Management Accounting Assignment: Process Costing, CVP, ABC

VerifiedAdded on 2021/06/16

|17

|1872

|15

Homework Assignment

AI Summary

This management accounting assignment solution provides detailed answers to five key questions. Question 1 explores process costing systems, calculating the cost of goods transferred and work-in-process. Question 2 delves into accounting for sustainability, discussing sustainability reports, key indicators, legal environments, and staff encouragement. Question 3 examines cost behavior, including the high-low method and least square regression. Question 4 focuses on cost-volume-profit (CVP) analysis, calculating break-even points, profit projections, and the impact of changes in sales price and variable costs. Finally, Question 5 covers activity-based costing (ABC) and management, analyzing product profitability and recommending strategic decisions. The assignment utilizes various financial concepts to analyze the provided financial information.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING

Table of Contents

Question 1: Process Costing Systems..............................................................................................3

Part 1:...........................................................................................................................................3

(a) Cost of units transferred to finished goods inventory during August:...............................3

(b) Cost of the Finishing Department's work in process inventory on 31 August:..................3

Part 2:...........................................................................................................................................3

Question 2: Accounting for sustainability.......................................................................................4

Part 1:...........................................................................................................................................4

Part 2:...........................................................................................................................................4

Part 3:...........................................................................................................................................5

Part 4:...........................................................................................................................................5

Question 3: Cost behaviour.............................................................................................................6

Part 1:...........................................................................................................................................6

Part 2:...........................................................................................................................................6

Part 4:...........................................................................................................................................7

Part 5:...........................................................................................................................................7

Part 6:...........................................................................................................................................7

Part 7:...........................................................................................................................................8

Question 4: Cost-volume-profit analysis.........................................................................................8

Table of Contents

Question 1: Process Costing Systems..............................................................................................3

Part 1:...........................................................................................................................................3

(a) Cost of units transferred to finished goods inventory during August:...............................3

(b) Cost of the Finishing Department's work in process inventory on 31 August:..................3

Part 2:...........................................................................................................................................3

Question 2: Accounting for sustainability.......................................................................................4

Part 1:...........................................................................................................................................4

Part 2:...........................................................................................................................................4

Part 3:...........................................................................................................................................5

Part 4:...........................................................................................................................................5

Question 3: Cost behaviour.............................................................................................................6

Part 1:...........................................................................................................................................6

Part 2:...........................................................................................................................................6

Part 4:...........................................................................................................................................7

Part 5:...........................................................................................................................................7

Part 6:...........................................................................................................................................7

Part 7:...........................................................................................................................................8

Question 4: Cost-volume-profit analysis.........................................................................................8

2MANAGEMENT ACCOUNTING

Part 1:...........................................................................................................................................8

Part 2:...........................................................................................................................................9

Part 3:.........................................................................................................................................10

Part 4:.........................................................................................................................................10

Part 5:.........................................................................................................................................11

Part 6:.........................................................................................................................................13

Question 5: Activity-based costing and management...................................................................14

Part 1:.........................................................................................................................................14

Part 2:.........................................................................................................................................14

Part 3:.........................................................................................................................................14

Part 5:.........................................................................................................................................15

Part 6:.........................................................................................................................................16

Part 7:.........................................................................................................................................16

Part 8:.........................................................................................................................................17

References......................................................................................................................................18

Part 1:...........................................................................................................................................8

Part 2:...........................................................................................................................................9

Part 3:.........................................................................................................................................10

Part 4:.........................................................................................................................................10

Part 5:.........................................................................................................................................11

Part 6:.........................................................................................................................................13

Question 5: Activity-based costing and management...................................................................14

Part 1:.........................................................................................................................................14

Part 2:.........................................................................................................................................14

Part 3:.........................................................................................................................................14

Part 5:.........................................................................................................................................15

Part 6:.........................................................................................................................................16

Part 7:.........................................................................................................................................16

Part 8:.........................................................................................................................................17

References......................................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING

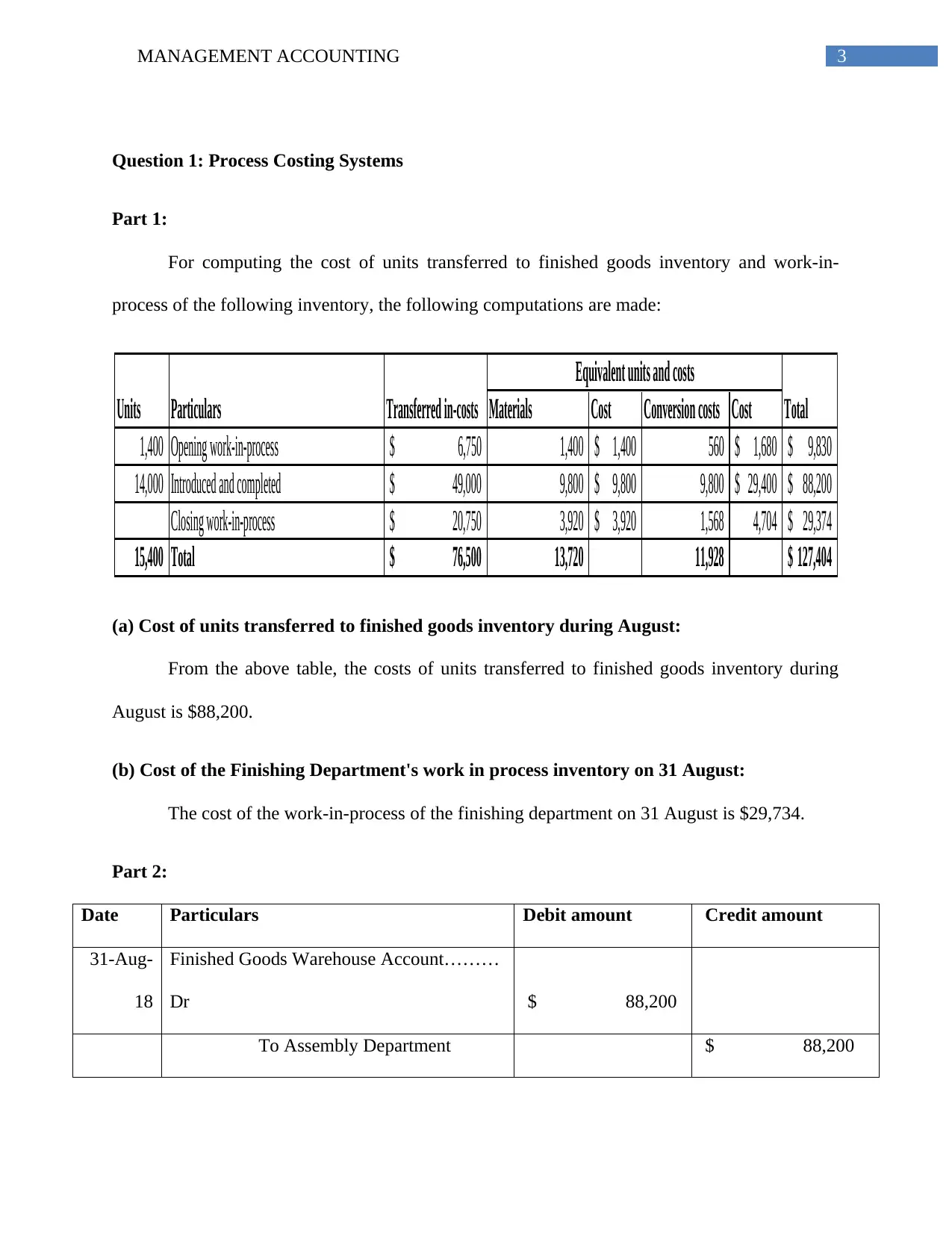

Question 1: Process Costing Systems

Part 1:

For computing the cost of units transferred to finished goods inventory and work-in-

process of the following inventory, the following computations are made:

Materials Cost Conversion costs Cost

1,400 Opening work-in-process 6,750$ 1,400 1,400$ 560 1,680$ 9,830$

14,000 Introduced and completed 49,000$ 9,800 9,800$ 9,800 29,400$ 88,200$

Closing work-in-process 20,750$ 3,920 3,920$ 1,568 4,704 29,374$

15,400 Total 76,500$ 13,720 11,928 127,404$

Particulars Transferred in-costs

Equivalent units and costs

TotalUnits

(a) Cost of units transferred to finished goods inventory during August:

From the above table, the costs of units transferred to finished goods inventory during

August is $88,200.

(b) Cost of the Finishing Department's work in process inventory on 31 August:

The cost of the work-in-process of the finishing department on 31 August is $29,734.

Part 2:

Date Particulars Debit amount Credit amount

31-Aug-

18

Finished Goods Warehouse Account………

Dr $ 88,200

To Assembly Department $ 88,200

Question 1: Process Costing Systems

Part 1:

For computing the cost of units transferred to finished goods inventory and work-in-

process of the following inventory, the following computations are made:

Materials Cost Conversion costs Cost

1,400 Opening work-in-process 6,750$ 1,400 1,400$ 560 1,680$ 9,830$

14,000 Introduced and completed 49,000$ 9,800 9,800$ 9,800 29,400$ 88,200$

Closing work-in-process 20,750$ 3,920 3,920$ 1,568 4,704 29,374$

15,400 Total 76,500$ 13,720 11,928 127,404$

Particulars Transferred in-costs

Equivalent units and costs

TotalUnits

(a) Cost of units transferred to finished goods inventory during August:

From the above table, the costs of units transferred to finished goods inventory during

August is $88,200.

(b) Cost of the Finishing Department's work in process inventory on 31 August:

The cost of the work-in-process of the finishing department on 31 August is $29,734.

Part 2:

Date Particulars Debit amount Credit amount

31-Aug-

18

Finished Goods Warehouse Account………

Dr $ 88,200

To Assembly Department $ 88,200

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING

Account

Question 2: Accounting for sustainability

Part 1:

Sustainability Report allows a corporation to evaluate the various type the factor which

are seen to be related to the economic, environment and social impacts which impacting on the

everyday activities. It needs to be further assessed that the different types of the reporting factors

for the sustainability reporting is synonymous with the non-financial reporting aspects. The

intrinsic element of the reporting has been able to combine the non-financial and financial

performance (Globalreporting.org, 2018). It is important for Wealth Wise to maintain the

relevant sustainability aspect due to the growing level of discontent among the employees. In

addition to this, there have been several types of the negative reports which are seen to be

published in the media which are related to the “treatment of businesses in Phuket and

Langkawi”.

Part 2:

The key indicators used by Wealth Wise are discerned in form of the financial indicators,

economic indicators, social indicators, and environment indicators. The financial measures will

be conducive in ensuring sustained profit for the business aligned with other objectives such as

“return on investment” and gross insurance premiums. It has been further assed that the different

parameters for economic factors are discerned with appropriate procedure for hiring and

spending on the local suppliers. It will also assist the company in achieving various development

projects for the public benefit. The social indicators maintained by Wealth Wise is depicted in

Account

Question 2: Accounting for sustainability

Part 1:

Sustainability Report allows a corporation to evaluate the various type the factor which

are seen to be related to the economic, environment and social impacts which impacting on the

everyday activities. It needs to be further assessed that the different types of the reporting factors

for the sustainability reporting is synonymous with the non-financial reporting aspects. The

intrinsic element of the reporting has been able to combine the non-financial and financial

performance (Globalreporting.org, 2018). It is important for Wealth Wise to maintain the

relevant sustainability aspect due to the growing level of discontent among the employees. In

addition to this, there have been several types of the negative reports which are seen to be

published in the media which are related to the “treatment of businesses in Phuket and

Langkawi”.

Part 2:

The key indicators used by Wealth Wise are discerned in form of the financial indicators,

economic indicators, social indicators, and environment indicators. The financial measures will

be conducive in ensuring sustained profit for the business aligned with other objectives such as

“return on investment” and gross insurance premiums. It has been further assed that the different

parameters for economic factors are discerned with appropriate procedure for hiring and

spending on the local suppliers. It will also assist the company in achieving various development

projects for the public benefit. The social indicators maintained by Wealth Wise is depicted in

5MANAGEMENT ACCOUNTING

from of employee satisfaction ratings, number of staff hired who were previously unemployed. It

has been also noted that the social indicators are conducive in building employee satisfaction

ratings (Onyebuchi, Nwankwo & Onuka, 2018).

Part 3:

The assessment of the various types of the legal environment will be conducive in terms

of depicting the reports which are claimed for the purpose of the assessment of the different

types of the factor, which are seen to be related to understanding of the insurance contract in the

situation of crisis such as earthquake and flood. The understanding of various types of the legal

environment by the company will be conducive to know about different type’s amount which

needs to be paid to the other business corporation during such a situation. The various types of

the alternative performance measures need to be further assed in terms of the depicting the

political impacts which are directly seen to relevant to the current operations of the insurance

company(Fehr-Duda & Fehr, 2016).

Part 4:

The different procedures to encourage the staff sustainability has been identified with the

providing the employees with greater responsibility towards making them aware of the social

ethics such. This are related to the increased preference for the use of public transportation rather

than private transportation. Some of the various types of the other initiatives which can be taken

by the employees are seen to be associated to the ensuring optimum use of office electricity

(Clancy, 2018). The use of performance measurement system will be conducive in terms of the

analysing, process and measurement of the individual initiatives towards sustainability goals.

from of employee satisfaction ratings, number of staff hired who were previously unemployed. It

has been also noted that the social indicators are conducive in building employee satisfaction

ratings (Onyebuchi, Nwankwo & Onuka, 2018).

Part 3:

The assessment of the various types of the legal environment will be conducive in terms

of depicting the reports which are claimed for the purpose of the assessment of the different

types of the factor, which are seen to be related to understanding of the insurance contract in the

situation of crisis such as earthquake and flood. The understanding of various types of the legal

environment by the company will be conducive to know about different type’s amount which

needs to be paid to the other business corporation during such a situation. The various types of

the alternative performance measures need to be further assed in terms of the depicting the

political impacts which are directly seen to relevant to the current operations of the insurance

company(Fehr-Duda & Fehr, 2016).

Part 4:

The different procedures to encourage the staff sustainability has been identified with the

providing the employees with greater responsibility towards making them aware of the social

ethics such. This are related to the increased preference for the use of public transportation rather

than private transportation. Some of the various types of the other initiatives which can be taken

by the employees are seen to be associated to the ensuring optimum use of office electricity

(Clancy, 2018). The use of performance measurement system will be conducive in terms of the

analysing, process and measurement of the individual initiatives towards sustainability goals.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING

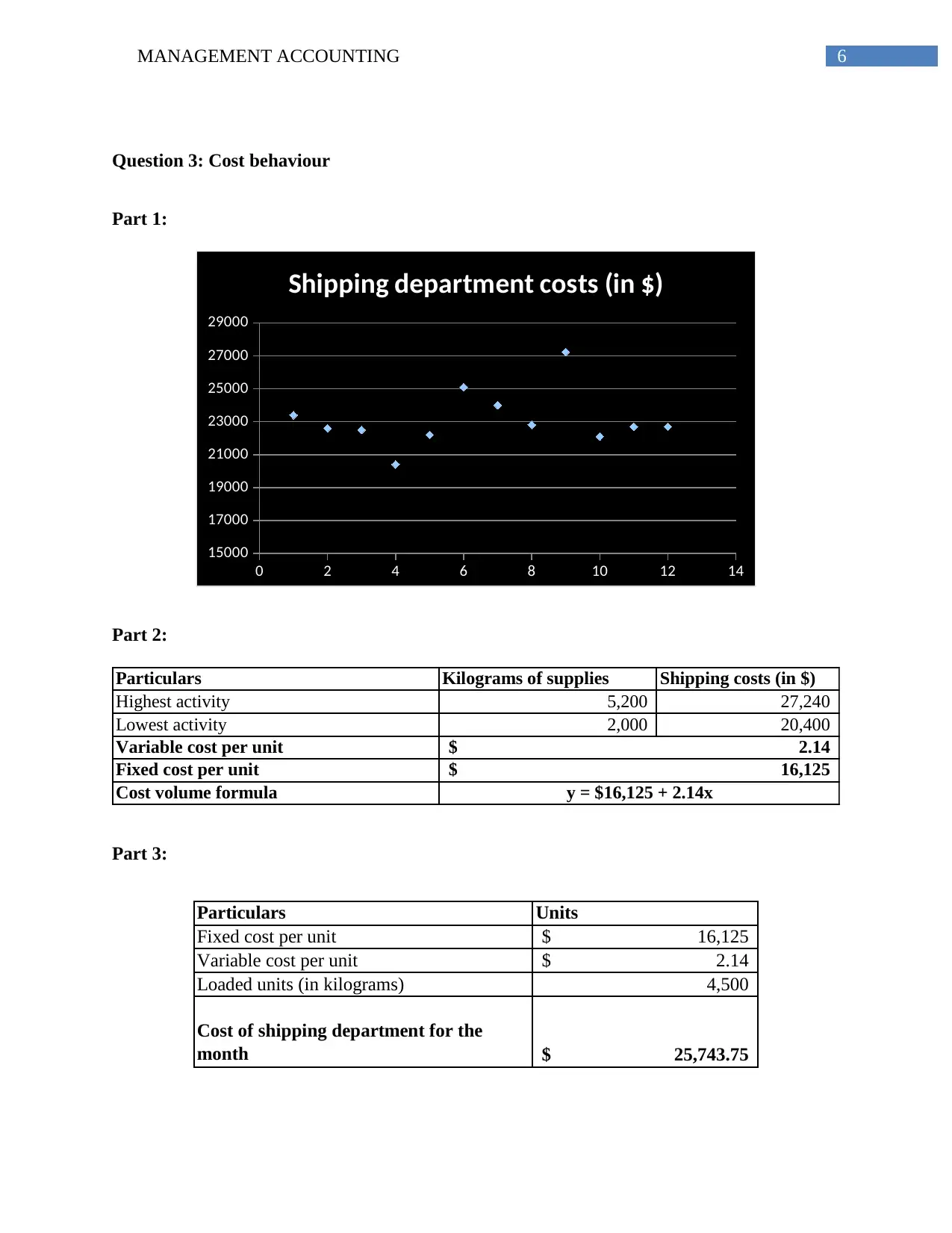

Question 3: Cost behaviour

Part 1:

0 2 4 6 8 10 12 14

15000

17000

19000

21000

23000

25000

27000

29000

Shipping department costs (in $)

Part 2:

Particulars Kilograms of supplies Shipping costs (in $)

Highest activity 5,200 27,240

Lowest activity 2,000 20,400

Variable cost per unit

Fixed cost per unit

Cost volume formula

2.14$

16,125$

y = $16,125 + 2.14x

Part 3:

Particulars Units

Fixed cost per unit 16,125$

Variable cost per unit 2.14$

Loaded units (in kilograms) 4,500

Cost of shipping department for the

month 25,743.75$

Question 3: Cost behaviour

Part 1:

0 2 4 6 8 10 12 14

15000

17000

19000

21000

23000

25000

27000

29000

Shipping department costs (in $)

Part 2:

Particulars Kilograms of supplies Shipping costs (in $)

Highest activity 5,200 27,240

Lowest activity 2,000 20,400

Variable cost per unit

Fixed cost per unit

Cost volume formula

2.14$

16,125$

y = $16,125 + 2.14x

Part 3:

Particulars Units

Fixed cost per unit 16,125$

Variable cost per unit 2.14$

Loaded units (in kilograms) 4,500

Cost of shipping department for the

month 25,743.75$

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING

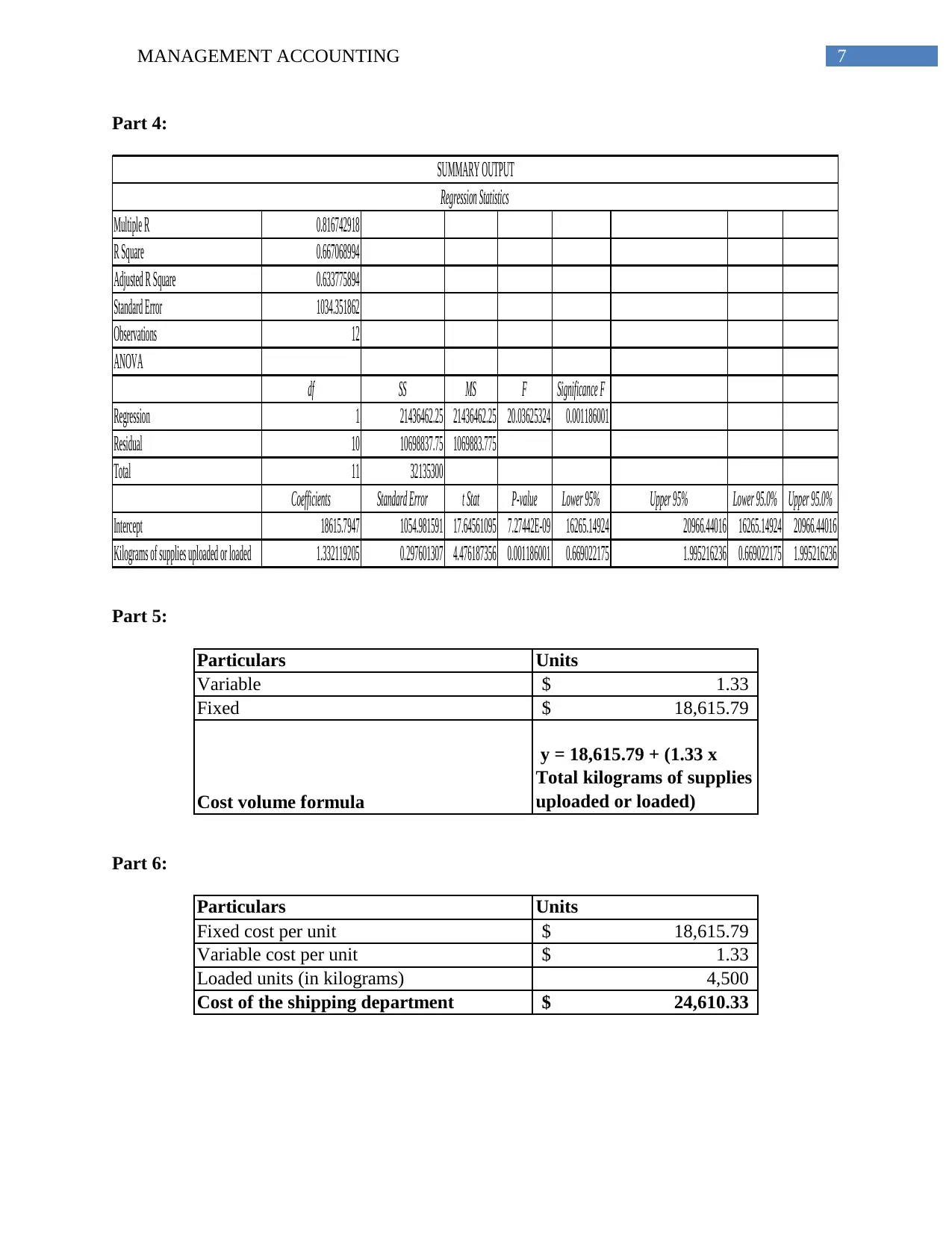

Part 4:

Multiple R 0.816742918

R Square 0.667068994

Adjusted R Square 0.633775894

Standard Error 1034.351862

Observations 12

ANOVA

df SS MS F Significance F

Regression 1 21436462.25 21436462.25 20.03625324 0.001186001

Residual 10 10698837.75 1069883.775

Total 11 32135300

Coefficients Standard Error t Stat P-value Lower 95% Upper 95% Lower 95.0% Upper 95.0%

Intercept 18615.7947 1054.981591 17.64561095 7.27442E-09 16265.14924 20966.44016 16265.14924 20966.44016

Kilograms of supplies uploaded or loaded 1.332119205 0.297601307 4.476187356 0.001186001 0.669022175 1.995216236 0.669022175 1.995216236

Regression Statistics

SUMMARY OUTPUT

Part 5:

Particulars Units

Variable 1.33$

Fixed 18,615.79$

Cost volume formula

y = 18,615.79 + (1.33 x

Total kilograms of supplies

uploaded or loaded)

Part 6:

Particulars Units

Fixed cost per unit 18,615.79$

Variable cost per unit 1.33$

Loaded units (in kilograms) 4,500

Cost of the shipping department 24,610.33$

Part 4:

Multiple R 0.816742918

R Square 0.667068994

Adjusted R Square 0.633775894

Standard Error 1034.351862

Observations 12

ANOVA

df SS MS F Significance F

Regression 1 21436462.25 21436462.25 20.03625324 0.001186001

Residual 10 10698837.75 1069883.775

Total 11 32135300

Coefficients Standard Error t Stat P-value Lower 95% Upper 95% Lower 95.0% Upper 95.0%

Intercept 18615.7947 1054.981591 17.64561095 7.27442E-09 16265.14924 20966.44016 16265.14924 20966.44016

Kilograms of supplies uploaded or loaded 1.332119205 0.297601307 4.476187356 0.001186001 0.669022175 1.995216236 0.669022175 1.995216236

Regression Statistics

SUMMARY OUTPUT

Part 5:

Particulars Units

Variable 1.33$

Fixed 18,615.79$

Cost volume formula

y = 18,615.79 + (1.33 x

Total kilograms of supplies

uploaded or loaded)

Part 6:

Particulars Units

Fixed cost per unit 18,615.79$

Variable cost per unit 1.33$

Loaded units (in kilograms) 4,500

Cost of the shipping department 24,610.33$

8MANAGEMENT ACCOUNTING

Part 7:

The high-low method considers two data points, which might not always signify the

general data trend. On the other hand, all data points are taken into consideration in least square

regression method and thus, more accurate results could be expected, which indicates its

superiority over the high-low method.

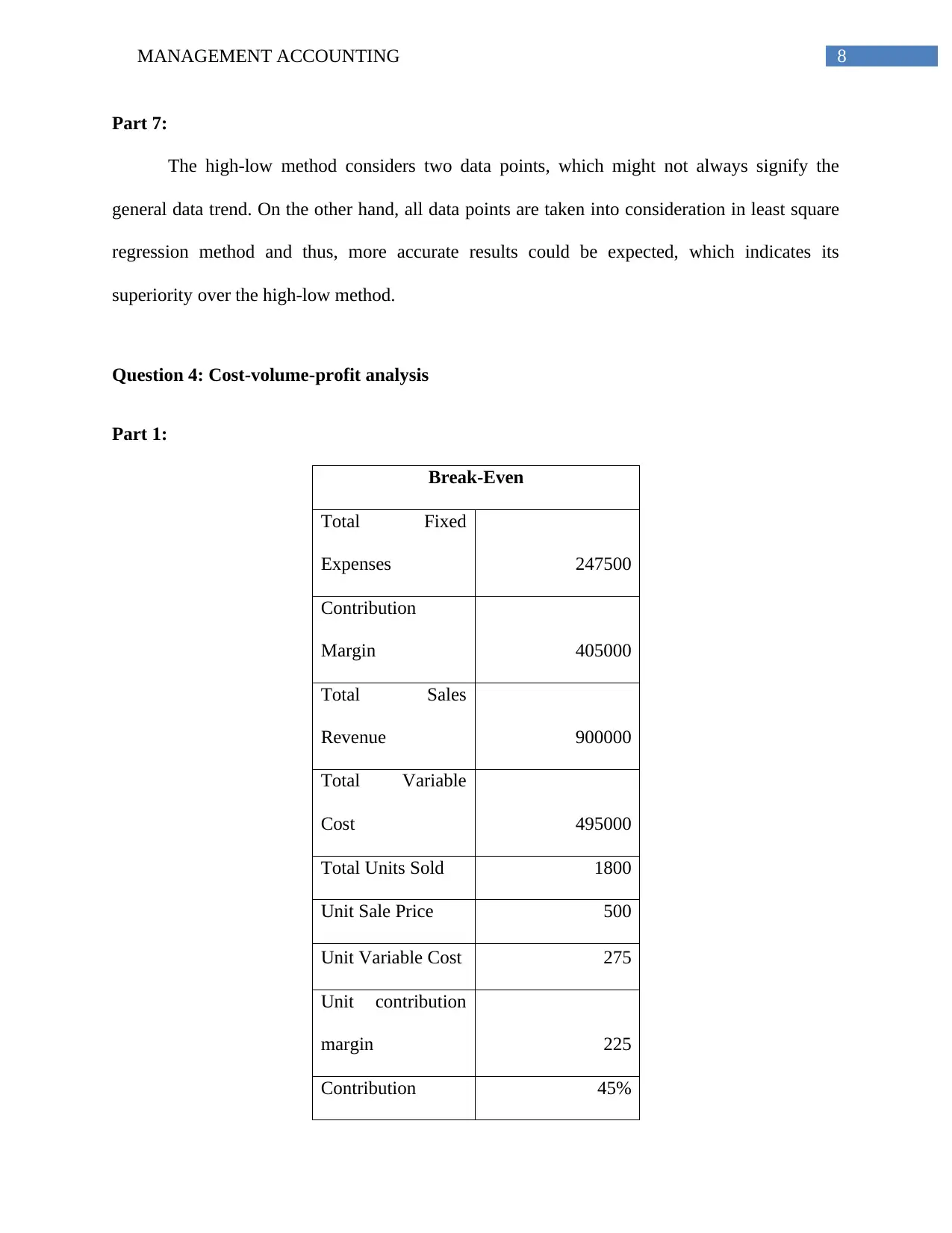

Question 4: Cost-volume-profit analysis

Part 1:

Break-Even

Total Fixed

Expenses 247500

Contribution

Margin 405000

Total Sales

Revenue 900000

Total Variable

Cost 495000

Total Units Sold 1800

Unit Sale Price 500

Unit Variable Cost 275

Unit contribution

margin 225

Contribution 45%

Part 7:

The high-low method considers two data points, which might not always signify the

general data trend. On the other hand, all data points are taken into consideration in least square

regression method and thus, more accurate results could be expected, which indicates its

superiority over the high-low method.

Question 4: Cost-volume-profit analysis

Part 1:

Break-Even

Total Fixed

Expenses 247500

Contribution

Margin 405000

Total Sales

Revenue 900000

Total Variable

Cost 495000

Total Units Sold 1800

Unit Sale Price 500

Unit Variable Cost 275

Unit contribution

margin 225

Contribution 45%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING

Margin Ratio

Break Even in

Tonnes (units) 1100

Break Even in

Dollars 550000

Part 2:

Profit Expected in

the next year

Total Fixed

Expenses 247500

Estimated

Sales (units) 2100

Unit Sale

Price 500

Unit

Variable

Cost 275

Net Profit 225000

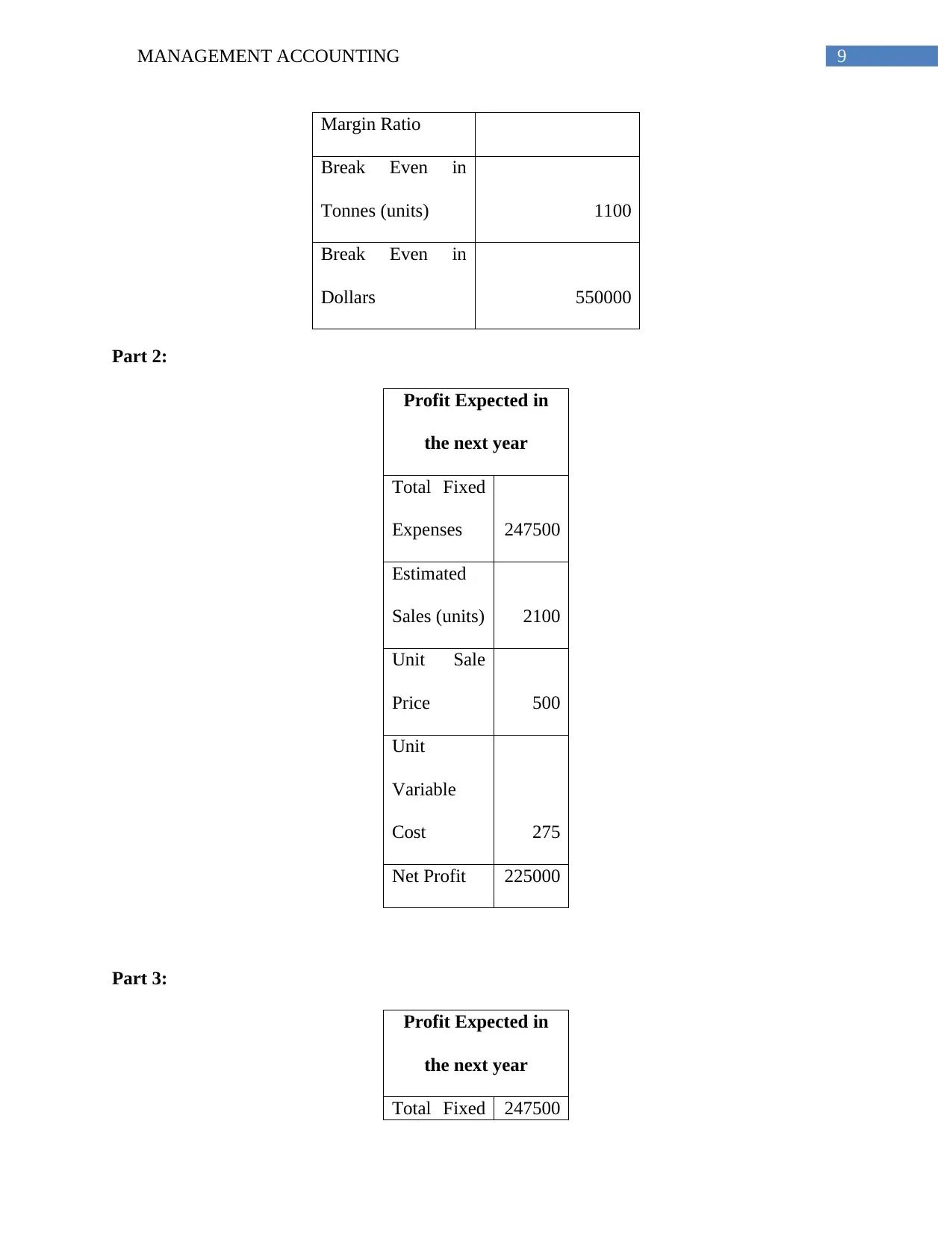

Part 3:

Profit Expected in

the next year

Total Fixed 247500

Margin Ratio

Break Even in

Tonnes (units) 1100

Break Even in

Dollars 550000

Part 2:

Profit Expected in

the next year

Total Fixed

Expenses 247500

Estimated

Sales (units) 2100

Unit Sale

Price 500

Unit

Variable

Cost 275

Net Profit 225000

Part 3:

Profit Expected in

the next year

Total Fixed 247500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING

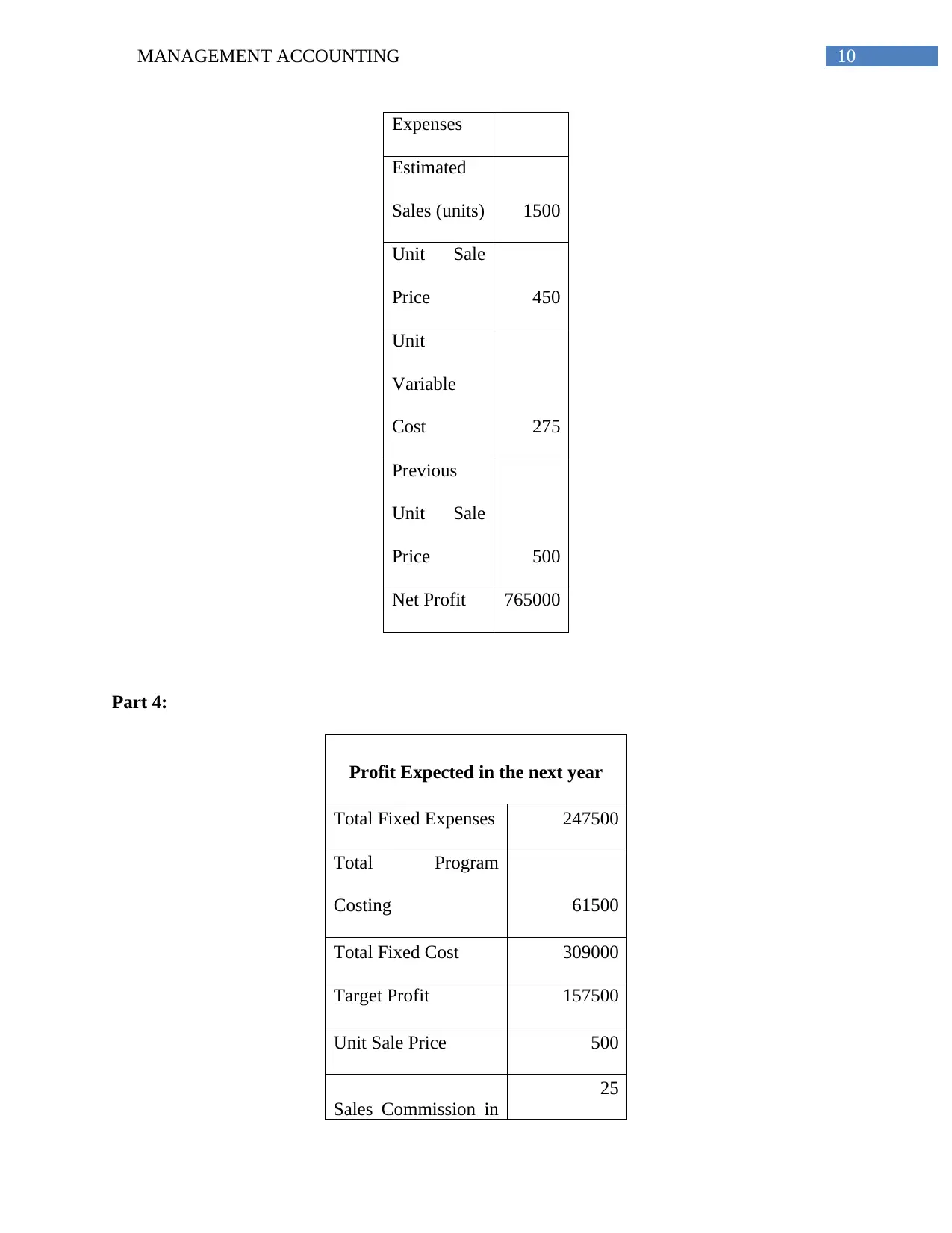

Expenses

Estimated

Sales (units) 1500

Unit Sale

Price 450

Unit

Variable

Cost 275

Previous

Unit Sale

Price 500

Net Profit 765000

Part 4:

Profit Expected in the next year

Total Fixed Expenses 247500

Total Program

Costing 61500

Total Fixed Cost 309000

Target Profit 157500

Unit Sale Price 500

Sales Commission in

25

Expenses

Estimated

Sales (units) 1500

Unit Sale

Price 450

Unit

Variable

Cost 275

Previous

Unit Sale

Price 500

Net Profit 765000

Part 4:

Profit Expected in the next year

Total Fixed Expenses 247500

Total Program

Costing 61500

Total Fixed Cost 309000

Target Profit 157500

Unit Sale Price 500

Sales Commission in

25

11MANAGEMENT ACCOUNTING

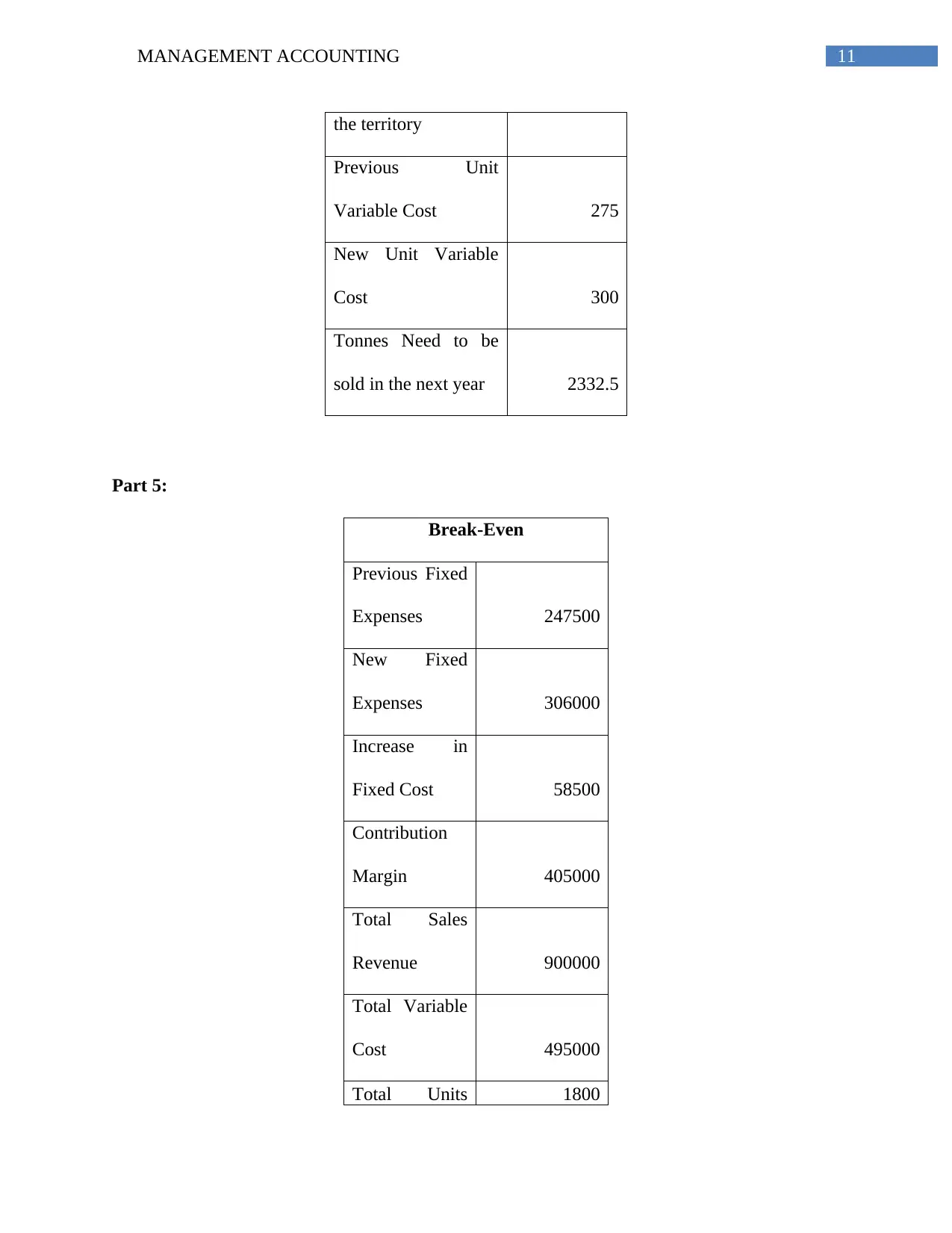

the territory

Previous Unit

Variable Cost 275

New Unit Variable

Cost 300

Tonnes Need to be

sold in the next year 2332.5

Part 5:

Break-Even

Previous Fixed

Expenses 247500

New Fixed

Expenses 306000

Increase in

Fixed Cost 58500

Contribution

Margin 405000

Total Sales

Revenue 900000

Total Variable

Cost 495000

Total Units 1800

the territory

Previous Unit

Variable Cost 275

New Unit Variable

Cost 300

Tonnes Need to be

sold in the next year 2332.5

Part 5:

Break-Even

Previous Fixed

Expenses 247500

New Fixed

Expenses 306000

Increase in

Fixed Cost 58500

Contribution

Margin 405000

Total Sales

Revenue 900000

Total Variable

Cost 495000

Total Units 1800

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.