Bizdaq's Management Accounting Systems and Reporting - Unit 5

VerifiedAdded on 2020/09/17

|19

|5901

|52

Report

AI Summary

This report provides a detailed analysis of management accounting principles and their application to the fictional company, Bizdaq. The report begins with an introduction to management accounting, emphasizing its role in decision-making and performance management. It then explores various management accounting systems, including inventory management, price optimization, job costing, and cost accounting, providing practical applications for Bizdaq. The report also covers different management accounting report methods such as budget reports, accounts receivable aging reports, job cost reports, inventory and manufacturing reports, and income statement reports, explaining their uses and benefits. The report further delves into the differences between marginal costing and absorption costing, demonstrating how to calculate income statements using both methods. It examines the advantages and disadvantages of different planning tools for budgetary control, and discusses the adoption of management accounting systems to address financial troubles, offering strategic recommendations for Bizdaq. The report concludes with a summary of the key findings and recommendations.

UNIT 5

MANAGEMENT

ACCOUNTING

MANAGEMENT

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Report to General Manager regarding concept of management accounting and

requirements of their types to company......................................................................................1

P2 Report to General manager regarding explanation of methods of management accounting

reports..........................................................................................................................................4

TASK 2............................................................................................................................................7

P3 Difference between Marginal costing and Absorption costing and calculation of Income

statement through these methods:...............................................................................................7

TASK 3..........................................................................................................................................11

P4 Report to General manager regarding advantages and disadvantage of different types of

planning tools for budgetary control.........................................................................................11

P5 Adopting management accounting systems for responding financial troubles..................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Report to General Manager regarding concept of management accounting and

requirements of their types to company......................................................................................1

P2 Report to General manager regarding explanation of methods of management accounting

reports..........................................................................................................................................4

TASK 2............................................................................................................................................7

P3 Difference between Marginal costing and Absorption costing and calculation of Income

statement through these methods:...............................................................................................7

TASK 3..........................................................................................................................................11

P4 Report to General manager regarding advantages and disadvantage of different types of

planning tools for budgetary control.........................................................................................11

P5 Adopting management accounting systems for responding financial troubles..................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting is the process in which managers utilises the guidelines and

regulations of data's of accounting to assess in decision-making system of an enterprises.

Management accounting consists of provisions which guides top management for dealing with

financial and non-financial informations for decision-making process (Armstrong and Taylor,

2014). Hence Management accounting is a procedure which involves make or buy decisions,

planning for allocation and performance management of a company. It also assists with the

proficiency while creating financial reports for management support.

Bizdaq was started in 2015 and its main business is sales, as it deals with only sale

projects. It's annual turnover is around £100,000 and less than 50 employees work in this

company. This assignment is based on the discussion of different types of management

accounting systems with various methods. This assignment is divided on the basis two different

scenario's, in first scenario, a report is written which concentrates on execution of accounting

techniques for business success. In second scenario, financial problem faced by Bizdaq is

discussed and a perfect resolution to deal with such a issue is given and explained to General

manager in a report.

The main focus of this report is to apply management accounting techniques like profit

analysis, marginal costs and absorption costs.

Management accounting is the process in which managers utilises the guidelines and

regulations of data's of accounting to assess in decision-making system of an enterprises.

Management accounting consists of provisions which guides top management for dealing with

financial and non-financial informations for decision-making process (Armstrong and Taylor,

2014). Hence Management accounting is a procedure which involves make or buy decisions,

planning for allocation and performance management of a company. It also assists with the

proficiency while creating financial reports for management support.

Bizdaq was started in 2015 and its main business is sales, as it deals with only sale

projects. It's annual turnover is around £100,000 and less than 50 employees work in this

company. This assignment is based on the discussion of different types of management

accounting systems with various methods. This assignment is divided on the basis two different

scenario's, in first scenario, a report is written which concentrates on execution of accounting

techniques for business success. In second scenario, financial problem faced by Bizdaq is

discussed and a perfect resolution to deal with such a issue is given and explained to General

manager in a report.

The main focus of this report is to apply management accounting techniques like profit

analysis, marginal costs and absorption costs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 1

P1 Report to General Manager regarding concept of management accounting and requirements

of their types to company

From: Management accounting officer

To: General manager of Bizdaq

Sub: Management accounting system

This report is focused on Management accounting concepts and it will explain how accounting

systems works. Various management accounting systems and their types like Inventory

management system, Price optimisation, Job costing system and Cost accounting system has

been described in this report.

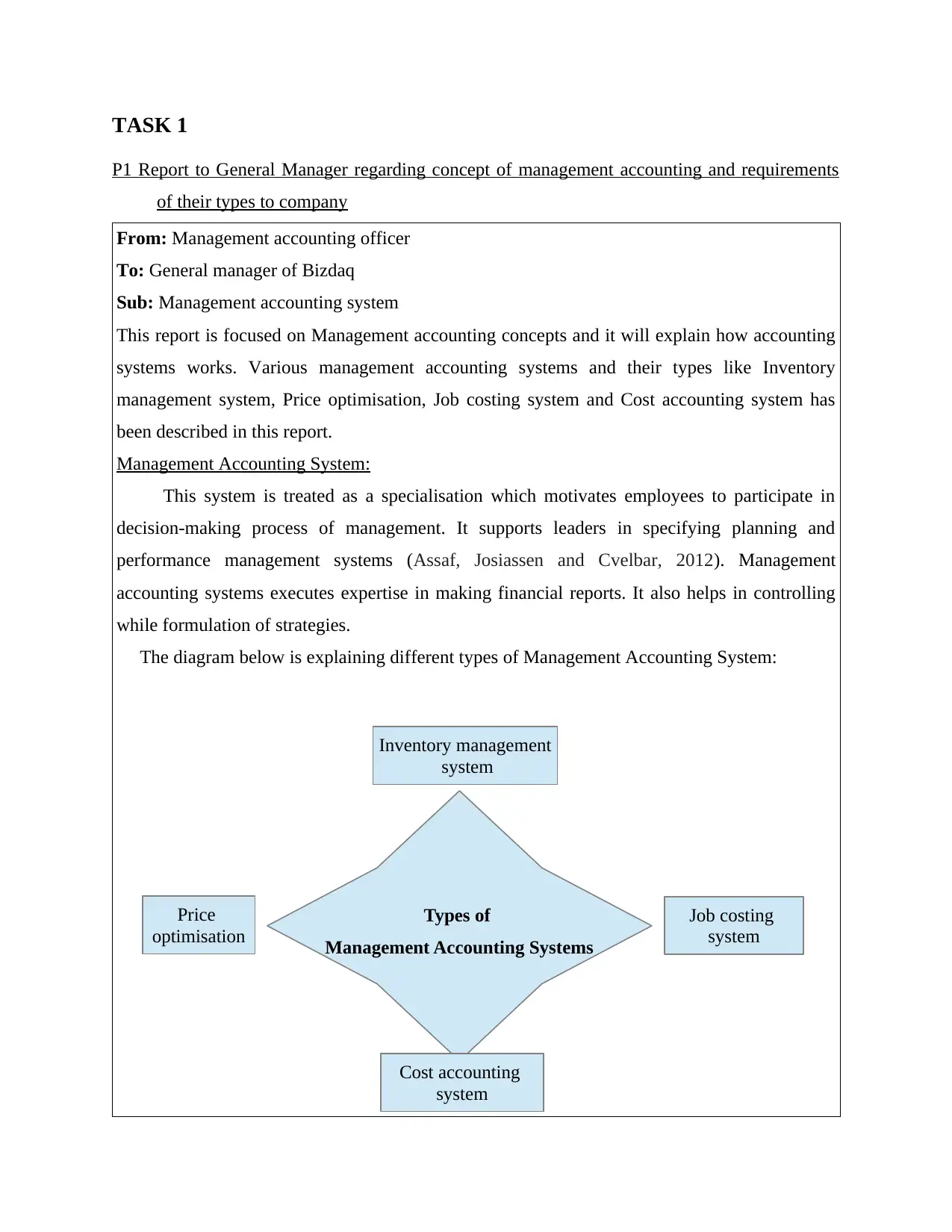

Management Accounting System:

This system is treated as a specialisation which motivates employees to participate in

decision-making process of management. It supports leaders in specifying planning and

performance management systems (Assaf, Josiassen and Cvelbar, 2012). Management

accounting systems executes expertise in making financial reports. It also helps in controlling

while formulation of strategies.

The diagram below is explaining different types of Management Accounting System:

Types of

Management Accounting Systems

Inventory management

system

Price

optimisation

Job costing

system

Cost accounting

system

P1 Report to General Manager regarding concept of management accounting and requirements

of their types to company

From: Management accounting officer

To: General manager of Bizdaq

Sub: Management accounting system

This report is focused on Management accounting concepts and it will explain how accounting

systems works. Various management accounting systems and their types like Inventory

management system, Price optimisation, Job costing system and Cost accounting system has

been described in this report.

Management Accounting System:

This system is treated as a specialisation which motivates employees to participate in

decision-making process of management. It supports leaders in specifying planning and

performance management systems (Assaf, Josiassen and Cvelbar, 2012). Management

accounting systems executes expertise in making financial reports. It also helps in controlling

while formulation of strategies.

The diagram below is explaining different types of Management Accounting System:

Types of

Management Accounting Systems

Inventory management

system

Price

optimisation

Job costing

system

Cost accounting

system

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

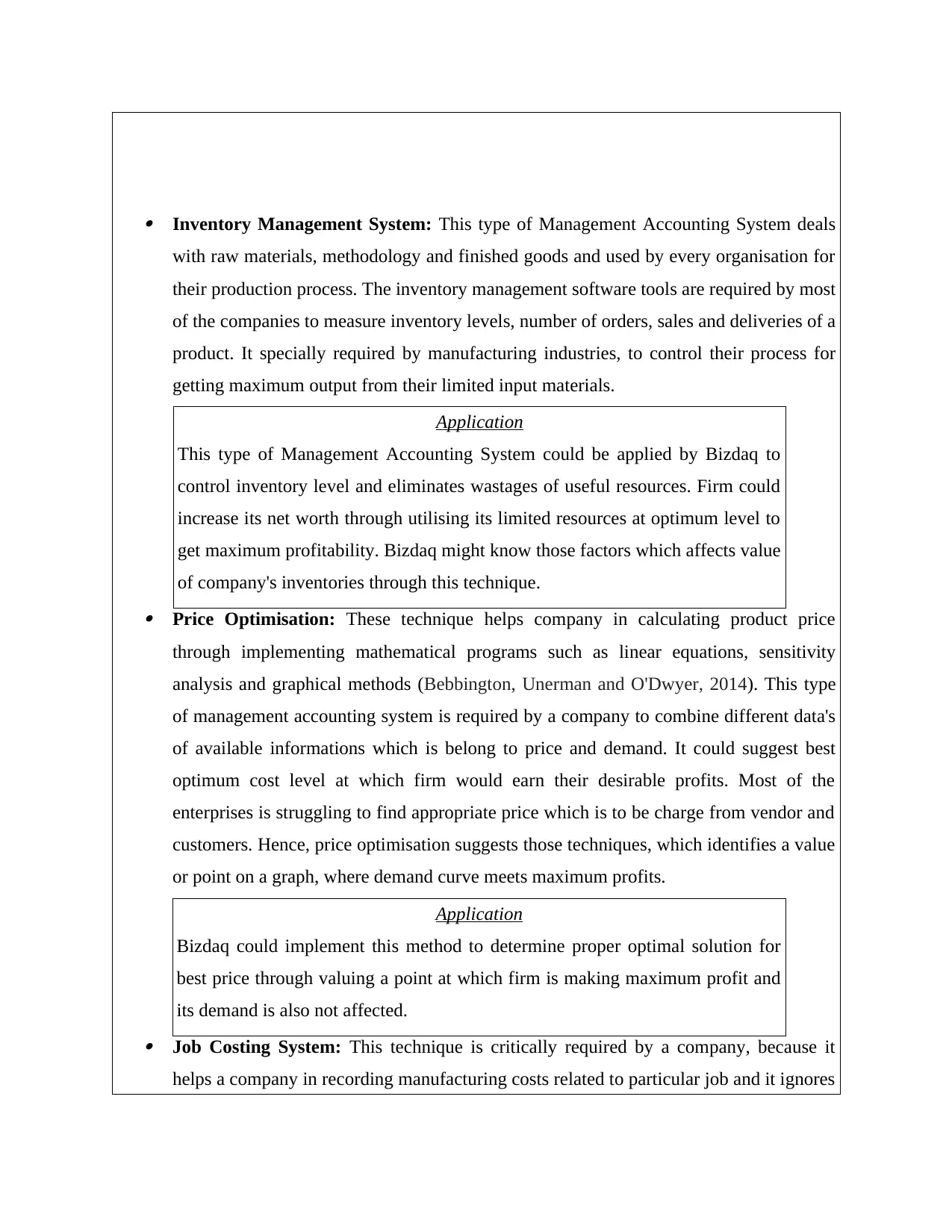

Inventory Management System: This type of Management Accounting System deals

with raw materials, methodology and finished goods and used by every organisation for

their production process. The inventory management software tools are required by most

of the companies to measure inventory levels, number of orders, sales and deliveries of a

product. It specially required by manufacturing industries, to control their process for

getting maximum output from their limited input materials.

Application

This type of Management Accounting System could be applied by Bizdaq to

control inventory level and eliminates wastages of useful resources. Firm could

increase its net worth through utilising its limited resources at optimum level to

get maximum profitability. Bizdaq might know those factors which affects value

of company's inventories through this technique. Price Optimisation: These technique helps company in calculating product price

through implementing mathematical programs such as linear equations, sensitivity

analysis and graphical methods (Bebbington, Unerman and O'Dwyer, 2014). This type

of management accounting system is required by a company to combine different data's

of available informations which is belong to price and demand. It could suggest best

optimum cost level at which firm would earn their desirable profits. Most of the

enterprises is struggling to find appropriate price which is to be charge from vendor and

customers. Hence, price optimisation suggests those techniques, which identifies a value

or point on a graph, where demand curve meets maximum profits.

Application

Bizdaq could implement this method to determine proper optimal solution for

best price through valuing a point at which firm is making maximum profit and

its demand is also not affected. Job Costing System: This technique is critically required by a company, because it

helps a company in recording manufacturing costs related to particular job and it ignores

with raw materials, methodology and finished goods and used by every organisation for

their production process. The inventory management software tools are required by most

of the companies to measure inventory levels, number of orders, sales and deliveries of a

product. It specially required by manufacturing industries, to control their process for

getting maximum output from their limited input materials.

Application

This type of Management Accounting System could be applied by Bizdaq to

control inventory level and eliminates wastages of useful resources. Firm could

increase its net worth through utilising its limited resources at optimum level to

get maximum profitability. Bizdaq might know those factors which affects value

of company's inventories through this technique. Price Optimisation: These technique helps company in calculating product price

through implementing mathematical programs such as linear equations, sensitivity

analysis and graphical methods (Bebbington, Unerman and O'Dwyer, 2014). This type

of management accounting system is required by a company to combine different data's

of available informations which is belong to price and demand. It could suggest best

optimum cost level at which firm would earn their desirable profits. Most of the

enterprises is struggling to find appropriate price which is to be charge from vendor and

customers. Hence, price optimisation suggests those techniques, which identifies a value

or point on a graph, where demand curve meets maximum profits.

Application

Bizdaq could implement this method to determine proper optimal solution for

best price through valuing a point at which firm is making maximum profit and

its demand is also not affected. Job Costing System: This technique is critically required by a company, because it

helps a company in recording manufacturing costs related to particular job and it ignores

process costs. Any company who has adopted Job Costing System could measure the

cost of particular job and they could also maintains feasibility of data of a business. This

technique is mostly relevant to construction industries like infrastructure sectors, as it

diversifies costs related to particular construction projects of a company.

Application

Bizdaq could apply this method for tracking different types of jobs such as direct

labour, material and it could allocate overhead costs among these jobs .

Company could also apply this techniques to measure all activities related to

profitability and a perfect job report would help Bizdaq in measuring its profit

and loss during a year. Cost Accounting System: This type of Management Accounting System also refer as

Product cost system. It is required by a company because it describes financial structure

through calculating its costs. It also supports company in estimating cost budget for next

financial year. It guides company to choose best cost accounting methods to calculate its

product costs and analyses profits.

Application

Cost Accounting System could be applied by Bizdaq in long run of business.

Company could refer marginal costing and absorption costing methods to

evaluate its net earnings during a year. As for example, in the given scenario, he

budgeted cost of production overhead, administration and selling cost were

identified only through this approach.

P2 Report to General manager regarding explanation of methods of management accounting

reports

From: Management accounting officer

To: General manager of Bizdaq

Sub: Management accounting report

In this report, different types of management accounting report methods has been explained.

This report is made to support company in decision-making process and how useful its

application is for Bizdaq.

cost of particular job and they could also maintains feasibility of data of a business. This

technique is mostly relevant to construction industries like infrastructure sectors, as it

diversifies costs related to particular construction projects of a company.

Application

Bizdaq could apply this method for tracking different types of jobs such as direct

labour, material and it could allocate overhead costs among these jobs .

Company could also apply this techniques to measure all activities related to

profitability and a perfect job report would help Bizdaq in measuring its profit

and loss during a year. Cost Accounting System: This type of Management Accounting System also refer as

Product cost system. It is required by a company because it describes financial structure

through calculating its costs. It also supports company in estimating cost budget for next

financial year. It guides company to choose best cost accounting methods to calculate its

product costs and analyses profits.

Application

Cost Accounting System could be applied by Bizdaq in long run of business.

Company could refer marginal costing and absorption costing methods to

evaluate its net earnings during a year. As for example, in the given scenario, he

budgeted cost of production overhead, administration and selling cost were

identified only through this approach.

P2 Report to General manager regarding explanation of methods of management accounting

reports

From: Management accounting officer

To: General manager of Bizdaq

Sub: Management accounting report

In this report, different types of management accounting report methods has been explained.

This report is made to support company in decision-making process and how useful its

application is for Bizdaq.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

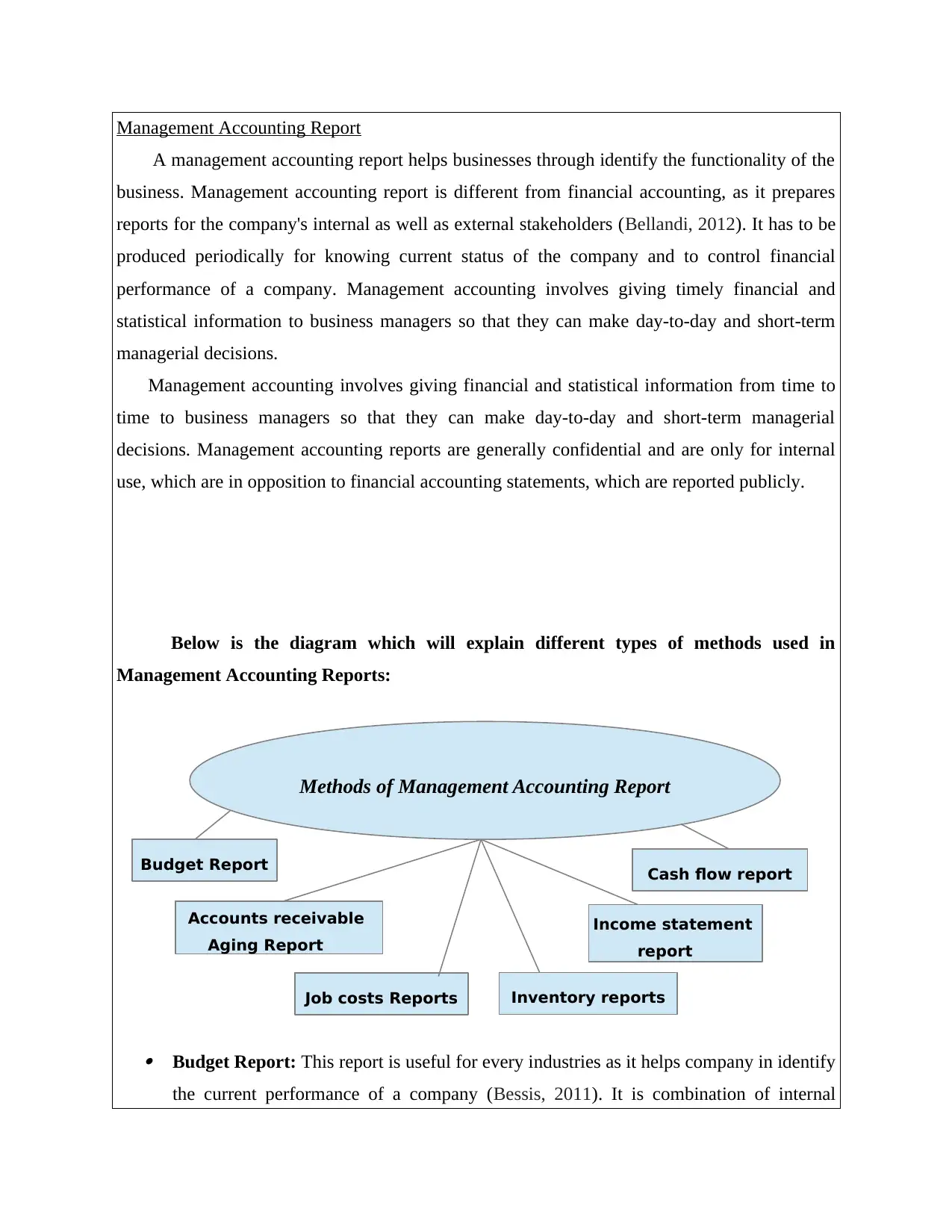

Management Accounting Report

A management accounting report helps businesses through identify the functionality of the

business. Management accounting report is different from financial accounting, as it prepares

reports for the company's internal as well as external stakeholders (Bellandi, 2012). It has to be

produced periodically for knowing current status of the company and to control financial

performance of a company. Management accounting involves giving timely financial and

statistical information to business managers so that they can make day-to-day and short-term

managerial decisions.

Management accounting involves giving financial and statistical information from time to

time to business managers so that they can make day-to-day and short-term managerial

decisions. Management accounting reports are generally confidential and are only for internal

use, which are in opposition to financial accounting statements, which are reported publicly.

Below is the diagram which will explain different types of methods used in

Management Accounting Reports:

Budget Report: This report is useful for every industries as it helps company in identify

the current performance of a company (Bessis, 2011). It is combination of internal

Methods of Management Accounting Report

Accounts receivable

Aging Report

Job costs Reports

Income statement

report

Cash flow report

Budget Report

Inventory reports

A management accounting report helps businesses through identify the functionality of the

business. Management accounting report is different from financial accounting, as it prepares

reports for the company's internal as well as external stakeholders (Bellandi, 2012). It has to be

produced periodically for knowing current status of the company and to control financial

performance of a company. Management accounting involves giving timely financial and

statistical information to business managers so that they can make day-to-day and short-term

managerial decisions.

Management accounting involves giving financial and statistical information from time to

time to business managers so that they can make day-to-day and short-term managerial

decisions. Management accounting reports are generally confidential and are only for internal

use, which are in opposition to financial accounting statements, which are reported publicly.

Below is the diagram which will explain different types of methods used in

Management Accounting Reports:

Budget Report: This report is useful for every industries as it helps company in identify

the current performance of a company (Bessis, 2011). It is combination of internal

Methods of Management Accounting Report

Accounts receivable

Aging Report

Job costs Reports

Income statement

report

Cash flow report

Budget Report

Inventory reports

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

reports which is used by management to compare the actual performance with estimated

figures. If the value of actual figure is more than estimated, then this condition is known

as under budgeting. On the other hand, if the estimation is more than actual

achievement, than this terms is known as overestimation or over budgeting. Hence,

budget report is build to analyse how close is the budgeted performance of a company as

compare to actual performance.

Application

This type of Management Accounting Report could be applied in Bizdaq's financial

operations to determine the variations in estimated and actual figures of a company.

As more gap indicates poor budgeting techniques adopted by the company. While

less gap indicates that, firm is utilising sound techniques to get proper estimations.

For example, the budgeted sales figures of Bizdaq was 450 units but its actual

production was 600 units, this indicates that company is unable to use proper

techniques of budgeting and hence its estimation results in under budget situation. Accounts Receivable Aging Report: Periodic report of the receivable age account is a

periodic report that receives a company's account on time-limit, which is an invoice

outstanding, the use of a gauge to determine the financial position of the customers of

the company (Bezhani, 2010). Is done in If the receipt of the receipt of the account

indicates that the acquisition of the company is being collected more slowly than usual,

then it is a warning sign that the business may be slow or that the company may take

more risks in its sales practices is more.

Application

Bizdaq can do application of Accounts receivable aging reports in determining

minimum balance of amount permitted for provide allowance on Doubtful Debts.

Bizdaq could made these budget tools through sorting sales invoices which are not

paid yet. It will be based on customers and date data's in ledger. This budget reports

are made regularly to update the sorting data's in sales invoice. Job costs Reports: The job cost reports is the process of clarifying those costs which

are related to particular work of company's business. It is mainly used by construction

industries, to allocate costs of individual projects of construction of a firm.

figures. If the value of actual figure is more than estimated, then this condition is known

as under budgeting. On the other hand, if the estimation is more than actual

achievement, than this terms is known as overestimation or over budgeting. Hence,

budget report is build to analyse how close is the budgeted performance of a company as

compare to actual performance.

Application

This type of Management Accounting Report could be applied in Bizdaq's financial

operations to determine the variations in estimated and actual figures of a company.

As more gap indicates poor budgeting techniques adopted by the company. While

less gap indicates that, firm is utilising sound techniques to get proper estimations.

For example, the budgeted sales figures of Bizdaq was 450 units but its actual

production was 600 units, this indicates that company is unable to use proper

techniques of budgeting and hence its estimation results in under budget situation. Accounts Receivable Aging Report: Periodic report of the receivable age account is a

periodic report that receives a company's account on time-limit, which is an invoice

outstanding, the use of a gauge to determine the financial position of the customers of

the company (Bezhani, 2010). Is done in If the receipt of the receipt of the account

indicates that the acquisition of the company is being collected more slowly than usual,

then it is a warning sign that the business may be slow or that the company may take

more risks in its sales practices is more.

Application

Bizdaq can do application of Accounts receivable aging reports in determining

minimum balance of amount permitted for provide allowance on Doubtful Debts.

Bizdaq could made these budget tools through sorting sales invoices which are not

paid yet. It will be based on customers and date data's in ledger. This budget reports

are made regularly to update the sorting data's in sales invoice. Job costs Reports: The job cost reports is the process of clarifying those costs which

are related to particular work of company's business. It is mainly used by construction

industries, to allocate costs of individual projects of construction of a firm.

Application

Bizdaq could implement this technique through creating different categories of

activities of fund utilisation and it could also sort those activities which consumes

more funds than other. The best suitable example of Job costing reports are;

production, selling and distribution costs reports of Bizdaq. Inventory and manufacturing reports: This management accounting reporting types

consists of joining values of various inventories at three stages of productions which are

manufacturing, whole-selling and retailing. It is required by company, because it

consists of sum of business sales at each three stages of production. This report is

mainly useful for supervisors to do inventory management, track inventory movement in

warehouse and a list of various categories like items at hold and visibility.

Application

Bizdaq could apply this method of reporting to identify available sources for

integration of various production activities. This report could help company in

counting cycle period and their variances in informations which is available daily,

weekly and monthly. Income statement report: Such management accounting system is used by the

financial authorities to determine and measure the total profit earned during the financial

year, which is usually December end (Crippa, 2010). It helps company in identifying its

current performance through comparing current and previous years income statements.

Application

Bizdaq could apply this method to identify firm's financial performance status and

profits during a year. Firm could also know how much outstanding expenses,

arrears and payments are due and what are the sources from where it will receive

incomes in future.

Conclusion

After analysing all the management accounting reports types, it can be said that unicorn grocery

should analyse all the features of different reports and these different reasons should be adopted

for presenting a useful report for specific reasons and purposes. Like cash activities, cash flow

Bizdaq could implement this technique through creating different categories of

activities of fund utilisation and it could also sort those activities which consumes

more funds than other. The best suitable example of Job costing reports are;

production, selling and distribution costs reports of Bizdaq. Inventory and manufacturing reports: This management accounting reporting types

consists of joining values of various inventories at three stages of productions which are

manufacturing, whole-selling and retailing. It is required by company, because it

consists of sum of business sales at each three stages of production. This report is

mainly useful for supervisors to do inventory management, track inventory movement in

warehouse and a list of various categories like items at hold and visibility.

Application

Bizdaq could apply this method of reporting to identify available sources for

integration of various production activities. This report could help company in

counting cycle period and their variances in informations which is available daily,

weekly and monthly. Income statement report: Such management accounting system is used by the

financial authorities to determine and measure the total profit earned during the financial

year, which is usually December end (Crippa, 2010). It helps company in identifying its

current performance through comparing current and previous years income statements.

Application

Bizdaq could apply this method to identify firm's financial performance status and

profits during a year. Firm could also know how much outstanding expenses,

arrears and payments are due and what are the sources from where it will receive

incomes in future.

Conclusion

After analysing all the management accounting reports types, it can be said that unicorn grocery

should analyse all the features of different reports and these different reasons should be adopted

for presenting a useful report for specific reasons and purposes. Like cash activities, cash flow

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

reports are required, inventory management tasks are required and reporting methods are to be

manufactured. The Cash Flow Statement report is useful for analysing the accuracy of the

business, the Income Statement Report determines how much the earnings were made with the

company's expansion activities and the company's recycled maintenance in order to support the

business. Budget reports are estimated based on estimates. These reports are required for the

allocation and distribution of Unicorn funds between different functional departments.

TASK 2

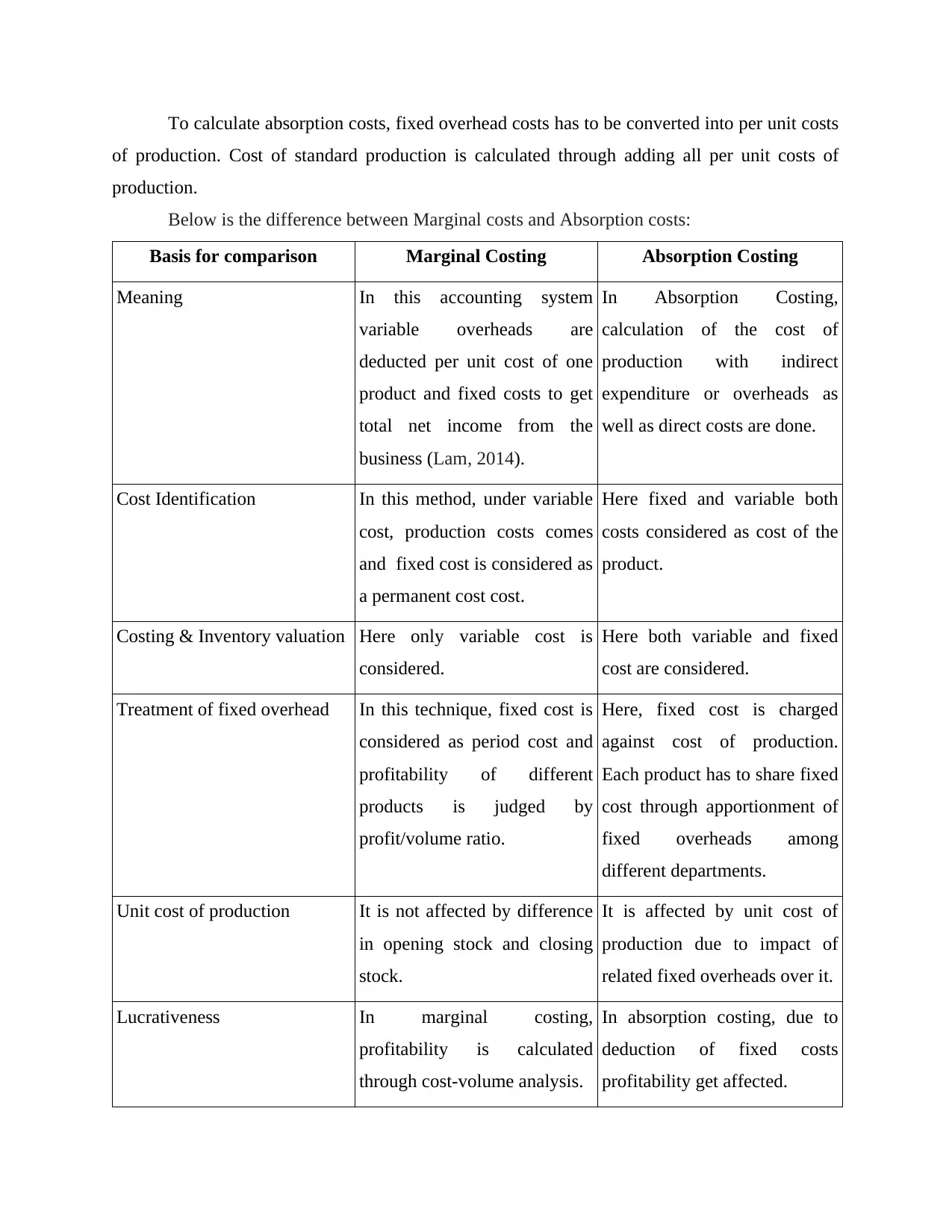

P3 Difference between Marginal costing and Absorption costing and calculation of Income

statement through these methods:

Management accounting usually aims different areas for making accurate reports, but

cost is the main part of this system. Through using appropriate cost approach, company could get

improved results.

Marginal Costing: It focuses on the extra expenditure, which one company has to make

during extra generation. The Slim Form of Cost focuses on fundamentally variable costs, if

Unicorn grocery can reduce its variable expenditure, then they can reduce the price of those

items which are being given in their stores (Kerzner, 2013). This can be used by managers to

make important decisions if the cost of a product is high, then the marginal cost of that item can

be increased or continued for its production, but if the cost of commodity is low Then the

company should stop selling that item in his shop. At the time of final calculation, the fixed cost

is considered in this situation, that is, in the final stage.

Absorption Costing: This costing method is traditional method of calculating costs of a

product. It also refers as full costing method. The main advantage of using this approach is that it

shows the right advantage because it involves all the expenses incurred by the company

(Laegreid and Christensen, 2013). Directly material, labour and upper, all are included in this

approach, there is no fluctuation in fixed costs in this method, its price is definitely assigned to

each unit, if it is added to the final and total amount in its manufacturing Does not go as it goes

into its marginal cost.

manufactured. The Cash Flow Statement report is useful for analysing the accuracy of the

business, the Income Statement Report determines how much the earnings were made with the

company's expansion activities and the company's recycled maintenance in order to support the

business. Budget reports are estimated based on estimates. These reports are required for the

allocation and distribution of Unicorn funds between different functional departments.

TASK 2

P3 Difference between Marginal costing and Absorption costing and calculation of Income

statement through these methods:

Management accounting usually aims different areas for making accurate reports, but

cost is the main part of this system. Through using appropriate cost approach, company could get

improved results.

Marginal Costing: It focuses on the extra expenditure, which one company has to make

during extra generation. The Slim Form of Cost focuses on fundamentally variable costs, if

Unicorn grocery can reduce its variable expenditure, then they can reduce the price of those

items which are being given in their stores (Kerzner, 2013). This can be used by managers to

make important decisions if the cost of a product is high, then the marginal cost of that item can

be increased or continued for its production, but if the cost of commodity is low Then the

company should stop selling that item in his shop. At the time of final calculation, the fixed cost

is considered in this situation, that is, in the final stage.

Absorption Costing: This costing method is traditional method of calculating costs of a

product. It also refers as full costing method. The main advantage of using this approach is that it

shows the right advantage because it involves all the expenses incurred by the company

(Laegreid and Christensen, 2013). Directly material, labour and upper, all are included in this

approach, there is no fluctuation in fixed costs in this method, its price is definitely assigned to

each unit, if it is added to the final and total amount in its manufacturing Does not go as it goes

into its marginal cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To calculate absorption costs, fixed overhead costs has to be converted into per unit costs

of production. Cost of standard production is calculated through adding all per unit costs of

production.

Below is the difference between Marginal costs and Absorption costs:

Basis for comparison Marginal Costing Absorption Costing

Meaning In this accounting system

variable overheads are

deducted per unit cost of one

product and fixed costs to get

total net income from the

business (Lam, 2014).

In Absorption Costing,

calculation of the cost of

production with indirect

expenditure or overheads as

well as direct costs are done.

Cost Identification In this method, under variable

cost, production costs comes

and fixed cost is considered as

a permanent cost cost.

Here fixed and variable both

costs considered as cost of the

product.

Costing & Inventory valuation Here only variable cost is

considered.

Here both variable and fixed

cost are considered.

Treatment of fixed overhead In this technique, fixed cost is

considered as period cost and

profitability of different

products is judged by

profit/volume ratio.

Here, fixed cost is charged

against cost of production.

Each product has to share fixed

cost through apportionment of

fixed overheads among

different departments.

Unit cost of production It is not affected by difference

in opening stock and closing

stock.

It is affected by unit cost of

production due to impact of

related fixed overheads over it.

Lucrativeness In marginal costing,

profitability is calculated

through cost-volume analysis.

In absorption costing, due to

deduction of fixed costs

profitability get affected.

of production. Cost of standard production is calculated through adding all per unit costs of

production.

Below is the difference between Marginal costs and Absorption costs:

Basis for comparison Marginal Costing Absorption Costing

Meaning In this accounting system

variable overheads are

deducted per unit cost of one

product and fixed costs to get

total net income from the

business (Lam, 2014).

In Absorption Costing,

calculation of the cost of

production with indirect

expenditure or overheads as

well as direct costs are done.

Cost Identification In this method, under variable

cost, production costs comes

and fixed cost is considered as

a permanent cost cost.

Here fixed and variable both

costs considered as cost of the

product.

Costing & Inventory valuation Here only variable cost is

considered.

Here both variable and fixed

cost are considered.

Treatment of fixed overhead In this technique, fixed cost is

considered as period cost and

profitability of different

products is judged by

profit/volume ratio.

Here, fixed cost is charged

against cost of production.

Each product has to share fixed

cost through apportionment of

fixed overheads among

different departments.

Unit cost of production It is not affected by difference

in opening stock and closing

stock.

It is affected by unit cost of

production due to impact of

related fixed overheads over it.

Lucrativeness In marginal costing,

profitability is calculated

through cost-volume analysis.

In absorption costing, due to

deduction of fixed costs

profitability get affected.

High spot Contribution per unit is the

high spot of this techniques.

High spot of this techniques is

calculation of both gross profit

and net profit from the cost of

various department centres.

Categorization of Expenses Costs are classified into

variable and fixed in marginal

costing. To find contribution

and net profit separately.

In absorption costing, there's

different classification for

Production to find gross profit

and selling & administration

costs to find net profit.

Cost Collection Cost is collected by outlining

the total contribution of each

product.

Cost is collected through

customary way to show the

cost of data.

Below is the calculation of Income statement through Marginal costing and Absorption

costing techniques:

Net profit calculation on the basis of marginal costing

Per unit price(£) No. of units Amount(£) Amount(£)

Sales revenue 35 600 21000

Less: Marginal cost

Opening Inventory Nil

Total Variable production cost 14 700 9800

Less: Closing Inventory 14 -100 -1400

8400

Contribution 12600

Less: Fixed overhead

Production overhead -2000

Administration cost -700

Selling cost -600

-3300

high spot of this techniques.

High spot of this techniques is

calculation of both gross profit

and net profit from the cost of

various department centres.

Categorization of Expenses Costs are classified into

variable and fixed in marginal

costing. To find contribution

and net profit separately.

In absorption costing, there's

different classification for

Production to find gross profit

and selling & administration

costs to find net profit.

Cost Collection Cost is collected by outlining

the total contribution of each

product.

Cost is collected through

customary way to show the

cost of data.

Below is the calculation of Income statement through Marginal costing and Absorption

costing techniques:

Net profit calculation on the basis of marginal costing

Per unit price(£) No. of units Amount(£) Amount(£)

Sales revenue 35 600 21000

Less: Marginal cost

Opening Inventory Nil

Total Variable production cost 14 700 9800

Less: Closing Inventory 14 -100 -1400

8400

Contribution 12600

Less: Fixed overhead

Production overhead -2000

Administration cost -700

Selling cost -600

-3300

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.