Management Accounting Application in British Foods: A Detailed Report

VerifiedAdded on 2023/06/08

|15

|4617

|167

Report

AI Summary

This report provides an analysis of management accounting principles and techniques within British Associative Foods, a multinational corporation headquartered in London. It covers the core principles of management accounting, including unbiased data presentation, accuracy, stability, punctuality, exception handling, problem forecasting, efficiency measurement, and resource optimization. The report explores various management accounting systems such as cost accounting, job costing, inventory management, and price optimization. Techniques like marginal and absorption costing are demonstrated through income statements. Furthermore, the document evaluates the integration of management accounting through cost reports, budget reports, accounts receivable aging reports, and inventory reports. It also discusses the benefits of these functions, including improved decision-making and strategic planning. Finally, the report examines how organizations adapt their management accounting systems to respond to financial problems, highlighting the advantages and disadvantages of different planning tools for budgetary control. Desklib offers a range of similar solved assignments and study resources for students.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................2

MAIN BODY..................................................................................................................................2

Part 1................................................................................................................................................2

Principles of Management Accounting.......................................................................................2

Role of Management Accounting and its systems.......................................................................3

Use of Techniques and Methods Used in Management Accounting...........................................4

Evaluating the integration of management accounting within the organization.........................6

Benefits of the Function to the Organization...............................................................................7

Conclusions for critical reflection of management accounting...................................................7

Part 2................................................................................................................................................7

Explaining the advantages and disadvantages of different types of planning tools used for

budgetary control.........................................................................................................................7

Comparing how organizations are adapting management accounting systems to respond to

financial problems.....................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

1

INTRODUCTION...........................................................................................................................2

MAIN BODY..................................................................................................................................2

Part 1................................................................................................................................................2

Principles of Management Accounting.......................................................................................2

Role of Management Accounting and its systems.......................................................................3

Use of Techniques and Methods Used in Management Accounting...........................................4

Evaluating the integration of management accounting within the organization.........................6

Benefits of the Function to the Organization...............................................................................7

Conclusions for critical reflection of management accounting...................................................7

Part 2................................................................................................................................................7

Explaining the advantages and disadvantages of different types of planning tools used for

budgetary control.........................................................................................................................7

Comparing how organizations are adapting management accounting systems to respond to

financial problems.....................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

1

INTRODUCTION

Management accounting is the process followed to identify, measure, analyse, interpret,

and communicate financial information to the managers to achieve the goals of organization.

British Associative Foods is Britain origin MNC, headquartered in London and dealing in ma

manufacturing of food products. The current report will highlight the principles of management

accounting. The different types of management accounting systems are covered. The methods of

reporting the results of management accounting practices are explained. Using the techniques of

management that are marginal and absorption costing the income statements will be prepared.

Different planning tools of the budgetary control along with its advantages and disadvantages

will be discussed. The ways in which organization are adapting to management accounting

principles will be covered.

MAIN BODY

Part 1

Principles of Management Accounting

Presentation of Unbiased Actual Data: It is one of the principles of management

accounting. As per this principle the information provide in management accounting

reports must be accurate & objective. This should not be subjected to anyone’s opinions

or desires.

Accuracy of Accounts: All the accounts, reports, information & documents must be

accurate and serve the purpose of being competent for management enabling them to take

decisions that are accurate (Lebedev, 2018). Accurate decisions are must for organization

to accomplish its objectives.

Stability and Consistency: The procedures and all policies based on which management

accounting is carried on must be stable and have consistency. It is crucial as any change

in such policies & procedures hamper the ability of management to take decisions.

Punctuality: It is another management accounting principle. It states that it is essential to

take correct decisions and right time by the management when the related information to

all the accounts get presented in time.

Principle of Exception: The aim of this principle is to make sure that the attention of

management draws on the issue that are important exceptionally. In case of observation

of deviation of any kind in the results that were planned and the actual ones, a report is

2

Management accounting is the process followed to identify, measure, analyse, interpret,

and communicate financial information to the managers to achieve the goals of organization.

British Associative Foods is Britain origin MNC, headquartered in London and dealing in ma

manufacturing of food products. The current report will highlight the principles of management

accounting. The different types of management accounting systems are covered. The methods of

reporting the results of management accounting practices are explained. Using the techniques of

management that are marginal and absorption costing the income statements will be prepared.

Different planning tools of the budgetary control along with its advantages and disadvantages

will be discussed. The ways in which organization are adapting to management accounting

principles will be covered.

MAIN BODY

Part 1

Principles of Management Accounting

Presentation of Unbiased Actual Data: It is one of the principles of management

accounting. As per this principle the information provide in management accounting

reports must be accurate & objective. This should not be subjected to anyone’s opinions

or desires.

Accuracy of Accounts: All the accounts, reports, information & documents must be

accurate and serve the purpose of being competent for management enabling them to take

decisions that are accurate (Lebedev, 2018). Accurate decisions are must for organization

to accomplish its objectives.

Stability and Consistency: The procedures and all policies based on which management

accounting is carried on must be stable and have consistency. It is crucial as any change

in such policies & procedures hamper the ability of management to take decisions.

Punctuality: It is another management accounting principle. It states that it is essential to

take correct decisions and right time by the management when the related information to

all the accounts get presented in time.

Principle of Exception: The aim of this principle is to make sure that the attention of

management draws on the issue that are important exceptionally. In case of observation

of deviation of any kind in the results that were planned and the actual ones, a report is

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

necessarily required to be prepared explaining the reason for such deviation or exception

in outcomes.

Forecasting and Detection of Problems: Another principle of management accounting

says that it is the duty to get the management informed about the problems that exists

currently and the potentiality of problems that occur in future (Zahid and Vagif, 2020).

With this principle of management accounting along with the identification of problems

steps are initiated to address them.

Measuring Efficiency: The skills of managers are managed on the basis of related

management activities through management accounting. There are certain techniques that

are used for this like ratio analysis.

Maximum Use of Resources: This principle of management accounting ensures efficient

and effective utilization of organization resources. The maximum use of resources gives

maximum profit earning to the organization.

Role of Management Accounting and its systems

Cost Accounting System: Costing system or product costing system are the other names

for cost accounting system. This system provides a framework to the firms for forecasting the

cost of products it produces. It is essential for the purpose of analysing the profitability of the

firm, figuring out the value of inventory and cost control. To make the operations profitable it is

essential to have an accurate estimate of product cost. For ascertaining which products are

profitable it is prerequisite to know the accurate cost of each product. It is also essential in

knowing the amount of closing stock, finished products and work in progress at year end. The

cost accounting system are of two types mainly: job order costing and process costing.

Job Costing System: It is a method in accounting that is designed for keeping track of

individual jobs & projects. There are two types of costs that are assessed here namely indirect

and direct costs. These are bifurcated into three classifications, labour costs, material costs and

cost of overhead. Each of these bifurcates are termed into direct and indirect costs (Gonçalves

and Gaio, 2021). The revenue and costs that are related to a particular project are tracked in a

precise manner. The decision of a business regarding what is to be charges from the customer for

its offerings is the most impactful one. An organization like – with accurate job costing can make

improvements in its profitability and also effectively manage its employees.

3

in outcomes.

Forecasting and Detection of Problems: Another principle of management accounting

says that it is the duty to get the management informed about the problems that exists

currently and the potentiality of problems that occur in future (Zahid and Vagif, 2020).

With this principle of management accounting along with the identification of problems

steps are initiated to address them.

Measuring Efficiency: The skills of managers are managed on the basis of related

management activities through management accounting. There are certain techniques that

are used for this like ratio analysis.

Maximum Use of Resources: This principle of management accounting ensures efficient

and effective utilization of organization resources. The maximum use of resources gives

maximum profit earning to the organization.

Role of Management Accounting and its systems

Cost Accounting System: Costing system or product costing system are the other names

for cost accounting system. This system provides a framework to the firms for forecasting the

cost of products it produces. It is essential for the purpose of analysing the profitability of the

firm, figuring out the value of inventory and cost control. To make the operations profitable it is

essential to have an accurate estimate of product cost. For ascertaining which products are

profitable it is prerequisite to know the accurate cost of each product. It is also essential in

knowing the amount of closing stock, finished products and work in progress at year end. The

cost accounting system are of two types mainly: job order costing and process costing.

Job Costing System: It is a method in accounting that is designed for keeping track of

individual jobs & projects. There are two types of costs that are assessed here namely indirect

and direct costs. These are bifurcated into three classifications, labour costs, material costs and

cost of overhead. Each of these bifurcates are termed into direct and indirect costs (Gonçalves

and Gaio, 2021). The revenue and costs that are related to a particular project are tracked in a

precise manner. The decision of a business regarding what is to be charges from the customer for

its offerings is the most impactful one. An organization like – with accurate job costing can make

improvements in its profitability and also effectively manage its employees.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

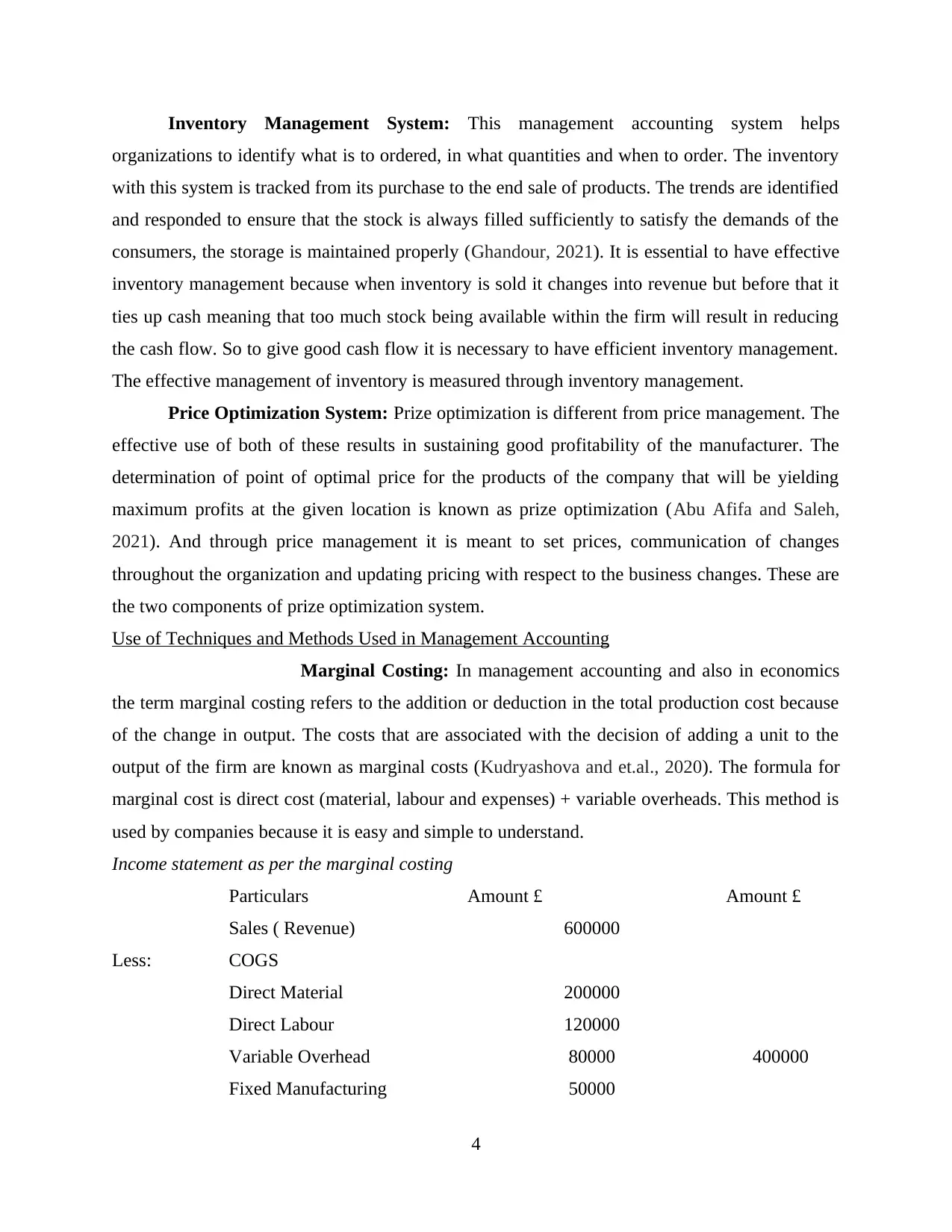

Inventory Management System: This management accounting system helps

organizations to identify what is to ordered, in what quantities and when to order. The inventory

with this system is tracked from its purchase to the end sale of products. The trends are identified

and responded to ensure that the stock is always filled sufficiently to satisfy the demands of the

consumers, the storage is maintained properly (Ghandour, 2021). It is essential to have effective

inventory management because when inventory is sold it changes into revenue but before that it

ties up cash meaning that too much stock being available within the firm will result in reducing

the cash flow. So to give good cash flow it is necessary to have efficient inventory management.

The effective management of inventory is measured through inventory management.

Price Optimization System: Prize optimization is different from price management. The

effective use of both of these results in sustaining good profitability of the manufacturer. The

determination of point of optimal price for the products of the company that will be yielding

maximum profits at the given location is known as prize optimization (Abu Afifa and Saleh,

2021). And through price management it is meant to set prices, communication of changes

throughout the organization and updating pricing with respect to the business changes. These are

the two components of prize optimization system.

Use of Techniques and Methods Used in Management Accounting

Marginal Costing: In management accounting and also in economics

the term marginal costing refers to the addition or deduction in the total production cost because

of the change in output. The costs that are associated with the decision of adding a unit to the

output of the firm are known as marginal costs (Kudryashova and et.al., 2020). The formula for

marginal cost is direct cost (material, labour and expenses) + variable overheads. This method is

used by companies because it is easy and simple to understand.

Income statement as per the marginal costing

Particulars Amount £ Amount £

Sales ( Revenue) 600000

Less: COGS

Direct Material 200000

Direct Labour 120000

Variable Overhead 80000 400000

Fixed Manufacturing 50000

4

organizations to identify what is to ordered, in what quantities and when to order. The inventory

with this system is tracked from its purchase to the end sale of products. The trends are identified

and responded to ensure that the stock is always filled sufficiently to satisfy the demands of the

consumers, the storage is maintained properly (Ghandour, 2021). It is essential to have effective

inventory management because when inventory is sold it changes into revenue but before that it

ties up cash meaning that too much stock being available within the firm will result in reducing

the cash flow. So to give good cash flow it is necessary to have efficient inventory management.

The effective management of inventory is measured through inventory management.

Price Optimization System: Prize optimization is different from price management. The

effective use of both of these results in sustaining good profitability of the manufacturer. The

determination of point of optimal price for the products of the company that will be yielding

maximum profits at the given location is known as prize optimization (Abu Afifa and Saleh,

2021). And through price management it is meant to set prices, communication of changes

throughout the organization and updating pricing with respect to the business changes. These are

the two components of prize optimization system.

Use of Techniques and Methods Used in Management Accounting

Marginal Costing: In management accounting and also in economics

the term marginal costing refers to the addition or deduction in the total production cost because

of the change in output. The costs that are associated with the decision of adding a unit to the

output of the firm are known as marginal costs (Kudryashova and et.al., 2020). The formula for

marginal cost is direct cost (material, labour and expenses) + variable overheads. This method is

used by companies because it is easy and simple to understand.

Income statement as per the marginal costing

Particulars Amount £ Amount £

Sales ( Revenue) 600000

Less: COGS

Direct Material 200000

Direct Labour 120000

Variable Overhead 80000 400000

Fixed Manufacturing 50000

4

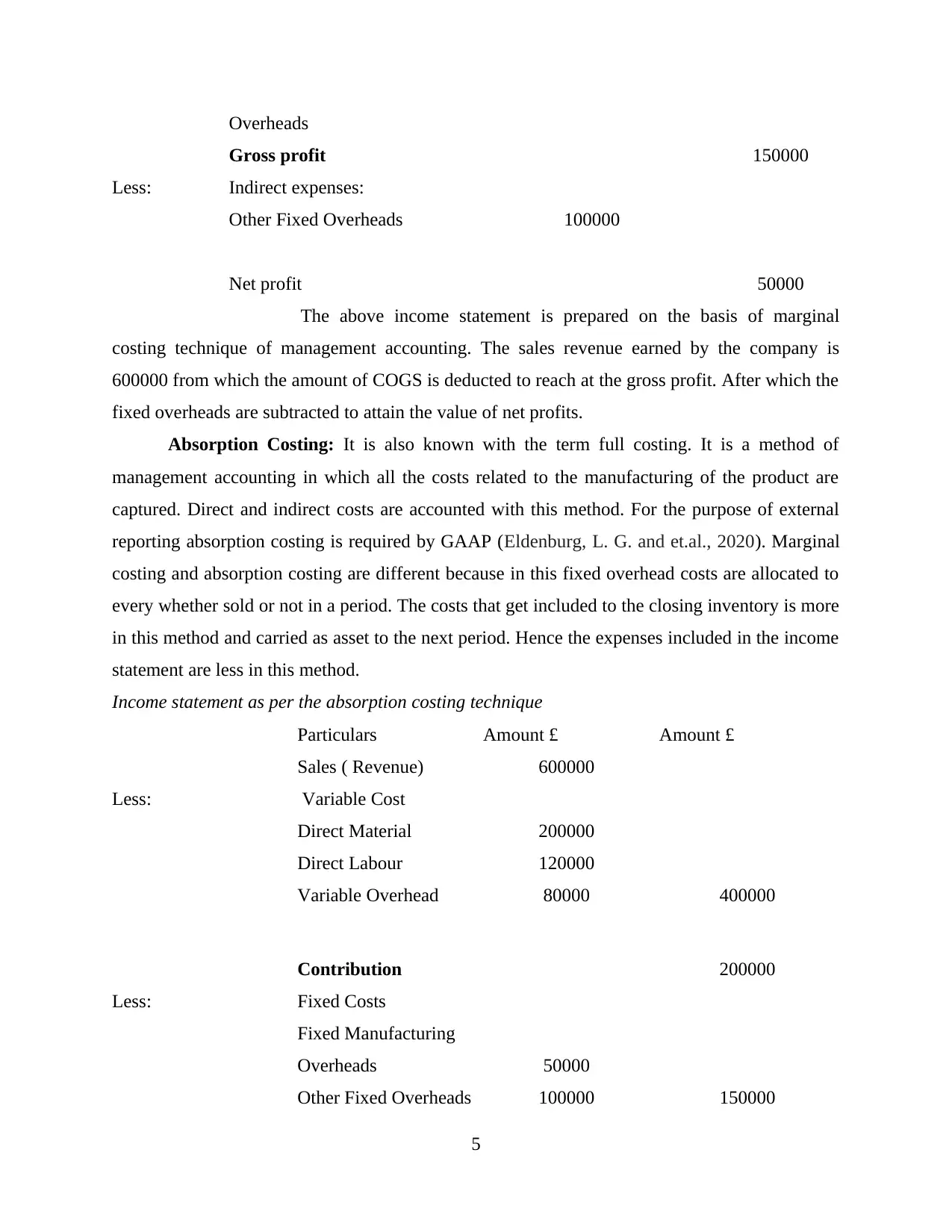

Overheads

Gross profit 150000

Less: Indirect expenses:

Other Fixed Overheads 100000

Net profit 50000

The above income statement is prepared on the basis of marginal

costing technique of management accounting. The sales revenue earned by the company is

600000 from which the amount of COGS is deducted to reach at the gross profit. After which the

fixed overheads are subtracted to attain the value of net profits.

Absorption Costing: It is also known with the term full costing. It is a method of

management accounting in which all the costs related to the manufacturing of the product are

captured. Direct and indirect costs are accounted with this method. For the purpose of external

reporting absorption costing is required by GAAP (Eldenburg, L. G. and et.al., 2020). Marginal

costing and absorption costing are different because in this fixed overhead costs are allocated to

every whether sold or not in a period. The costs that get included to the closing inventory is more

in this method and carried as asset to the next period. Hence the expenses included in the income

statement are less in this method.

Income statement as per the absorption costing technique

Particulars Amount £ Amount £

Sales ( Revenue) 600000

Less: Variable Cost

Direct Material 200000

Direct Labour 120000

Variable Overhead 80000 400000

Contribution 200000

Less: Fixed Costs

Fixed Manufacturing

Overheads 50000

Other Fixed Overheads 100000 150000

5

Gross profit 150000

Less: Indirect expenses:

Other Fixed Overheads 100000

Net profit 50000

The above income statement is prepared on the basis of marginal

costing technique of management accounting. The sales revenue earned by the company is

600000 from which the amount of COGS is deducted to reach at the gross profit. After which the

fixed overheads are subtracted to attain the value of net profits.

Absorption Costing: It is also known with the term full costing. It is a method of

management accounting in which all the costs related to the manufacturing of the product are

captured. Direct and indirect costs are accounted with this method. For the purpose of external

reporting absorption costing is required by GAAP (Eldenburg, L. G. and et.al., 2020). Marginal

costing and absorption costing are different because in this fixed overhead costs are allocated to

every whether sold or not in a period. The costs that get included to the closing inventory is more

in this method and carried as asset to the next period. Hence the expenses included in the income

statement are less in this method.

Income statement as per the absorption costing technique

Particulars Amount £ Amount £

Sales ( Revenue) 600000

Less: Variable Cost

Direct Material 200000

Direct Labour 120000

Variable Overhead 80000 400000

Contribution 200000

Less: Fixed Costs

Fixed Manufacturing

Overheads 50000

Other Fixed Overheads 100000 150000

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

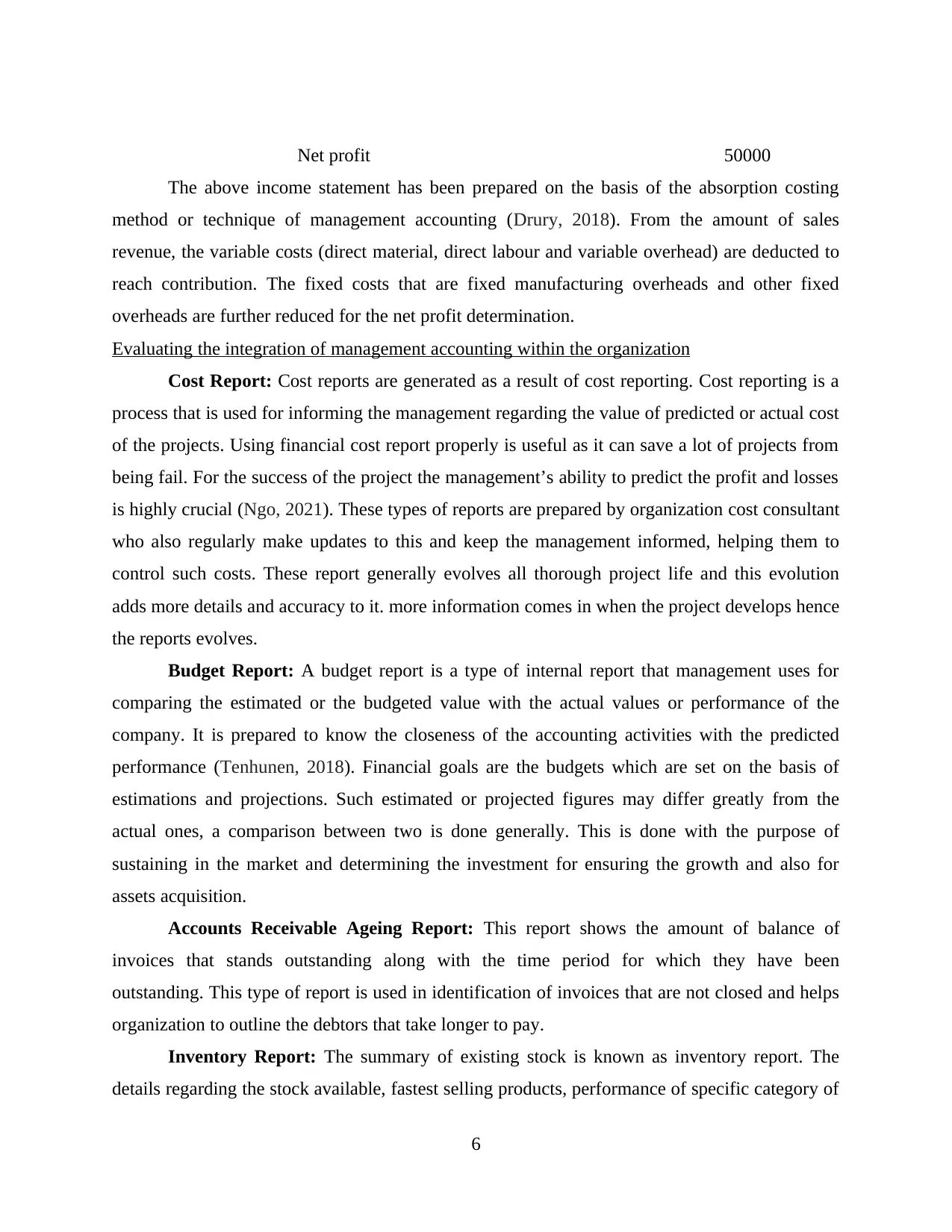

Net profit 50000

The above income statement has been prepared on the basis of the absorption costing

method or technique of management accounting (Drury, 2018). From the amount of sales

revenue, the variable costs (direct material, direct labour and variable overhead) are deducted to

reach contribution. The fixed costs that are fixed manufacturing overheads and other fixed

overheads are further reduced for the net profit determination.

Evaluating the integration of management accounting within the organization

Cost Report: Cost reports are generated as a result of cost reporting. Cost reporting is a

process that is used for informing the management regarding the value of predicted or actual cost

of the projects. Using financial cost report properly is useful as it can save a lot of projects from

being fail. For the success of the project the management’s ability to predict the profit and losses

is highly crucial (Ngo, 2021). These types of reports are prepared by organization cost consultant

who also regularly make updates to this and keep the management informed, helping them to

control such costs. These report generally evolves all thorough project life and this evolution

adds more details and accuracy to it. more information comes in when the project develops hence

the reports evolves.

Budget Report: A budget report is a type of internal report that management uses for

comparing the estimated or the budgeted value with the actual values or performance of the

company. It is prepared to know the closeness of the accounting activities with the predicted

performance (Tenhunen, 2018). Financial goals are the budgets which are set on the basis of

estimations and projections. Such estimated or projected figures may differ greatly from the

actual ones, a comparison between two is done generally. This is done with the purpose of

sustaining in the market and determining the investment for ensuring the growth and also for

assets acquisition.

Accounts Receivable Ageing Report: This report shows the amount of balance of

invoices that stands outstanding along with the time period for which they have been

outstanding. This type of report is used in identification of invoices that are not closed and helps

organization to outline the debtors that take longer to pay.

Inventory Report: The summary of existing stock is known as inventory report. The

details regarding the stock available, fastest selling products, performance of specific category of

6

The above income statement has been prepared on the basis of the absorption costing

method or technique of management accounting (Drury, 2018). From the amount of sales

revenue, the variable costs (direct material, direct labour and variable overhead) are deducted to

reach contribution. The fixed costs that are fixed manufacturing overheads and other fixed

overheads are further reduced for the net profit determination.

Evaluating the integration of management accounting within the organization

Cost Report: Cost reports are generated as a result of cost reporting. Cost reporting is a

process that is used for informing the management regarding the value of predicted or actual cost

of the projects. Using financial cost report properly is useful as it can save a lot of projects from

being fail. For the success of the project the management’s ability to predict the profit and losses

is highly crucial (Ngo, 2021). These types of reports are prepared by organization cost consultant

who also regularly make updates to this and keep the management informed, helping them to

control such costs. These report generally evolves all thorough project life and this evolution

adds more details and accuracy to it. more information comes in when the project develops hence

the reports evolves.

Budget Report: A budget report is a type of internal report that management uses for

comparing the estimated or the budgeted value with the actual values or performance of the

company. It is prepared to know the closeness of the accounting activities with the predicted

performance (Tenhunen, 2018). Financial goals are the budgets which are set on the basis of

estimations and projections. Such estimated or projected figures may differ greatly from the

actual ones, a comparison between two is done generally. This is done with the purpose of

sustaining in the market and determining the investment for ensuring the growth and also for

assets acquisition.

Accounts Receivable Ageing Report: This report shows the amount of balance of

invoices that stands outstanding along with the time period for which they have been

outstanding. This type of report is used in identification of invoices that are not closed and helps

organization to outline the debtors that take longer to pay.

Inventory Report: The summary of existing stock is known as inventory report. The

details regarding the stock available, fastest selling products, performance of specific category of

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

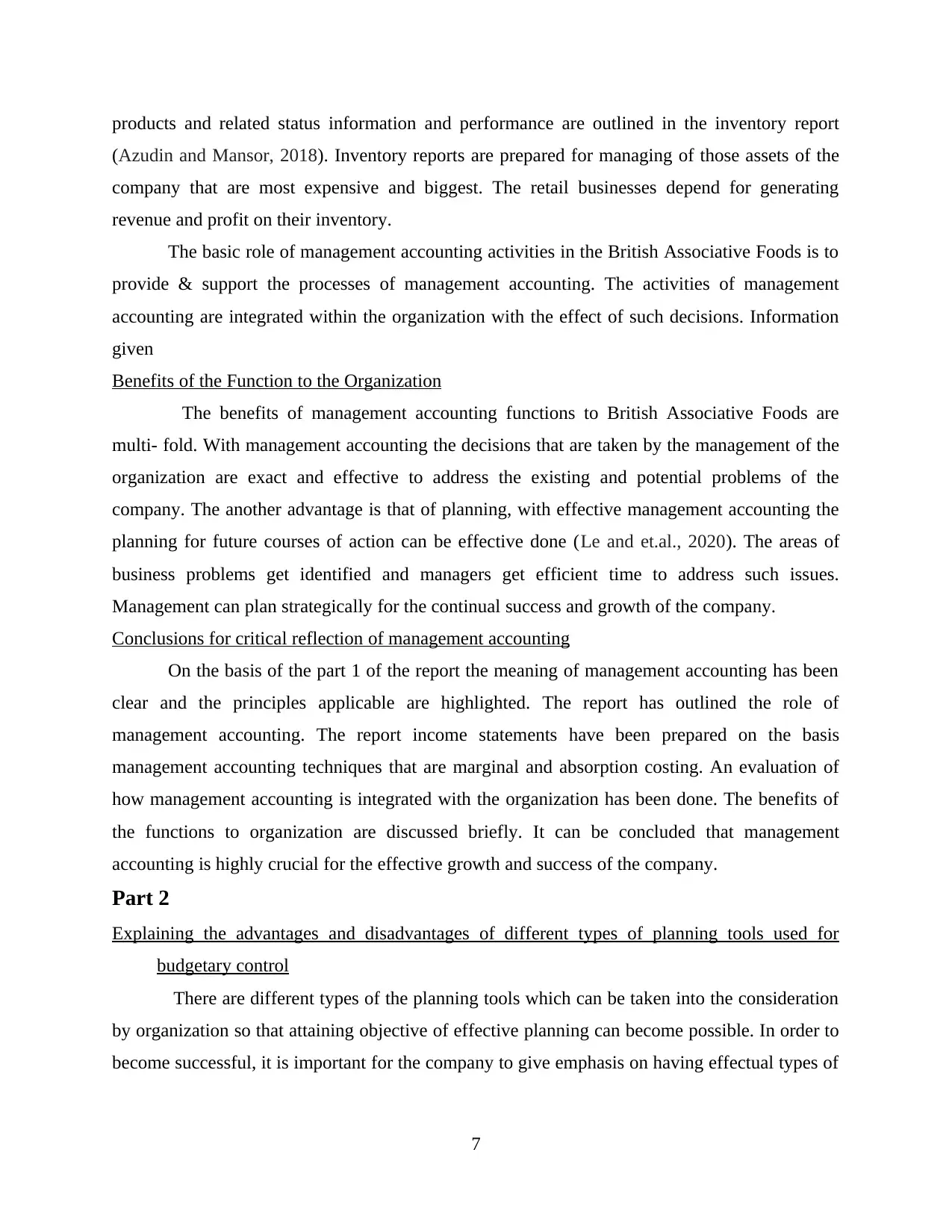

products and related status information and performance are outlined in the inventory report

(Azudin and Mansor, 2018). Inventory reports are prepared for managing of those assets of the

company that are most expensive and biggest. The retail businesses depend for generating

revenue and profit on their inventory.

The basic role of management accounting activities in the British Associative Foods is to

provide & support the processes of management accounting. The activities of management

accounting are integrated within the organization with the effect of such decisions. Information

given

Benefits of the Function to the Organization

The benefits of management accounting functions to British Associative Foods are

multi- fold. With management accounting the decisions that are taken by the management of the

organization are exact and effective to address the existing and potential problems of the

company. The another advantage is that of planning, with effective management accounting the

planning for future courses of action can be effective done (Le and et.al., 2020). The areas of

business problems get identified and managers get efficient time to address such issues.

Management can plan strategically for the continual success and growth of the company.

Conclusions for critical reflection of management accounting

On the basis of the part 1 of the report the meaning of management accounting has been

clear and the principles applicable are highlighted. The report has outlined the role of

management accounting. The report income statements have been prepared on the basis

management accounting techniques that are marginal and absorption costing. An evaluation of

how management accounting is integrated with the organization has been done. The benefits of

the functions to organization are discussed briefly. It can be concluded that management

accounting is highly crucial for the effective growth and success of the company.

Part 2

Explaining the advantages and disadvantages of different types of planning tools used for

budgetary control

There are different types of the planning tools which can be taken into the consideration

by organization so that attaining objective of effective planning can become possible. In order to

become successful, it is important for the company to give emphasis on having effectual types of

7

(Azudin and Mansor, 2018). Inventory reports are prepared for managing of those assets of the

company that are most expensive and biggest. The retail businesses depend for generating

revenue and profit on their inventory.

The basic role of management accounting activities in the British Associative Foods is to

provide & support the processes of management accounting. The activities of management

accounting are integrated within the organization with the effect of such decisions. Information

given

Benefits of the Function to the Organization

The benefits of management accounting functions to British Associative Foods are

multi- fold. With management accounting the decisions that are taken by the management of the

organization are exact and effective to address the existing and potential problems of the

company. The another advantage is that of planning, with effective management accounting the

planning for future courses of action can be effective done (Le and et.al., 2020). The areas of

business problems get identified and managers get efficient time to address such issues.

Management can plan strategically for the continual success and growth of the company.

Conclusions for critical reflection of management accounting

On the basis of the part 1 of the report the meaning of management accounting has been

clear and the principles applicable are highlighted. The report has outlined the role of

management accounting. The report income statements have been prepared on the basis

management accounting techniques that are marginal and absorption costing. An evaluation of

how management accounting is integrated with the organization has been done. The benefits of

the functions to organization are discussed briefly. It can be concluded that management

accounting is highly crucial for the effective growth and success of the company.

Part 2

Explaining the advantages and disadvantages of different types of planning tools used for

budgetary control

There are different types of the planning tools which can be taken into the consideration

by organization so that attaining objective of effective planning can become possible. In order to

become successful, it is important for the company to give emphasis on having effectual types of

7

the planning tools so that significant growth and development of organizational processes can be

achieved.

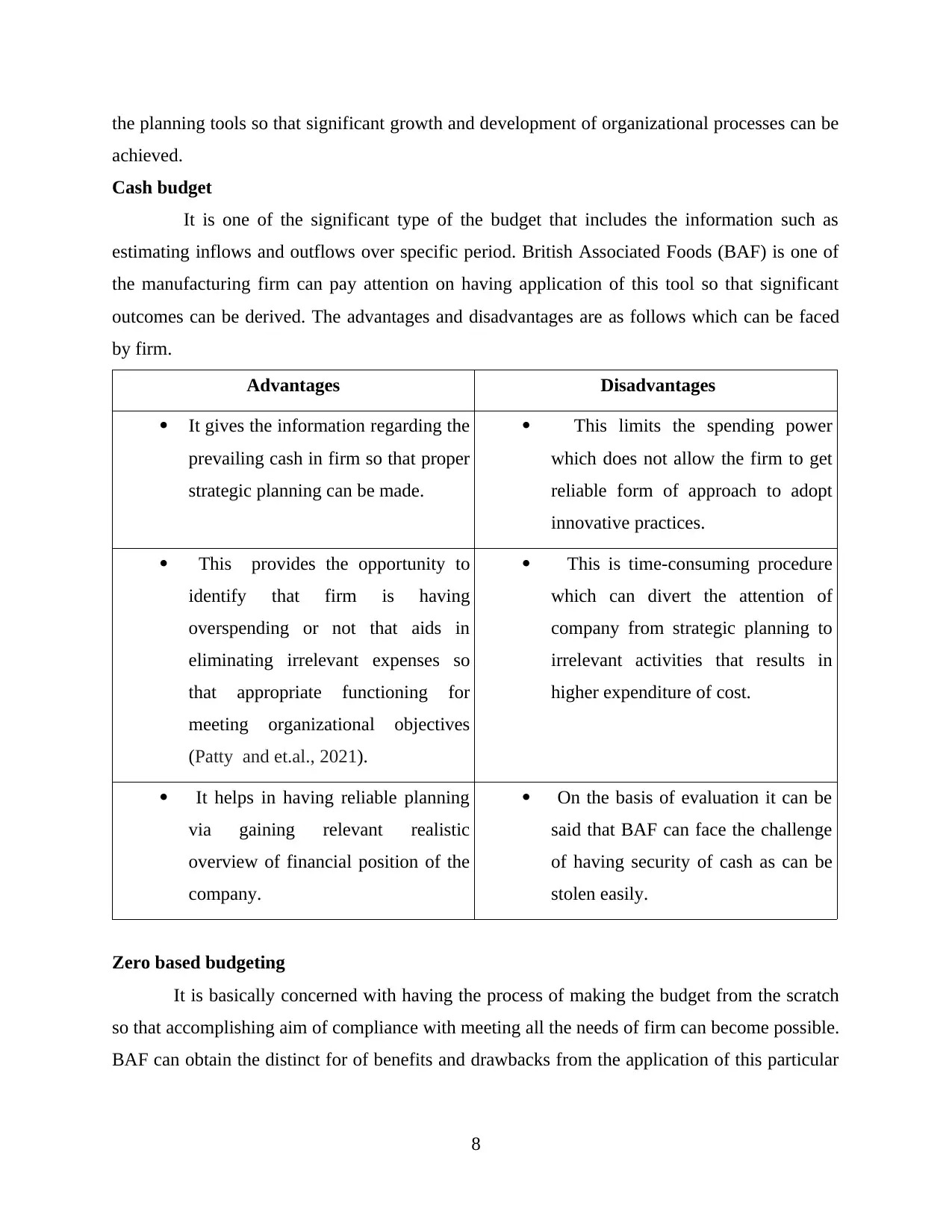

Cash budget

It is one of the significant type of the budget that includes the information such as

estimating inflows and outflows over specific period. British Associated Foods (BAF) is one of

the manufacturing firm can pay attention on having application of this tool so that significant

outcomes can be derived. The advantages and disadvantages are as follows which can be faced

by firm.

Advantages Disadvantages

It gives the information regarding the

prevailing cash in firm so that proper

strategic planning can be made.

This limits the spending power

which does not allow the firm to get

reliable form of approach to adopt

innovative practices.

This provides the opportunity to

identify that firm is having

overspending or not that aids in

eliminating irrelevant expenses so

that appropriate functioning for

meeting organizational objectives

(Patty and et.al., 2021).

This is time-consuming procedure

which can divert the attention of

company from strategic planning to

irrelevant activities that results in

higher expenditure of cost.

It helps in having reliable planning

via gaining relevant realistic

overview of financial position of the

company.

On the basis of evaluation it can be

said that BAF can face the challenge

of having security of cash as can be

stolen easily.

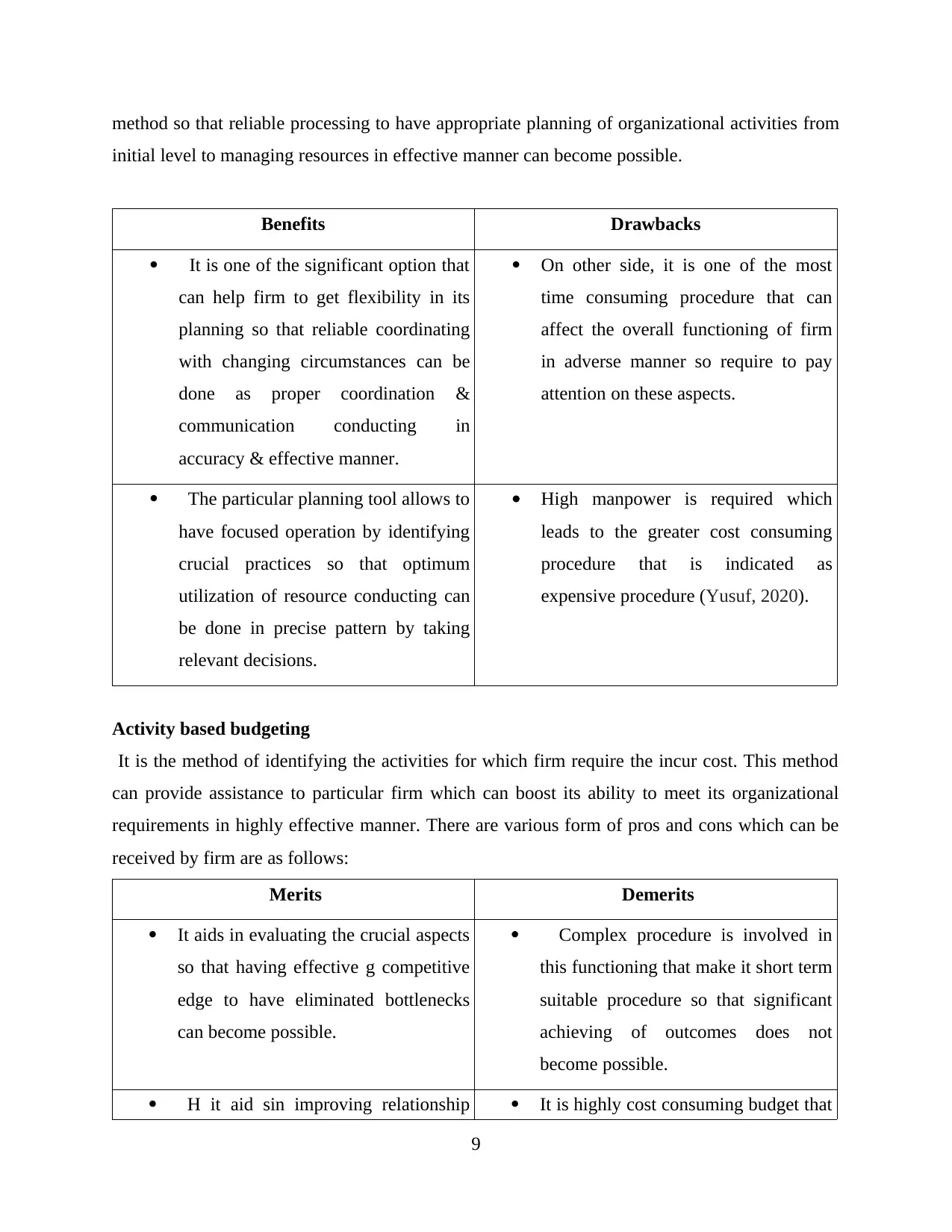

Zero based budgeting

It is basically concerned with having the process of making the budget from the scratch

so that accomplishing aim of compliance with meeting all the needs of firm can become possible.

BAF can obtain the distinct for of benefits and drawbacks from the application of this particular

8

achieved.

Cash budget

It is one of the significant type of the budget that includes the information such as

estimating inflows and outflows over specific period. British Associated Foods (BAF) is one of

the manufacturing firm can pay attention on having application of this tool so that significant

outcomes can be derived. The advantages and disadvantages are as follows which can be faced

by firm.

Advantages Disadvantages

It gives the information regarding the

prevailing cash in firm so that proper

strategic planning can be made.

This limits the spending power

which does not allow the firm to get

reliable form of approach to adopt

innovative practices.

This provides the opportunity to

identify that firm is having

overspending or not that aids in

eliminating irrelevant expenses so

that appropriate functioning for

meeting organizational objectives

(Patty and et.al., 2021).

This is time-consuming procedure

which can divert the attention of

company from strategic planning to

irrelevant activities that results in

higher expenditure of cost.

It helps in having reliable planning

via gaining relevant realistic

overview of financial position of the

company.

On the basis of evaluation it can be

said that BAF can face the challenge

of having security of cash as can be

stolen easily.

Zero based budgeting

It is basically concerned with having the process of making the budget from the scratch

so that accomplishing aim of compliance with meeting all the needs of firm can become possible.

BAF can obtain the distinct for of benefits and drawbacks from the application of this particular

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

method so that reliable processing to have appropriate planning of organizational activities from

initial level to managing resources in effective manner can become possible.

Benefits Drawbacks

It is one of the significant option that

can help firm to get flexibility in its

planning so that reliable coordinating

with changing circumstances can be

done as proper coordination &

communication conducting in

accuracy & effective manner.

On other side, it is one of the most

time consuming procedure that can

affect the overall functioning of firm

in adverse manner so require to pay

attention on these aspects.

The particular planning tool allows to

have focused operation by identifying

crucial practices so that optimum

utilization of resource conducting can

be done in precise pattern by taking

relevant decisions.

High manpower is required which

leads to the greater cost consuming

procedure that is indicated as

expensive procedure (Yusuf, 2020).

Activity based budgeting

It is the method of identifying the activities for which firm require the incur cost. This method

can provide assistance to particular firm which can boost its ability to meet its organizational

requirements in highly effective manner. There are various form of pros and cons which can be

received by firm are as follows:

Merits Demerits

It aids in evaluating the crucial aspects

so that having effective g competitive

edge to have eliminated bottlenecks

can become possible.

Complex procedure is involved in

this functioning that make it short term

suitable procedure so that significant

achieving of outcomes does not

become possible.

H it aid sin improving relationship It is highly cost consuming budget that

9

initial level to managing resources in effective manner can become possible.

Benefits Drawbacks

It is one of the significant option that

can help firm to get flexibility in its

planning so that reliable coordinating

with changing circumstances can be

done as proper coordination &

communication conducting in

accuracy & effective manner.

On other side, it is one of the most

time consuming procedure that can

affect the overall functioning of firm

in adverse manner so require to pay

attention on these aspects.

The particular planning tool allows to

have focused operation by identifying

crucial practices so that optimum

utilization of resource conducting can

be done in precise pattern by taking

relevant decisions.

High manpower is required which

leads to the greater cost consuming

procedure that is indicated as

expensive procedure (Yusuf, 2020).

Activity based budgeting

It is the method of identifying the activities for which firm require the incur cost. This method

can provide assistance to particular firm which can boost its ability to meet its organizational

requirements in highly effective manner. There are various form of pros and cons which can be

received by firm are as follows:

Merits Demerits

It aids in evaluating the crucial aspects

so that having effective g competitive

edge to have eliminated bottlenecks

can become possible.

Complex procedure is involved in

this functioning that make it short term

suitable procedure so that significant

achieving of outcomes does not

become possible.

H it aid sin improving relationship It is highly cost consuming budget that

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

within firm that allows getting

appropriate pricing of activities by

having reliable functioning

can lead firm towards ineffective

planning as its functioning affects the

profitability.

Comparing how organizations are adapting management accounting systems to respond to

financial problems

In order to become successful, it is important for the firm to get insights regarding the

prevailing lacking areas so that accomplishing relevant tools that can allow overcoming

irrelevant functioning that can affect the functioning of organization. For having effective

operational planning there are various form of the challenges that can be overcome to get greater

profitability in firm.

Benchmarking

it is one of the important method that can be taken into the procedure by firm so that

significant ability to overcome the lacking areas can become possible. For becoming successful

its utilization helps in comparing the actual results with standardized so that having reliable

processing can become possible. This offers the distinct advantages which are having improved

performance, greater ability to eliminate the irrelevant aspects, inclined level of quality

performance, etc. On the other side, the lacking areas which can be faced by BAF while using

this as improvement method that includes higher burden on employees, time-consuming

procedure, etc.

Key performance indicator

This is highly taken into the consideration as it helps in getting the ability to set

standards which allows comparing actual with estimated outcome so that prevailing lacking can

become possible (What Is the Importance of KPIs for Performance Measurement? 2022). This

can be used for both financial and non-monetary aspects so that accomplishing the objective of

higher profitability via eliminating prevailing aspects can become possible. This permits to get

the benefit of having higher quality performance, clarity & accountability, increased visibility,

better decision-making, etc. can become possible. On the contrast to this, the drawback which

can hamper the company's objective of overcoming financial problem includes higher time-

consuming procedures can create complications, difficulty to choose the particular KPI, etc.

10

appropriate pricing of activities by

having reliable functioning

can lead firm towards ineffective

planning as its functioning affects the

profitability.

Comparing how organizations are adapting management accounting systems to respond to

financial problems

In order to become successful, it is important for the firm to get insights regarding the

prevailing lacking areas so that accomplishing relevant tools that can allow overcoming

irrelevant functioning that can affect the functioning of organization. For having effective

operational planning there are various form of the challenges that can be overcome to get greater

profitability in firm.

Benchmarking

it is one of the important method that can be taken into the procedure by firm so that

significant ability to overcome the lacking areas can become possible. For becoming successful

its utilization helps in comparing the actual results with standardized so that having reliable

processing can become possible. This offers the distinct advantages which are having improved

performance, greater ability to eliminate the irrelevant aspects, inclined level of quality

performance, etc. On the other side, the lacking areas which can be faced by BAF while using

this as improvement method that includes higher burden on employees, time-consuming

procedure, etc.

Key performance indicator

This is highly taken into the consideration as it helps in getting the ability to set

standards which allows comparing actual with estimated outcome so that prevailing lacking can

become possible (What Is the Importance of KPIs for Performance Measurement? 2022). This

can be used for both financial and non-monetary aspects so that accomplishing the objective of

higher profitability via eliminating prevailing aspects can become possible. This permits to get

the benefit of having higher quality performance, clarity & accountability, increased visibility,

better decision-making, etc. can become possible. On the contrast to this, the drawback which

can hamper the company's objective of overcoming financial problem includes higher time-

consuming procedures can create complications, difficulty to choose the particular KPI, etc.

10

these can hamper the processing of firm in adverse manner so that taking into functioning require

focus.

Variance analysis

This is basically study of the deviation of actual results as compared to the foretasted

figures so that overcoming prevailing lacking areas can become possible (Benefits of using

variance analysis, 2022). Firm in order to get the benefit can use this particular method which

includes achieving the organizational targets via mitigating risks, identifying the lacking aspects

impacting quality performance, causes, etc. can be identified (Seabrooke and Tsingou, 2021). On

the other side, the drawbacks which can be faced by firm involves non standardized production,

assignment of responsibilities, reporting delays and behavioural issues.

Financial governance

The manner in which collection, management, monitoring and controlling of financial

information is done is known as financial governance. Tracking of financial transactions by the

company, performance management and data controlling, operations, compliance & disclosures

are the activities included in financial governance. A good financial governance is essential to

eliminate the occurrence of frauds, material errors, poor decision, regulatory penalties,

misappropriation, reduction of confidence by stakeholders. With financial governance of a

company internal controls, audits (both internal & external), financial policies, financial controls,

workflow, data security & tracking and validation are referred to. The advantages of financial

governance are that it ensures that the data is accurate, helps in producing reports of regulation

and disclosures. Further the ownership & accountability are clear with effective financial

governance.

Balance scorecard

It is a strategic management performance metrics which is used in identifying and

improving the internal functions of the business along with their external results. This concept

was introduced in the year 1992 and was given by Robert Kaplan & David Norton. In this the

previously used performance matrix that was used to include the financial aspects was modified

to include the non –financial aspects as these are essential elements that contributes of the

success of an organization (Camilleri, 2021). There are certain advantages for which the

balanced scorecard is used by the organizations. It brings structure that is essential for shaping

the strategy of the business towards the success of the company. The communication of the

11

focus.

Variance analysis

This is basically study of the deviation of actual results as compared to the foretasted

figures so that overcoming prevailing lacking areas can become possible (Benefits of using

variance analysis, 2022). Firm in order to get the benefit can use this particular method which

includes achieving the organizational targets via mitigating risks, identifying the lacking aspects

impacting quality performance, causes, etc. can be identified (Seabrooke and Tsingou, 2021). On

the other side, the drawbacks which can be faced by firm involves non standardized production,

assignment of responsibilities, reporting delays and behavioural issues.

Financial governance

The manner in which collection, management, monitoring and controlling of financial

information is done is known as financial governance. Tracking of financial transactions by the

company, performance management and data controlling, operations, compliance & disclosures

are the activities included in financial governance. A good financial governance is essential to

eliminate the occurrence of frauds, material errors, poor decision, regulatory penalties,

misappropriation, reduction of confidence by stakeholders. With financial governance of a

company internal controls, audits (both internal & external), financial policies, financial controls,

workflow, data security & tracking and validation are referred to. The advantages of financial

governance are that it ensures that the data is accurate, helps in producing reports of regulation

and disclosures. Further the ownership & accountability are clear with effective financial

governance.

Balance scorecard

It is a strategic management performance metrics which is used in identifying and

improving the internal functions of the business along with their external results. This concept

was introduced in the year 1992 and was given by Robert Kaplan & David Norton. In this the

previously used performance matrix that was used to include the financial aspects was modified

to include the non –financial aspects as these are essential elements that contributes of the

success of an organization (Camilleri, 2021). There are certain advantages for which the

balanced scorecard is used by the organizations. It brings structure that is essential for shaping

the strategy of the business towards the success of the company. The communication of the

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.