Management Accounting: Budgeting, Types, and Cash Flow Analysis

VerifiedAdded on 2020/07/22

|10

|2711

|36

Report

AI Summary

This report delves into the realm of management accounting, focusing on the critical aspect of budgeting. It begins with an introduction to management accounting and the significance of budgeting, especially for companies like Pine Limited, a furniture manufacturer. The report explores various types and methods of budgeting, including master budgets, cash flow budgets, incremental, zero-based, and top-down budgeting. It provides a detailed analysis of the merits and demerits of each method, recommending zero-based budgeting as the most suitable approach for Pine Limited. The report also covers the preparation of a cash budget, outlining its key elements, steps, and importance compared to other budget types. The provided cash budget data from 2011 to 2015 illustrates cash inflow and outflow, highlighting the importance of managing liquidity for business growth. The conclusion summarizes the key findings and emphasizes the importance of effective budgeting in mitigating financial risks and ensuring operational efficiency.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF

CONTENTSINTRODUCTION...........................................................................................................................1

TASK .............................................................................................................................................1

1. Explanation of budgeting........................................................................................................1

2. Types and methods of budgeting ...........................................................................................1

3. Merits and demerits of different budgeting methodologies....................................................2

4. Preparation of cash budget......................................................................................................3

5. Importance of cash budget compared to other kind of budgets..............................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

CONTENTSINTRODUCTION...........................................................................................................................1

TASK .............................................................................................................................................1

1. Explanation of budgeting........................................................................................................1

2. Types and methods of budgeting ...........................................................................................1

3. Merits and demerits of different budgeting methodologies....................................................2

4. Preparation of cash budget......................................................................................................3

5. Importance of cash budget compared to other kind of budgets..............................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION

Management accounting is the procedure of analysing data or information which can be

related to finance or other topics. Budgeting is considered as a crucial part of managerial

accounts because it can minimise various kinds of risks that are present in business (Vakalfotis,

Ballantine and Wall, 2013). Pine Limited is a furniture manufacturing company, they sell their

products to the public as well as to commercial enterprises also. This assignment will discuss

different kinds and methods of budgeting. Budgeting methods will also become an important part

of this file. Importance of cash budgets will also be discussed at the end of this report.

TASK

1. Explanation of budgeting

It is a process of planning all the expenditure that a company is going to do in upcoming

time. The estimation of income is another significant part of this procedure. If an organisation

will not form a budget then they may spend their money on useless things, this may create a big

trouble when the need of financial and other resources is more than normal. The main purpose of

making plans is optimum utilisation of the funds that are present in the enterprise. There are

different types of budget like cash flow, operating, financial etc. Every corporation have a fear or

uncertainty, they plan their income and expenditure so they can run their daily operations in an

effective way and at the same time they minimise the nature of risk that is present in business. In

budgeting process, generally the budget is made for one year but there is no hard and fast rules

and one can do make estimation of a short or long period of time (Tsamenyi, Sahadev and Qiao,

2011). The importance of making budget is continuously growing in business environment

because many companies are failing to cope up with the rapid changes then it happening in

almost every industry.

2. Types and methods of budgeting

Below are main kind of budget which Pine limited can make for proper utilisation of the

available resources:

Master budget – This kind of planning is done by keeping big picture in mind. All the

department and various activities performed in the organisation is analysed at the time of

formation of this budget. Different factors like sales, assets, expenditure etc. are included at the

1

Management accounting is the procedure of analysing data or information which can be

related to finance or other topics. Budgeting is considered as a crucial part of managerial

accounts because it can minimise various kinds of risks that are present in business (Vakalfotis,

Ballantine and Wall, 2013). Pine Limited is a furniture manufacturing company, they sell their

products to the public as well as to commercial enterprises also. This assignment will discuss

different kinds and methods of budgeting. Budgeting methods will also become an important part

of this file. Importance of cash budgets will also be discussed at the end of this report.

TASK

1. Explanation of budgeting

It is a process of planning all the expenditure that a company is going to do in upcoming

time. The estimation of income is another significant part of this procedure. If an organisation

will not form a budget then they may spend their money on useless things, this may create a big

trouble when the need of financial and other resources is more than normal. The main purpose of

making plans is optimum utilisation of the funds that are present in the enterprise. There are

different types of budget like cash flow, operating, financial etc. Every corporation have a fear or

uncertainty, they plan their income and expenditure so they can run their daily operations in an

effective way and at the same time they minimise the nature of risk that is present in business. In

budgeting process, generally the budget is made for one year but there is no hard and fast rules

and one can do make estimation of a short or long period of time (Tsamenyi, Sahadev and Qiao,

2011). The importance of making budget is continuously growing in business environment

because many companies are failing to cope up with the rapid changes then it happening in

almost every industry.

2. Types and methods of budgeting

Below are main kind of budget which Pine limited can make for proper utilisation of the

available resources:

Master budget – This kind of planning is done by keeping big picture in mind. All the

department and various activities performed in the organisation is analysed at the time of

formation of this budget. Different factors like sales, assets, expenditure etc. are included at the

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

time of planning and whole performance of the company is also analysed by bringing all the

managers on same page.

Cash flow budget – All the plans relating to incoming and outgoing of cash is estimated

in this planning. Account payable and receivable are significant part of this estimation.

Operating budget – It is basically the forecasting of all the expected income and

expenditure that a company will do in a specific period of time (Shaw, Agahi and Krause, 2011).

Manufacturing cost, sales, expenses relating to administration etc. are some of the crucial factors

of this planning.

Methods of budgeting

Incremental – In this approach, the current budget is increased by a certain percentage or

amount. Formation of this estimation is very simple and it does not involve much cost in its

preparation.

Zero-based budgeting – In this method, all kind of expenditure that is happening in

company is examined and then if managers do not find a proper justification for an expense than

it is eliminated from the budget. Its preparation can be bit expensive but at the same time it can

reduce their total cost of business. It is more accurate compare to other one and necessary

changes in this method of planning can be done without hampering whole plan.

Top down budgeting – In this approach, senior managers of the company do the work of

estimation of profits and expenditure. They do not involve middle and lower level employees,

this can be considered as the prime reason that budget in this methods are formed in short time

period and without much conflicts. But if the higher authority do not have sound knowledge

about day to day business then cannot do effective planning (What is Budgetary control?, 2017).

3. Merits and demerits of different budgeting methodologies

As mentioned above there are three methods of budgeting. Below are their advantages

and disadvantages:

Incremental

Merits – Its formation is very simple and manager can make any understand about what

is the addition funds which company is going to spend of various expenses. Costing of preparing

is budget is very important factor, if a company is use any other approach then they may have to

incur huge amount of making of an estimation (Otley and Emmanuel, 2013). Normally the

conflicts in an organisation arise because some departments get more funds while other get less

2

managers on same page.

Cash flow budget – All the plans relating to incoming and outgoing of cash is estimated

in this planning. Account payable and receivable are significant part of this estimation.

Operating budget – It is basically the forecasting of all the expected income and

expenditure that a company will do in a specific period of time (Shaw, Agahi and Krause, 2011).

Manufacturing cost, sales, expenses relating to administration etc. are some of the crucial factors

of this planning.

Methods of budgeting

Incremental – In this approach, the current budget is increased by a certain percentage or

amount. Formation of this estimation is very simple and it does not involve much cost in its

preparation.

Zero-based budgeting – In this method, all kind of expenditure that is happening in

company is examined and then if managers do not find a proper justification for an expense than

it is eliminated from the budget. Its preparation can be bit expensive but at the same time it can

reduce their total cost of business. It is more accurate compare to other one and necessary

changes in this method of planning can be done without hampering whole plan.

Top down budgeting – In this approach, senior managers of the company do the work of

estimation of profits and expenditure. They do not involve middle and lower level employees,

this can be considered as the prime reason that budget in this methods are formed in short time

period and without much conflicts. But if the higher authority do not have sound knowledge

about day to day business then cannot do effective planning (What is Budgetary control?, 2017).

3. Merits and demerits of different budgeting methodologies

As mentioned above there are three methods of budgeting. Below are their advantages

and disadvantages:

Incremental

Merits – Its formation is very simple and manager can make any understand about what

is the addition funds which company is going to spend of various expenses. Costing of preparing

is budget is very important factor, if a company is use any other approach then they may have to

incur huge amount of making of an estimation (Otley and Emmanuel, 2013). Normally the

conflicts in an organisation arise because some departments get more funds while other get less

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

sum. In this method, this trouble will not arise. All the division will get same amount and they do

not have to depend on other for additional resources.

Demerits – Most of the managers do not like use this method of budgeting because they

think that it does not show accurate figures. If the planning is does in proper way then it is not

possible to implement the budget and attain desired results. Incremental budgeting does not

allow changes in the new planning. This is not a good feature because in this business

environment changes happens on constant basis.

Zero-based budgeting

Merits – This is a flexible budget and it’s mainly concentrate on key area of operations. It

does not cost much and it has many advantages. If method of estimation is executed in a correct

manner then total cost of business of a company can easily go down.

Demerits – Showing term planning is generally ignored in this method and manager can

easily manipulate the funds towards the activities which are important for them (Zoni, Dossi and

Morelli, 2012).

Top Down budgeting

Merit – Finance is considered as the backbone of every firm, the prime advantage of this

method is the financial resources will remain in the hand of top level management so the

problem of wastage of funds will get minimise. It is a fast process because limited number of

senior managers have to take decision and it help in reducing conflicts and disputes in the

organisation.

Demerit – The moral of employees may go down if they are not involved in planning

process. The chances of inaccurate forecasting is also high because higher authority generally do

not have ground knowledge.

Justification of Selected approach

Zero based budgeting will be most suitable method for Pine limited because if will help

them in removing various kind of insignificant expenditure which is increasing their cost of

operation. They need to adopt a methods where changes can easily be done and this approach

will be best for them.

4. Preparation of cash budget

Every organisation want to use their liquid assets in an effective way so they can reduce

the wastage of monetary resources (Nemet, Baker and Jenni, 2013). It also help a company in

3

not have to depend on other for additional resources.

Demerits – Most of the managers do not like use this method of budgeting because they

think that it does not show accurate figures. If the planning is does in proper way then it is not

possible to implement the budget and attain desired results. Incremental budgeting does not

allow changes in the new planning. This is not a good feature because in this business

environment changes happens on constant basis.

Zero-based budgeting

Merits – This is a flexible budget and it’s mainly concentrate on key area of operations. It

does not cost much and it has many advantages. If method of estimation is executed in a correct

manner then total cost of business of a company can easily go down.

Demerits – Showing term planning is generally ignored in this method and manager can

easily manipulate the funds towards the activities which are important for them (Zoni, Dossi and

Morelli, 2012).

Top Down budgeting

Merit – Finance is considered as the backbone of every firm, the prime advantage of this

method is the financial resources will remain in the hand of top level management so the

problem of wastage of funds will get minimise. It is a fast process because limited number of

senior managers have to take decision and it help in reducing conflicts and disputes in the

organisation.

Demerit – The moral of employees may go down if they are not involved in planning

process. The chances of inaccurate forecasting is also high because higher authority generally do

not have ground knowledge.

Justification of Selected approach

Zero based budgeting will be most suitable method for Pine limited because if will help

them in removing various kind of insignificant expenditure which is increasing their cost of

operation. They need to adopt a methods where changes can easily be done and this approach

will be best for them.

4. Preparation of cash budget

Every organisation want to use their liquid assets in an effective way so they can reduce

the wastage of monetary resources (Nemet, Baker and Jenni, 2013). It also help a company in

3

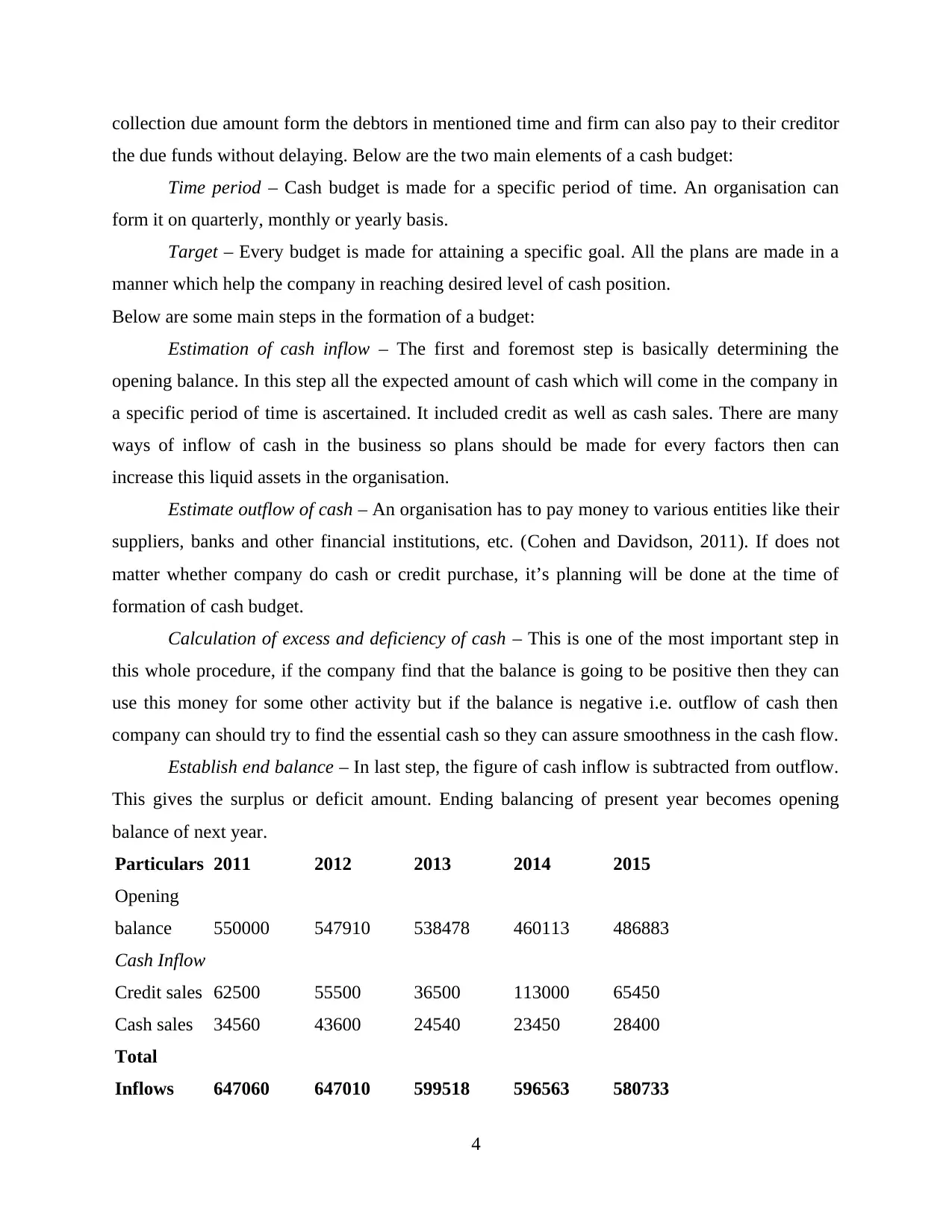

collection due amount form the debtors in mentioned time and firm can also pay to their creditor

the due funds without delaying. Below are the two main elements of a cash budget:

Time period – Cash budget is made for a specific period of time. An organisation can

form it on quarterly, monthly or yearly basis.

Target – Every budget is made for attaining a specific goal. All the plans are made in a

manner which help the company in reaching desired level of cash position.

Below are some main steps in the formation of a budget:

Estimation of cash inflow – The first and foremost step is basically determining the

opening balance. In this step all the expected amount of cash which will come in the company in

a specific period of time is ascertained. It included credit as well as cash sales. There are many

ways of inflow of cash in the business so plans should be made for every factors then can

increase this liquid assets in the organisation.

Estimate outflow of cash – An organisation has to pay money to various entities like their

suppliers, banks and other financial institutions, etc. (Cohen and Davidson, 2011). If does not

matter whether company do cash or credit purchase, it’s planning will be done at the time of

formation of cash budget.

Calculation of excess and deficiency of cash – This is one of the most important step in

this whole procedure, if the company find that the balance is going to be positive then they can

use this money for some other activity but if the balance is negative i.e. outflow of cash then

company can should try to find the essential cash so they can assure smoothness in the cash flow.

Establish end balance – In last step, the figure of cash inflow is subtracted from outflow.

This gives the surplus or deficit amount. Ending balancing of present year becomes opening

balance of next year.

Particulars 2011 2012 2013 2014 2015

Opening

balance 550000 547910 538478 460113 486883

Cash Inflow

Credit sales 62500 55500 36500 113000 65450

Cash sales 34560 43600 24540 23450 28400

Total

Inflows 647060 647010 599518 596563 580733

4

the due funds without delaying. Below are the two main elements of a cash budget:

Time period – Cash budget is made for a specific period of time. An organisation can

form it on quarterly, monthly or yearly basis.

Target – Every budget is made for attaining a specific goal. All the plans are made in a

manner which help the company in reaching desired level of cash position.

Below are some main steps in the formation of a budget:

Estimation of cash inflow – The first and foremost step is basically determining the

opening balance. In this step all the expected amount of cash which will come in the company in

a specific period of time is ascertained. It included credit as well as cash sales. There are many

ways of inflow of cash in the business so plans should be made for every factors then can

increase this liquid assets in the organisation.

Estimate outflow of cash – An organisation has to pay money to various entities like their

suppliers, banks and other financial institutions, etc. (Cohen and Davidson, 2011). If does not

matter whether company do cash or credit purchase, it’s planning will be done at the time of

formation of cash budget.

Calculation of excess and deficiency of cash – This is one of the most important step in

this whole procedure, if the company find that the balance is going to be positive then they can

use this money for some other activity but if the balance is negative i.e. outflow of cash then

company can should try to find the essential cash so they can assure smoothness in the cash flow.

Establish end balance – In last step, the figure of cash inflow is subtracted from outflow.

This gives the surplus or deficit amount. Ending balancing of present year becomes opening

balance of next year.

Particulars 2011 2012 2013 2014 2015

Opening

balance 550000 547910 538478 460113 486883

Cash Inflow

Credit sales 62500 55500 36500 113000 65450

Cash sales 34560 43600 24540 23450 28400

Total

Inflows 647060 647010 599518 596563 580733

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

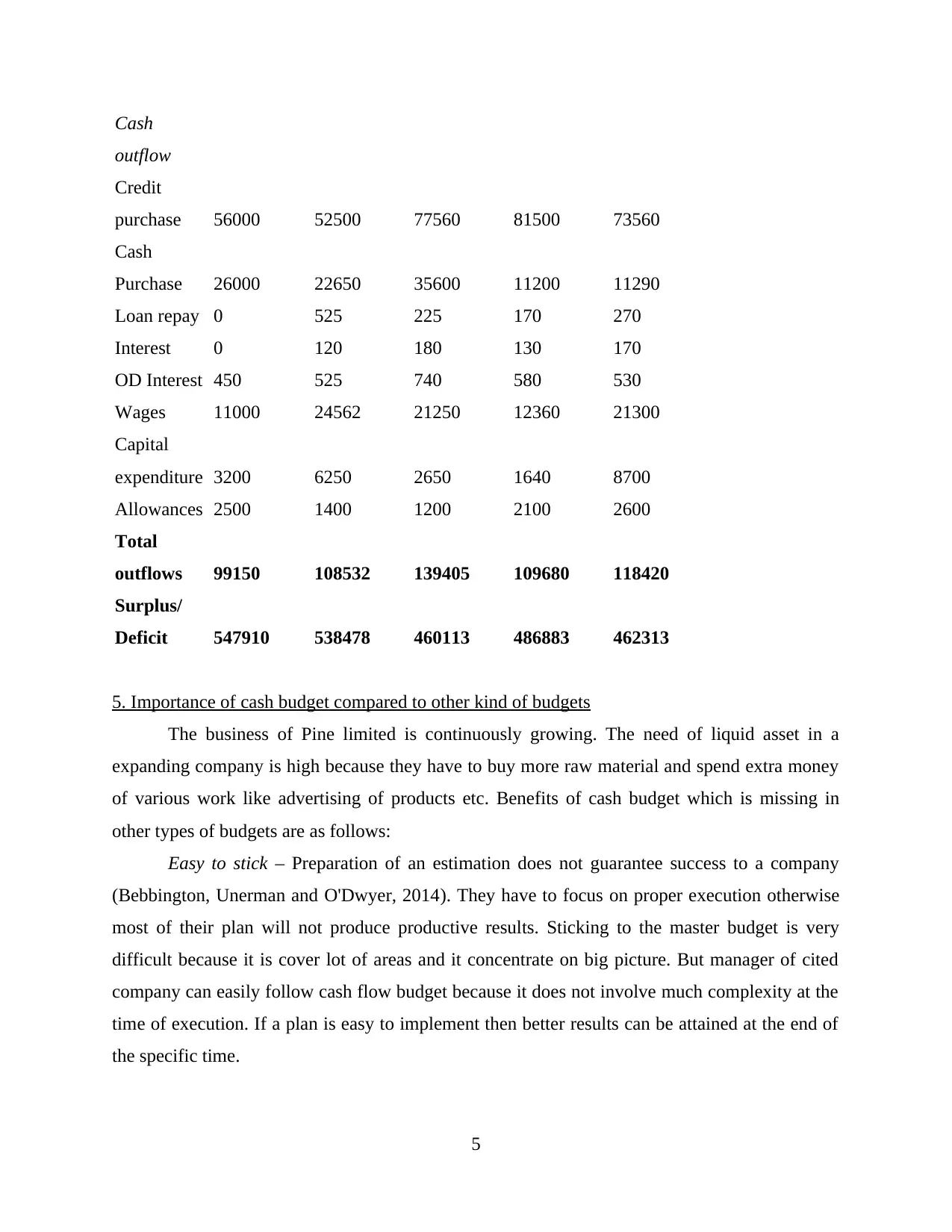

Cash

outflow

Credit

purchase 56000 52500 77560 81500 73560

Cash

Purchase 26000 22650 35600 11200 11290

Loan repay 0 525 225 170 270

Interest 0 120 180 130 170

OD Interest 450 525 740 580 530

Wages 11000 24562 21250 12360 21300

Capital

expenditure 3200 6250 2650 1640 8700

Allowances 2500 1400 1200 2100 2600

Total

outflows 99150 108532 139405 109680 118420

Surplus/

Deficit 547910 538478 460113 486883 462313

5. Importance of cash budget compared to other kind of budgets

The business of Pine limited is continuously growing. The need of liquid asset in a

expanding company is high because they have to buy more raw material and spend extra money

of various work like advertising of products etc. Benefits of cash budget which is missing in

other types of budgets are as follows:

Easy to stick – Preparation of an estimation does not guarantee success to a company

(Bebbington, Unerman and O'Dwyer, 2014). They have to focus on proper execution otherwise

most of their plan will not produce productive results. Sticking to the master budget is very

difficult because it is cover lot of areas and it concentrate on big picture. But manager of cited

company can easily follow cash flow budget because it does not involve much complexity at the

time of execution. If a plan is easy to implement then better results can be attained at the end of

the specific time.

5

outflow

Credit

purchase 56000 52500 77560 81500 73560

Cash

Purchase 26000 22650 35600 11200 11290

Loan repay 0 525 225 170 270

Interest 0 120 180 130 170

OD Interest 450 525 740 580 530

Wages 11000 24562 21250 12360 21300

Capital

expenditure 3200 6250 2650 1640 8700

Allowances 2500 1400 1200 2100 2600

Total

outflows 99150 108532 139405 109680 118420

Surplus/

Deficit 547910 538478 460113 486883 462313

5. Importance of cash budget compared to other kind of budgets

The business of Pine limited is continuously growing. The need of liquid asset in a

expanding company is high because they have to buy more raw material and spend extra money

of various work like advertising of products etc. Benefits of cash budget which is missing in

other types of budgets are as follows:

Easy to stick – Preparation of an estimation does not guarantee success to a company

(Bebbington, Unerman and O'Dwyer, 2014). They have to focus on proper execution otherwise

most of their plan will not produce productive results. Sticking to the master budget is very

difficult because it is cover lot of areas and it concentrate on big picture. But manager of cited

company can easily follow cash flow budget because it does not involve much complexity at the

time of execution. If a plan is easy to implement then better results can be attained at the end of

the specific time.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Short term – Normally estimation like master and operating budget are ascertained for a

year, but cash budget can be made for every month or quarter. Its preparation do not take much

time and resources. The debtor, who may get convert into defaulters, can be tracked in short time

period by doing effective planning in this type of budget.

Liquidity – A growing business need high liquidity and this task can be attaining by

making cash flow budget. Other estimations like operation and master budget do not put much

focus on cash and other liquid asset (Agbejule, 2011). They cover different aspect of the business

so it is difficult for them to focus on single element like cash. This factor i.e. ''liquidity'' increase

the importance of cash budget.

Smooth function – Master and operating budget do not focus on smooth functioning in the

organisation, but cash budget do not make plan for keeping proper inflow and outflow of the

cash. Many big corporations saw failure in their business because they failed to manage money

in correct manner.

CONCLUSION

From the above report, it can be concluded that making budget has various advantages.

There are different kinds of budgets and a company should select one type according to their

need and suitability. Methods of budgeting should be adopted by keeping current position of

company in mind. Most of the corporations make budget so that they can reduce the wastage of

resources and invest their funds in right areas. If this work is not done properly then an

organisation can face huge loss and confusion and conflicts in the firm will also increase.

6

year, but cash budget can be made for every month or quarter. Its preparation do not take much

time and resources. The debtor, who may get convert into defaulters, can be tracked in short time

period by doing effective planning in this type of budget.

Liquidity – A growing business need high liquidity and this task can be attaining by

making cash flow budget. Other estimations like operation and master budget do not put much

focus on cash and other liquid asset (Agbejule, 2011). They cover different aspect of the business

so it is difficult for them to focus on single element like cash. This factor i.e. ''liquidity'' increase

the importance of cash budget.

Smooth function – Master and operating budget do not focus on smooth functioning in the

organisation, but cash budget do not make plan for keeping proper inflow and outflow of the

cash. Many big corporations saw failure in their business because they failed to manage money

in correct manner.

CONCLUSION

From the above report, it can be concluded that making budget has various advantages.

There are different kinds of budgets and a company should select one type according to their

need and suitability. Methods of budgeting should be adopted by keeping current position of

company in mind. Most of the corporations make budget so that they can reduce the wastage of

resources and invest their funds in right areas. If this work is not done properly then an

organisation can face huge loss and confusion and conflicts in the firm will also increase.

6

REFERENCES

Books and Journals

Agbejule, A., 2011. Organizational culture and performance: the role of management accounting

system. Journal of Applied Accounting Research. 12(1). pp.74-89.

Bebbington, J., Unerman, J. and O'Dwyer, B. eds., 2014. Sustainability accounting and

accountability. Routledge.

Cohen, A. and Davidson, S., 2011. The watershed approach: Challenges, antecedents, and the

transition from technical tool to governance unit. Water alternatives. 4(1). p.1.

Nemet, G.F., Baker, E. and Jenni, K.E., 2013. Modeling the future costs of carbon capture using

experts' elicited probabilities under policy scenarios. Energy. 56. pp.218-228.

Zoni, L., Dossi, A. and Morelli, M., 2012. Management accounting system (MAS) change: field

evidence. Asia-Pacific Journal of Accounting & Economics. 19(1). pp.119-138.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management control.

Springer.

Shaw, B.A., Agahi, N. and Krause, N., 2011. Are changes in financial strain associated with

changes in alcohol use and smoking among older adults?. Journal of studies on alcohol

and drugs. 72(6). pp.917-925.

Tsamenyi, M., Sahadev, S. and Qiao, Z.S., 2011. The relationship between business strategy,

management control systems and performance: Evidence from China. Advances in

Accounting. 27(1). pp.193-203.

Vakalfotis, N., Ballantine, J. and Wall, A. P., 2013. A literature review on the impact of

Enterprise Systems on management accounting.

Online

What is Budgetary control?. 2017. [Online]. Available Through:

<https://accountlearning.com/budgetary-control-objectives-advantages-disadvantages/>.

[Accessed On 9th November 2017].

7

Books and Journals

Agbejule, A., 2011. Organizational culture and performance: the role of management accounting

system. Journal of Applied Accounting Research. 12(1). pp.74-89.

Bebbington, J., Unerman, J. and O'Dwyer, B. eds., 2014. Sustainability accounting and

accountability. Routledge.

Cohen, A. and Davidson, S., 2011. The watershed approach: Challenges, antecedents, and the

transition from technical tool to governance unit. Water alternatives. 4(1). p.1.

Nemet, G.F., Baker, E. and Jenni, K.E., 2013. Modeling the future costs of carbon capture using

experts' elicited probabilities under policy scenarios. Energy. 56. pp.218-228.

Zoni, L., Dossi, A. and Morelli, M., 2012. Management accounting system (MAS) change: field

evidence. Asia-Pacific Journal of Accounting & Economics. 19(1). pp.119-138.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management control.

Springer.

Shaw, B.A., Agahi, N. and Krause, N., 2011. Are changes in financial strain associated with

changes in alcohol use and smoking among older adults?. Journal of studies on alcohol

and drugs. 72(6). pp.917-925.

Tsamenyi, M., Sahadev, S. and Qiao, Z.S., 2011. The relationship between business strategy,

management control systems and performance: Evidence from China. Advances in

Accounting. 27(1). pp.193-203.

Vakalfotis, N., Ballantine, J. and Wall, A. P., 2013. A literature review on the impact of

Enterprise Systems on management accounting.

Online

What is Budgetary control?. 2017. [Online]. Available Through:

<https://accountlearning.com/budgetary-control-objectives-advantages-disadvantages/>.

[Accessed On 9th November 2017].

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.