Deakin University, MAA262: Management Accounting Concepts Assignment

VerifiedAdded on 2023/06/10

|12

|1859

|430

Homework Assignment

AI Summary

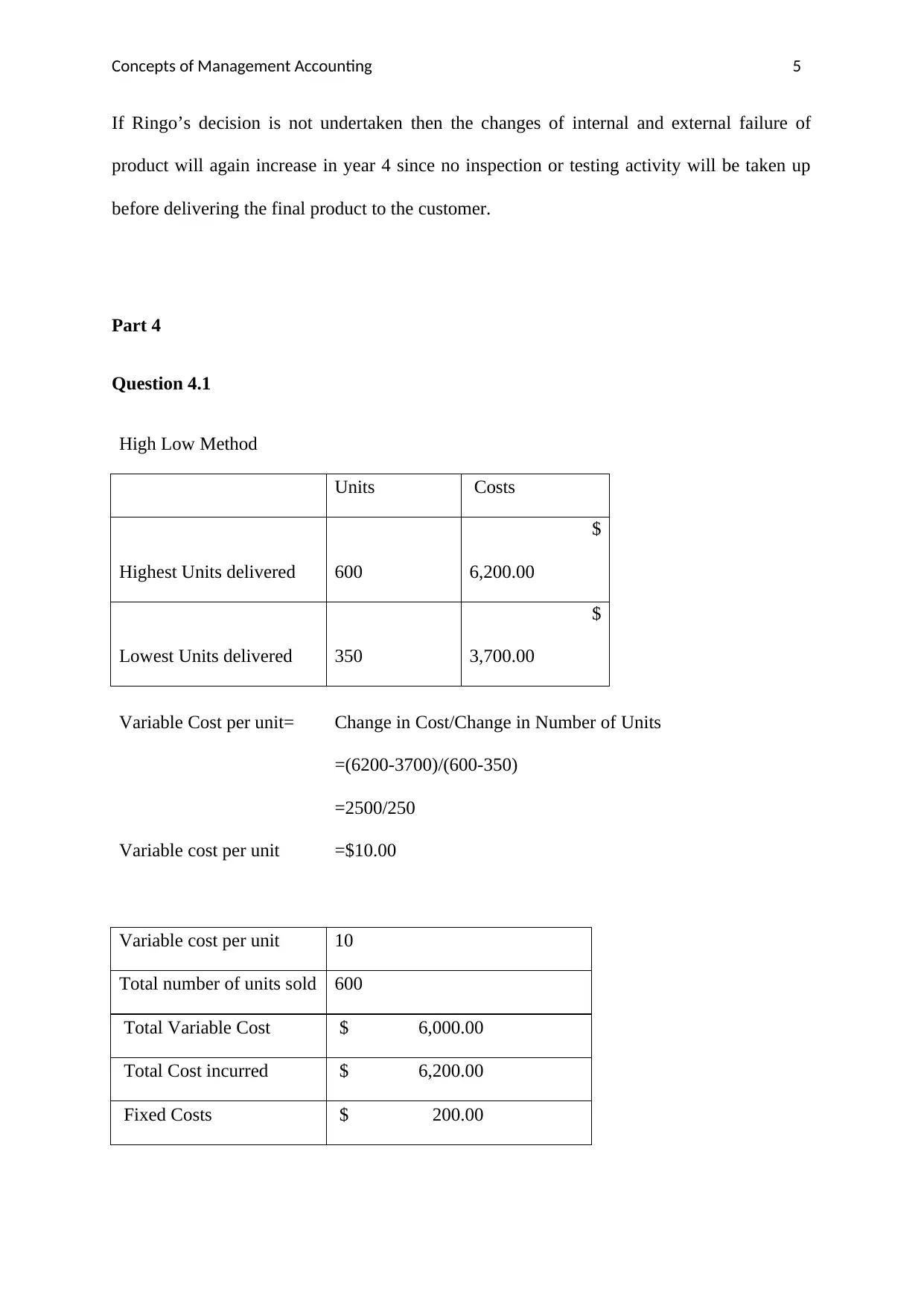

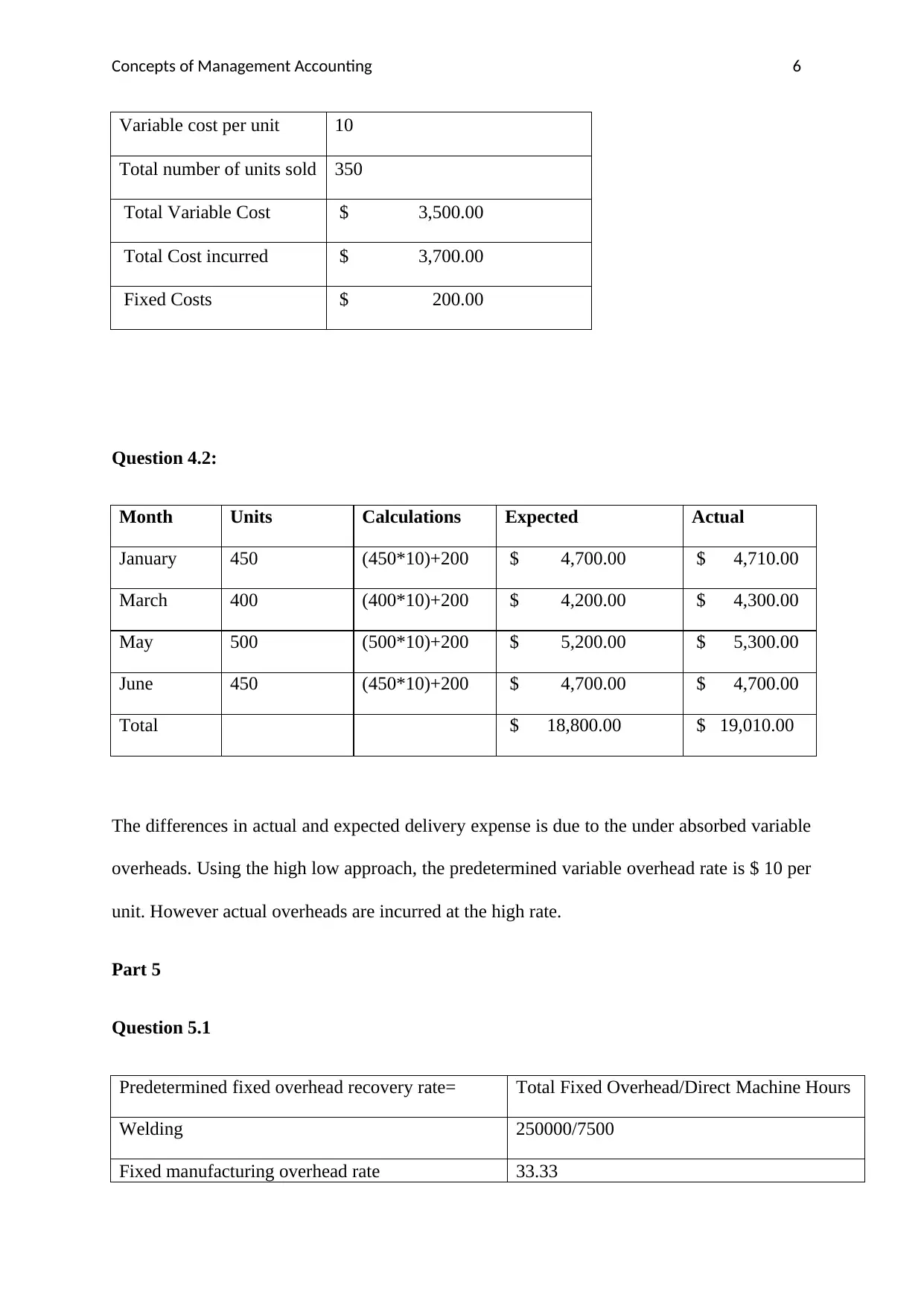

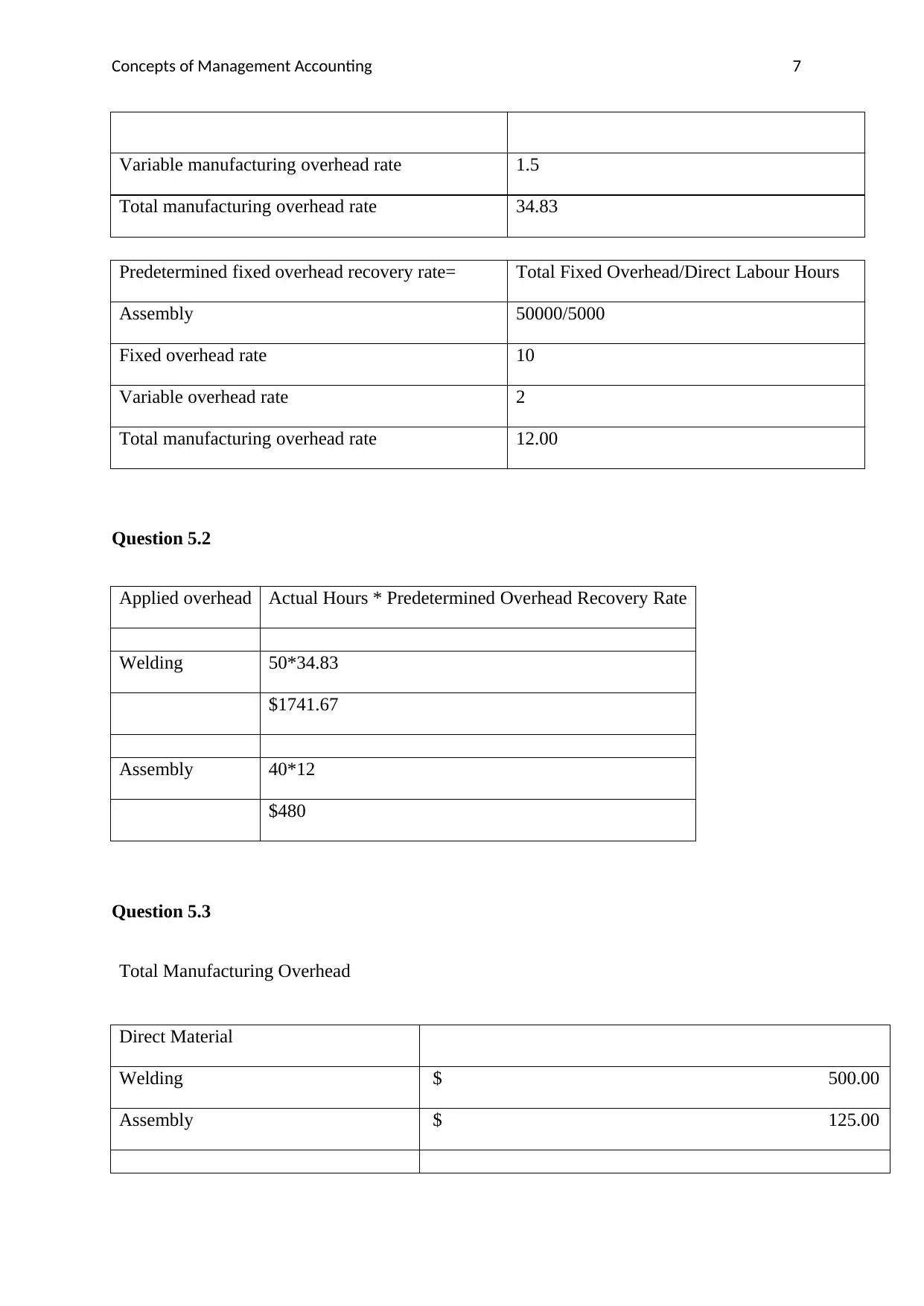

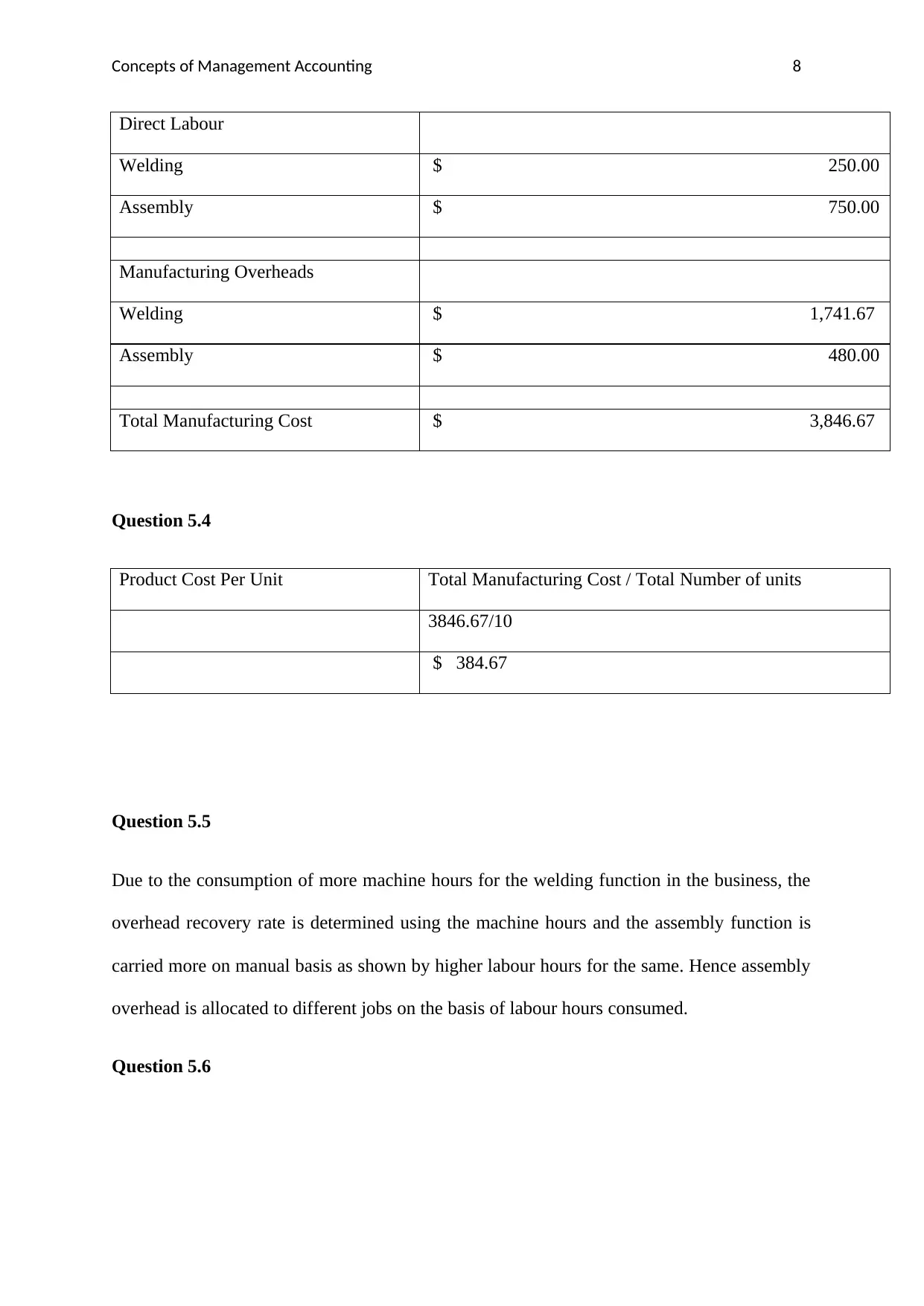

This document presents a comprehensive solution to a management accounting assignment, addressing key concepts such as ethical considerations in hiring, quality costs (prevention, appraisal, internal and external failures), and their impact. It further explores cost behavior analysis using the high-low method, overhead allocation (fixed and variable), and the application of Key Performance Indicators (KPIs) in business performance measurement. The assignment also delves into pricing strategies, comparing cost-plus pricing with value-based pricing, and their respective benefits and limitations. The solution provides detailed calculations, explanations, and references to support the analysis, offering a complete understanding of the management accounting principles discussed.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.