Management Accounting Report: Cost Analysis of Aston Martin

VerifiedAdded on 2021/01/02

|19

|5119

|200

Report

AI Summary

This report delves into the realm of management accounting, using Aston Martin as a case study to illustrate key concepts and practical applications. It begins with an introduction to management accounting, emphasizing its role in providing crucial financial and statistical information for effective decision-making. The report then explores various management accounting systems, including cost accounting, job costing, price optimization, and inventory management, highlighting their benefits and applications within Aston Martin. Furthermore, it examines different management accounting reporting methods, such as budget reports, account receivable aging reports, performance reports, and cost managerial accounting reports. The report also includes an analysis of the integration of management accounting systems and reporting within organizational processes. The report concludes with an income statement prepared using marginal costing methods and absorption costing methods, providing a comparative analysis of the two approaches. The report emphasizes the importance of these systems and reports in aiding financial managers in making critical decisions for the betterment of companies to achieve desired profits and builds brand image in the competitive market place.

MANAGEMENT

ACCOUNTING

t

o

a

c

c

t

o

a

c

c

ACCOUNTING

t

o

a

c

c

t

o

a

c

c

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

Part A...........................................................................................................................................1

Part B...........................................................................................................................................5

ACTIVITY 2....................................................................................................................................9

Part A...........................................................................................................................................9

Part B.........................................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

Part A...........................................................................................................................................1

Part B...........................................................................................................................................5

ACTIVITY 2....................................................................................................................................9

Part A...........................................................................................................................................9

Part B.........................................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is the process of preparing management reports & accounts

which provide accurate & timely financial & statistical information that is helpful for the

management to take effective decisions (Kaplan and Atkinson, 2015). It provide information to

different stakeholders about the financial position of organisation and on the basis of it they take

important decisions. As the accountant of corporation is responsible to following principles of

management accounting so that books of accounts can prepare as per the requirement. To better

understand this concept Aston Martin has been chosen which is a luxury sports car

manufacturing company of United Kingdom. This report discuss about various topics such as:

the concept of management accounting & distinct types of management accounting systems,

methods used for management accounting reporting and to use appropriate techniques of cost

analysis to prepare an income statement using marginal & absorption cost. Apart from this, it

also discuss about planning tools used in management accounting and how management

accounting systems are helpful to solve the financial problems.

ACTIVITY 1

Part A

Management accounting is also known as managerial accounting. It is used by the

managers for taking decisions for performing operations and to control various functions for the

betterment of organisation (Ward, 2012). It involves preparation of management reports to

provide accurate and reliable information for framing short term as well as long term plans for

the purpose of achieving objectives of firm. Using such accounting, budgets along with trend

charts are designed for allocating key resources for generating revenues to attaining growth. This

accounting plays very crucial functions to manage internal operations of any business. Such

accounting helps in building positive variances by applying techniques to eliminate or reduce the

negative ones to ensure that work is performed as per the planned activities. Some of the types of

accounting systems are the followings:

Cost accounting system: Cost accounting system is a type of management accounting

which is used by the managers for recording activities, analysing production costs and

tracking materials at different phases of production from raw material to finished

products. Such system is helpful in estimating associated costs for analysing profitability,

1

Management accounting is the process of preparing management reports & accounts

which provide accurate & timely financial & statistical information that is helpful for the

management to take effective decisions (Kaplan and Atkinson, 2015). It provide information to

different stakeholders about the financial position of organisation and on the basis of it they take

important decisions. As the accountant of corporation is responsible to following principles of

management accounting so that books of accounts can prepare as per the requirement. To better

understand this concept Aston Martin has been chosen which is a luxury sports car

manufacturing company of United Kingdom. This report discuss about various topics such as:

the concept of management accounting & distinct types of management accounting systems,

methods used for management accounting reporting and to use appropriate techniques of cost

analysis to prepare an income statement using marginal & absorption cost. Apart from this, it

also discuss about planning tools used in management accounting and how management

accounting systems are helpful to solve the financial problems.

ACTIVITY 1

Part A

Management accounting is also known as managerial accounting. It is used by the

managers for taking decisions for performing operations and to control various functions for the

betterment of organisation (Ward, 2012). It involves preparation of management reports to

provide accurate and reliable information for framing short term as well as long term plans for

the purpose of achieving objectives of firm. Using such accounting, budgets along with trend

charts are designed for allocating key resources for generating revenues to attaining growth. This

accounting plays very crucial functions to manage internal operations of any business. Such

accounting helps in building positive variances by applying techniques to eliminate or reduce the

negative ones to ensure that work is performed as per the planned activities. Some of the types of

accounting systems are the followings:

Cost accounting system: Cost accounting system is a type of management accounting

which is used by the managers for recording activities, analysing production costs and

tracking materials at different phases of production from raw material to finished

products. Such system is helpful in estimating associated costs for analysing profitability,

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

controlling cost as well as valuation of inventory (DRURY, 2013). Aston Martin Plc

applies such system for evaluating various costs at each stage of product to focus on

those products or services which will be more beneficial to the organisation. This system

is essentially required for evaluation of costs such as direct, indirect, fixed and variable

costs in the selected firm.

Job costing system: Job costing system includes procedures to accumulate information

related to costs associated in production of particular product or specific job. It uses

material cost documents, overhead cost documents, job cost sheets for tracking expenses

incurred on producing jobs. Chosen firm provides numerous services to its clients so it is

an important function to make proper and accurate estimation of individual unit costs

associated with the jobs. Such system is essentially required in the firm to track the true

value of costs integrated with delivering specific job.

Price optimisation system: Price optimisation system involves the usage of

mathematical programs for determining reliable prices of products and services in such a

manner which are suitable for customers as well as helpful in maximising profits of

business entity. It is used by respective company to tailor prices of their products as per

the perceptions of clients, dynamic market situations, developing strategies as well as to

attract target clients. It is essentially required to set pricing strategies along with

promotional strategies for attaining customer satisfaction and organisational profits.

Inventory management system: Inventory management system is useful for production

managers to track status of available as well as required inventory for continuous

performing of operations. It is helpful in minimizing situations such as under stock or

overstock of inventory at work place. In relation to Aston Martin Plc, such system is used

for tracking the stock at warehouses and shipping to track the incoming as well as

outgoing of goods with the help of supply chain management. Inventory management

system is essentially required for checking status of inventory available and placing the

order at correct time, in correct quantity and at right place (Parker, 2012).

Management accounting reporting: Management accounting report is a statement

which is helpful to identify different aspects of business accounting system. By using this report

corporation can analyse the performance of its business. As the organisation prepare it on

quarterly or yearly basis as per its requirement. Aston Martin use this so that it can know the true

2

applies such system for evaluating various costs at each stage of product to focus on

those products or services which will be more beneficial to the organisation. This system

is essentially required for evaluation of costs such as direct, indirect, fixed and variable

costs in the selected firm.

Job costing system: Job costing system includes procedures to accumulate information

related to costs associated in production of particular product or specific job. It uses

material cost documents, overhead cost documents, job cost sheets for tracking expenses

incurred on producing jobs. Chosen firm provides numerous services to its clients so it is

an important function to make proper and accurate estimation of individual unit costs

associated with the jobs. Such system is essentially required in the firm to track the true

value of costs integrated with delivering specific job.

Price optimisation system: Price optimisation system involves the usage of

mathematical programs for determining reliable prices of products and services in such a

manner which are suitable for customers as well as helpful in maximising profits of

business entity. It is used by respective company to tailor prices of their products as per

the perceptions of clients, dynamic market situations, developing strategies as well as to

attract target clients. It is essentially required to set pricing strategies along with

promotional strategies for attaining customer satisfaction and organisational profits.

Inventory management system: Inventory management system is useful for production

managers to track status of available as well as required inventory for continuous

performing of operations. It is helpful in minimizing situations such as under stock or

overstock of inventory at work place. In relation to Aston Martin Plc, such system is used

for tracking the stock at warehouses and shipping to track the incoming as well as

outgoing of goods with the help of supply chain management. Inventory management

system is essentially required for checking status of inventory available and placing the

order at correct time, in correct quantity and at right place (Parker, 2012).

Management accounting reporting: Management accounting report is a statement

which is helpful to identify different aspects of business accounting system. By using this report

corporation can analyse the performance of its business. As the organisation prepare it on

quarterly or yearly basis as per its requirement. Aston Martin use this so that it can know the true

2

and fair picture of its business and there are various management accounting reports which are

being discuss as below:

Budget reports: Budget is a formal statement which is an estimation of revenue

& expenditure and it prepare for future in order to achieve goals of business. As

budget reports can prepare for short term as well as long term purpose

(Wickramasinghe and Alawattage, 2012). It is beneficial for planning &

performance measurement purpose and it is useful to take important decisions for

the business growth. As Aston Martin prepares budget in order to anticipate

income and expenses for future and which help the company to take effective

decisions for the expansion of business. It is the responsibility of management to

prepare appropriate budget by analysing all variable factors which can affect the

business operations of corporation.

Account receivable ageing report: This report is prepared by the organisation in

which it records the details of those consumers who purchase the goods on credit

basis. Such report is only prepared by those businesses which performs trading in

credit. It is useful for financial purposes to examining the due amount for payment

by multiple customers. Dates are clearly mentioned along with name and further

details related to the credit transactions. Aston martin prepares this report by

collecting information for determining invoices which are due for payments. It is

used by management for analysing potential bad debts and further they are revised

for doubtful accounts.

Performance reports: This report is prepared for analysing and evaluating

performance of employees or projects in any business. These are helpful in

monitoring as well as evaluating financial along with non financial performances

for generating actual results. Such reports are used by shareholders, employees,

managers, government authorities and many more for analysing performances for

current and future events. Herein, the managers of Aston Martin uses such reports

to understand performances and improve them by formulating plans, programmes

as well as policies for successfully performing operations towards achievement of

objectives. When performance is not up to the standards various decisions are

taken to improve them using such reports (Hilton and Platt, 2013).

3

being discuss as below:

Budget reports: Budget is a formal statement which is an estimation of revenue

& expenditure and it prepare for future in order to achieve goals of business. As

budget reports can prepare for short term as well as long term purpose

(Wickramasinghe and Alawattage, 2012). It is beneficial for planning &

performance measurement purpose and it is useful to take important decisions for

the business growth. As Aston Martin prepares budget in order to anticipate

income and expenses for future and which help the company to take effective

decisions for the expansion of business. It is the responsibility of management to

prepare appropriate budget by analysing all variable factors which can affect the

business operations of corporation.

Account receivable ageing report: This report is prepared by the organisation in

which it records the details of those consumers who purchase the goods on credit

basis. Such report is only prepared by those businesses which performs trading in

credit. It is useful for financial purposes to examining the due amount for payment

by multiple customers. Dates are clearly mentioned along with name and further

details related to the credit transactions. Aston martin prepares this report by

collecting information for determining invoices which are due for payments. It is

used by management for analysing potential bad debts and further they are revised

for doubtful accounts.

Performance reports: This report is prepared for analysing and evaluating

performance of employees or projects in any business. These are helpful in

monitoring as well as evaluating financial along with non financial performances

for generating actual results. Such reports are used by shareholders, employees,

managers, government authorities and many more for analysing performances for

current and future events. Herein, the managers of Aston Martin uses such reports

to understand performances and improve them by formulating plans, programmes

as well as policies for successfully performing operations towards achievement of

objectives. When performance is not up to the standards various decisions are

taken to improve them using such reports (Hilton and Platt, 2013).

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost managerial accounting reports: Such report is used for computing

associated costs in manufacturing of organisational products or services. Costs

related to overhead, labour and so on taken into consideration. Information related

to costs, product lines, employees and investments are recorded under such

reports in appropriate manner (Fullerton, Kennedy and Widener, 2014). It

involves calculation of expenses before any product is offered for selling purpose

and comparison of expenses is done to earn profits. The profits are calculated by

analysing cost managerial accounting reports. Managers of selected entity

prepares such reports for analysing profits as well as losses and formulating plans

for future situations.

Inventory cost reports: Inventory cost reports is a combination of various

elements which are belonged to the business. Such report is helpful in computing

cots assigned at different organisational stores. This report is very useful for

tracking the required and current inventory to complete the work on time without

any delays. It break downs items related to material, fixed overheads, variable

overheads, labour and service costs. This report helps the selected business for

providing accurate information related to the inventory and costs for the purpose

of determining efficiency in the inventory system.

Evaluation of benefits of various management accounting systems

Management accounting methods have their own importance and benefits applied in

different businesses. It depends on the managers of companies in relation to their usages in

appropriate manner (Otley and Emmanuel, 2013). Benefits of management accounting systems

applied at Aston Martin are the followings:

Advantages of cost accounting system: This system benefits the business by effectively

measuring aspects related to time, costs and expenses. With the help of such system, manager

scan ascertain profitable as well as unprofitable activities which causes profits and losses. Cost

accounting system is used by Aston Martin managers to assign engineering projects at right

prices.

Advantages of job costing system: Such system is helpful to managers for calculating

costs involved in particular jobs. It is also helpful as through such system executives can

4

associated costs in manufacturing of organisational products or services. Costs

related to overhead, labour and so on taken into consideration. Information related

to costs, product lines, employees and investments are recorded under such

reports in appropriate manner (Fullerton, Kennedy and Widener, 2014). It

involves calculation of expenses before any product is offered for selling purpose

and comparison of expenses is done to earn profits. The profits are calculated by

analysing cost managerial accounting reports. Managers of selected entity

prepares such reports for analysing profits as well as losses and formulating plans

for future situations.

Inventory cost reports: Inventory cost reports is a combination of various

elements which are belonged to the business. Such report is helpful in computing

cots assigned at different organisational stores. This report is very useful for

tracking the required and current inventory to complete the work on time without

any delays. It break downs items related to material, fixed overheads, variable

overheads, labour and service costs. This report helps the selected business for

providing accurate information related to the inventory and costs for the purpose

of determining efficiency in the inventory system.

Evaluation of benefits of various management accounting systems

Management accounting methods have their own importance and benefits applied in

different businesses. It depends on the managers of companies in relation to their usages in

appropriate manner (Otley and Emmanuel, 2013). Benefits of management accounting systems

applied at Aston Martin are the followings:

Advantages of cost accounting system: This system benefits the business by effectively

measuring aspects related to time, costs and expenses. With the help of such system, manager

scan ascertain profitable as well as unprofitable activities which causes profits and losses. Cost

accounting system is used by Aston Martin managers to assign engineering projects at right

prices.

Advantages of job costing system: Such system is helpful to managers for calculating

costs involved in particular jobs. It is also helpful as through such system executives can

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ascertain the desirability of specific jobs for the future situations. It provides advantage to chosen

firm by providing fair values of costs associated with delivering particular job.

Advantages of price optimisation system: Price optimisation system provides

advantage of determining reliable prices of business products or services in the open market. It is

helpful in determining price level which benefits to customers as well as organisation. Such

system is useful for selected business managers as it helps in assigning accurate prices of

engineering projects by considering clients perceptions towards prices.

Advantages of inventory management system: This system provides status of present

along with required inventory for eliminating the delays in completion of projects (Renz, 2016).

Such system benefits selected entity to effectively achieve efficiency along with productivity in

completing operations by minimising expenses and maximising profits. It saves time by

preparing the status of inventory in proper format which can be used anytime.

Management accounting system and reporting integration within the organisational processes

Management accounting systems and management accounting reports are inter related

within the organisational processes. Accounting system includes various systems such as cost

accounting system, job costing system, price optimisation system and inventory management

system. All these systems plays very crucial function for preparation of management accounting

reports by providing financial as well as non financial informations. If such systems fails to

provide required information then it becomes very difficult to prepare the management

accounting reports. Financial mangers of Aston Martin uses management accounting systems for

carefully preparing the management accounting reports with the help of various tools and

techniques. Accounting systems reduces the complexity for composition of reports in accurate

manner. Such reports are used by various stakeholders for taking investment decisions. All

management systems and accounting reports are used for taking critical decisions for the

betterment of the companies to achieve desired profits and builds brand image in the competitive

market place. Thus, management accounting systems and reports are integrated within

organisational processes (Maas, Schaltegger and Crutzen, 2016).

Part B

ANNEX (A)

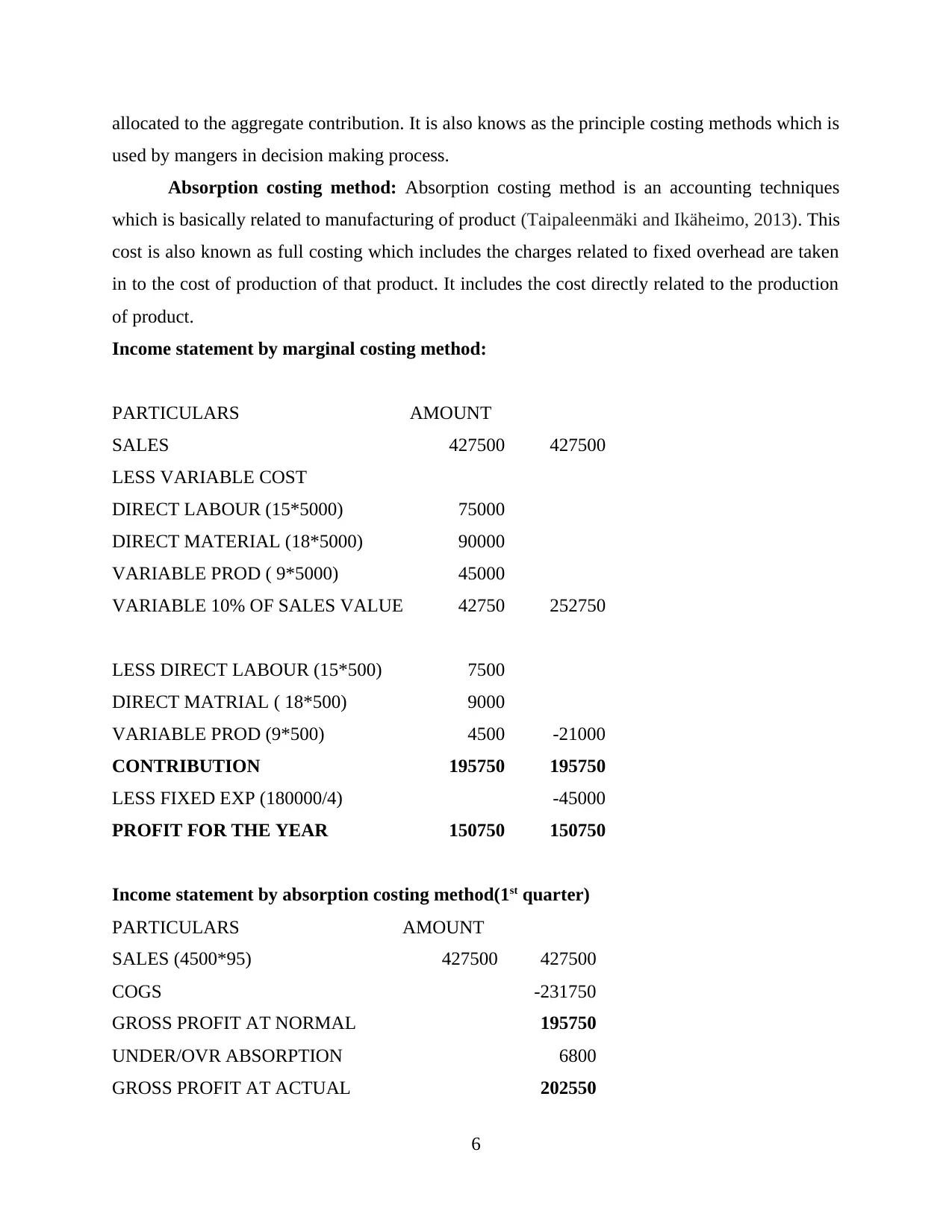

Marginal costing method: Marginal costing method is an accounting technique which is

used by cost accountants to charge the variable cost to the cost of unit and total fixed cost is

5

firm by providing fair values of costs associated with delivering particular job.

Advantages of price optimisation system: Price optimisation system provides

advantage of determining reliable prices of business products or services in the open market. It is

helpful in determining price level which benefits to customers as well as organisation. Such

system is useful for selected business managers as it helps in assigning accurate prices of

engineering projects by considering clients perceptions towards prices.

Advantages of inventory management system: This system provides status of present

along with required inventory for eliminating the delays in completion of projects (Renz, 2016).

Such system benefits selected entity to effectively achieve efficiency along with productivity in

completing operations by minimising expenses and maximising profits. It saves time by

preparing the status of inventory in proper format which can be used anytime.

Management accounting system and reporting integration within the organisational processes

Management accounting systems and management accounting reports are inter related

within the organisational processes. Accounting system includes various systems such as cost

accounting system, job costing system, price optimisation system and inventory management

system. All these systems plays very crucial function for preparation of management accounting

reports by providing financial as well as non financial informations. If such systems fails to

provide required information then it becomes very difficult to prepare the management

accounting reports. Financial mangers of Aston Martin uses management accounting systems for

carefully preparing the management accounting reports with the help of various tools and

techniques. Accounting systems reduces the complexity for composition of reports in accurate

manner. Such reports are used by various stakeholders for taking investment decisions. All

management systems and accounting reports are used for taking critical decisions for the

betterment of the companies to achieve desired profits and builds brand image in the competitive

market place. Thus, management accounting systems and reports are integrated within

organisational processes (Maas, Schaltegger and Crutzen, 2016).

Part B

ANNEX (A)

Marginal costing method: Marginal costing method is an accounting technique which is

used by cost accountants to charge the variable cost to the cost of unit and total fixed cost is

5

allocated to the aggregate contribution. It is also knows as the principle costing methods which is

used by mangers in decision making process.

Absorption costing method: Absorption costing method is an accounting techniques

which is basically related to manufacturing of product (Taipaleenmäki and Ikäheimo, 2013). This

cost is also known as full costing which includes the charges related to fixed overhead are taken

in to the cost of production of that product. It includes the cost directly related to the production

of product.

Income statement by marginal costing method:

PARTICULARS AMOUNT

SALES 427500 427500

LESS VARIABLE COST

DIRECT LABOUR (15*5000) 75000

DIRECT MATERIAL (18*5000) 90000

VARIABLE PROD ( 9*5000) 45000

VARIABLE 10% OF SALES VALUE 42750 252750

LESS DIRECT LABOUR (15*500) 7500

DIRECT MATRIAL ( 18*500) 9000

VARIABLE PROD (9*500) 4500 -21000

CONTRIBUTION 195750 195750

LESS FIXED EXP (180000/4) -45000

PROFIT FOR THE YEAR 150750 150750

Income statement by absorption costing method(1st quarter)

PARTICULARS AMOUNT

SALES (4500*95) 427500 427500

COGS -231750

GROSS PROFIT AT NORMAL 195750

UNDER/OVR ABSORPTION 6800

GROSS PROFIT AT ACTUAL 202550

6

used by mangers in decision making process.

Absorption costing method: Absorption costing method is an accounting techniques

which is basically related to manufacturing of product (Taipaleenmäki and Ikäheimo, 2013). This

cost is also known as full costing which includes the charges related to fixed overhead are taken

in to the cost of production of that product. It includes the cost directly related to the production

of product.

Income statement by marginal costing method:

PARTICULARS AMOUNT

SALES 427500 427500

LESS VARIABLE COST

DIRECT LABOUR (15*5000) 75000

DIRECT MATERIAL (18*5000) 90000

VARIABLE PROD ( 9*5000) 45000

VARIABLE 10% OF SALES VALUE 42750 252750

LESS DIRECT LABOUR (15*500) 7500

DIRECT MATRIAL ( 18*500) 9000

VARIABLE PROD (9*500) 4500 -21000

CONTRIBUTION 195750 195750

LESS FIXED EXP (180000/4) -45000

PROFIT FOR THE YEAR 150750 150750

Income statement by absorption costing method(1st quarter)

PARTICULARS AMOUNT

SALES (4500*95) 427500 427500

COGS -231750

GROSS PROFIT AT NORMAL 195750

UNDER/OVR ABSORPTION 6800

GROSS PROFIT AT ACTUAL 202550

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

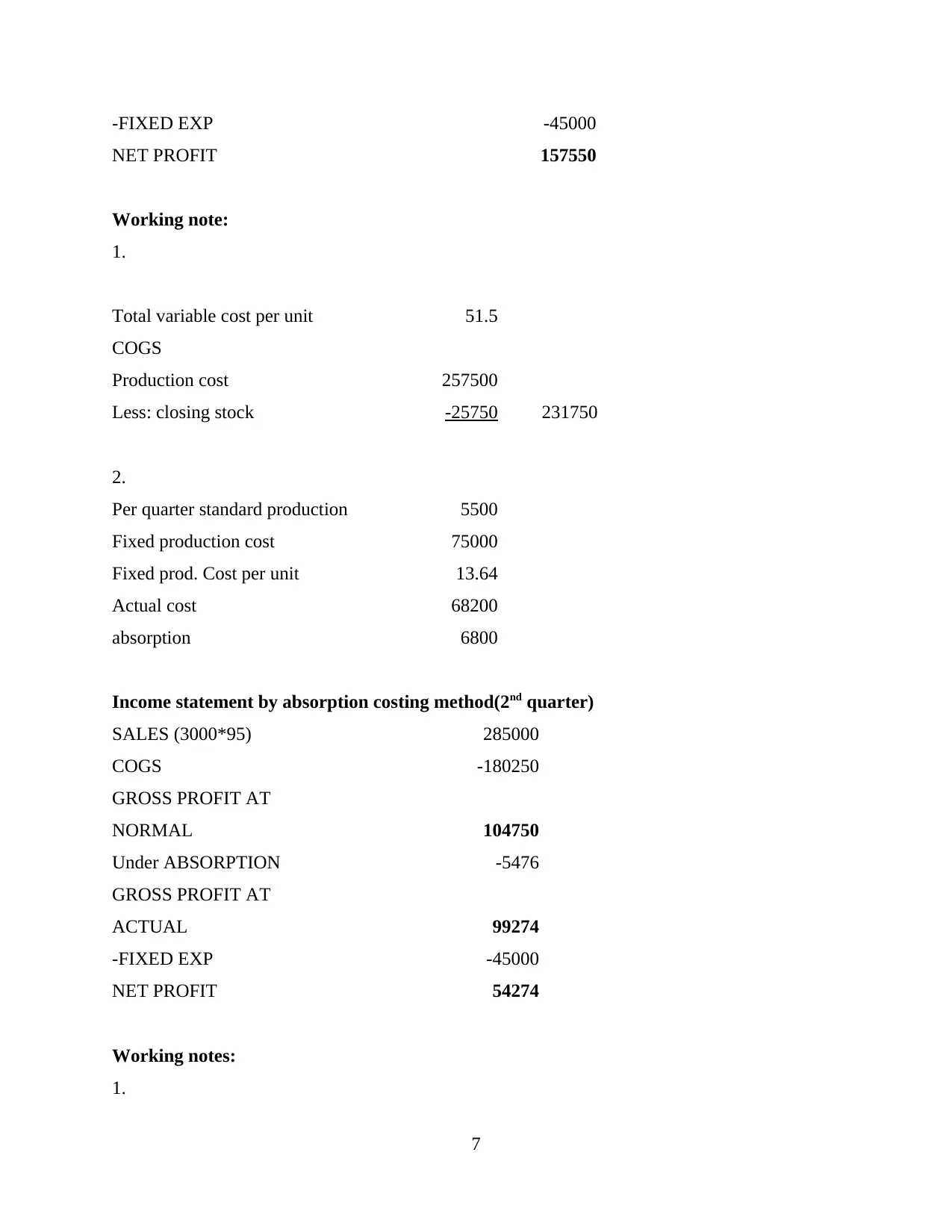

-FIXED EXP -45000

NET PROFIT 157550

Working note:

1.

Total variable cost per unit 51.5

COGS

Production cost 257500

Less: closing stock -25750 231750

2.

Per quarter standard production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 68200

absorption 6800

Income statement by absorption costing method(2nd quarter)

SALES (3000*95) 285000

COGS -180250

GROSS PROFIT AT

NORMAL 104750

Under ABSORPTION -5476

GROSS PROFIT AT

ACTUAL 99274

-FIXED EXP -45000

NET PROFIT 54274

Working notes:

1.

7

NET PROFIT 157550

Working note:

1.

Total variable cost per unit 51.5

COGS

Production cost 257500

Less: closing stock -25750 231750

2.

Per quarter standard production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 68200

absorption 6800

Income statement by absorption costing method(2nd quarter)

SALES (3000*95) 285000

COGS -180250

GROSS PROFIT AT

NORMAL 104750

Under ABSORPTION -5476

GROSS PROFIT AT

ACTUAL 99274

-FIXED EXP -45000

NET PROFIT 54274

Working notes:

1.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

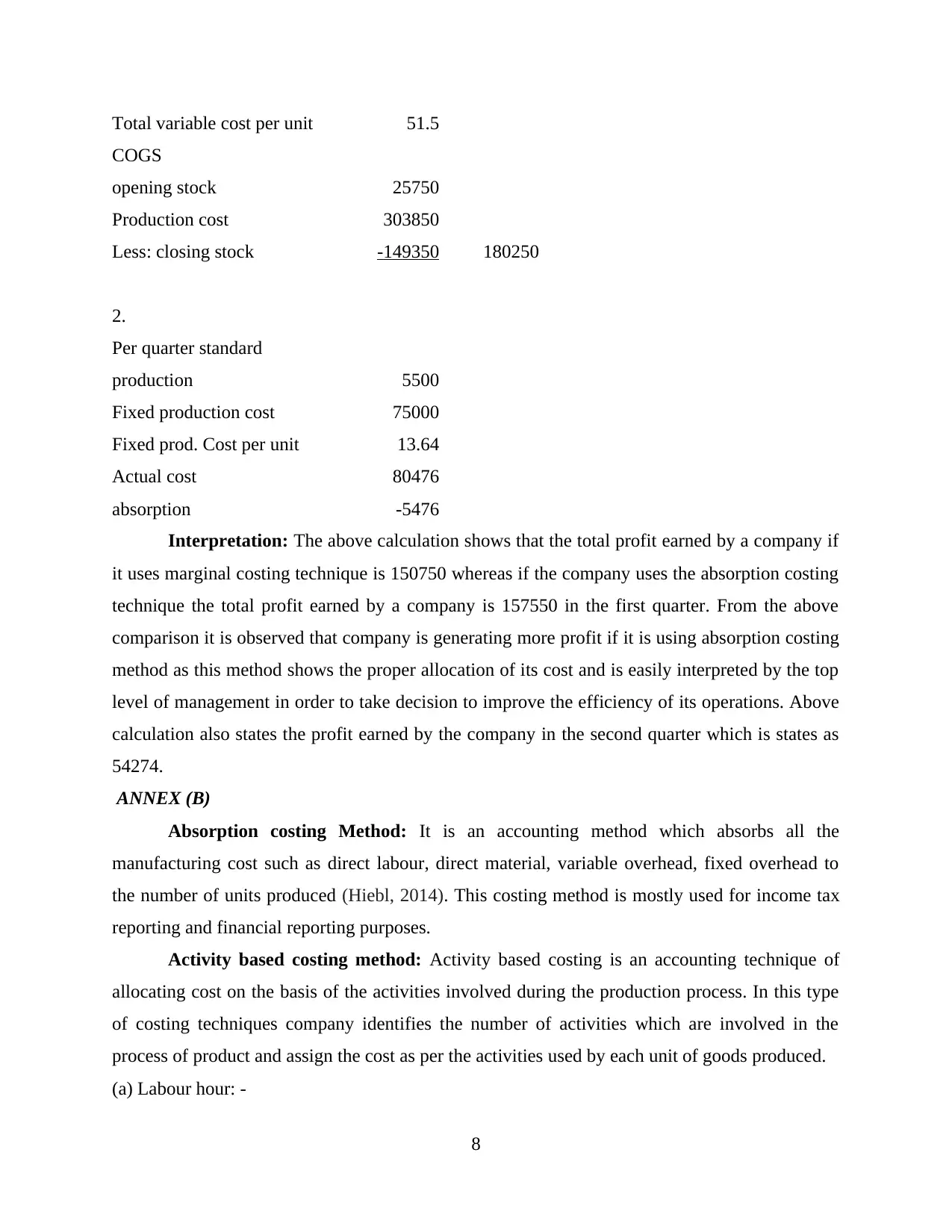

Total variable cost per unit 51.5

COGS

opening stock 25750

Production cost 303850

Less: closing stock -149350 180250

2.

Per quarter standard

production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 80476

absorption -5476

Interpretation: The above calculation shows that the total profit earned by a company if

it uses marginal costing technique is 150750 whereas if the company uses the absorption costing

technique the total profit earned by a company is 157550 in the first quarter. From the above

comparison it is observed that company is generating more profit if it is using absorption costing

method as this method shows the proper allocation of its cost and is easily interpreted by the top

level of management in order to take decision to improve the efficiency of its operations. Above

calculation also states the profit earned by the company in the second quarter which is states as

54274.

ANNEX (B)

Absorption costing Method: It is an accounting method which absorbs all the

manufacturing cost such as direct labour, direct material, variable overhead, fixed overhead to

the number of units produced (Hiebl, 2014). This costing method is mostly used for income tax

reporting and financial reporting purposes.

Activity based costing method: Activity based costing is an accounting technique of

allocating cost on the basis of the activities involved during the production process. In this type

of costing techniques company identifies the number of activities which are involved in the

process of product and assign the cost as per the activities used by each unit of goods produced.

(a) Labour hour: -

8

COGS

opening stock 25750

Production cost 303850

Less: closing stock -149350 180250

2.

Per quarter standard

production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 80476

absorption -5476

Interpretation: The above calculation shows that the total profit earned by a company if

it uses marginal costing technique is 150750 whereas if the company uses the absorption costing

technique the total profit earned by a company is 157550 in the first quarter. From the above

comparison it is observed that company is generating more profit if it is using absorption costing

method as this method shows the proper allocation of its cost and is easily interpreted by the top

level of management in order to take decision to improve the efficiency of its operations. Above

calculation also states the profit earned by the company in the second quarter which is states as

54274.

ANNEX (B)

Absorption costing Method: It is an accounting method which absorbs all the

manufacturing cost such as direct labour, direct material, variable overhead, fixed overhead to

the number of units produced (Hiebl, 2014). This costing method is mostly used for income tax

reporting and financial reporting purposes.

Activity based costing method: Activity based costing is an accounting technique of

allocating cost on the basis of the activities involved during the production process. In this type

of costing techniques company identifies the number of activities which are involved in the

process of product and assign the cost as per the activities used by each unit of goods produced.

(a) Labour hour: -

8

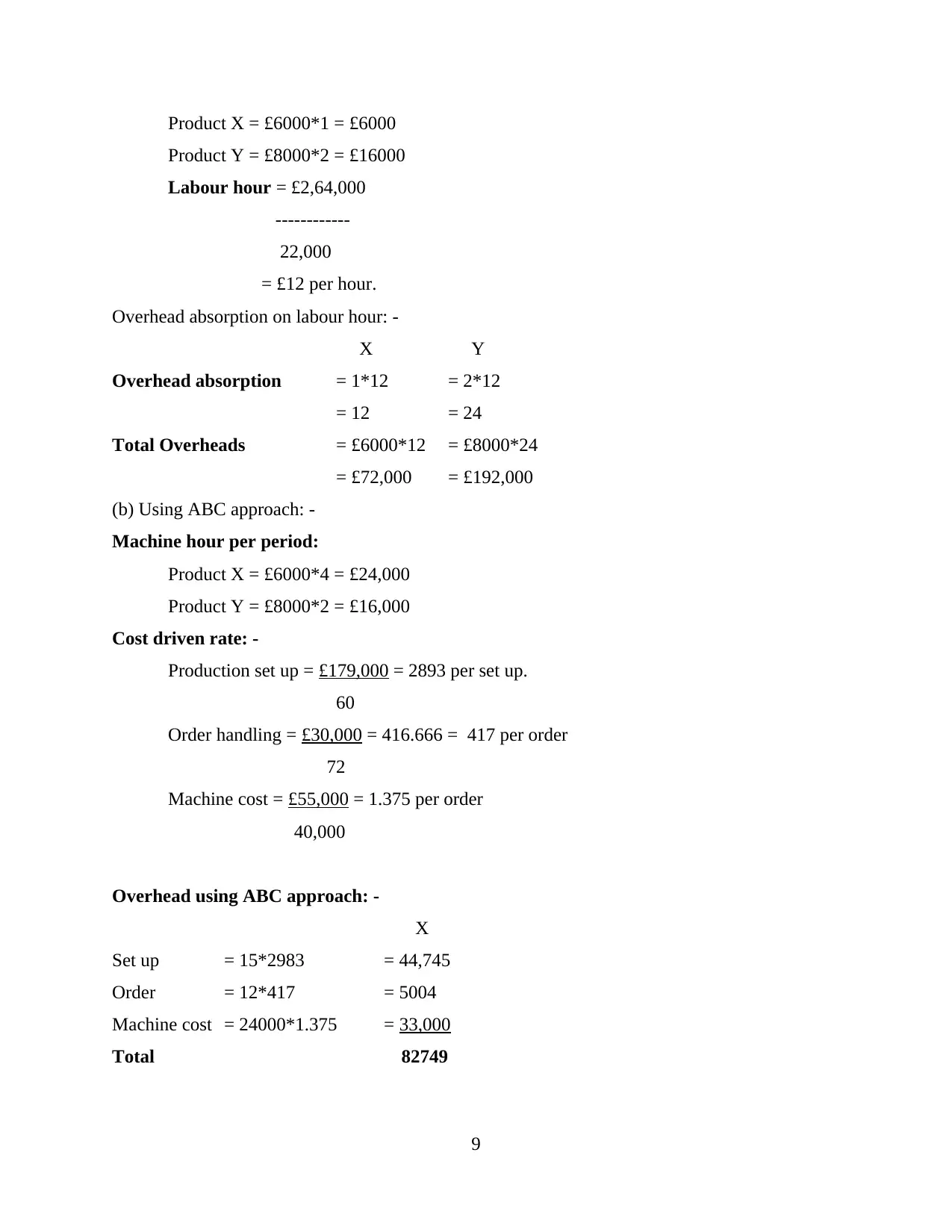

Product X = £6000*1 = £6000

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

= 12 = 24

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X = £6000*4 = £24,000

Product Y = £8000*2 = £16,000

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

9

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

= 12 = 24

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X = £6000*4 = £24,000

Product Y = £8000*2 = £16,000

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.