Management Accounting Assignment - Module Name, University

VerifiedAdded on 2019/10/30

|14

|1136

|207

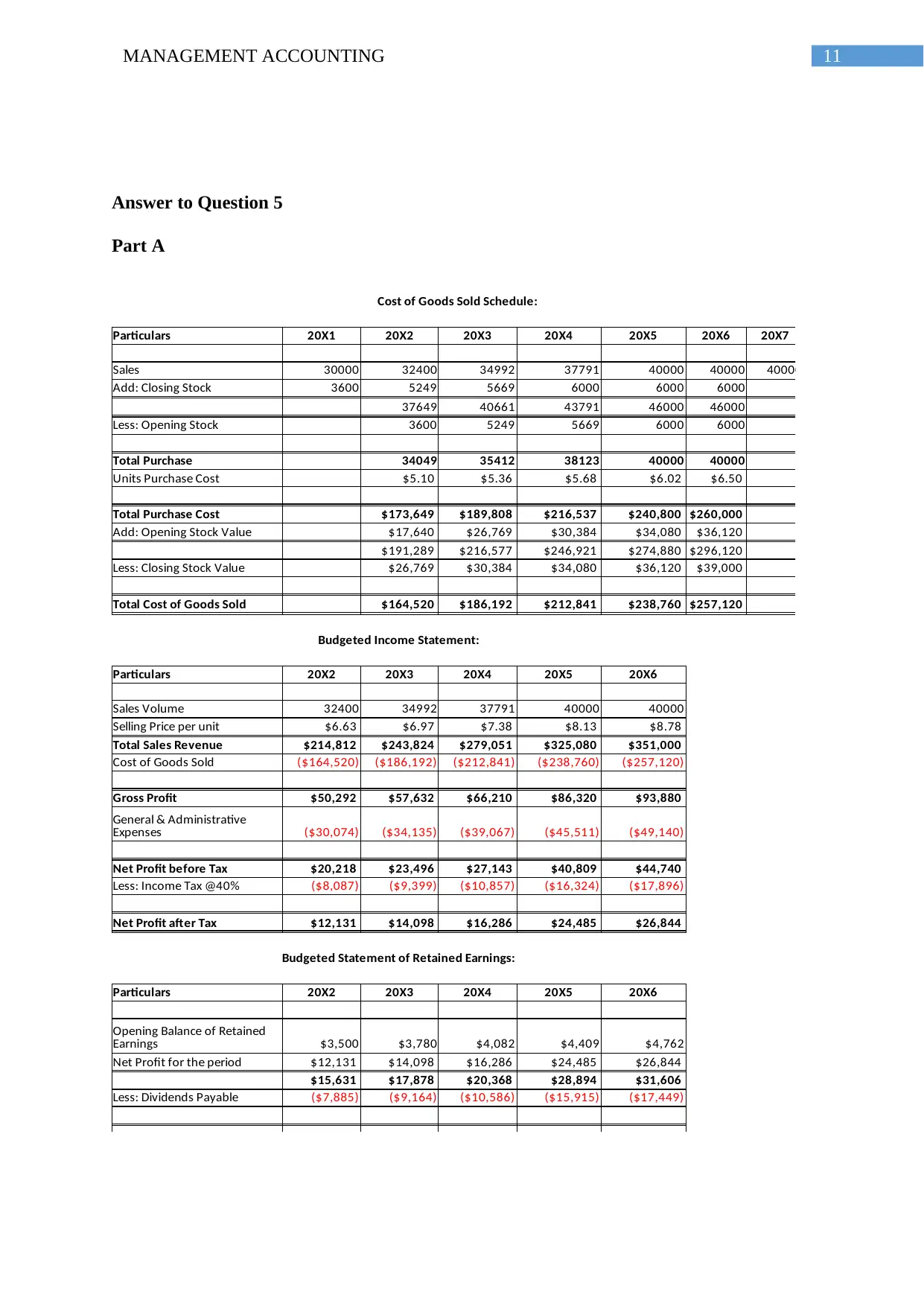

Homework Assignment

AI Summary

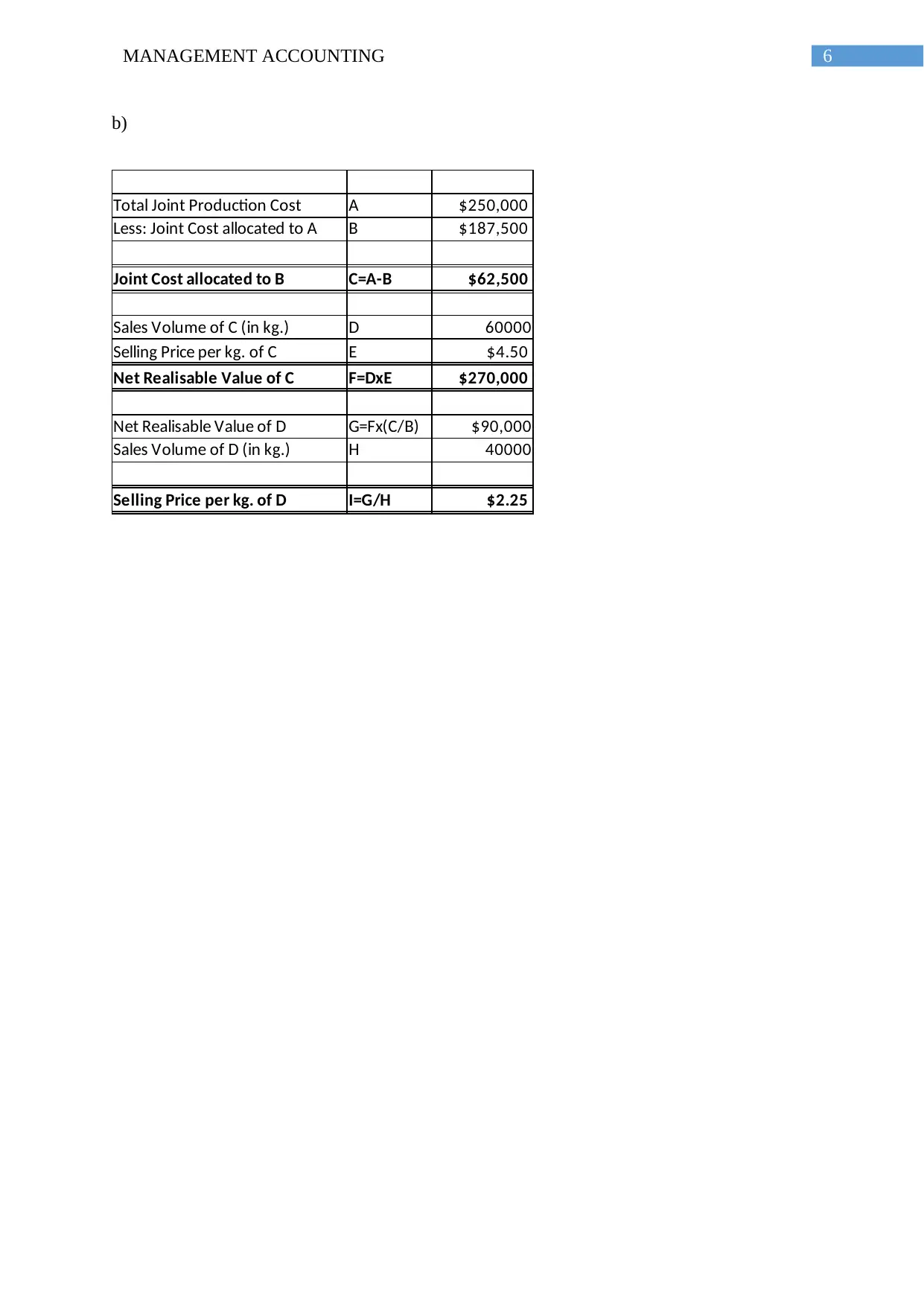

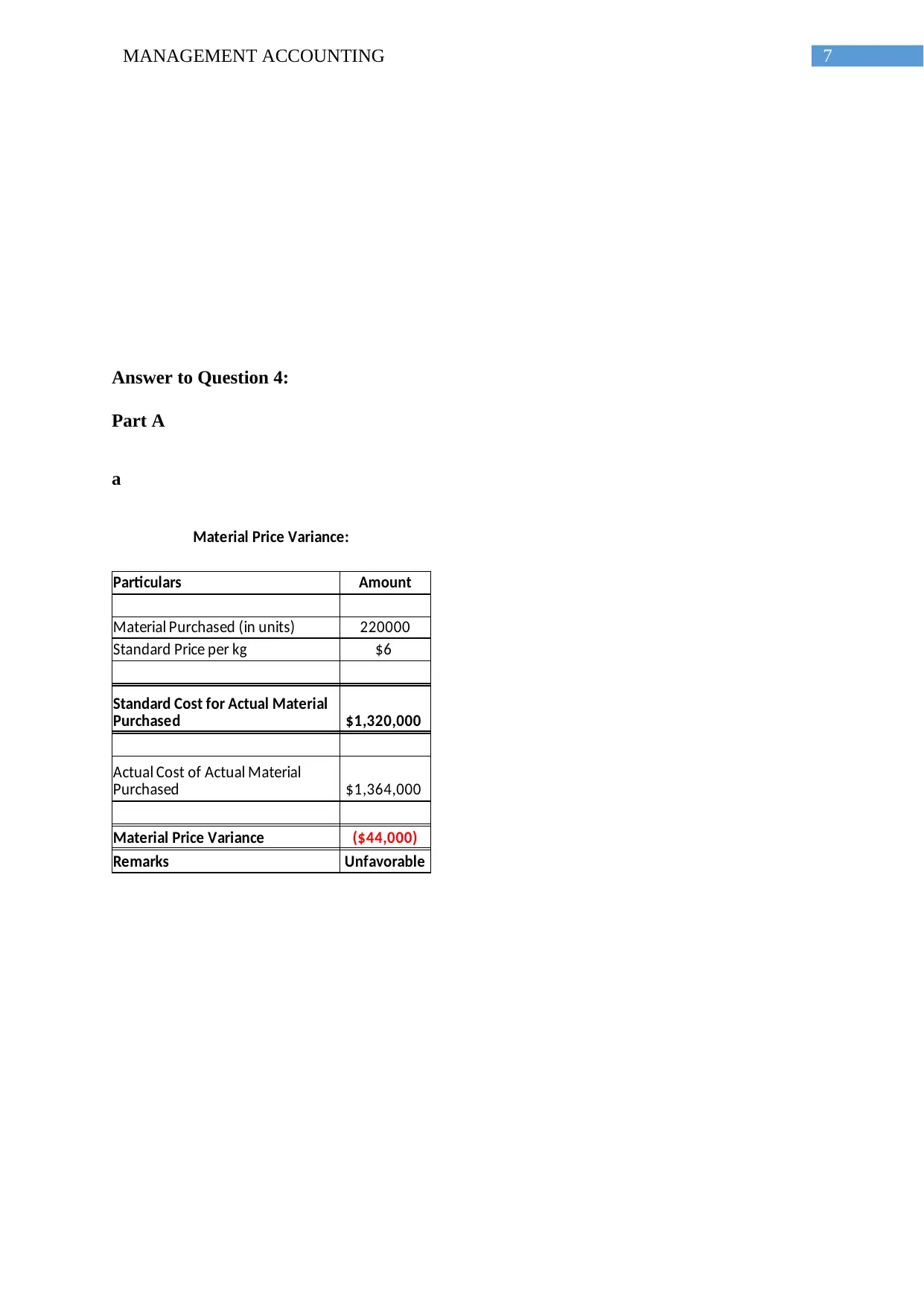

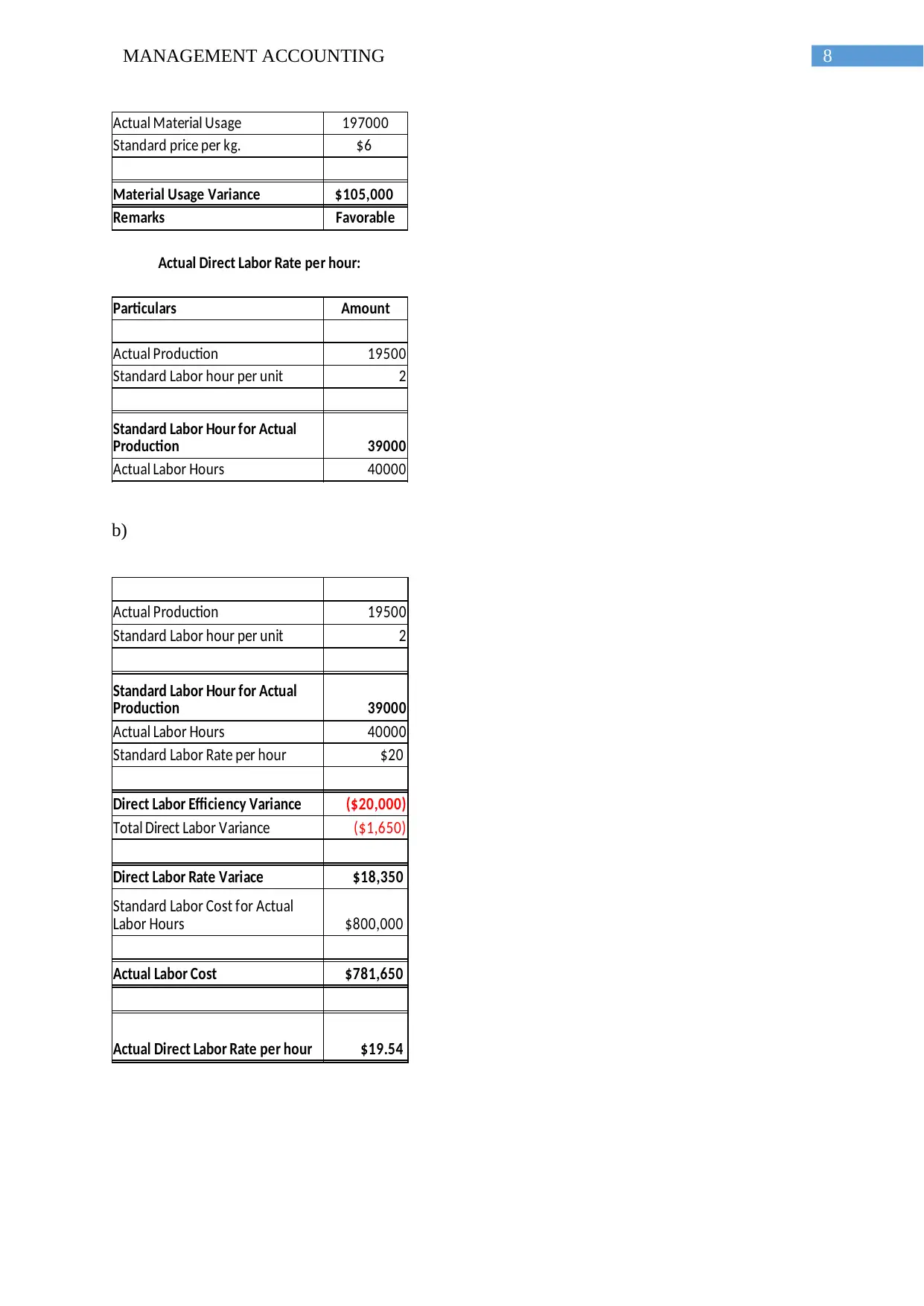

This document presents a comprehensive solution to a management accounting assignment. The assignment addresses key concepts including the application of modern cost management accounting to the construction of the Great Pyramid of Giza, the process of variance analysis in business management, and the importance of budgeting within an organization. The solution delves into the traditional approach versus modern cost accounting methods, explaining how processed costing can aid in cost regulation. It also explores variance analysis, highlighting its role in identifying causes of budget discrepancies, improving overall budgeting activities, and enhancing organizational performance. Furthermore, the assignment discusses the core dimensions of budget formulation, the influence of political factors, and the necessity of aligning budgets with governmental priorities and policies. References to relevant academic sources are included to support the analysis.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.