Management Accounting Report: Budgeting and Investment

VerifiedAdded on 2021/05/31

|14

|1441

|26

Report

AI Summary

This report analyzes a management accounting assignment, focusing on the preparation of a master budget, investment decisions, and the comparison of participative and imposed budgetary approaches. Part A details the components of a master budget, including sales, production, direct labor, purchase, direct material, manufacturing overhead, cash, cost of goods manufactured, and income statements. Part B assesses an investment decision made by a production manager, evaluating its impact through budget analysis. The analysis reveals declining sales and potential losses, suggesting the investment plan might not be viable. Part C contrasts participative and imposed budgetary approaches, highlighting the benefits of the participative method for flexibility and employee involvement, advocating for its use by the sales and production manager to formulate an appropriate budget. The report references key academic sources to support its findings and recommendations.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGEMENT ACCOUNTING

Table of Contents

Part A...............................................................................................................................................2

Preparation of Master Budget......................................................................................................2

Part B.............................................................................................................................................10

Investment Decision..................................................................................................................10

Part C.............................................................................................................................................12

Participative and Imposed Budgetary Approach.......................................................................12

Reference.......................................................................................................................................13

MANAGEMENT ACCOUNTING

Table of Contents

Part A...............................................................................................................................................2

Preparation of Master Budget......................................................................................................2

Part B.............................................................................................................................................10

Investment Decision..................................................................................................................10

Part C.............................................................................................................................................12

Participative and Imposed Budgetary Approach.......................................................................12

Reference.......................................................................................................................................13

2

MANAGEMENT ACCOUNTING

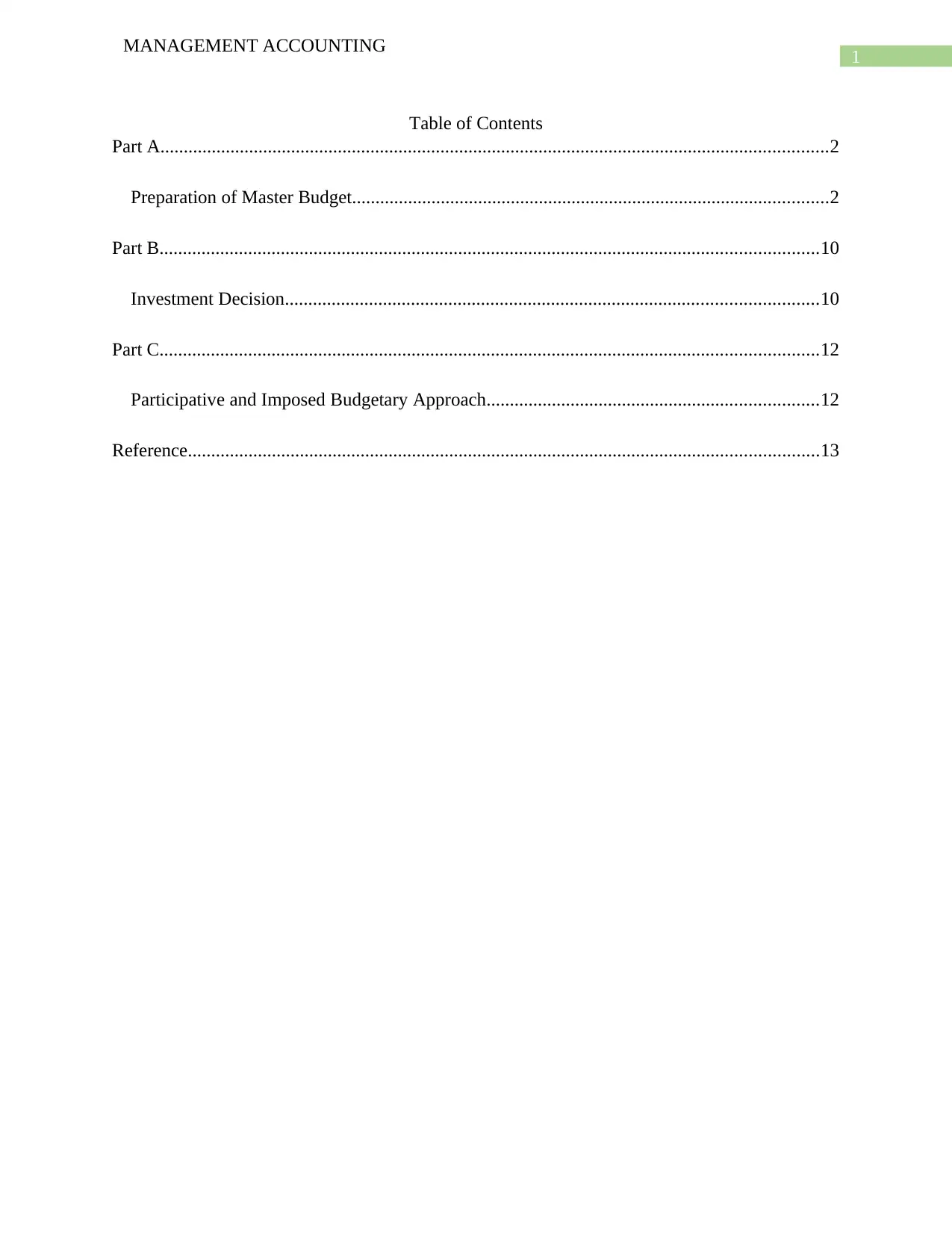

Part A

Preparation of Master Budget

A master budget is the aggregate of all budgets which are prepared by different

departments of the management covering different areas or functions in an organization and also

includes a cash forecast budget, financial plan and a forecasted income statement which is

related to the activities of the business. A master Budget is prepared generally for a quarter or on

a month’s basis so that all activities of the business can be monitored and directed towards the

achievement of the common goal of the company (Edwards, Harris & McCaffer, 2014). The

components of a master budget are shown below:

Sales Budget:

Particulars October November December January

Sales Volume in units 43500 34800 39150 52200

Selling Price per unit $3,940.00 $3,940.00 $3,940.00 $3,940.00

Budgeted Sales Revenue $1713,90,000 $1371,12,000 $1542,51,000 $2056,68,000

Figure 1: (Image showing Sales Budget)

Source: (Created by Author)

MANAGEMENT ACCOUNTING

Part A

Preparation of Master Budget

A master budget is the aggregate of all budgets which are prepared by different

departments of the management covering different areas or functions in an organization and also

includes a cash forecast budget, financial plan and a forecasted income statement which is

related to the activities of the business. A master Budget is prepared generally for a quarter or on

a month’s basis so that all activities of the business can be monitored and directed towards the

achievement of the common goal of the company (Edwards, Harris & McCaffer, 2014). The

components of a master budget are shown below:

Sales Budget:

Particulars October November December January

Sales Volume in units 43500 34800 39150 52200

Selling Price per unit $3,940.00 $3,940.00 $3,940.00 $3,940.00

Budgeted Sales Revenue $1713,90,000 $1371,12,000 $1542,51,000 $2056,68,000

Figure 1: (Image showing Sales Budget)

Source: (Created by Author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGEMENT ACCOUNTING

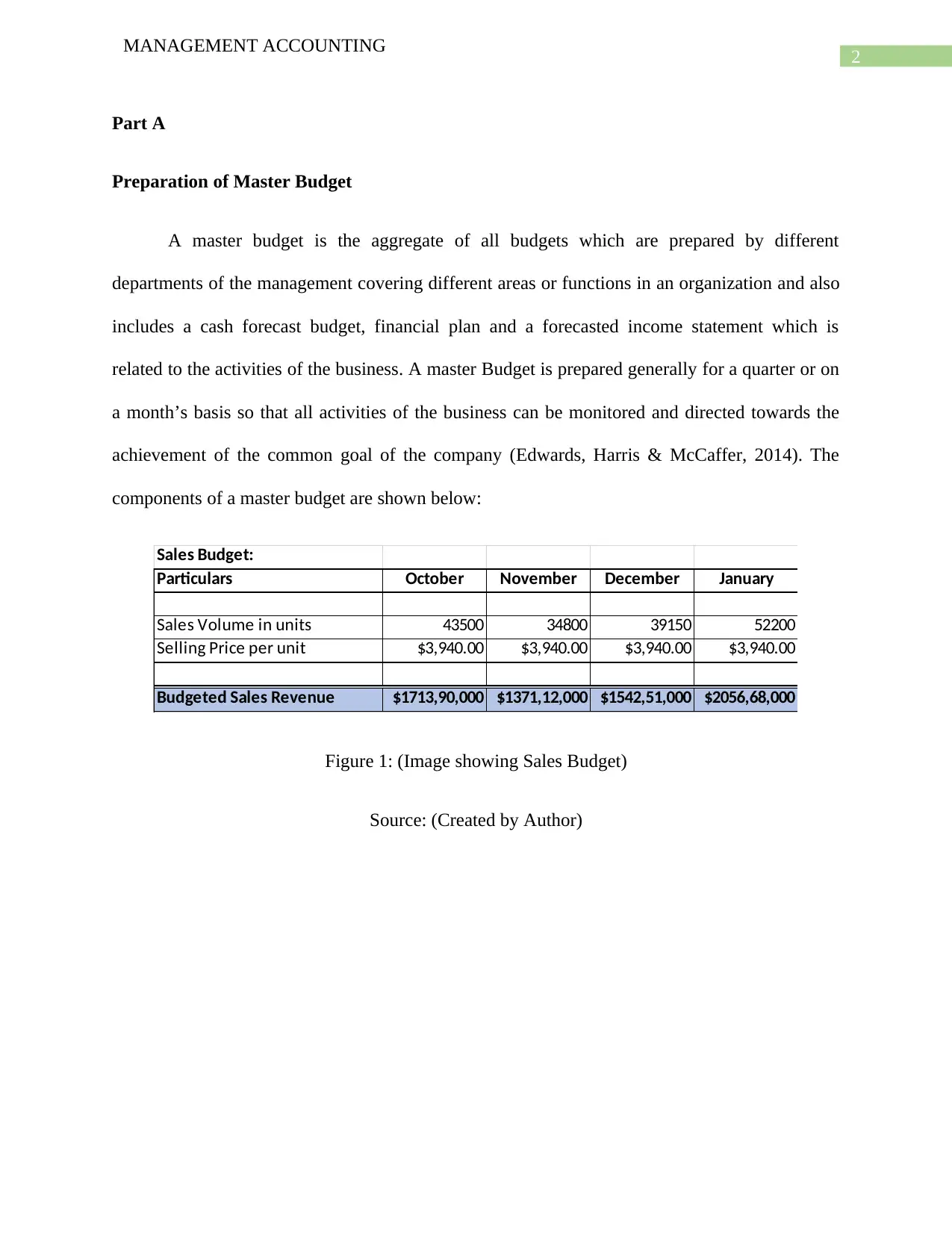

Production Budget:

Particulars October November December January

Sales Volume in units 43500 34800 39150 52200

Add: Closing Inventory of

Finished Goods 6960 7830 10440

50460 42630 49590

Less: Opening Inventory of

Finished Goods 27800 6960 7830

Budgeted Production Volume 22660 35670 41760

Figure 2: (Image showing Production Budget)

Source: (Created by Author)

Direct Labour Budget:

Particulars October November December

Budgeted Production Volume 22660 35670 41760

Labor Hours required per unit 5 5 5

Total Direct Labor Hour Required 113300 178350 208800

Direct Labor Cost per Hour $30.00 $30.00 $30.00

Budgeted Direct Labor Cost $33,99,000 $53,50,500 $62,64,000

Quarters

Figure 3: (Image showing Direct Labor Budget)

Source: (Created by Author)

MANAGEMENT ACCOUNTING

Production Budget:

Particulars October November December January

Sales Volume in units 43500 34800 39150 52200

Add: Closing Inventory of

Finished Goods 6960 7830 10440

50460 42630 49590

Less: Opening Inventory of

Finished Goods 27800 6960 7830

Budgeted Production Volume 22660 35670 41760

Figure 2: (Image showing Production Budget)

Source: (Created by Author)

Direct Labour Budget:

Particulars October November December

Budgeted Production Volume 22660 35670 41760

Labor Hours required per unit 5 5 5

Total Direct Labor Hour Required 113300 178350 208800

Direct Labor Cost per Hour $30.00 $30.00 $30.00

Budgeted Direct Labor Cost $33,99,000 $53,50,500 $62,64,000

Quarters

Figure 3: (Image showing Direct Labor Budget)

Source: (Created by Author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGEMENT ACCOUNTING

Purchase Budget:

Particulars October November December January

Budgeted Sales Volume 43500 34800 39150 52200

Budgeted Production Volume 22660 35670 41760

Sensors required per unit 3 3 3

Total Sensors Required 67980 107010 125280

Add: Closing Inventory of Sensors 62640 70470 93960

130620 177480 219240

Less: Opening Inventory of Sensors 78300 62640 70470

Budgeted Purchase Volume (in units) 52320 114840 148770

Sensors Cost per unit $52.00 $52.00 $52.00

Total Cost of Sensors $27,20,640 $59,71,680 $77,36,040

Gears required per unit 3 3 3 3

Total Gears Required 67980 107010 125280

Add: Closing Inventory of Gears 62640 70470 93960

130620 177480 219240

Less: Opening Inventory of Gears 78300 62640 70470

Budgeted Purchase Volume (in units) 52320 114840 148770

Gears Cost per unit $70.00 $70.00 $70.00

Total Cost of Gears $47,58,600 $74,90,700 $87,69,600

Budgeted Direct Material Purchase $74,79,240 $134,62,380 $165,05,640

Figure 4: (Image showing Purchase Budget)

Source: (Created by Author)

MANAGEMENT ACCOUNTING

Purchase Budget:

Particulars October November December January

Budgeted Sales Volume 43500 34800 39150 52200

Budgeted Production Volume 22660 35670 41760

Sensors required per unit 3 3 3

Total Sensors Required 67980 107010 125280

Add: Closing Inventory of Sensors 62640 70470 93960

130620 177480 219240

Less: Opening Inventory of Sensors 78300 62640 70470

Budgeted Purchase Volume (in units) 52320 114840 148770

Sensors Cost per unit $52.00 $52.00 $52.00

Total Cost of Sensors $27,20,640 $59,71,680 $77,36,040

Gears required per unit 3 3 3 3

Total Gears Required 67980 107010 125280

Add: Closing Inventory of Gears 62640 70470 93960

130620 177480 219240

Less: Opening Inventory of Gears 78300 62640 70470

Budgeted Purchase Volume (in units) 52320 114840 148770

Gears Cost per unit $70.00 $70.00 $70.00

Total Cost of Gears $47,58,600 $74,90,700 $87,69,600

Budgeted Direct Material Purchase $74,79,240 $134,62,380 $165,05,640

Figure 4: (Image showing Purchase Budget)

Source: (Created by Author)

5

MANAGEMENT ACCOUNTING

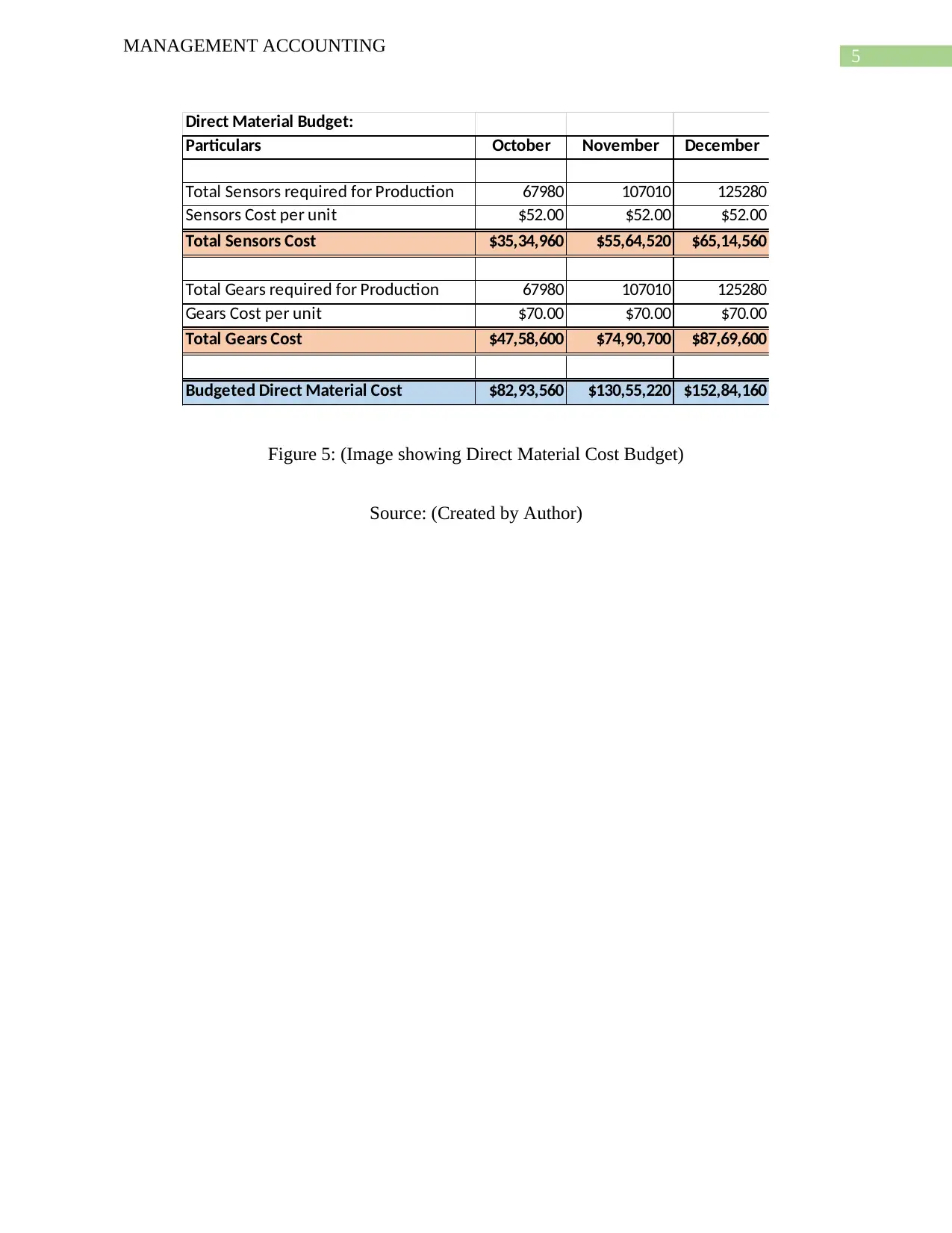

Direct Material Budget:

Particulars October November December

Total Sensors required for Production 67980 107010 125280

Sensors Cost per unit $52.00 $52.00 $52.00

Total Sensors Cost $35,34,960 $55,64,520 $65,14,560

Total Gears required for Production 67980 107010 125280

Gears Cost per unit $70.00 $70.00 $70.00

Total Gears Cost $47,58,600 $74,90,700 $87,69,600

Budgeted Direct Material Cost $82,93,560 $130,55,220 $152,84,160

Figure 5: (Image showing Direct Material Cost Budget)

Source: (Created by Author)

MANAGEMENT ACCOUNTING

Direct Material Budget:

Particulars October November December

Total Sensors required for Production 67980 107010 125280

Sensors Cost per unit $52.00 $52.00 $52.00

Total Sensors Cost $35,34,960 $55,64,520 $65,14,560

Total Gears required for Production 67980 107010 125280

Gears Cost per unit $70.00 $70.00 $70.00

Total Gears Cost $47,58,600 $74,90,700 $87,69,600

Budgeted Direct Material Cost $82,93,560 $130,55,220 $152,84,160

Figure 5: (Image showing Direct Material Cost Budget)

Source: (Created by Author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGEMENT ACCOUNTING

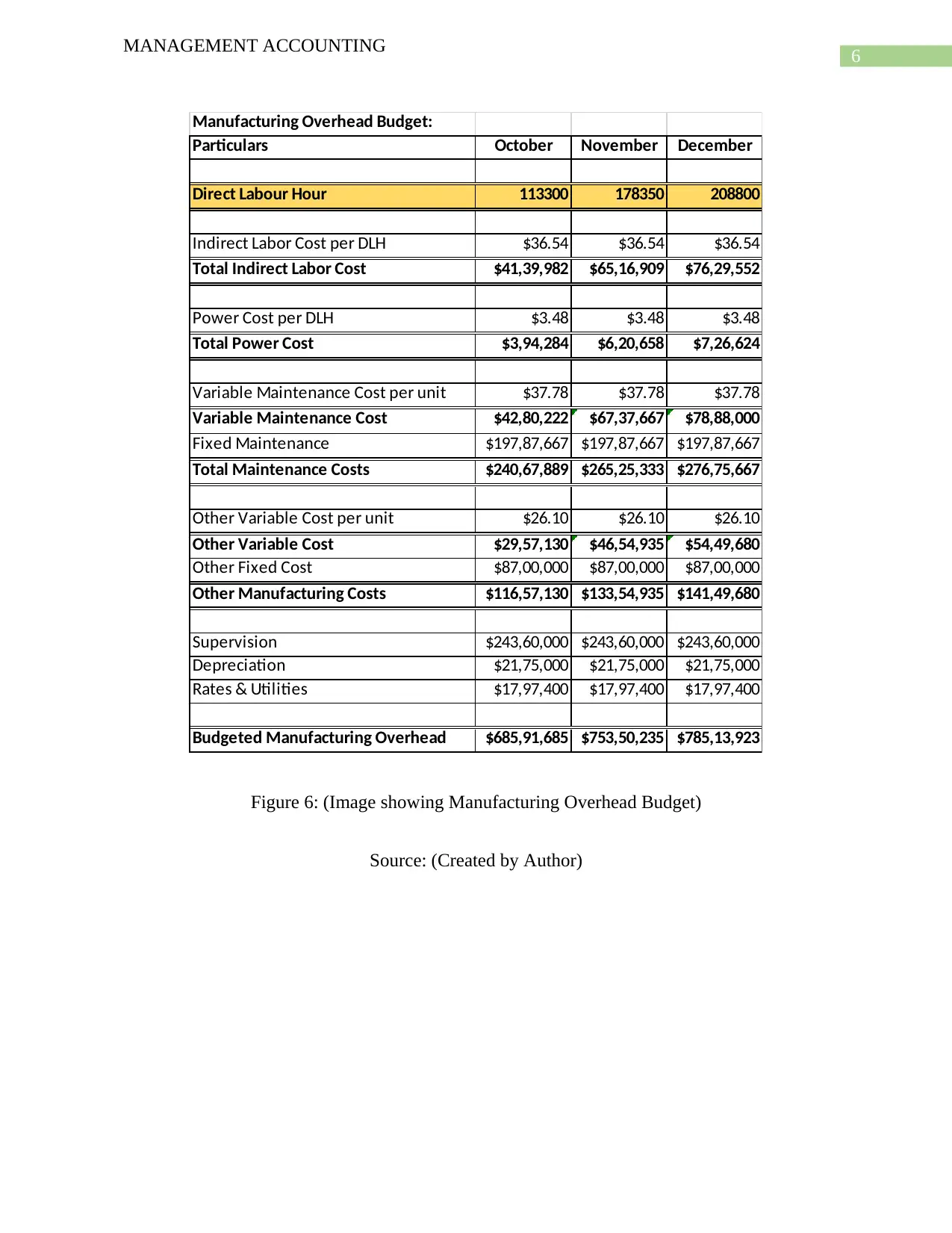

Manufacturing Overhead Budget:

Particulars October November December

Direct Labour Hour 113300 178350 208800

Indirect Labor Cost per DLH $36.54 $36.54 $36.54

Total Indirect Labor Cost $41,39,982 $65,16,909 $76,29,552

Power Cost per DLH $3.48 $3.48 $3.48

Total Power Cost $3,94,284 $6,20,658 $7,26,624

Variable Maintenance Cost per unit $37.78 $37.78 $37.78

Variable Maintenance Cost $42,80,222 $67,37,667 $78,88,000

Fixed Maintenance $197,87,667 $197,87,667 $197,87,667

Total Maintenance Costs $240,67,889 $265,25,333 $276,75,667

Other Variable Cost per unit $26.10 $26.10 $26.10

Other Variable Cost $29,57,130 $46,54,935 $54,49,680

Other Fixed Cost $87,00,000 $87,00,000 $87,00,000

Other Manufacturing Costs $116,57,130 $133,54,935 $141,49,680

Supervision $243,60,000 $243,60,000 $243,60,000

Depreciation $21,75,000 $21,75,000 $21,75,000

Rates & Utilities $17,97,400 $17,97,400 $17,97,400

Budgeted Manufacturing Overhead $685,91,685 $753,50,235 $785,13,923

Figure 6: (Image showing Manufacturing Overhead Budget)

Source: (Created by Author)

MANAGEMENT ACCOUNTING

Manufacturing Overhead Budget:

Particulars October November December

Direct Labour Hour 113300 178350 208800

Indirect Labor Cost per DLH $36.54 $36.54 $36.54

Total Indirect Labor Cost $41,39,982 $65,16,909 $76,29,552

Power Cost per DLH $3.48 $3.48 $3.48

Total Power Cost $3,94,284 $6,20,658 $7,26,624

Variable Maintenance Cost per unit $37.78 $37.78 $37.78

Variable Maintenance Cost $42,80,222 $67,37,667 $78,88,000

Fixed Maintenance $197,87,667 $197,87,667 $197,87,667

Total Maintenance Costs $240,67,889 $265,25,333 $276,75,667

Other Variable Cost per unit $26.10 $26.10 $26.10

Other Variable Cost $29,57,130 $46,54,935 $54,49,680

Other Fixed Cost $87,00,000 $87,00,000 $87,00,000

Other Manufacturing Costs $116,57,130 $133,54,935 $141,49,680

Supervision $243,60,000 $243,60,000 $243,60,000

Depreciation $21,75,000 $21,75,000 $21,75,000

Rates & Utilities $17,97,400 $17,97,400 $17,97,400

Budgeted Manufacturing Overhead $685,91,685 $753,50,235 $785,13,923

Figure 6: (Image showing Manufacturing Overhead Budget)

Source: (Created by Author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGEMENT ACCOUNTING

Cash Collection from Debtors:

Particulars October November December

Total Sales Revenue $1713,90,000 $1371,12,000 $1542,51,000

Collection in the month of Sales $685,56,000 $548,44,800 $617,00,400

Collection in the following month of

Sales $634,21,260 $994,06,200 $795,24,960

Total Collection from Debtors $1319,77,260 $1542,51,000 $1412,25,360

Figure 7: (Image showing Total Collection from Debtors)

Source: (Created by Author)

MANAGEMENT ACCOUNTING

Cash Collection from Debtors:

Particulars October November December

Total Sales Revenue $1713,90,000 $1371,12,000 $1542,51,000

Collection in the month of Sales $685,56,000 $548,44,800 $617,00,400

Collection in the following month of

Sales $634,21,260 $994,06,200 $795,24,960

Total Collection from Debtors $1319,77,260 $1542,51,000 $1412,25,360

Figure 7: (Image showing Total Collection from Debtors)

Source: (Created by Author)

8

MANAGEMENT ACCOUNTING

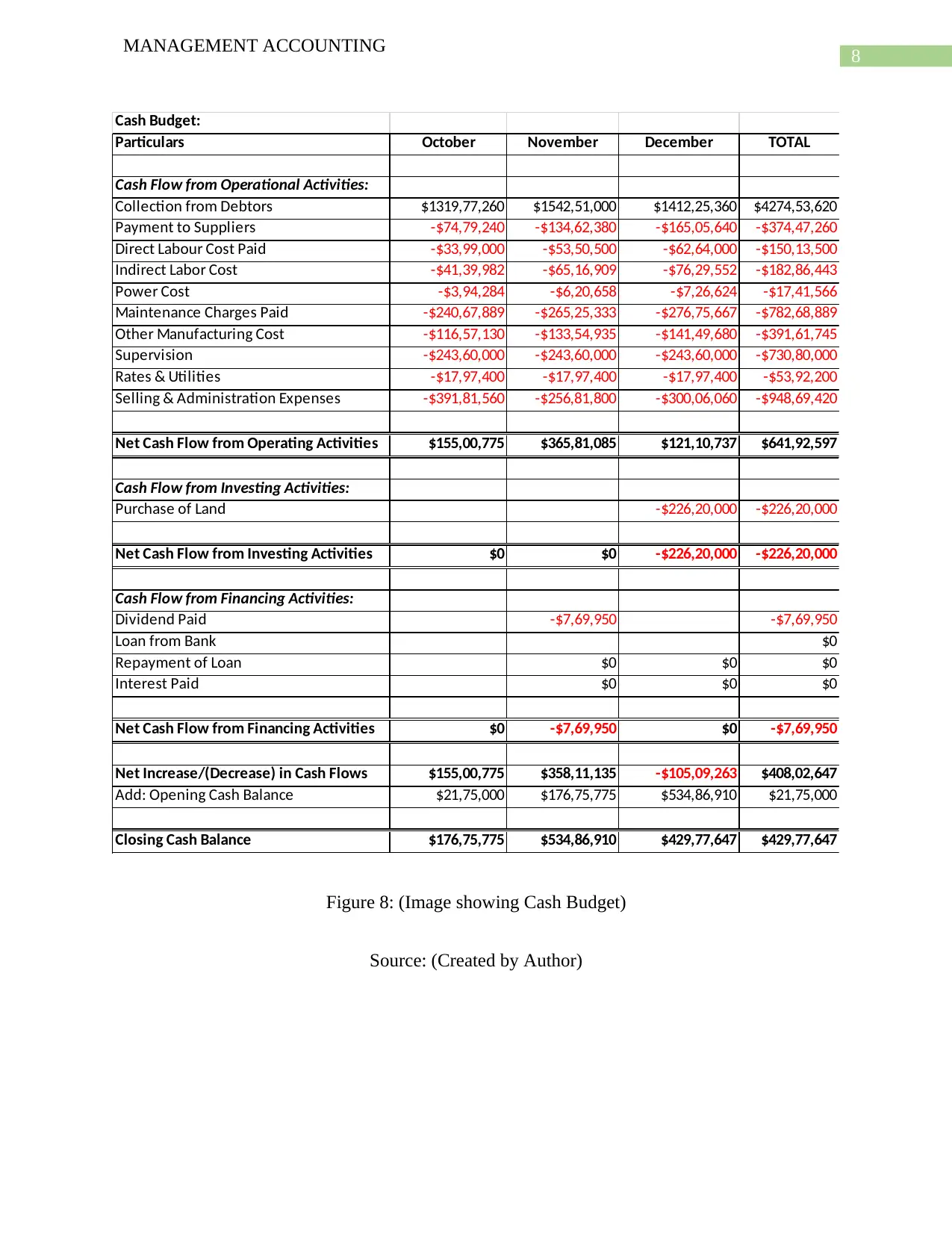

Cash Budget:

Particulars October November December TOTAL

Cash Flow from Operational Activities:

Collection from Debtors $1319,77,260 $1542,51,000 $1412,25,360 $4274,53,620

Payment to Suppliers -$74,79,240 -$134,62,380 -$165,05,640 -$374,47,260

Direct Labour Cost Paid -$33,99,000 -$53,50,500 -$62,64,000 -$150,13,500

Indirect Labor Cost -$41,39,982 -$65,16,909 -$76,29,552 -$182,86,443

Power Cost -$3,94,284 -$6,20,658 -$7,26,624 -$17,41,566

Maintenance Charges Paid -$240,67,889 -$265,25,333 -$276,75,667 -$782,68,889

Other Manufacturing Cost -$116,57,130 -$133,54,935 -$141,49,680 -$391,61,745

Supervision -$243,60,000 -$243,60,000 -$243,60,000 -$730,80,000

Rates & Utilities -$17,97,400 -$17,97,400 -$17,97,400 -$53,92,200

Selling & Administration Expenses -$391,81,560 -$256,81,800 -$300,06,060 -$948,69,420

Net Cash Flow from Operating Activities $155,00,775 $365,81,085 $121,10,737 $641,92,597

Cash Flow from Investing Activities:

Purchase of Land -$226,20,000 -$226,20,000

Net Cash Flow from Investing Activities $0 $0 -$226,20,000 -$226,20,000

Cash Flow from Financing Activities:

Dividend Paid -$7,69,950 -$7,69,950

Loan from Bank $0

Repayment of Loan $0 $0 $0

Interest Paid $0 $0 $0

Net Cash Flow from Financing Activities $0 -$7,69,950 $0 -$7,69,950

Net Increase/(Decrease) in Cash Flows $155,00,775 $358,11,135 -$105,09,263 $408,02,647

Add: Opening Cash Balance $21,75,000 $176,75,775 $534,86,910 $21,75,000

Closing Cash Balance $176,75,775 $534,86,910 $429,77,647 $429,77,647

Figure 8: (Image showing Cash Budget)

Source: (Created by Author)

MANAGEMENT ACCOUNTING

Cash Budget:

Particulars October November December TOTAL

Cash Flow from Operational Activities:

Collection from Debtors $1319,77,260 $1542,51,000 $1412,25,360 $4274,53,620

Payment to Suppliers -$74,79,240 -$134,62,380 -$165,05,640 -$374,47,260

Direct Labour Cost Paid -$33,99,000 -$53,50,500 -$62,64,000 -$150,13,500

Indirect Labor Cost -$41,39,982 -$65,16,909 -$76,29,552 -$182,86,443

Power Cost -$3,94,284 -$6,20,658 -$7,26,624 -$17,41,566

Maintenance Charges Paid -$240,67,889 -$265,25,333 -$276,75,667 -$782,68,889

Other Manufacturing Cost -$116,57,130 -$133,54,935 -$141,49,680 -$391,61,745

Supervision -$243,60,000 -$243,60,000 -$243,60,000 -$730,80,000

Rates & Utilities -$17,97,400 -$17,97,400 -$17,97,400 -$53,92,200

Selling & Administration Expenses -$391,81,560 -$256,81,800 -$300,06,060 -$948,69,420

Net Cash Flow from Operating Activities $155,00,775 $365,81,085 $121,10,737 $641,92,597

Cash Flow from Investing Activities:

Purchase of Land -$226,20,000 -$226,20,000

Net Cash Flow from Investing Activities $0 $0 -$226,20,000 -$226,20,000

Cash Flow from Financing Activities:

Dividend Paid -$7,69,950 -$7,69,950

Loan from Bank $0

Repayment of Loan $0 $0 $0

Interest Paid $0 $0 $0

Net Cash Flow from Financing Activities $0 -$7,69,950 $0 -$7,69,950

Net Increase/(Decrease) in Cash Flows $155,00,775 $358,11,135 -$105,09,263 $408,02,647

Add: Opening Cash Balance $21,75,000 $176,75,775 $534,86,910 $21,75,000

Closing Cash Balance $176,75,775 $534,86,910 $429,77,647 $429,77,647

Figure 8: (Image showing Cash Budget)

Source: (Created by Author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGEMENT ACCOUNTING

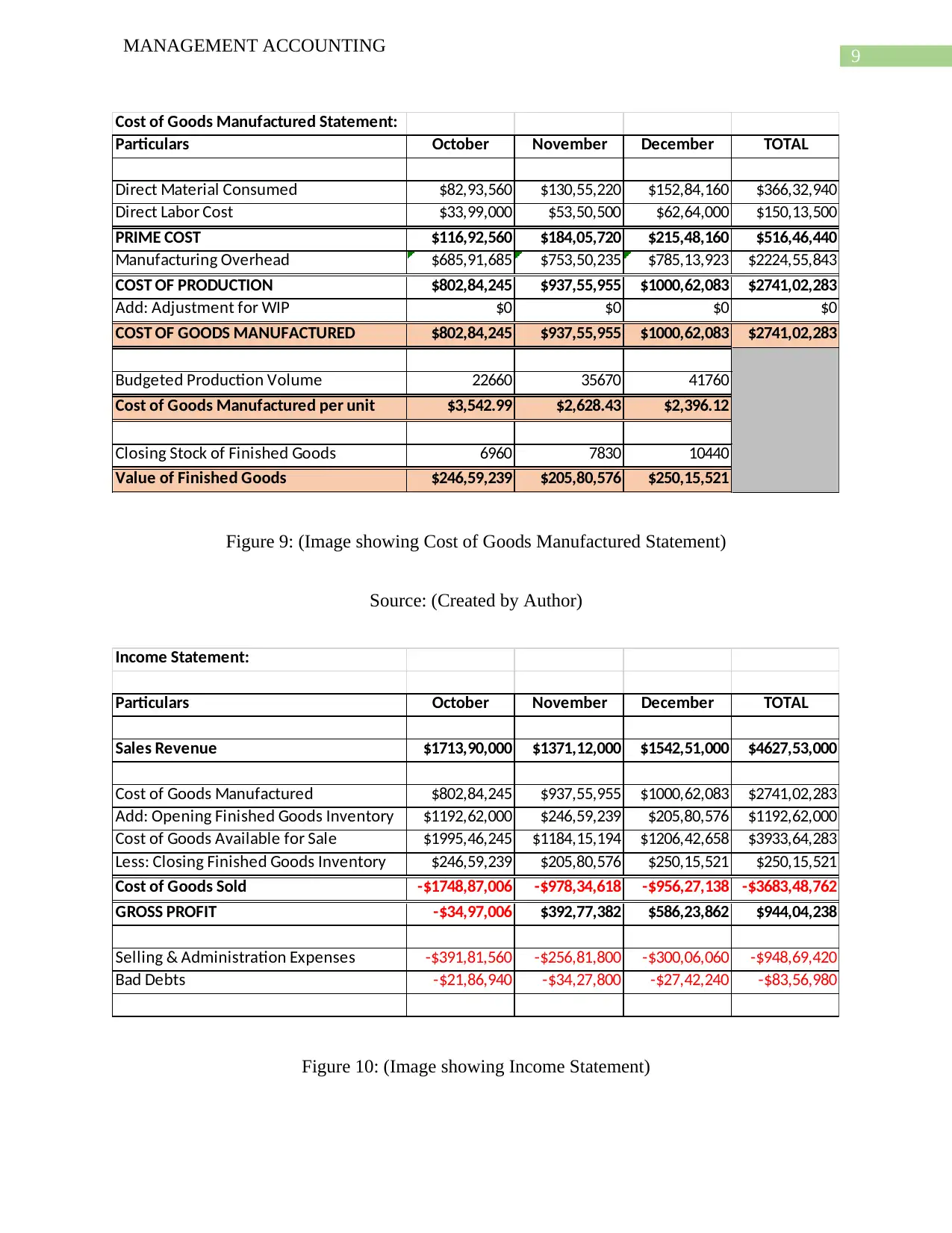

Cost of Goods Manufactured Statement:

Particulars October November December TOTAL

Direct Material Consumed $82,93,560 $130,55,220 $152,84,160 $366,32,940

Direct Labor Cost $33,99,000 $53,50,500 $62,64,000 $150,13,500

PRIME COST $116,92,560 $184,05,720 $215,48,160 $516,46,440

Manufacturing Overhead $685,91,685 $753,50,235 $785,13,923 $2224,55,843

COST OF PRODUCTION $802,84,245 $937,55,955 $1000,62,083 $2741,02,283

Add: Adjustment for WIP $0 $0 $0 $0

COST OF GOODS MANUFACTURED $802,84,245 $937,55,955 $1000,62,083 $2741,02,283

Budgeted Production Volume 22660 35670 41760

Cost of Goods Manufactured per unit $3,542.99 $2,628.43 $2,396.12

Closing Stock of Finished Goods 6960 7830 10440

Value of Finished Goods $246,59,239 $205,80,576 $250,15,521

Figure 9: (Image showing Cost of Goods Manufactured Statement)

Source: (Created by Author)

Income Statement:

Particulars October November December TOTAL

Sales Revenue $1713,90,000 $1371,12,000 $1542,51,000 $4627,53,000

Cost of Goods Manufactured $802,84,245 $937,55,955 $1000,62,083 $2741,02,283

Add: Opening Finished Goods Inventory $1192,62,000 $246,59,239 $205,80,576 $1192,62,000

Cost of Goods Available for Sale $1995,46,245 $1184,15,194 $1206,42,658 $3933,64,283

Less: Closing Finished Goods Inventory $246,59,239 $205,80,576 $250,15,521 $250,15,521

Cost of Goods Sold -$1748,87,006 -$978,34,618 -$956,27,138 -$3683,48,762

GROSS PROFIT -$34,97,006 $392,77,382 $586,23,862 $944,04,238

Selling & Administration Expenses -$391,81,560 -$256,81,800 -$300,06,060 -$948,69,420

Bad Debts -$21,86,940 -$34,27,800 -$27,42,240 -$83,56,980

Figure 10: (Image showing Income Statement)

MANAGEMENT ACCOUNTING

Cost of Goods Manufactured Statement:

Particulars October November December TOTAL

Direct Material Consumed $82,93,560 $130,55,220 $152,84,160 $366,32,940

Direct Labor Cost $33,99,000 $53,50,500 $62,64,000 $150,13,500

PRIME COST $116,92,560 $184,05,720 $215,48,160 $516,46,440

Manufacturing Overhead $685,91,685 $753,50,235 $785,13,923 $2224,55,843

COST OF PRODUCTION $802,84,245 $937,55,955 $1000,62,083 $2741,02,283

Add: Adjustment for WIP $0 $0 $0 $0

COST OF GOODS MANUFACTURED $802,84,245 $937,55,955 $1000,62,083 $2741,02,283

Budgeted Production Volume 22660 35670 41760

Cost of Goods Manufactured per unit $3,542.99 $2,628.43 $2,396.12

Closing Stock of Finished Goods 6960 7830 10440

Value of Finished Goods $246,59,239 $205,80,576 $250,15,521

Figure 9: (Image showing Cost of Goods Manufactured Statement)

Source: (Created by Author)

Income Statement:

Particulars October November December TOTAL

Sales Revenue $1713,90,000 $1371,12,000 $1542,51,000 $4627,53,000

Cost of Goods Manufactured $802,84,245 $937,55,955 $1000,62,083 $2741,02,283

Add: Opening Finished Goods Inventory $1192,62,000 $246,59,239 $205,80,576 $1192,62,000

Cost of Goods Available for Sale $1995,46,245 $1184,15,194 $1206,42,658 $3933,64,283

Less: Closing Finished Goods Inventory $246,59,239 $205,80,576 $250,15,521 $250,15,521

Cost of Goods Sold -$1748,87,006 -$978,34,618 -$956,27,138 -$3683,48,762

GROSS PROFIT -$34,97,006 $392,77,382 $586,23,862 $944,04,238

Selling & Administration Expenses -$391,81,560 -$256,81,800 -$300,06,060 -$948,69,420

Bad Debts -$21,86,940 -$34,27,800 -$27,42,240 -$83,56,980

Figure 10: (Image showing Income Statement)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGEMENT ACCOUNTING

Source: (Created by Author)

Part B

Investment Decision

As per the situation which is given in the question, the production manager of the

company has made the decision to undertake an investment which will benefit the business and

improve the overall production capacity of the business. The new manufacturing policy which is

adopted by the business will be ensuring that the business is able maximize the production

process and thereby increasing the revenue of the business.

For the purpose of judging the effectiveness of the manufacturing plan which is intended

by the management various forecasting and planning is done with the help of using Budgeting

tool. The various budgets which are prepared by the management of the company are sales,

budget, purchase budget, production budget, direct labor, direct material budget, cash budget and

income statement. The Sales budget which is prepared by the company shows that the sales

volume of the company decreases from the estimates of month of October as shown in the month

of November and December which is 34800 units and 39150 units. The overall sales of the

company which is estimated in the budget for the month of January is shown to be $ 2056,68,000

which is significantly higher than the sales which is estimated to be achieved in the month of

December which is $ 1542,51,000. This shows that the company is expecting increase in the

sales of the company in the month of January. The production budget reveals that the anticipated

volume of production is expected to be highest in the month of January which is shown to be

52200 units. The budgeted production volume from the month of October shows an increasing

trend which means that the business is anticipating growth. The direct labor budget shows that

MANAGEMENT ACCOUNTING

Source: (Created by Author)

Part B

Investment Decision

As per the situation which is given in the question, the production manager of the

company has made the decision to undertake an investment which will benefit the business and

improve the overall production capacity of the business. The new manufacturing policy which is

adopted by the business will be ensuring that the business is able maximize the production

process and thereby increasing the revenue of the business.

For the purpose of judging the effectiveness of the manufacturing plan which is intended

by the management various forecasting and planning is done with the help of using Budgeting

tool. The various budgets which are prepared by the management of the company are sales,

budget, purchase budget, production budget, direct labor, direct material budget, cash budget and

income statement. The Sales budget which is prepared by the company shows that the sales

volume of the company decreases from the estimates of month of October as shown in the month

of November and December which is 34800 units and 39150 units. The overall sales of the

company which is estimated in the budget for the month of January is shown to be $ 2056,68,000

which is significantly higher than the sales which is estimated to be achieved in the month of

December which is $ 1542,51,000. This shows that the company is expecting increase in the

sales of the company in the month of January. The production budget reveals that the anticipated

volume of production is expected to be highest in the month of January which is shown to be

52200 units. The budgeted production volume from the month of October shows an increasing

trend which means that the business is anticipating growth. The direct labor budget shows that

11

MANAGEMENT ACCOUNTING

the anticipated labor cost is also expected to rise as the labor is increasing keeping the rate

charged by the labor constant. As the production level of the company increases it is natural that

the level of variable costs which includes labor cost will also be increasing. The budgeted labor

cost is anticipated to be $ 62,654,000 as shown in figure 3 above. As the budgeted Sales Volume

is known from the sales budget and the expected production level is also known the management

needs to know how much material needs to be purchased for keeping the estimates of sales and

production budget intact. The budgeted direct material purchased for the month of December

shows a significant rise of more than $ 3,0000. The direct material which is needed to be

purchased is of the value of $ 165,05,640. The manufacturing overhead which is prepared shows

the various indirect expenses which are undertaken by the management of the company which

needs to be estimated. The budget shows both indirect costs of variable and fixed nature. The

budgeted manufacturing overhead for the month of December is shown to be $ 785,13,923. The

cash budgets show the various expenses which the management expects they will be incurring

during the quarter (Almaree et al., 2015). The cash from operating activities shows positive

results for all months which suggest that the management believes in the operation strength of

the business. The closing cash balance for the month of December shows that the business

anticipated a cash balance of $ 429,77,647. The income statement shows loss when the aggregate

profit for all the months are considered.

Thus, from the above analysis it is clearly shown in the income statement which

anticipates the income and expenses of the business that the business will be earning losses in

aggregate therefore the management should not undertake the production plan.

MANAGEMENT ACCOUNTING

the anticipated labor cost is also expected to rise as the labor is increasing keeping the rate

charged by the labor constant. As the production level of the company increases it is natural that

the level of variable costs which includes labor cost will also be increasing. The budgeted labor

cost is anticipated to be $ 62,654,000 as shown in figure 3 above. As the budgeted Sales Volume

is known from the sales budget and the expected production level is also known the management

needs to know how much material needs to be purchased for keeping the estimates of sales and

production budget intact. The budgeted direct material purchased for the month of December

shows a significant rise of more than $ 3,0000. The direct material which is needed to be

purchased is of the value of $ 165,05,640. The manufacturing overhead which is prepared shows

the various indirect expenses which are undertaken by the management of the company which

needs to be estimated. The budget shows both indirect costs of variable and fixed nature. The

budgeted manufacturing overhead for the month of December is shown to be $ 785,13,923. The

cash budgets show the various expenses which the management expects they will be incurring

during the quarter (Almaree et al., 2015). The cash from operating activities shows positive

results for all months which suggest that the management believes in the operation strength of

the business. The closing cash balance for the month of December shows that the business

anticipated a cash balance of $ 429,77,647. The income statement shows loss when the aggregate

profit for all the months are considered.

Thus, from the above analysis it is clearly shown in the income statement which

anticipates the income and expenses of the business that the business will be earning losses in

aggregate therefore the management should not undertake the production plan.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.