Management Accounting Report: Costing Techniques Analysis

VerifiedAdded on 2020/10/22

|15

|4942

|486

Report

AI Summary

This report provides a comprehensive analysis of management accounting, focusing on its application within a small company, Aston Chemicals. It explores various management accounting systems, including cost accounting, price optimization, inventory management, and job costing, detailing their benefits and applications. The report further examines different management accounting reporting methods like performance reporting, inventory management reporting, job cost reporting, and account receivable reporting. It also includes calculations of costs using marginal and absorption costing techniques. Moreover, the report addresses financial problems faced by businesses and discusses planning tools and techniques for budgetary control, concluding with how management accounting contributes to sustainable success in resolving financial issues. The report provides a detailed overview of management accounting principles, techniques, and their practical application within a business context.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and its types of management accounting systems........................1

P2. Different methods used for management accounting reporting............................................3

M1: Evaluate the benefits of management accounting system and its applications...................4

D1. Management accounting system and its reporting within organisation process..................5

TASK 2............................................................................................................................................5

P3: Calculation of cost using an appropriate technique..............................................................5

M2: Various types of accounting techniques and financial reporting documents......................7

D2: Data interpretation................................................................................................................7

TASK 3............................................................................................................................................7

P4: Advantages and disadvantages of different planning tools used for budgetary control.......7

M3: Uses and applications of planning tools for preparing and forecasting budgets.................9

TASK 4............................................................................................................................................9

P5: Responses of management accounting system to deal with financial problems..................9

M4: Management accounting lead to sustainable success in responding to financial problems

...................................................................................................................................................11

D3: Planning tools respond appropriately to resolve financial problems.................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and its types of management accounting systems........................1

P2. Different methods used for management accounting reporting............................................3

M1: Evaluate the benefits of management accounting system and its applications...................4

D1. Management accounting system and its reporting within organisation process..................5

TASK 2............................................................................................................................................5

P3: Calculation of cost using an appropriate technique..............................................................5

M2: Various types of accounting techniques and financial reporting documents......................7

D2: Data interpretation................................................................................................................7

TASK 3............................................................................................................................................7

P4: Advantages and disadvantages of different planning tools used for budgetary control.......7

M3: Uses and applications of planning tools for preparing and forecasting budgets.................9

TASK 4............................................................................................................................................9

P5: Responses of management accounting system to deal with financial problems..................9

M4: Management accounting lead to sustainable success in responding to financial problems

...................................................................................................................................................11

D3: Planning tools respond appropriately to resolve financial problems.................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is a sub division of accounting system which is concerned with

preparation of managerial and cost accounts in order to provide non monetary and statistical

information. In order to better understand the concept of management accounting a small

company is selected and that is Aston chemicals. This is a private limited company located in

England, United Kingdom and deals in distributing chemicals in the European Personal Care

industry. The main aim of this project report is to provide an understanding about the concept of

management accounting as a Management Accounting officer (Bisbe and Malagueño, 2012).

In this project report various types of management accounting systems are discussed

along with reporting methods. This branch of accounting system often includes costing

techniques which are described along with its numerical solutions. Every business organisations

faces several financial issues which are addressed in this project report along with its planning

tools and techniques which assist in tackling those issues.

TASK 1

P1. Management accounting and its types of management accounting systems

Management accounting is a concept which includes process of analysing business costs

and operations by the help of internal financial reports and managerial accounts which are

prepared by internal managers of an organisation. Aston Chemicals is a small scale company

which endeavour to seek development and growth due to which they incorporate this concept to

increase efficiency of the organisational operations. The primary benefits of this concept are

better decision making and attainment of overall organisational goals. Financial information

including various accounting statements and reports are analysed and interpreted in this concept

so that it can be understandable in order to make reliable decision for the organisational activities

(Budding, Grossi and Tagesson, 2014).

Managerial accounting system is a framework which help in perform and manage various

activities of an organisation such as inventory, costing and many more. There are several types

of management accounting system and some of them which are used by Aston Chemicals are

discussed below:

Cost Accounting System: This type of managerial accounting system records and keeps

track of all costs which are incurred in course of organisational operations. Costs which are

1

Management accounting is a sub division of accounting system which is concerned with

preparation of managerial and cost accounts in order to provide non monetary and statistical

information. In order to better understand the concept of management accounting a small

company is selected and that is Aston chemicals. This is a private limited company located in

England, United Kingdom and deals in distributing chemicals in the European Personal Care

industry. The main aim of this project report is to provide an understanding about the concept of

management accounting as a Management Accounting officer (Bisbe and Malagueño, 2012).

In this project report various types of management accounting systems are discussed

along with reporting methods. This branch of accounting system often includes costing

techniques which are described along with its numerical solutions. Every business organisations

faces several financial issues which are addressed in this project report along with its planning

tools and techniques which assist in tackling those issues.

TASK 1

P1. Management accounting and its types of management accounting systems

Management accounting is a concept which includes process of analysing business costs

and operations by the help of internal financial reports and managerial accounts which are

prepared by internal managers of an organisation. Aston Chemicals is a small scale company

which endeavour to seek development and growth due to which they incorporate this concept to

increase efficiency of the organisational operations. The primary benefits of this concept are

better decision making and attainment of overall organisational goals. Financial information

including various accounting statements and reports are analysed and interpreted in this concept

so that it can be understandable in order to make reliable decision for the organisational activities

(Budding, Grossi and Tagesson, 2014).

Managerial accounting system is a framework which help in perform and manage various

activities of an organisation such as inventory, costing and many more. There are several types

of management accounting system and some of them which are used by Aston Chemicals are

discussed below:

Cost Accounting System: This type of managerial accounting system records and keeps

track of all costs which are incurred in course of organisational operations. Costs which are

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

managed and maintained are continuously transacted by mangers despite of the nature of

inventory in which cost is incurred. The main aim of this system is to keep track of all incurred

costs so that future profitability can be ascertained. This system includes preparation of cost

budget which includes all costs which are incurred against organisational expenses.

Aston Chemicals has a team of professionals which look after their all managerial affairs

in order to improve their efficiency. Their managers uses this system to determine their future

profitability by keeping track of their present cost involvement (Derchi, Burkert and Oyon,

2013).

Price Optimisation System: According to this managerial accounting system, prices of

products and services should be allotted by keeping all the factors in mind such as willingness of

customers to pay, income group of target market and many more. This process is concerned with

assigning right price to right product in order to satisfy customer and also to earn a decent

amount of profit. Price optimisation helps organisations like Aston Chemicals to use formula of

this system to identify market demand of their chemical products so that they can determine

effect of all market factor like level of competition and market demand. By considering all these

factors they allocate appropriate prices to their products.

Job cost System: In this system various jobs are identified and analysed which are

performed or needed to be performed in an organisation to achieve their organisational business

goals. These jobs are assigned a certain amount of cost which are allotted by managers of an

organisation. This system is an expense monitoring process which determines cost of each job or

operation. These job costs are managed by classifying them into categories such as overhead

costs, direct material costs and direct labour costs (Huber and Scheytt, 2013).

For example, Aston Chemicals uses this system to determine costs engaged in their every

job and operation category. By ascertaining these costs, organisation can be benefited as they can

now ascertain in what job high costs are involved and what are its problem areas.

Inventory Management System: This system helps an organisation to keeps track of

every unit in their inventory. Here, inventory refers to the stock which is available in the

organisation including raw material, stock engaged in work in progress and warehoused goods.

Aston chemicals uses this system to manage their inventories and track record of every inflow

and outflow of stock. This process assist in minimising the risk involved in inventory

management and helps to control stock related affairs of an organisation.

2

inventory in which cost is incurred. The main aim of this system is to keep track of all incurred

costs so that future profitability can be ascertained. This system includes preparation of cost

budget which includes all costs which are incurred against organisational expenses.

Aston Chemicals has a team of professionals which look after their all managerial affairs

in order to improve their efficiency. Their managers uses this system to determine their future

profitability by keeping track of their present cost involvement (Derchi, Burkert and Oyon,

2013).

Price Optimisation System: According to this managerial accounting system, prices of

products and services should be allotted by keeping all the factors in mind such as willingness of

customers to pay, income group of target market and many more. This process is concerned with

assigning right price to right product in order to satisfy customer and also to earn a decent

amount of profit. Price optimisation helps organisations like Aston Chemicals to use formula of

this system to identify market demand of their chemical products so that they can determine

effect of all market factor like level of competition and market demand. By considering all these

factors they allocate appropriate prices to their products.

Job cost System: In this system various jobs are identified and analysed which are

performed or needed to be performed in an organisation to achieve their organisational business

goals. These jobs are assigned a certain amount of cost which are allotted by managers of an

organisation. This system is an expense monitoring process which determines cost of each job or

operation. These job costs are managed by classifying them into categories such as overhead

costs, direct material costs and direct labour costs (Huber and Scheytt, 2013).

For example, Aston Chemicals uses this system to determine costs engaged in their every

job and operation category. By ascertaining these costs, organisation can be benefited as they can

now ascertain in what job high costs are involved and what are its problem areas.

Inventory Management System: This system helps an organisation to keeps track of

every unit in their inventory. Here, inventory refers to the stock which is available in the

organisation including raw material, stock engaged in work in progress and warehoused goods.

Aston chemicals uses this system to manage their inventories and track record of every inflow

and outflow of stock. This process assist in minimising the risk involved in inventory

management and helps to control stock related affairs of an organisation.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2. Different methods used for management accounting reporting

Management accounting reporting is an approach used to understand company's

management reports that is helpful in decision-making process. Many organisation use this

reporting tool for measuring it's quarterly or yearly performance on the basis of financial reports

like income and cash flows statements, balance sheet etc. Aston chemicals use various reporting

methods like performance, inventory management, account receivable and job cost reporting.

This helps in developing and implementing plans that improves company's performance in order

to expand its market without any problems (Ji, 2017). These reports consist an accurate and

transparent information that is useful for both internal and external stakeholders.

The different types of reports are described below:

Performance reporting: This reporting method measure continuous performance of the

company that involves collecting and scattering of project information. Then communicate its

progress to stakeholders. This report includes evaluation of previous performance, details of

modification if any in reporting period, results of variance analysis and present status of risks

involved in process etc. Aston chemicals use this reporting method for estimating its present

performance at various departments. It also forecast future working by comparing actual

distribution with standard. For identifying and resolving issues, company establish certain rules

and regulation for manager at various departments. This reporting system helps in preparing

performance report which consist accurate information related to company's performance that

assist in distribution activities.

Inventory Management Reporting: This report displays the actual information related

to inventory of the company. Manger prepares this report to get the accurate information of the

stock such as the flow of inventory in process or distribution and quantity of stock in storage.

Aston chemicals is a distributor of chemicals and wants to identify product demand, turnover of

specific accounting period. Company uses this reporting method for keep a record of its

inventory in the operations. It also helps manager in dealing with situation like under or

overstock of inventory (Kirli and Gümüş, 2011). This reporting method provide correct

information about inventory that assist in preparing effective reports.

Job Cost Reporting: In this method company identify the cost of each job at various

level of operation and also monitor expenses involved in process. In this reporting company

identify the issues related to current job and ignore problems that might be occur in future job.

3

Management accounting reporting is an approach used to understand company's

management reports that is helpful in decision-making process. Many organisation use this

reporting tool for measuring it's quarterly or yearly performance on the basis of financial reports

like income and cash flows statements, balance sheet etc. Aston chemicals use various reporting

methods like performance, inventory management, account receivable and job cost reporting.

This helps in developing and implementing plans that improves company's performance in order

to expand its market without any problems (Ji, 2017). These reports consist an accurate and

transparent information that is useful for both internal and external stakeholders.

The different types of reports are described below:

Performance reporting: This reporting method measure continuous performance of the

company that involves collecting and scattering of project information. Then communicate its

progress to stakeholders. This report includes evaluation of previous performance, details of

modification if any in reporting period, results of variance analysis and present status of risks

involved in process etc. Aston chemicals use this reporting method for estimating its present

performance at various departments. It also forecast future working by comparing actual

distribution with standard. For identifying and resolving issues, company establish certain rules

and regulation for manager at various departments. This reporting system helps in preparing

performance report which consist accurate information related to company's performance that

assist in distribution activities.

Inventory Management Reporting: This report displays the actual information related

to inventory of the company. Manger prepares this report to get the accurate information of the

stock such as the flow of inventory in process or distribution and quantity of stock in storage.

Aston chemicals is a distributor of chemicals and wants to identify product demand, turnover of

specific accounting period. Company uses this reporting method for keep a record of its

inventory in the operations. It also helps manager in dealing with situation like under or

overstock of inventory (Kirli and Gümüş, 2011). This reporting method provide correct

information about inventory that assist in preparing effective reports.

Job Cost Reporting: In this method company identify the cost of each job at various

level of operation and also monitor expenses involved in process. In this reporting company

identify the issues related to current job and ignore problems that might be occur in future job.

3

Aston chemicals use this reporting method for identifying its expenditure such as cost of direct

material, labour, overheads and equipments purchased of a specific job related to present status

and to enhance future profitability.

Account Receivable Reporting: This reporting method helps in preparing aging report

by which company gets an exact idea related to amount outstanding with customers. This report

is based on those customers who are unable to pay at the time of purchase but promise to pay

later. It also display duration of collection period. Aston chemicals use this reporting method for

keeping records of those customers whose invoice are due (Maskell, Baggaley and Grasso,

2016). This report shows a list of unpaid customers, due invoices and average collection cycle

that helps in increasing sales practices. It also assist in recovering the due amount with

customers.

M1: Evaluate the benefits of management accounting system and its applications

Management accounting system Benefits

Cost accounting system This management accounting system helps in

reducing the cost of manufacturing and other

activities conducted by an organisation. Aston

Chemicals is benefited by this system as they

can now keep record for all their costs which

are involved in an organisation.

Price optimisation system This system helps Aston Chemicals to attract

their customers by assigning effective prices to

their products which are cost effective an also

allows organisation to earn decent amount of

profit (McLean, McGovern and Davie, 2015).

Inventory management system The main benefit of this managerial system is

optimum utilisation of resources. Aston

Chemicals uses this system to keep record of

all their inventories which benefits them by

clutter free management.

Job costing system It helps to ascertain cost involvement in all the

4

material, labour, overheads and equipments purchased of a specific job related to present status

and to enhance future profitability.

Account Receivable Reporting: This reporting method helps in preparing aging report

by which company gets an exact idea related to amount outstanding with customers. This report

is based on those customers who are unable to pay at the time of purchase but promise to pay

later. It also display duration of collection period. Aston chemicals use this reporting method for

keeping records of those customers whose invoice are due (Maskell, Baggaley and Grasso,

2016). This report shows a list of unpaid customers, due invoices and average collection cycle

that helps in increasing sales practices. It also assist in recovering the due amount with

customers.

M1: Evaluate the benefits of management accounting system and its applications

Management accounting system Benefits

Cost accounting system This management accounting system helps in

reducing the cost of manufacturing and other

activities conducted by an organisation. Aston

Chemicals is benefited by this system as they

can now keep record for all their costs which

are involved in an organisation.

Price optimisation system This system helps Aston Chemicals to attract

their customers by assigning effective prices to

their products which are cost effective an also

allows organisation to earn decent amount of

profit (McLean, McGovern and Davie, 2015).

Inventory management system The main benefit of this managerial system is

optimum utilisation of resources. Aston

Chemicals uses this system to keep record of

all their inventories which benefits them by

clutter free management.

Job costing system It helps to ascertain cost involvement in all the

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

jibs conducted by Aston chemicals by which

they can ascertain which job needs highest cost

and what are its reasons and problem areas.

D1. Management accounting system and its reporting within organisation process

Company uses cost accounting, inventory management, prime optimisation and job

costing systems and its reporting within operations. This helps in effective planning and

controlling of management performance. Company create best pricing strategy in order to

increase product demand by attracting more customers. It also follow inventory management

system for determining inflow and outflow of stock in way to maintain future demand of

chemicals. Management accounting reports display many useful information to manager which

helps in determining actual performance and create a positive image in marketplace.

TASK 2

P3: Calculation of cost using an appropriate technique

Cost: It is the amount of resources given up in exchange for some goods or services. The

amount spent on the purchase of raw material or producing a product is also known as cost.

Aston Chemicals set a right cost of its product i.e. chemicals in order to attract more customers.

Buyers evaluate product cost before they purchase that product. Establishing a right cost is the

key to maximise profit (Proctor, 2012). Costing is the technique and process of ascertaining

costs. It refers to as classifying and recording appropriate allocation of expenditure for the

determination of product cost or services. Below are two costing techniques that Aston

Chemicals use for calculating its net operating income.

Marginal costing: It is an ascertainment of variable cost and effect on profit. Aston

Chemicals use this technique for identifying change in output by differentiating between fixed

and variable cost. It is related to only marginal cost of the product.

Absorption costing: This technique charges all costs, both variable and fixed to

operations, processes or products. Here costs are ascertained after they have been incurred, it

does not help in controlling over costs. This technique assist Aston Chemicals in providing

details information about all costs in its production process.

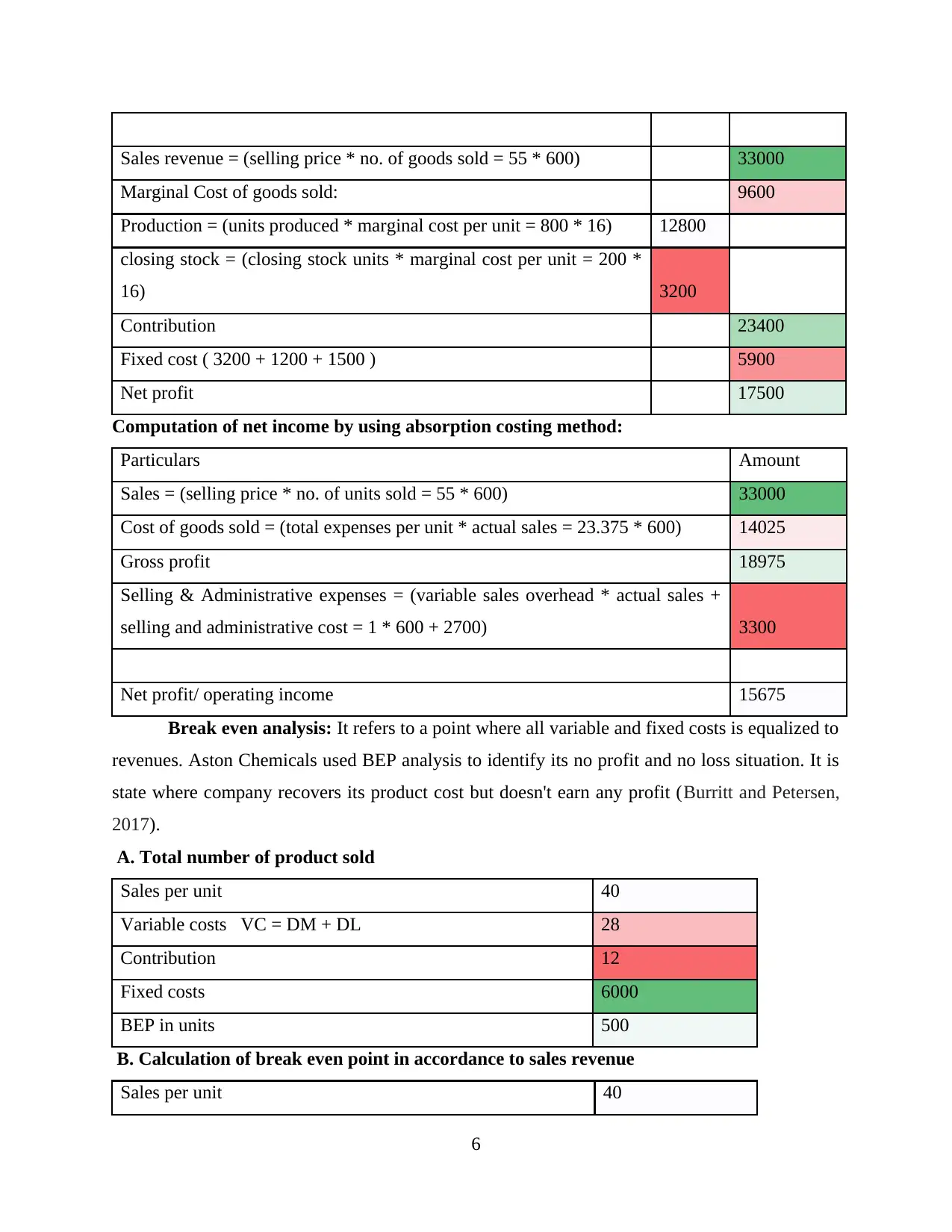

Calculation of net profit by using marginal costing method:

Particulars Amount

5

they can ascertain which job needs highest cost

and what are its reasons and problem areas.

D1. Management accounting system and its reporting within organisation process

Company uses cost accounting, inventory management, prime optimisation and job

costing systems and its reporting within operations. This helps in effective planning and

controlling of management performance. Company create best pricing strategy in order to

increase product demand by attracting more customers. It also follow inventory management

system for determining inflow and outflow of stock in way to maintain future demand of

chemicals. Management accounting reports display many useful information to manager which

helps in determining actual performance and create a positive image in marketplace.

TASK 2

P3: Calculation of cost using an appropriate technique

Cost: It is the amount of resources given up in exchange for some goods or services. The

amount spent on the purchase of raw material or producing a product is also known as cost.

Aston Chemicals set a right cost of its product i.e. chemicals in order to attract more customers.

Buyers evaluate product cost before they purchase that product. Establishing a right cost is the

key to maximise profit (Proctor, 2012). Costing is the technique and process of ascertaining

costs. It refers to as classifying and recording appropriate allocation of expenditure for the

determination of product cost or services. Below are two costing techniques that Aston

Chemicals use for calculating its net operating income.

Marginal costing: It is an ascertainment of variable cost and effect on profit. Aston

Chemicals use this technique for identifying change in output by differentiating between fixed

and variable cost. It is related to only marginal cost of the product.

Absorption costing: This technique charges all costs, both variable and fixed to

operations, processes or products. Here costs are ascertained after they have been incurred, it

does not help in controlling over costs. This technique assist Aston Chemicals in providing

details information about all costs in its production process.

Calculation of net profit by using marginal costing method:

Particulars Amount

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200 + 1200 + 1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break even analysis: It refers to a point where all variable and fixed costs is equalized to

revenues. Aston Chemicals used BEP analysis to identify its no profit and no loss situation. It is

state where company recovers its product cost but doesn't earn any profit (Burritt and Petersen,

2017).

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

B. Calculation of break even point in accordance to sales revenue

Sales per unit 40

6

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200 + 1200 + 1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break even analysis: It refers to a point where all variable and fixed costs is equalized to

revenues. Aston Chemicals used BEP analysis to identify its no profit and no loss situation. It is

state where company recovers its product cost but doesn't earn any profit (Burritt and Petersen,

2017).

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

B. Calculation of break even point in accordance to sales revenue

Sales per unit 40

6

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

C. Calculation for getting desired profit of 10000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety: In this technique variation in intrinsic and market value of the product

is identify. Aston Chemicals use margin of safety for evaluating the difference between actual

and break-even sales of its chemicals (Smith, Brännström and Jansson, 2015.). This tool helps in

identifying risk involve in distribution and also assist in modifying its sale practices.

D. The margin of safety, if 800 units are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2: Various types of accounting techniques and financial reporting documents

Standard, marginal and absorption costing are the different types of accounting

techniques used in evaluating financial reporting documents. Aston Chemicals use marginal and

absorption costing technique of ascertaining net operating income. The cost of an extra unit of

production is identified under marginal costing. In absorption, all costs whether it is variable or

fixed incurred in product, process or operations of company is identify. Company finds marginal

costing is the best method for determining net profit that helps in creating financial reporting

documents. It also assist in decision-making because cost is matched with revenue to determine

profit.

7

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

C. Calculation for getting desired profit of 10000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety: In this technique variation in intrinsic and market value of the product

is identify. Aston Chemicals use margin of safety for evaluating the difference between actual

and break-even sales of its chemicals (Smith, Brännström and Jansson, 2015.). This tool helps in

identifying risk involve in distribution and also assist in modifying its sale practices.

D. The margin of safety, if 800 units are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2: Various types of accounting techniques and financial reporting documents

Standard, marginal and absorption costing are the different types of accounting

techniques used in evaluating financial reporting documents. Aston Chemicals use marginal and

absorption costing technique of ascertaining net operating income. The cost of an extra unit of

production is identified under marginal costing. In absorption, all costs whether it is variable or

fixed incurred in product, process or operations of company is identify. Company finds marginal

costing is the best method for determining net profit that helps in creating financial reporting

documents. It also assist in decision-making because cost is matched with revenue to determine

profit.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

D2: Data interpretation

Marginal and absorption costing technique is used to determine net operating profit.

Company achieve a profit of £17500 under marginal where as £15675 by absorption costing. It

finds a variation of £1825 in profit by comparing both methods. Therefore, company finds

marginal costing is best techniques for evaluating net profit. Aston Chemicals also determine its

break-even point and evaluate total BEP sales of £20000, units sold are 500. Company sales

1333.3 units in order to achieve a minimum profit of £10000. The margin of safety is 37.5, when

800 units are sold.

TASK 3

P4: Advantages and disadvantages of different planning tools used for budgetary control

Budgetary control: It is a system that use budgets as a way of planning and controlling

all aspects of creating or selling products. A 'budget' is a source and 'budgetary-control' is the last

result. A major function of management is to control company's operations therefore, Aston

Chemicals use budgetary control as a planning tool. It provides feedback to management about

its operation and distribution activities. Company use contingency, forecasting and scenario

planning tool for predicting future events and plans accordingly in order to run operations

effectively (Šoljaková, 2012).

Forecasting Tool: In this tool future conditions of the business are forecasted on the

basis of previous events. It assist in decision-making by planning, estimating and budgeting

future growth. Aston Chemicals uses forecasting planning tool to deal with future uncertainty by

collecting information from past and present outcomes. Manager use this tool for predicting

chemicals sales, form budgets on the basis of their knowledge and experience. The benefits and

drawbacks of this tool are explained below:

Advantages Disadvantages

It provides useful information to work

efficiently under any conditions such as

increase in product demand or decrease in

sales.

This tool is not always reliable because based

on estimates and assumptions made

accordingly.

8

Marginal and absorption costing technique is used to determine net operating profit.

Company achieve a profit of £17500 under marginal where as £15675 by absorption costing. It

finds a variation of £1825 in profit by comparing both methods. Therefore, company finds

marginal costing is best techniques for evaluating net profit. Aston Chemicals also determine its

break-even point and evaluate total BEP sales of £20000, units sold are 500. Company sales

1333.3 units in order to achieve a minimum profit of £10000. The margin of safety is 37.5, when

800 units are sold.

TASK 3

P4: Advantages and disadvantages of different planning tools used for budgetary control

Budgetary control: It is a system that use budgets as a way of planning and controlling

all aspects of creating or selling products. A 'budget' is a source and 'budgetary-control' is the last

result. A major function of management is to control company's operations therefore, Aston

Chemicals use budgetary control as a planning tool. It provides feedback to management about

its operation and distribution activities. Company use contingency, forecasting and scenario

planning tool for predicting future events and plans accordingly in order to run operations

effectively (Šoljaková, 2012).

Forecasting Tool: In this tool future conditions of the business are forecasted on the

basis of previous events. It assist in decision-making by planning, estimating and budgeting

future growth. Aston Chemicals uses forecasting planning tool to deal with future uncertainty by

collecting information from past and present outcomes. Manager use this tool for predicting

chemicals sales, form budgets on the basis of their knowledge and experience. The benefits and

drawbacks of this tool are explained below:

Advantages Disadvantages

It provides useful information to work

efficiently under any conditions such as

increase in product demand or decrease in

sales.

This tool is not always reliable because based

on estimates and assumptions made

accordingly.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It helps in decision making by estimating

future possibilities.

It consist of inadequate information and not

full proof

Contingency Tool: This planning tool helps in identifying events that might be interrupt

operations. It is a process in which actual response system are placed in way to prevent from any

uncertain event. Aston Chemicals use this tool for protecting its resources and minimises

customer inconvenience (Spekle and Verbeeten, 2014). Company identify key employees for

assigning specific responsibilities in case of emergency situations.

Advantages Disadvantages

It helps Aston Chemicals in dealing with any

uncertainty that occur in future.

Extensive planning displays a negative impact

on the operations.

It helps in better coordination and effective

planning.

Cost and resources spent on this planning is not

always useful.

Scenario Tool: It is based on the analysing and understanding of current and historic

events and trends. It includes a consistent explanation of possible future situations. Aston

Chemicals use scenario planning tool for identifying possible ways towards its future vision by

developing a sets of narrative scenarios. It helps in predicting favourable and unfavourable

events that might happen in future.

Advantages Disadvantages

Company focus to look ahead with better use

of resources.

It may be difficult to implement with rapidly

changes in market because some unplanned

opportunities may be missed at the time of

scenario planning.

It provides a direction and helps in monitoring

Aston Chemicals progress.

It is expensive and time consuming planning

process.

M3: Uses and applications of planning tools for preparing and forecasting budgets

Forecasting, contingency and scenario planning tool assist Aston Chemicals in preparing

and forecasting budgets. Company forecast chemical sells with the help of previous and current

sales. By this it estimate future conditions which also helps in identifying risk involved in

operations. In contingency tool, company determine unpredictable events that might be influence

9

future possibilities.

It consist of inadequate information and not

full proof

Contingency Tool: This planning tool helps in identifying events that might be interrupt

operations. It is a process in which actual response system are placed in way to prevent from any

uncertain event. Aston Chemicals use this tool for protecting its resources and minimises

customer inconvenience (Spekle and Verbeeten, 2014). Company identify key employees for

assigning specific responsibilities in case of emergency situations.

Advantages Disadvantages

It helps Aston Chemicals in dealing with any

uncertainty that occur in future.

Extensive planning displays a negative impact

on the operations.

It helps in better coordination and effective

planning.

Cost and resources spent on this planning is not

always useful.

Scenario Tool: It is based on the analysing and understanding of current and historic

events and trends. It includes a consistent explanation of possible future situations. Aston

Chemicals use scenario planning tool for identifying possible ways towards its future vision by

developing a sets of narrative scenarios. It helps in predicting favourable and unfavourable

events that might happen in future.

Advantages Disadvantages

Company focus to look ahead with better use

of resources.

It may be difficult to implement with rapidly

changes in market because some unplanned

opportunities may be missed at the time of

scenario planning.

It provides a direction and helps in monitoring

Aston Chemicals progress.

It is expensive and time consuming planning

process.

M3: Uses and applications of planning tools for preparing and forecasting budgets

Forecasting, contingency and scenario planning tool assist Aston Chemicals in preparing

and forecasting budgets. Company forecast chemical sells with the help of previous and current

sales. By this it estimate future conditions which also helps in identifying risk involved in

operations. In contingency tool, company determine unpredictable events that might be influence

9

its future operations. Company also focus on future situations under scenario tool, with better

utilisation of resources by giving directions to management. Aston Chemicals uses this

budgetary-control planning tool to develop an effective system for management.

TASK 4

P5: Responses of management accounting system to deal with financial problems

Financial issues are mainly related to the lack of money in organisation activities or

operations. Many organisation are suffering from various financial problems in its working or at

the time of expansion. Insolvency, improper cash management, inadequacy of finance, high level

of debt etc. are various financial problems from which companies are dealing now a days (Stout

and Propri, 2011). Aston Chemicals is a small size distributor and desire to expand in future.

Company is also suffering from various monetary issues which are explained below:

Insufficient funds: Company has not sufficient amount of funds available in order to

expand its business. Therefore, company need funds to arise sufficient amount of capital.

Large number of creditors: Regular credit sales increase the number of creditors which

lead to high level of debts. Aston Chemicals supply product to customers on credit but

unable to recover outstanding amount of them.

Excess of spending: Managers of Aston Chemicals spent too much in promotional and

distribution activities. This also impact in company's profitability because amount of

expenses are more than its revenue.

KPI(Key performance indicator): This tool is used to examine and measure company's

performance in a particular time period that help in favourable decision-making. Aston

Chemicals use this technique for comparing its finance and distribution performance that impact

negatively on its operations. Company is facing a financial issue related to excess of spending, so

that company follow key performance indicator (What is a KPI, 2018). With the help of this tool

company measure its employees activities like, where they are spending more. Company identify

that, management is spending more on promotion and distribution activities for reducing

expenses it use types of key performance indicators that are explained below:

Leading KPI- In this indicator company estimates future events and evaluate market

trends which helps in decision-making. Aston Chemicals follow leading indicator for

measuring its unnecessary expenses such as extra spending on distribution and promotion

10

utilisation of resources by giving directions to management. Aston Chemicals uses this

budgetary-control planning tool to develop an effective system for management.

TASK 4

P5: Responses of management accounting system to deal with financial problems

Financial issues are mainly related to the lack of money in organisation activities or

operations. Many organisation are suffering from various financial problems in its working or at

the time of expansion. Insolvency, improper cash management, inadequacy of finance, high level

of debt etc. are various financial problems from which companies are dealing now a days (Stout

and Propri, 2011). Aston Chemicals is a small size distributor and desire to expand in future.

Company is also suffering from various monetary issues which are explained below:

Insufficient funds: Company has not sufficient amount of funds available in order to

expand its business. Therefore, company need funds to arise sufficient amount of capital.

Large number of creditors: Regular credit sales increase the number of creditors which

lead to high level of debts. Aston Chemicals supply product to customers on credit but

unable to recover outstanding amount of them.

Excess of spending: Managers of Aston Chemicals spent too much in promotional and

distribution activities. This also impact in company's profitability because amount of

expenses are more than its revenue.

KPI(Key performance indicator): This tool is used to examine and measure company's

performance in a particular time period that help in favourable decision-making. Aston

Chemicals use this technique for comparing its finance and distribution performance that impact

negatively on its operations. Company is facing a financial issue related to excess of spending, so

that company follow key performance indicator (What is a KPI, 2018). With the help of this tool

company measure its employees activities like, where they are spending more. Company identify

that, management is spending more on promotion and distribution activities for reducing

expenses it use types of key performance indicators that are explained below:

Leading KPI- In this indicator company estimates future events and evaluate market

trends which helps in decision-making. Aston Chemicals follow leading indicator for

measuring its unnecessary expenses such as extra spending on distribution and promotion

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.