Management Accounting Report: Analysis of BAT's Business Structure

VerifiedAdded on 2023/06/03

|8

|1851

|454

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices applicable to British American Tobacco (BAT). It begins with an introduction to management accounting and its importance, followed by a discussion of various tools such as budgetary control, standard costing, benchmarking, and cash flow analysis. The report then applies absorption and marginal costing techniques to BAT's products (B&H Strawberry and B&H Cherry) to determine selling prices and profitability. Findings highlight the need for improvements in BAT's costing system, including a switch to activity-based costing and the adoption of budgetary control and benchmarking techniques. The conclusion summarizes the key findings and recommendations for enhancing BAT's business structure through effective management accounting practices.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGEMENT ACCOUNTING

Table of Contents

1.0 Introduction................................................................................................................................2

2.0 Discussion..................................................................................................................................2

2.1 Importance of Management Accounting...............................................................................2

2.2 Range of Management Accounting Tools.............................................................................3

2.3 Application of Management Accounting Tool......................................................................4

2.4 Findings and Recommendations............................................................................................5

3.0 Conclusion.................................................................................................................................6

4.0 Reference...................................................................................................................................7

MANAGEMENT ACCOUNTING

Table of Contents

1.0 Introduction................................................................................................................................2

2.0 Discussion..................................................................................................................................2

2.1 Importance of Management Accounting...............................................................................2

2.2 Range of Management Accounting Tools.............................................................................3

2.3 Application of Management Accounting Tool......................................................................4

2.4 Findings and Recommendations............................................................................................5

3.0 Conclusion.................................................................................................................................6

4.0 Reference...................................................................................................................................7

2

MANAGEMENT ACCOUNTING

1.0 Introduction

The main purpose of this assessment is to analyse the business structure of British

American Tobacco and identify the management accounting practices which can be beneficial

for the business. The management of the company is considering two of its products such as

B&H Strawberry and B&H Cherry and comparison between the costs and prices of the products

would be considered for the analysis (Maas, Schaltegger and Crutzen 2016). The assessment

would be focusing on the importance of management accounting tools which are applicable on

the business. The assessment would be assessing the importance of such tools in business and

recommend best alternative management tool available to the business.

2.0 Discussion

2.1 Importance of Management Accounting

Management accounting may be defined as the process of applying tools and formulating

management reports for the purpose of taking important management decisions of the business.

The management accounting tools can be used effectively for the purpose of taking major

decisions relating to the business (Contrafatto and Burns 2013). Management accounting is an

internal management tool which can be used for internal decision making and it is directly

responsible for improving the business structure. In the case of BAT, management accounting

tools can be used for the purpose improving the decision-making process of the business and also

improve the overall business structure. The importance of management accounting tools in the

business of BAT is be further explained in details below:

Forecasting of Future: One of the key advantages of using management accounting tool

in the business of BAT is that it can help the management in forecasting the future more

effectively. The management can forecast revenues of the business effectively and

thereby as per the estimation plan for achieving the targets of the business.

Decision Making Process: Some of the management accounting tool are used

extensively for the purpose of taking major decisions for the business. For instances,

budgeting is a tool which can be used by the management of company for setting targets

for revenue and costs and take major decisions accordingly.

MANAGEMENT ACCOUNTING

1.0 Introduction

The main purpose of this assessment is to analyse the business structure of British

American Tobacco and identify the management accounting practices which can be beneficial

for the business. The management of the company is considering two of its products such as

B&H Strawberry and B&H Cherry and comparison between the costs and prices of the products

would be considered for the analysis (Maas, Schaltegger and Crutzen 2016). The assessment

would be focusing on the importance of management accounting tools which are applicable on

the business. The assessment would be assessing the importance of such tools in business and

recommend best alternative management tool available to the business.

2.0 Discussion

2.1 Importance of Management Accounting

Management accounting may be defined as the process of applying tools and formulating

management reports for the purpose of taking important management decisions of the business.

The management accounting tools can be used effectively for the purpose of taking major

decisions relating to the business (Contrafatto and Burns 2013). Management accounting is an

internal management tool which can be used for internal decision making and it is directly

responsible for improving the business structure. In the case of BAT, management accounting

tools can be used for the purpose improving the decision-making process of the business and also

improve the overall business structure. The importance of management accounting tools in the

business of BAT is be further explained in details below:

Forecasting of Future: One of the key advantages of using management accounting tool

in the business of BAT is that it can help the management in forecasting the future more

effectively. The management can forecast revenues of the business effectively and

thereby as per the estimation plan for achieving the targets of the business.

Decision Making Process: Some of the management accounting tool are used

extensively for the purpose of taking major decisions for the business. For instances,

budgeting is a tool which can be used by the management of company for setting targets

for revenue and costs and take major decisions accordingly.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGEMENT ACCOUNTING

Combating Competitive Pressure: Another importance of management accounting tool is

that the same is used by management of a company for combating competitive pressure

in the market (Agasisti and Johnes 2015). There are tools such as benchmarking, business

process reengineering which are used by the management of company to bring about

changes in the business and appropriately meet market rivalry. In the case of BAT, the

management of the company recognises that the competition in the market is immense so

management accounting tools are of utmost importance for the business.

Allocation of Costs: The allocation of costs is an important consideration which the

management of BAT needs to consider as the same has direct impact on the selling price

and profitability of the products which is offered by the business. The management needs

to appropriately allocate the overhead costs for which it has the option of using either

marginal costing techniques or absorption costing techniques (Bromwich and Scapens

2016). These techniques are more often used in the business for the purpose of treating

the overhead costs of the business.

2.2 Range of Management Accounting Tools

There are a wide range of management accounting tools which are available to

management for improving the structure of the business effectively. The different types of tools

which are available to BAT are listed below in details:

Budgetary Control: The management of the company needs to appropriately formulate

budgets which can be used for forecasting and planning of expenses and revenues which

are associated with the business (Lewis 2013). The management of the company can also

use budgets for the purpose of controlling the activities of the business and ensure that

the same are as per the goals and objectives of the business. Budgets are also a means for

ensuring effective communication is established between different departments. Standard Costing: Another important tool which is available to the management of the

company is standard costing which allows the management of the company to make

comparisons between actual results and budgeted results and identify the variance in

results (Griffith, Stephenson and Watson 2014). The standard costing is a tool which can

appropriate control the activities of the business and it is mainly used along with budgets

so that comparisons can be made effectively.

MANAGEMENT ACCOUNTING

Combating Competitive Pressure: Another importance of management accounting tool is

that the same is used by management of a company for combating competitive pressure

in the market (Agasisti and Johnes 2015). There are tools such as benchmarking, business

process reengineering which are used by the management of company to bring about

changes in the business and appropriately meet market rivalry. In the case of BAT, the

management of the company recognises that the competition in the market is immense so

management accounting tools are of utmost importance for the business.

Allocation of Costs: The allocation of costs is an important consideration which the

management of BAT needs to consider as the same has direct impact on the selling price

and profitability of the products which is offered by the business. The management needs

to appropriately allocate the overhead costs for which it has the option of using either

marginal costing techniques or absorption costing techniques (Bromwich and Scapens

2016). These techniques are more often used in the business for the purpose of treating

the overhead costs of the business.

2.2 Range of Management Accounting Tools

There are a wide range of management accounting tools which are available to

management for improving the structure of the business effectively. The different types of tools

which are available to BAT are listed below in details:

Budgetary Control: The management of the company needs to appropriately formulate

budgets which can be used for forecasting and planning of expenses and revenues which

are associated with the business (Lewis 2013). The management of the company can also

use budgets for the purpose of controlling the activities of the business and ensure that

the same are as per the goals and objectives of the business. Budgets are also a means for

ensuring effective communication is established between different departments. Standard Costing: Another important tool which is available to the management of the

company is standard costing which allows the management of the company to make

comparisons between actual results and budgeted results and identify the variance in

results (Griffith, Stephenson and Watson 2014). The standard costing is a tool which can

appropriate control the activities of the business and it is mainly used along with budgets

so that comparisons can be made effectively.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGEMENT ACCOUNTING

Benchmarking: This is another effective tool which is used by the management of the

company for making comparisons between their business structure and the business

structure of its competitors (Santini 2013). The management of BAT needs to consider

this tool as the level of competition in the market is immense and this can help the

management to effective formulate plans for combatting competition in the market. Cash Flow analysis: This is another very important tool which can significantly help in

the decision-making process of the business. The cash flow statement helps the

management to identify the cash inflows and outflows of the business and appropriately

take decisions regarding the cash flows of the business. The cash flow analysis is also

useful for taking liquidity decisions.

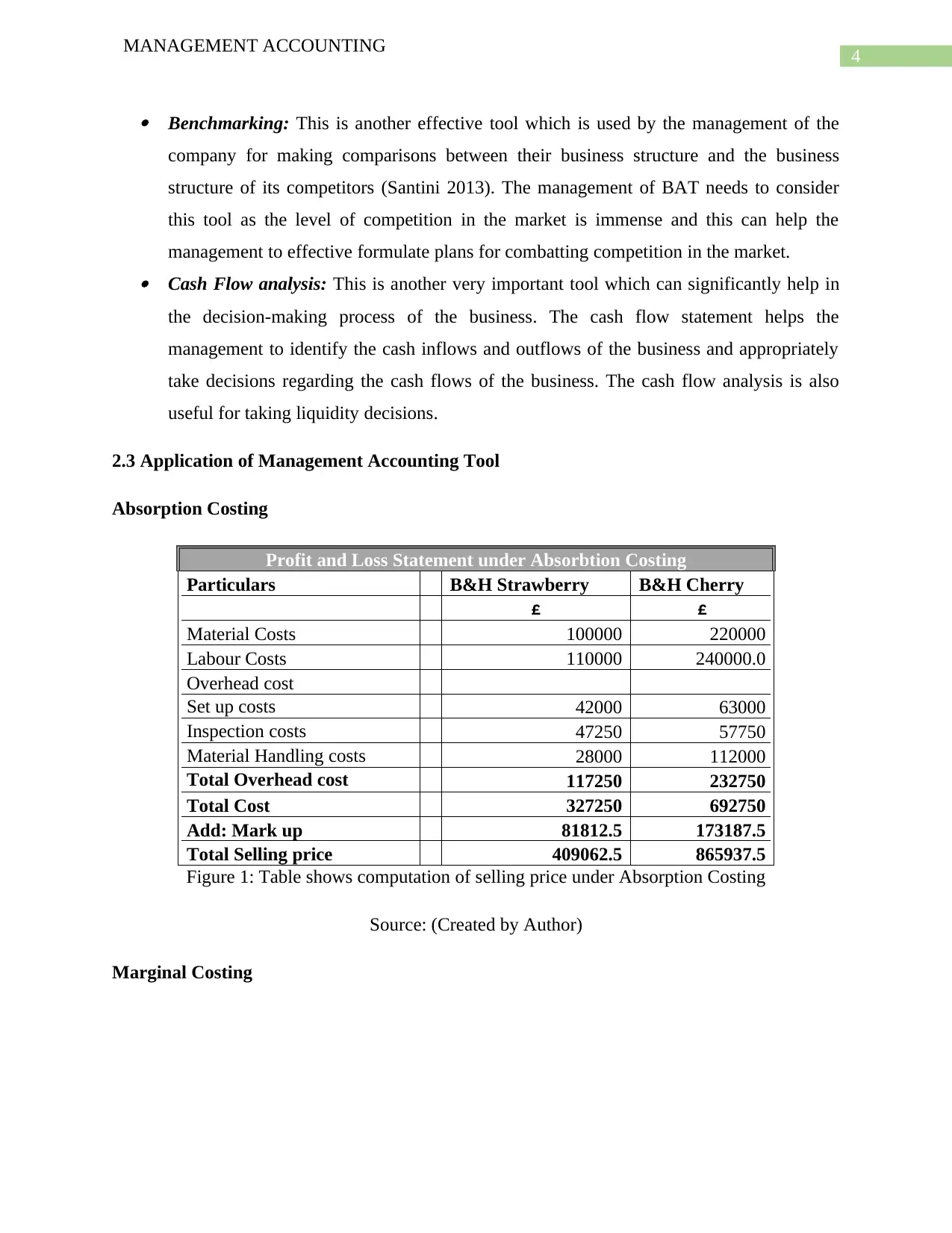

2.3 Application of Management Accounting Tool

Absorption Costing

Profit and Loss Statement under Absorbtion Costing

Particulars B&H Strawberry B&H Cherry

£ £

Material Costs 100000 220000

Labour Costs 110000 240000.0

Overhead cost

Set up costs 42000 63000

Inspection costs 47250 57750

Material Handling costs 28000 112000

Total Overhead cost 117250 232750

Total Cost 327250 692750

Add: Mark up 81812.5 173187.5

Total Selling price 409062.5 865937.5

Figure 1: Table shows computation of selling price under Absorption Costing

Source: (Created by Author)

Marginal Costing

MANAGEMENT ACCOUNTING

Benchmarking: This is another effective tool which is used by the management of the

company for making comparisons between their business structure and the business

structure of its competitors (Santini 2013). The management of BAT needs to consider

this tool as the level of competition in the market is immense and this can help the

management to effective formulate plans for combatting competition in the market. Cash Flow analysis: This is another very important tool which can significantly help in

the decision-making process of the business. The cash flow statement helps the

management to identify the cash inflows and outflows of the business and appropriately

take decisions regarding the cash flows of the business. The cash flow analysis is also

useful for taking liquidity decisions.

2.3 Application of Management Accounting Tool

Absorption Costing

Profit and Loss Statement under Absorbtion Costing

Particulars B&H Strawberry B&H Cherry

£ £

Material Costs 100000 220000

Labour Costs 110000 240000.0

Overhead cost

Set up costs 42000 63000

Inspection costs 47250 57750

Material Handling costs 28000 112000

Total Overhead cost 117250 232750

Total Cost 327250 692750

Add: Mark up 81812.5 173187.5

Total Selling price 409062.5 865937.5

Figure 1: Table shows computation of selling price under Absorption Costing

Source: (Created by Author)

Marginal Costing

5

MANAGEMENT ACCOUNTING

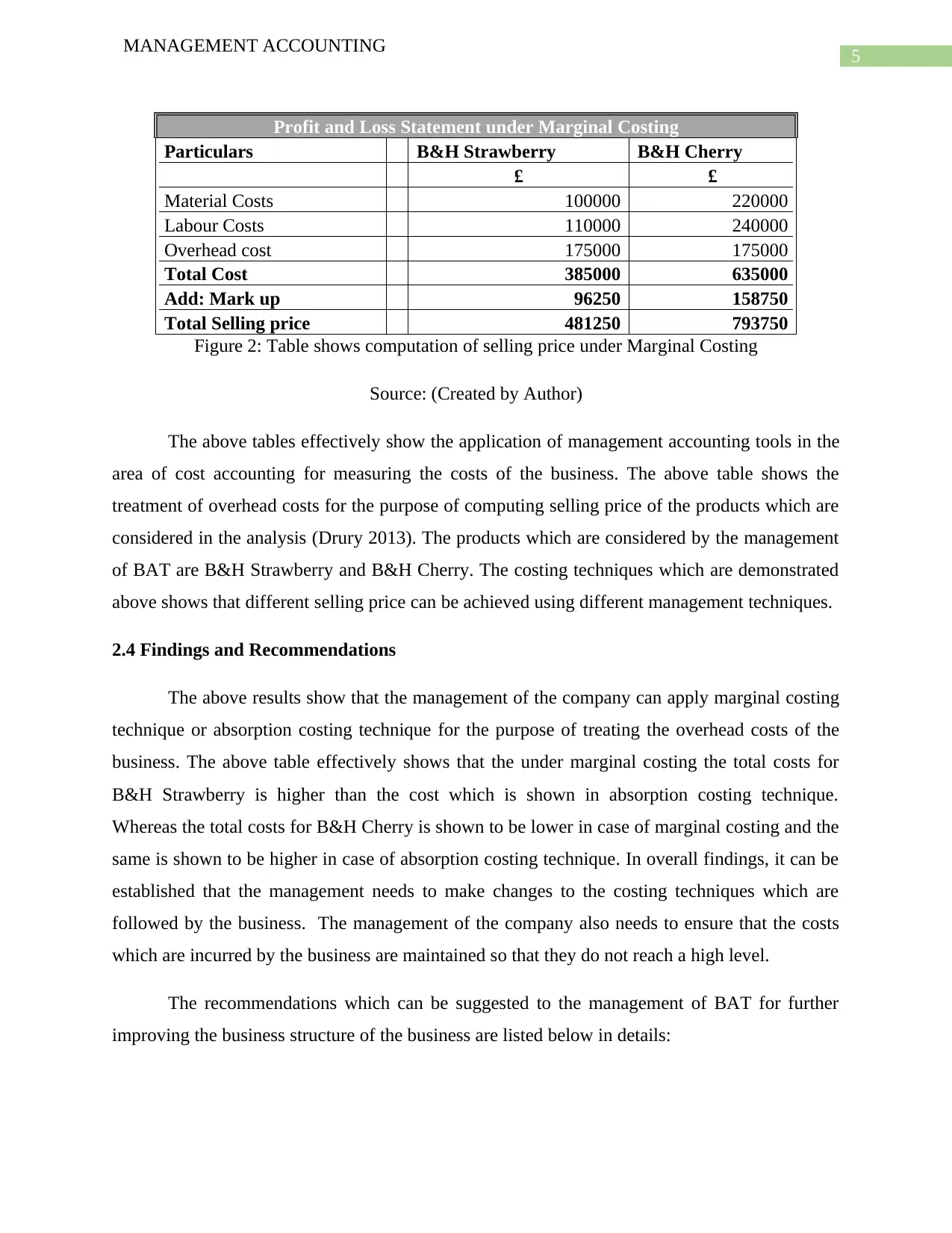

Profit and Loss Statement under Marginal Costing

Particulars B&H Strawberry B&H Cherry

£ £

Material Costs 100000 220000

Labour Costs 110000 240000

Overhead cost 175000 175000

Total Cost 385000 635000

Add: Mark up 96250 158750

Total Selling price 481250 793750

Figure 2: Table shows computation of selling price under Marginal Costing

Source: (Created by Author)

The above tables effectively show the application of management accounting tools in the

area of cost accounting for measuring the costs of the business. The above table shows the

treatment of overhead costs for the purpose of computing selling price of the products which are

considered in the analysis (Drury 2013). The products which are considered by the management

of BAT are B&H Strawberry and B&H Cherry. The costing techniques which are demonstrated

above shows that different selling price can be achieved using different management techniques.

2.4 Findings and Recommendations

The above results show that the management of the company can apply marginal costing

technique or absorption costing technique for the purpose of treating the overhead costs of the

business. The above table effectively shows that the under marginal costing the total costs for

B&H Strawberry is higher than the cost which is shown in absorption costing technique.

Whereas the total costs for B&H Cherry is shown to be lower in case of marginal costing and the

same is shown to be higher in case of absorption costing technique. In overall findings, it can be

established that the management needs to make changes to the costing techniques which are

followed by the business. The management of the company also needs to ensure that the costs

which are incurred by the business are maintained so that they do not reach a high level.

The recommendations which can be suggested to the management of BAT for further

improving the business structure of the business are listed below in details:

MANAGEMENT ACCOUNTING

Profit and Loss Statement under Marginal Costing

Particulars B&H Strawberry B&H Cherry

£ £

Material Costs 100000 220000

Labour Costs 110000 240000

Overhead cost 175000 175000

Total Cost 385000 635000

Add: Mark up 96250 158750

Total Selling price 481250 793750

Figure 2: Table shows computation of selling price under Marginal Costing

Source: (Created by Author)

The above tables effectively show the application of management accounting tools in the

area of cost accounting for measuring the costs of the business. The above table shows the

treatment of overhead costs for the purpose of computing selling price of the products which are

considered in the analysis (Drury 2013). The products which are considered by the management

of BAT are B&H Strawberry and B&H Cherry. The costing techniques which are demonstrated

above shows that different selling price can be achieved using different management techniques.

2.4 Findings and Recommendations

The above results show that the management of the company can apply marginal costing

technique or absorption costing technique for the purpose of treating the overhead costs of the

business. The above table effectively shows that the under marginal costing the total costs for

B&H Strawberry is higher than the cost which is shown in absorption costing technique.

Whereas the total costs for B&H Cherry is shown to be lower in case of marginal costing and the

same is shown to be higher in case of absorption costing technique. In overall findings, it can be

established that the management needs to make changes to the costing techniques which are

followed by the business. The management of the company also needs to ensure that the costs

which are incurred by the business are maintained so that they do not reach a high level.

The recommendations which can be suggested to the management of BAT for further

improving the business structure of the business are listed below in details:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGEMENT ACCOUNTING

The management of the company needs to switch to activity based costing techniques so

that a proper costing structure of the business can be established.

The management of BAT needs to adopt budgetary control techniques along with

standards costing so that proper control can be maintained over the activities of the

business. The management can also forecast and plan effectively for all activities of the

business using budgets.

The management can also appropriately use benchmarking techniques for the purpose of

competing effectively with other businesses which are operating in the market. The

management can also appropriately manage the activities of the business and bring about

efficiency in the operations of the business.

3.0 Conclusion

The above discussion shows that the management of British American Tobacco needs to

implement management accounting tools for the purpose of improving the business structure.

The management needs to implement a better costing system so that the costing structure of the

business can be improved. The assessment also considers computations of marginal costing

techniques and absorption costings. The assessment suggests certain amendments which can be

brought about in the business in order to improve the business structure.

MANAGEMENT ACCOUNTING

The management of the company needs to switch to activity based costing techniques so

that a proper costing structure of the business can be established.

The management of BAT needs to adopt budgetary control techniques along with

standards costing so that proper control can be maintained over the activities of the

business. The management can also forecast and plan effectively for all activities of the

business using budgets.

The management can also appropriately use benchmarking techniques for the purpose of

competing effectively with other businesses which are operating in the market. The

management can also appropriately manage the activities of the business and bring about

efficiency in the operations of the business.

3.0 Conclusion

The above discussion shows that the management of British American Tobacco needs to

implement management accounting tools for the purpose of improving the business structure.

The management needs to implement a better costing system so that the costing structure of the

business can be improved. The assessment also considers computations of marginal costing

techniques and absorption costings. The assessment suggests certain amendments which can be

brought about in the business in order to improve the business structure.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGEMENT ACCOUNTING

4.0 Reference

Agasisti, T. and Johnes, G., 2015. Efficiency, costs, rankings and heterogeneity: the case of US

higher education. Studies in Higher Education, 40(1), pp.60-82.

Bromwich, M. and Scapens, R.W., 2016. Management accounting research: 25 years

on. Management Accounting Research, 31, pp.1-9.

Contrafatto, M. and Burns, J., 2013. Social and environmental accounting, organisational change

and management accounting: A processual view. Management Accounting Research, 24(4),

pp.349-365.

Drury, C., 2013. Costing: an introduction. Springer.

Griffith, A., Stephenson, P. and Watson, P., 2014. Management systems for construction.

Routledge.

Lewis, W.A., 2013. Overhead costs (Vol. 6). Routledge.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production, 136, pp.237-

248.

Santini, F., 2013. Strategic Management Accounting and financial performance in the small and

medium sized Italian manufacturing enterprises. Management Control.

MANAGEMENT ACCOUNTING

4.0 Reference

Agasisti, T. and Johnes, G., 2015. Efficiency, costs, rankings and heterogeneity: the case of US

higher education. Studies in Higher Education, 40(1), pp.60-82.

Bromwich, M. and Scapens, R.W., 2016. Management accounting research: 25 years

on. Management Accounting Research, 31, pp.1-9.

Contrafatto, M. and Burns, J., 2013. Social and environmental accounting, organisational change

and management accounting: A processual view. Management Accounting Research, 24(4),

pp.349-365.

Drury, C., 2013. Costing: an introduction. Springer.

Griffith, A., Stephenson, P. and Watson, P., 2014. Management systems for construction.

Routledge.

Lewis, W.A., 2013. Overhead costs (Vol. 6). Routledge.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production, 136, pp.237-

248.

Santini, F., 2013. Strategic Management Accounting and financial performance in the small and

medium sized Italian manufacturing enterprises. Management Control.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.