Financial Analysis and Management Accounting Report for AstraZeneca

VerifiedAdded on 2023/01/19

|25

|5615

|25

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within AstraZeneca, a pharmaceutical and biotechnology company. It begins with an overview of management accounting, its importance, and the different accounting systems used, including cost accounting, inventory management, price optimization, and job order costing. The report then delves into various management accounting reporting methods, such as inventory management reports, accounts receivable aging reports, and budget reports. The advantages of these systems are explained, along with their practical applications. The report also presents income statements developed using both marginal and absorption costing methods, illustrating the differences between the two approaches. Furthermore, the report explores the benefits and limitations of planning tools, such as budgetary control, and their application in developing and forecasting budgets. Finally, it examines how management accounting techniques can be used to solve financial issues, comparing different companies and their approaches to financial challenges. The report concludes with a summary of the key findings and insights gained throughout the analysis.

Name:

Registration Number

Date:

Is this a First Submission or Second Submission ?

Word Count

Turnitin Score

Learner’s statement of authenticity

I certify that the work submitted for this project is my own. Where the work of others

has been used to support my work then credit has been acknowledged. I have

identified and acknowledged all sources used in this project and have referenced

according to the Harvard referencing system. I have read and understood the

Plagiarism and Collusion section provided with the project brief and understood the

consequences of plagiarising.

Signature: ___________________ Date: ___/___/_____

wor

ds %

Registration Number

Date:

Is this a First Submission or Second Submission ?

Word Count

Turnitin Score

Learner’s statement of authenticity

I certify that the work submitted for this project is my own. Where the work of others

has been used to support my work then credit has been acknowledged. I have

identified and acknowledged all sources used in this project and have referenced

according to the Harvard referencing system. I have read and understood the

Plagiarism and Collusion section provided with the project brief and understood the

consequences of plagiarising.

Signature: ___________________ Date: ___/___/_____

wor

ds %

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and requirement of different accounting systems...................1

P2. Various method of accounting of management reporting...............................................3

M1. Advantages of management accounting systems and their application for context of

companies...............................................................................................................................5

D1 Management accounting system and reporting integrated with organisational process.. 6

TASK 2............................................................................................................................................6

P3. Development of income statements as per the marginal and absorption costing...........6

M2. Management accounting techniques to produce financial reports................................13

D2. Interpretation of produced financial statements............................................................13

TASK 3..........................................................................................................................................14

P4. Benefits and limitations of tools of planning ................................................................14

M3. Various types of planning tools and their application for developing and forecasting of

budget...................................................................................................................................15

TASK 4..........................................................................................................................................15

P5. Comparison of companies to solve the financial issues with the help of systems of

accounting.............................................................................................................................15

M4. Management accounting to solve the financial issues..................................................17

D3. Planning tools to solve the financial issues...................................................................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and requirement of different accounting systems...................1

P2. Various method of accounting of management reporting...............................................3

M1. Advantages of management accounting systems and their application for context of

companies...............................................................................................................................5

D1 Management accounting system and reporting integrated with organisational process.. 6

TASK 2............................................................................................................................................6

P3. Development of income statements as per the marginal and absorption costing...........6

M2. Management accounting techniques to produce financial reports................................13

D2. Interpretation of produced financial statements............................................................13

TASK 3..........................................................................................................................................14

P4. Benefits and limitations of tools of planning ................................................................14

M3. Various types of planning tools and their application for developing and forecasting of

budget...................................................................................................................................15

TASK 4..........................................................................................................................................15

P5. Comparison of companies to solve the financial issues with the help of systems of

accounting.............................................................................................................................15

M4. Management accounting to solve the financial issues..................................................17

D3. Planning tools to solve the financial issues...................................................................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION

Management Accounting can be explained as the procedure for maintaining all the

internal data of an organization through which better strategies can be formulated for achieving

organizational goals. It is necessary because it helps manager, directors, shareholder to analyse

about overall performance of the organization. Also, it gives idea to outsiders, whether they

should invest within the company or not. For this project, the chosen financial consultancy is

AstraZeneca. This company belongs to pharmaceutical and biotechnology industry. It offers

various types of pharmaceuticals products. It was founded in year 1999. Headquarter of company

is located in England, UK. Different planning tools in budgetary control will also be explained

with their pros and cons. Also, there will be explanation about how financial problem can be

resolved with the help of management accounting.

TASK 1

P1. Management accounting and requirement of different accounting systems.

As per the institute of Cost and Management Accountants, management accounting refers

to the use of professional skill and knowledge in prepartion of accounting information that helps

management in developing policies.

It involves methods and concepts that are essential for effectively plan for selecting among

alternative actions for interpretation of performance (Chenhall and Moers, 2015).

The role of management accounting includes recording, gathering and reporting financial

information from different units of firm and analysing the budget and suggesting allocation.

Its major role is to conduct budgeting. It guides company regarding all the expenditures (Jefrey,

ed., 2018).

It is the process of the system of accounting which helps directors of an organisation to

take any of the decision as per the situation arises in front of them. There are number of reports

which is being prepared by organization and all of those reports are directly related with

management accounting (Chenhall and Moers, 2015). In context of AstraZeneca, it has been

helpful for them because they are able to take any of the effective decision with the help of

management accounting. There are numbers of the system of management accounting and they

are:

1

Management Accounting can be explained as the procedure for maintaining all the

internal data of an organization through which better strategies can be formulated for achieving

organizational goals. It is necessary because it helps manager, directors, shareholder to analyse

about overall performance of the organization. Also, it gives idea to outsiders, whether they

should invest within the company or not. For this project, the chosen financial consultancy is

AstraZeneca. This company belongs to pharmaceutical and biotechnology industry. It offers

various types of pharmaceuticals products. It was founded in year 1999. Headquarter of company

is located in England, UK. Different planning tools in budgetary control will also be explained

with their pros and cons. Also, there will be explanation about how financial problem can be

resolved with the help of management accounting.

TASK 1

P1. Management accounting and requirement of different accounting systems.

As per the institute of Cost and Management Accountants, management accounting refers

to the use of professional skill and knowledge in prepartion of accounting information that helps

management in developing policies.

It involves methods and concepts that are essential for effectively plan for selecting among

alternative actions for interpretation of performance (Chenhall and Moers, 2015).

The role of management accounting includes recording, gathering and reporting financial

information from different units of firm and analysing the budget and suggesting allocation.

Its major role is to conduct budgeting. It guides company regarding all the expenditures (Jefrey,

ed., 2018).

It is the process of the system of accounting which helps directors of an organisation to

take any of the decision as per the situation arises in front of them. There are number of reports

which is being prepared by organization and all of those reports are directly related with

management accounting (Chenhall and Moers, 2015). In context of AstraZeneca, it has been

helpful for them because they are able to take any of the effective decision with the help of

management accounting. There are numbers of the system of management accounting and they

are:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost accounting system: In any of the organization, top-level management uses cost

accounting system for finding the actual price of any manufacturing products. It even helps them

to analyse any of the direct or indirect cost mainly occurs within business organization. In short,

it helps business organization to help collect all of relevant information related to expenses of a

company. It is being maintained by AstraZeneca, for the purpose of maintaining any of the

records which occurs during manufacturing process.

DIRECT COST- It refers to the expenditure that can be directly allocated to the production of

particular goods or services.

INDIRECT COST- These are those expenses that are incurred for proper working of the

business. They cannot be directly attributed to a cost object. It includes fixed cost that remain

fixed inspite of change in volume of sales. Variable cost that changes with a change in volume of

sales.

Inventory Management System: It is helpful for this company which are engaged

within manufacturing process. AstraZeneca applies IMS so that they can easily maintain all of

the records which are taken while conducting manufacturing process. (Englund and Gerdin,

2014). There are three types of Inventory management systems such as FIFO, LIFO & AVCO.

When it comes to FIFO, the products which where bough in beginning are needed to be used

whereas in case of LIFO, the products which are bough recently is needed to be used for

manufacturing process. In case of AVCO, production is needed to be done on the basis of

average cost. In case of AstraZeneca, they use FIFO for manufacturing process because that

helps them to maintain the data related to inventories and whole of the procedure can be

conducted in systematic manner.

EOQ- It is the proper quantity that should be purchased by firm to reduce cost of inventory like

shortage cost, holding cost, order cost etc.

ROP- Reorder point is the quantity that triggers the buying of a specific amount of

replenishment stock.

JIT- It is the strategy of management that integrate orders of raw material from suppliers directly

with schedule of production.

Price Optimisation System: The most important accounting system for management is

the system of price optimization because it helps to set the standard price of product which has

been manufactured. Also, it tries to find whether expectation of customers is meet or not with

2

accounting system for finding the actual price of any manufacturing products. It even helps them

to analyse any of the direct or indirect cost mainly occurs within business organization. In short,

it helps business organization to help collect all of relevant information related to expenses of a

company. It is being maintained by AstraZeneca, for the purpose of maintaining any of the

records which occurs during manufacturing process.

DIRECT COST- It refers to the expenditure that can be directly allocated to the production of

particular goods or services.

INDIRECT COST- These are those expenses that are incurred for proper working of the

business. They cannot be directly attributed to a cost object. It includes fixed cost that remain

fixed inspite of change in volume of sales. Variable cost that changes with a change in volume of

sales.

Inventory Management System: It is helpful for this company which are engaged

within manufacturing process. AstraZeneca applies IMS so that they can easily maintain all of

the records which are taken while conducting manufacturing process. (Englund and Gerdin,

2014). There are three types of Inventory management systems such as FIFO, LIFO & AVCO.

When it comes to FIFO, the products which where bough in beginning are needed to be used

whereas in case of LIFO, the products which are bough recently is needed to be used for

manufacturing process. In case of AVCO, production is needed to be done on the basis of

average cost. In case of AstraZeneca, they use FIFO for manufacturing process because that

helps them to maintain the data related to inventories and whole of the procedure can be

conducted in systematic manner.

EOQ- It is the proper quantity that should be purchased by firm to reduce cost of inventory like

shortage cost, holding cost, order cost etc.

ROP- Reorder point is the quantity that triggers the buying of a specific amount of

replenishment stock.

JIT- It is the strategy of management that integrate orders of raw material from suppliers directly

with schedule of production.

Price Optimisation System: The most important accounting system for management is

the system of price optimization because it helps to set the standard price of product which has

been manufactured. Also, it tries to find whether expectation of customers is meet or not with

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

price range which has been decided by organization. In context of AstraZeneca, they help to

select the price of the clothes so that it can be sold within the marketplace at reasonable price.

Job Order Costing System: It is the method of costing which is used by organisation in

the situation where products are manufactured on the basis of specific order by any of the

customers. It helps to determine accurate cost of product through which it can be easily found

whether company is having loss or profit in any of the job. In context of AstraZeneca, they uses

job order costing system because they manufacture different variety of product where price are

different and it can easily calculated with the help of this accounting system.

P2. Various method of accounting of management reporting.

Management accounting reporting can be explained as the procedure which delivers

different types of information regarding daily basis operation which is being managed within the

company (Maas, Schaltegger and Crutzen, 2016). Some of the management accounting reports

are explained below:

Inventory management report- This report contains any of the information which is

related with the stock available within the company and that helps organisation to

calculate that when they are required reorder raw material. Here, Production department

of AstraZeneca uses this report just to find actual amount of product which they have

manufactured and additional amount of raw material which they will require in future.

Account receivable ageing report- This management accounting is being prepared for

the purpose of finding the debtors who are unable to clear their account even after the

end of deadlines. This report is helpful in deciding whether organisation should allow for

future credit dealings or not (Melnyk and et. al., 2014). In short helps to determine the

relationship between organization and their customers who deals in credit facilities.

While talking about AstraZeneca, their finance department is responsible for this report

where they check which debtors is needed to pay debt amount to organization.

Cost accounting report- In this report it is being checked that what is the total expenses

that company has incurred while conducting any of the particular activity. It is helpful

for company because they can easily find the expenses incurred in conducting any of the

activity. AstraZeneca requires to prepare this particular report in order to manage the

overall cost while manufacturing clothing products.

3

select the price of the clothes so that it can be sold within the marketplace at reasonable price.

Job Order Costing System: It is the method of costing which is used by organisation in

the situation where products are manufactured on the basis of specific order by any of the

customers. It helps to determine accurate cost of product through which it can be easily found

whether company is having loss or profit in any of the job. In context of AstraZeneca, they uses

job order costing system because they manufacture different variety of product where price are

different and it can easily calculated with the help of this accounting system.

P2. Various method of accounting of management reporting.

Management accounting reporting can be explained as the procedure which delivers

different types of information regarding daily basis operation which is being managed within the

company (Maas, Schaltegger and Crutzen, 2016). Some of the management accounting reports

are explained below:

Inventory management report- This report contains any of the information which is

related with the stock available within the company and that helps organisation to

calculate that when they are required reorder raw material. Here, Production department

of AstraZeneca uses this report just to find actual amount of product which they have

manufactured and additional amount of raw material which they will require in future.

Account receivable ageing report- This management accounting is being prepared for

the purpose of finding the debtors who are unable to clear their account even after the

end of deadlines. This report is helpful in deciding whether organisation should allow for

future credit dealings or not (Melnyk and et. al., 2014). In short helps to determine the

relationship between organization and their customers who deals in credit facilities.

While talking about AstraZeneca, their finance department is responsible for this report

where they check which debtors is needed to pay debt amount to organization.

Cost accounting report- In this report it is being checked that what is the total expenses

that company has incurred while conducting any of the particular activity. It is helpful

for company because they can easily find the expenses incurred in conducting any of the

activity. AstraZeneca requires to prepare this particular report in order to manage the

overall cost while manufacturing clothing products.

3

Budget report- These reports are very important in measuring the performance of firm

and are generated for various departments. Every firm develop overall budget yto

understand the overall scheme of business.

Performance report- These reports are developed to review the performance of firm as

a whole and for individual employee's.

4

and are generated for various departments. Every firm develop overall budget yto

understand the overall scheme of business.

Performance report- These reports are developed to review the performance of firm as

a whole and for individual employee's.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

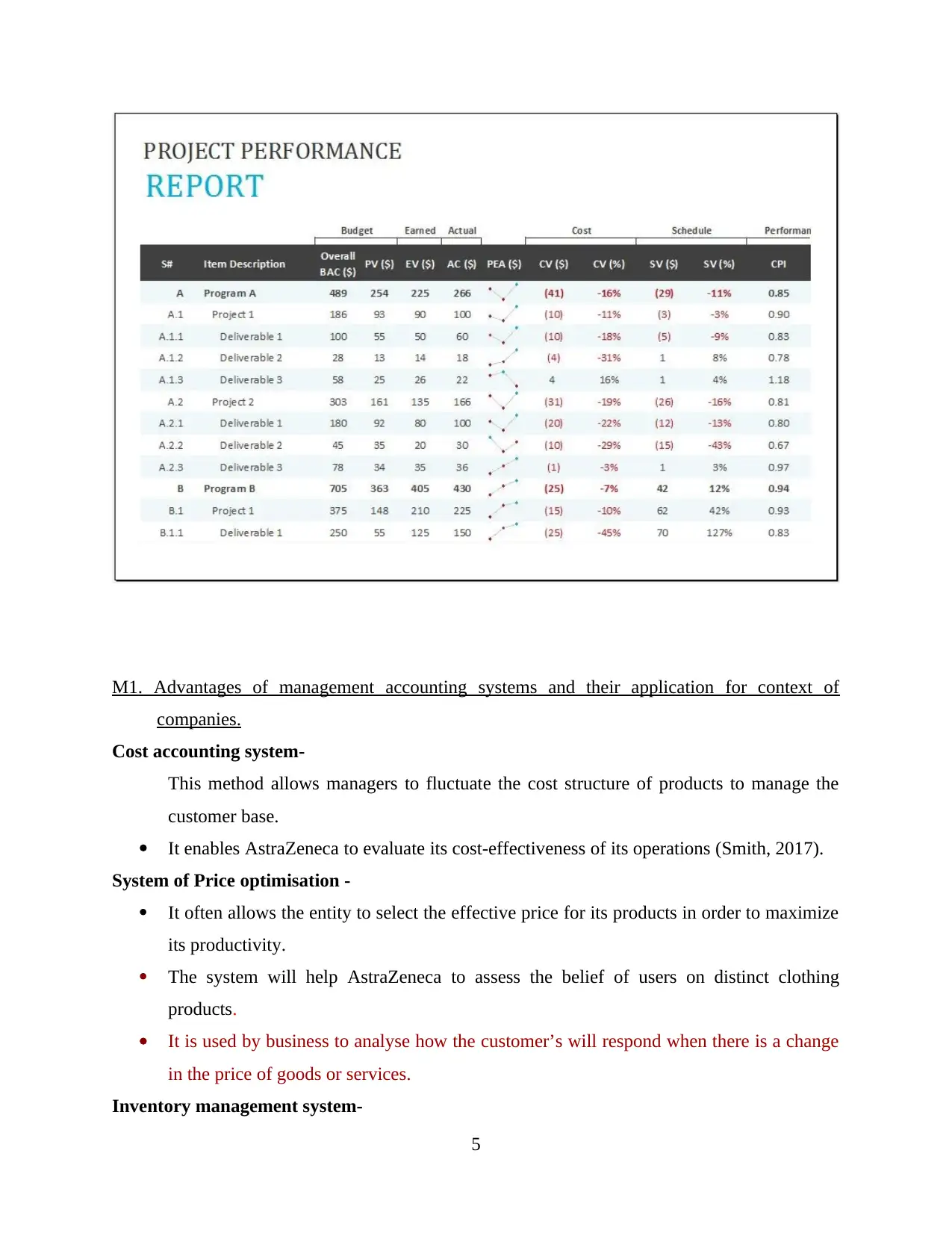

M1. Advantages of management accounting systems and their application for context of

companies.

Cost accounting system-

This method allows managers to fluctuate the cost structure of products to manage the

customer base.

It enables AstraZeneca to evaluate its cost-effectiveness of its operations (Smith, 2017).

System of Price optimisation -

It often allows the entity to select the effective price for its products in order to maximize

its productivity.

The system will help AstraZeneca to assess the belief of users on distinct clothing

products.

It is used by business to analyse how the customer’s will respond when there is a change

in the price of goods or services.

Inventory management system-

5

companies.

Cost accounting system-

This method allows managers to fluctuate the cost structure of products to manage the

customer base.

It enables AstraZeneca to evaluate its cost-effectiveness of its operations (Smith, 2017).

System of Price optimisation -

It often allows the entity to select the effective price for its products in order to maximize

its productivity.

The system will help AstraZeneca to assess the belief of users on distinct clothing

products.

It is used by business to analyse how the customer’s will respond when there is a change

in the price of goods or services.

Inventory management system-

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

By depleting the stock, an organization can minimize its costs, maximize revenues, or

maximize benefit.

It is very useful system for organization because it will assist to preserve the records of

stock with accuracy.

It is used for by manufacturing firms to develop a work order, production related

documents and bill of materials.

D1 Management accounting system and reporting integrated with organisational process.

Most of the accounting monitoring system is connected with the managerial reporting. A

further example that works with both the regime of the cost measurement system to facilitate the

industry along with determining the exact cost of all its products (Tucker and Lowe, 2014). This

declaration could be comprehended using the instance as when the program introduced

throughout the enterprise of its stock management so all the operations linked to the inventory

could be acquired through coverage of inventory control.

TASK 2.

P3. Development of income statements as per the marginal and absorption costing.

Absorption costing- In these types of costing techniques, both variable & fixed cost are

assumed as cost of unit or even product too. This types of costing methods are mainly

used in this organisation who need to perform business activity at a greater platform

(Nitzl, 2016)(Quattrone, 2016).

Marginal costing- Here, it is necessary to take fixed cost as periodic cost whereas

variable cost is known as unit cost. Fixed cost does not change for certain period within

marginal costing.

6

maximize benefit.

It is very useful system for organization because it will assist to preserve the records of

stock with accuracy.

It is used for by manufacturing firms to develop a work order, production related

documents and bill of materials.

D1 Management accounting system and reporting integrated with organisational process.

Most of the accounting monitoring system is connected with the managerial reporting. A

further example that works with both the regime of the cost measurement system to facilitate the

industry along with determining the exact cost of all its products (Tucker and Lowe, 2014). This

declaration could be comprehended using the instance as when the program introduced

throughout the enterprise of its stock management so all the operations linked to the inventory

could be acquired through coverage of inventory control.

TASK 2.

P3. Development of income statements as per the marginal and absorption costing.

Absorption costing- In these types of costing techniques, both variable & fixed cost are

assumed as cost of unit or even product too. This types of costing methods are mainly

used in this organisation who need to perform business activity at a greater platform

(Nitzl, 2016)(Quattrone, 2016).

Marginal costing- Here, it is necessary to take fixed cost as periodic cost whereas

variable cost is known as unit cost. Fixed cost does not change for certain period within

marginal costing.

6

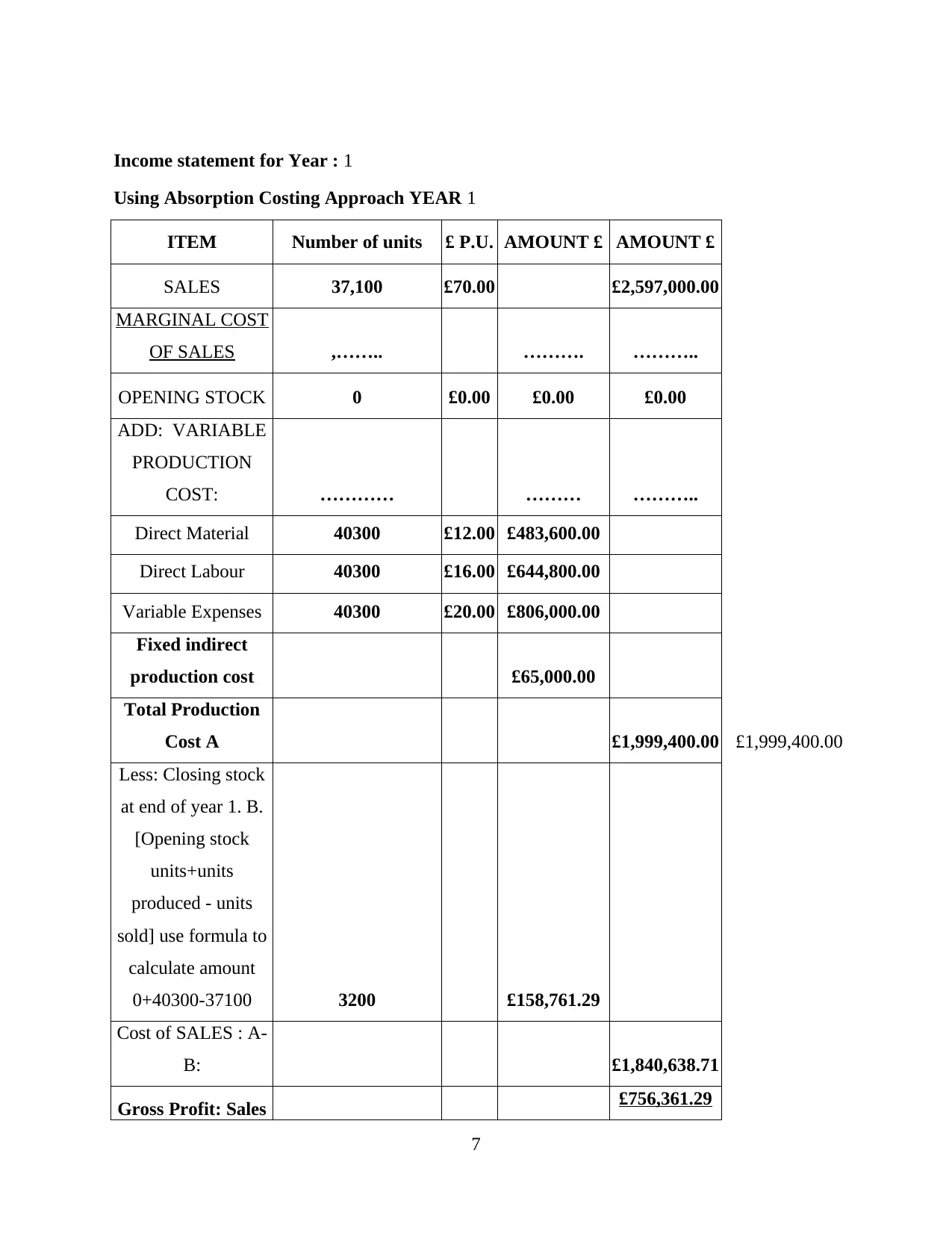

Income statement for Year : 1

Using Absorption Costing Approach YEAR 1

ITEM Number of units £ P.U. AMOUNT £ AMOUNT £

SALES 37,100 £70.00 £2,597,000.00

MARGINAL COST

OF SALES ,…….. ………. ………..

OPENING STOCK 0 £0.00 £0.00 £0.00

ADD: VARIABLE

PRODUCTION

COST: ………… ……… ………..

Direct Material 40300 £12.00 £483,600.00

Direct Labour 40300 £16.00 £644,800.00

Variable Expenses 40300 £20.00 £806,000.00

Fixed indirect

production cost £65,000.00

Total Production

Cost A £1,999,400.00 £1,999,400.00

Less: Closing stock

at end of year 1. B.

[Opening stock

units+units

produced - units

sold] use formula to

calculate amount

0+40300-37100 3200 £158,761.29

Cost of SALES : A-

B: £1,840,638.71

Gross Profit: Sales £756,361.29

7

Using Absorption Costing Approach YEAR 1

ITEM Number of units £ P.U. AMOUNT £ AMOUNT £

SALES 37,100 £70.00 £2,597,000.00

MARGINAL COST

OF SALES ,…….. ………. ………..

OPENING STOCK 0 £0.00 £0.00 £0.00

ADD: VARIABLE

PRODUCTION

COST: ………… ……… ………..

Direct Material 40300 £12.00 £483,600.00

Direct Labour 40300 £16.00 £644,800.00

Variable Expenses 40300 £20.00 £806,000.00

Fixed indirect

production cost £65,000.00

Total Production

Cost A £1,999,400.00 £1,999,400.00

Less: Closing stock

at end of year 1. B.

[Opening stock

units+units

produced - units

sold] use formula to

calculate amount

0+40300-37100 3200 £158,761.29

Cost of SALES : A-

B: £1,840,638.71

Gross Profit: Sales £756,361.29

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

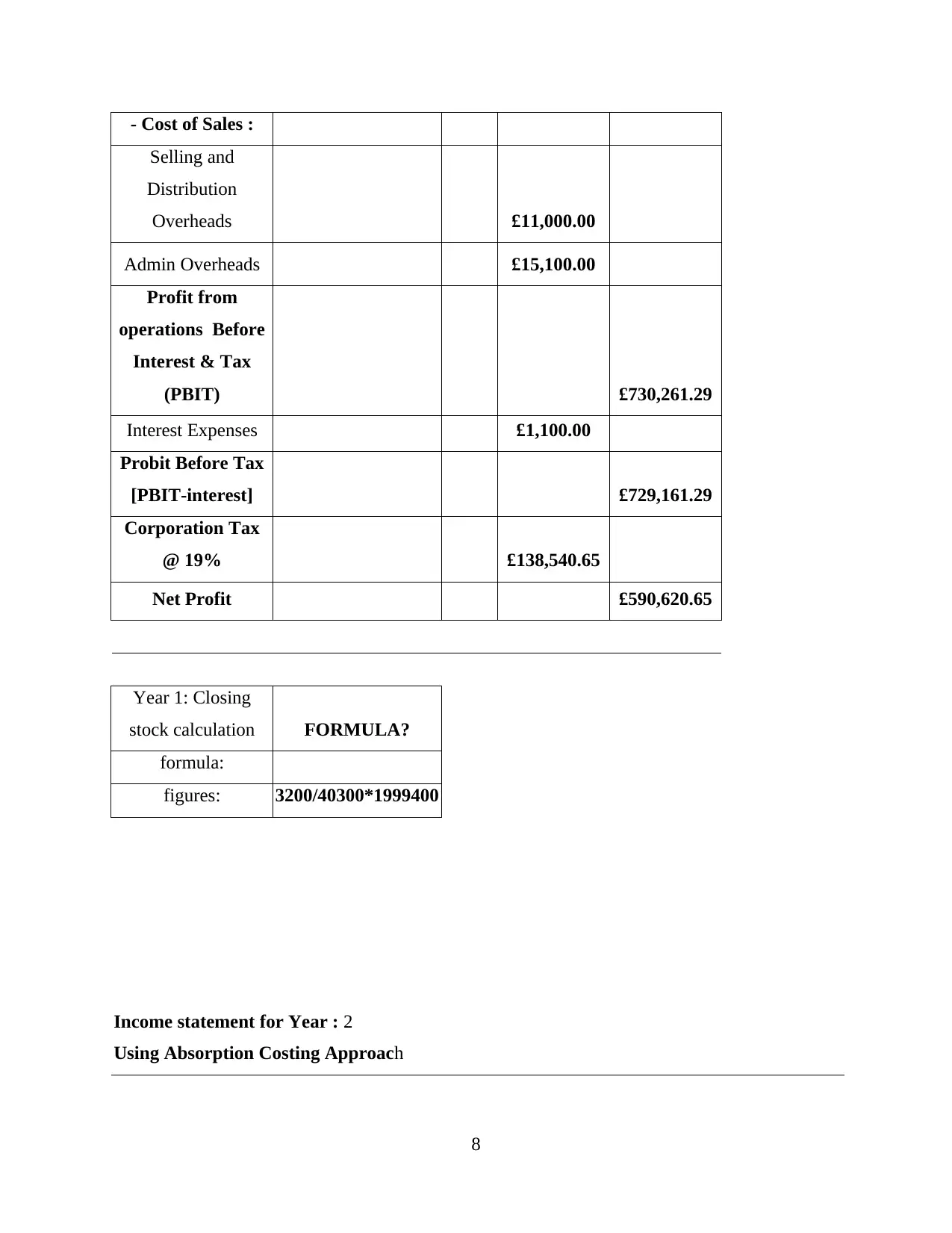

- Cost of Sales :

Selling and

Distribution

Overheads £11,000.00

Admin Overheads £15,100.00

Profit from

operations Before

Interest & Tax

(PBIT) £730,261.29

Interest Expenses £1,100.00

Probit Before Tax

[PBIT-interest] £729,161.29

Corporation Tax

@ 19% £138,540.65

Net Profit £590,620.65

Year 1: Closing

stock calculation FORMULA?

formula:

figures: 3200/40300*1999400

Income statement for Year : 2

Using Absorption Costing Approach

8

Selling and

Distribution

Overheads £11,000.00

Admin Overheads £15,100.00

Profit from

operations Before

Interest & Tax

(PBIT) £730,261.29

Interest Expenses £1,100.00

Probit Before Tax

[PBIT-interest] £729,161.29

Corporation Tax

@ 19% £138,540.65

Net Profit £590,620.65

Year 1: Closing

stock calculation FORMULA?

formula:

figures: 3200/40300*1999400

Income statement for Year : 2

Using Absorption Costing Approach

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

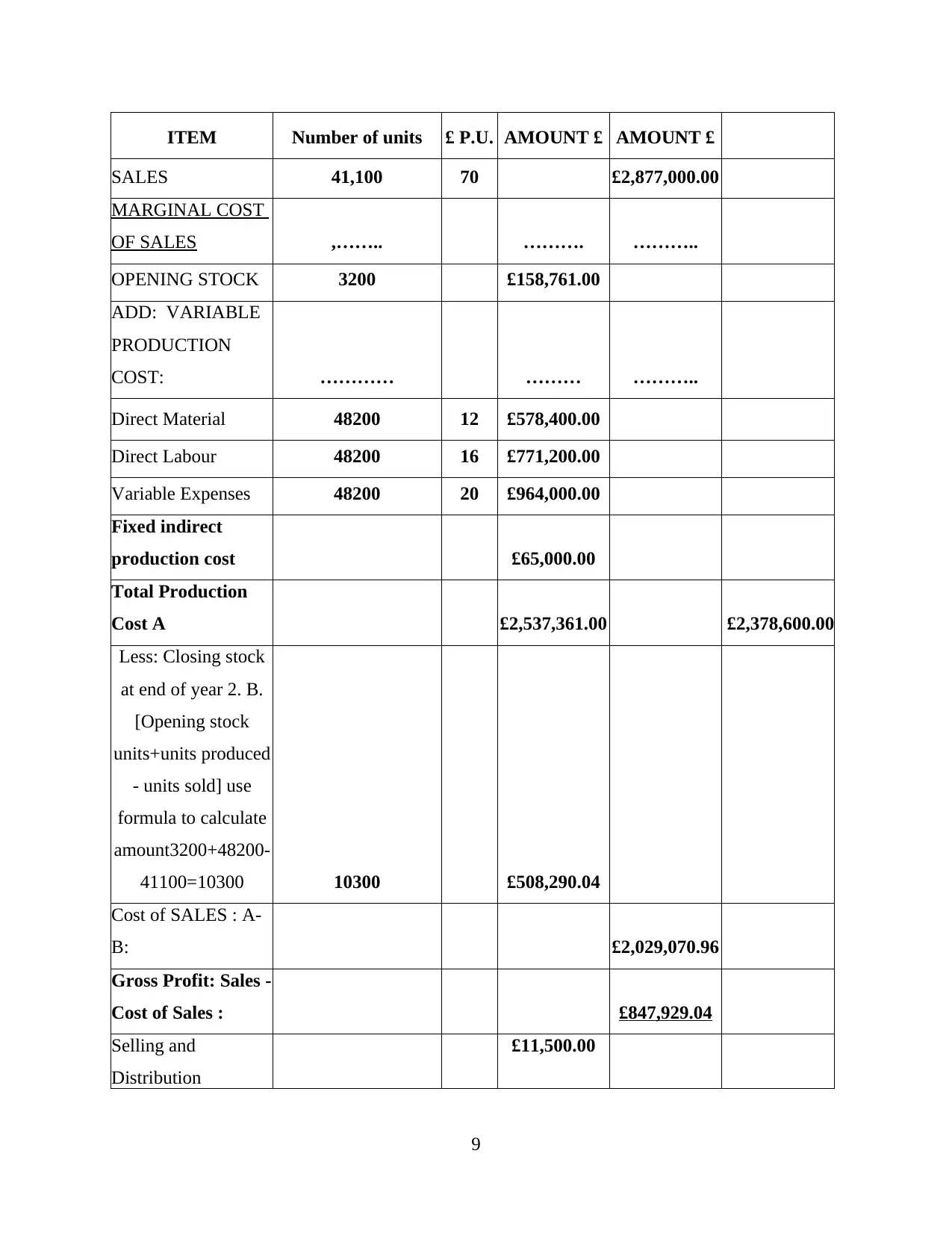

ITEM Number of units £ P.U. AMOUNT £ AMOUNT £

SALES 41,100 70 £2,877,000.00

MARGINAL COST

OF SALES ,…….. ………. ………..

OPENING STOCK 3200 £158,761.00

ADD: VARIABLE

PRODUCTION

COST: ………… ……… ………..

Direct Material 48200 12 £578,400.00

Direct Labour 48200 16 £771,200.00

Variable Expenses 48200 20 £964,000.00

Fixed indirect

production cost £65,000.00

Total Production

Cost A £2,537,361.00 £2,378,600.00

Less: Closing stock

at end of year 2. B.

[Opening stock

units+units produced

- units sold] use

formula to calculate

amount3200+48200-

41100=10300 10300 £508,290.04

Cost of SALES : A-

B: £2,029,070.96

Gross Profit: Sales -

Cost of Sales : £847,929.04

Selling and

Distribution

£11,500.00

9

SALES 41,100 70 £2,877,000.00

MARGINAL COST

OF SALES ,…….. ………. ………..

OPENING STOCK 3200 £158,761.00

ADD: VARIABLE

PRODUCTION

COST: ………… ……… ………..

Direct Material 48200 12 £578,400.00

Direct Labour 48200 16 £771,200.00

Variable Expenses 48200 20 £964,000.00

Fixed indirect

production cost £65,000.00

Total Production

Cost A £2,537,361.00 £2,378,600.00

Less: Closing stock

at end of year 2. B.

[Opening stock

units+units produced

- units sold] use

formula to calculate

amount3200+48200-

41100=10300 10300 £508,290.04

Cost of SALES : A-

B: £2,029,070.96

Gross Profit: Sales -

Cost of Sales : £847,929.04

Selling and

Distribution

£11,500.00

9

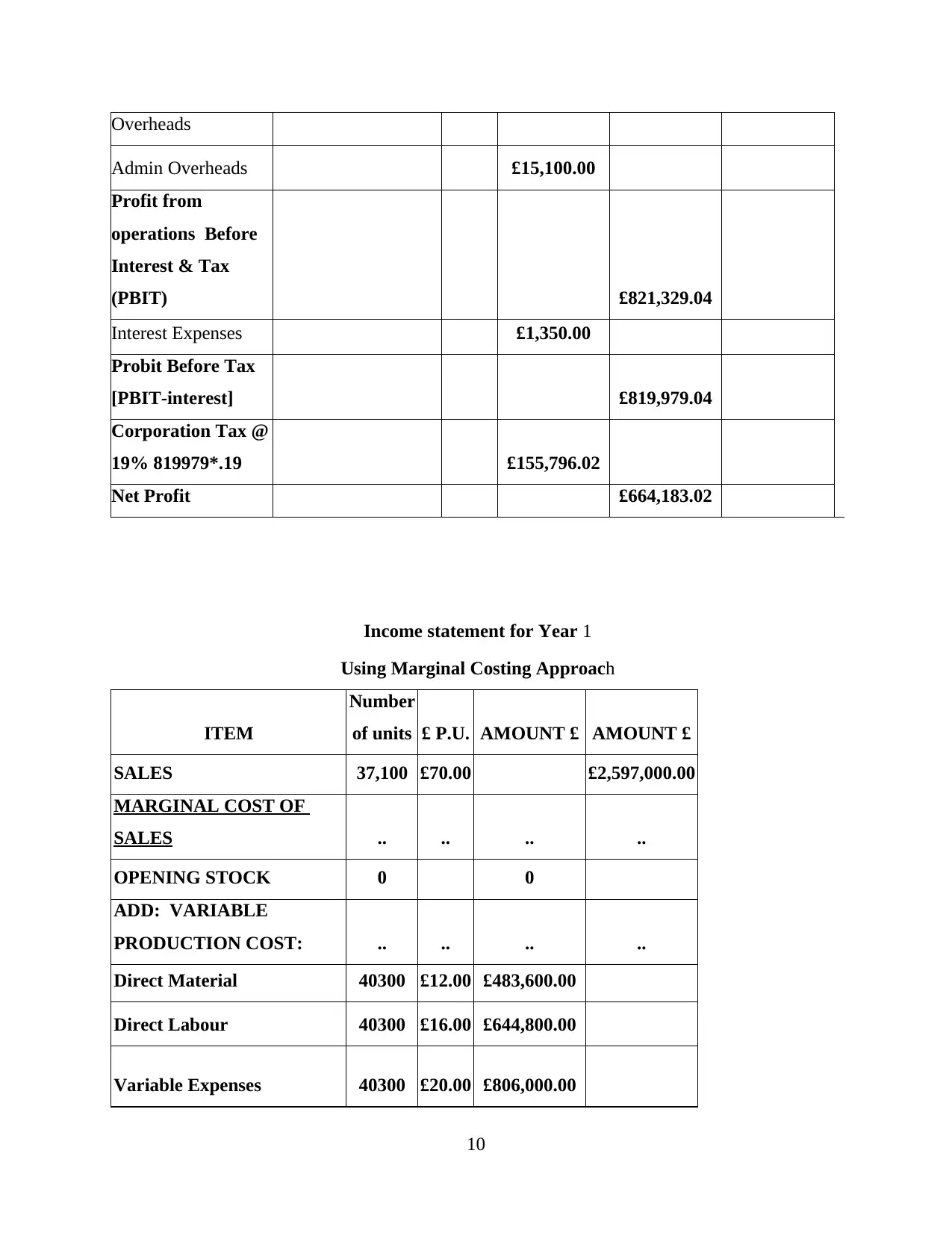

Overheads

Admin Overheads £15,100.00

Profit from

operations Before

Interest & Tax

(PBIT) £821,329.04

Interest Expenses £1,350.00

Probit Before Tax

[PBIT-interest] £819,979.04

Corporation Tax @

19% 819979*.19 £155,796.02

Net Profit £664,183.02

Income statement for Year 1

Using Marginal Costing Approach

ITEM

Number

of units £ P.U. AMOUNT £ AMOUNT £

SALES 37,100 £70.00 £2,597,000.00

MARGINAL COST OF

SALES .. .. .. ..

OPENING STOCK 0 0

ADD: VARIABLE

PRODUCTION COST: .. .. .. ..

Direct Material 40300 £12.00 £483,600.00

Direct Labour 40300 £16.00 £644,800.00

Variable Expenses 40300 £20.00 £806,000.00

10

Admin Overheads £15,100.00

Profit from

operations Before

Interest & Tax

(PBIT) £821,329.04

Interest Expenses £1,350.00

Probit Before Tax

[PBIT-interest] £819,979.04

Corporation Tax @

19% 819979*.19 £155,796.02

Net Profit £664,183.02

Income statement for Year 1

Using Marginal Costing Approach

ITEM

Number

of units £ P.U. AMOUNT £ AMOUNT £

SALES 37,100 £70.00 £2,597,000.00

MARGINAL COST OF

SALES .. .. .. ..

OPENING STOCK 0 0

ADD: VARIABLE

PRODUCTION COST: .. .. .. ..

Direct Material 40300 £12.00 £483,600.00

Direct Labour 40300 £16.00 £644,800.00

Variable Expenses 40300 £20.00 £806,000.00

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.