MAA262 Assessment 2: Individual Assignment - Management Accounting

VerifiedAdded on 2022/10/18

|16

|3265

|117

Homework Assignment

AI Summary

This document presents a comprehensive solution to a management accounting assignment, addressing various aspects of cost analysis, budgeting, and ethical considerations. The assignment explores a case study involving a company's cost structure, quality management, and overhead allocation. It delves into ethical standards for management accountants, the classification of quality costs (prevention, appraisal, internal failure, and external failure), and the importance of long-term quality management strategies. The solution also includes the high-low method for analyzing delivery expenses, and calculation of predetermined overhead rates, and the application of overhead costs to a specific job. The assignment also considers the allocation of overhead costs and comparisons to industry benchmarks. This detailed solution is designed to help students understand and apply management accounting principles in a practical context.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING

Table of Contents

Answer to question 1:......................................................................................................................2

Answer to question 2:......................................................................................................................3

Sub part (a):.................................................................................................................................3

Sub part (b):.................................................................................................................................4

Answer to question 3:......................................................................................................................5

Sub part (a):.................................................................................................................................5

Sub part (b):.................................................................................................................................6

Answer to question 4:......................................................................................................................6

Sub part (a):.................................................................................................................................6

Sub part (b):.................................................................................................................................7

Answer to question 5:......................................................................................................................8

Sub part (a):.................................................................................................................................8

Sub part (b):.................................................................................................................................8

Sub part (c):.................................................................................................................................9

Sub part (d):.................................................................................................................................9

Sub part (e):.................................................................................................................................9

Answer to question 6:....................................................................................................................10

Sub part (a):...............................................................................................................................10

Table of Contents

Answer to question 1:......................................................................................................................2

Answer to question 2:......................................................................................................................3

Sub part (a):.................................................................................................................................3

Sub part (b):.................................................................................................................................4

Answer to question 3:......................................................................................................................5

Sub part (a):.................................................................................................................................5

Sub part (b):.................................................................................................................................6

Answer to question 4:......................................................................................................................6

Sub part (a):.................................................................................................................................6

Sub part (b):.................................................................................................................................7

Answer to question 5:......................................................................................................................8

Sub part (a):.................................................................................................................................8

Sub part (b):.................................................................................................................................8

Sub part (c):.................................................................................................................................9

Sub part (d):.................................................................................................................................9

Sub part (e):.................................................................................................................................9

Answer to question 6:....................................................................................................................10

Sub part (a):...............................................................................................................................10

2MANAGEMENT ACCOUNTING

Sub part (b):...............................................................................................................................10

Answer to question 7:....................................................................................................................11

Sub part (a):...............................................................................................................................11

Sub part (b):...............................................................................................................................11

References and bibliography:........................................................................................................13

Sub part (b):...............................................................................................................................10

Answer to question 7:....................................................................................................................11

Sub part (a):...............................................................................................................................11

Sub part (b):...............................................................................................................................11

References and bibliography:........................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING

Answer to question 1:

In the given case study, Mr. John has hired Mr. Gorge who is a plumber by his profession

for the post of management account who will be analyzing the costs structure of the company to

find out the reasons for unnecessary costs and strategies to reduce those costs. Institute of

Management Accountants is the prime body of professional Management Accountants. IMA

have issued a statement of ethical standards, which needs to be followed by the professional

management accounts (Imanet.org 2019). The statement includes four ethical standards,

Competence, Confidentiality, Integrity and Credibility. The most important ethical standard is

the Competence, which requires the management accountant should have appropriate

professional expertise, knowledge and skill. In the given case study, Mr. George is a plumber

who have been appointed as the management accountant, hence the ethical standard of

competence have been jeopardized.

Further, the competence standard requires the management accountant to perform

respective duties in accordance with the applicable laws, regulations and standards. If a

management accountant does not have such competencies and knowledge about the respective

laws, regulations and technical standards, then the management accountant would not be able to

perform his duties deliver his obligations properly.

Being unable to analyze the cost accounting information and cost related data the

management accountant would be failing to provide adequate, clear and accurate decisions

support information, which is the intended objective of appointment of a management

accountant. Hence, the appointment of Mr. George by Mr. John for the post of Management

Answer to question 1:

In the given case study, Mr. John has hired Mr. Gorge who is a plumber by his profession

for the post of management account who will be analyzing the costs structure of the company to

find out the reasons for unnecessary costs and strategies to reduce those costs. Institute of

Management Accountants is the prime body of professional Management Accountants. IMA

have issued a statement of ethical standards, which needs to be followed by the professional

management accounts (Imanet.org 2019). The statement includes four ethical standards,

Competence, Confidentiality, Integrity and Credibility. The most important ethical standard is

the Competence, which requires the management accountant should have appropriate

professional expertise, knowledge and skill. In the given case study, Mr. George is a plumber

who have been appointed as the management accountant, hence the ethical standard of

competence have been jeopardized.

Further, the competence standard requires the management accountant to perform

respective duties in accordance with the applicable laws, regulations and standards. If a

management accountant does not have such competencies and knowledge about the respective

laws, regulations and technical standards, then the management accountant would not be able to

perform his duties deliver his obligations properly.

Being unable to analyze the cost accounting information and cost related data the

management accountant would be failing to provide adequate, clear and accurate decisions

support information, which is the intended objective of appointment of a management

accountant. Hence, the appointment of Mr. George by Mr. John for the post of Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING

accountant has been jeopardized the Competence ethical standard of the IMA statement of

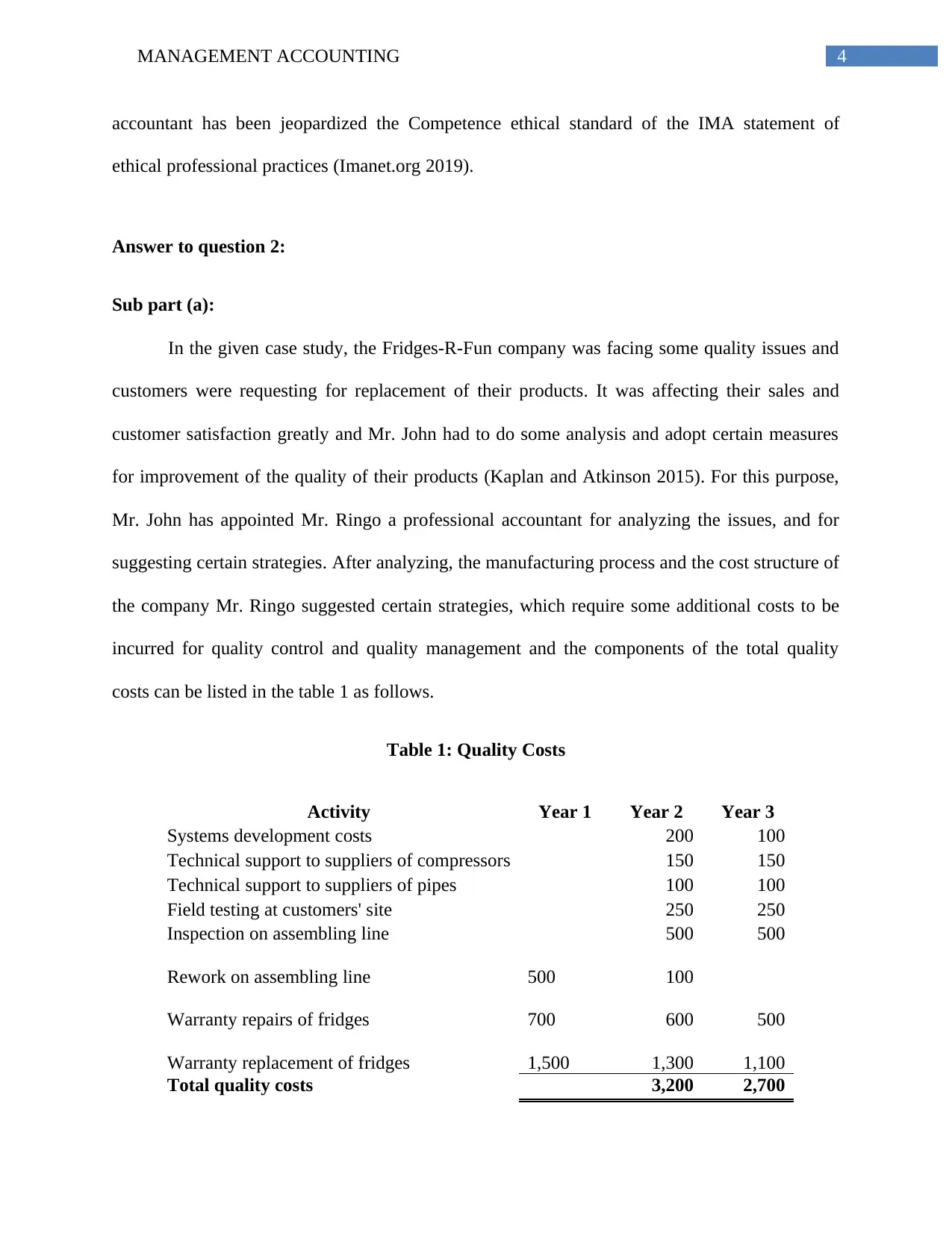

ethical professional practices (Imanet.org 2019).

Answer to question 2:

Sub part (a):

In the given case study, the Fridges-R-Fun company was facing some quality issues and

customers were requesting for replacement of their products. It was affecting their sales and

customer satisfaction greatly and Mr. John had to do some analysis and adopt certain measures

for improvement of the quality of their products (Kaplan and Atkinson 2015). For this purpose,

Mr. John has appointed Mr. Ringo a professional accountant for analyzing the issues, and for

suggesting certain strategies. After analyzing, the manufacturing process and the cost structure of

the company Mr. Ringo suggested certain strategies, which require some additional costs to be

incurred for quality control and quality management and the components of the total quality

costs can be listed in the table 1 as follows.

Table 1: Quality Costs

Activity Year 1 Year 2 Year 3

Systems development costs 200 100

Technical support to suppliers of compressors 150 150

Technical support to suppliers of pipes 100 100

Field testing at customers' site 250 250

Inspection on assembling line 500 500

Rework on assembling line 500 100

Warranty repairs of fridges 700 600 500

Warranty replacement of fridges 1,500 1,300 1,100

Total quality costs 3,200 2,700

accountant has been jeopardized the Competence ethical standard of the IMA statement of

ethical professional practices (Imanet.org 2019).

Answer to question 2:

Sub part (a):

In the given case study, the Fridges-R-Fun company was facing some quality issues and

customers were requesting for replacement of their products. It was affecting their sales and

customer satisfaction greatly and Mr. John had to do some analysis and adopt certain measures

for improvement of the quality of their products (Kaplan and Atkinson 2015). For this purpose,

Mr. John has appointed Mr. Ringo a professional accountant for analyzing the issues, and for

suggesting certain strategies. After analyzing, the manufacturing process and the cost structure of

the company Mr. Ringo suggested certain strategies, which require some additional costs to be

incurred for quality control and quality management and the components of the total quality

costs can be listed in the table 1 as follows.

Table 1: Quality Costs

Activity Year 1 Year 2 Year 3

Systems development costs 200 100

Technical support to suppliers of compressors 150 150

Technical support to suppliers of pipes 100 100

Field testing at customers' site 250 250

Inspection on assembling line 500 500

Rework on assembling line 500 100

Warranty repairs of fridges 700 600 500

Warranty replacement of fridges 1,500 1,300 1,100

Total quality costs 3,200 2,700

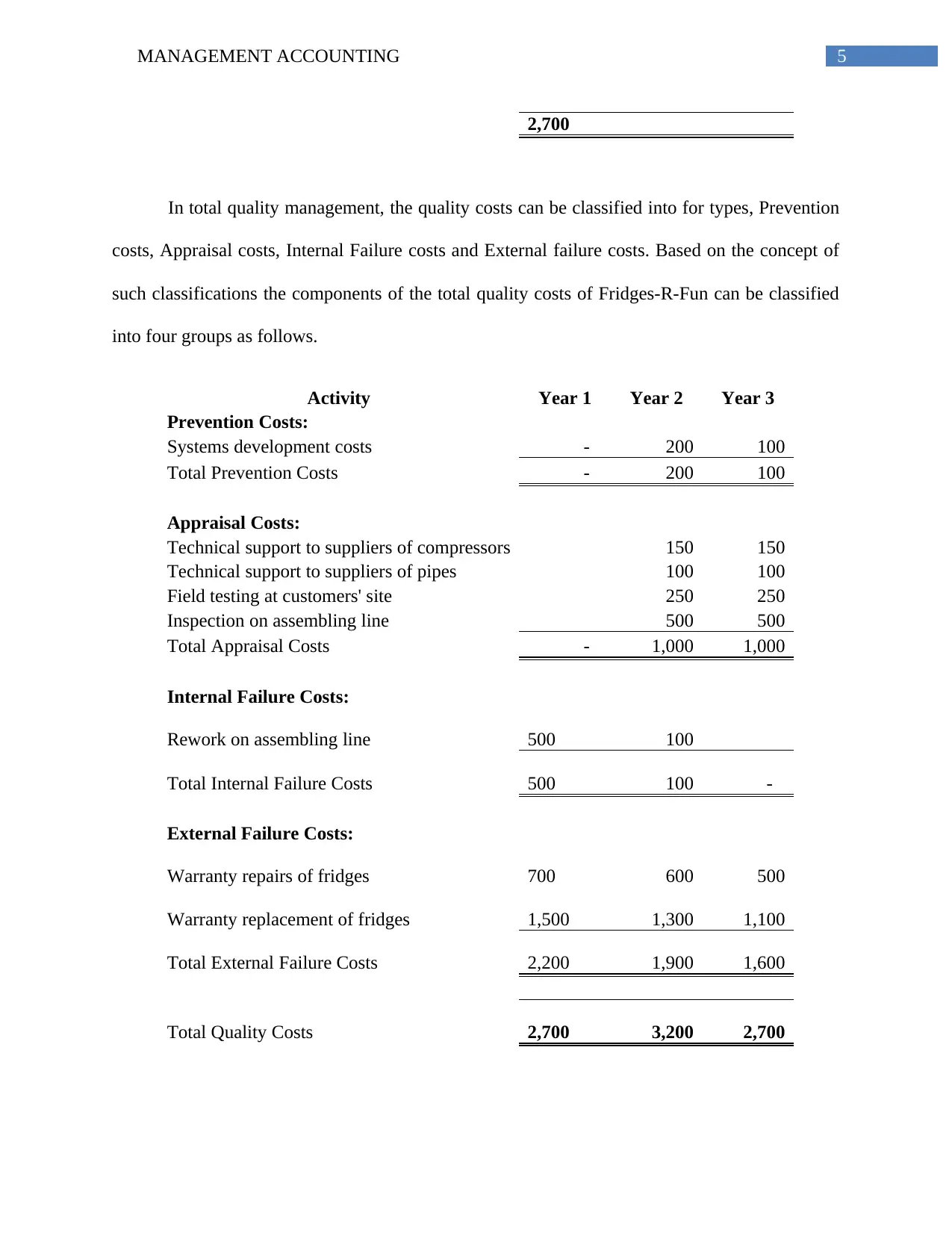

5MANAGEMENT ACCOUNTING

2,700

In total quality management, the quality costs can be classified into for types, Prevention

costs, Appraisal costs, Internal Failure costs and External failure costs. Based on the concept of

such classifications the components of the total quality costs of Fridges-R-Fun can be classified

into four groups as follows.

Activity Year 1 Year 2 Year 3

Prevention Costs:

Systems development costs - 200 100

Total Prevention Costs - 200 100

Appraisal Costs:

Technical support to suppliers of compressors 150 150

Technical support to suppliers of pipes 100 100

Field testing at customers' site 250 250

Inspection on assembling line 500 500

Total Appraisal Costs - 1,000 1,000

Internal Failure Costs:

Rework on assembling line 500 100

Total Internal Failure Costs 500 100 -

External Failure Costs:

Warranty repairs of fridges 700 600 500

Warranty replacement of fridges 1,500 1,300 1,100

Total External Failure Costs 2,200 1,900 1,600

Total Quality Costs 2,700 3,200 2,700

2,700

In total quality management, the quality costs can be classified into for types, Prevention

costs, Appraisal costs, Internal Failure costs and External failure costs. Based on the concept of

such classifications the components of the total quality costs of Fridges-R-Fun can be classified

into four groups as follows.

Activity Year 1 Year 2 Year 3

Prevention Costs:

Systems development costs - 200 100

Total Prevention Costs - 200 100

Appraisal Costs:

Technical support to suppliers of compressors 150 150

Technical support to suppliers of pipes 100 100

Field testing at customers' site 250 250

Inspection on assembling line 500 500

Total Appraisal Costs - 1,000 1,000

Internal Failure Costs:

Rework on assembling line 500 100

Total Internal Failure Costs 500 100 -

External Failure Costs:

Warranty repairs of fridges 700 600 500

Warranty replacement of fridges 1,500 1,300 1,100

Total External Failure Costs 2,200 1,900 1,600

Total Quality Costs 2,700 3,200 2,700

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING

Sub part (b):

The prevention cost includes costs related to some preventive measures, which are taken

for reducing the number of defects and for improvement in the quality of the products. It

includes the product development and design costs and other services, which are incurred far

advance before the manufacturing with an intention to reduce the possible defects in the output.

With the achievement in efficiency, the prevention costs decreases. Appraisal costs are incurred

for testing and inspecting the materials coming into the production line and going out from the

production line (Kaplan and Atkinson 2015). It is a continuous process and costs related to such

activities are variable in nature. With the increase in volume of output, the appraisal cost also

increases. Internal failure cost includes the rework costs and costs related to minor rectifications

done within the manufacturing process. Initially the internal failure cost becomes high and

gradually it decreases with the increase in efficiency and effectiveness of the prevention policies.

The external failure costs are extensive in nature, which are incurred to replace and rework the

products after it has been sold to the customers. Like the internal failure costs, the external

failure costs also decrease with the improvement in quality and with the increase in effectiveness

of the preventive measures (Kaplan and Atkinson 2015).

Answer to question 3:

Sub part (a):

Quality management is a long-term process and takes time to be effective in practice and

to give a positive result. In the initial stage, some amount needs to be invested in the preventive

measures such as process reengineering and product designing, and after applying the new

design and new manufacturing process, a continuous efforts needs to be given in testing and

Sub part (b):

The prevention cost includes costs related to some preventive measures, which are taken

for reducing the number of defects and for improvement in the quality of the products. It

includes the product development and design costs and other services, which are incurred far

advance before the manufacturing with an intention to reduce the possible defects in the output.

With the achievement in efficiency, the prevention costs decreases. Appraisal costs are incurred

for testing and inspecting the materials coming into the production line and going out from the

production line (Kaplan and Atkinson 2015). It is a continuous process and costs related to such

activities are variable in nature. With the increase in volume of output, the appraisal cost also

increases. Internal failure cost includes the rework costs and costs related to minor rectifications

done within the manufacturing process. Initially the internal failure cost becomes high and

gradually it decreases with the increase in efficiency and effectiveness of the prevention policies.

The external failure costs are extensive in nature, which are incurred to replace and rework the

products after it has been sold to the customers. Like the internal failure costs, the external

failure costs also decrease with the improvement in quality and with the increase in effectiveness

of the preventive measures (Kaplan and Atkinson 2015).

Answer to question 3:

Sub part (a):

Quality management is a long-term process and takes time to be effective in practice and

to give a positive result. In the initial stage, some amount needs to be invested in the preventive

measures such as process reengineering and product designing, and after applying the new

design and new manufacturing process, a continuous efforts needs to be given in testing and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING

inspecting the incoming and outgoing materials, which constitutes the appraisal costs (Kaplan

and Atkinson 2015). Mr. John thinks that, the quality management is a short-term process and he

expects the results promptly. On the other hand, Mr. Ringo thinks that, the quality management

is a long-term process and initially there would be a huge investment but with the application of

the strategies and initiatives, the total quality costs will be decreasing gradually. Being a

professional management accountant Mr. Ringo has argued the right concept of the total quality

management.

Sub part (b):

If Mr. Ringo’s decisions are kept then in the fourth year it is expected that the internal

and external failure costs will decrease by a significant margin which in turn reduce the total

quality costs to certain extent.

If Mr. Ringo’s decisions are cancelled then, though there would be no prevention costs

and appraisal cost, but the failure costs would be increased to significant level. Therefore, it can

be recommended for the company to keep the decisions and adopt the strategies as suggested by

Mr. Ringo.

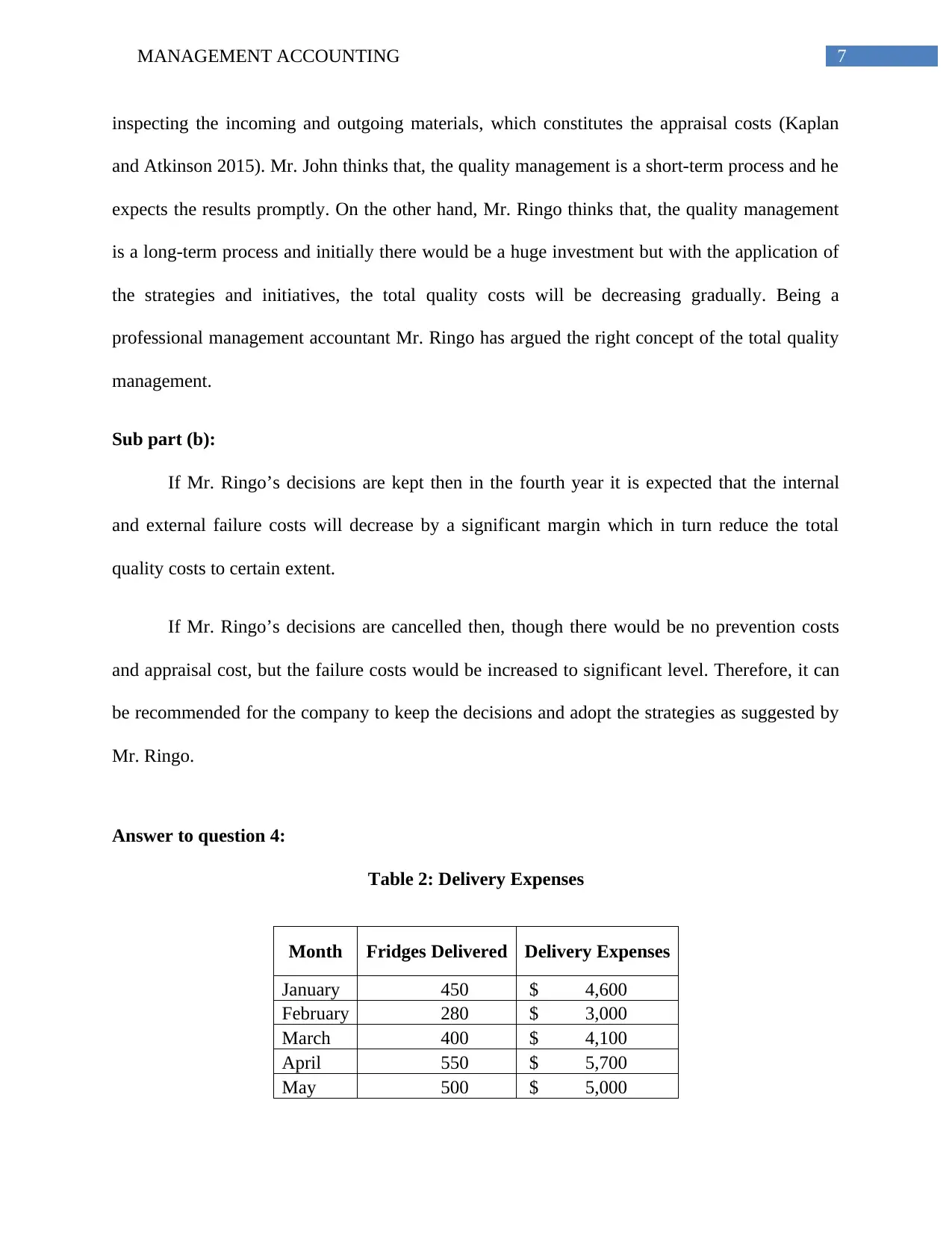

Answer to question 4:

Table 2: Delivery Expenses

Month Fridges Delivered Delivery Expenses

January 450 $ 4,600

February 280 $ 3,000

March 400 $ 4,100

April 550 $ 5,700

May 500 $ 5,000

inspecting the incoming and outgoing materials, which constitutes the appraisal costs (Kaplan

and Atkinson 2015). Mr. John thinks that, the quality management is a short-term process and he

expects the results promptly. On the other hand, Mr. Ringo thinks that, the quality management

is a long-term process and initially there would be a huge investment but with the application of

the strategies and initiatives, the total quality costs will be decreasing gradually. Being a

professional management accountant Mr. Ringo has argued the right concept of the total quality

management.

Sub part (b):

If Mr. Ringo’s decisions are kept then in the fourth year it is expected that the internal

and external failure costs will decrease by a significant margin which in turn reduce the total

quality costs to certain extent.

If Mr. Ringo’s decisions are cancelled then, though there would be no prevention costs

and appraisal cost, but the failure costs would be increased to significant level. Therefore, it can

be recommended for the company to keep the decisions and adopt the strategies as suggested by

Mr. Ringo.

Answer to question 4:

Table 2: Delivery Expenses

Month Fridges Delivered Delivery Expenses

January 450 $ 4,600

February 280 $ 3,000

March 400 $ 4,100

April 550 $ 5,700

May 500 $ 5,000

8MANAGEMENT ACCOUNTING

June 450 $ 4,700

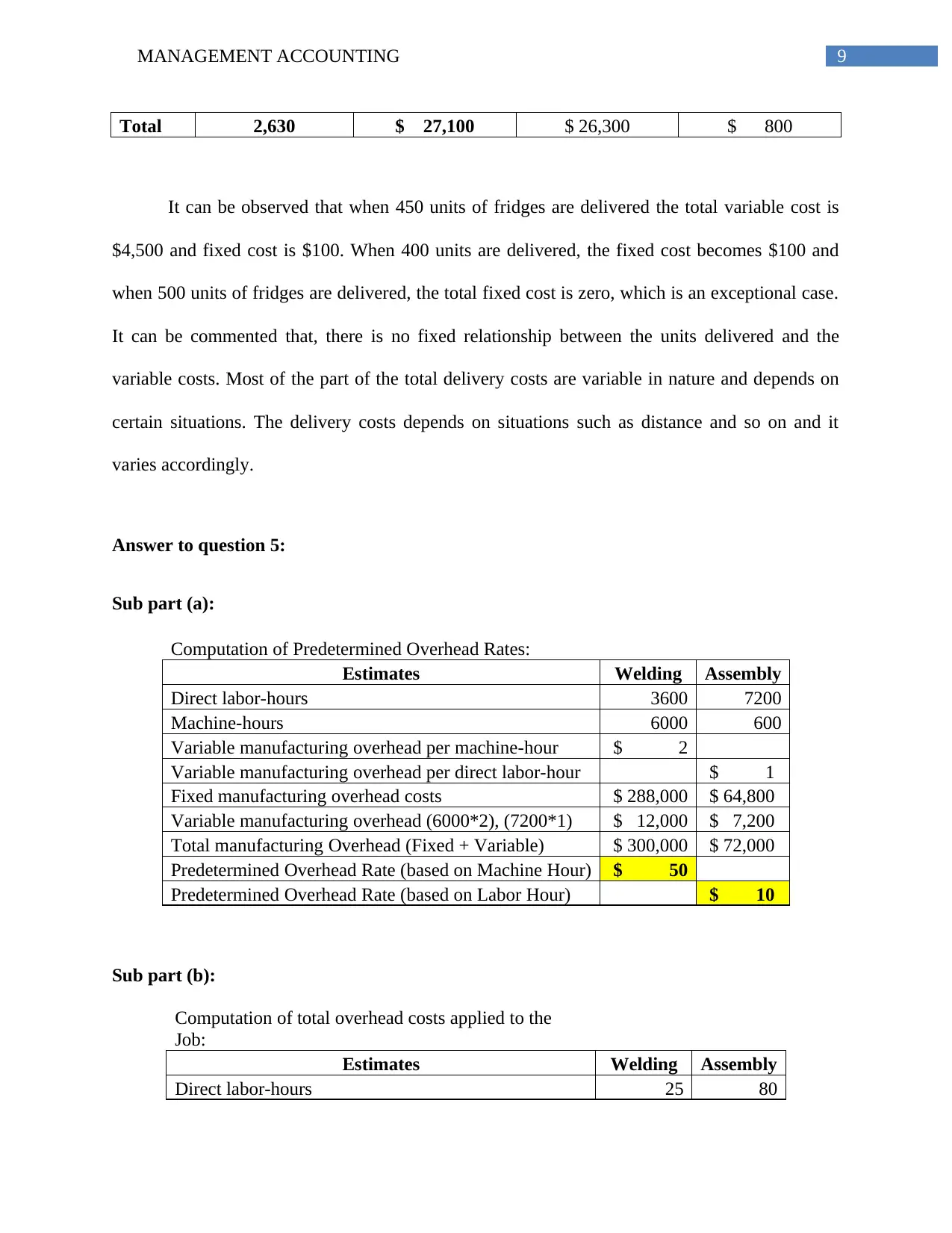

Total 2,630 $ 27,100

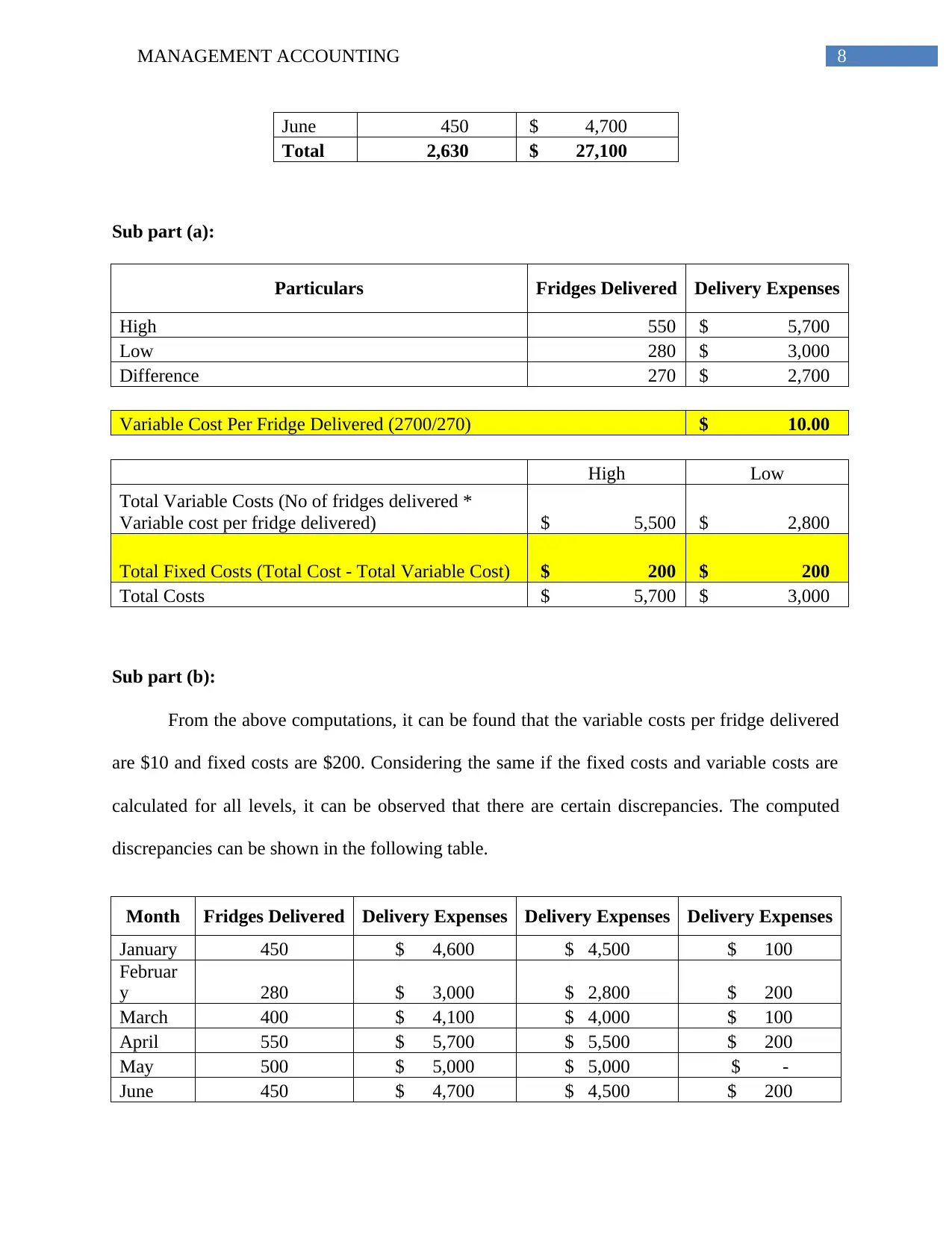

Sub part (a):

Particulars Fridges Delivered Delivery Expenses

High 550 $ 5,700

Low 280 $ 3,000

Difference 270 $ 2,700

Variable Cost Per Fridge Delivered (2700/270) $ 10.00

High Low

Total Variable Costs (No of fridges delivered *

Variable cost per fridge delivered) $ 5,500 $ 2,800

Total Fixed Costs (Total Cost - Total Variable Cost) $ 200 $ 200

Total Costs $ 5,700 $ 3,000

Sub part (b):

From the above computations, it can be found that the variable costs per fridge delivered

are $10 and fixed costs are $200. Considering the same if the fixed costs and variable costs are

calculated for all levels, it can be observed that there are certain discrepancies. The computed

discrepancies can be shown in the following table.

Month Fridges Delivered Delivery Expenses Delivery Expenses Delivery Expenses

January 450 $ 4,600 $ 4,500 $ 100

Februar

y 280 $ 3,000 $ 2,800 $ 200

March 400 $ 4,100 $ 4,000 $ 100

April 550 $ 5,700 $ 5,500 $ 200

May 500 $ 5,000 $ 5,000 $ -

June 450 $ 4,700 $ 4,500 $ 200

June 450 $ 4,700

Total 2,630 $ 27,100

Sub part (a):

Particulars Fridges Delivered Delivery Expenses

High 550 $ 5,700

Low 280 $ 3,000

Difference 270 $ 2,700

Variable Cost Per Fridge Delivered (2700/270) $ 10.00

High Low

Total Variable Costs (No of fridges delivered *

Variable cost per fridge delivered) $ 5,500 $ 2,800

Total Fixed Costs (Total Cost - Total Variable Cost) $ 200 $ 200

Total Costs $ 5,700 $ 3,000

Sub part (b):

From the above computations, it can be found that the variable costs per fridge delivered

are $10 and fixed costs are $200. Considering the same if the fixed costs and variable costs are

calculated for all levels, it can be observed that there are certain discrepancies. The computed

discrepancies can be shown in the following table.

Month Fridges Delivered Delivery Expenses Delivery Expenses Delivery Expenses

January 450 $ 4,600 $ 4,500 $ 100

Februar

y 280 $ 3,000 $ 2,800 $ 200

March 400 $ 4,100 $ 4,000 $ 100

April 550 $ 5,700 $ 5,500 $ 200

May 500 $ 5,000 $ 5,000 $ -

June 450 $ 4,700 $ 4,500 $ 200

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING

Total 2,630 $ 27,100 $ 26,300 $ 800

It can be observed that when 450 units of fridges are delivered the total variable cost is

$4,500 and fixed cost is $100. When 400 units are delivered, the fixed cost becomes $100 and

when 500 units of fridges are delivered, the total fixed cost is zero, which is an exceptional case.

It can be commented that, there is no fixed relationship between the units delivered and the

variable costs. Most of the part of the total delivery costs are variable in nature and depends on

certain situations. The delivery costs depends on situations such as distance and so on and it

varies accordingly.

Answer to question 5:

Sub part (a):

Computation of Predetermined Overhead Rates:

Estimates Welding Assembly

Direct labor-hours 3600 7200

Machine-hours 6000 600

Variable manufacturing overhead per machine-hour $ 2

Variable manufacturing overhead per direct labor-hour $ 1

Fixed manufacturing overhead costs $ 288,000 $ 64,800

Variable manufacturing overhead (6000*2), (7200*1) $ 12,000 $ 7,200

Total manufacturing Overhead (Fixed + Variable) $ 300,000 $ 72,000

Predetermined Overhead Rate (based on Machine Hour) $ 50

Predetermined Overhead Rate (based on Labor Hour) $ 10

Sub part (b):

Computation of total overhead costs applied to the

Job:

Estimates Welding Assembly

Direct labor-hours 25 80

Total 2,630 $ 27,100 $ 26,300 $ 800

It can be observed that when 450 units of fridges are delivered the total variable cost is

$4,500 and fixed cost is $100. When 400 units are delivered, the fixed cost becomes $100 and

when 500 units of fridges are delivered, the total fixed cost is zero, which is an exceptional case.

It can be commented that, there is no fixed relationship between the units delivered and the

variable costs. Most of the part of the total delivery costs are variable in nature and depends on

certain situations. The delivery costs depends on situations such as distance and so on and it

varies accordingly.

Answer to question 5:

Sub part (a):

Computation of Predetermined Overhead Rates:

Estimates Welding Assembly

Direct labor-hours 3600 7200

Machine-hours 6000 600

Variable manufacturing overhead per machine-hour $ 2

Variable manufacturing overhead per direct labor-hour $ 1

Fixed manufacturing overhead costs $ 288,000 $ 64,800

Variable manufacturing overhead (6000*2), (7200*1) $ 12,000 $ 7,200

Total manufacturing Overhead (Fixed + Variable) $ 300,000 $ 72,000

Predetermined Overhead Rate (based on Machine Hour) $ 50

Predetermined Overhead Rate (based on Labor Hour) $ 10

Sub part (b):

Computation of total overhead costs applied to the

Job:

Estimates Welding Assembly

Direct labor-hours 25 80

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING

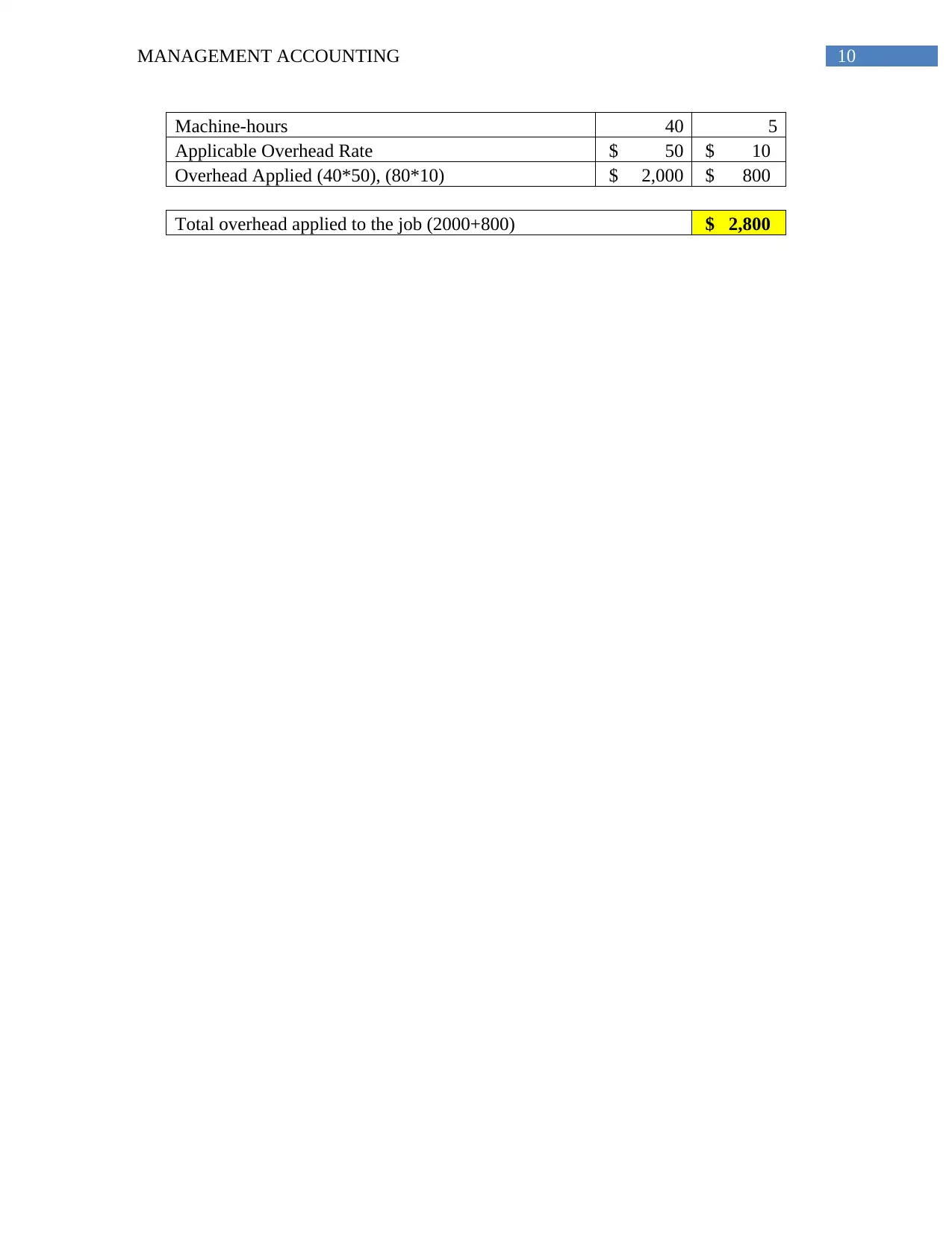

Machine-hours 40 5

Applicable Overhead Rate $ 50 $ 10

Overhead Applied (40*50), (80*10) $ 2,000 $ 800

Total overhead applied to the job (2000+800) $ 2,800

Machine-hours 40 5

Applicable Overhead Rate $ 50 $ 10

Overhead Applied (40*50), (80*10) $ 2,000 $ 800

Total overhead applied to the job (2000+800) $ 2,800

11MANAGEMENT ACCOUNTING

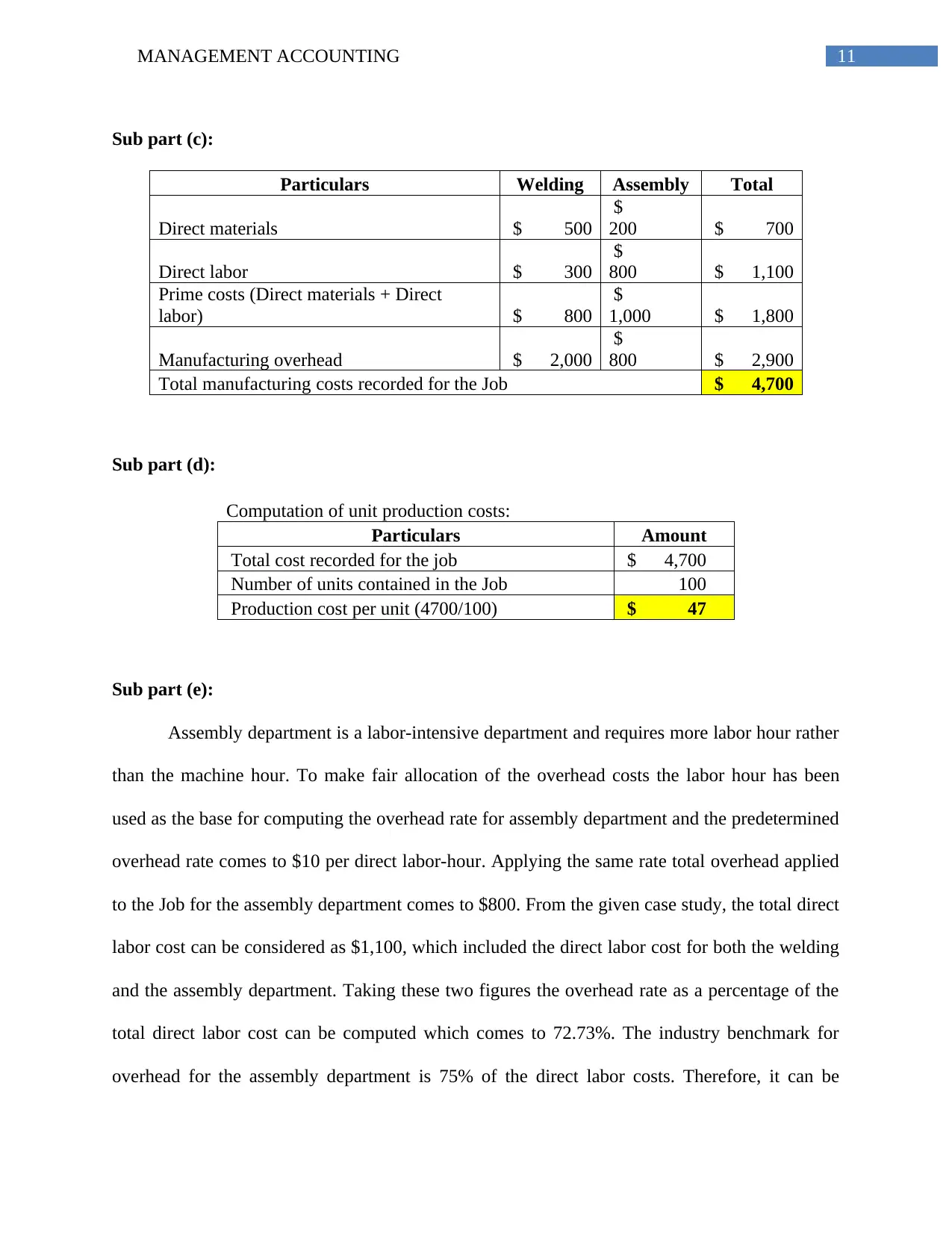

Sub part (c):

Particulars Welding Assembly Total

Direct materials $ 500

$

200 $ 700

Direct labor $ 300

$

800 $ 1,100

Prime costs (Direct materials + Direct

labor) $ 800

$

1,000 $ 1,800

Manufacturing overhead $ 2,000

$

800 $ 2,900

Total manufacturing costs recorded for the Job $ 4,700

Sub part (d):

Computation of unit production costs:

Particulars Amount

Total cost recorded for the job $ 4,700

Number of units contained in the Job 100

Production cost per unit (4700/100) $ 47

Sub part (e):

Assembly department is a labor-intensive department and requires more labor hour rather

than the machine hour. To make fair allocation of the overhead costs the labor hour has been

used as the base for computing the overhead rate for assembly department and the predetermined

overhead rate comes to $10 per direct labor-hour. Applying the same rate total overhead applied

to the Job for the assembly department comes to $800. From the given case study, the total direct

labor cost can be considered as $1,100, which included the direct labor cost for both the welding

and the assembly department. Taking these two figures the overhead rate as a percentage of the

total direct labor cost can be computed which comes to 72.73%. The industry benchmark for

overhead for the assembly department is 75% of the direct labor costs. Therefore, it can be

Sub part (c):

Particulars Welding Assembly Total

Direct materials $ 500

$

200 $ 700

Direct labor $ 300

$

800 $ 1,100

Prime costs (Direct materials + Direct

labor) $ 800

$

1,000 $ 1,800

Manufacturing overhead $ 2,000

$

800 $ 2,900

Total manufacturing costs recorded for the Job $ 4,700

Sub part (d):

Computation of unit production costs:

Particulars Amount

Total cost recorded for the job $ 4,700

Number of units contained in the Job 100

Production cost per unit (4700/100) $ 47

Sub part (e):

Assembly department is a labor-intensive department and requires more labor hour rather

than the machine hour. To make fair allocation of the overhead costs the labor hour has been

used as the base for computing the overhead rate for assembly department and the predetermined

overhead rate comes to $10 per direct labor-hour. Applying the same rate total overhead applied

to the Job for the assembly department comes to $800. From the given case study, the total direct

labor cost can be considered as $1,100, which included the direct labor cost for both the welding

and the assembly department. Taking these two figures the overhead rate as a percentage of the

total direct labor cost can be computed which comes to 72.73%. The industry benchmark for

overhead for the assembly department is 75% of the direct labor costs. Therefore, it can be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.