Management Accounting Applications for BKL - Detailed Report

VerifiedAdded on 2020/07/22

|20

|6789

|91

Report

AI Summary

This report provides a comprehensive overview of management accounting applications, specifically tailored for BKL. It delves into the essential requirements of various management accounting systems, including cost accounting, job costing, price optimization, and inventory management systems. The report further explores different management accounting reporting methods such as performance reports, inventory control reports, and variable analysis reports, while also discussing the merits of these systems. A significant portion is dedicated to cost calculation and income statement preparation using both marginal and absorption costing techniques. Furthermore, the report examines the application of different planning tools for budgetary control, highlighting their merits and demerits. It concludes by addressing how accounting systems can be used to solve financial problems and contribute to the sustainable growth of the company, with detailed analysis and interpretation of data produced by the reports.

Management Accounting

Applications

Applications

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

(P1) Management accounting and essential requirement of various management accounting

systems...................................................................................................................................1

(P2) Various methods available in respect of management accounting reporting.................3

(M1) Merits of management accounting systems..................................................................4

(D1) Integration between management accounting systems and reporting............................5

(P3) Cost calculation and income statement preparation by using marginal and absorption

costing.....................................................................................................................................5

(M2) Application of different management accounting techniques for financial reporting.. 7

(D2) Interpretation of data that is produced by the reports....................................................8

(P4) Merits and demerits of various planning tools that are used for budgetary control.......9

(M3) use and application of different planning tools for preparation of budgets................12

(P5) Manner in which accounting systems will be used for solving financial problems.....13

(M4) Use of management accounting in the sustainable growth of the company...............15

(D3) Solving of financial problems by using various planning tools...................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

(P1) Management accounting and essential requirement of various management accounting

systems...................................................................................................................................1

(P2) Various methods available in respect of management accounting reporting.................3

(M1) Merits of management accounting systems..................................................................4

(D1) Integration between management accounting systems and reporting............................5

(P3) Cost calculation and income statement preparation by using marginal and absorption

costing.....................................................................................................................................5

(M2) Application of different management accounting techniques for financial reporting.. 7

(D2) Interpretation of data that is produced by the reports....................................................8

(P4) Merits and demerits of various planning tools that are used for budgetary control.......9

(M3) use and application of different planning tools for preparation of budgets................12

(P5) Manner in which accounting systems will be used for solving financial problems.....13

(M4) Use of management accounting in the sustainable growth of the company...............15

(D3) Solving of financial problems by using various planning tools...................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting is the process in which various activities are undertaken

which includes measurement, identification and analysation (Ajibolade, Arowomole and

Ojikutu, 2010). All this is done so that decisions can be made in better manner by which

it will be possible for any organisation to achieve its goals and objectives as by this only

the overall profitability of it will be improved. With the help of it performance will be

evaluated on the basis of the plans that will be formulated by using the information

which is collected while carrying out various processes. All the data will be required to

be recorded and for that proper reports will be made which will be used by the owner

and managers for various purposes. There are various aspects that should be

understood in respect of management accounting such as various systems and

reporting methods, tools used in budgetary control, costing methods that can be used in

preparation of income statement and manner in which financial problems can be solved

with the help of it. All these will be discussed in the below mentioned report which is

prepared in relation to BKL for using it in trade show by the firm.

TASK

(P1) Management accounting and essential requirement of various management

accounting systems.

In every business, there are certain goals and objectives that are set by the

management that are required to achieved by it in order to make the business a

success (Albelda, 2011). For this purpose various processes are required to be

undertaken which will involve identification, measurement, evaluation, interpretation and

communication. All these processes will together be covered in management

accounting. By this various information will be collected that will be used for the purpose

of making reports and those will be used by the managers in taking the decisions. As

the decisions that will be made will be correct due to the appropriate data, it will result in

the overall growth of the BKL. Risk management, performance management and

strategic management are some of the main areas in which management accounting is

used.

Essential requirement of various systems:

1

Management accounting is the process in which various activities are undertaken

which includes measurement, identification and analysation (Ajibolade, Arowomole and

Ojikutu, 2010). All this is done so that decisions can be made in better manner by which

it will be possible for any organisation to achieve its goals and objectives as by this only

the overall profitability of it will be improved. With the help of it performance will be

evaluated on the basis of the plans that will be formulated by using the information

which is collected while carrying out various processes. All the data will be required to

be recorded and for that proper reports will be made which will be used by the owner

and managers for various purposes. There are various aspects that should be

understood in respect of management accounting such as various systems and

reporting methods, tools used in budgetary control, costing methods that can be used in

preparation of income statement and manner in which financial problems can be solved

with the help of it. All these will be discussed in the below mentioned report which is

prepared in relation to BKL for using it in trade show by the firm.

TASK

(P1) Management accounting and essential requirement of various management

accounting systems.

In every business, there are certain goals and objectives that are set by the

management that are required to achieved by it in order to make the business a

success (Albelda, 2011). For this purpose various processes are required to be

undertaken which will involve identification, measurement, evaluation, interpretation and

communication. All these processes will together be covered in management

accounting. By this various information will be collected that will be used for the purpose

of making reports and those will be used by the managers in taking the decisions. As

the decisions that will be made will be correct due to the appropriate data, it will result in

the overall growth of the BKL. Risk management, performance management and

strategic management are some of the main areas in which management accounting is

used.

Essential requirement of various systems:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

All the systems which are available with the company shall be utilised as they are

very important. It is because the data will be collected with the help of them and by that

various decisions can be taken. Managers require different tyoe of information and that

can only be gained by use of the systems.

Some of the main systems that are present in this respect are described here under :

1. cost accounting systems : perpetual inventory system is the system that is

used for the purpose of recording of various data and that is considered in this

system. In the whole process there are five parts that are required to be

achieved (Arroyo, 2012). The first part will cover the input measurement aspect

in which decision will taken regarding the amount of input that will be used by the

firm. Than various methods that are available for the valuation of inventory will

be used to calculate the value such as marginal and absorption costing. After the

value has been ascertained it will be needed that total cost that has been

incurred in the process is determined which will be done with the help of cost

accumulation methods that are present. Then cash flow assumption will be

carried out and at last internal capabilities will be recorded which will be done

with the help of the various methods available that includes periodic method and

perpetual method. The resources that are available will be allocated on the basis

of the information and by this the profits of various departments will be

calculated.

2. Job costing system : this is the system in which the cost that has been

incurred in relation to various jobs will be taken into consideration (Bodie, 2013).

As in any process there are various activities that will be undertaken and they

cannot be allocated on individual basis, so in order to calculate the per unit cost

this system will be undertaken by the company. In this all the cost of various jobs

will be accumulated and than that will be divided by the total number of units that

will be made and by this the unit cost will be determined. The cost will be

compared with the estimates that have been set and by this variations will be

found which will help the managers in determining the processes that are

inefficient and those will be eliminated so that the targets that have been set can

2

very important. It is because the data will be collected with the help of them and by that

various decisions can be taken. Managers require different tyoe of information and that

can only be gained by use of the systems.

Some of the main systems that are present in this respect are described here under :

1. cost accounting systems : perpetual inventory system is the system that is

used for the purpose of recording of various data and that is considered in this

system. In the whole process there are five parts that are required to be

achieved (Arroyo, 2012). The first part will cover the input measurement aspect

in which decision will taken regarding the amount of input that will be used by the

firm. Than various methods that are available for the valuation of inventory will

be used to calculate the value such as marginal and absorption costing. After the

value has been ascertained it will be needed that total cost that has been

incurred in the process is determined which will be done with the help of cost

accumulation methods that are present. Then cash flow assumption will be

carried out and at last internal capabilities will be recorded which will be done

with the help of the various methods available that includes periodic method and

perpetual method. The resources that are available will be allocated on the basis

of the information and by this the profits of various departments will be

calculated.

2. Job costing system : this is the system in which the cost that has been

incurred in relation to various jobs will be taken into consideration (Bodie, 2013).

As in any process there are various activities that will be undertaken and they

cannot be allocated on individual basis, so in order to calculate the per unit cost

this system will be undertaken by the company. In this all the cost of various jobs

will be accumulated and than that will be divided by the total number of units that

will be made and by this the unit cost will be determined. The cost will be

compared with the estimates that have been set and by this variations will be

found which will help the managers in determining the processes that are

inefficient and those will be eliminated so that the targets that have been set can

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

be achieved and cost can be reduced so that the level of profits will be

maximised.

3. Price optimisation system : price an demand are two main aspects that are

required to be taken into consideration by any firm because they both are

interrelated. There is a inverse relation between them which means that if the

price will be reduced than the demand of the goods will be increased and if price

is increased then demand will reduce (Chenhall, 2012). For this purpose it is

necessary that optimum price should be set which will be beneficial to both,

company as well as consumers. It should be decided at that level that will give it

the maximum return and also will be affordable to all.

4. Inventory management system : inventory is the thing that is required in all

business and it is the responsibility of the managers to make correct decisions

regarding them .so it will be needed that the level at which it should be

maintained should be identified (France, 2010). It should be done so that no

problem of shortage or excessive stock is there. By this the cash that will be

saved will be used by the company in some other projects that will yield

additional returns to it. Also no shortage should be there as by that the process

will be hindered and this will not be a profitable for the BKL.

(P2) Various methods available in respect of management accounting reporting.

There are various methods that can be used in the process of reporting and

those are described under :

1. performance report : For enhancing the working of the firm it will be needed

that the performance of all the employees should be evaluated to identify that

whether the work is being carried out in the appropriate manner or not. There are

various techniques that can be used in relation to this (Hiebl, 2014). The budgets

that are made will be compared with the actuals by which it will be identified that

what are the differences and the reasons behind them. By this several measures

will be undertaken so that the performance can be enhanced. This will also work

as motivation as employees know that their performance is being checked so

they will work with full potential.

3

maximised.

3. Price optimisation system : price an demand are two main aspects that are

required to be taken into consideration by any firm because they both are

interrelated. There is a inverse relation between them which means that if the

price will be reduced than the demand of the goods will be increased and if price

is increased then demand will reduce (Chenhall, 2012). For this purpose it is

necessary that optimum price should be set which will be beneficial to both,

company as well as consumers. It should be decided at that level that will give it

the maximum return and also will be affordable to all.

4. Inventory management system : inventory is the thing that is required in all

business and it is the responsibility of the managers to make correct decisions

regarding them .so it will be needed that the level at which it should be

maintained should be identified (France, 2010). It should be done so that no

problem of shortage or excessive stock is there. By this the cash that will be

saved will be used by the company in some other projects that will yield

additional returns to it. Also no shortage should be there as by that the process

will be hindered and this will not be a profitable for the BKL.

(P2) Various methods available in respect of management accounting reporting.

There are various methods that can be used in the process of reporting and

those are described under :

1. performance report : For enhancing the working of the firm it will be needed

that the performance of all the employees should be evaluated to identify that

whether the work is being carried out in the appropriate manner or not. There are

various techniques that can be used in relation to this (Hiebl, 2014). The budgets

that are made will be compared with the actuals by which it will be identified that

what are the differences and the reasons behind them. By this several measures

will be undertaken so that the performance can be enhanced. This will also work

as motivation as employees know that their performance is being checked so

they will work with full potential.

3

2. Inventory control report : Report in relation to inventory will be made with the

help of information that has been collected with the help of various systems that

are undertaken (Hülle, Kaspar and Möller, 2011). In this all the aspects related to

it will be covered. It will be analysed that whether the firm is maintaining the

quality or not as this is the main key by which customers can be retained and if

they are compromising with it than its effect will be seen on the profitability of the

firm.

3. Job costing report : in this report all the information related to various jobs that

are done in the business and the cost that has been incurred in relation to them

will be recorded. These will be used by the managers to take appropriate

decisions. All the amounts will be accumulated and than allocated to the various

units and by this profit will be increased by reducing the total expenditure made

on irrelevant activities.

4. Variable analysis report : variable cost are those cost that are incurred in

relation to a particulars activity or item and is incurred on individual basis

(Kaplan, and Atkinson, 2015). This has direct relation with the level of activities

which means that it will increase if more services are provided and vice versa. All

the variable cost that are incurred will be recorded in this report as by them the

profit will be affected to great extent. This is because fixed cost does not change

but it changes with the change in the level of activities undertaken.

5. Budgets : Budgets are the plans that are made in which it is specified that what

all activities are to be undertaken and to what extent. By this a limit is fixed that is

required to be achieved in order to maintain the business growth. It will help in

setting targets for the employees and by that they will be inspired and also their

performance will be evaluated. If it is found to be unsatisfactory that corrective

measures will be taken.

(M1) Merits of management accounting systems.

Management accounting systems will be helpful for the mangers as by that they

will be able to take correct and proper decisions as important and relevant information

will be collected that will be useful (Kinney, Raiborn and Poznanski, 2011). Also

expenses that are made will be reduces as the irrelevant activities that are not

4

help of information that has been collected with the help of various systems that

are undertaken (Hülle, Kaspar and Möller, 2011). In this all the aspects related to

it will be covered. It will be analysed that whether the firm is maintaining the

quality or not as this is the main key by which customers can be retained and if

they are compromising with it than its effect will be seen on the profitability of the

firm.

3. Job costing report : in this report all the information related to various jobs that

are done in the business and the cost that has been incurred in relation to them

will be recorded. These will be used by the managers to take appropriate

decisions. All the amounts will be accumulated and than allocated to the various

units and by this profit will be increased by reducing the total expenditure made

on irrelevant activities.

4. Variable analysis report : variable cost are those cost that are incurred in

relation to a particulars activity or item and is incurred on individual basis

(Kaplan, and Atkinson, 2015). This has direct relation with the level of activities

which means that it will increase if more services are provided and vice versa. All

the variable cost that are incurred will be recorded in this report as by them the

profit will be affected to great extent. This is because fixed cost does not change

but it changes with the change in the level of activities undertaken.

5. Budgets : Budgets are the plans that are made in which it is specified that what

all activities are to be undertaken and to what extent. By this a limit is fixed that is

required to be achieved in order to maintain the business growth. It will help in

setting targets for the employees and by that they will be inspired and also their

performance will be evaluated. If it is found to be unsatisfactory that corrective

measures will be taken.

(M1) Merits of management accounting systems.

Management accounting systems will be helpful for the mangers as by that they

will be able to take correct and proper decisions as important and relevant information

will be collected that will be useful (Kinney, Raiborn and Poznanski, 2011). Also

expenses that are made will be reduces as the irrelevant activities that are not

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

contributing to the profits will be identified and eliminated thereby saving the cost. But

there will research which is required to be conducted for this and in that time will be

utilised and that is one of its demerit. So it can be concluded that the advantages which

are attained by use of systems are more than its drawbacks so it shall be taken into

consideration by company.

(D1) Integration between management accounting systems and reporting.

Both management accounting systems and reports are interrelated as with the

help of the information that will be collected by using systems various reports will be

prepared. Also by comparing the budgeted and actual amounts, variations will be

determined and then they will be recorded in the reports to be used by managers as on

the basis of them corrective measures will be taken by them. So it can be said that

without one another can never be done. It is because without information, no reports

can be made so it is very essential that both shall be used together by the company.

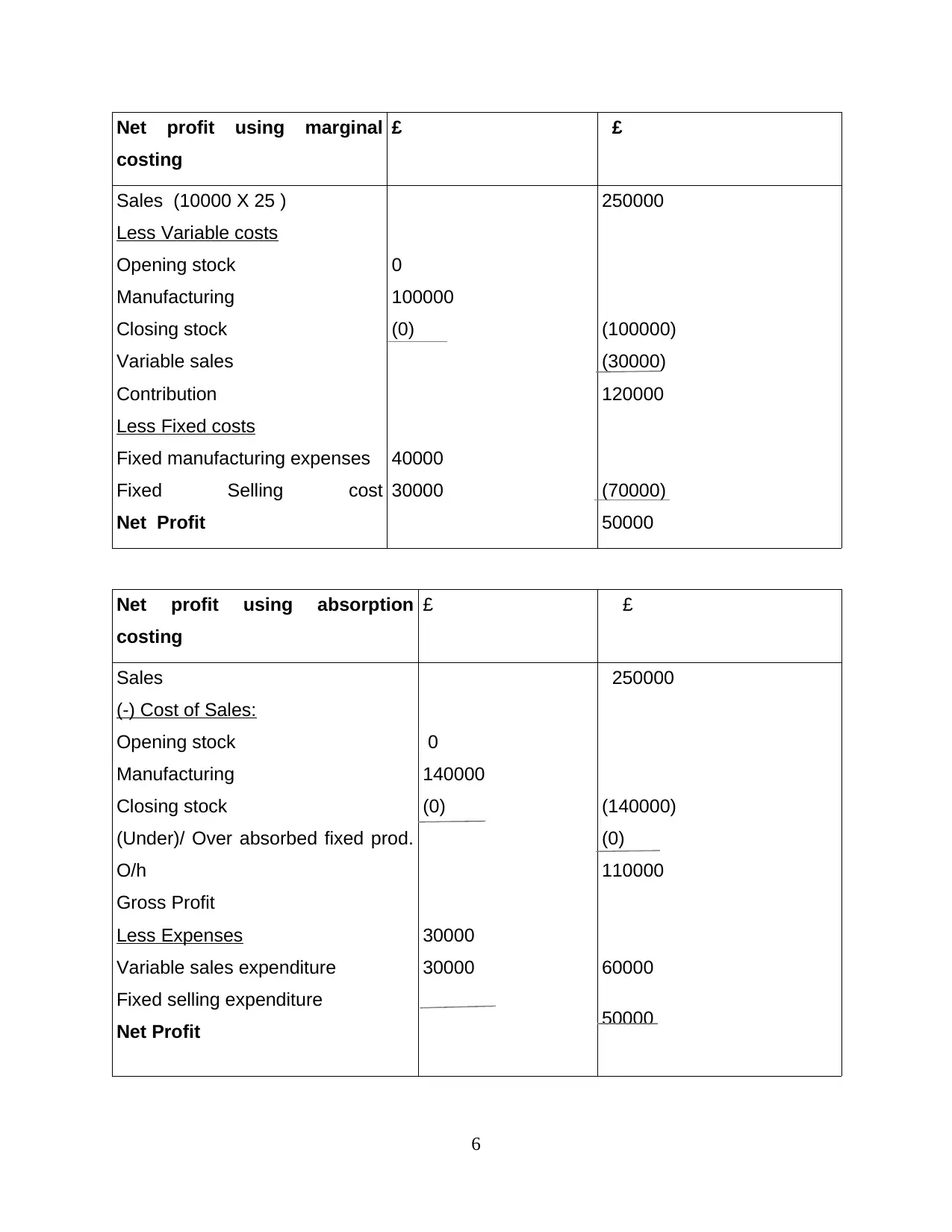

(P3) Cost calculation and income statement preparation by using marginal and

absorption costing.

In the calculation of cost, the two most commonly used methods are absorption

and marginal costing which are described below :

Absorption costing : the cost are mainly divided into two parts which are variable and

fixed cost. In calculation of total cost, both of them will be covered. In this method fixed

cost will be allocated in all the goods that are produced (Macintosh and Quattrone,

2010). For this purpose there are various techniques that can be used such as activity

based costing. On the basis of it income statement will be prepared in which it will be

considered together with the under or over absorption.

Marginal costing : In this method while calculating total cost only variable cost will be

taken into consideration. Variable cost is that cost that is charged on the per unit basis

which means that it will change with the change in level of production (Quinn, 2011). If

there will be increase in the units than variable cost will also increase and vice versa. In

the income statement variable cost will be deducted from the sales value in order to

derive the contribution and then to calculate net profit fixed cost will be deducted from

the contribution.

5

there will research which is required to be conducted for this and in that time will be

utilised and that is one of its demerit. So it can be concluded that the advantages which

are attained by use of systems are more than its drawbacks so it shall be taken into

consideration by company.

(D1) Integration between management accounting systems and reporting.

Both management accounting systems and reports are interrelated as with the

help of the information that will be collected by using systems various reports will be

prepared. Also by comparing the budgeted and actual amounts, variations will be

determined and then they will be recorded in the reports to be used by managers as on

the basis of them corrective measures will be taken by them. So it can be said that

without one another can never be done. It is because without information, no reports

can be made so it is very essential that both shall be used together by the company.

(P3) Cost calculation and income statement preparation by using marginal and

absorption costing.

In the calculation of cost, the two most commonly used methods are absorption

and marginal costing which are described below :

Absorption costing : the cost are mainly divided into two parts which are variable and

fixed cost. In calculation of total cost, both of them will be covered. In this method fixed

cost will be allocated in all the goods that are produced (Macintosh and Quattrone,

2010). For this purpose there are various techniques that can be used such as activity

based costing. On the basis of it income statement will be prepared in which it will be

considered together with the under or over absorption.

Marginal costing : In this method while calculating total cost only variable cost will be

taken into consideration. Variable cost is that cost that is charged on the per unit basis

which means that it will change with the change in level of production (Quinn, 2011). If

there will be increase in the units than variable cost will also increase and vice versa. In

the income statement variable cost will be deducted from the sales value in order to

derive the contribution and then to calculate net profit fixed cost will be deducted from

the contribution.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net profit using marginal

costing

£ £

Sales (10000 X 25 )

Less Variable costs

Opening stock

Manufacturing

Closing stock

Variable sales

Contribution

Less Fixed costs

Fixed manufacturing expenses

Fixed Selling cost

Net Profit

0

100000

(0)

40000

30000

250000

(100000)

(30000)

120000

(70000)

50000

Net profit using absorption

costing

£ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed selling expenditure

Net Profit

0

140000

(0)

30000

30000

250000

(140000)

(0)

110000

60000

50000

6

costing

£ £

Sales (10000 X 25 )

Less Variable costs

Opening stock

Manufacturing

Closing stock

Variable sales

Contribution

Less Fixed costs

Fixed manufacturing expenses

Fixed Selling cost

Net Profit

0

100000

(0)

40000

30000

250000

(100000)

(30000)

120000

(70000)

50000

Net profit using absorption

costing

£ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed selling expenditure

Net Profit

0

140000

(0)

30000

30000

250000

(140000)

(0)

110000

60000

50000

6

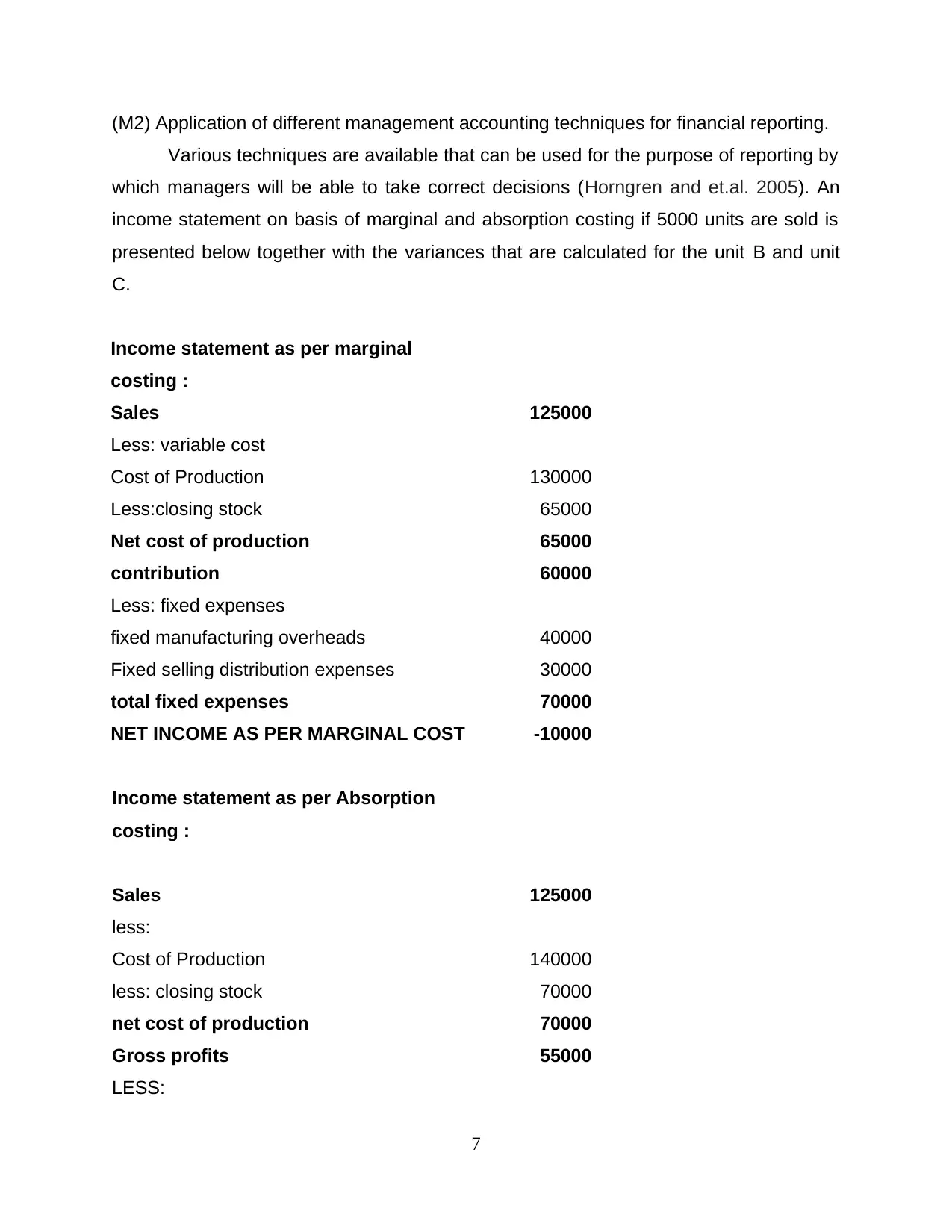

(M2) Application of different management accounting techniques for financial reporting.

Various techniques are available that can be used for the purpose of reporting by

which managers will be able to take correct decisions (Horngren and et.al. 2005). An

income statement on basis of marginal and absorption costing if 5000 units are sold is

presented below together with the variances that are calculated for the unit B and unit

C.

Income statement as per marginal

costing :

Sales 125000

Less: variable cost

Cost of Production 130000

Less:closing stock 65000

Net cost of production 65000

contribution 60000

Less: fixed expenses

fixed manufacturing overheads 40000

Fixed selling distribution expenses 30000

total fixed expenses 70000

NET INCOME AS PER MARGINAL COST -10000

Income statement as per Absorption

costing :

Sales 125000

less:

Cost of Production 140000

less: closing stock 70000

net cost of production 70000

Gross profits 55000

LESS:

7

Various techniques are available that can be used for the purpose of reporting by

which managers will be able to take correct decisions (Horngren and et.al. 2005). An

income statement on basis of marginal and absorption costing if 5000 units are sold is

presented below together with the variances that are calculated for the unit B and unit

C.

Income statement as per marginal

costing :

Sales 125000

Less: variable cost

Cost of Production 130000

Less:closing stock 65000

Net cost of production 65000

contribution 60000

Less: fixed expenses

fixed manufacturing overheads 40000

Fixed selling distribution expenses 30000

total fixed expenses 70000

NET INCOME AS PER MARGINAL COST -10000

Income statement as per Absorption

costing :

Sales 125000

less:

Cost of Production 140000

less: closing stock 70000

net cost of production 70000

Gross profits 55000

LESS:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

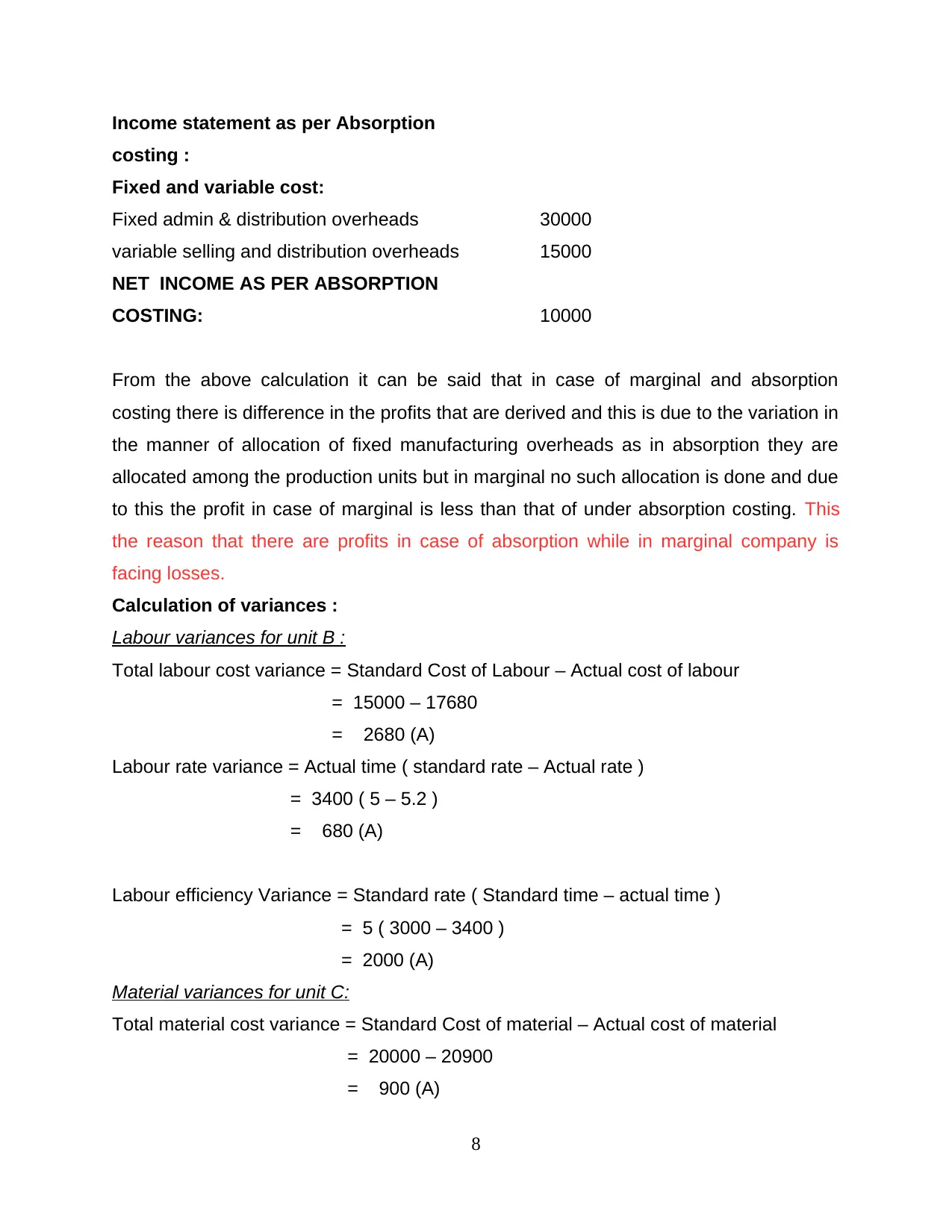

Income statement as per Absorption

costing :

Fixed and variable cost:

Fixed admin & distribution overheads 30000

variable selling and distribution overheads 15000

NET INCOME AS PER ABSORPTION

COSTING: 10000

From the above calculation it can be said that in case of marginal and absorption

costing there is difference in the profits that are derived and this is due to the variation in

the manner of allocation of fixed manufacturing overheads as in absorption they are

allocated among the production units but in marginal no such allocation is done and due

to this the profit in case of marginal is less than that of under absorption costing. This

the reason that there are profits in case of absorption while in marginal company is

facing losses.

Calculation of variances :

Labour variances for unit B :

Total labour cost variance = Standard Cost of Labour – Actual cost of labour

= 15000 – 17680

= 2680 (A)

Labour rate variance = Actual time ( standard rate – Actual rate )

= 3400 ( 5 – 5.2 )

= 680 (A)

Labour efficiency Variance = Standard rate ( Standard time – actual time )

= 5 ( 3000 – 3400 )

= 2000 (A)

Material variances for unit C:

Total material cost variance = Standard Cost of material – Actual cost of material

= 20000 – 20900

= 900 (A)

8

costing :

Fixed and variable cost:

Fixed admin & distribution overheads 30000

variable selling and distribution overheads 15000

NET INCOME AS PER ABSORPTION

COSTING: 10000

From the above calculation it can be said that in case of marginal and absorption

costing there is difference in the profits that are derived and this is due to the variation in

the manner of allocation of fixed manufacturing overheads as in absorption they are

allocated among the production units but in marginal no such allocation is done and due

to this the profit in case of marginal is less than that of under absorption costing. This

the reason that there are profits in case of absorption while in marginal company is

facing losses.

Calculation of variances :

Labour variances for unit B :

Total labour cost variance = Standard Cost of Labour – Actual cost of labour

= 15000 – 17680

= 2680 (A)

Labour rate variance = Actual time ( standard rate – Actual rate )

= 3400 ( 5 – 5.2 )

= 680 (A)

Labour efficiency Variance = Standard rate ( Standard time – actual time )

= 5 ( 3000 – 3400 )

= 2000 (A)

Material variances for unit C:

Total material cost variance = Standard Cost of material – Actual cost of material

= 20000 – 20900

= 900 (A)

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

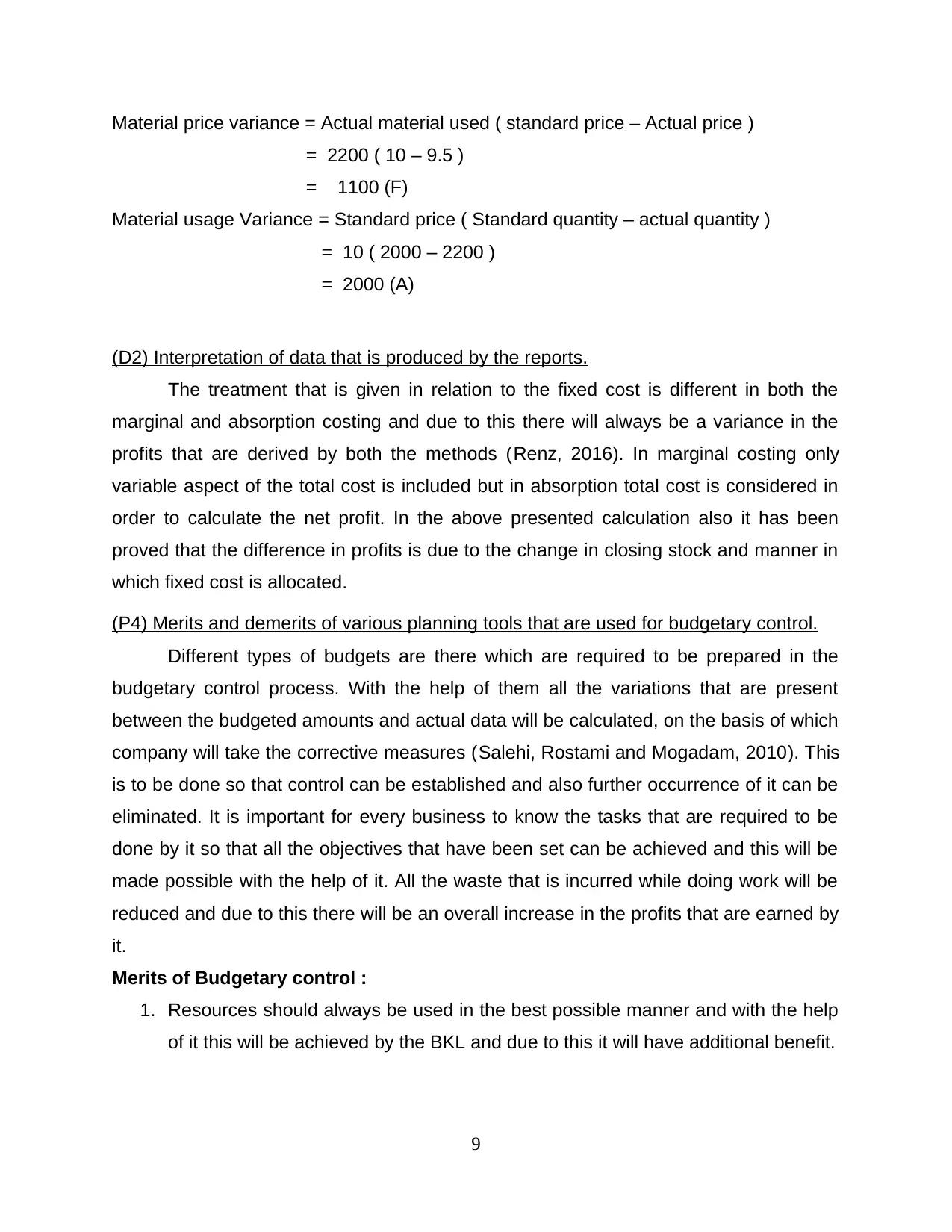

Material price variance = Actual material used ( standard price – Actual price )

= 2200 ( 10 – 9.5 )

= 1100 (F)

Material usage Variance = Standard price ( Standard quantity – actual quantity )

= 10 ( 2000 – 2200 )

= 2000 (A)

(D2) Interpretation of data that is produced by the reports.

The treatment that is given in relation to the fixed cost is different in both the

marginal and absorption costing and due to this there will always be a variance in the

profits that are derived by both the methods (Renz, 2016). In marginal costing only

variable aspect of the total cost is included but in absorption total cost is considered in

order to calculate the net profit. In the above presented calculation also it has been

proved that the difference in profits is due to the change in closing stock and manner in

which fixed cost is allocated.

(P4) Merits and demerits of various planning tools that are used for budgetary control.

Different types of budgets are there which are required to be prepared in the

budgetary control process. With the help of them all the variations that are present

between the budgeted amounts and actual data will be calculated, on the basis of which

company will take the corrective measures (Salehi, Rostami and Mogadam, 2010). This

is to be done so that control can be established and also further occurrence of it can be

eliminated. It is important for every business to know the tasks that are required to be

done by it so that all the objectives that have been set can be achieved and this will be

made possible with the help of it. All the waste that is incurred while doing work will be

reduced and due to this there will be an overall increase in the profits that are earned by

it.

Merits of Budgetary control :

1. Resources should always be used in the best possible manner and with the help

of it this will be achieved by the BKL and due to this it will have additional benefit.

9

= 2200 ( 10 – 9.5 )

= 1100 (F)

Material usage Variance = Standard price ( Standard quantity – actual quantity )

= 10 ( 2000 – 2200 )

= 2000 (A)

(D2) Interpretation of data that is produced by the reports.

The treatment that is given in relation to the fixed cost is different in both the

marginal and absorption costing and due to this there will always be a variance in the

profits that are derived by both the methods (Renz, 2016). In marginal costing only

variable aspect of the total cost is included but in absorption total cost is considered in

order to calculate the net profit. In the above presented calculation also it has been

proved that the difference in profits is due to the change in closing stock and manner in

which fixed cost is allocated.

(P4) Merits and demerits of various planning tools that are used for budgetary control.

Different types of budgets are there which are required to be prepared in the

budgetary control process. With the help of them all the variations that are present

between the budgeted amounts and actual data will be calculated, on the basis of which

company will take the corrective measures (Salehi, Rostami and Mogadam, 2010). This

is to be done so that control can be established and also further occurrence of it can be

eliminated. It is important for every business to know the tasks that are required to be

done by it so that all the objectives that have been set can be achieved and this will be

made possible with the help of it. All the waste that is incurred while doing work will be

reduced and due to this there will be an overall increase in the profits that are earned by

it.

Merits of Budgetary control :

1. Resources should always be used in the best possible manner and with the help

of it this will be achieved by the BKL and due to this it will have additional benefit.

9

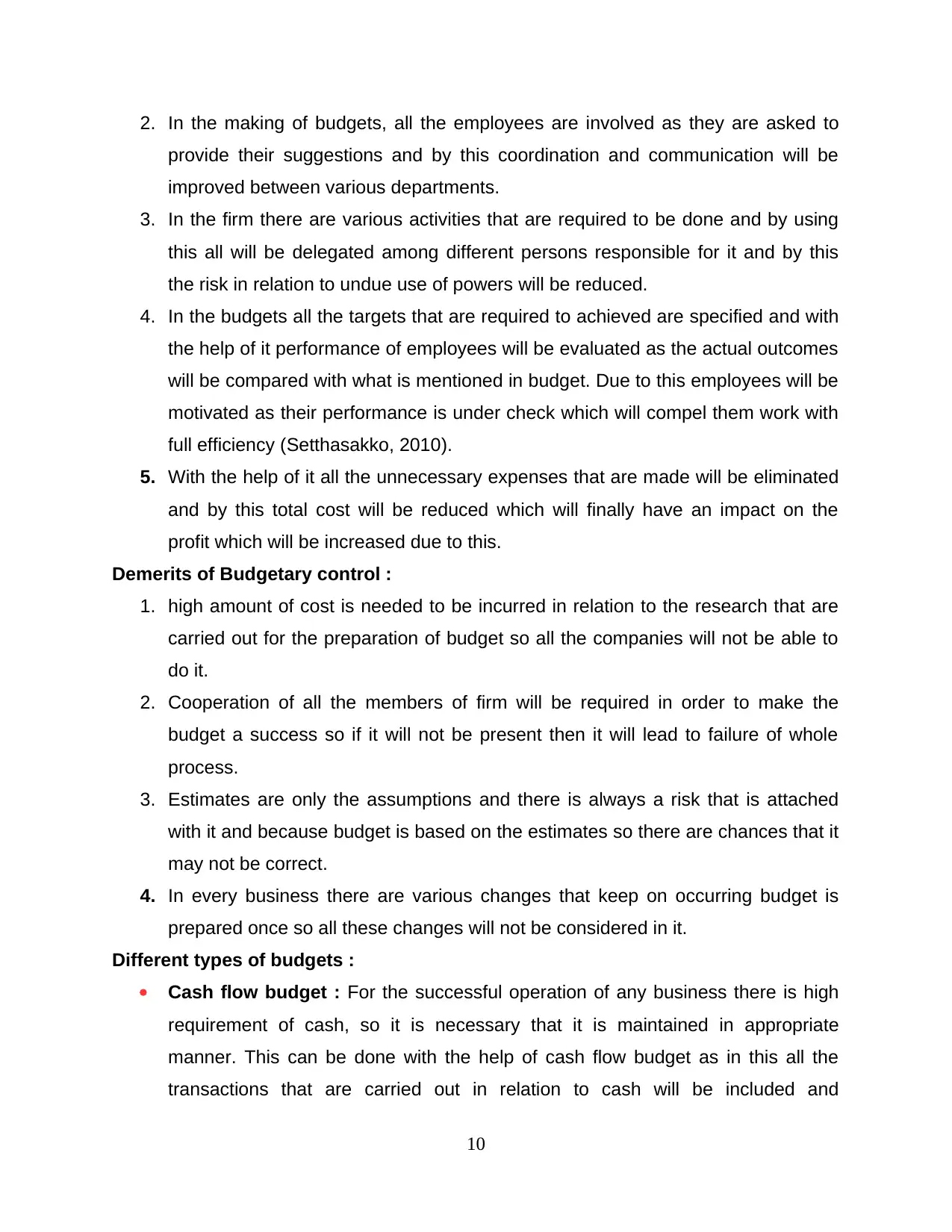

2. In the making of budgets, all the employees are involved as they are asked to

provide their suggestions and by this coordination and communication will be

improved between various departments.

3. In the firm there are various activities that are required to be done and by using

this all will be delegated among different persons responsible for it and by this

the risk in relation to undue use of powers will be reduced.

4. In the budgets all the targets that are required to achieved are specified and with

the help of it performance of employees will be evaluated as the actual outcomes

will be compared with what is mentioned in budget. Due to this employees will be

motivated as their performance is under check which will compel them work with

full efficiency (Setthasakko, 2010).

5. With the help of it all the unnecessary expenses that are made will be eliminated

and by this total cost will be reduced which will finally have an impact on the

profit which will be increased due to this.

Demerits of Budgetary control :

1. high amount of cost is needed to be incurred in relation to the research that are

carried out for the preparation of budget so all the companies will not be able to

do it.

2. Cooperation of all the members of firm will be required in order to make the

budget a success so if it will not be present then it will lead to failure of whole

process.

3. Estimates are only the assumptions and there is always a risk that is attached

with it and because budget is based on the estimates so there are chances that it

may not be correct.

4. In every business there are various changes that keep on occurring budget is

prepared once so all these changes will not be considered in it.

Different types of budgets :

Cash flow budget : For the successful operation of any business there is high

requirement of cash, so it is necessary that it is maintained in appropriate

manner. This can be done with the help of cash flow budget as in this all the

transactions that are carried out in relation to cash will be included and

10

provide their suggestions and by this coordination and communication will be

improved between various departments.

3. In the firm there are various activities that are required to be done and by using

this all will be delegated among different persons responsible for it and by this

the risk in relation to undue use of powers will be reduced.

4. In the budgets all the targets that are required to achieved are specified and with

the help of it performance of employees will be evaluated as the actual outcomes

will be compared with what is mentioned in budget. Due to this employees will be

motivated as their performance is under check which will compel them work with

full efficiency (Setthasakko, 2010).

5. With the help of it all the unnecessary expenses that are made will be eliminated

and by this total cost will be reduced which will finally have an impact on the

profit which will be increased due to this.

Demerits of Budgetary control :

1. high amount of cost is needed to be incurred in relation to the research that are

carried out for the preparation of budget so all the companies will not be able to

do it.

2. Cooperation of all the members of firm will be required in order to make the

budget a success so if it will not be present then it will lead to failure of whole

process.

3. Estimates are only the assumptions and there is always a risk that is attached

with it and because budget is based on the estimates so there are chances that it

may not be correct.

4. In every business there are various changes that keep on occurring budget is

prepared once so all these changes will not be considered in it.

Different types of budgets :

Cash flow budget : For the successful operation of any business there is high

requirement of cash, so it is necessary that it is maintained in appropriate

manner. This can be done with the help of cash flow budget as in this all the

transactions that are carried out in relation to cash will be included and

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.