Management Accounting: Systems, Budgeting, and Financial Analysis

VerifiedAdded on 2024/07/01

|20

|4628

|144

Report

AI Summary

This report provides a comprehensive analysis of management accounting, highlighting its role in business decision-making and contrasting it with financial accounting. It explores various management accounting systems, including inventory management, job costing, price optimization, and cost accounting, detailing their advantages. The report includes a quantitative analysis of desired sales levels and break-even points, applying these concepts to a scenario involving All-Ace Ltd. Furthermore, it discusses different types of budgets, such as static and flexible budgets, weighing their pros and cons. The report concludes by examining how an organization adapts management accounting information to address financial challenges, offering insights into effective financial management and strategic planning.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction:.................................................................................................................................... 3

Section1:.......................................................................................................................................... 4

Question1:....................................................................................................................................4

a): Management accounting and its role in business:..................................................................4

b): Difference among Financial accounting and management accounting:.................................6

C: Different management accounting system and advantages:...................................................8

Question 2:.................................................................................................................................10

a): the Desired level of sales...................................................................................................... 10

b): Break-even point.................................................................................................................11

Section 2........................................................................................................................................12

Question 3:.................................................................................................................................12

A: different budgets with pros and cons....................................................................................12

B: Explain the importance of preparing budgets for those managers who think it is pointless.15

Question 4:.................................................................................................................................16

Using the Scenario compare how the organization is adapting the management accounting

information to respond the financial problem........................................................................... 16

Conclusion:.................................................................................................................................... 18

References:.................................................................................................................................... 19

2

Introduction:.................................................................................................................................... 3

Section1:.......................................................................................................................................... 4

Question1:....................................................................................................................................4

a): Management accounting and its role in business:..................................................................4

b): Difference among Financial accounting and management accounting:.................................6

C: Different management accounting system and advantages:...................................................8

Question 2:.................................................................................................................................10

a): the Desired level of sales...................................................................................................... 10

b): Break-even point.................................................................................................................11

Section 2........................................................................................................................................12

Question 3:.................................................................................................................................12

A: different budgets with pros and cons....................................................................................12

B: Explain the importance of preparing budgets for those managers who think it is pointless.15

Question 4:.................................................................................................................................16

Using the Scenario compare how the organization is adapting the management accounting

information to respond the financial problem........................................................................... 16

Conclusion:.................................................................................................................................... 18

References:.................................................................................................................................... 19

2

Introduction:

Management accounting system is the first choice of every business manager due to its

intelligent beneficial specialities for business and this report is based on the management

accounting and, describes the character of this system for a business. A comparative view of

management accounting and financial accounting will be described in this report so that user can

understand that management accounting is ample differ from financial bookkeeping. Sub-

systems of management accounting system along with usefulness will be explained in this report.

A part of the report is based on All-Ace Ltd which is thinking about the proposals provided by

the company managers and appropriate solution will be provided in the report after all analysis.

Section B of this report is dedicated to the budgetary control techniques and different budgets

along with their merits and comparative view of LIFO and FIFO will be explained.

3

Management accounting system is the first choice of every business manager due to its

intelligent beneficial specialities for business and this report is based on the management

accounting and, describes the character of this system for a business. A comparative view of

management accounting and financial accounting will be described in this report so that user can

understand that management accounting is ample differ from financial bookkeeping. Sub-

systems of management accounting system along with usefulness will be explained in this report.

A part of the report is based on All-Ace Ltd which is thinking about the proposals provided by

the company managers and appropriate solution will be provided in the report after all analysis.

Section B of this report is dedicated to the budgetary control techniques and different budgets

along with their merits and comparative view of LIFO and FIFO will be explained.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Section1:

Question1:

Introduction:

This assignment is based on management accounting and its tools and will be made to provide

information to the Finance manager of Wentworth company about the suitability of management

accounting practices and how it is different from financial accounting so that he can take a

decision about the adoption of management system in the organization.

a): Management accounting and its role in business:

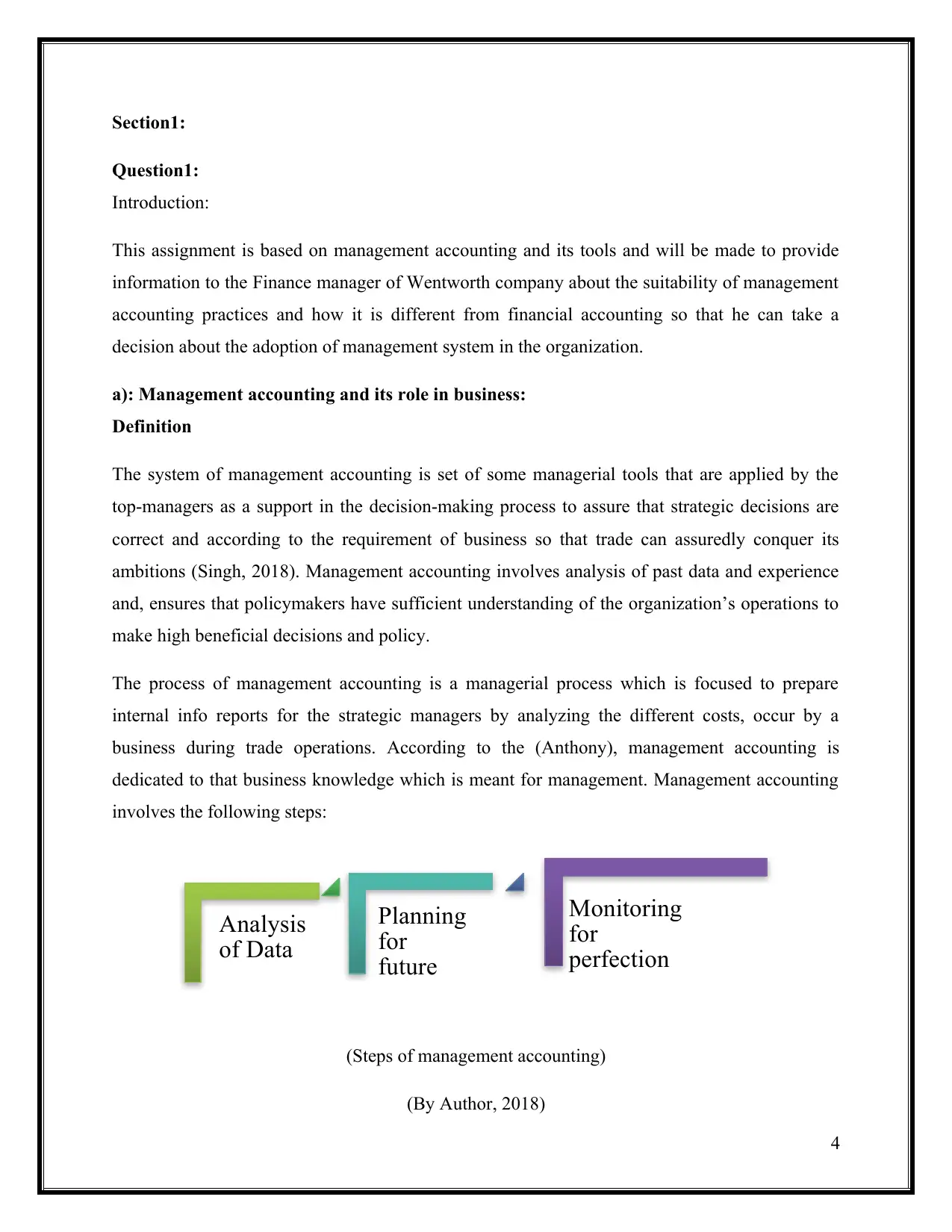

Definition

The system of management accounting is set of some managerial tools that are applied by the

top-managers as a support in the decision-making process to assure that strategic decisions are

correct and according to the requirement of business so that trade can assuredly conquer its

ambitions (Singh, 2018). Management accounting involves analysis of past data and experience

and, ensures that policymakers have sufficient understanding of the organization’s operations to

make high beneficial decisions and policy.

The process of management accounting is a managerial process which is focused to prepare

internal info reports for the strategic managers by analyzing the different costs, occur by a

business during trade operations. According to the (Anthony), management accounting is

dedicated to that business knowledge which is meant for management. Management accounting

involves the following steps:

(Steps of management accounting)

(By Author, 2018)

4

Analysis

of Data

Planning

for

future

Monitoring

for

perfection

Question1:

Introduction:

This assignment is based on management accounting and its tools and will be made to provide

information to the Finance manager of Wentworth company about the suitability of management

accounting practices and how it is different from financial accounting so that he can take a

decision about the adoption of management system in the organization.

a): Management accounting and its role in business:

Definition

The system of management accounting is set of some managerial tools that are applied by the

top-managers as a support in the decision-making process to assure that strategic decisions are

correct and according to the requirement of business so that trade can assuredly conquer its

ambitions (Singh, 2018). Management accounting involves analysis of past data and experience

and, ensures that policymakers have sufficient understanding of the organization’s operations to

make high beneficial decisions and policy.

The process of management accounting is a managerial process which is focused to prepare

internal info reports for the strategic managers by analyzing the different costs, occur by a

business during trade operations. According to the (Anthony), management accounting is

dedicated to that business knowledge which is meant for management. Management accounting

involves the following steps:

(Steps of management accounting)

(By Author, 2018)

4

Analysis

of Data

Planning

for

future

Monitoring

for

perfection

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting is not limited to analysis and reporting of financial and non-financial

data, but it works being associated with every process of business and ensures that every activity

will be performed in a planned and beneficial manner (Singh, 2018). Use of management

practices reliefs the business bosses to detect the weak segments and works on it for

enhancement. Role of Practices and tools of management accounting for a business are classified

as below:

Timely availability of information:

Management accounting produces certain types of reports related to the monetary and non-

financial terms of business and avails timely information to managers according to their

necessities to certify the individuality of the solution. By providing such need-based information,

it helps to make a comparison between different factors which is essential for a trade like,

comparison report of sales and demand to investigate the reasons of insufficient supply.

Finance management: Management accounting involves analysis of historical data to find the

existing financial condition and predict the future financial needs of the business so that proper

funding for each business activity can be provided (Singh, 2018). For example, if the marketing

activities of Wentworth required extra funding during the med of year, the company can reduce

expenses of other activity and allocate this fund to the marketing department.

Enables coordination:

In large organizations, various departments work together and coordination among these

departments is essential to play the business operations comfortably. Management accounting

provides useful information which is used to make planning and ensures proper flow of

information so that very division can work according to the vision strategy of the business.

Forecast of forthcoming: Due to the uncertainty of business activities, there is always a possible

threat of adverse market change and for the same, management accounting helps to manage this

threat by providing proper analyzed information to support the future prediction (Leung, 2016).

By the application of management practices, Wentworth can identify and improve its capability

to face possible negative market changes.

5

data, but it works being associated with every process of business and ensures that every activity

will be performed in a planned and beneficial manner (Singh, 2018). Use of management

practices reliefs the business bosses to detect the weak segments and works on it for

enhancement. Role of Practices and tools of management accounting for a business are classified

as below:

Timely availability of information:

Management accounting produces certain types of reports related to the monetary and non-

financial terms of business and avails timely information to managers according to their

necessities to certify the individuality of the solution. By providing such need-based information,

it helps to make a comparison between different factors which is essential for a trade like,

comparison report of sales and demand to investigate the reasons of insufficient supply.

Finance management: Management accounting involves analysis of historical data to find the

existing financial condition and predict the future financial needs of the business so that proper

funding for each business activity can be provided (Singh, 2018). For example, if the marketing

activities of Wentworth required extra funding during the med of year, the company can reduce

expenses of other activity and allocate this fund to the marketing department.

Enables coordination:

In large organizations, various departments work together and coordination among these

departments is essential to play the business operations comfortably. Management accounting

provides useful information which is used to make planning and ensures proper flow of

information so that very division can work according to the vision strategy of the business.

Forecast of forthcoming: Due to the uncertainty of business activities, there is always a possible

threat of adverse market change and for the same, management accounting helps to manage this

threat by providing proper analyzed information to support the future prediction (Leung, 2016).

By the application of management practices, Wentworth can identify and improve its capability

to face possible negative market changes.

5

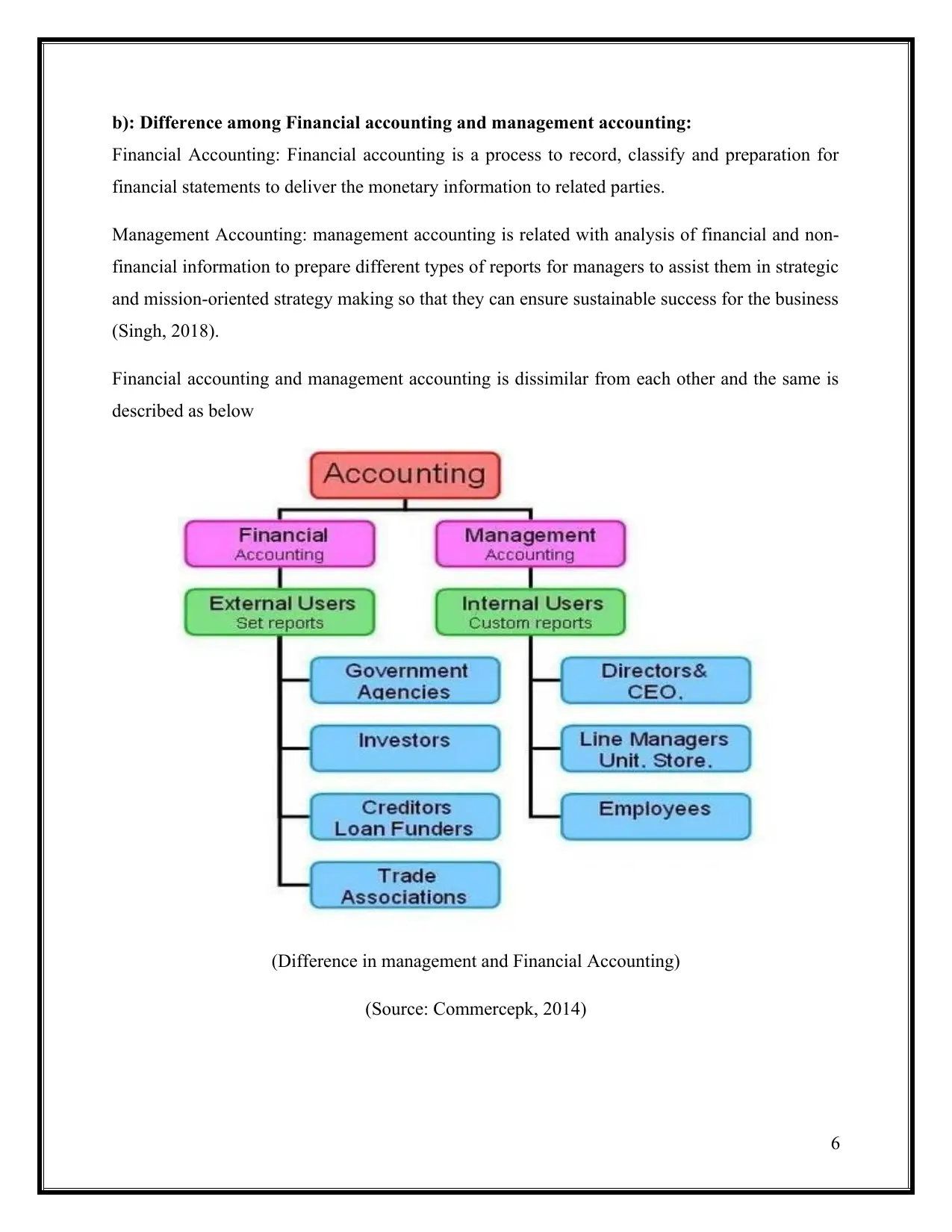

b): Difference among Financial accounting and management accounting:

Financial Accounting: Financial accounting is a process to record, classify and preparation for

financial statements to deliver the monetary information to related parties.

Management Accounting: management accounting is related with analysis of financial and non-

financial information to prepare different types of reports for managers to assist them in strategic

and mission-oriented strategy making so that they can ensure sustainable success for the business

(Singh, 2018).

Financial accounting and management accounting is dissimilar from each other and the same is

described as below

(Difference in management and Financial Accounting)

(Source: Commercepk, 2014)

6

Financial Accounting: Financial accounting is a process to record, classify and preparation for

financial statements to deliver the monetary information to related parties.

Management Accounting: management accounting is related with analysis of financial and non-

financial information to prepare different types of reports for managers to assist them in strategic

and mission-oriented strategy making so that they can ensure sustainable success for the business

(Singh, 2018).

Financial accounting and management accounting is dissimilar from each other and the same is

described as below

(Difference in management and Financial Accounting)

(Source: Commercepk, 2014)

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

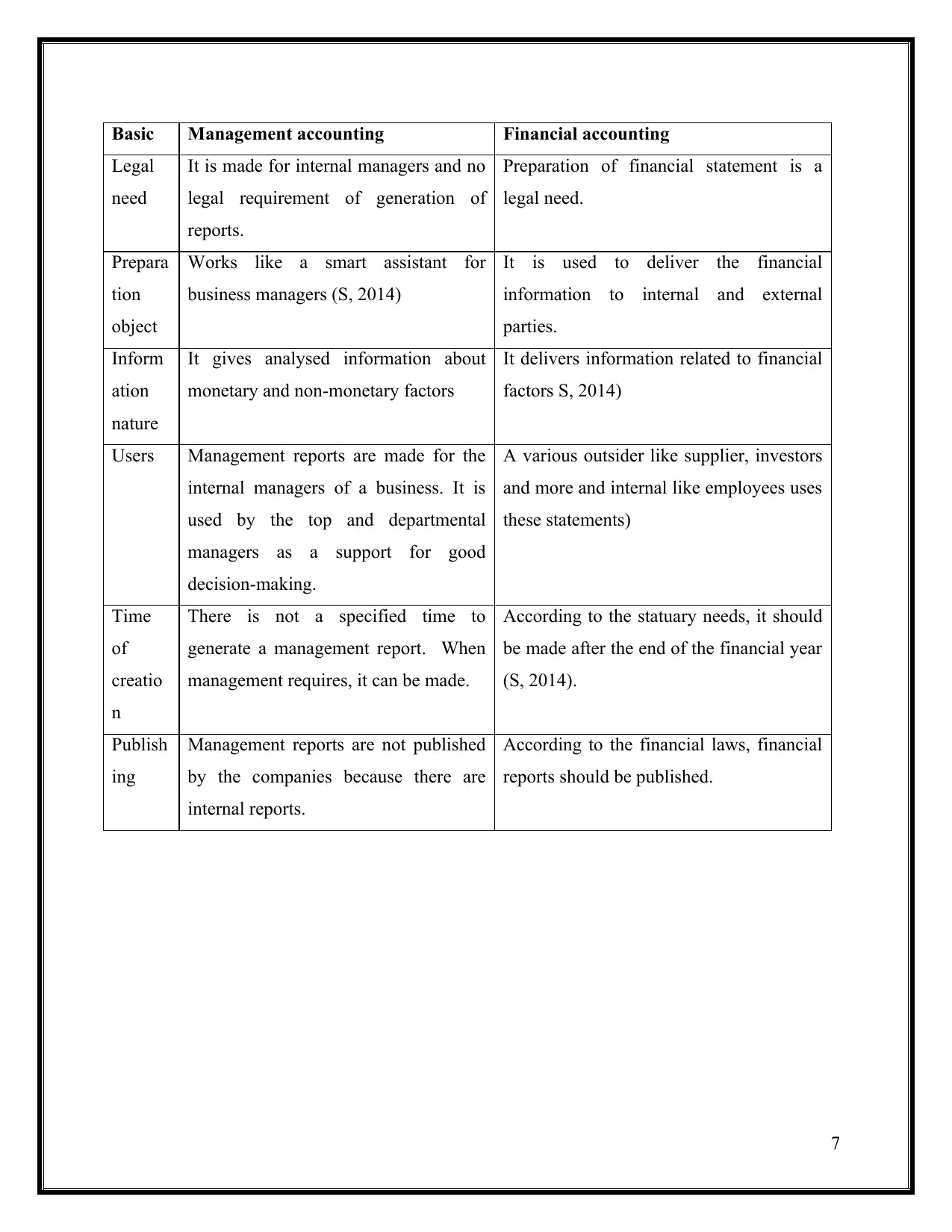

Basic Management accounting Financial accounting

Legal

need

It is made for internal managers and no

legal requirement of generation of

reports.

Preparation of financial statement is a

legal need.

Prepara

tion

object

Works like a smart assistant for

business managers (S, 2014)

It is used to deliver the financial

information to internal and external

parties.

Inform

ation

nature

It gives analysed information about

monetary and non-monetary factors

It delivers information related to financial

factors S, 2014)

Users Management reports are made for the

internal managers of a business. It is

used by the top and departmental

managers as a support for good

decision-making.

A various outsider like supplier, investors

and more and internal like employees uses

these statements)

Time

of

creatio

n

There is not a specified time to

generate a management report. When

management requires, it can be made.

According to the statuary needs, it should

be made after the end of the financial year

(S, 2014).

Publish

ing

Management reports are not published

by the companies because there are

internal reports.

According to the financial laws, financial

reports should be published.

Basic Management accounting Financial accounting

Legal

need

It is made for internal managers and no

legal requirement of generation of

reports.

Preparation of financial statement is a

legal need.

Prepara

tion

object

Works like a smart assistant for

business managers (S, 2014)

It is used to deliver the financial

information to internal and external

parties.

Inform

ation

nature

It gives analysed information about

monetary and non-monetary factors

It delivers information related to financial

factors S, 2014)

Users Management reports are made for the

internal managers of a business. It is

used by the top and departmental

managers as a support for good

decision-making.

A various outsider like supplier, investors

and more and internal like employees uses

these statements)

Time

of

creatio

n

There is not a specified time to

generate a management report. When

management requires, it can be made.

According to the statuary needs, it should

be made after the end of the financial year

(S, 2014).

Publish

ing

Management reports are not published

by the companies because there are

internal reports.

According to the financial laws, financial

reports should be published.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

C: Different management accounting system and advantages:

Management accounting involves several types of tools which can be utilized by the managers of

a Wentworth company to manage the altered commercial events in correct tactic. Some different

systems of management accounting are classified as below:

Inventory management system:

As a system to manage the stock and inventory items, IMS is a useful tool for the mangers of

Wentworth for the administration and regulation of inventory raw and finished goods. In modern

business, IMS stands for an integrated system which helps to accomplish the target of least

gathering and stowing cost by preserving the opposite level of underdone stuff (Leung, 2016). It

generates the following advantages of a business:

To maintain the required level of raw items it is essential.

It helps to control the cost of the order and receiving and minimize the storage (Leung,

2016).

It saves time and money for the business because no extra effort is required

Job costing system:

Mostly job costing is unlisted by those manufacturing companies which are engaged in the

production work on the basis of special batches or jobs or producing unique products like

machinery for a special purpose (Lodha, 2018). This system identifies the cost of each batch and

helps to allocate it separately so that cost of different products or group can be managed as per

requirements. Some benefits of job costing system are as below:

It is necessary for order based production units.

The absorption structure of cost according to the quality of batch identified easily.

Profitability accounting for each process can be made to identify and remove the motive of

abnormal cost.

Price optimization system:

Package inspects the react of buyer towards the purchase of the product at different matched of

prices and denotes an optimal price level where sales and profit will be superlative (Spacey,

8

Management accounting involves several types of tools which can be utilized by the managers of

a Wentworth company to manage the altered commercial events in correct tactic. Some different

systems of management accounting are classified as below:

Inventory management system:

As a system to manage the stock and inventory items, IMS is a useful tool for the mangers of

Wentworth for the administration and regulation of inventory raw and finished goods. In modern

business, IMS stands for an integrated system which helps to accomplish the target of least

gathering and stowing cost by preserving the opposite level of underdone stuff (Leung, 2016). It

generates the following advantages of a business:

To maintain the required level of raw items it is essential.

It helps to control the cost of the order and receiving and minimize the storage (Leung,

2016).

It saves time and money for the business because no extra effort is required

Job costing system:

Mostly job costing is unlisted by those manufacturing companies which are engaged in the

production work on the basis of special batches or jobs or producing unique products like

machinery for a special purpose (Lodha, 2018). This system identifies the cost of each batch and

helps to allocate it separately so that cost of different products or group can be managed as per

requirements. Some benefits of job costing system are as below:

It is necessary for order based production units.

The absorption structure of cost according to the quality of batch identified easily.

Profitability accounting for each process can be made to identify and remove the motive of

abnormal cost.

Price optimization system:

Package inspects the react of buyer towards the purchase of the product at different matched of

prices and denotes an optimal price level where sales and profit will be superlative (Spacey,

8

2017). POS is presented to set the optimal design of prices of products which will be acceptable

for a maximal number of clients for buy and, organization will be gain budgeted profit. Some

edges of price optimization areas down:

Wentworth can use it to make market-based sales strategy to be going concern and gainful.

Price optimization finds reasonable price according to the behaviour of clients and sets

majorly accepted price of the product for sales maximization (Spacey, 2017).

To attain Break-even and economics of scale, it is an essential tool.

Cost accounting system:

Cost accounting system is a way to determine and control the costs absorbed by the different

production and administration processes so that business can attain its target of profit superlative

(Lodha, 2018). It covers recording, classification, and control of those abnormal costs which are

increasing the cost of the final product and controllable through the better management of

activities. Some benefits of cost accounting system;

The system can be applied by Wentworth to be cost-effective and profitable (Lodha, 2018).

Absorption of each cost factor can be an exam on the table of appropriateness.

9

for a maximal number of clients for buy and, organization will be gain budgeted profit. Some

edges of price optimization areas down:

Wentworth can use it to make market-based sales strategy to be going concern and gainful.

Price optimization finds reasonable price according to the behaviour of clients and sets

majorly accepted price of the product for sales maximization (Spacey, 2017).

To attain Break-even and economics of scale, it is an essential tool.

Cost accounting system:

Cost accounting system is a way to determine and control the costs absorbed by the different

production and administration processes so that business can attain its target of profit superlative

(Lodha, 2018). It covers recording, classification, and control of those abnormal costs which are

increasing the cost of the final product and controllable through the better management of

activities. Some benefits of cost accounting system;

The system can be applied by Wentworth to be cost-effective and profitable (Lodha, 2018).

Absorption of each cost factor can be an exam on the table of appropriateness.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

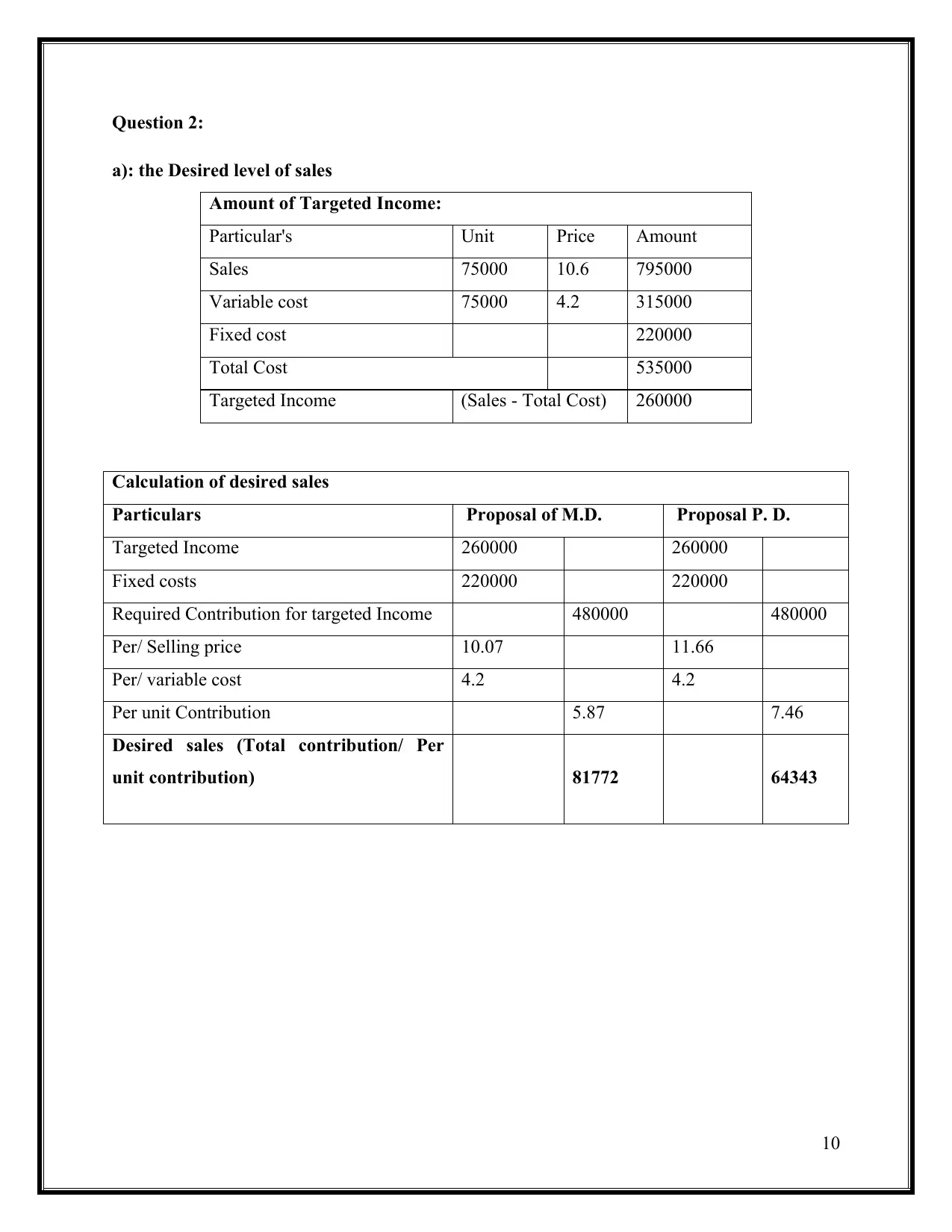

Question 2:

a): the Desired level of sales

Amount of Targeted Income:

Particular's Unit Price Amount

Sales 75000 10.6 795000

Variable cost 75000 4.2 315000

Fixed cost 220000

Total Cost 535000

Targeted Income (Sales - Total Cost) 260000

Calculation of desired sales

Particulars Proposal of M.D. Proposal P. D.

Targeted Income 260000 260000

Fixed costs 220000 220000

Required Contribution for targeted Income 480000 480000

Per/ Selling price 10.07 11.66

Per/ variable cost 4.2 4.2

Per unit Contribution 5.87 7.46

Desired sales (Total contribution/ Per

unit contribution) 81772 64343

10

a): the Desired level of sales

Amount of Targeted Income:

Particular's Unit Price Amount

Sales 75000 10.6 795000

Variable cost 75000 4.2 315000

Fixed cost 220000

Total Cost 535000

Targeted Income (Sales - Total Cost) 260000

Calculation of desired sales

Particulars Proposal of M.D. Proposal P. D.

Targeted Income 260000 260000

Fixed costs 220000 220000

Required Contribution for targeted Income 480000 480000

Per/ Selling price 10.07 11.66

Per/ variable cost 4.2 4.2

Per unit Contribution 5.87 7.46

Desired sales (Total contribution/ Per

unit contribution) 81772 64343

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

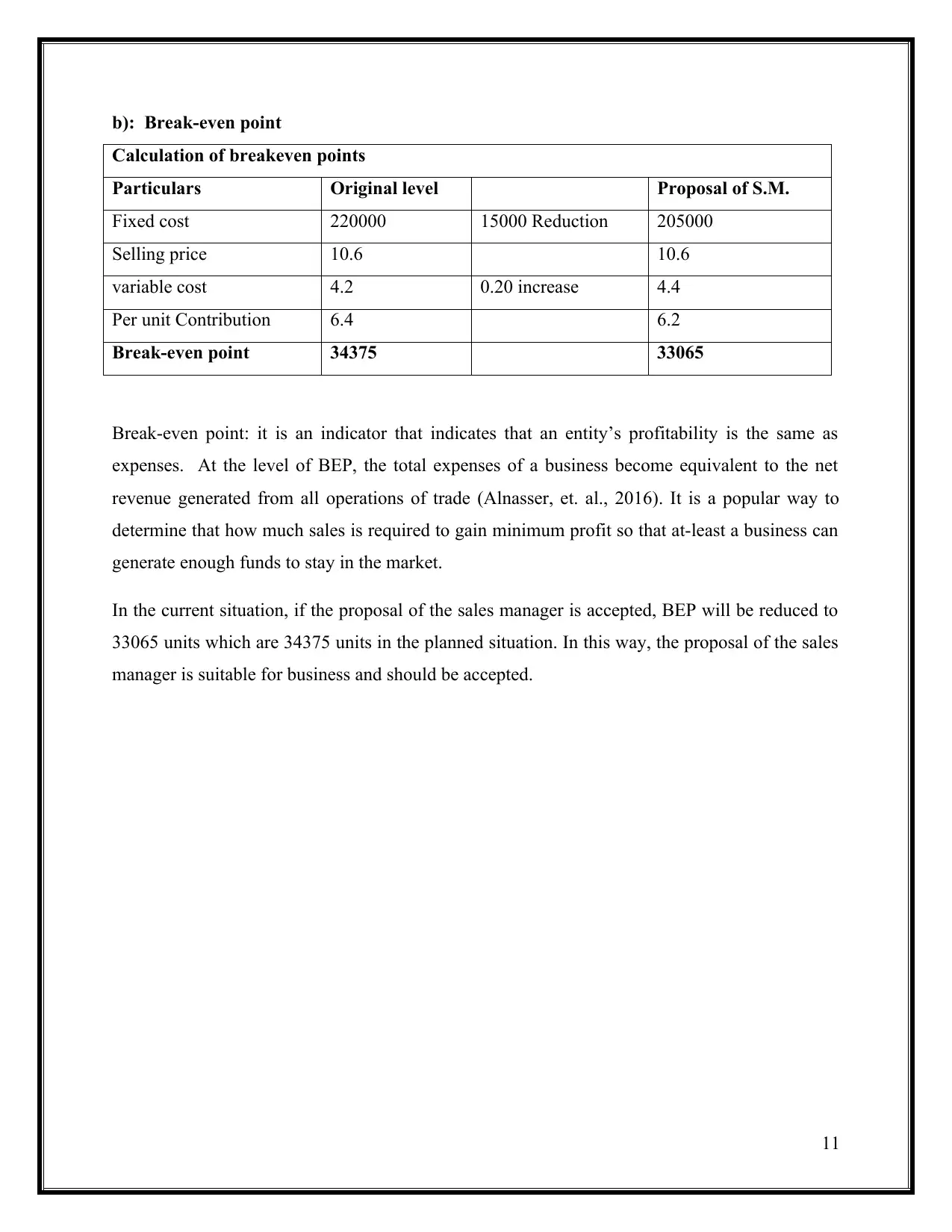

b): Break-even point

Calculation of breakeven points

Particulars Original level Proposal of S.M.

Fixed cost 220000 15000 Reduction 205000

Selling price 10.6 10.6

variable cost 4.2 0.20 increase 4.4

Per unit Contribution 6.4 6.2

Break-even point 34375 33065

Break-even point: it is an indicator that indicates that an entity’s profitability is the same as

expenses. At the level of BEP, the total expenses of a business become equivalent to the net

revenue generated from all operations of trade (Alnasser, et. al., 2016). It is a popular way to

determine that how much sales is required to gain minimum profit so that at-least a business can

generate enough funds to stay in the market.

In the current situation, if the proposal of the sales manager is accepted, BEP will be reduced to

33065 units which are 34375 units in the planned situation. In this way, the proposal of the sales

manager is suitable for business and should be accepted.

11

Calculation of breakeven points

Particulars Original level Proposal of S.M.

Fixed cost 220000 15000 Reduction 205000

Selling price 10.6 10.6

variable cost 4.2 0.20 increase 4.4

Per unit Contribution 6.4 6.2

Break-even point 34375 33065

Break-even point: it is an indicator that indicates that an entity’s profitability is the same as

expenses. At the level of BEP, the total expenses of a business become equivalent to the net

revenue generated from all operations of trade (Alnasser, et. al., 2016). It is a popular way to

determine that how much sales is required to gain minimum profit so that at-least a business can

generate enough funds to stay in the market.

In the current situation, if the proposal of the sales manager is accepted, BEP will be reduced to

33065 units which are 34375 units in the planned situation. In this way, the proposal of the sales

manager is suitable for business and should be accepted.

11

Section 2

Question 3:

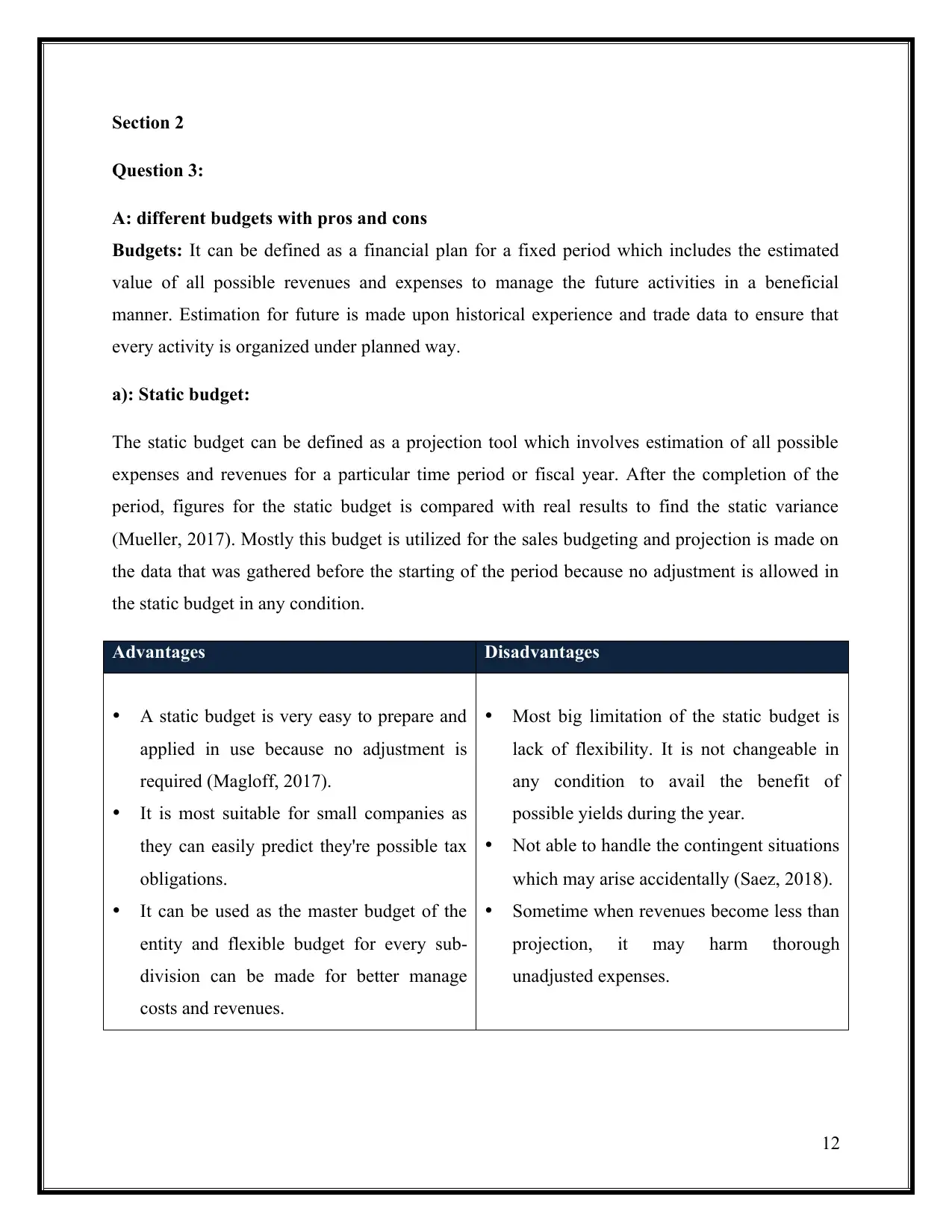

A: different budgets with pros and cons

Budgets: It can be defined as a financial plan for a fixed period which includes the estimated

value of all possible revenues and expenses to manage the future activities in a beneficial

manner. Estimation for future is made upon historical experience and trade data to ensure that

every activity is organized under planned way.

a): Static budget:

The static budget can be defined as a projection tool which involves estimation of all possible

expenses and revenues for a particular time period or fiscal year. After the completion of the

period, figures for the static budget is compared with real results to find the static variance

(Mueller, 2017). Mostly this budget is utilized for the sales budgeting and projection is made on

the data that was gathered before the starting of the period because no adjustment is allowed in

the static budget in any condition.

Advantages Disadvantages

A static budget is very easy to prepare and

applied in use because no adjustment is

required (Magloff, 2017).

It is most suitable for small companies as

they can easily predict they're possible tax

obligations.

It can be used as the master budget of the

entity and flexible budget for every sub-

division can be made for better manage

costs and revenues.

Most big limitation of the static budget is

lack of flexibility. It is not changeable in

any condition to avail the benefit of

possible yields during the year.

Not able to handle the contingent situations

which may arise accidentally (Saez, 2018).

Sometime when revenues become less than

projection, it may harm thorough

unadjusted expenses.

12

Question 3:

A: different budgets with pros and cons

Budgets: It can be defined as a financial plan for a fixed period which includes the estimated

value of all possible revenues and expenses to manage the future activities in a beneficial

manner. Estimation for future is made upon historical experience and trade data to ensure that

every activity is organized under planned way.

a): Static budget:

The static budget can be defined as a projection tool which involves estimation of all possible

expenses and revenues for a particular time period or fiscal year. After the completion of the

period, figures for the static budget is compared with real results to find the static variance

(Mueller, 2017). Mostly this budget is utilized for the sales budgeting and projection is made on

the data that was gathered before the starting of the period because no adjustment is allowed in

the static budget in any condition.

Advantages Disadvantages

A static budget is very easy to prepare and

applied in use because no adjustment is

required (Magloff, 2017).

It is most suitable for small companies as

they can easily predict they're possible tax

obligations.

It can be used as the master budget of the

entity and flexible budget for every sub-

division can be made for better manage

costs and revenues.

Most big limitation of the static budget is

lack of flexibility. It is not changeable in

any condition to avail the benefit of

possible yields during the year.

Not able to handle the contingent situations

which may arise accidentally (Saez, 2018).

Sometime when revenues become less than

projection, it may harm thorough

unadjusted expenses.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.