Management Accounting Report: Budgeting Process and Analysis

VerifiedAdded on 2022/11/28

|11

|2558

|431

Report

AI Summary

This report provides a comprehensive analysis of the budgeting process within the context of management accounting. It begins with an executive summary highlighting the importance of budgeting in strategic planning, followed by an introduction that emphasizes its role in implementing business plans and achieving objectives. The report is divided into two main parts: the first presents a detailed computation of inventory, purchases, and budgeted gross profit through tables and working notes. The second part delves into budgeting as a non-technical process, outlining key steps such as financial objective determination, fund availability assessment, and the consideration of environmental uncertainties. It explores various budget types, including sales, cash, and production budgets, emphasizing the significance of sales budgets. The report also discusses the roles of top-down and bottom-up budgeting approaches, alongside the budget's broader impact on the economy and government policies. A concluding section summarizes the key findings and offers recommendations, supported by a comprehensive list of references.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Executive Summary.........................................................................................................................3

Introduction......................................................................................................................................3

Part one............................................................................................................................................3

Part Two...........................................................................................................................................4

A) Budgeting: A non-technical process.......................................................................................4

B) Professional Presentation........................................................................................................9

Conclusion and Recommendation...................................................................................................9

References......................................................................................................................................10

Executive Summary.........................................................................................................................3

Introduction......................................................................................................................................3

Part one............................................................................................................................................3

Part Two...........................................................................................................................................4

A) Budgeting: A non-technical process.......................................................................................4

B) Professional Presentation........................................................................................................9

Conclusion and Recommendation...................................................................................................9

References......................................................................................................................................10

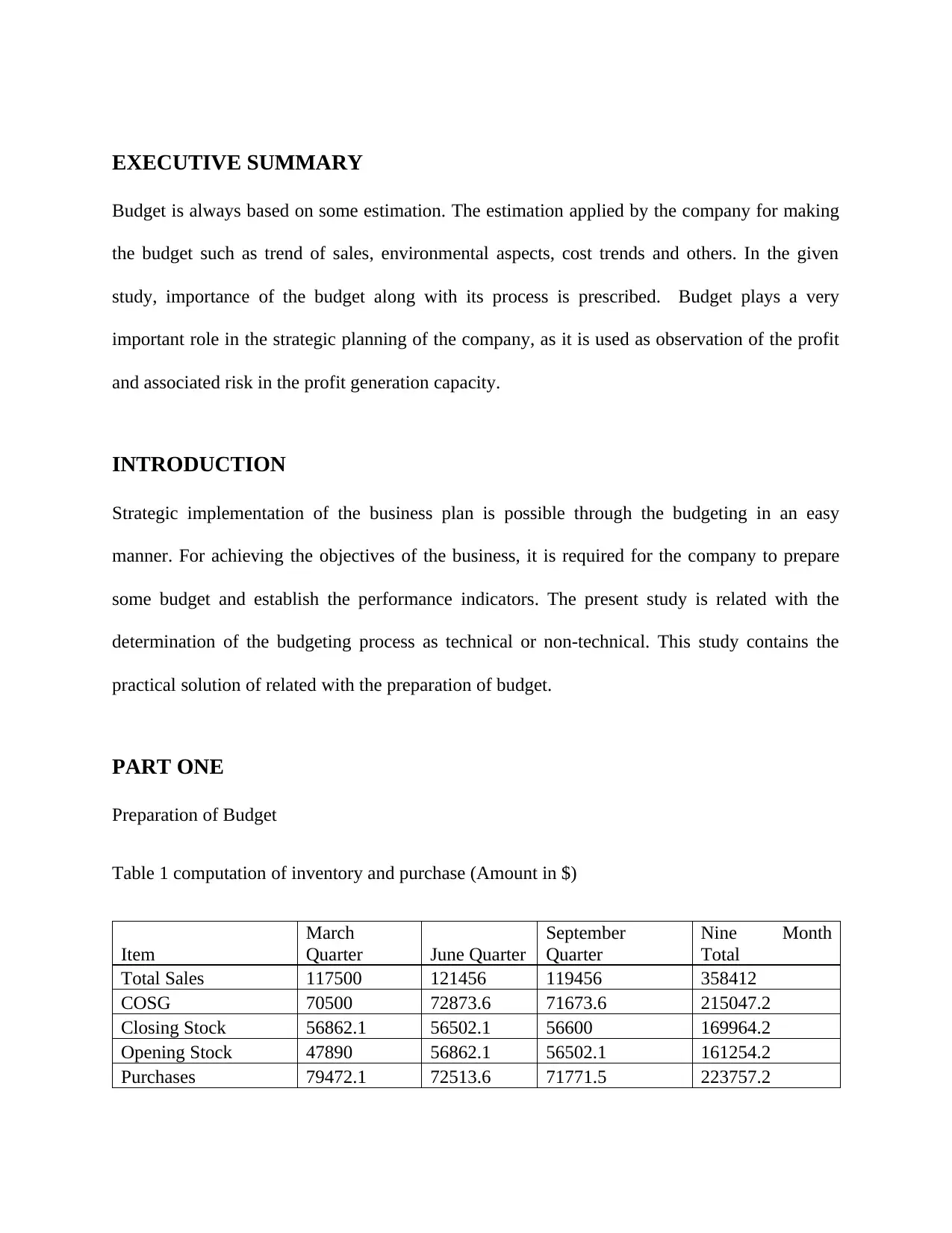

EXECUTIVE SUMMARY

Budget is always based on some estimation. The estimation applied by the company for making

the budget such as trend of sales, environmental aspects, cost trends and others. In the given

study, importance of the budget along with its process is prescribed. Budget plays a very

important role in the strategic planning of the company, as it is used as observation of the profit

and associated risk in the profit generation capacity.

INTRODUCTION

Strategic implementation of the business plan is possible through the budgeting in an easy

manner. For achieving the objectives of the business, it is required for the company to prepare

some budget and establish the performance indicators. The present study is related with the

determination of the budgeting process as technical or non-technical. This study contains the

practical solution of related with the preparation of budget.

PART ONE

Preparation of Budget

Table 1 computation of inventory and purchase (Amount in $)

Item

March

Quarter June Quarter

September

Quarter

Nine Month

Total

Total Sales 117500 121456 119456 358412

COSG 70500 72873.6 71673.6 215047.2

Closing Stock 56862.1 56502.1 56600 169964.2

Opening Stock 47890 56862.1 56502.1 161254.2

Purchases 79472.1 72513.6 71771.5 223757.2

Budget is always based on some estimation. The estimation applied by the company for making

the budget such as trend of sales, environmental aspects, cost trends and others. In the given

study, importance of the budget along with its process is prescribed. Budget plays a very

important role in the strategic planning of the company, as it is used as observation of the profit

and associated risk in the profit generation capacity.

INTRODUCTION

Strategic implementation of the business plan is possible through the budgeting in an easy

manner. For achieving the objectives of the business, it is required for the company to prepare

some budget and establish the performance indicators. The present study is related with the

determination of the budgeting process as technical or non-technical. This study contains the

practical solution of related with the preparation of budget.

PART ONE

Preparation of Budget

Table 1 computation of inventory and purchase (Amount in $)

Item

March

Quarter June Quarter

September

Quarter

Nine Month

Total

Total Sales 117500 121456 119456 358412

COSG 70500 72873.6 71673.6 215047.2

Closing Stock 56862.1 56502.1 56600 169964.2

Opening Stock 47890 56862.1 56502.1 161254.2

Purchases 79472.1 72513.6 71771.5 223757.2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Statement of Budgeted Gross Profit

Table 2 Statement of Budgeted Gross Profit (Amount in $)

Item

March

Quarter

June

Quarter

September

Quarter

Nine Month

Total

Total Sales 117500 121456 119456 358412

Add - Closing Stock 56862.1 56502.1 56600 169964

Less – Purchase 79472.1 72513.6 71771.5 223757

Less - Opening Stock 47890 56862.1 56502.1 161254

Gross Profit 47000 48582.4 47782.4 143365

Working Notes –

Cost of goods sold is like 60% of total sales of the current quarter

Closing stock is computed by 35000 plus 30% of the cost of goods sold of next three

months (quarter).

Opening stock is the closing stock of last quarter.

Purchases are computed by addition of the closing stock in the cost of goods sold and

deduction of the opening stock.

PART TWO

A) Budgeting: A non-technical process

Future profit or expenditure can be determined by the implementation of the budget process

(King, 2015). For keeping the record of income and expenditure budgeting process is applied by

the organizations. In order to the management of the finance of the company, it is considered as

Table 2 Statement of Budgeted Gross Profit (Amount in $)

Item

March

Quarter

June

Quarter

September

Quarter

Nine Month

Total

Total Sales 117500 121456 119456 358412

Add - Closing Stock 56862.1 56502.1 56600 169964

Less – Purchase 79472.1 72513.6 71771.5 223757

Less - Opening Stock 47890 56862.1 56502.1 161254

Gross Profit 47000 48582.4 47782.4 143365

Working Notes –

Cost of goods sold is like 60% of total sales of the current quarter

Closing stock is computed by 35000 plus 30% of the cost of goods sold of next three

months (quarter).

Opening stock is the closing stock of last quarter.

Purchases are computed by addition of the closing stock in the cost of goods sold and

deduction of the opening stock.

PART TWO

A) Budgeting: A non-technical process

Future profit or expenditure can be determined by the implementation of the budget process

(King, 2015). For keeping the record of income and expenditure budgeting process is applied by

the organizations. In order to the management of the finance of the company, it is considered as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

controlling and monitoring technique. This process is started by the determination of the

financial objective of the company, and on the basis of this budget will build. In addition,

prediction, controlling, monitoring, analyzing, and evaluation of the monetary objectives are

considered as other important elements of the budgeting process (McDONALD, 2016).

For any business entity, the budget process plays a very important role. A business can tract its

earnings and expenditure only through a proper budget. It is referred as a guideline, which can be

used by the company for observation of its profit stream and can ascertain probable risk

associated with its earning generating capacity (Wolf, and Floyd, 2017). It is an important

technique with respect to putting control in the manner of spending by business. The main

objective of the company preparing the budget is to ensure that all money spends in the right

direction and for the achievement of the financial objective.

Although budgeting is the detailed process, in which some steps are included, it is not a technical

process(Blanchard, 2015). Steps, which should be followed by the company, at the time of

preparation of the budget is as follows –

These estimations must be review by the management by considering the present situation,

before building the budget (Dudin et al. 2015).Non-availability of the money may lead to

difficulty for the company. Therefore, the company should give sufficient consideration to the

availability of the fund as and when required. Further, the adequacy of investable funds will

ascertain the starting of viable projects (Fenton et al. 2015).

Due to the uncertainty in the environment, there is a possibility that it may face any difficulty

and problem, which may lead to a change in manner of calculation total cost. Therefore, the

management should consider the elements by which the cost structure of the company may

financial objective of the company, and on the basis of this budget will build. In addition,

prediction, controlling, monitoring, analyzing, and evaluation of the monetary objectives are

considered as other important elements of the budgeting process (McDONALD, 2016).

For any business entity, the budget process plays a very important role. A business can tract its

earnings and expenditure only through a proper budget. It is referred as a guideline, which can be

used by the company for observation of its profit stream and can ascertain probable risk

associated with its earning generating capacity (Wolf, and Floyd, 2017). It is an important

technique with respect to putting control in the manner of spending by business. The main

objective of the company preparing the budget is to ensure that all money spends in the right

direction and for the achievement of the financial objective.

Although budgeting is the detailed process, in which some steps are included, it is not a technical

process(Blanchard, 2015). Steps, which should be followed by the company, at the time of

preparation of the budget is as follows –

These estimations must be review by the management by considering the present situation,

before building the budget (Dudin et al. 2015).Non-availability of the money may lead to

difficulty for the company. Therefore, the company should give sufficient consideration to the

availability of the fund as and when required. Further, the adequacy of investable funds will

ascertain the starting of viable projects (Fenton et al. 2015).

Due to the uncertainty in the environment, there is a possibility that it may face any difficulty

and problem, which may lead to a change in manner of calculation total cost. Therefore, the

management should consider the elements by which the cost structure of the company may

changes, at the time of preparation of the budget. For the reliability of budgeting factors, all these

elements are identified in advance by the management of the company (Johnsen, 2015).

For making the current period budget, management should consider the data of the previous year.

On the basis of any change in environmental conditions, updating in the previous budget is

required. Budget package is considered as a type of outline, on the basis of which budget is

prepared (Sull, Homkes, and Sull, 2015).

There are several types of budget which are prepared by the company, such as cash budget,

purchase budget, sales budget, production budget and many others. Among these budget, sales

budget is one of the comprehensive budgets. Moreover, all budgets are made after considering

the sales budget. By the sales budget, a company can ascertain whether it can generate adequate

revenue, which is essential for the survival of the business. Therefore, management should give

sufficientconsideration for the prediction of the demand, so that sales budget can be made on the

basis of reliable assumptions (Reilly, Souder, and Ranucci, 2016).

By obtaining the budget of departments, a company can identify the budget expenditure for the

entire budgeted period. Every department of the company prepares its own budget, and all the

departmental budget are combined in order to create the master budget (Shaw, 2016).In the

process of budget, reimbursement plays a significant role. Since the reimbursement provided by

the company is subject to yearly enhancement; therefore, it must be prepared by management

carefully. The top management or senior executives are responsible for approving increment in

the compensation should be obtained, and on the basis of this budget process is determined

(Papke-Shields, and Boyer-Wright, 2017).

elements are identified in advance by the management of the company (Johnsen, 2015).

For making the current period budget, management should consider the data of the previous year.

On the basis of any change in environmental conditions, updating in the previous budget is

required. Budget package is considered as a type of outline, on the basis of which budget is

prepared (Sull, Homkes, and Sull, 2015).

There are several types of budget which are prepared by the company, such as cash budget,

purchase budget, sales budget, production budget and many others. Among these budget, sales

budget is one of the comprehensive budgets. Moreover, all budgets are made after considering

the sales budget. By the sales budget, a company can ascertain whether it can generate adequate

revenue, which is essential for the survival of the business. Therefore, management should give

sufficientconsideration for the prediction of the demand, so that sales budget can be made on the

basis of reliable assumptions (Reilly, Souder, and Ranucci, 2016).

By obtaining the budget of departments, a company can identify the budget expenditure for the

entire budgeted period. Every department of the company prepares its own budget, and all the

departmental budget are combined in order to create the master budget (Shaw, 2016).In the

process of budget, reimbursement plays a significant role. Since the reimbursement provided by

the company is subject to yearly enhancement; therefore, it must be prepared by management

carefully. The top management or senior executives are responsible for approving increment in

the compensation should be obtained, and on the basis of this budget process is determined

(Papke-Shields, and Boyer-Wright, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

For the encouragement to the employee of the company, the bonus plan is announced. It is

considered as appraisal method, by which workers are guided towards for improving their

performance. If the bonus plans are not considered at the time of preparation of the budget, then

it may significantly affect the budgeted profits. Therefore, any bonus plan which will be

announced by the company in the budgeted period must be considered by management in

advance while preparing of the budget (Arnold, and Gillenkirch, 2015).

The company incurs the capital expenditure for the expansion of the business. It assists the

company in grabbing the opportunities which are essential for the growth. If the company has

any planning for capital expenditure, then management must consider this expenditure in the

budgeting process in advance (Bagheri, 2016).

If there is any change in the estimation, then management should change the model of budget

accordingly and prepare the final budget in a timely manner. After the preparation of the budget,

it should be reviewed by the management by which an error can be identified. Any minor error

may lead to failure of the budgeting process (Ebdon, and Franklin, 2015).

After all the above process, it must be presented to the top management of the company for

getting the permission of implementation of the budget. The top management of the company

reviews the budget and ascertainswhether it is prepared according to the existingcondition of the

company;whether all essential points are considered while making a budget and many other

aspects. Finally, if it is approved by top management, then there is no change required in the

budget.

After the approval by top management of the company, the budget is issued, and all operation is

taking place as per the budget process. By considering the above analysis, it has been drawn that

considered as appraisal method, by which workers are guided towards for improving their

performance. If the bonus plans are not considered at the time of preparation of the budget, then

it may significantly affect the budgeted profits. Therefore, any bonus plan which will be

announced by the company in the budgeted period must be considered by management in

advance while preparing of the budget (Arnold, and Gillenkirch, 2015).

The company incurs the capital expenditure for the expansion of the business. It assists the

company in grabbing the opportunities which are essential for the growth. If the company has

any planning for capital expenditure, then management must consider this expenditure in the

budgeting process in advance (Bagheri, 2016).

If there is any change in the estimation, then management should change the model of budget

accordingly and prepare the final budget in a timely manner. After the preparation of the budget,

it should be reviewed by the management by which an error can be identified. Any minor error

may lead to failure of the budgeting process (Ebdon, and Franklin, 2015).

After all the above process, it must be presented to the top management of the company for

getting the permission of implementation of the budget. The top management of the company

reviews the budget and ascertainswhether it is prepared according to the existingcondition of the

company;whether all essential points are considered while making a budget and many other

aspects. Finally, if it is approved by top management, then there is no change required in the

budget.

After the approval by top management of the company, the budget is issued, and all operation is

taking place as per the budget process. By considering the above analysis, it has been drawn that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the process of the preparation of the budget is the lengthy process, which required significant

time. It is not a technical process. A small business organization, as well as a large business

organization, can prepare their budget easily. Along with this, there are two approaches, namely,

Top – Down Budget and Bottom-up Budget by which a budget can be prepared, which are

defined as below –

Top-Down Budget:In this approach, the primary outline of the budget is created by the top

executives of the company. They identify the financial objective of a company which is required

to maintain. In addition, estimations related to the sales, reimbursement, capital budget and many

others are provided by senior executives of the company. In this time, the participation by the

lower management is very less. They only execute the plans which are provided by the top

executives in the budgeting process.

Bottom – Up Budget:This approach is referred to as the contributory approach in the budgeting

process. In this type, the lower level management or the employee of the company prepare the

budget. They prepare a budget as per the guidelines provided by the top executives of the

company. Every division of the company formulates its own budget as per the guidelines

provided by the top management of the company. In this, an employee of the company seems

more committed to following the budget, as they participate in the budgeting process (Beckeret

al. 2016).

Apart from the above aspects, the budget play significant role in the economy of the country. It

provides detailed guidelines; on the basis of this government make the policies to run the

country. It sets the target for the revenue and costs, which can be obtained through a variety of

manner. Along with this, it also makes plans for capital expenditure of the country;the

time. It is not a technical process. A small business organization, as well as a large business

organization, can prepare their budget easily. Along with this, there are two approaches, namely,

Top – Down Budget and Bottom-up Budget by which a budget can be prepared, which are

defined as below –

Top-Down Budget:In this approach, the primary outline of the budget is created by the top

executives of the company. They identify the financial objective of a company which is required

to maintain. In addition, estimations related to the sales, reimbursement, capital budget and many

others are provided by senior executives of the company. In this time, the participation by the

lower management is very less. They only execute the plans which are provided by the top

executives in the budgeting process.

Bottom – Up Budget:This approach is referred to as the contributory approach in the budgeting

process. In this type, the lower level management or the employee of the company prepare the

budget. They prepare a budget as per the guidelines provided by the top executives of the

company. Every division of the company formulates its own budget as per the guidelines

provided by the top management of the company. In this, an employee of the company seems

more committed to following the budget, as they participate in the budgeting process (Beckeret

al. 2016).

Apart from the above aspects, the budget play significant role in the economy of the country. It

provides detailed guidelines; on the basis of this government make the policies to run the

country. It sets the target for the revenue and costs, which can be obtained through a variety of

manner. Along with this, it also makes plans for capital expenditure of the country;the

government can ascertain about the availability of funds and accordingly make the strategies for

the investment of funds since the budget reliability outlines the expenditure. Therefore the

budgeting process assists the government in putting control over the spending. Without a proper

budget, the government cannot track the records of its revenue and expenditures. Therefore, it

can be said that the budget offers them several predictions by which they can ascertain about the

manner of carrying the operations.

B) Professional Presentation

Given in the power point presentation

CONCLUSION AND RECOMMENDATION

By considering all the above aspect, it has been drawn that by development of the predicated

financial statement, management can prepare the plans and policies and determines whether it is

beneficial for the company to run the business. Therefore, the management thinks that it is

purely technical process, which requires the prediction, controlling and the evaluation of the

financial objectives of company. Further, it has been analyzed that the budget is a non-technical

process, with aspect to the adequacy of budgeting as a political process. Financial management

system of the country significantly influenced by the political governance, therefore for

establishing the responsibility of governance system, proper budgeting system is required.

the investment of funds since the budget reliability outlines the expenditure. Therefore the

budgeting process assists the government in putting control over the spending. Without a proper

budget, the government cannot track the records of its revenue and expenditures. Therefore, it

can be said that the budget offers them several predictions by which they can ascertain about the

manner of carrying the operations.

B) Professional Presentation

Given in the power point presentation

CONCLUSION AND RECOMMENDATION

By considering all the above aspect, it has been drawn that by development of the predicated

financial statement, management can prepare the plans and policies and determines whether it is

beneficial for the company to run the business. Therefore, the management thinks that it is

purely technical process, which requires the prediction, controlling and the evaluation of the

financial objectives of company. Further, it has been analyzed that the budget is a non-technical

process, with aspect to the adequacy of budgeting as a political process. Financial management

system of the country significantly influenced by the political governance, therefore for

establishing the responsibility of governance system, proper budgeting system is required.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Arnold, M.C. and Gillenkirch, R.M., 2015. Using negotiated budgets for planning and

performance evaluation: An experimental study. Accounting, organizations and society, 43(1),

pp.1-16.

Bagheri, J., 2016. Overlaps between human resources’ strategic planning and strategic

management tools in public organizations. Procedia-Social and Behavioral Sciences, 230(1),

pp.430-438.

Becker, S.D., Mahlendorf, M.D., Schäffer, U. and Thaten, M., 2016. Budgeting in times of

economic crisis. Contemporary Accounting Research, 33(4), pp.1489-1517.

Blanchard, L.A., 2015. PART and performance budgeting effectiveness. In Performance

Management and Budgeting(pp. 81-105). Routledge.

Dudin, M., Kucuri, G., Fedorova, I., Dzusova, S. and Namitulina, A., 2015. The innovative

business model canvas in the system of effective budgeting. Asian Social Science, 11(7), pp.290-

296.

Ebdon, C. and Franklin, A.L., 2015. Democracy, public participation, and budgeting: Mutually

exclusive or just exhausting?. In Democracy and public administration (pp. 96-118). Routledge.

Fenton, P., Gustafsson, S., Ivner, J. and Palm, J., 2015. Sustainable Energy and Climate

Strategies: lessons from planning processes in five municipalities. Journal of Cleaner

Production, 98(1), pp.213-221.

Johnsen, Å., 2015. Strategic management thinking and practice in the public sector: A strategic

planning for all seasons?. Financial Accountability & Management, 31(3), pp.243-268.

King, W.R., 2015. Planning for Information Systems: An Introduction. In Planning for

information systems (pp. 15-28). Routledge.

McDONALD, M.A.L.C.O.L.M., 2016. Strategic marketing planning: theory and practice. In The

marketing book (pp. 108-142). Routledge.

Papke-Shields, K.E. and Boyer-Wright, K.M., 2017. Strategic planning characteristics applied to

project management. International Journal of Project Management, 35(2), pp.169-179.

Reilly, G., Souder, D. and Ranucci, R., 2016. Time horizon of investments in the resource

allocation process: Review and framework for next steps. Journal of Management, 42(5),

pp.1169-1194.

Shaw, T., 2016. Performance budgeting practices and procedures. OECD Journal on

Budgeting, 15(3), pp.65-136.

Arnold, M.C. and Gillenkirch, R.M., 2015. Using negotiated budgets for planning and

performance evaluation: An experimental study. Accounting, organizations and society, 43(1),

pp.1-16.

Bagheri, J., 2016. Overlaps between human resources’ strategic planning and strategic

management tools in public organizations. Procedia-Social and Behavioral Sciences, 230(1),

pp.430-438.

Becker, S.D., Mahlendorf, M.D., Schäffer, U. and Thaten, M., 2016. Budgeting in times of

economic crisis. Contemporary Accounting Research, 33(4), pp.1489-1517.

Blanchard, L.A., 2015. PART and performance budgeting effectiveness. In Performance

Management and Budgeting(pp. 81-105). Routledge.

Dudin, M., Kucuri, G., Fedorova, I., Dzusova, S. and Namitulina, A., 2015. The innovative

business model canvas in the system of effective budgeting. Asian Social Science, 11(7), pp.290-

296.

Ebdon, C. and Franklin, A.L., 2015. Democracy, public participation, and budgeting: Mutually

exclusive or just exhausting?. In Democracy and public administration (pp. 96-118). Routledge.

Fenton, P., Gustafsson, S., Ivner, J. and Palm, J., 2015. Sustainable Energy and Climate

Strategies: lessons from planning processes in five municipalities. Journal of Cleaner

Production, 98(1), pp.213-221.

Johnsen, Å., 2015. Strategic management thinking and practice in the public sector: A strategic

planning for all seasons?. Financial Accountability & Management, 31(3), pp.243-268.

King, W.R., 2015. Planning for Information Systems: An Introduction. In Planning for

information systems (pp. 15-28). Routledge.

McDONALD, M.A.L.C.O.L.M., 2016. Strategic marketing planning: theory and practice. In The

marketing book (pp. 108-142). Routledge.

Papke-Shields, K.E. and Boyer-Wright, K.M., 2017. Strategic planning characteristics applied to

project management. International Journal of Project Management, 35(2), pp.169-179.

Reilly, G., Souder, D. and Ranucci, R., 2016. Time horizon of investments in the resource

allocation process: Review and framework for next steps. Journal of Management, 42(5),

pp.1169-1194.

Shaw, T., 2016. Performance budgeting practices and procedures. OECD Journal on

Budgeting, 15(3), pp.65-136.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sull, D., Homkes, R. and Sull, C., 2015. Why strategy execution unravels—and what to do about

it. Harvard Business Review, 93(3), pp.57-66.

Wolf, C. and Floyd, S.W., 2017. Strategic planning research: Toward a theory-driven

agenda. Journal of Management, 43(6), pp.1754-1788.

it. Harvard Business Review, 93(3), pp.57-66.

Wolf, C. and Floyd, S.W., 2017. Strategic planning research: Toward a theory-driven

agenda. Journal of Management, 43(6), pp.1754-1788.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.