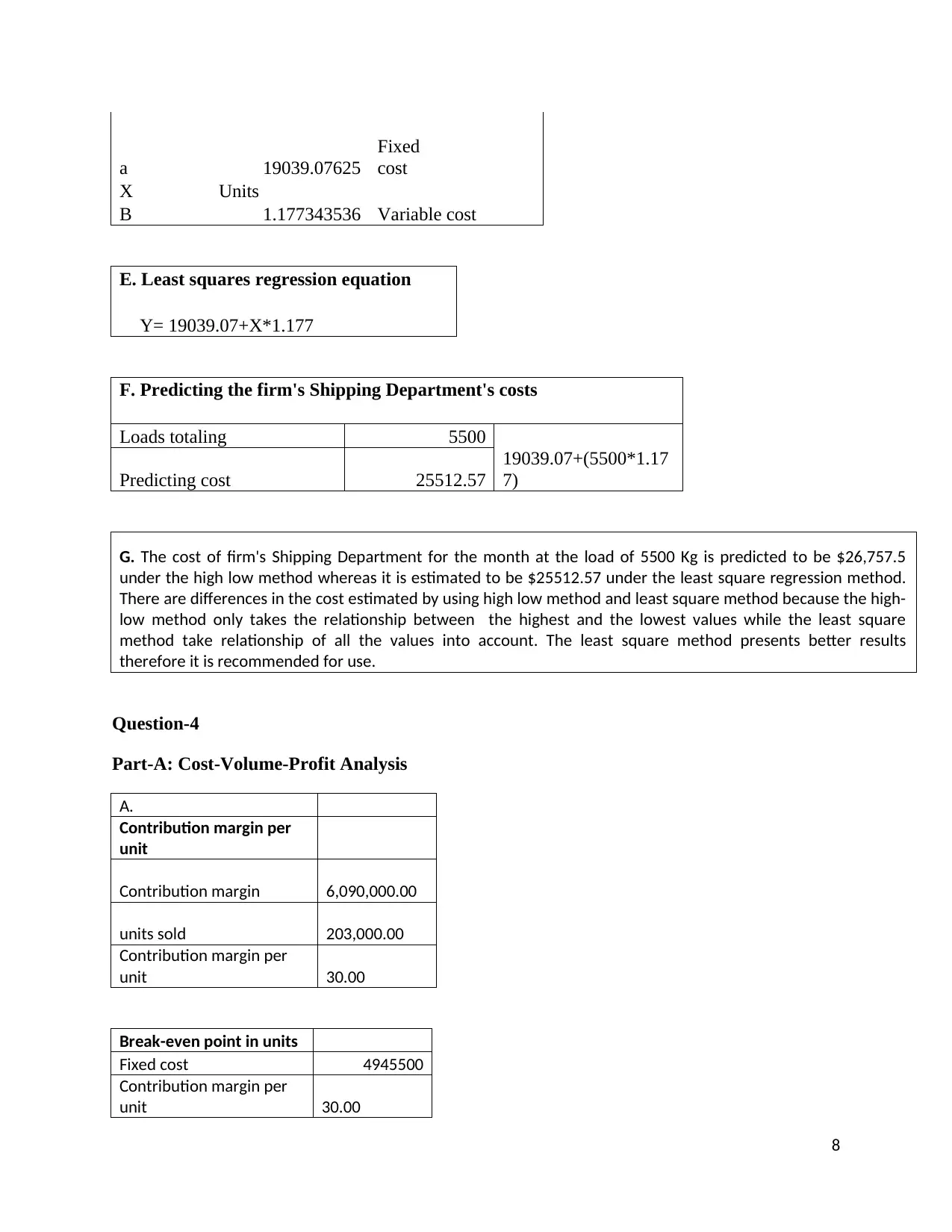

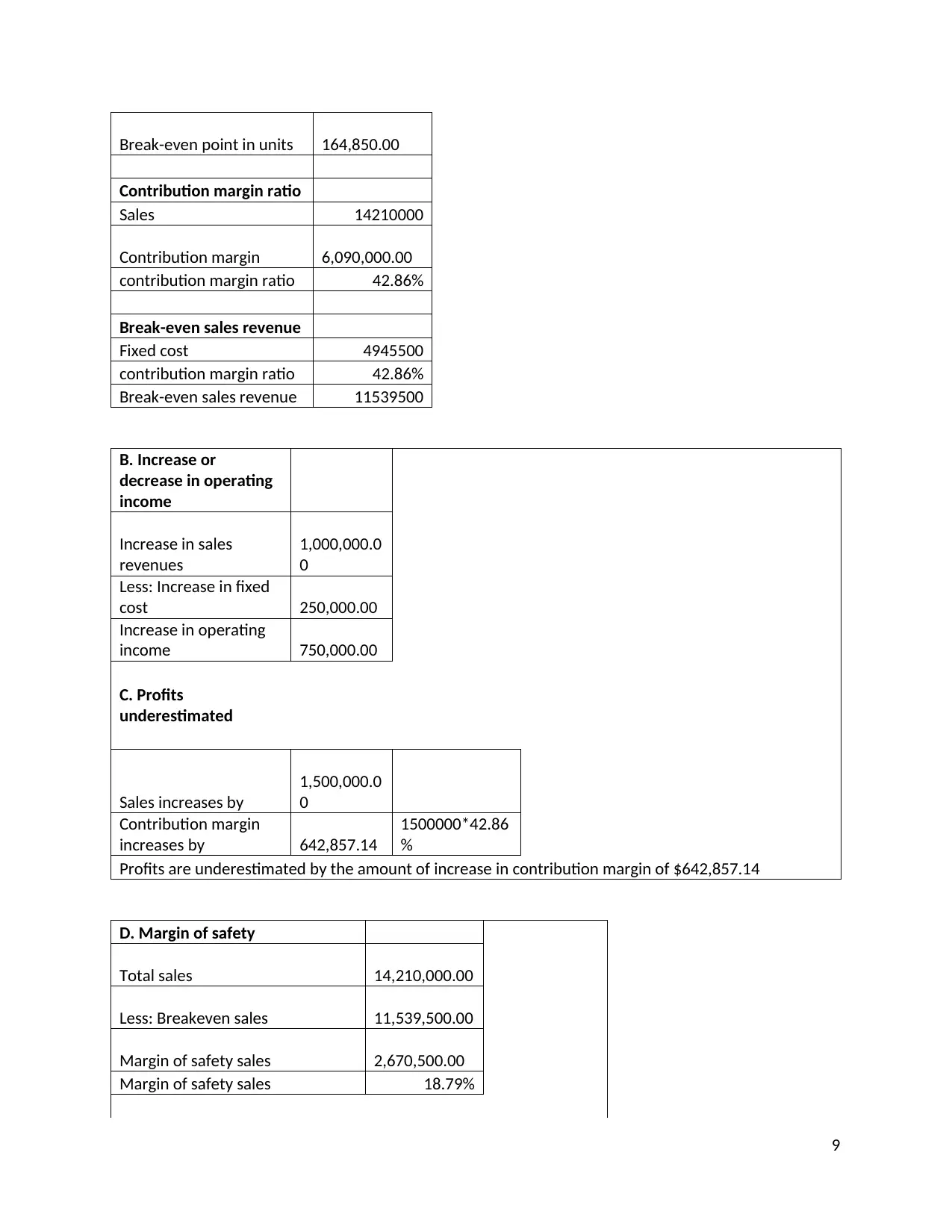

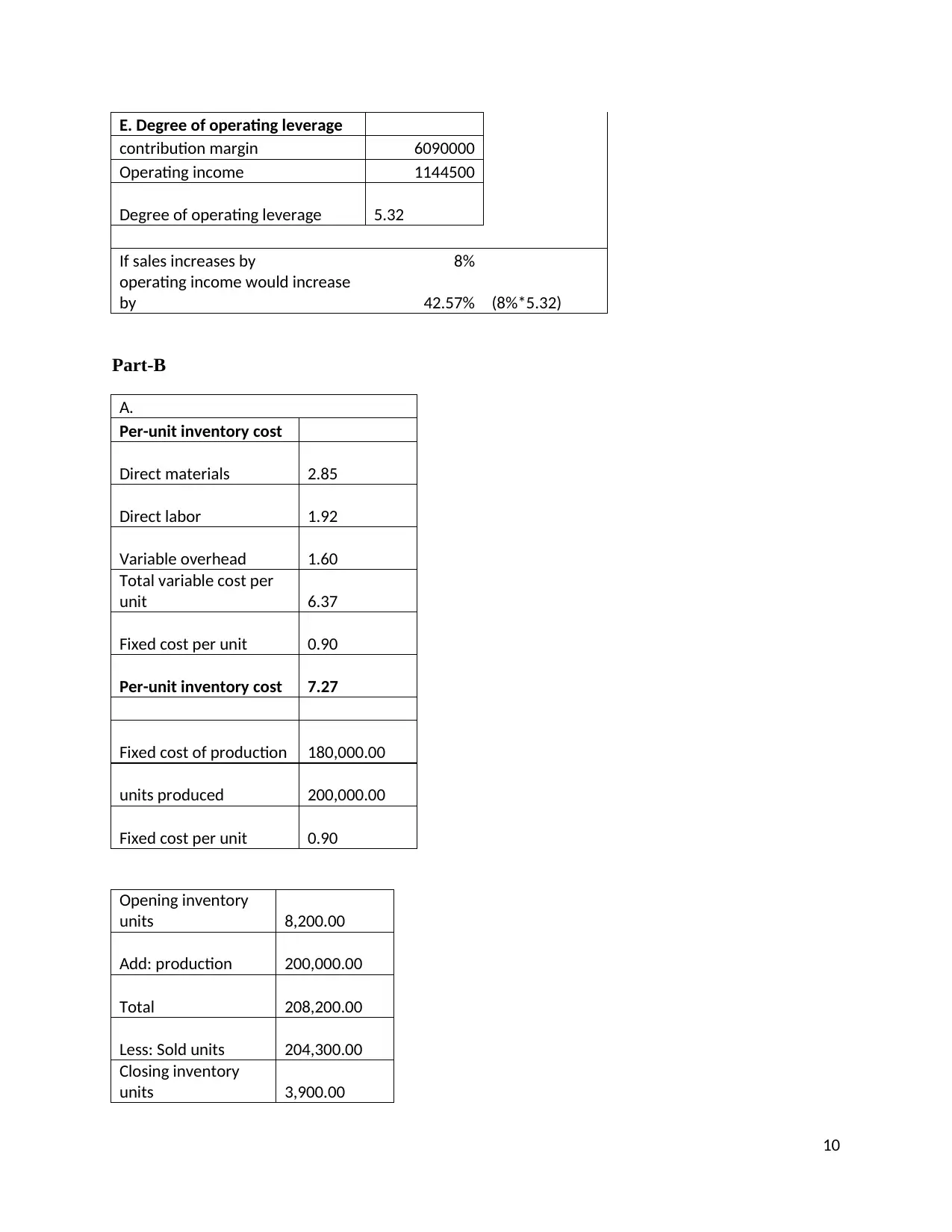

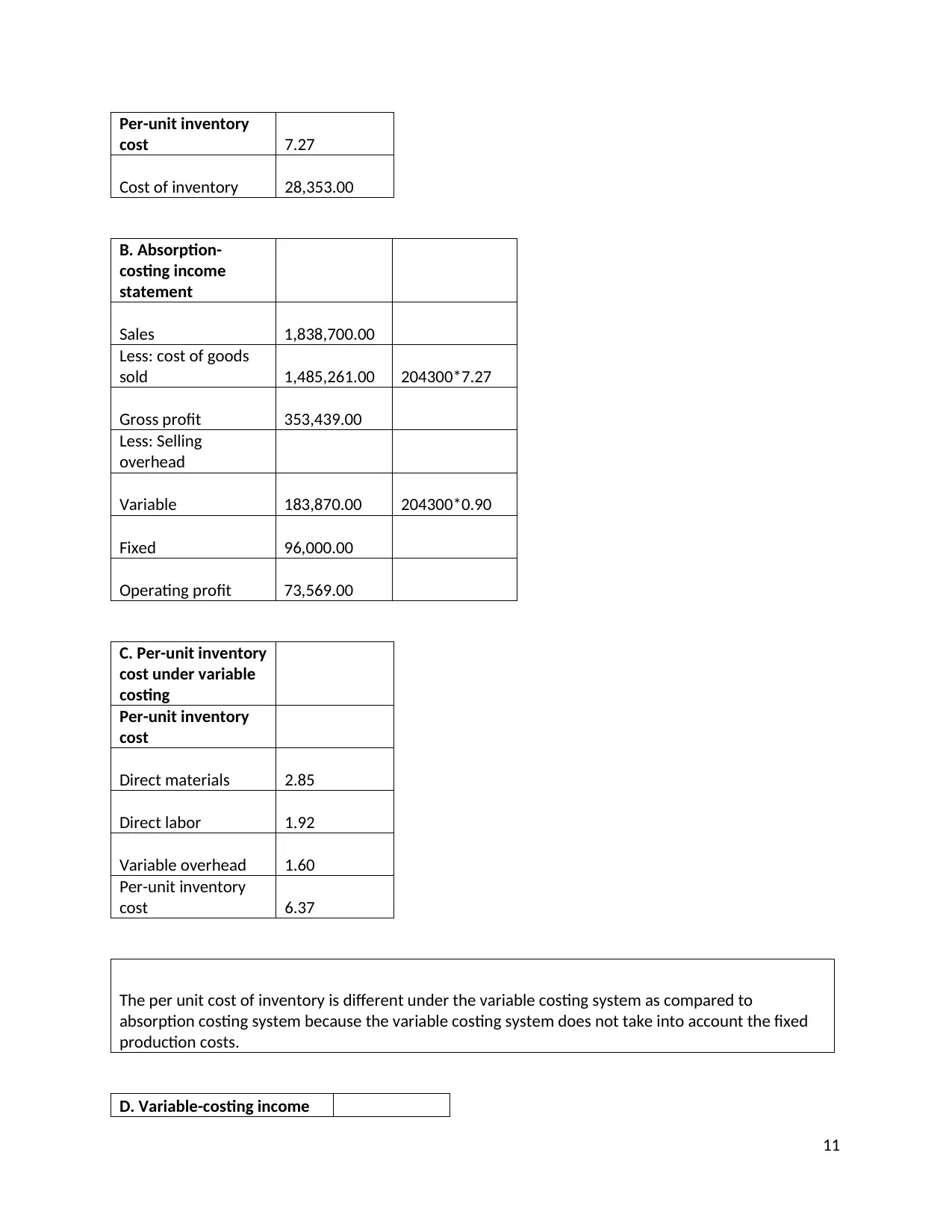

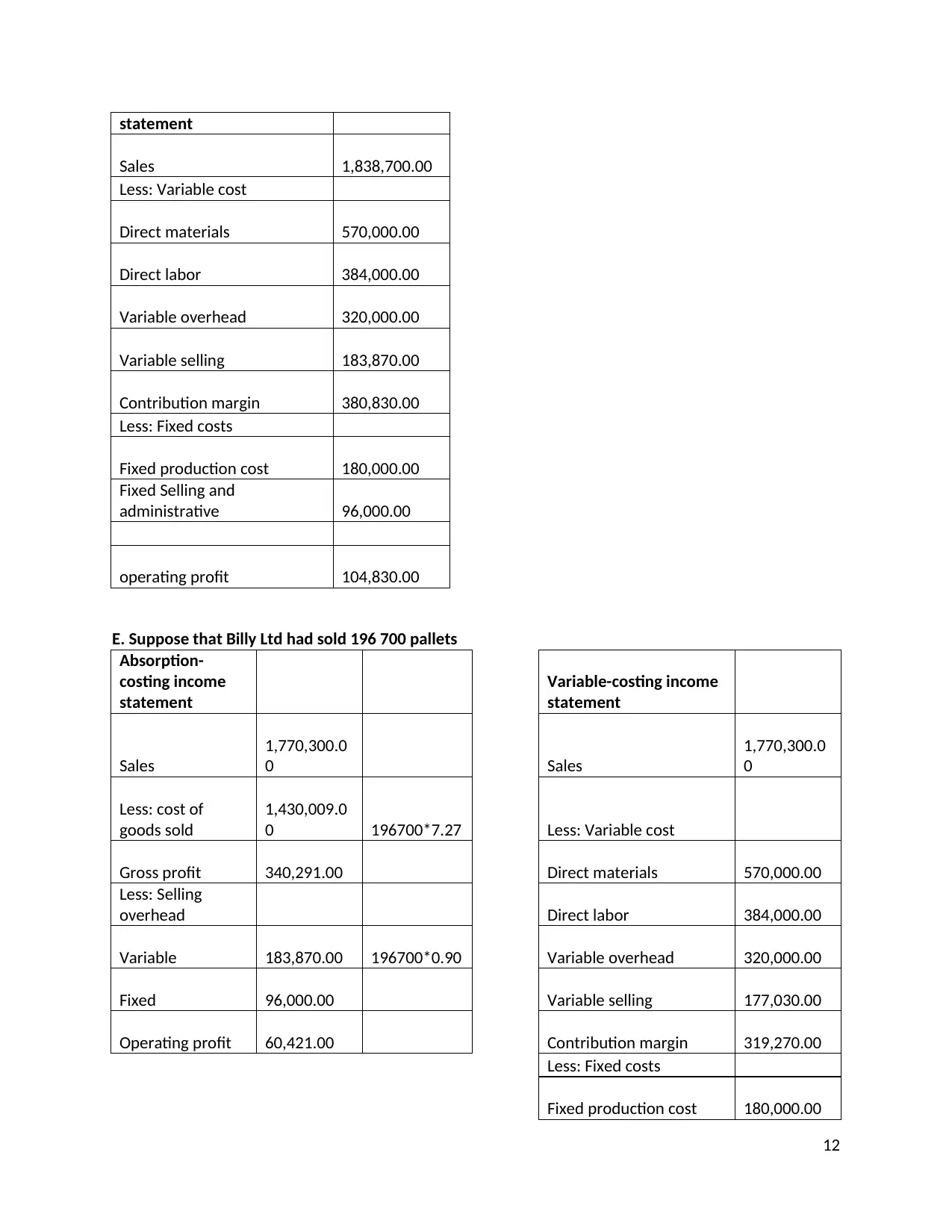

This document provides a comprehensive solution to a management accounting assignment. It begins with a physical flow and equivalent units analysis for the assembly department, including unit cost calculations and cost reconciliation. The solution then delves into corporate sustainability, examining financial, social, and environmental considerations for setting up a new factory. Furthermore, it includes analysis of shipping department costs using high-low and least squares regression methods, along with cost-volume-profit analysis, exploring break-even points, margin of safety, and operating leverage. Finally, the assignment covers inventory costing under both absorption and variable costing systems, along with a comparison of product costing using traditional and activity-based costing methods and includes a memorandum to the CEO regarding the change of costing methods.

1 out of 16

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.